monthly report june 2016 [email protected] sandhya...

TRANSCRIPT

1

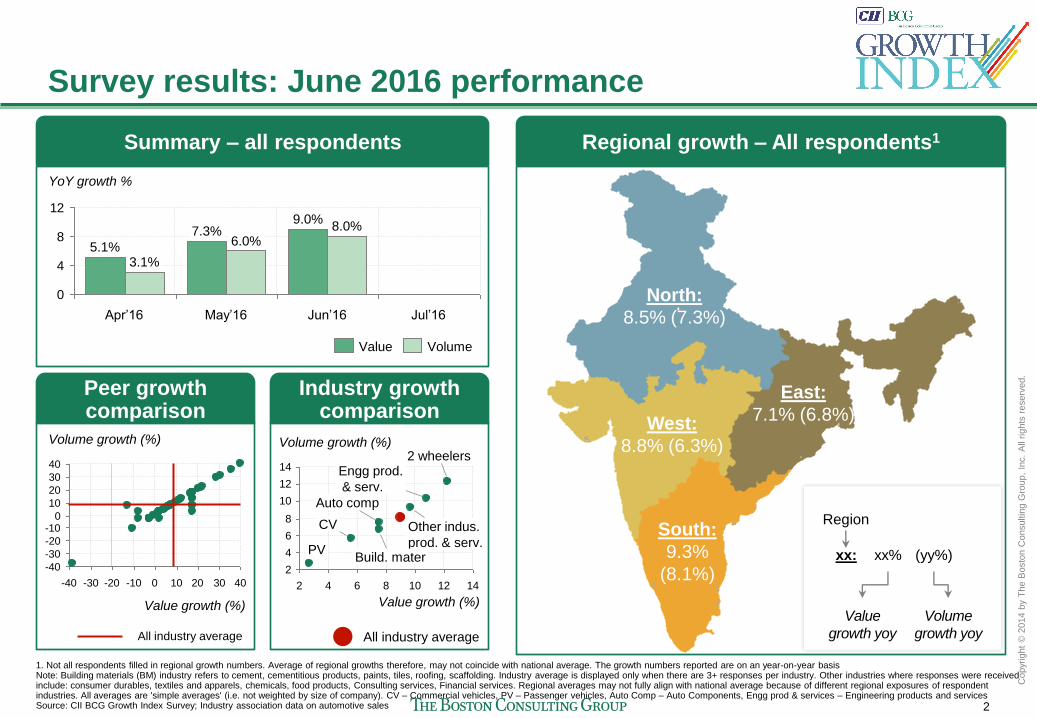

Summary growth trends: June 2016

Overall, June registered a stronger growth of ~9.0% for the Indian industry

compared to May and April that showed growth of 7.3% and 5.1% respectively

Growth was high across all the regions with South witnessing the highest growth

of ~9.3% ; West and North saw healthy growth of ~8.8% and ~8.5% respectively,

while East grew at ~7.7%

Inflation seemed to be in the range of ~1% year-on-year – similar to May and April;

West saw above average price increments as indicated by an inflation of ~2.5%

Engineering products and services, 2-wheelers emerged as winners in June

posting a growth of over 10%; Building materials and Auto components registered

modest growth of ~7.5%, while Commercial vehicles (5.6%) and Passenger

vehicles (2.8%) witnessed relatively weak growth

1. Not all respondents filled in regional growth numbers. Average of regional growths therefore, may not coincide with national average. The growth numbers reported are on an year-on-year basis. Inflation reported above is the value over volume growth based on the survey results. Growth numbers reported are on year-on-year basis Source: CII BCG Growth Index Survey; Industry association data on automotive sales

2

Copyr

ight

© 2

014 b

y T

he B

osto

n C

onsultin

g G

roup,

Inc.

All

rights

reserv

ed.

Value

growth yoy

Volume

growth yoy

Region

xx: xx% (yy%)

Survey results: June 2016 performance

1. Not all respondents filled in regional growth numbers. Average of regional growths therefore, may not coincide with national average. The growth numbers reported are on an year-on-year basis Note: Building materials (BM) industry refers to cement, cementitious products, paints, tiles, roofing, scaffolding. Industry average is displayed only when there are 3+ responses per industry. Other industries where responses were received include: consumer durables, textiles and apparels, chemicals, food products, Consulting services, Financial services. Regional averages may not fully align with national average because of different regional exposures of respondent industries. All averages are 'simple averages' (i.e. not weighted by size of company). CV – Commercial vehicles, PV – Passenger vehicles, Auto Comp – Auto Components, Engg prod & services – Engineering products and services Source: CII BCG Growth Index Survey; Industry association data on automotive sales

Volume Value

0

4

8

12

YoY growth %

Jul’16 Jun’16

8.0% 9.0%

May’16

6.0% 7.3%

Apr’16

3.1% 5.1%

Summary – all respondents Regional growth – All respondents1

Industry growth comparison

Value growth (%)

Peer growth comparison

20 0 -10 -20 -30 -40

40

30

20

10

0 -10

-20

-30

-40

40 30 10

Volume growth (%)

Value growth (%)

2

4

6

8

10

12

14

2 4 6 8 10 12 14

Other indus.

prod. & serv.

2 wheelers

PV

CV

Auto comp

Engg prod.

& serv.

Build. mater

Volume growth (%)

West:

8.8% (6.3%)

South:

9.3%

(8.1%)

North:

8.5% (7.3%)

East:

7.1% (6.8%)

All industry average All industry average

3

Copyr

ight

© 2

014 b

y T

he B

osto

n C

onsultin

g G

roup,

Inc.

All

rights

reserv

ed.

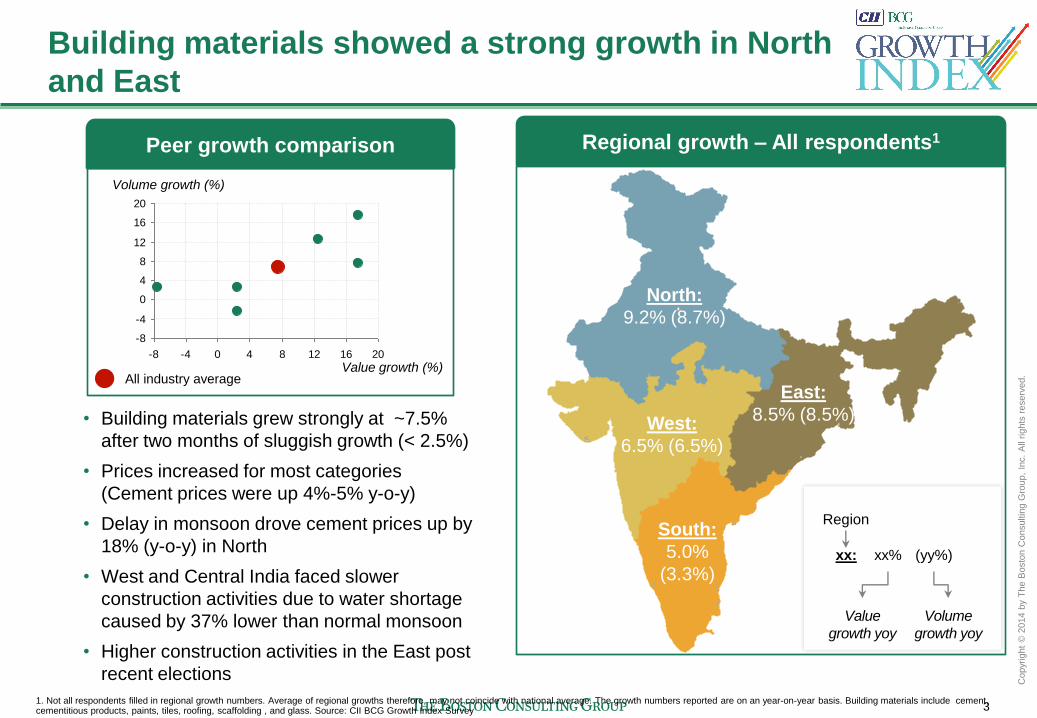

Building materials showed a strong growth in North

and East

Value

growth yoy

Volume

growth yoy

xx: xx% (yy%)

Regional growth – All respondents1

West:

6.5% (6.5%)

South:

5.0%

(3.3%)

North:

9.2% (8.7%)

East:

8.5% (8.5%)

Peer growth comparison

Value growth (%) All industry average

-8

-4

0

4

8

12

16

20

-8 -4 0 4 8 12 16 20

Volume growth (%)

1. Not all respondents filled in regional growth numbers. Average of regional growths therefore, may not coincide with national average. The growth numbers reported are on an year-on-year basis. Building materials include cement, cementitious products, paints, tiles, roofing, scaffolding , and glass. Source: CII BCG Growth Index Survey

• Building materials grew strongly at ~7.5%

after two months of sluggish growth (< 2.5%)

• Prices increased for most categories

(Cement prices were up 4%-5% y-o-y)

• Delay in monsoon drove cement prices up by

18% (y-o-y) in North

• West and Central India faced slower

construction activities due to water shortage

caused by 37% lower than normal monsoon

• Higher construction activities in the East post

recent elections

Region

4

Copyr

ight

© 2

014 b

y T

he B

osto

n C

onsultin

g G

roup,

Inc.

All

rights

reserv

ed.

Automotive industry continued to grow on the back

of a good monsoon and recent 7th pay commission

Passenger vehicle (PV)

• PV showed weak growth of

2.6% (y-o-y)

• Maruti Suzuki witnessed a y-o-y

de-growth of ~10%

• Renault and Ford emerged as

winners posting growth >100%

• Higher growth expected in July

on back of monsoon discounts

and recent pay revisions

Commercial vehicle (CV)

• CV showed modest growth of

5.7% (y-o-y)

• Growth drivers - Govt's push

towards clearing long term road

projects and increasing demand

for heavy truck transportation

• Short term concerns -

Increasing diesel prices and

truck rentals

2-wheelers

Value growth (%) All industry average

-40

-20

0

20

40

60

80

100

120

120 100 80 60 40 20 0 -20 -40

Volume growth (%)

Value growth (%) All industry average

0

4

8

12

16

20

24

0 4 8 12 16 20 24

Volume growth (%)

Value growth (%) All industry average

0

5

10

15

20

25

30

35

40

36 32 28 24 20 16 12 8 4 0

Volume growth (%)

• 2-wheelers witnessed strong

growth of ~12% (y-o-y)

• Yamaha and Royal Enfield

posted growth upwards of 30%

• Govt's pay revision and good

monsoon expected to drive

high growth

1. Not all respondents filled in regional growth numbers. Average of regional growths therefore, may not coincide with national average. The growth numbers reported are on an year-on-year basis Source: CII BCG Growth Index Survey, Industry association data on automotive sales

5

Copyr

ight

© 2

014 b

y T

he B

osto

n C

onsultin

g G

roup,

Inc.

All

rights

reserv

ed.

Engineering products witnessed a high growth

across all the regions

Value

growth yoy

Volume

growth yoy

xx: xx% (yy%)

Regional growth – All respondents1

West:

12.5% (11.3%)

South:

12.5%

(11.3%)

North:

12.5% (11.3%)

East:

11.3% (10%)

Peer growth comparison

Value growth (%) All industry average

-8

-4

0

4

8

12

16

20

-4 0 4 8 12 16 20

Volume growth (%)

1. Not all respondents filled in regional growth numbers. Average of regional growths therefore, may not coincide with national average. The growth numbers reported are on an year-on-year basis. MHE – Material handling equipments Source: CII BCG Growth Index Survey

• Engineering products and services grew

~12% in June 2016 (y-o-y)

• Heavy engineering and electrical segment

get boost from capacity expansion in power

sector and infrastructure – industrial

corridors, airports and road construction

• Steel production to remain low until August -

govt. to review minimum import price

• 100% FDI (automatic route) expected to

intensify competition

Region

6

Copyr

ight

© 2

014 b

y T

he B

osto

n C

onsultin

g G

roup,

Inc.

All

rights

reserv

ed.

MHE riding high on e-commerce, retail boom; South

witnesses highest growth (2/2)

Value

growth yoy

Volume

growth yoy

xx: xx% (yy%)

Regional growth – All respondents1

West:

10.5% (6.5%)

South:

12.5%

(13.5%)

North:

1.0% (5.0%)

East:

4.5% (6.5%)

Peer growth comparison

Value growth (%) All industry average

-8

-4

0

4

8

12

16

20

-8 -4 0 4 8 12 16 20

Volume growth (%)

1. Not all respondents filled in regional growth numbers. Average of regional growths therefore, may not coincide with national average. The growth numbers reported are on an year-on-year basis. MHE – Material handling equipments Source: CII BCG Growth Index Survey

• More than half of the surveyed companies

reported growth of over 15% (y-o-y)

• Rising e-commerce and retail provide major

boost to MHE sector in South and West

• Growth in South driven by government's

push to expand ports, harbours and better

warehousing

• More than average monsoon to drive MHE

demand in agri-warehousing, cold storage,

and automotive sector

Region

7

Commercial vehicle sales

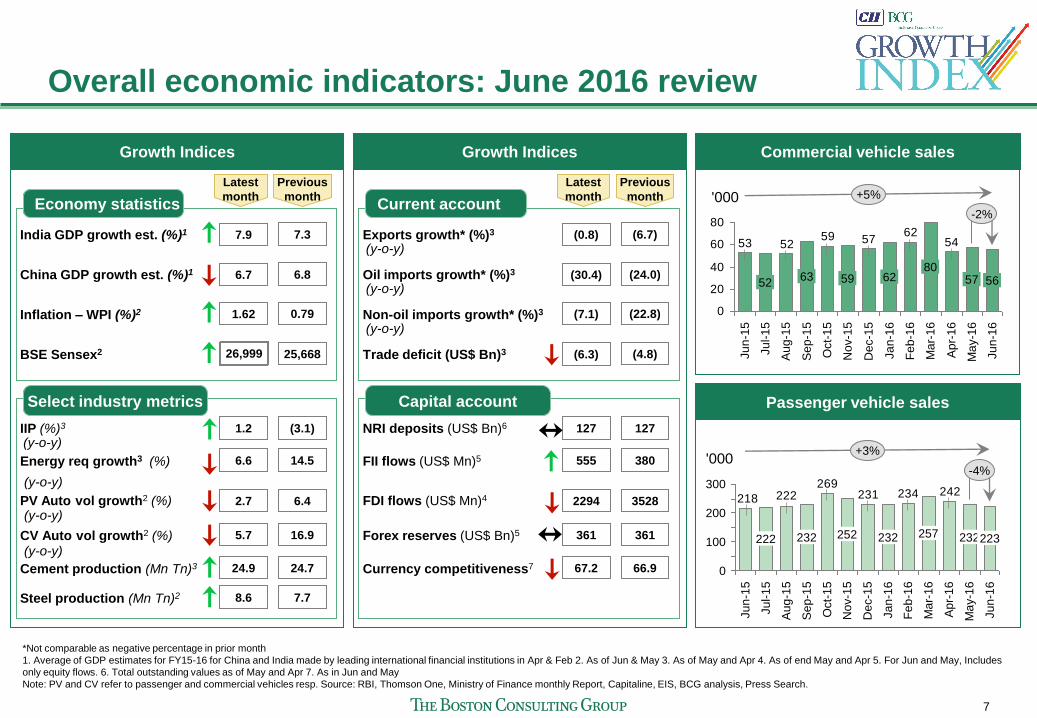

Overall economic indicators: June 2016 review

*Not comparable as negative percentage in prior month

1. Average of GDP estimates for FY15-16 for China and India made by leading international financial institutions in Apr & Feb 2. As of Jun & May 3. As of May and Apr 4. As of end May and Apr 5. For Jun and May, Includes

only equity flows. 6. Total outstanding values as of May and Apr 7. As in Jun and May

Note: PV and CV refer to passenger and commercial vehicles resp. Source: RBI, Thomson One, Ministry of Finance monthly Report, Capitaline, EIS, BCG analysis, Press Search.

Latest

month

Previous

month

India GDP growth est. (%)1

China GDP growth est. (%)1

Inflation – WPI (%)2

BSE Sensex2

Growth Indices

1.62

7.9

6.7

0.79

25,668

7.3

6.8

(y-o-y)

(y-o-y)

(y-o-y)

IIP (%)3

Steel production (Mn Tn)2

CV Auto vol growth2 (%)

Cement production (Mn Tn)3

Energy req growth3 (%)

PV Auto vol growth2 (%)

(y-o-y)

1.2

24.9

6.6

5.7

8.6

2.7

(3.1)

24.7

14.5

16.9

7.7

6.4

Growth Indices

Latest

month

Previous

month

Exports growth* (%)3

Oil imports growth* (%)3

Non-oil imports growth* (%)3

Trade deficit (US$ Bn)3

(7.1)

(6.3)

(0.8)

(30.4)

(22.8)

(4.8)

(6.7)

(24.0)

NRI deposits (US$ Bn)6

Forex reserves (US$ Bn)5

Currency competitiveness7

FII flows (US$ Mn)5

FDI flows (US$ Mn)4

127

67.2

555

361

2294

127

66.9

380

361

3528

Economy statistics

Select industry metrics

Current account

Capital account

(y-o-y)

(y-o-y)

(y-o-y)

Passenger vehicle sales

5462

57595253

0

20

40

60

80

'000

52

Ju

n-1

5

Ja

n-1

6

62

Dec-1

5

Nov-1

5

59

Oct-

15

Se

p-1

5

63

Au

g-1

5

Ju

l-1

5

56

Ju

n-1

6

+5%

-2%

Ma

y-1

6

57

Ap

r-1

6

Ma

r-1

6

80

Fe

b-1

6

242234231269

222218

200

300

100

0

+3%

-4%

Ma

y-1

6

232

Ap

r-1

6

'000

Ma

r-1

6

257

Fe

b-1

6

Ja

n-1

6

232

Dec-1

5

Nov-1

5

252

Oct-

15

Se

p-1

5

232 223

Au

g-1

5

Ju

l-1

5

222

Ju

n-1

5

Ju

n-1

6

26,999

8

Good monsoon to provide further boost to Indian

businesses

Monsoon 2016 forecast

• Overall, 6-7% higher than average monsoon expected (June – Sept)

• Last year, 15% lower than average monsoon was received ~20% higher than last year

• Good monsoon to positively affect Automotive, Building materials, Warehousing, MHE, consumer durables,

and FMCG sectors

June statistics

• Arrived a week late on June 7

• The cumulative monsoon in June (until June 21) was 21% less than normal

– East and North-east: 29% below normal

– Central India: 37% below normal

– North India: 8% below normal

– Southern peninsula: 13% above normal

Forecast for July

• Higher than normal monsoon expected in July across India; 35% more than normal precipitation in the first

week of July

• Central and North (MP, UT, HP, Delhi, East Rajasthan) India to receive higher than normal precipitation in the

2nd and 3rd week – flood conditions and disruption due to river swelling Source: Indian Meteorological Department. MHE – Material Handling Equipments

Thank you

bcg.com | bcgperspectives.com