monthly market outlook presentation july 2015€¦ · monthly market outlook presentation ......

TRANSCRIPT

1

Monthly Market

Outlook Presentation

July 2015

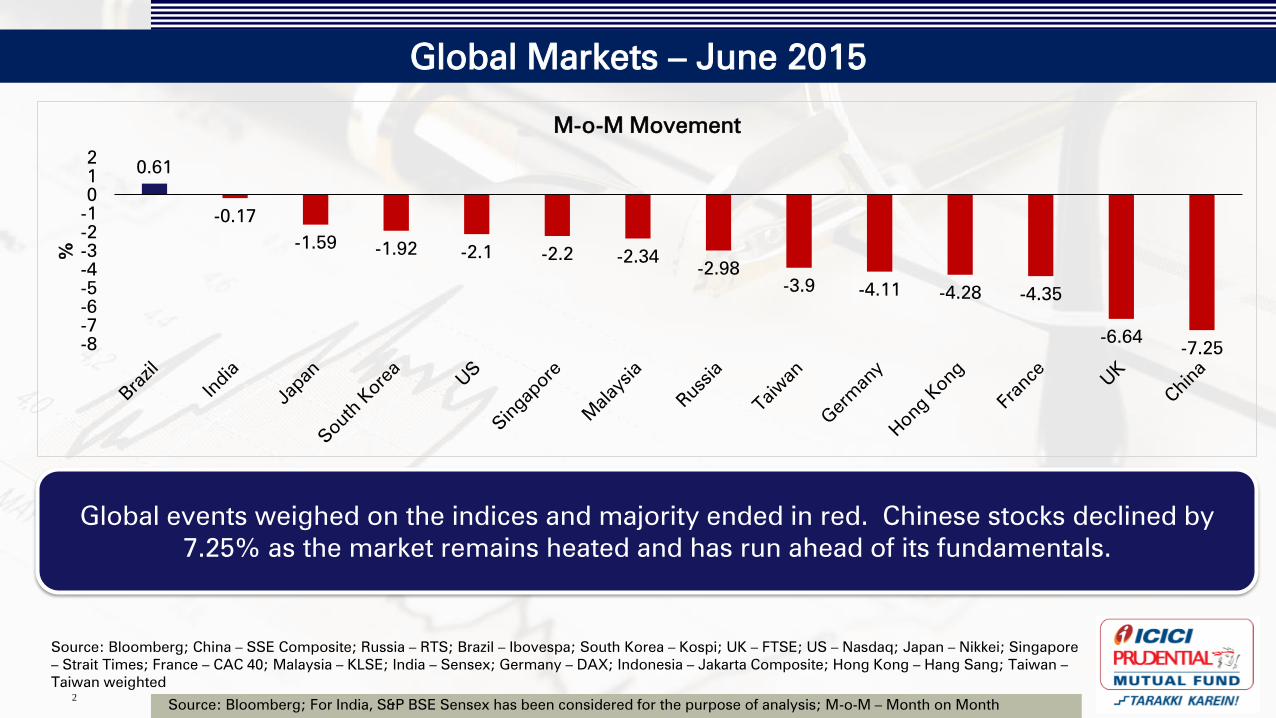

Global Markets – June 2015

Source: Bloomberg; For India, S&P BSE Sensex has been considered for the purpose of analysis; M-o-M – Month on Month 2

Global events weighed on the indices and majority ended in red. Chinese stocks declined by

7.25% as the market remains heated and has run ahead of its fundamentals.

Source: Bloomberg; China – SSE Composite; Russia – RTS; Brazil – Ibovespa; South Korea – Kospi; UK – FTSE; US – Nasdaq; Japan – Nikkei; Singapore

– Strait Times; France – CAC 40; Malaysia – KLSE; India – Sensex; Germany – DAX; Indonesia – Jakarta Composite; Hong Kong – Hang Sang; Taiwan –

Taiwan weighted

0.61

-0.17

-1.59 -1.92 -2.1 -2.2 -2.34

-2.98

-3.9 -4.11 -4.28 -4.35

-6.64 -7.25 -8

-7

-6

-5

-4

-3

-2

-1

0

1

2

%

M-o-M Movement

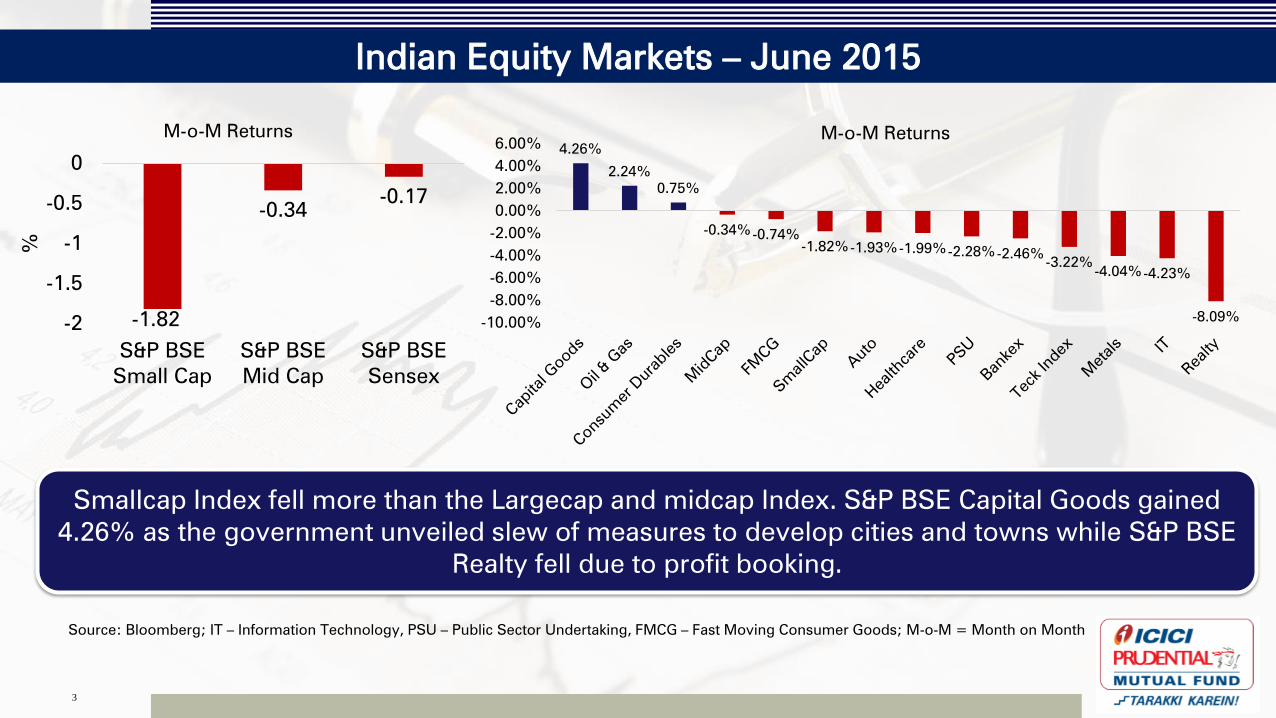

Indian Equity Markets – June 2015

3

Source: Bloomberg; IT – Information Technology, PSU – Public Sector Undertaking, FMCG – Fast Moving Consumer Goods; M-o-M = Month on Month

-1.82

-0.34 -0.17

-2

-1.5

-1

-0.5

0

S&P BSE

Small Cap

S&P BSE

Mid Cap

S&P BSE

Sensex

%

M-o-M Returns

Smallcap Index fell more than the Largecap and midcap Index. S&P BSE Capital Goods gained

4.26% as the government unveiled slew of measures to develop cities and towns while S&P BSE

Realty fell due to profit booking.

4.26%

2.24%

0.75%

-0.34% -0.74%

-1.82% -1.93% -1.99% -2.28% -2.46% -3.22%

-4.04% -4.23%

-8.09% -10.00%

-8.00%

-6.00%

-4.00%

-2.00%

0.00%

2.00%

4.00%

6.00%M-o-M Returns

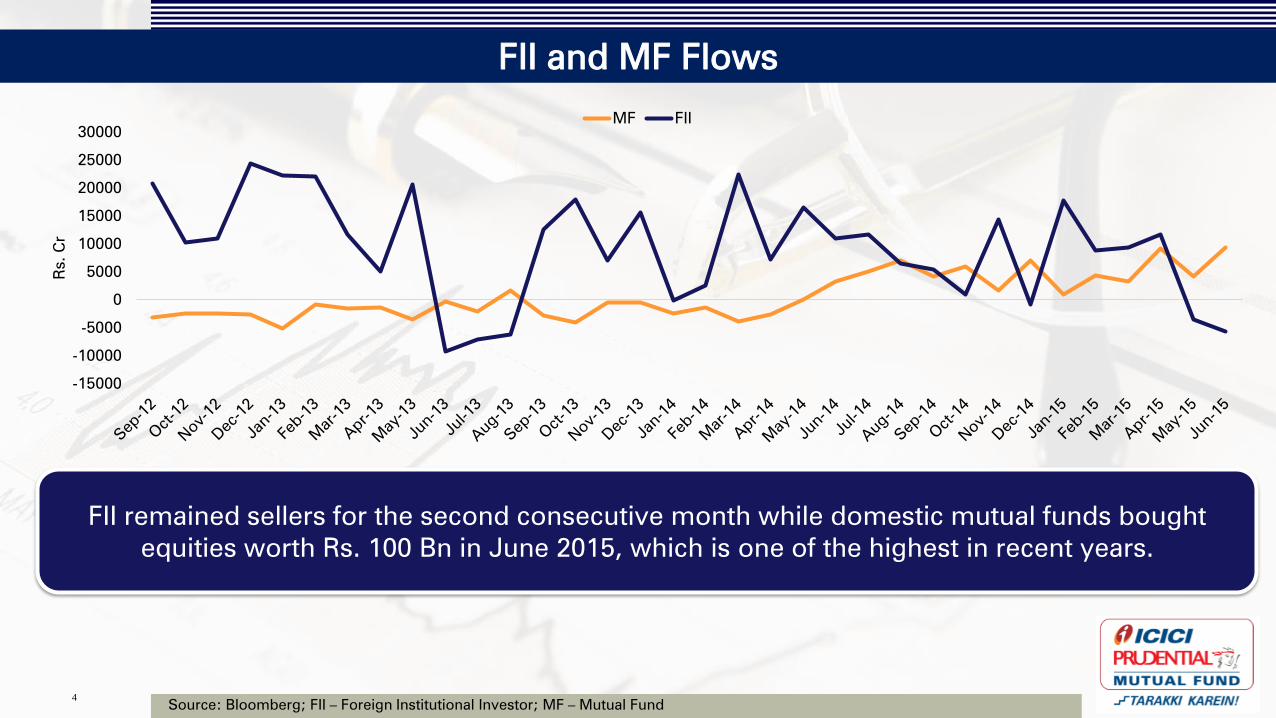

FII and MF Flows

Source: Bloomberg; FII – Foreign Institutional Investor; MF – Mutual Fund 4

FII remained sellers for the second consecutive month while domestic mutual funds bought

equities worth Rs. 100 Bn in June 2015, which is one of the highest in recent years.

-15000

-10000

-5000

0

5000

10000

15000

20000

25000

30000

Rs. C

r

MF FII

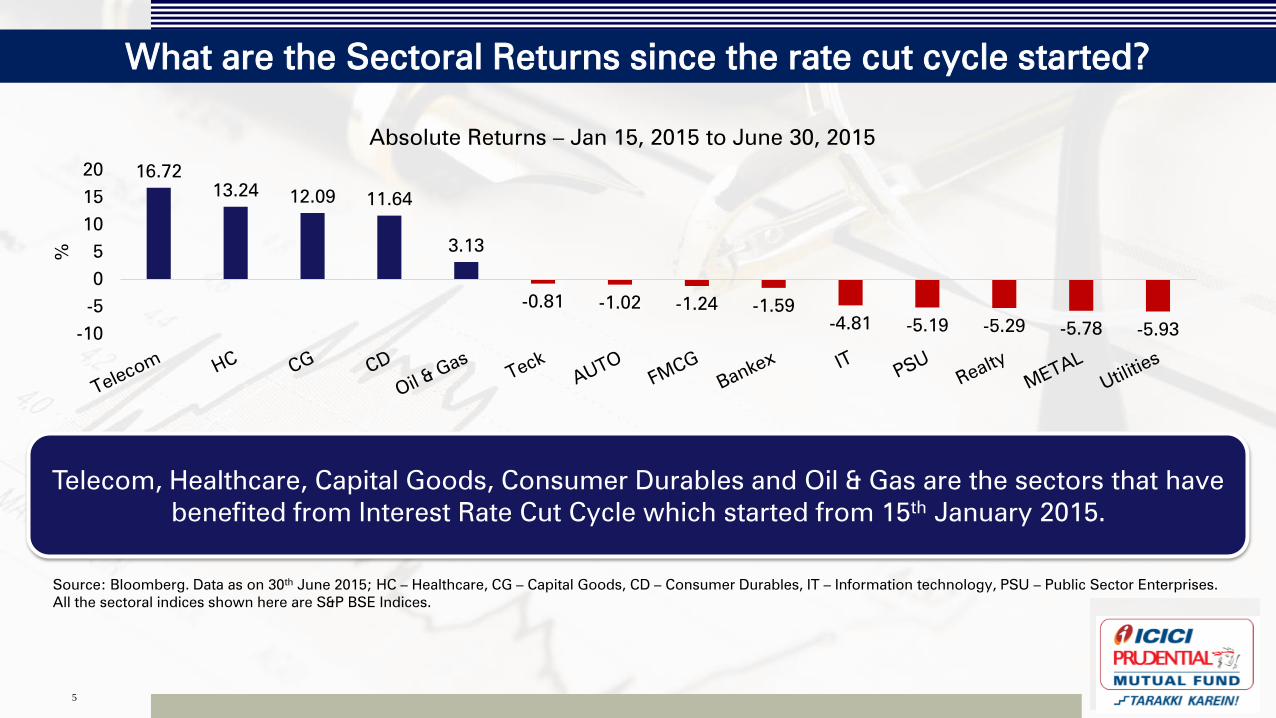

What are the Sectoral Returns since the rate cut cycle started?

Source: Bloomberg. Data as on 30th

June 2015; HC – Healthcare, CG – Capital Goods, CD – Consumer Durables, IT – Information technology, PSU – Public Sector Enterprises.

All the sectoral indices shown here are S&P BSE Indices.

5

Telecom, Healthcare, Capital Goods, Consumer Durables and Oil & Gas are the sectors that have

benefited from Interest Rate Cut Cycle which started from 15th

January 2015.

16.72

13.24 12.09 11.64

3.13

-0.81 -1.02 -1.24 -1.59

-4.81 -5.19 -5.29 -5.78 -5.93 -10

-5

0

5

10

15

20

%

Absolute Returns – Jan 15, 2015 to June 30, 2015

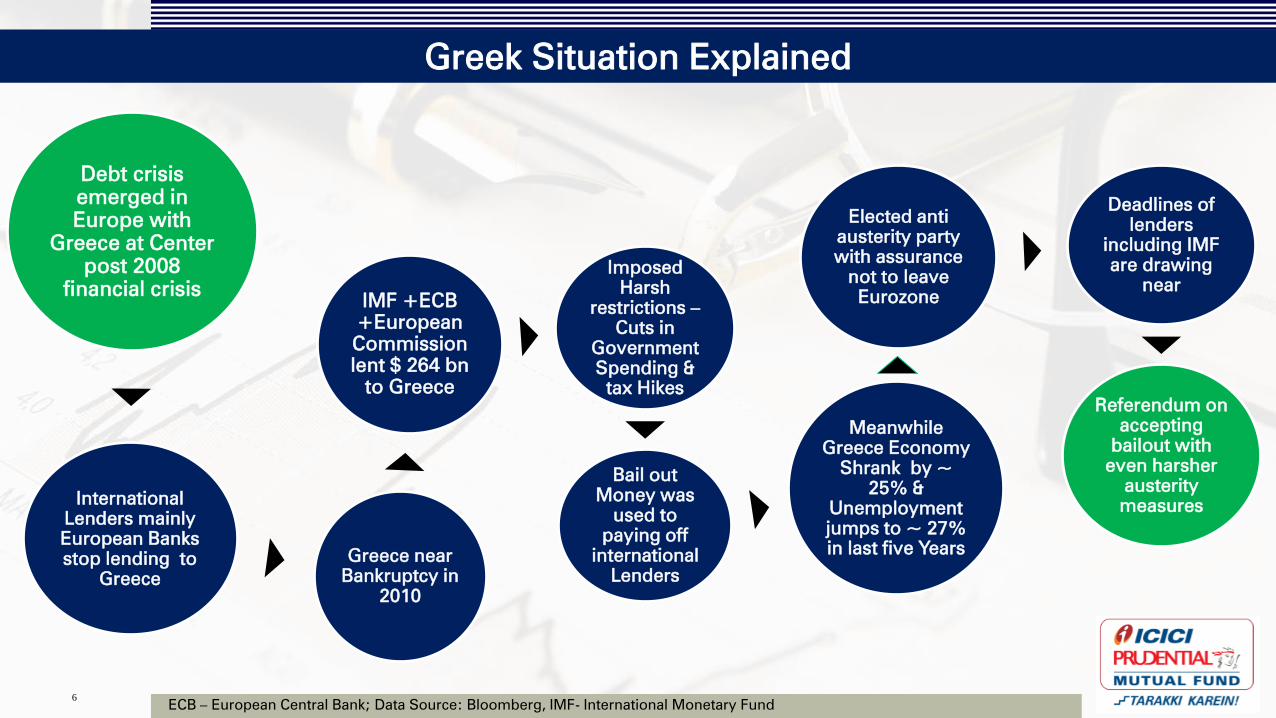

Greek Situation Explained

6

Debt crisis

emerged in

Europe with

Greece at Center

post 2008

financial crisis

International

Lenders mainly

European Banks

stop lending to

Greece

Greece near

Bankruptcy in

2010

IMF +ECB

+European

Commission

lent $ 264 bn

to Greece

Imposed

Harsh

restrictions –

Cuts in

Government

Spending &

tax Hikes

Bail out

Money was

used to

paying off

international

Lenders

Meanwhile

Greece Economy

Shrank by ~

25% &

Unemployment

jumps to ~ 27%

in last five Years

Elected anti

austerity party

with assurance

not to leave

Eurozone

Deadlines of

lenders

including IMF

are drawing

near

Referendum on

accepting

bailout with

even harsher

austerity

measures

ECB – European Central Bank; Data Source: Bloomberg, IMF- International Monetary Fund

Greece Situation is Another Opportunity To Invest

7

Similar situation in Greece in 2012 had limited impact on

Indian Markets

Indian equity and fixed income markets had recovered

immediately after this event

Current crisis is just a sentimental risk off event than a

fundamental one

Hence, yet another buying opportunity into equities

Past performance may or may not be sustained in future

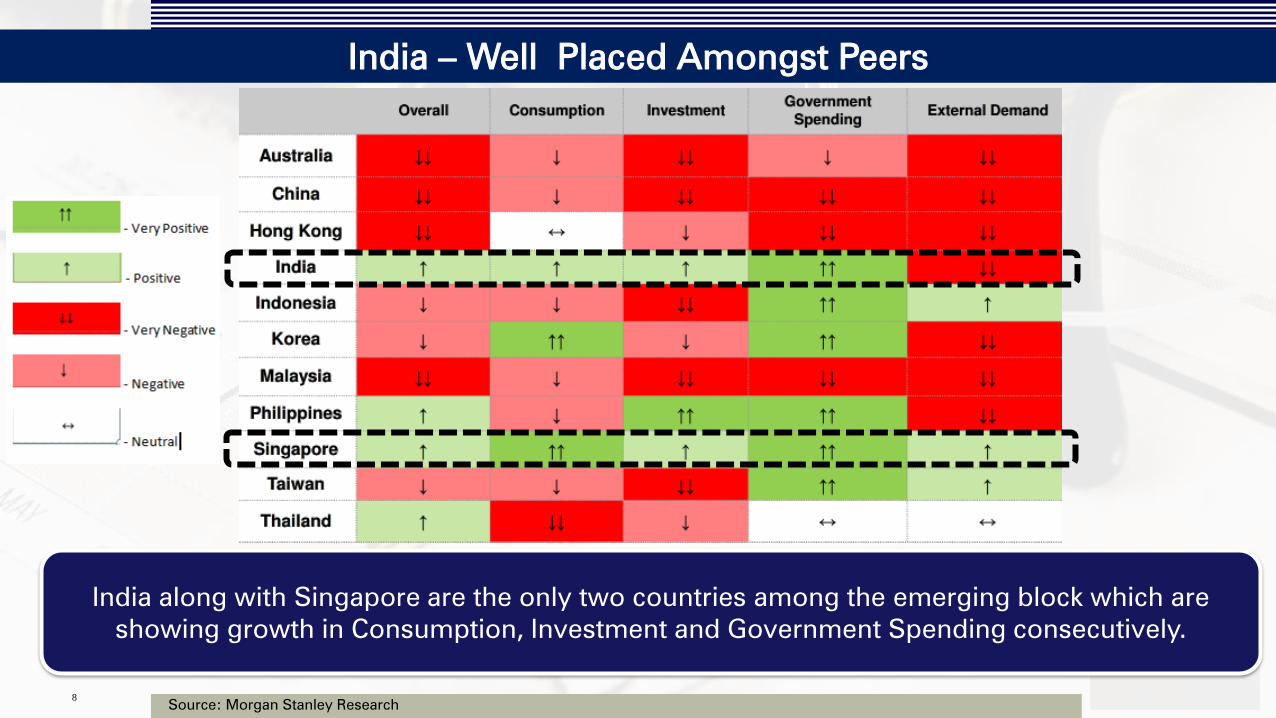

India – Well Placed Amongst Peers

Source: Morgan Stanley Research 8

India along with Singapore are the only two countries among the emerging block which are

showing growth in Consumption, Investment and Government Spending consecutively.

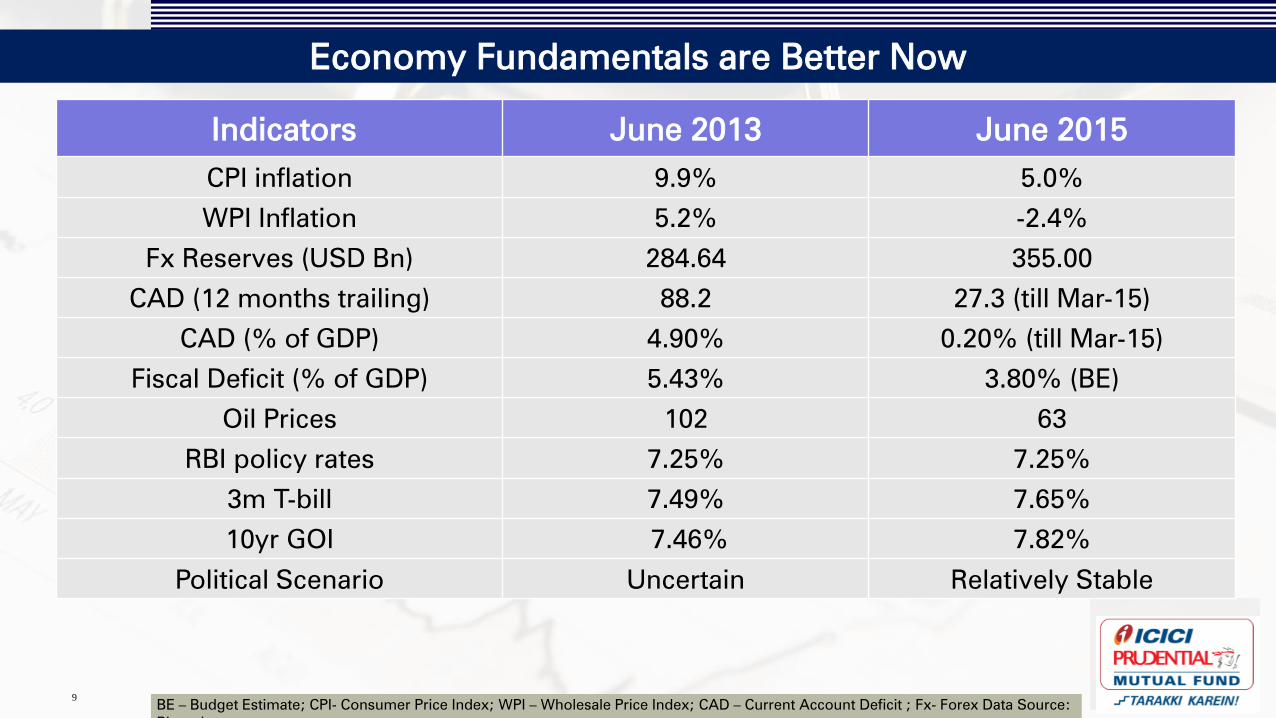

Economy Fundamentals are Better Now

9

Indicators June 2013 June 2015

CPI inflation 9.9% 5.0%

WPI Inflation 5.2% -2.4%

Fx Reserves (USD Bn) 284.64 355.00

CAD (12 months trailing) 88.2 27.3 (till Mar-15)

CAD (% of GDP) 4.90% 0.20% (till Mar-15)

Fiscal Deficit (% of GDP) 5.43% 3.80% (BE)

Oil Prices 102 63

RBI policy rates 7.25% 7.25%

3m T-bill 7.49% 7.65%

10yr GOI 7.46% 7.82%

Political Scenario Uncertain Relatively Stable

BE – Budget Estimate; CPI- Consumer Price Index; WPI – Wholesale Price Index; CAD – Current Account Deficit ; Fx- Forex Data Source:

Bloomberg

Enough Forex Reserves to Combat Global Volatility

10

India has enough foreign exchange reserves to cushion

itself from any global contagion risk

As on June 19, 2015 , India had US$ 355.46 Bn of

foreign exchange reserves

Foreign Currency Assets form the largest part of India’s

forex reserves

Item US$ Bn

Foreign Currency

Assets 330.71

Gold 19.34

SDRs 4.08

Reserve Position in

the IMF 1.32

Total Reserves 355.46

Source: RBI; IMF – International Monetary Fund; SDR – Special Drawing Rights

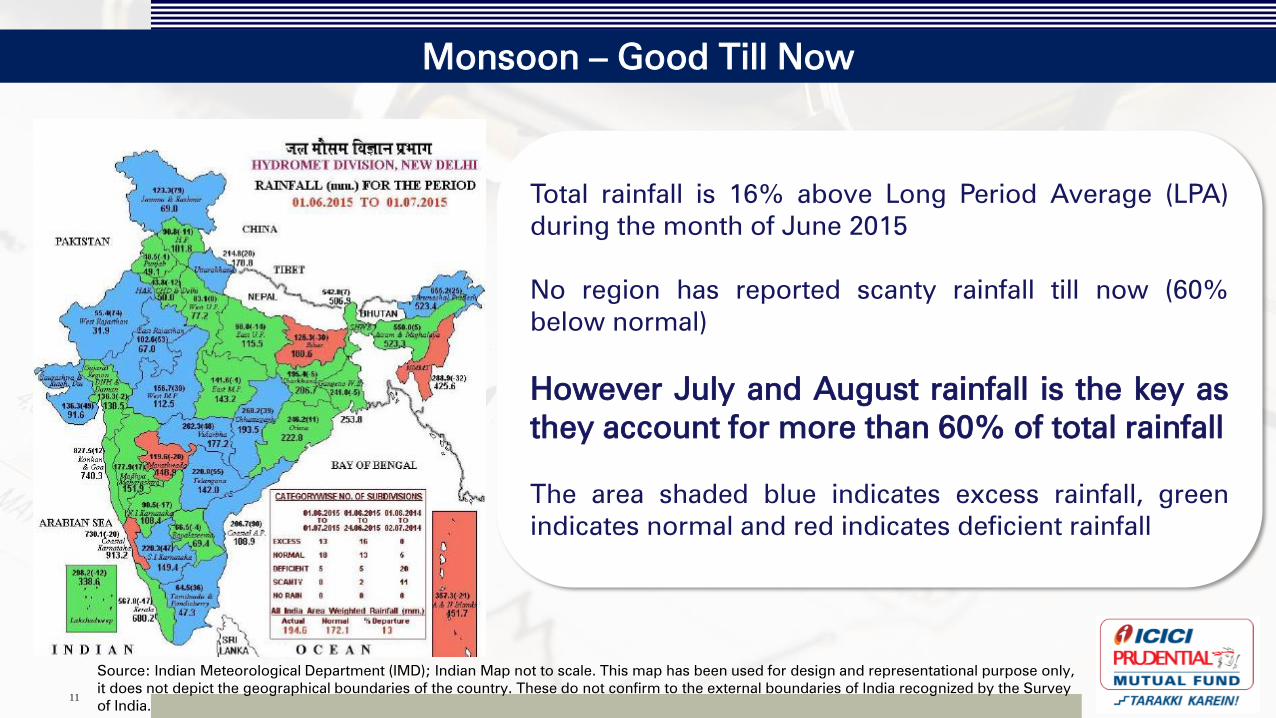

Monsoon – Good Till Now

11

Total rainfall is 16% above Long Period Average (LPA)

during the month of June 2015

No region has reported scanty rainfall till now (60%

below normal)

However July and August rainfall is the key as

they account for more than 60% of total rainfall

The area shaded blue indicates excess rainfall, green

indicates normal and red indicates deficient rainfall

Source: Indian Meteorological Department (IMD); Indian Map not to scale. This map has been used for design and representational purpose only,

it does not depict the geographical boundaries of the country. These do not confirm to the external boundaries of India recognized by the Survey

of India.

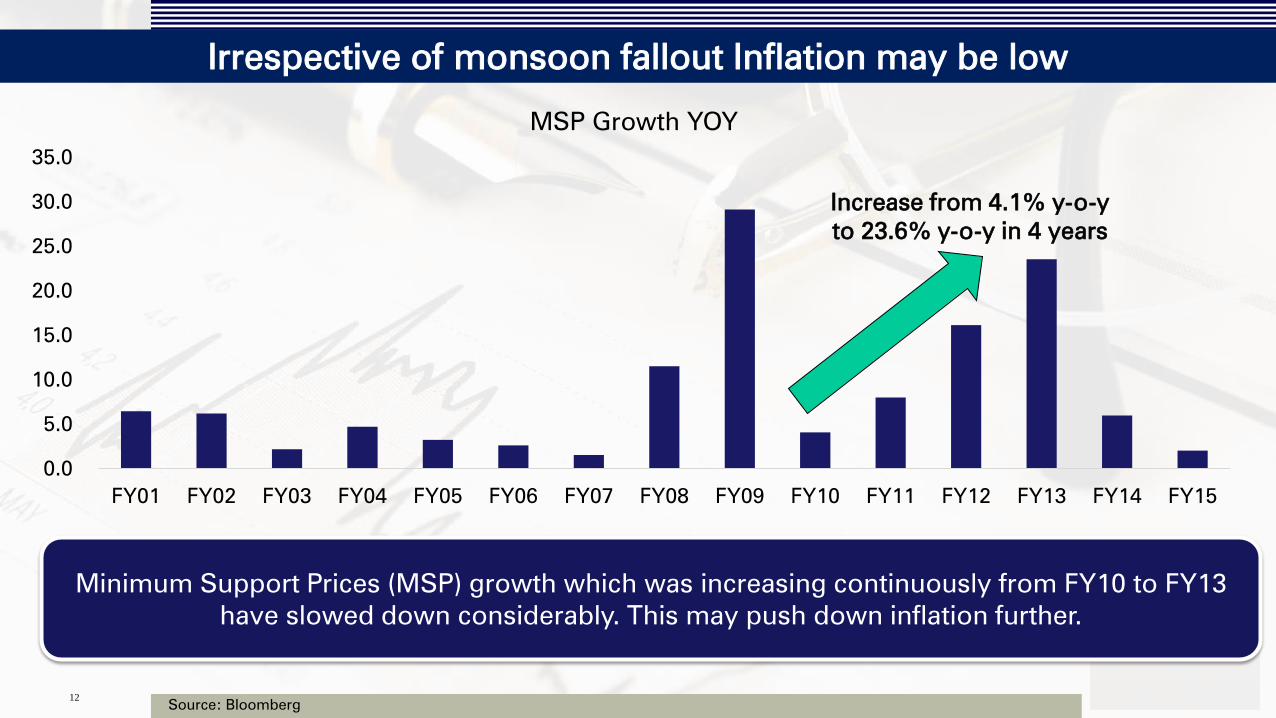

Irrespective of monsoon fallout Inflation may be low

Source: Bloomberg 12

Minimum Support Prices (MSP) growth which was increasing continuously from FY10 to FY13

have slowed down considerably. This may push down inflation further.

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

FY01 FY02 FY03 FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15

MSP Growth YOY

Increase from 4.1% y-o-y

to 23.6% y-o-y in 4 years

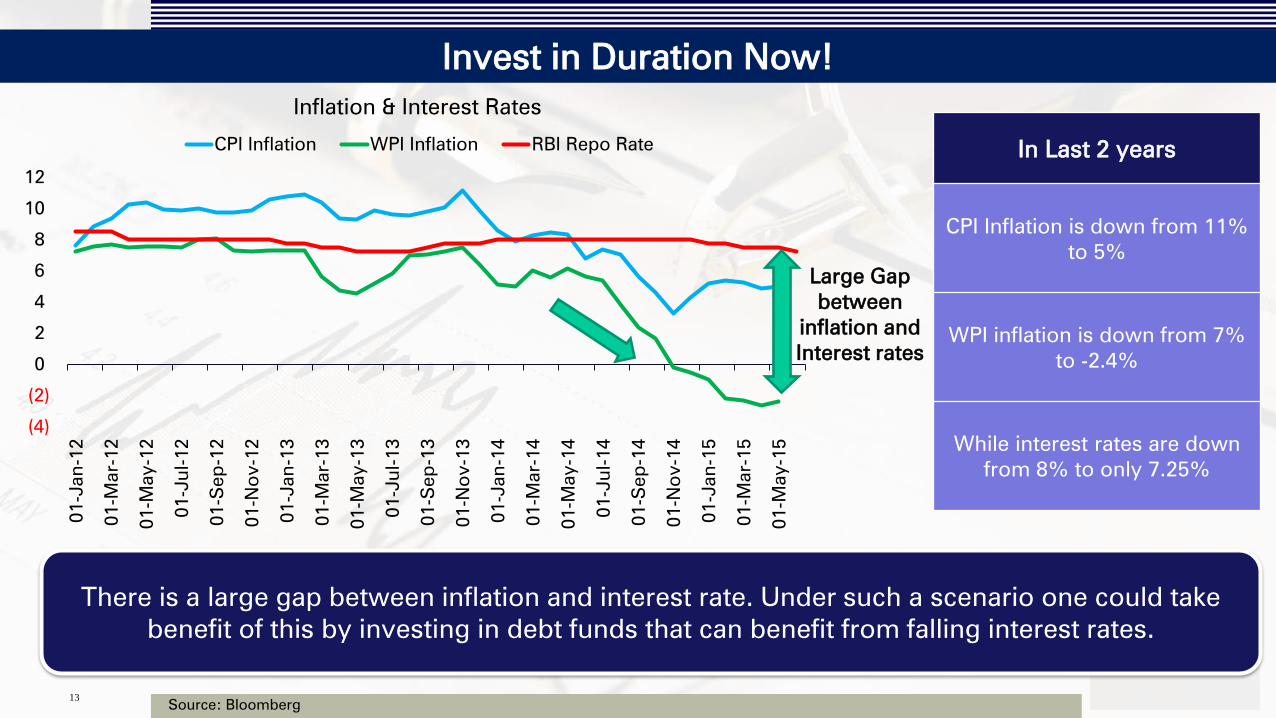

Invest in Duration Now!

Source: Bloomberg 13

There is a large gap between inflation and interest rate. Under such a scenario one could take

benefit of this by investing in debt funds that can benefit from falling interest rates.

(4)

(2)

0

2

4

6

8

10

12

01-Jan

-12

01-M

ar-12

01-M

ay-12

01-Ju

l-12

01-S

ep

-12

01-N

ov-12

01-Jan

-13

01-M

ar-13

01-M

ay-13

01-Ju

l-13

01-S

ep

-13

01-N

ov-13

01-Jan

-14

01-M

ar-14

01-M

ay-14

01-Ju

l-14

01-S

ep

-14

01-N

ov-14

01-Jan

-15

01-M

ar-15

01-M

ay-15

Inflation & Interest Rates

CPI Inflation WPI Inflation RBI Repo Rate

Large Gap

between

inflation and

Interest rates

In Last 2 years

CPI Inflation is down from 11%

to 5%

WPI inflation is down from 7%

to -2.4%

While interest rates are down

from 8% to only 7.25%

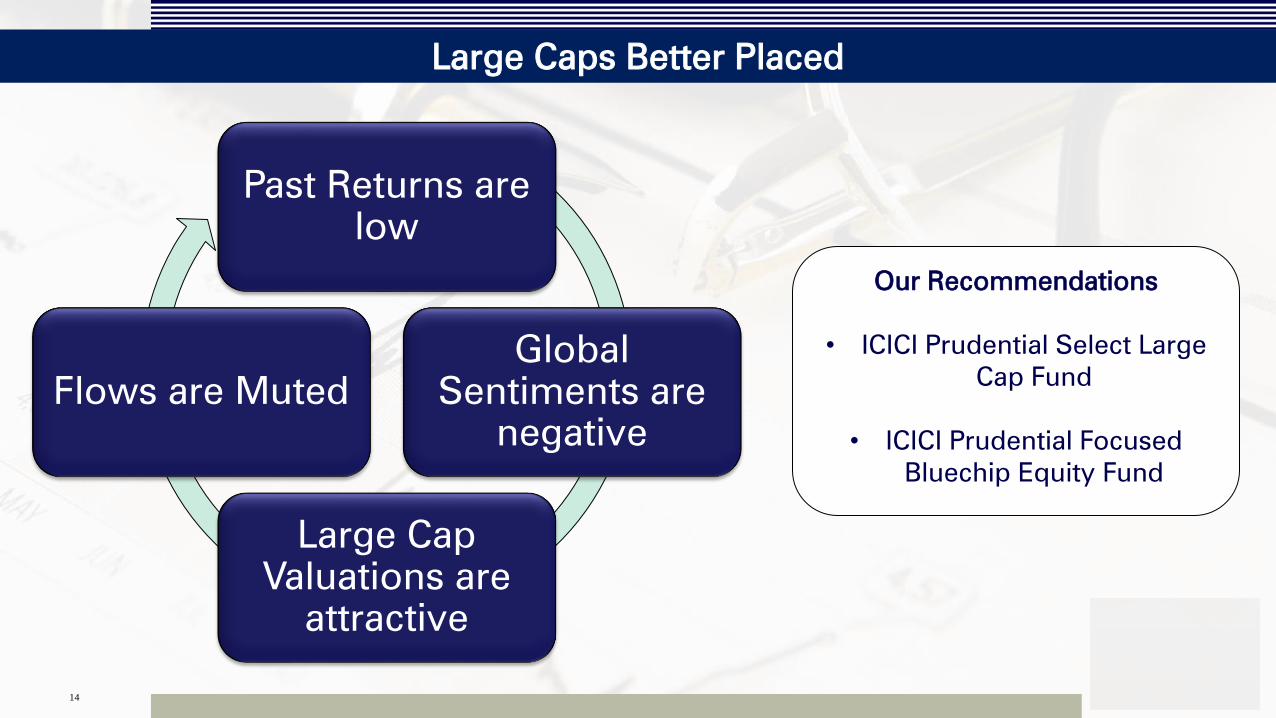

Large Caps Better Placed

14

Past Returns are

low

Global

Sentiments are

negative

Large Cap

Valuations are

attractive

Flows are Muted

Our Recommendations

• ICICI Prudential Select Large

Cap Fund

• ICICI Prudential Focused

Bluechip Equity Fund

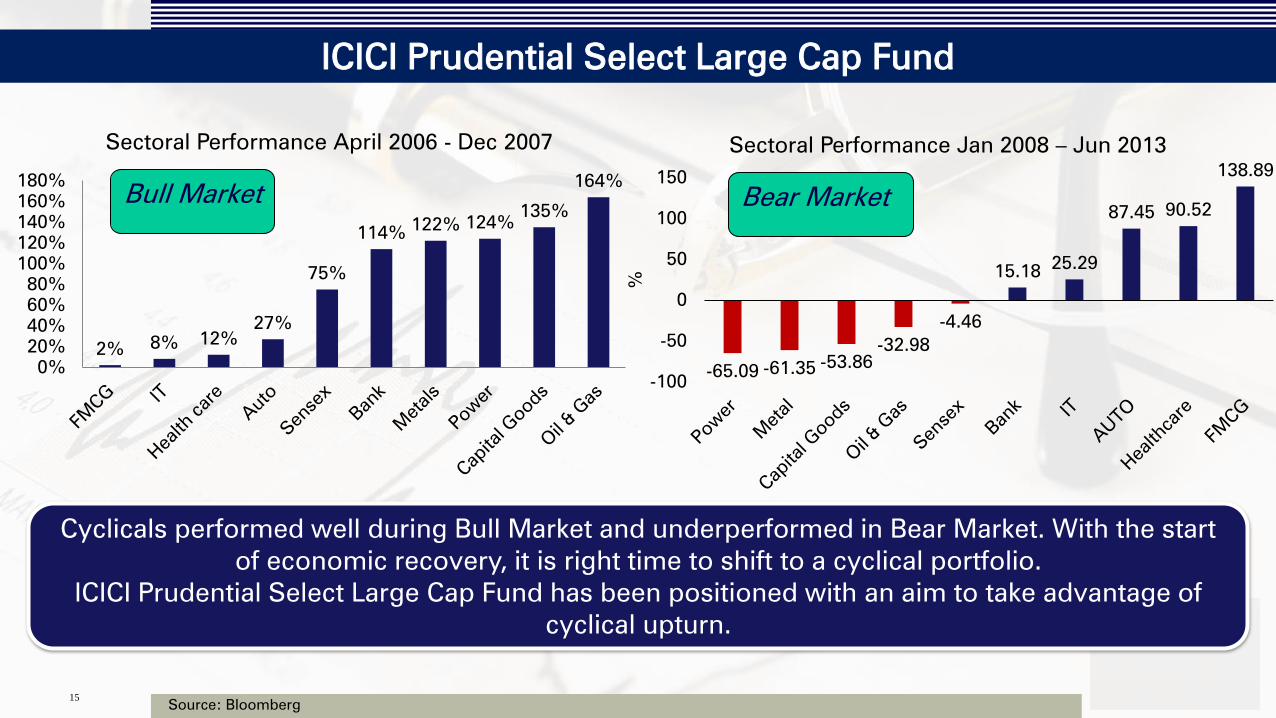

ICICI Prudential Select Large Cap Fund

Source: Bloomberg 15

Cyclicals performed well during Bull Market and underperformed in Bear Market. With the start

of economic recovery, it is right time to shift to a cyclical portfolio.

ICICI Prudential Select Large Cap Fund has been positioned with an aim to take advantage of

cyclical upturn.

2% 8% 12%

27%

75%

114% 122% 124%

135%

164%

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

Sectoral Performance April 2006 - Dec 2007

Bull Market Bear Market

-65.09 -61.35 -53.86

-32.98

-4.46

15.18 25.29

87.45 90.52

138.89

-100

-50

0

50

100

150

%

Sectoral Performance Jan 2008 – Jun 2013

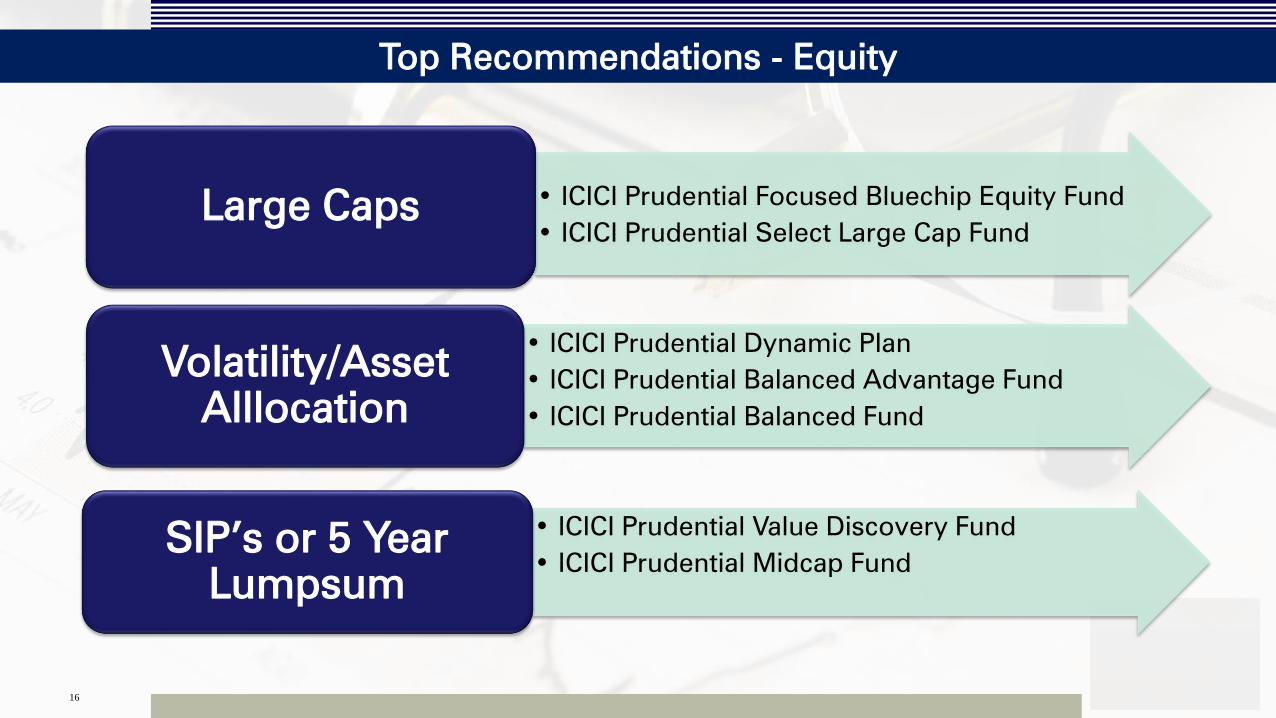

Top Recommendations - Equity

16

• ICICI Prudential Focused Bluechip Equity Fund

• ICICI Prudential Select Large Cap Fund

Large Caps

• ICICI Prudential Dynamic Plan

• ICICI Prudential Balanced Advantage Fund

• ICICI Prudential Balanced Fund

Volatility/Asset

Alllocation

• ICICI Prudential Value Discovery Fund

• ICICI Prudential Midcap Fund

SIP’s or 5 Year

Lumpsum

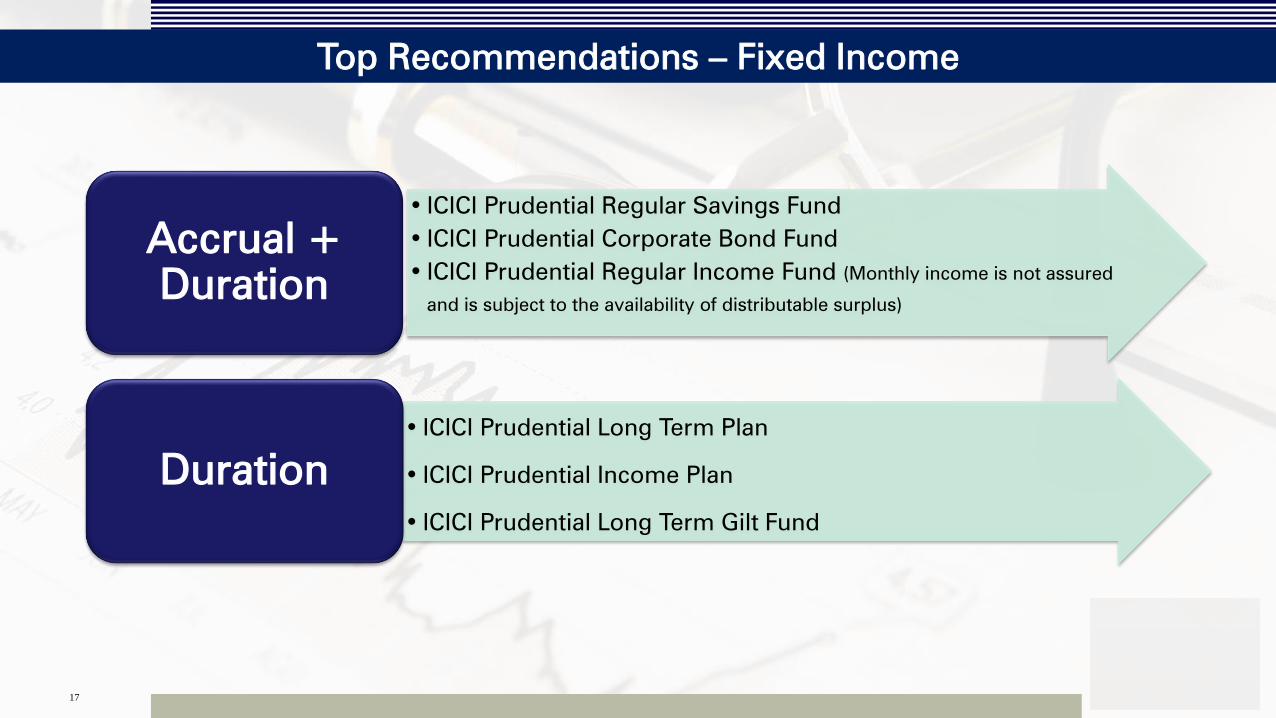

Top Recommendations – Fixed Income

17

• ICICI Prudential Regular Savings Fund

• ICICI Prudential Corporate Bond Fund

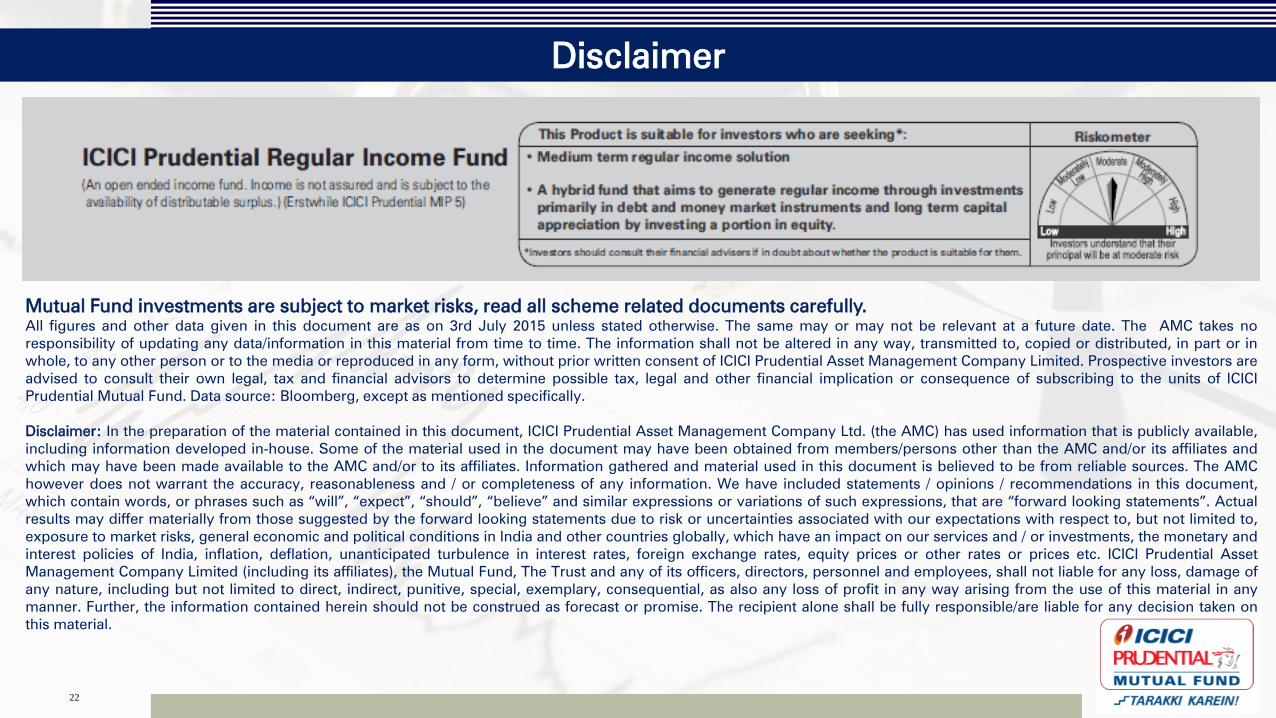

• ICICI Prudential Regular Income Fund (Monthly income is not assured

and is subject to the availability of distributable surplus)

Accrual +

Duration

• ICICI Prudential Long Term Plan

• ICICI Prudential Income Plan

• ICICI Prudential Long Term Gilt Fund

Duration

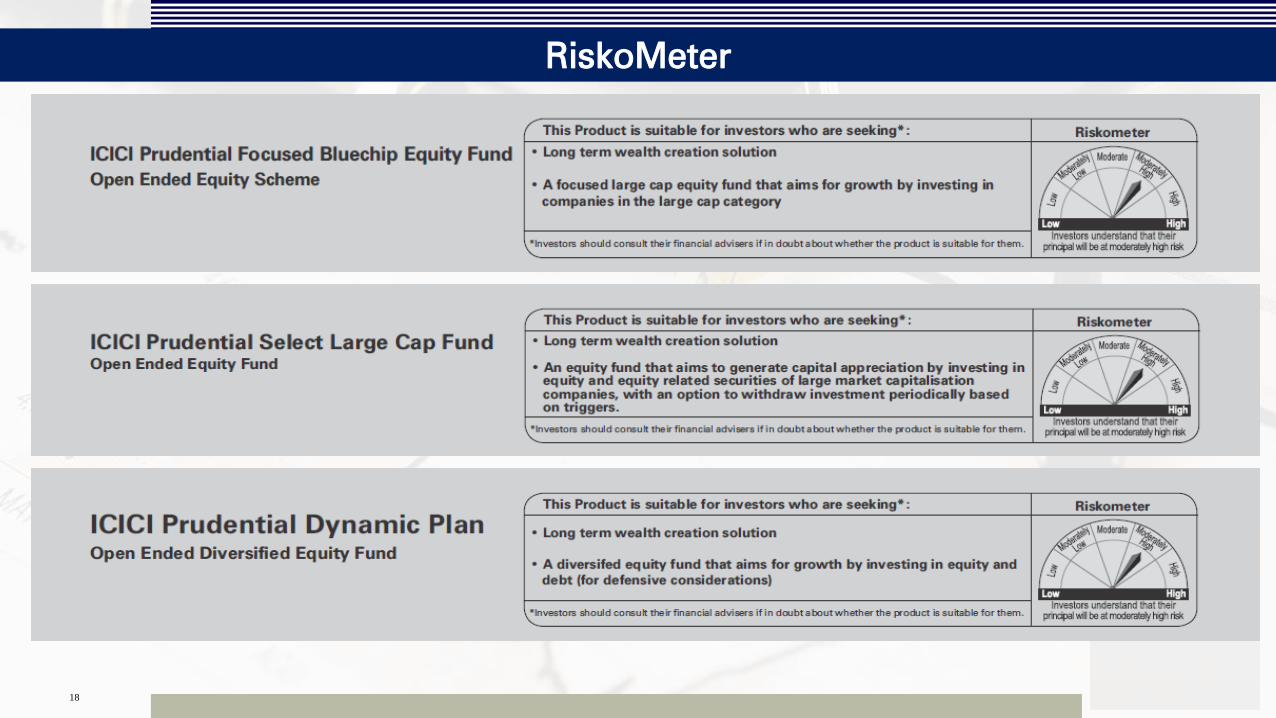

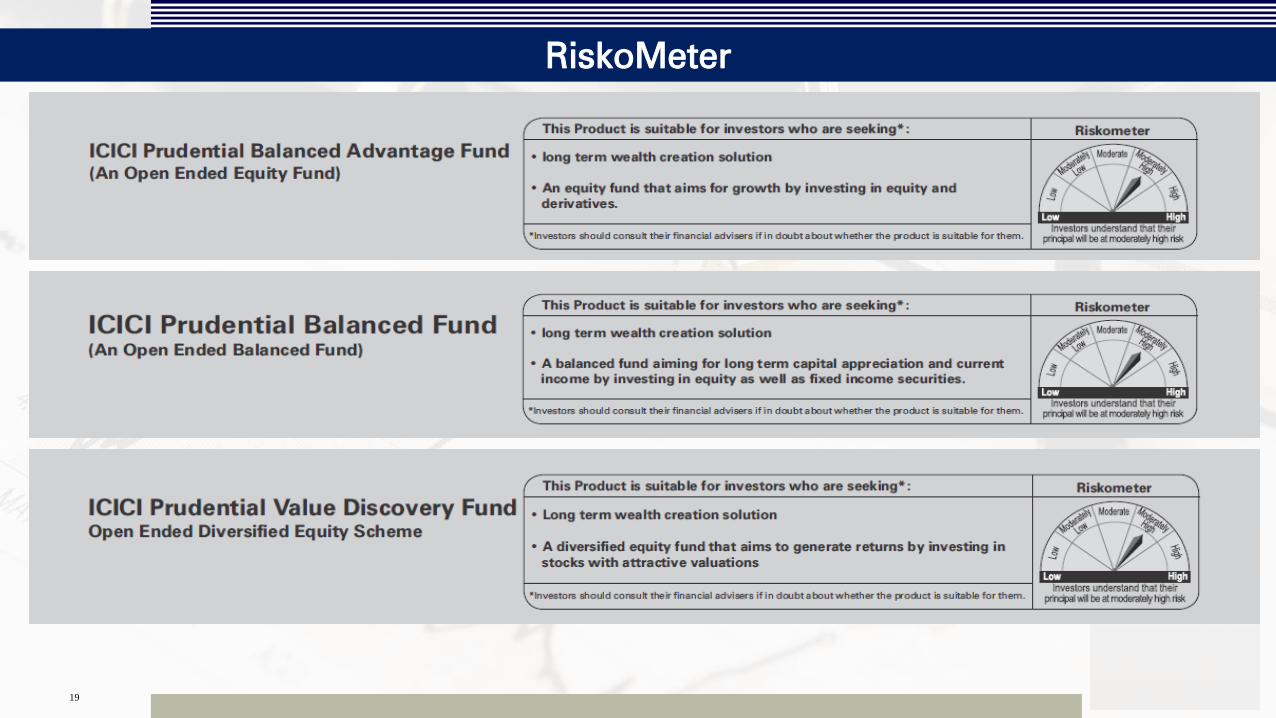

RiskoMeter

18

RiskoMeter

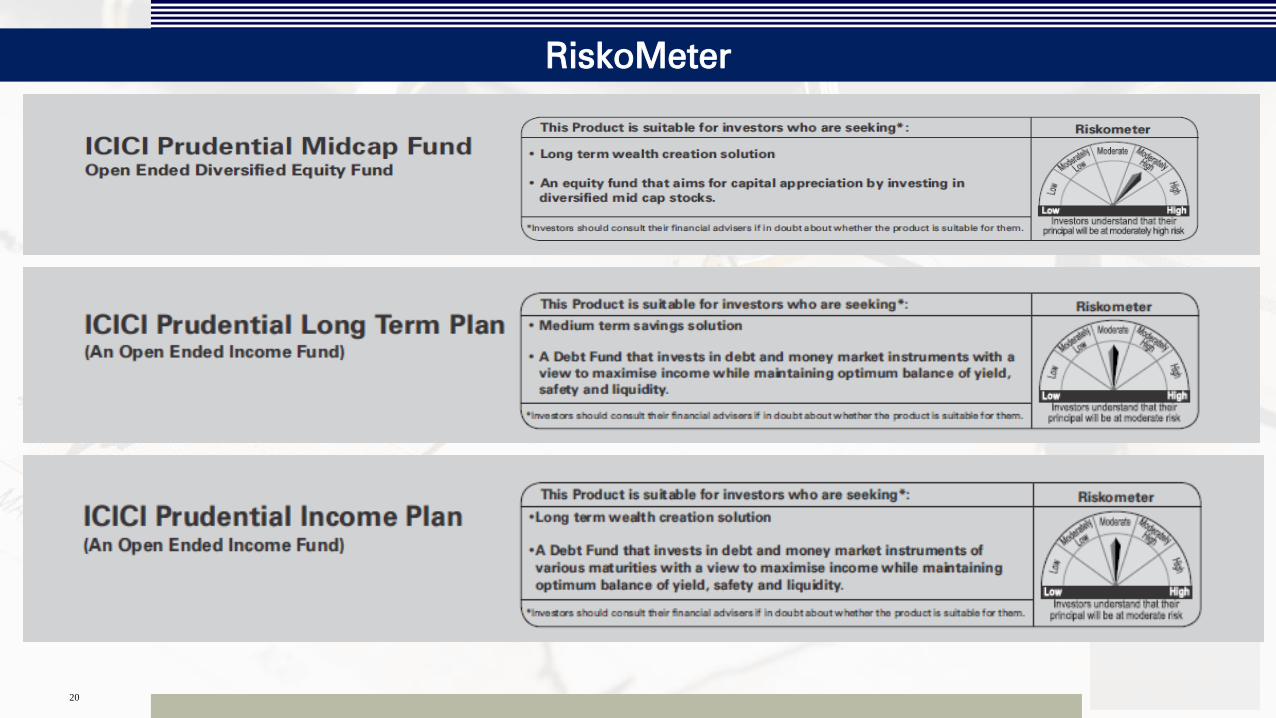

19

RiskoMeter

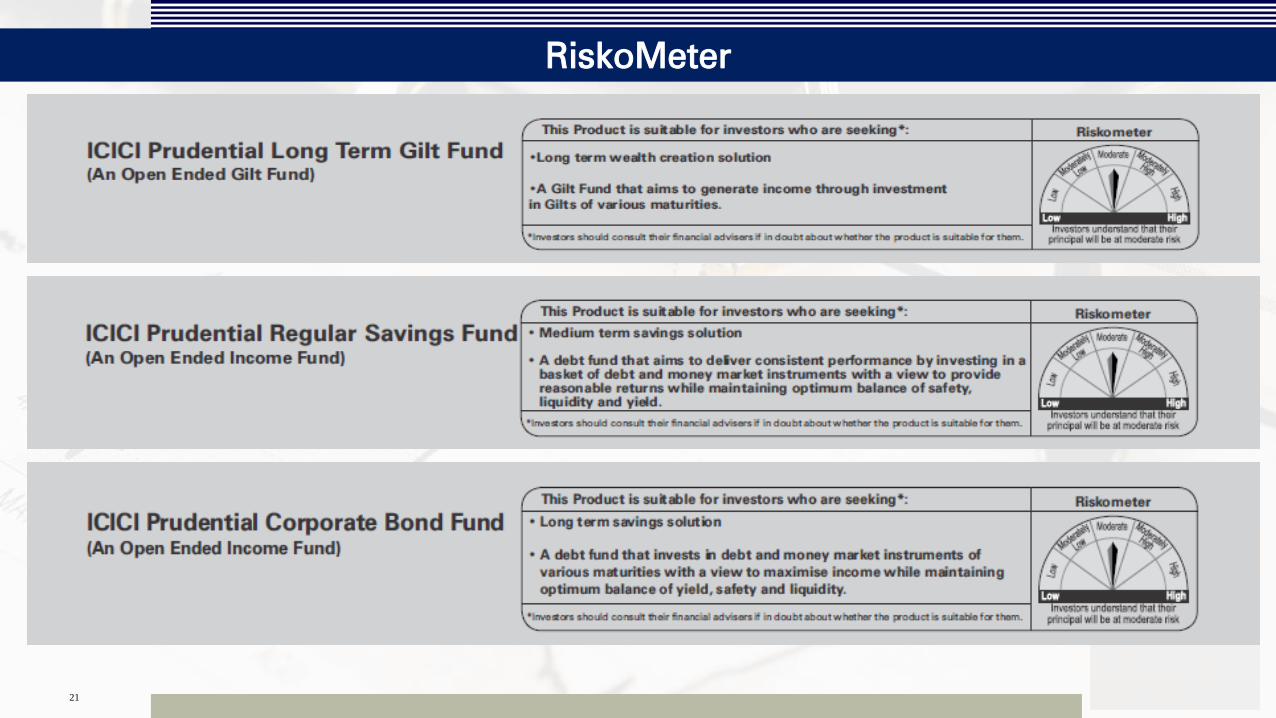

20

RiskoMeter

21

Disclaimer

22

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.

All figures and other data given in this document are as on 3rd July 2015 unless stated otherwise. The same may or may not be relevant at a future date. The AMC takes no

responsibility of updating any data/information in this material from time to time. The information shall not be altered in any way, transmitted to, copied or distributed, in part or in

whole, to any other person or to the media or reproduced in any form, without prior written consent of ICICI Prudential Asset Management Company Limited. Prospective investors are

advised to consult their own legal, tax and financial advisors to determine possible tax, legal and other financial implication or consequence of subscribing to the units of ICICI

Prudential Mutual Fund. Data source: Bloomberg, except as mentioned specifically.

Disclaimer: In the preparation of the material contained in this document, ICICI Prudential Asset Management Company Ltd. (the AMC) has used information that is publicly available,

including information developed in-house. Some of the material used in the document may have been obtained from members/persons other than the AMC and/or its affiliates and

which may have been made available to the AMC and/or to its affiliates. Information gathered and material used in this document is believed to be from reliable sources. The AMC

however does not warrant the accuracy, reasonableness and / or completeness of any information. We have included statements / opinions / recommendations in this document,

which contain words, or phrases such as “will”, “expect”, “should”, “believe” and similar expressions or variations of such expressions, that are “forward looking statements”. Actual

results may differ materially from those suggested by the forward looking statements due to risk or uncertainties associated with our expectations with respect to, but not limited to,

exposure to market risks, general economic and political conditions in India and other countries globally, which have an impact on our services and / or investments, the monetary and

interest policies of India, inflation, deflation, unanticipated turbulence in interest rates, foreign exchange rates, equity prices or other rates or prices etc. ICICI Prudential Asset

Management Company Limited (including its affiliates), the Mutual Fund, The Trust and any of its officers, directors, personnel and employees, shall not liable for any loss, damage of

any nature, including but not limited to direct, indirect, punitive, special, exemplary, consequential, as also any loss of profit in any way arising from the use of this material in any

manner. Further, the information contained herein should not be construed as forecast or promise. The recipient alone shall be fully responsible/are liable for any decision taken on

this material.