moody’s muni bond rating criteria & ks local government trends conference presentations/denise...

TRANSCRIPT

Moody’s Muni Bond Rating Criteria & KS Local Government TrendsDenise Rappmund, VP – Senior Analyst October 2017

Kansas City and County Ratings 2

Agenda1. Introduction to Moody’s 2. General Obligation Methodology & Scorecard3. Municipal Utility Methodology & Scorecard4. Kansas City & County Credit Trends5. Publication links

1 Introduction to Moody’s

Kansas City and County Ratings 4

Moody’s Investors Service

» Moody’s Investors Service (MIS) provides credit ratings on bonds issued by commercial & government entities

» MIS has analysts that specialize in specific sectors, determined by pledged security– Local Government– States– Infrastructure– Higher Education, Housing, Heath care

» In Kansas, our local government team rate cities, counties, school districts, CCDs, park districts, and utility systems

» The credit rating methodologies we are using in Kansas are largely General Obligation and Municipal Utility

Kansas City and County Ratings 5

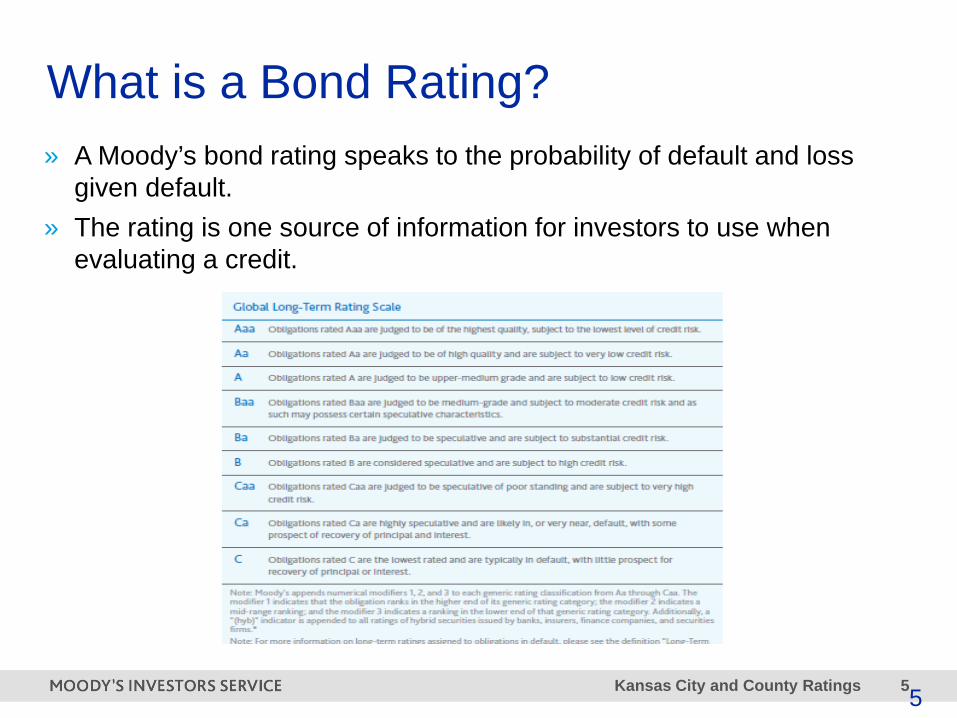

What is a Bond Rating?» A Moody’s bond rating speaks to the probability of default and loss

given default.» The rating is one source of information for investors to use when

evaluating a credit.

5

2 General Obligation Methodology & Scorecard

Kansas City and County Ratings 7

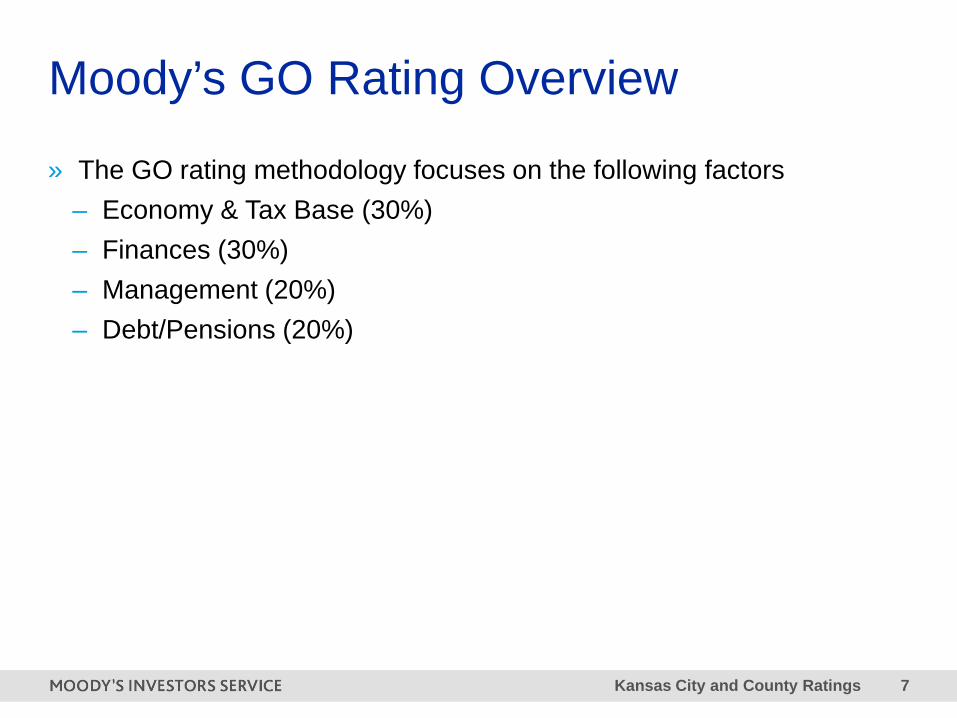

Moody’s GO Rating Overview

» The GO rating methodology focuses on the following factors– Economy & Tax Base (30%) – Finances (30%) – Management (20%) – Debt/Pensions (20%)

Kansas City and County Ratings 8

Economy & Tax Base (30%)

» Considerations generally include– Tax base size, growth rate & tax rates– Institutional presence & diversity– Major employers– Tax base concentration– Population and migration trends– Wealth & income indices (MFI, unemployment, poverty)

Kansas City and County Ratings 9

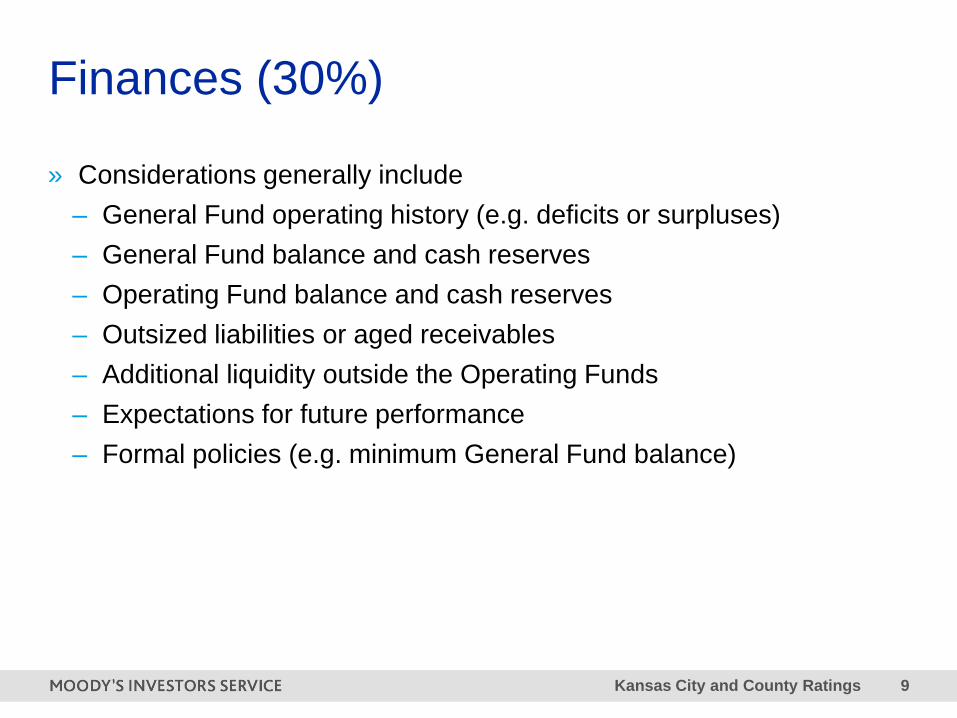

Finances (30%)

» Considerations generally include– General Fund operating history (e.g. deficits or surpluses)– General Fund balance and cash reserves– Operating Fund balance and cash reserves– Outsized liabilities or aged receivables – Additional liquidity outside the Operating Funds– Expectations for future performance– Formal policies (e.g. minimum General Fund balance)

Kansas City and County Ratings 10

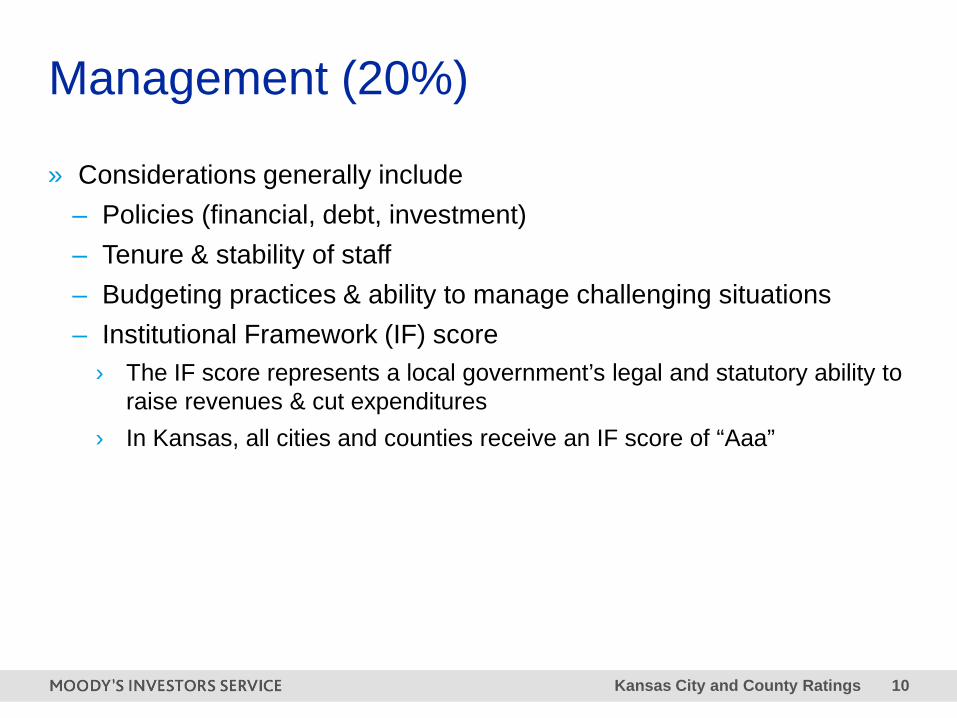

Management (20%)

» Considerations generally include– Policies (financial, debt, investment)– Tenure & stability of staff– Budgeting practices & ability to manage challenging situations– Institutional Framework (IF) score

› The IF score represents a local government’s legal and statutory ability to raise revenues & cut expenditures

› In Kansas, all cities and counties receive an IF score of “Aaa”

Kansas City and County Ratings 11

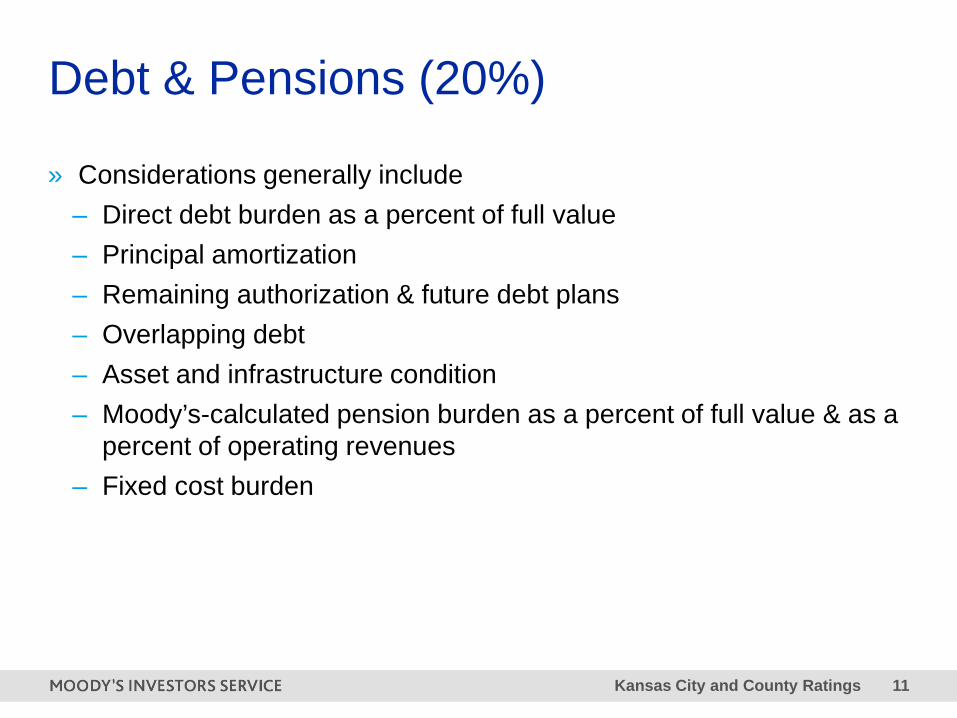

Debt & Pensions (20%)

» Considerations generally include– Direct debt burden as a percent of full value – Principal amortization – Remaining authorization & future debt plans– Overlapping debt– Asset and infrastructure condition– Moody’s-calculated pension burden as a percent of full value & as a

percent of operating revenues– Fixed cost burden

Kansas City and County Ratings 12

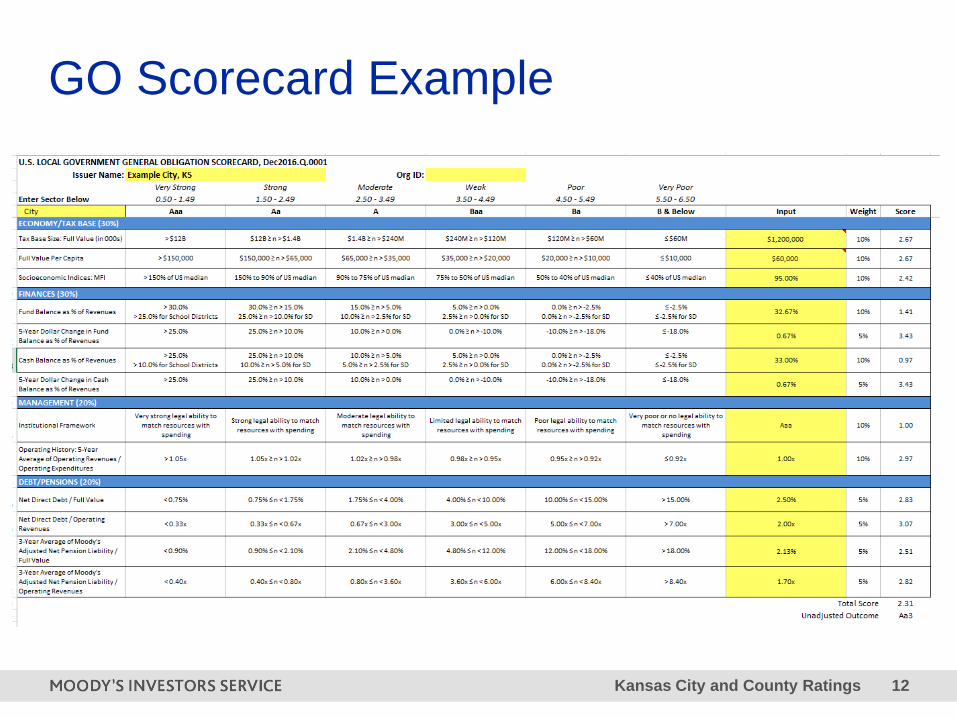

GO Scorecard Example

Kansas City and County Ratings 13

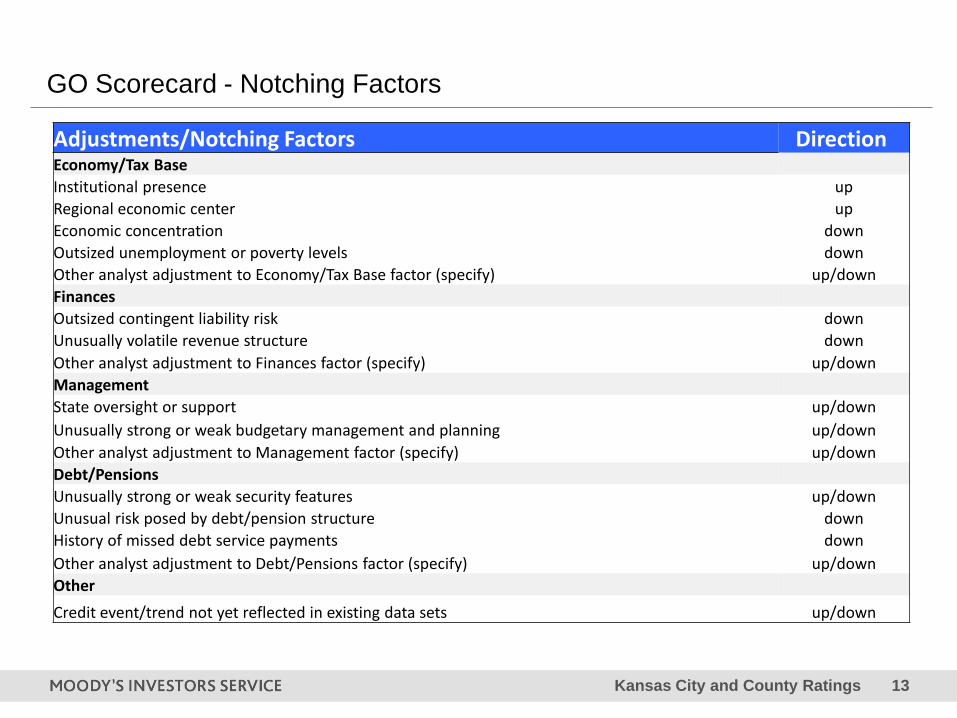

GO Scorecard - Notching Factors

Adjustments/Notching Factors DirectionEconomy/Tax BaseInstitutional presence upRegional economic center upEconomic concentration downOutsized unemployment or poverty levels downOther analyst adjustment to Economy/Tax Base factor (specify) up/downFinancesOutsized contingent liability risk downUnusually volatile revenue structure downOther analyst adjustment to Finances factor (specify) up/downManagementState oversight or support up/downUnusually strong or weak budgetary management and planning up/downOther analyst adjustment to Management factor (specify) up/downDebt/PensionsUnusually strong or weak security features up/downUnusual risk posed by debt/pension structure downHistory of missed debt service payments downOther analyst adjustment to Debt/Pensions factor (specify) up/downOtherCredit event/trend not yet reflected in existing data sets up/down

Kansas City and County Ratings 14

Use of Methodology ScorecardsPurpose and Use of Methodology Scorecards:

Enhance the transparency of our rating process

Capture the key considerations that correspond to particular rating categories

Not an exhaustive list of factors that we consider in every rating assignment

Scorecards are mostly quantitative, but include some qualitative metrics

May adjust up or down from scorecard-indicated outcome based on additional factors

Scorecard acts as a starting point for a more thorough and individualistic analysis

Final rating is determined by a Rating Committee after consideration of all relevant facts

Kansas City and County Ratings 15

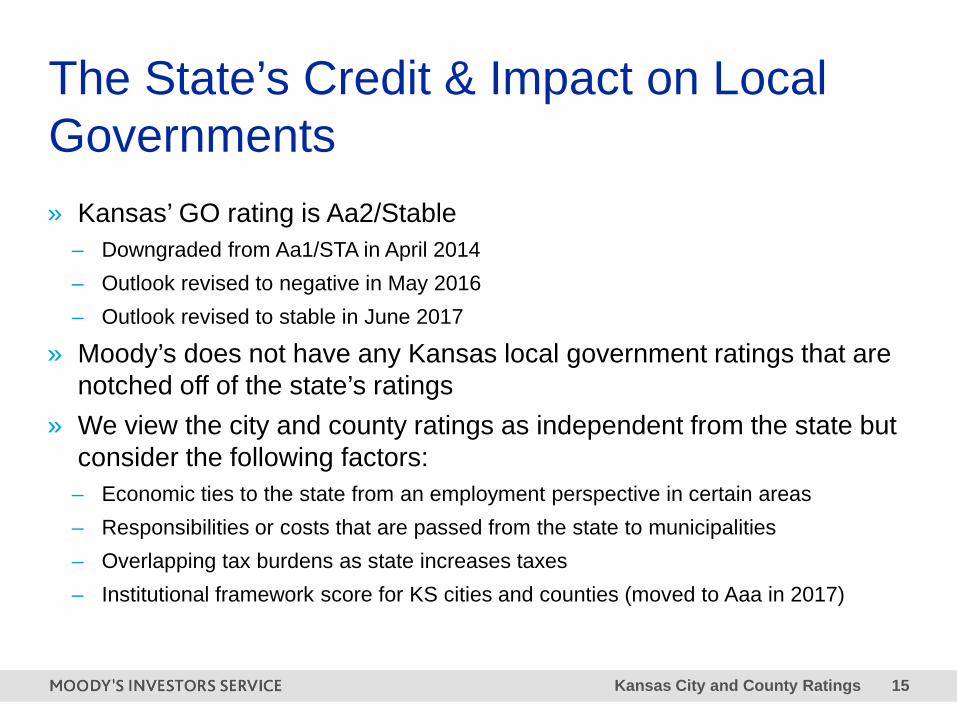

The State’s Credit & Impact on Local Governments» Kansas’ GO rating is Aa2/Stable

– Downgraded from Aa1/STA in April 2014– Outlook revised to negative in May 2016– Outlook revised to stable in June 2017

» Moody’s does not have any Kansas local government ratings that are notched off of the state’s ratings

» We view the city and county ratings as independent from the state but consider the following factors:

– Economic ties to the state from an employment perspective in certain areas– Responsibilities or costs that are passed from the state to municipalities– Overlapping tax burdens as state increases taxes– Institutional framework score for KS cities and counties (moved to Aaa in 2017)

Kansas City and County Ratings 16

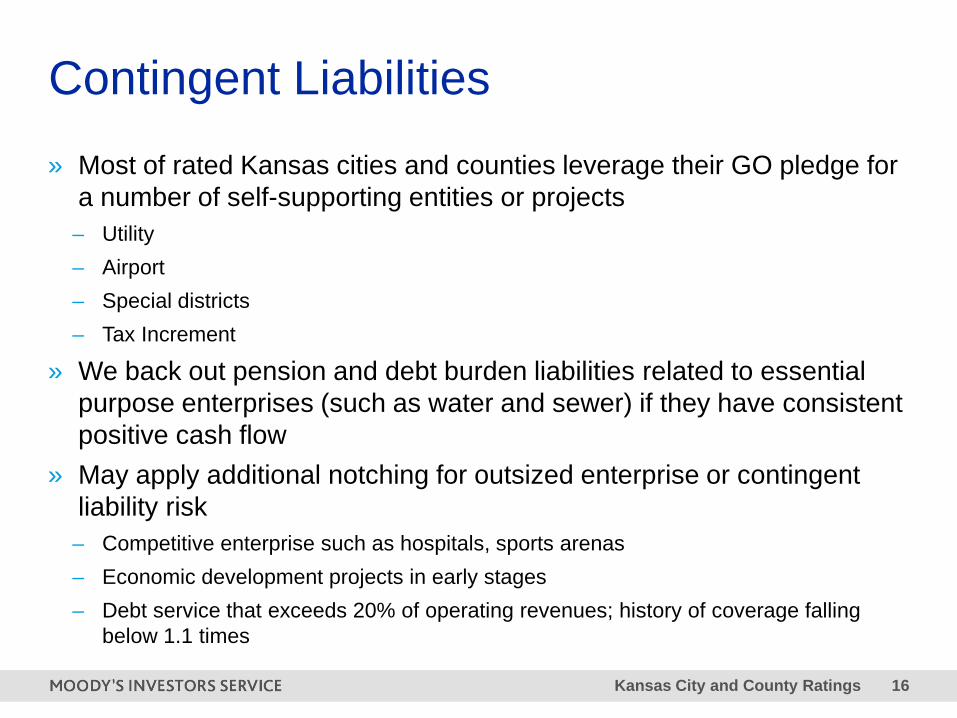

Contingent Liabilities» Most of rated Kansas cities and counties leverage their GO pledge for

a number of self-supporting entities or projects– Utility– Airport– Special districts– Tax Increment

» We back out pension and debt burden liabilities related to essential purpose enterprises (such as water and sewer) if they have consistent positive cash flow

» May apply additional notching for outsized enterprise or contingent liability risk

– Competitive enterprise such as hospitals, sports arenas– Economic development projects in early stages– Debt service that exceeds 20% of operating revenues; history of coverage falling

below 1.1 times

Kansas City and County Ratings 17

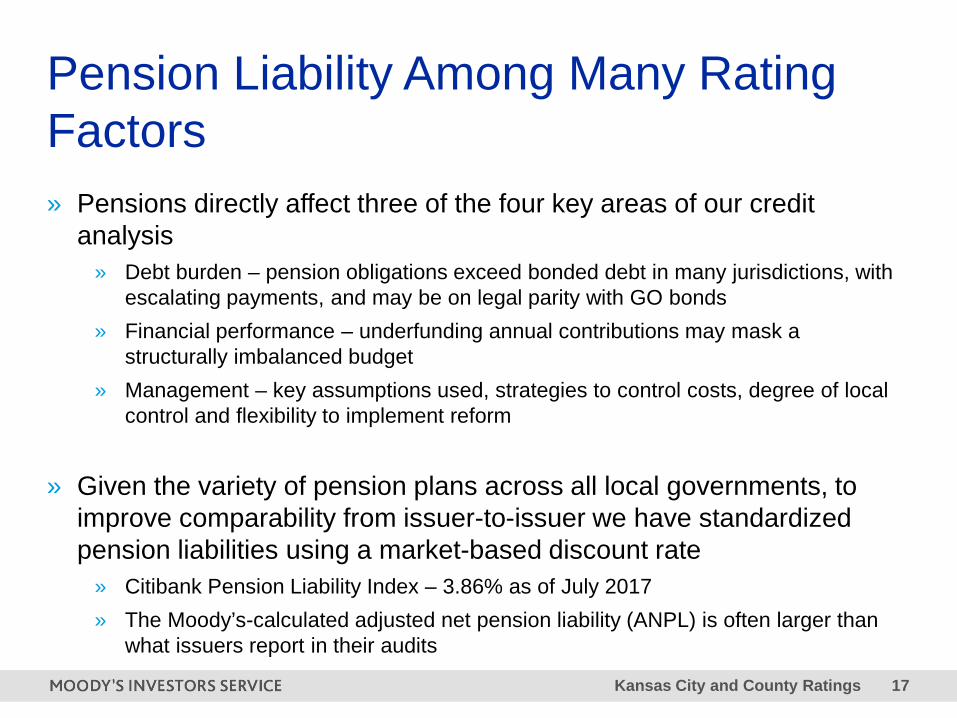

Pension Liability Among Many Rating Factors» Pensions directly affect three of the four key areas of our credit

analysis» Debt burden – pension obligations exceed bonded debt in many jurisdictions, with

escalating payments, and may be on legal parity with GO bonds» Financial performance – underfunding annual contributions may mask a

structurally imbalanced budget» Management – key assumptions used, strategies to control costs, degree of local

control and flexibility to implement reform

» Given the variety of pension plans across all local governments, to improve comparability from issuer-to-issuer we have standardized pension liabilities using a market-based discount rate

» Citibank Pension Liability Index – 3.86% as of July 2017» The Moody’s-calculated adjusted net pension liability (ANPL) is often larger than

what issuers report in their audits

Kansas City and County Ratings 18

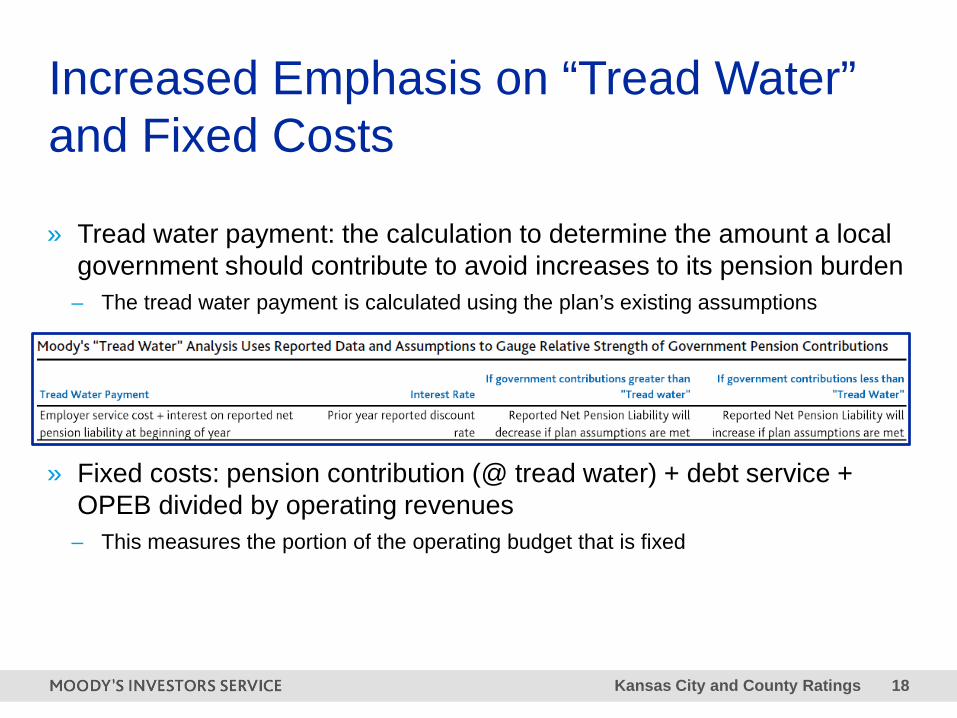

» Tread water payment: the calculation to determine the amount a local government should contribute to avoid increases to its pension burden

– The tread water payment is calculated using the plan’s existing assumptions

» Fixed costs: pension contribution (@ tread water) + debt service + OPEB divided by operating revenues

– This measures the portion of the operating budget that is fixed

Increased Emphasis on “Tread Water” and Fixed Costs

3 Municipal Utility Methodology & Scorecard

Kansas City and County Ratings 20

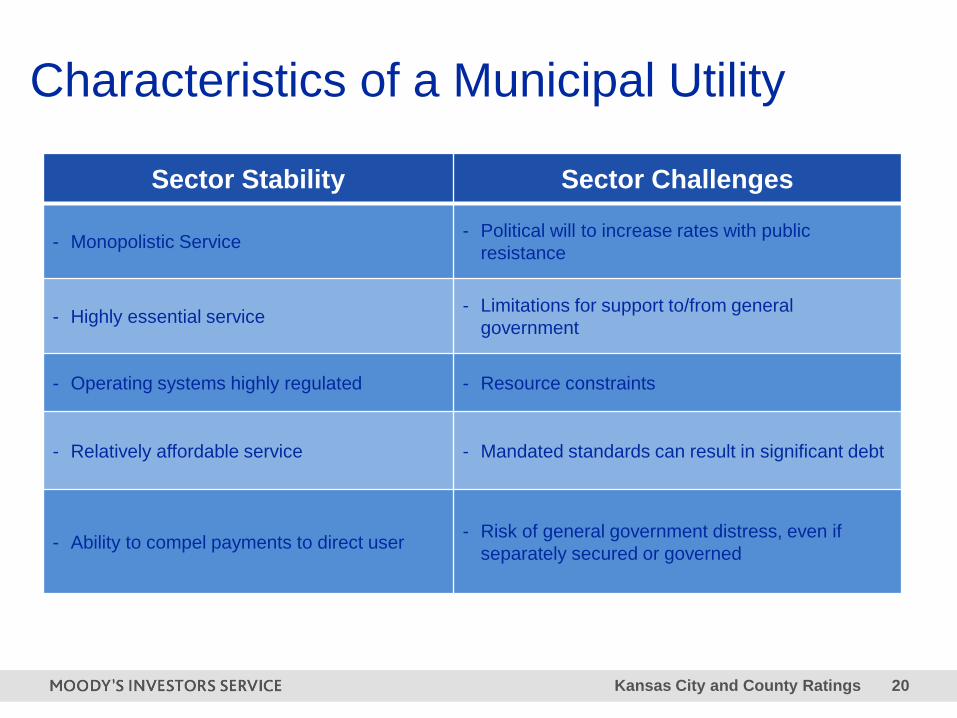

Characteristics of a Municipal Utility

Sector Stability Sector Challenges

- Monopolistic Service - Political will to increase rates with public resistance

- Highly essential service - Limitations for support to/from general government

- Operating systems highly regulated - Resource constraints

- Relatively affordable service - Mandated standards can result in significant debt

- Ability to compel payments to direct user - Risk of general government distress, even if separately secured or governed

Kansas City and County Ratings 21

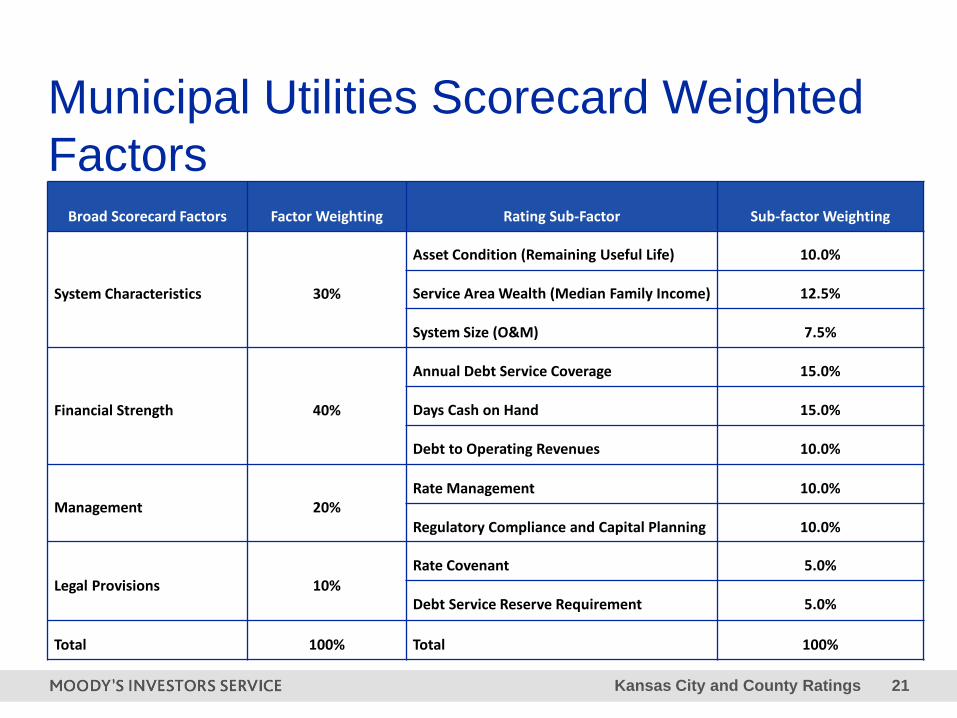

Municipal Utilities Scorecard Weighted Factors

Broad Scorecard Factors Factor Weighting Rating Sub-Factor Sub-factor Weighting

System Characteristics 30%

Asset Condition (Remaining Useful Life) 10.0%

Service Area Wealth (Median Family Income) 12.5%

System Size (O&M) 7.5%

Financial Strength 40%

Annual Debt Service Coverage 15.0%

Days Cash on Hand 15.0%

Debt to Operating Revenues 10.0%

Management 20%Rate Management 10.0%

Regulatory Compliance and Capital Planning 10.0%

Legal Provisions 10%Rate Covenant 5.0%

Debt Service Reserve Requirement 5.0%

Total 100% Total 100%

Kansas City and County Ratings 22

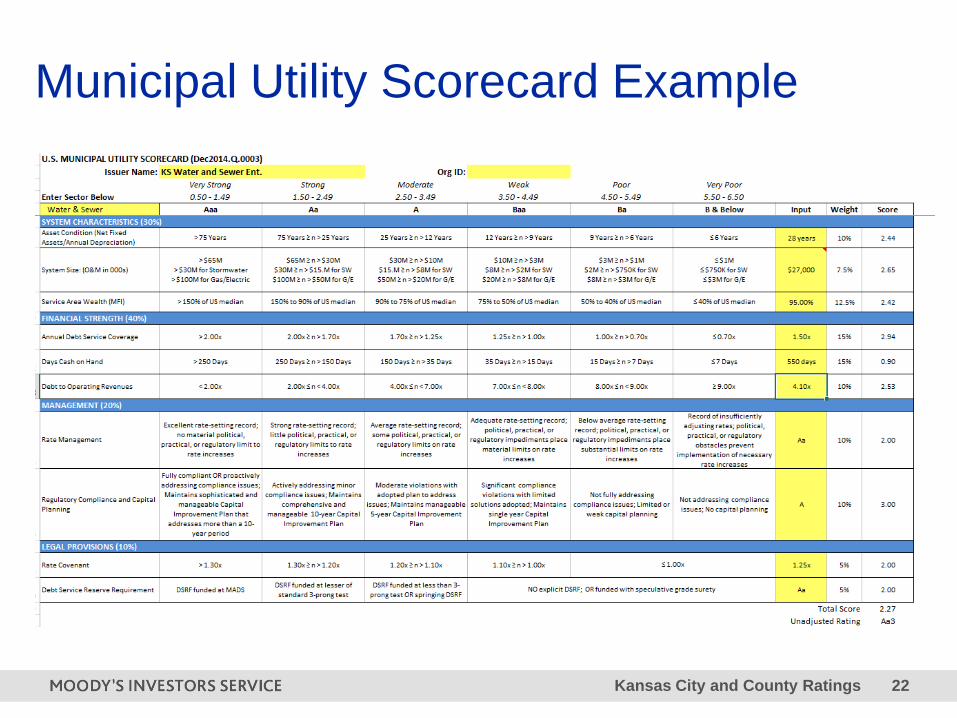

Municipal Utility Scorecard Example

Kansas City and County Ratings 23

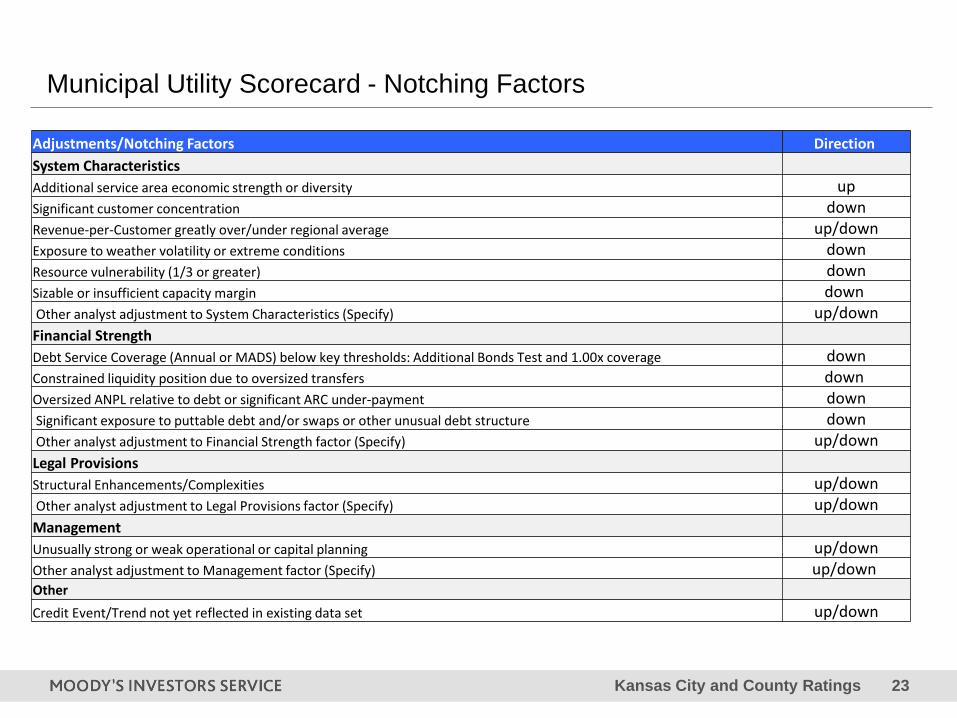

Municipal Utility Scorecard - Notching Factors

Adjustments/Notching Factors DirectionSystem CharacteristicsAdditional service area economic strength or diversity upSignificant customer concentration downRevenue-per-Customer greatly over/under regional average up/downExposure to weather volatility or extreme conditions downResource vulnerability (1/3 or greater) downSizable or insufficient capacity margin downOther analyst adjustment to System Characteristics (Specify) up/downFinancial StrengthDebt Service Coverage (Annual or MADS) below key thresholds: Additional Bonds Test and 1.00x coverage downConstrained liquidity position due to oversized transfers downOversized ANPL relative to debt or significant ARC under-payment downSignificant exposure to puttable debt and/or swaps or other unusual debt structure downOther analyst adjustment to Financial Strength factor (Specify) up/downLegal ProvisionsStructural Enhancements/Complexities up/downOther analyst adjustment to Legal Provisions factor (Specify) up/downManagementUnusually strong or weak operational or capital planning up/downOther analyst adjustment to Management factor (Specify) up/downOtherCredit Event/Trend not yet reflected in existing data set up/down

Kansas City and County Ratings 24

Relationship with GO Rating» A municipal utility’s credit quality is related to the strength of its

associated local government entity. Examples of credit linkages include:

» Economy: Coterminous or overlapping economic base and service area» Finances: Cash can often flow between the two entities » Debt: Revenues to support GO and utility paid by the same group of constituents» Management and Governance: Management teams may be the same or have

close ties» Capital Markets: GO and utility need to access the same capital markets for

funding

» Rating levels are usually similar (within 2 notches) due to these linkages

4 Kansas City and County Credit Trends

Kansas City and County Ratings 26

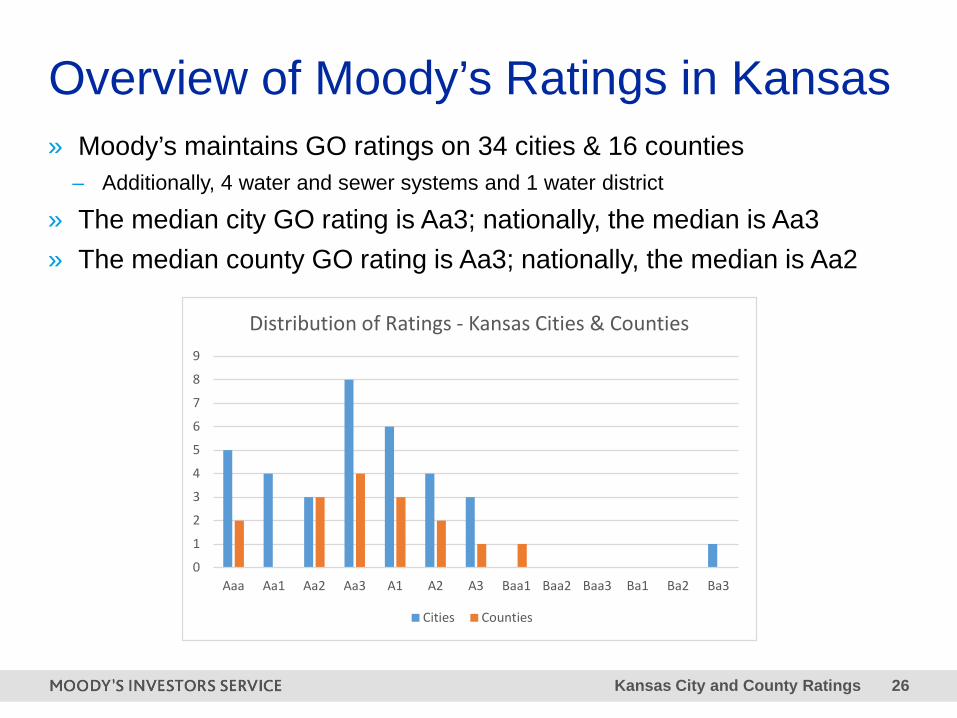

Overview of Moody’s Ratings in Kansas» Moody’s maintains GO ratings on 34 cities & 16 counties

– Additionally, 4 water and sewer systems and 1 water district

» The median city GO rating is Aa3; nationally, the median is Aa3» The median county GO rating is Aa3; nationally, the median is Aa2

0

1

2

3

4

5

6

7

8

9

Aaa Aa1 Aa2 Aa3 A1 A2 A3 Baa1 Baa2 Baa3 Ba1 Ba2 Ba3

Distribution of Ratings - Kansas Cities & Counties

Cities Counties

Kansas City and County Ratings 27

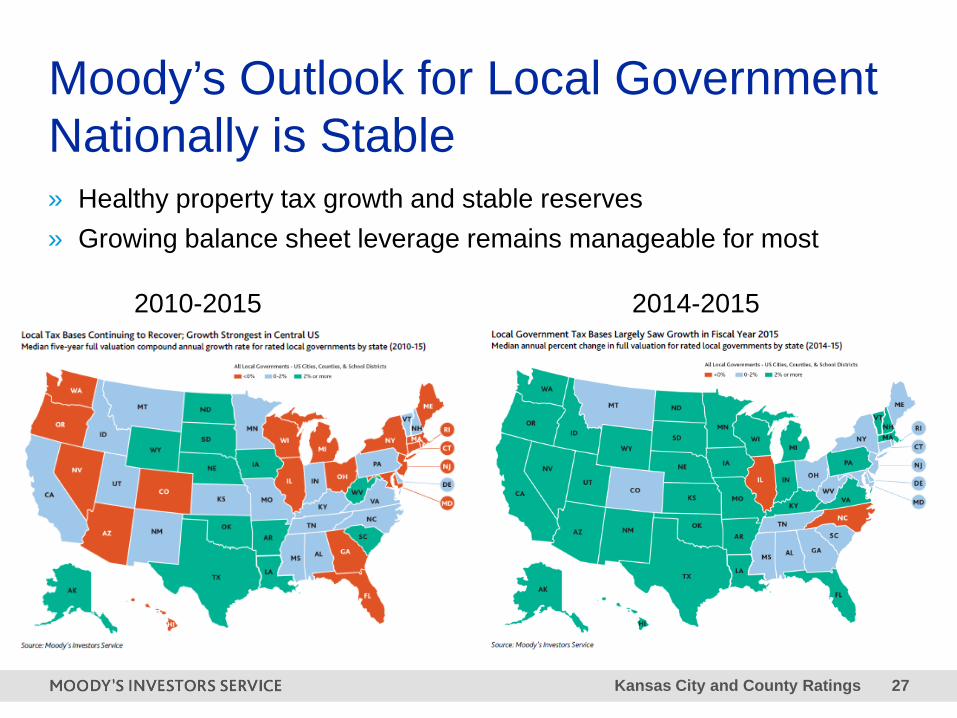

Moody’s Outlook for Local Government Nationally is Stable» Healthy property tax growth and stable reserves» Growing balance sheet leverage remains manageable for most

2010-2015 2014-2015

Kansas City and County Ratings 28

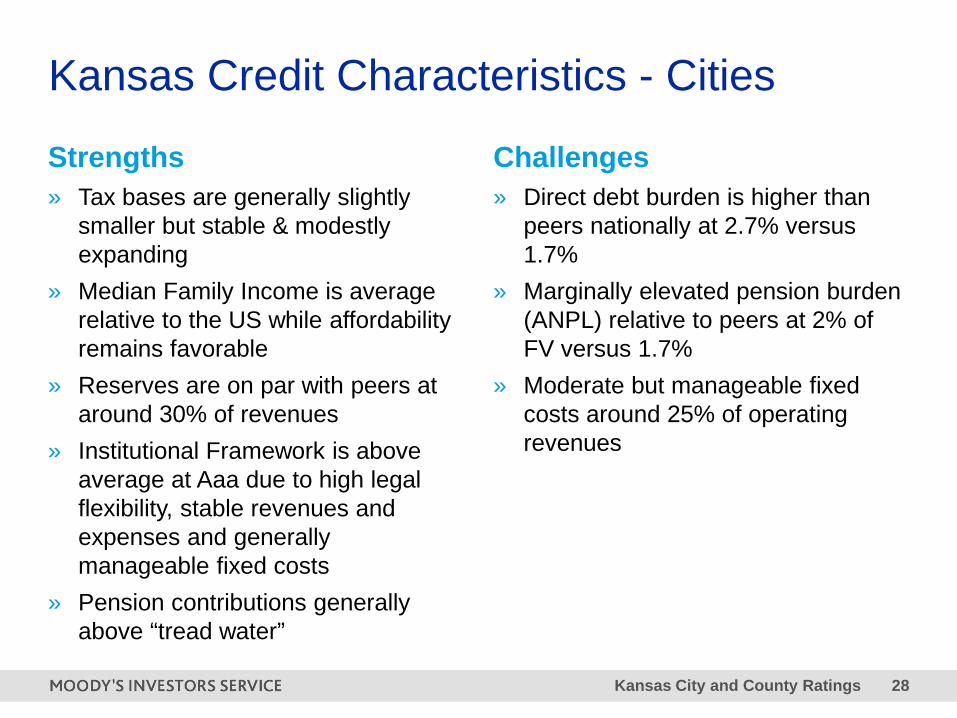

Kansas Credit Characteristics - Cities

Strengths» Tax bases are generally slightly

smaller but stable & modestly expanding

» Median Family Income is average relative to the US while affordability remains favorable

» Reserves are on par with peers at around 30% of revenues

» Institutional Framework is above average at Aaa due to high legal flexibility, stable revenues and expenses and generally manageable fixed costs

» Pension contributions generally above “tread water”

Challenges» Direct debt burden is higher than

peers nationally at 2.7% versus 1.7%

» Marginally elevated pension burden (ANPL) relative to peers at 2% of FV versus 1.7%

» Moderate but manageable fixed costs around 25% of operating revenues

Kansas City and County Ratings 29

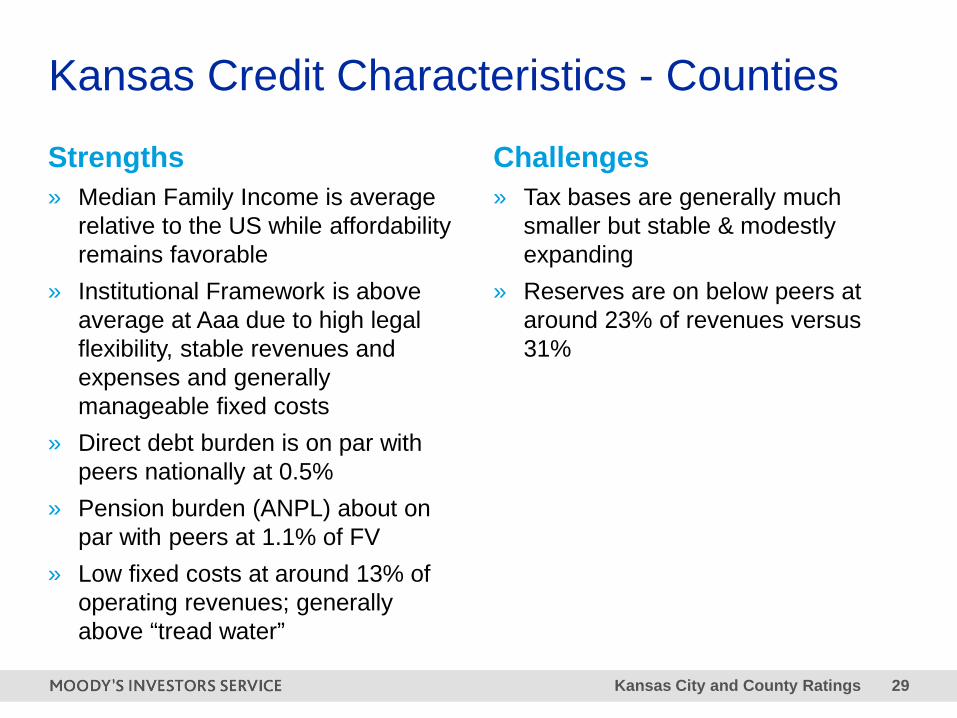

Kansas Credit Characteristics - Counties

Strengths» Median Family Income is average

relative to the US while affordability remains favorable

» Institutional Framework is above average at Aaa due to high legal flexibility, stable revenues and expenses and generally manageable fixed costs

» Direct debt burden is on par with peers nationally at 0.5%

» Pension burden (ANPL) about on par with peers at 1.1% of FV

» Low fixed costs at around 13% of operating revenues; generally above “tread water”

Challenges» Tax bases are generally much

smaller but stable & modestly expanding

» Reserves are on below peers at around 23% of revenues versus 31%

5 Publications

Kansas City and County Ratings 31

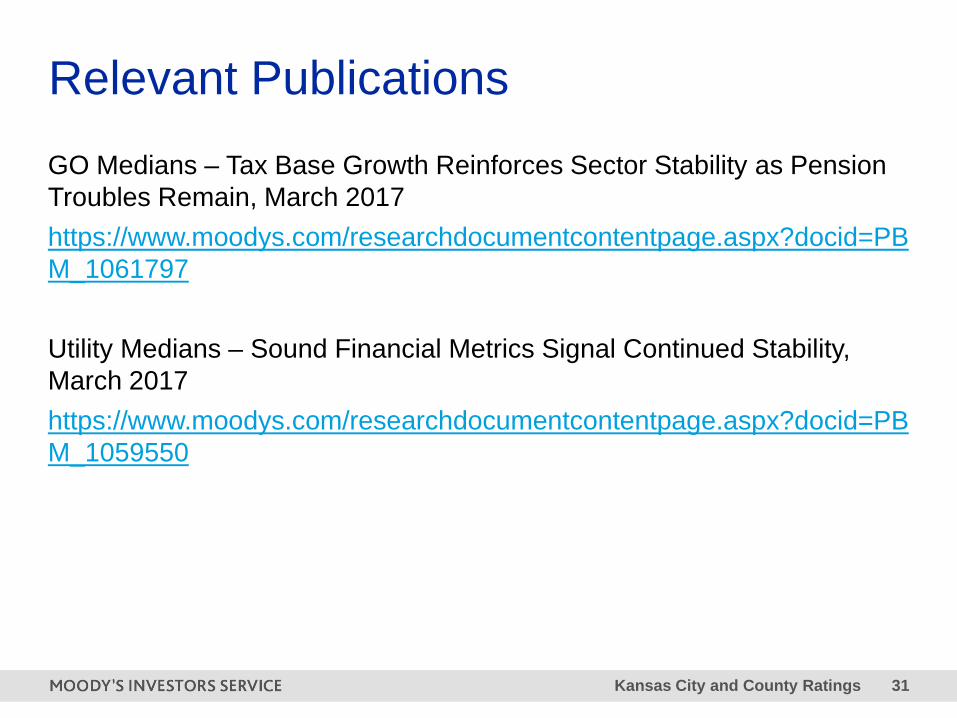

Relevant PublicationsGO Medians – Tax Base Growth Reinforces Sector Stability as Pension Troubles Remain, March 2017https://www.moodys.com/researchdocumentcontentpage.aspx?docid=PBM_1061797

Utility Medians – Sound Financial Metrics Signal Continued Stability, March 2017https://www.moodys.com/researchdocumentcontentpage.aspx?docid=PBM_1059550

Kansas City and County Ratings 33

© 2017 Moody’s Corporation, Moody’s Investors Service, Inc., Moody’s Analytics, Inc. and/or their licensors and affiliates (collectively, “MOODY’S”). All rights reserved.

CREDIT RATINGS ISSUED BY MOODY'S INVESTORS SERVICE, INC. AND ITS RATINGS AFFILIATES (“MIS”) ARE MOODY’S CURRENT OPINIONS OF THE RELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES, AND MOODY’S PUBLICATIONS MAY INCLUDE MOODY’S CURRENT OPINIONS OF THE RELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES. MOODY’S DEFINES CREDIT RISK AS THE RISK THAT AN ENTITY MAY NOT MEET ITS CONTRACTUAL, FINANCIAL OBLIGATIONS AS THEY COME DUE AND ANY ESTIMATED FINANCIAL LOSS IN THE EVENT OF DEFAULT. CREDIT RATINGS DO NOT ADDRESS ANY OTHER RISK, INCLUDING BUT NOT LIMITED TO: LIQUIDITY RISK, MARKET VALUE RISK, OR PRICE VOLATILITY. CREDIT RATINGS AND MOODY’S OPINIONS INCLUDED IN MOODY’S PUBLICATIONS ARE NOT STATEMENTS OF CURRENT OR HISTORICAL FACT. MOODY’S PUBLICATIONS MAY ALSO INCLUDE QUANTITATIVE MODEL-BASED ESTIMATES OF CREDIT RISK AND RELATED OPINIONS OR COMMENTARY PUBLISHED BY MOODY’S ANALYTICS, INC. CREDIT RATINGS AND MOODY’S PUBLICATIONS DO NOT CONSTITUTE OR PROVIDE INVESTMENT OR FINANCIAL ADVICE, AND CREDIT RATINGS AND MOODY’S PUBLICATIONS ARE NOT AND DO NOT PROVIDE RECOMMENDATIONS TO PURCHASE, SELL, OR HOLD PARTICULAR SECURITIES. NEITHER CREDIT RATINGS NOR MOODY’S PUBLICATIONS COMMENT ON THE SUITABILITY OF AN INVESTMENT FOR ANY PARTICULAR INVESTOR. MOODY’S ISSUES ITS CREDIT RATINGS AND PUBLISHES MOODY’S PUBLICATIONS WITH THE EXPECTATION AND UNDERSTANDING THAT EACH INVESTOR WILL, WITH DUE CARE, MAKE ITS OWN STUDY AND EVALUATION OF EACH SECURITY THAT IS UNDER CONSIDERATION FOR PURCHASE, HOLDING, OR SALE.

MOODY’S CREDIT RATINGS AND MOODY’S PUBLICATIONS ARE NOT INTENDED FOR USE BY RETAIL INVESTORS AND IT WOULD BE RECKLESS AND INAPPROPRIATE FOR RETAIL INVESTORS TO USE MOODY’S CREDIT RATINGS OR MOODY’S PUBLICATIONS WHEN MAKING AN INVESTMENT DECISION. IF IN DOUBT YOU SHOULD CONTACT YOUR FINANCIAL OR OTHER PROFESSIONAL ADVISER.

ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY LAW, INCLUDING BUT NOT LIMITED TO, COPYRIGHT LAW, AND NONE OF SUCH INFORMATION MAY BE COPIED OR OTHERWISE REPRODUCED, REPACKAGED, FURTHER TRANSMITTED, TRANSFERRED, DISSEMINATED, REDISTRIBUTED OR RESOLD, OR STORED FOR SUBSEQUENT USE FOR ANY SUCH PURPOSE, IN WHOLE OR IN PART, IN ANY FORM OR MANNER OR BY ANY MEANS WHATSOEVER, BY ANY PERSON WITHOUT MOODY’S PRIOR WRITTEN CONSENT.

All information contained herein is obtained by MOODY’S from sources believed by it to be accurate and reliable. Because of the possibility of human or mechanical error as well as other factors, however, all information contained herein is provided “AS IS” without warranty of any kind. MOODY'S adopts all necessary measures so that the information it uses in assigning a credit rating is of sufficient quality and from sources MOODY'S considers to be reliable including, when appropriate, independent third-party sources. However, MOODY’S is not an auditor and cannot in every instance independently verify or validate information received in the rating process or in preparing the Moody’s publications.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability to any person or entity for any indirect, special, consequential, or incidental losses or damages whatsoever arising from or in connection with the information contained herein or the use of or inability to use any such information, even if MOODY’S or any of its directors, officers, employees, agents, representatives, licensors or suppliers is advised in advance of the possibility of such losses or damages, including but not limited to: (a) any loss of present or prospective profits or (b) any loss or damage arising where the relevant financial instrument is not the subject of a particular credit rating assigned by MOODY’S.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability for any direct or compensatory losses or damages caused to any person or entity, including but not limited to by any negligence (but excluding fraud, willful misconduct or any other type of liability that, for the avoidance of doubt, by law cannot be excluded) on the part of, or any contingency within or beyond the control of, MOODY’S or any of its directors, officers, employees, agents, representatives, licensors or suppliers, arising from or in connection with the information contained herein or the use of or inability to use any such information.

NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY SUCH RATING OR OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY MOODY’S IN ANY FORM OR MANNER WHATSOEVER.

Moody’s Investors Service, Inc., a wholly-owned credit rating agency subsidiary of Moody’s Corporation (“MCO”), hereby discloses that most issuers of debt securities (including corporate and municipal bonds, debentures, notes and commercial paper) and preferred stock rated by Moody’s Investors Service, Inc. have, prior to assignment of any rating, agreed to pay to Moody’s Investors Service, Inc. for appraisal and rating services rendered by it fees ranging from $1,500 to approximately $2,500,000. MCO and MIS also maintain policies and procedures to address the independence of MIS’s ratings and rating processes. Information regarding certain affiliations that may exist between directors of MCO and rated entities, and between entities who hold ratings from MIS and have also publicly reported to the SEC an ownership interest in MCO of more than 5%, is posted annually at www.moodys.com under the heading “Investor Relations — Corporate Governance — Director and Shareholder Affiliation Policy.”

Additional terms for Australia only: Any publication into Australia of this document is pursuant to the Australian Financial Services License of MOODY’S affiliate, Moody’s Investors Service Pty Limited ABN 61 003 399 657AFSL 336969 and/or Moody’s Analytics Australia Pty Ltd ABN 94 105 136 972 AFSL 383569 (as applicable). This document is intended to be provided only to “wholesale clients” within the meaning of section 761G of the Corporations Act 2001. By continuing to access this document from within Australia, you represent to MOODY’S that you are, or are accessing the document as a representative of, a “wholesale client” and that neither you nor the entity you represent will directly or indirectly disseminate this document or its contents to “retail clients” within the meaning of section 761G of the Corporations Act 2001. MOODY’S credit rating is an opinion as to the creditworthiness of a debt obligation of the issuer, not on the equity securities of the issuer or any form of security that is available to retail investors. It would be reckless and inappropriate for retail investors to use MOODY’S credit ratings or publications when making an investment decision. If in doubt you should contact your financial or other professional adviser.

Additional terms for Japan only: Moody's Japan K.K. (“MJKK”) is a wholly-owned credit rating agency subsidiary of Moody's Group Japan G.K., which is wholly-owned by Moody’s Overseas Holdings Inc., a wholly-owned subsidiary of MCO. Moody’s SF Japan K.K. (“MSFJ”) is a wholly-owned credit rating agency subsidiary of MJKK. MSFJ is not a Nationally Recognized Statistical Rating Organization (“NRSRO”). Therefore, credit ratings assigned by MSFJ are Non-NRSRO Credit Ratings. Non-NRSRO Credit Ratings are assigned by an entity that is not a NRSRO and, consequently, the rated obligation will not qualify for certain types of treatment under U.S. laws. MJKK and MSFJ are credit rating agencies registered with the Japan Financial Services Agency and their registration numbers are FSA Commissioner (Ratings) No. 2 and 3 respectively.

MJKK or MSFJ (as applicable) hereby disclose that most issuers of debt securities (including corporate and municipal bonds, debentures, notes and commercial paper) and preferred stock rated by MJKK or MSFJ (as applicable) have, prior to assignment of any rating, agreed to pay to MJKK or MSFJ (as applicable) for appraisal and rating services rendered by it fees ranging from JPY200,000 to approximately JPY350,000,000.

MJKK and MSFJ also maintain policies and procedures to address Japanese regulatory requirements.

This publication does not announce a credit rating action. For any credit ratings referenced in this publication, please see the ratings tab on the issuer/entity page on www.moodys.com for the most updated credit rating action information and rating history.