monthly world energy review-september-2018 · 2018/09/06 · corp, ecopetrol sa and equinor brasil...

TRANSCRIPT

Monthly World EnergyMarket Review

Release Date: September 6, 2018

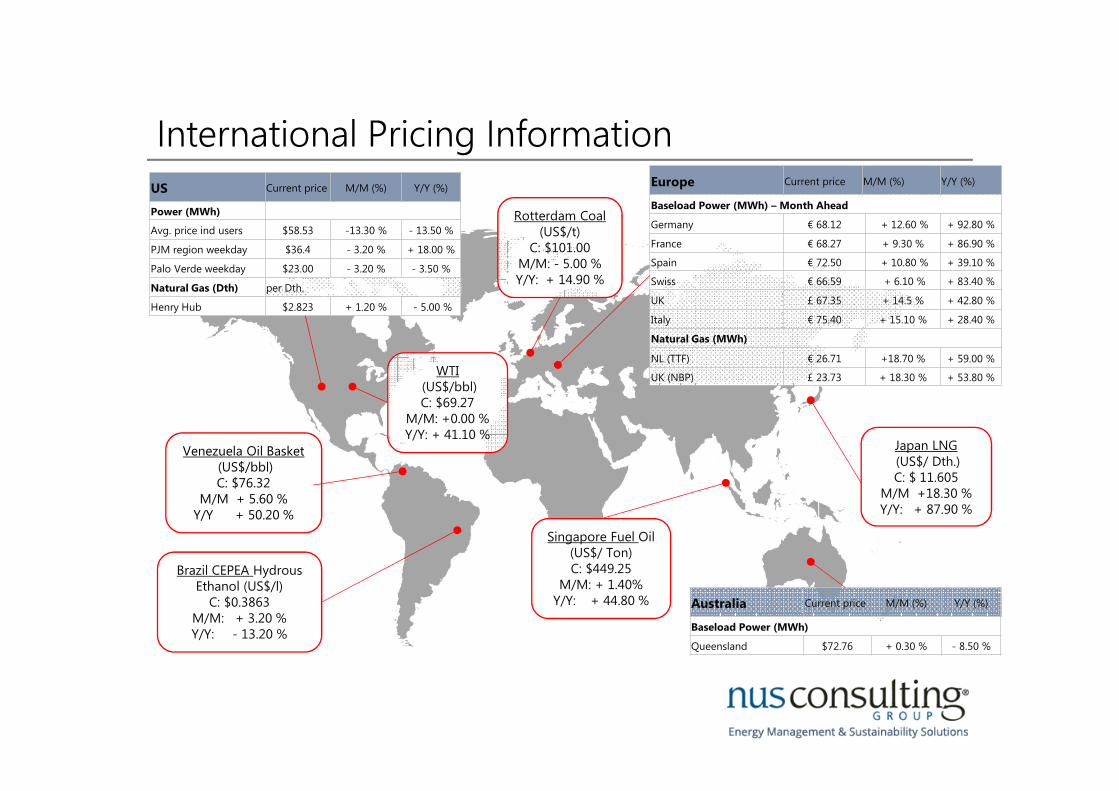

International Pricing Information

US Current price M/M (%) Y/Y (%)

Power (MWh)

Avg. price ind users $58.53 -13.30 % - 13.50 %

PJM region weekday $36.4 - 3.20 % + 18.00 %

Palo Verde weekday $23.00 - 3.20 % - 3.50 %

Natural Gas (Dth) per Dth.

Henry Hub $2.823 + 1.20 % - 5.00 %

WTI (US$/bbl)C: $69.27

M/M: +0.00 %Y/Y: + 41.10 %

Venezuela Oil Basket(US$/bbl)C: $76.32

M/M + 5.60 %Y/Y + 50.20 %

Brazil CEPEA Hydrous Ethanol (US$/l)

C: $0.3863M/M: + 3.20 %Y/Y: - 13.20 %

Europe Current price M/M (%) Y/Y (%)

Baseload Power (MWh) – Month Ahead

Germany € 68.12 + 12.60 % + 92.80 %

France € 68.27 + 9.30 % + 86.90 %

Spain € 72.50 + 10.80 % + 39.10 %

Swiss € 66.59 + 6.10 % + 83.40 %

UK £ 67.35 + 14.5 % + 42.80 %

Italy € 75.40 + 15.10 % + 28.40 %

Natural Gas (MWh)

NL (TTF) € 26.71 +18.70 % + 59.00 %

UK (NBP) £ 23.73 + 18.30 % + 53.80 %

Rotterdam Coal (US$/t)

C: $101.00M/M: - 5.00 %Y/Y: + 14.90 %

Singapore Fuel Oil (US$/ Ton)C: $449.25

M/M: + 1.40%Y/Y: + 44.80 %

Japan LNG(US$/ Dth.)C: $ 11.605

M/M +18.30 %Y/Y: + 87.90 %

Australia Current price M/M (%) Y/Y (%)

Baseload Power (MWh)

Queensland $72.76 + 0.30 % - 8.50 %

Global Energy Review – International Markets

• China wants grid companies to restructure and turn their electricity trading arms into independent firms. The plan is part of

China’s year-long efforts to liberalize its electricity market. All types of companies will be encouraged to invest in the new

electricity trading firms, with non-grid companies taking at least 20 percent stakes. Grid companies must submit their plans for

reforming electricity trading arms to central government by the end of September, and the reforms need to be completed by the

end of this year.

• Russian coal exports rose 5% year on year in August to a multi-year high of 555,000t/day (17.2m tonnes), amid buoyant Asian

demand and improved logistics infrastructure. The rise was likely fuelled by increased Asia-Pacific demand for Russian coal,

particularly in light of limited Australian availability last month. The increase in Russian exports came despite disruptions to

loadings at the country’s largest European export hub of Ust-Luga, near St Petersburg, which was carrying out maintenance

work.

• Japan has acknowledged for the first time that a worker at the Fukushima nuclear power plant, destroyed by an earthquake and

tsunami more than seven years ago, died from radiation exposure. A 9.0 magnitude earthquake struck in March 2011,

triggering a tsunami that killed some 18,000 people and the world’s worst nuclear disaster since Chernobyl 25 years earlier.

The worker had spent his career working at nuclear plants around Japan and worked at the Fukushima Daiichi plant operated

by Tokyo Electric Power at least twice after the March 2011 meltdowns at the station. Hundreds of deaths have been attributed

to the chaos of evacuations during the crisis and because of the hardship and mental trauma refugees have experienced since

then, but the government had said that radiation was not a cause.

International Energy Markets - Review

Global Energy Review – US Markets

• Crude oil pricing extended July losses during the first half of August before reversing course over the last two weeks of the month. The

prompt-month NYMEX WTI futures contract traded below $65 per barrel on August 15 and 16, but rallied back above $70 per barrel by

the end of the month. Brent crude futures were similarly higher over the last two weeks of August, rallying from an intra-month low of

$70.30 per barrel to a high of $78 ahead of the Labor Day weekend. A reduction in Iranian oil exports following renewed U.S.

sanctions, tensions in Libya that threaten additional output, and lost export capacity in Venezuela following an accident at the key Port

of Jose terminal have contributed to rising concerns over supply availability in the global market. The October 2018 NYMEX crude oil

futures contract closed on August 31 at $69.80 per barrel, with Brent crude at $77.42 per barrel.

• After breaking above $2.85 per MMBtu in the opening days of August, prompt-month NYMEX natural gas futures generally held in a

tight range between $2.85 and $3.00 per MMBtu for the balance of the month. Market participants continue to weigh record U.S. gas

production levels against robust demand and lackluster storage inventories. The U.S. Energy Information Administration (EIA)

reported weekly natural gas production above 82 Bcf per day throughout the last month, at times more than 10 Bcf per day ahead of

the same period last year. However, demand growth generally kept pace, as evidenced by continued weakness in summer injections

to natural gas storage inventories. Through the week ending August 24, storage sat at 2,505 Bcf, a deficit of almost 600 Bcf to the

benchmark five-year average and 646 Bcf behind year-ago levels. The October 2018 NYMEX natural gas futures contract closed on

July 31 at $2.916 per MMBtu, with average pricing for calendar year 2019 at $2.787 per MMBtu.

United States Energy Markets - Review

Global Energy Review – European Markets

• Belgium will have sufficient power supply this winter despite extended outages at nuclear power reactors Doel 1 and 2 until December.

Fears of power shortages have mounted as only three out of the country’s seven nuclear plants are currently offline and expected back

close to the start of the winter. Belgium has had its power supply reserve in place since its launch in the winter of 2014/2015 when

power prices plummeted and forced more expensive gas-fired plants off the market. This tallied with unexpected nuclear outages in

Belgium, threatening security of supply, which caused the minister to extend the lifetime of reactors until mid-2025.

• Spain: Gas volumes traded on Spain’s gas exchange Mibgas set a new record high of 2 TWh in August, or 8.3% of the country’s gas

demand in the month. However, the volume of gas futures traded beyond the month-ahead were limited to 34 GWh, including

quarterly, seasonal and annual contracts. The September contract hit EUR 29.50/MWh in August’s last daily auction, the highest on a

rolling basis since Mibgas started operations in 2016.

• Poland will hold its first capacity auctions on 15 November for conventional plants providing back-up power for 2021 start-up with aims

to secure 22.7 GW. The auctions – with two similar ones planned for December for delivery in 2022 (up to 23 W) and 2023 (up to 23.3

GW), respectively – would be open to coal-fired plants, as well as gas and renewable technology. Foreign plants from neighbouring

countries can bid in auctions from 2025 but only for contracts of up to a year. The so-called capacity market would remunerate plant

owners for keeping their units on standby for use at times of tight supply. Many countries, such as the UK and France, use capacity

auctions as a way of ensuring security of supply and to help balance the grid during periods of peak demand.

• Prompt prices on the UK’s NBP hub soared again – after jumping in the prior session – amid a short system and forecasts of cool

weather. The UK market is very short and weather forecasts look dry and colder, which means more demand for gas-fired power.

European Energy Markets - Review

Global Energy Review – Asia/Pac Markets

• Indonesia will widen a biofuel mandate to cover railways and power plants starting next month as they seek to save billions of

dollars in fossil fuel imports. The railways and electricity generators will need to use fuel blended with 20 percent palm

biodiesel from Sept. 1. The government had earlier said the expanded mandate would also include military and mining

vehicles. The mandate will help the country cut crude oil imports worth about 50 trillion rupiah ($3.5 billion) annually. Indonesia

is battling an emerging-market selloff and a deteriorating current-account deficit, prompting President Joko Widodo to consider

options to boost foreign-exchange earnings and stem a rout in its currency. The push for increased use of biodiesel will also

help cushion the impact of soaring costs for subsidizing fuel and electricity after Widodo pledged not to raise tariffs ahead of

next year’s general election.

• Singapore is opening up its retail electricity market to full competition this year. Once this has been completed, solar power

developers will be able to tap the residential consumer market to offer green electricity. After 2020, the pace of installation is

expected to be even faster; given the target to reach 1 GW capacity 'beyond 2020. Singapore’s focus on large-scale solar

systems despite the lack of physical space and the long-term impact of the looming carbon tax scheme — serve to illustrate

Singapore’s growing pains in its drive to become a renewables leader in Southeast Asia. The OEM is one of the key projects

meant to propel solar power development in Singapore and enable the country to meet its target of 350 MW installed capacity,

and it has a lot more ground to cover.

• China: Chinese energy companies Sinopec Corporation and Zhejiang Energy have agreed to jointly develop the 3 Mt/year

LNG regasification terminal project in Wenzhou (Zhejiang province, East China). The first phase of the project is set for

operation by the end of 2021 while the whole project is slated for completion by 2025.

Asia-Pac Energy Markets - Review

Global Energy Review – LATAM Markets

• Mexico: Mexico’s next government plans to build what could be the country’s largest oil refinery, with construction set to begin

as soon as next year. The winner of July’s presidential election Andres Manuel Lopez Obrador is seeking to end Mexico’s

massive fuel imports, nearly all of which come from the United States, while boosting domestic refining during the first half of

his six-year term. While his aides have provided some details on the plans, Lopez Obrador himself has mostly spoken in

general terms and had not previously provided numbers. It will be a refinery that will produce 400,000 barrels per day of

gasoline with an approximate cost of $8 billion that Mexico wants to build in three years.

• Brazil: Brazil’s oil industry regulator ANP informed that it had approved an additional six energy companies to bid for four sub-

salt blocks in the Campos and Santos Basins to be auctioned on Sept. 28, expanding the number of potential bidders to 12.

The companies newly approved to bid are Chevron Corp , CNOOC Petroleum Brasil Ltda, Petroleo Brasileiro SA, Exxon Mobil

Corp, Ecopetrol SA and Equinor Brasil Energia Ltda.

• Venezuela: Venezuela’s crude sales to the United States fell in August for the second month in a row as exports of two of the

South American country’s main grades dropped following port interruptions by a tanker collision. Venezuela’s state-run oil

company Petróleos de Venezuela’s shipments have been affected in recent weeks by export limitations at the country’s main

oil port, Jose, after a minor tanker collision forced the state-run firm to halt operations at one of its three berths. The Jose dock

problem came as the country was attempting to reverse a series of blows to oil exports, including declining output, a severe

lack of investment in its energy infrastructure and asset seizure attempts by creditors. PDVSA last week started a contingency

plan for diverting tankers waiting at Jose to load to the nearby terminal of Puerto la Cruz. The state-run company last month

exported to the United States a 500,000-barrel cargo of Merey crude and three 500,000-barrel cargoes of Zuata crude, two of

the OPEC-nation’s main grades for exports.

LATAM Energy Markets - Review

Appendix – Commodity Pricing Data

Brent Crude - month ahead contract (US$ per barrel)

Foreign Exchange (Euro/USD)

Appendix – Commodity Pricing Data

Coal CIF ARA 2018 delivery ($/T)

Natural gas prices, “Calendar year 2018” (NBP in £p/therm & TTF in €/MW/h)

Appendix – Commodity Pricing Data

European electricity prices for “Calendar Year 2019” (€/MWh)

Appendix – Commodity Pricing Data

European day ahead electricity prices (€/MWh)

Glossary

Term Definition

Avg Price Industrial Users Latest unit cost for electricity consumed by industrial users as reported by the U.S. Energy Information Administration (EIA). The EIA usually publishes the data 4 months after the month of consumption.

Henry Hub Natural GasThe Henry hub in Erath, Louisiana serves as the pricing point for natural gas futures traded on the New York Mercantile Exchange (NYMEX).

WTI Crude Oil

The reported WTI light crude oil future price is the market determined value of next month’s contract to either buy or sell in multiples of 1,000 barrels West Texas Intermediate or other light sweet crude oil. WTI light crude oil contracts are only executed for physical delivery in relatively few cases but nevertheless they serve as an important pricing mechanism for contracts that are actually executed for physical delivery.

PJM Region Weekday

The Pennsylvania-New Jersey-Maryland (PJM) interconnection functions as a power pool for all or parts of Delaware, Illinois, Indiana, Kentucky, Maryland, Michigan, New Jersey, North Carolina, Ohio, Pennsylvania, Tennessee, Virginia, West Virginia and the District of Columbia. The PJM power pool is currently the largest competitive wholesale electricity market. The price reported here is the price during weekdays.

Palo Verde Weekday

The Palo Verde switchyard located in Tonopah, Arizona is a key point in the western states power grid and is used as a pricing point for electricity across the southwest United States. The price reported here is the average market price for peak electricity to be consumed on the next day. Peak hours under this contract are from Mon – Sat between 0700 – 2200 hours local time.

Brazilian EthanolThe market price for a next month delivery of 1liter of ethanol at the mill gate in Sao Palo state as calculated by Cepea.

Rotterdam CoalThe market price for a next month delivery of coal in the Amsterdam – Rotterdam – Antwerp (ARA) port area.

GermanyThe market price for one MWh of baseload electricity to be delivered next month as traded on the EPEX Spot Market www.epexspot.com.

FranceThe market price for one MWh of baseload electricity to be delivered next month as traded on the EPEX Spot Market www.epexspot.com.

Glossary

Term Definition

SpainThe market price for one MWh of baseload electricity to be delivered next month as traded on the trading platform belonging to the Operador do Mercado Iberico de Energia (OMIP).

SwissThe market price for one MWh of baseload electricity to be delivered next month as traded on the European Energy Exchange (EEX).

UKThe market price for one MWh of baseload electricity to be delivered next EFA month as traded on the Intercontinental Exchange (ICE). EFA month stands for the specific calendar in use under the Electricity Forwards Agreement that breaks up the year in equal blocks of 4 and 5 weeks so as to simplify trading.

TTFThe Title Transfer Facility (TTF) is a virtual hub that serves as a pricing point for natural gas contracts within the Dutch gas network. The actual contracts are traded on the European Energy Derivatives Exchange (ENDEX).

NBPThe National Balancing Point (NBP) is a virtual hub that serves as a pricing point for natural gas contracts within the United Kingdown. The actual contracts are traded on the Intercontinental exchange (ICE).

Singapore Fuel OilThe market price for Free on Board (FOB) 180 Centistoke (CST) fuel oil in Singapore port to be delivered next month.

Japan LNGThe reported price for LNG in Japan is derived from the price of West Texas Intermediate (WTI) crude oil by means of an index formula and is reported in US Dollar per decatherm.

Queensland Baseload PowerThe market price for one MWh of baseload electricity to be delivered next month in Queensland as traded on the Australian Securities Exchange (ASX).

Brent Crude OilBrent crude oil is a combination of light crude oil from 15 different oil fields located in the North Sea. Due to the high quality of Brent crude, it is ideal for making gasoline and middle distillates. As such, Brent crude forms the pricing benchmark in Europe and Africa.

Glossary

Term Definition

Foreign ExchangeThe blue line in the graph presents the daily exchange rates Euro to USD while the red line represents the moving average over the last 14 trading days.

Coal CIF ARA 20XX DeliveryCoal is an important input fuel for electricity generation. The coal price reported in appendix 3 is inclusive of commodity Cost, Insurance and Freight (CIF) from its origin to the ports of Amsterdam – Rotterdam –Antwerp (ARA) to be delivered next month.

Natural Gas Price for Calendar 20XX

The featured contracts in this graph are for the delivery of natural gas in the UK (NBP), Dutch (TTF) and German (EEX) markets in the next Calendar year. The benefit of the annual contract is that the buyer has an average price throughout the year rather than individual prices for each month that are priced according to market conditions and can show great variances between winter and summer prices. For further information on the specific country contracts, please refer to the glossary for the world report.

European Electricity Prices for Calendar Year 20XX

The featured contracts represent the current market price for one MWh of baseload electricity to be delivered next calendar year (except UK) as traded on each of the respective exchanges mentioned as source. The electricity market in the UK features the season contract as its longest contract. As a result, the reported market price is the average of the nearest summer and winter contracts.

European Day Ahead Electricity Prices

Next to future contracts, each electricity exchange also features a day ahead contract. The day ahead contracts are characterized by greater volatility than the monthly and longer period future contracts as they are more susceptible to actual supply and demand on the day as well as the other factors influencing the longer contract prices.

Confidential

This presentation and the information contained herein is confidential and

intended for NUS Consulting Group clients.

The material contained herein represents the opinion and views of NUS Consulting

Group and is provided to discuss general market activity, industry and sector

trends, as well as other broad-based economic, market and political conditions.

This information should not be construed as research or investment/purchasing

advice. Persons responsible for the purchase of energy for an organisation must

consider their organisation’s own objectives, risk tolerance and market forecast

when undertaking energy purchasing decisions.

The circulation or distribution of this presentation or the information contained

herein to persons other than the Intended Entity or its employees is strictly

prohibited