mortgage suitability letter – error spotting exercise · lender hsbc product type fixed initial...

TRANSCRIPT

Index & Fact Find Information Mortgage Suitability Letter Sourcing List & Research Mortgage KFI

1.Summary 2.Suitabilty 3.AlternativesConsidered

4.PossibleDisadvantages 5.Affordability 6.Protection 7.Keeping in touch

Mortgage Suitability Letter – Error Spotting Exercise

Mr & Mrs Richards Remortgage Case Study – Fact Find Sourcing List & Research Mortgage Key Facts Illustration

• Jen & Angus Richards are aged 48 & 44

• They are in full time employment and earn £35,000 & £24,000

• They have a daughter, Heather who is 13

• They are coming to the end of their current 3 year fixed mortgage

• Their current mortgage is with the Newbury Building Society

• They have a preference for having stability in the amount of their monthly mortgage payment, as they want to know what their mortgage would be for a minimum of 3 years as this will tie in with when their daughter finishes school.

• There are both planning to retire when Jen reaches state retirement age, which is currently 67 for her date of birth

• The current mortgage is for £192,000 & has 17 years left to run on it. They want to have their new mortgage over a similar term to ensure its within their monthly budget of £1,110

• They are comfortable with having an arrangement fee added to their mortgage as long as it is not above £1000

Error Spotting Exercise

There are 5 case checking errors in this Mortgage Suitability Letter.

Check the CHECK BOXES to indicate where you think the error is, and use the TEXT FIELDS to explain what the error is.

sections that contain errors

sections that do not contain errors

You have correctly identified

You have incorrectly identified Intrinsic Training & Development – Version 1.0 June 2017

Index & Fact Find Information Mortgage Suitability Letter Sourcing List & Research Mortgage KFI

1.Summary 2.Suitabilty 3.AlternativesConsidered

4.PossibleDisadvantages 5.Affordability 6.Protection 7.Keeping in touch

MORTGAGE SUITABILITY REPORT

CONTENTS 1. Summary of my mortgage recommendation to you2. Why the recommendation is suitable for you3. Alternatives considered4. Possible disadvantages5. Affordability6. Confirmation of our discussions regarding protection7. Keeping in touch

Prepared for: Mrs J. Richards and Mr. A. Richards

Date prepared: 15/05/2017

Prepared by: Mr J. Davies

The aim of this report is to provide you with a summary of my recommendation and why this is suitable for you.

It is really important that you fully understand my recommended solution.

I ask that you read it carefully and come back to me with any questions you may have.

Index & Fact Find Information Mortgage Suitability Letter Sourcing List & Research Mortgage KFI

1.Summary 2.Suitabilty 3.AlternativesConsidered

4.PossibleDisadvantages 5.Affordability 6.Protection 7.Keeping in touch

1. SUMMARY OF MY MORTGAGE RECOMMENDATION TO YOUDetails of the mortgage

Loan purpose Re-mortgage

Purchase price / Valuation £230000

Loan amount £192000

Loan type Repayment

Term 17 years

Lender HSBC

Product type Fixed

Initial product term 30/09/2020

Initial product rate % 1.89%

What you will pay

Your monthly mortgage payment, based on the initial rate, is £1106.92 until 30/09/2020.

Following your initial period, the payments will increase to £1243.51, which is based on the current SVR of 3.69%.

Please refer to the Mortgage Illustration provided for further details. I have explained to you the impact that any interest rise can have on your monthly payments.

Index & Fact Find Information Mortgage Suitability Letter Sourcing List & Research Mortgage Illustration

1.Summary 2.Suitabilty 3.AlternativesConsidered

4.PossibleDisadvantages 5.Affordability 6.Protection 7.Keeping in touch

2. WHY THE RECOMMENDATION IS SUITABLE FOR YOU1. £192,000 of borrowing has been recommended because this is the outstanding amount on your

current mortgage which you are re-mortgaging. You are adding an arrangement fee to your mortgage of £999, making the total borrowing £192,999

2. A deposit of £38,000 was available, this was sourced from the existing equity in your current property and matches the current mortgage.

3. A term of 17 years has been recommended because it matches the outstanding term on your current mortgage.

4. A HSBC 3 Year Fixed Standard (Intrinsic) Remortgage has been recommended because you wanted to have stability in your monthly mortgage payments for next three years.

5. A Repayment mortgage has been recommended because you want to ensure that at the end of the 17 year mortgage term that you have repaid the loan in full.

6. When we originally spoke the following was important to you• Fixing your interest rate for a certain period• Ability to add fees to the loan

However, during our discussions I identified the following was most important to you and have based my recommendation on these preferences

• Fixing your interest rate for a certain period• Ability to add fees to the loan

7. It is the least expensive taking into account all the pricing elements identified as beingimportant. I looked at the cost of the mortgages over 3 years because the HSBC offered thelowest monthly rate of 1.89%.

Index & Fact Find Information Mortgage Suitability Letter Sourcing List & Research Mortgage KFI

1.Summary 2.Suitabilty 3.AlternativesConsidered

4.PossibleDisadvantages 5.Affordability 6.Protection 7.Keeping in touch

2. WHY THE RECOMMENDATION IS SUITABLE FOR YOU (continued)8. The HSBC mortgage is within your monthly budget of £1,110.

9. The HSBC Mortgage enables you to make overpayments up to 10% of your annual remaining balance per year.

10. The HSBC mortgage includes free legal fees

3. ALTERNATIVES CONSIDEREDI discounted two other HSBC products that were slightly cheaper at £1,105.49 per month as you were not eligible for these as you need to be either a HSBC Advance or Premier customer.

4. THE POSSIBLE DISADVANTAGESYou wanted to add any arrangement fee to the mortgage up to a maximum of £1000. An arrangement fee of £995 has been added to this loan.

There are Early Repayment Charges on this mortgage during the 3 year fixed period,

• 3% of the outstanding loan in the 1st year

• 2% of the outstanding loan in the 2nd year

• 1% of the outstanding loan in the 3rd year

Index & Fact Find Information Mortgage Suitability Letter Sourcing List & Research Mortgage KFI

1.Summary 2.Suitabilty 3.AlternativesConsidered

4.PossibleDisadvantages 5.Affordability 6.Protection 7.Keeping in touch

5. AFFORDABILITYWe have reviewed your income, expenditure and current budget for your monthly payments and evidenced that you can afford this recommendation.

At the end of the initial mortgage term we discussed the fact that your payments are likely to increase but we have agreed that given your current income and expenditure this would be affordable.

6. CONFIRMATION OF OUR DISCUSSIONS REGARDING PROTECTIONTo ensure that you and your family are able to remain in your home, it is important you protect yourself against the effects of your death, diagnosis of certain critical illnesses or being unable to work through ill health or unemployment with the appropriate protection products.

It is also important to ensure your home and its contents are protected against damage or loss.

Please see my separate recommendation on protecting your mortgage in the event of death or critical illness.

Index & Fact Find Information Mortgage Suitability Letter Sourcing List & Research Mortgage Illustration

1.Summary 2.Suitabilty 3.AlternativesConsidered

4.PossibleDisadvantages 5.Affordability 6.Protection 7.Keeping in touch

7. KEEPING IN TOUCHAs agreed, I will keep in contact with you throughout the application process.

Please inform me immediately if any detail of your application changes prior to completion. A new mortgage offer may need to be issued by the lender before any new loan can commence.

Following completion of the mortgage, it is equally important that we regularly review your situation, particularly where your circumstances change, to ensure our recommendations remain appropriate.

I look forward to speaking with you again in the future. If you wish to discuss this letter or need any additional information please do not hesitate to contact me

Yours sincerely

Mr J. Davies

Notes • A first charge over your property is required as security for the loan.• The formal mortgage offer of an advance will be subject to a valuation and other satisfactory references.• Your home may be repossessed if you do not keep up repayments on your mortgage

Product List Report

Date: 12/05/2017 Richards, Jen & Richards, Angus

Page 1 of 3

Loan Details

Loan Type Government Scheme Value Loan Amt Existing Mortgage

£192,000 £192,000

Deposit/Equity LTV Term(yrs/mths)

Residential None £230,000 £38,000 83.48 17 / 0

Purpose

Remortgage

Remortgage Reason Repayment Type

Standard Remortgage Repayment

Lender Panel Offset

Intrinsic Panel No

Only products with the following features were selected:

3

0

0

Arrange/Booking Fee Addable

£1,000.00

Total to Pay Over(yrs)

Discount Price

Buy To Let

Stepped ProductsExclusives

Term 17Yrs 0Mths

Fixed

Fee:

Maximum Arrange/Booking Fee:

Total to Pay Options:

Property Features:

Tenancy:

Quote Filters:

Rate Types:

Init Term: 3 Years

Index & Fact Find Information Mortgage Suitability Letter Sourcing List & Research Mortgage KFI

1.Summary 2.Suitabilty 3.AlternativesConsidered

4.PossibleDisadvantages 5.Affordability 6.Protection 7.Keeping in touch

Lender Type Init Rate Init Period Init Payment Revert Rate APR Fees Total to Pay

Fixed 1.94% 30/06/2020 £1,111.38 3.74% 3.24% £995.00 £40,010

Fixed 1.94% 01/09/2020 £1,111.38 4.29% 3.63% £995.00 £40,010

Fixed 1.89% 30/09/2020 £1,105.49 3.69% 3.14% £976.00 £40,025

Fixed 1.89% 30/09/2020 £1,105.49 3.69% 3.14% £976.00 £40,025

Fixed 1.95% 30/06/2020 £1,112.29 4.24% 3.62% £1,007.00 £40,050

Fixed 1.89% 30/09/2020 £1,106.92 3.69% 3.15% £1,226.00 £40,076

Fixed 1.88% 31/07/2020 £1,106.01 5.34% 4.27% £1,347.50 £40,169

Fixed 1.99% 31/07/2020 £1,115.88 4.49% 3.73% £999.00 £40,172

Fixed 1.93% 31/07/2020 £1,107.60 4.24% 3.54% £835.00 £40,214

Fixed 1.99% 30/06/2020 £1,115.88 5.44% 4.39% £1,154.00 £40,327

Fixed 2.1% 30/06/2020 £1,119.97 4.74% 3.9% £25.00 £40,344

Fixed 2.08% 31/07/2020 £1,123.96 5.34% 4.32% £1,112.50 £40,580

Fixed 2.14% 31/07/2020 £1,126.46 4.24% 3.6% £525.00 £40,583

Fixed 2.19% 30/09/2020 £1,128.07 3.69% 3.18% £0.00 £40,611

Fixed 2.24% 30/06/2020 £1,132.59 5.44% 4.41% £35.00 £40,808

Fixed 2.29% 30/06/2020 £1,143.04 4.24% 3.74% £1,007.00 £41,157

Fixed 2.39% 31/07/2020 £1,146.21 4.49% 3.81% £0.00 £41,264

TSB4Intermediaries

Virgin Money plc

HSBC

HSBC

Coventry Building Society/Godiva

HSBC

Accord Mortgages

Platform

BOI4Intermediaries

Leeds Building Society

Principality Building Society

Accord Mortgages

BOI4Intermediaries

HSBC

Leeds Building Society

Coventry Building Society/Godiva

Platform

West Brom Fixed 2.39% 30/06/2020 £1,146.21 3.99% 3.5% £0.00 £41,264

Fixed 2.44% 30/06/2020 £1,150.78 3.74% 3.34% £0.00 £41,428

Fixed 2.39% 3 years £1,152.18 3.75% 3.4% £1,034.00 £41,513

Fixed 2.29% 3 years £1,143.04 3.75% 3.39% £1,469.00 £41,619

Fixed 2.39% 30/09/2020 £1,150.68 3.69% 3.33% £976.00 £41,651

Fixed 2.39% 30/09/2020 £1,150.68 3.69% 3.33% £976.00 £41,651

Fixed 2.39% 30/09/2020 £1,152.18 3.69% 3.34% £1,226.00 £41,705

TSB4Intermediaries

Metro Bank

Metro Bank

HSBC

HSBC

HSBC

Accord Mortgages Fixed 2.37% 31/07/2020 £1,150.32 5.34% 4.45% £1,347.50 £41,764

Page 2 of 3

Index & Fact Find Information Mortgage Suitability Letter Sourcing List & Research Mortgage KFI

1.Summary 2.Suitabilty 3.AlternativesConsidered

4.PossibleDisadvantages 5.Affordability 6.Protection 7.Keeping in touch

Fixed 2.74% 01/09/2020 £1,178.39 4.29% 3.86% £0.00 £42,422

Fixed 2.79% 31/07/2020 £1,183.03 4.24% 3.8% £30.00 £42,619

Fixed 2.84% 31/07/2020 £1,187.68 4.49% 3.97% £0.00 £42,756

Fixed 2.85% 01/07/2020 £1,188.61 5.49% 4.63% £30.00 £42,820

Fixed 2.98% 3 years £1,207.01 5.29% 4.64% £1,044.00 £43,497

Fixed 3.69% 30/06/2020 £1,268.44 5.44% 4.93% £155.00 £45,819

Fixed 3.69% 30/06/2020 £1,268.44 5.44% 4.93% £155.00 £45,819

Fixed 3.89% 30/06/2020 £1,287.90 5.7% 5.18% £25.00 £46,389

Fixed 3.89% 30/06/2020 £1,287.90 5.7% 5.18% £25.00 £46,389

Fixed 4.04% 3 years £1,302.61 5.3% 4.97% £18.00 £46,912

Fixed 4.04% 3 years £1,302.61 5.3% 4.97% £18.00 £46,912

Virgin Money plc

BOI4Intermediaries

Platform

Nottingham

Furness Building Society

Leeds Building Society

Leeds Building Society

Marsden Building Society

Marsden Building Society

Kensington Mortgage Company Limited

Kensington Mortgage Company Limited

Buckinghamshire Building Society

Fixed 3.89% 31/08/2020 £1,293.60 4.99% 4.77% £1,230.00 £46,950

Fixed 2.54% 3 years £1,159.94 3.75% 3.39% £35.00 £41,793

Fixed 2.49% 3 years £1,161.36 3.75% 3.44% £1,034.00 £41,844

Metro Bank

Metro Bank

Metro Bank Fixed 2.39% 3 years £1,152.18 3.75% 3.42% £1,469.00 £41,948

Fixed 2.55% 31/10/2020 £1,166.89 3.74% 3.41% £1,034.00 £42,043

Fixed 2.55% 31/10/2020 £1,166.89 3.74% 3.41% £1,034.00 £42,043

Fixed 2.64% 30/06/2020 £1,169.14 3.99% 3.58% £0.00 £42,089

Fixed 2.58% 01/09/2020 £1,169.64 4.29% 3.87% £995.00 £42,107

Fixed 2.64% 3 years £1,169.14 3.75% 3.42% £35.00 £42,124

Fixed 2.59% 31/07/2020 £1,170.59 4.49% 3.95% £999.00 £42,141

Fixed 2.69% 30/09/2020 £1,173.76 3.69% 3.37% £0.00 £42,255

Fixed 2.69% 01/09/2020 £1,173.76 4.29% 3.84% £0.00 £42,255

Fixed 2.69% 31/07/2020 £1,173.76 5.7% 4.71% £25.00 £42,280

Barclays

Barclays

West Brom

Virgin Money plc

Metro Bank

Platform

HSBC

Virgin Money plc

Marsden Building Society

Marsden Building Society Fixed 2.69% 31/07/2020 £1,173.76 5.7% 4.71% £25.00 £42,280

Lender Type Init Rate Init Period Init Payment Revert Rate APR Fees Total to Pay

Page 3 of 3

Index & Fact Find Information Mortgage Suitability Letter Sourcing List & Research Mortgage KFI

1.Summary 2.Suitabilty 3.AlternativesConsidered

4.PossibleDisadvantages 5.Affordability 6.Protection 7.Keeping in touch

about this mortgage

Personalised illustration for: Jen Richards & Angus RichardsDate produced: 12th May 2017 13:48Valid until: This illustration is valid only on the date produced.This is not a legally binding mortgage offer and does not oblige HSBC Bank plc to provide you withthe mortgage described in this illustration.

1. About this illustration• We are required by the Financial Conduct Authority (FCA) - the independent watchdog

that regulates, financial services - to provide you with this illustration.

• All firms selling mortgages are required to give you illustrations like this one, thatcontain similar information presented in the same way.

• Ensure that you obtain other illustrations if you want to compare this mortgage withmortgages from other lenders.

2. Which service are we providing you with?J. Davies recommends, having assessed your needs, that you take out this mortgage.

J. Davies is not recommending a particular mortgage for you. However, based on youranswers to some questions, we are giving you information about this mortgage so that youcan make your own choice.

3. What you have told usThis illustration is based on a mortgage loan for a remortgage.

• Loan Amount £192,000.00 , plus £999.00 for fees that will be added to theloan. These and the additional fees that you will need to payare shown in Section 8. For details of any insurancecharges, see Section 9.

• Repayment Method Repayment• Term of Mortgage 17 years• Value £230,000.00

This means you will be borrowing 83.91% of the property's value.Changes to any of the information you have given us and any valuation report that may be carriedout on your property, could alter the details in this illustration. If this is the case please ask for arevised illustration.

Reference: 1000400244 Page 1 of 8 Prepared By Training 249

Index & Fact Find Information

Mortgage Suitability Letter

Sourcing List & Research Mortgage KFI

1.Summary 2.Suitabilty 3.AlternativesConsidered

4.PossibleDisadvantages 5.Affordability 6.Protection 7.Keeping in

touch

4. Description of this mortgageThis illustration is provided on HSBC Bank plc's 4049134 3 Year Fixed Standard (Intrinsic) RMGmortgage.The mortgage is summarised below:Loan Amount Initial

RatePayable

Product Description Repayment Method Term ofLoan

£192,999.00 1.89% A fixed rate of 1.89% that will applyfrom completion until 30

September 2020.

Repayment 17 Years

4049134 3 Year Fixed Standard (Intrinsic) RMGStep 1 of your mortgage is described in the table above.

Step 2 of your mortgage product starts after 30 September 2020, and the rate that will apply isHSBC Bank plc's Standard Variable Rate, currently 3.69% for the remaining term of the mortgage.Any changes to the variable rate as a result of a Bank of England base rate change will take effectthe day after that change.Restrictions on this mortgageNo restrictions applyOther informationThe terms of this mortgage reflect past or present financial difficulties.

5. Overall cost of this mortgageThe overall cost takes into account the payments in Sections 6 and 8 below.With a repayment mortgage you gradually pay off the amount you have borrowed, as well as theinterest, over the life of the mortgage.The total amount you must pay back, including the amountborrowed is

£249,075.00

This means you pay back £1.29 for every £1 borrowedThe APRC applicable to your loan isAn explanation of the APRC (Annual Percentage Rate of Charge) isdetailed in Section 13.

3.19% APRC

The figures in this section will vary following interest rate changes and if you do not keep themortgage for 17 years.Only use the figures in this section to compare the cost with another repayment mortgage.

6. What you will need to pay each month Monthlypayments

These payments are based on a Repayment Only mortgage of £192,999.00 andinclude the fees that are shown in Section 8 as being added to your mortgage andassumes that the mortgage will start on 1st July 2017.

The actual number of any concessionary payments payable is dependent on thedrawdown date of the mortgage. Where the mortgage draws down one month or morefrom today's date the number of concessionary payments will reduce accordingly.

39 payments at a fixed rate of 1.89% £1,106.92

Followed by165 payments at a variable rate, currently 3.69% £1,243.51

Reference: 1000400244 Page 2 of 8 Prepared By Training 249

Index & Fact Find Information

Mortgage Suitability Letter

Sourcing List & Research Mortgage KFI

1.Summary 2.Suitabilty 3.AlternativesConsidered

4.PossibleDisadvantages 5.Affordability 6.Protection 7.Keeping in

touch

7. Are you comfortable with the risks?What if interest rates go up?The monthly payments shown in this illustration could be considerably different if interest rateschange. For example, after the Fixed rate ends after 30th September 2020, for one percentage pointincrease in the Standard Variable Rate, your monthly payment will increase by around £80.06.

RATES MAY INCREASE BY MUCH MORE THAN THIS SO MAKE SURE YOU CAN AFFORDTHE MONTHLY PAYMENT.

What if your income goes down?You will still have to pay your mortgage if you lose your job or if illness prevents you from working.Think about whether you could do this.

MAKE SURE YOU CAN AFFORD YOUR MORTGAGE IF YOUR INCOME FALLS.

The Money Advice Service information sheet 'You can afford your mortgage now, but what if...?' willhelp you consider the risks. You can get a free copy from http://www.moneyadviceservice.org.uk, orby calling 0300 500 5000.

Reference: 1000400244 Page 3 of 8 Prepared By Training 249

Index & Fact Find Information

Mortgage Suitability Letter

Sourcing List & Research Mortgage KFI

1.Summary 2.Suitabilty 3.AlternativesConsidered

4.PossibleDisadvantages 5.Affordability 6.Protection 7.Keeping in

touch

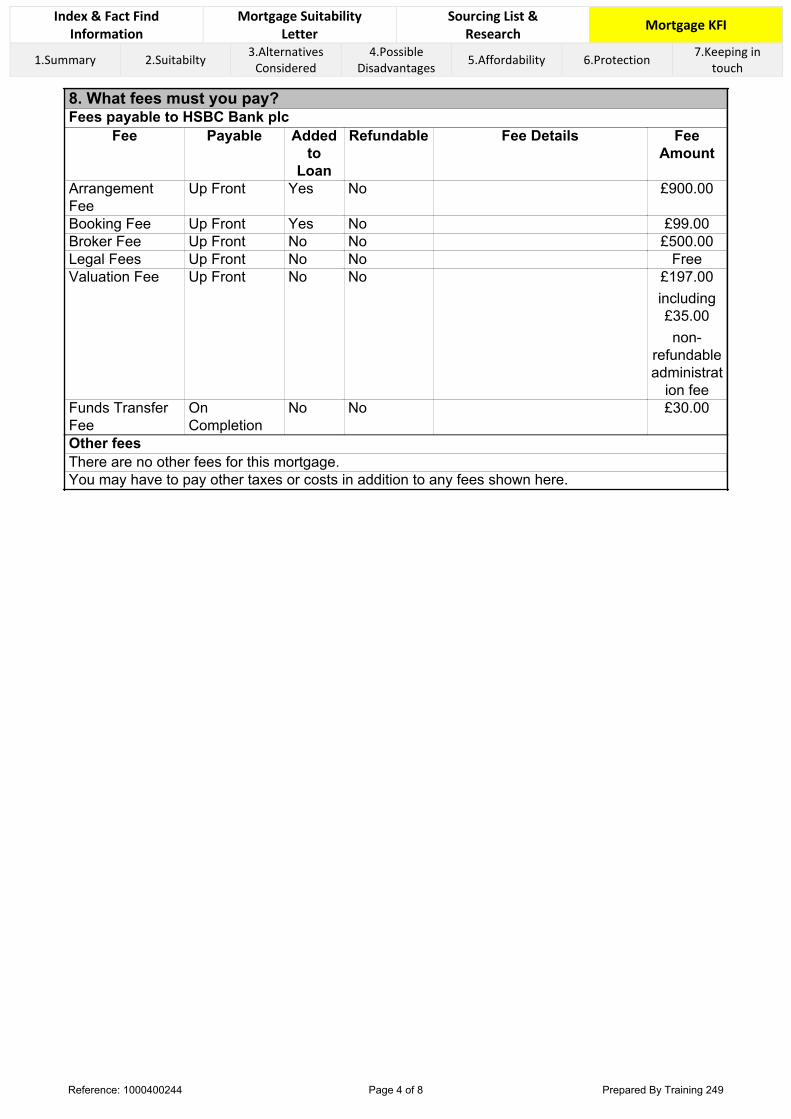

8. What fees must you pay?Fees payable to HSBC Bank plc

Fee Payable Addedto

Loan

Refundable Fee Details FeeAmount

ArrangementFee

Up Front Yes No £900.00

Booking Fee Up Front Yes No £99.00Broker Fee Up Front No No £500.00Legal Fees Up Front No No FreeValuation Fee Up Front No No £197.00

including£35.00non-

refundableadministrat

ion feeFunds TransferFee

OnCompletion

No No £30.00

Other feesThere are no other fees for this mortgage.You may have to pay other taxes or costs in addition to any fees shown here.

Reference: 1000400244 Page 4 of 8 Prepared By Training 249

Index & Fact Find Information

Mortgage Suitability Letter

Sourcing List & Research Mortgage KFI

1.Summary 2.Suitabilty 3.AlternativesConsidered

4.PossibleDisadvantages 5.Affordability 6.Protection 7.Keeping in

touch

9. Insurance Monthly PaymentInsurance you must take out through HSBC Bank plc or J. DaviesYou are not required to buy any insurance through HSBC Bank plc or J.DaviesInsurance you must take out as a condition of this mortgage but that youdo not have to take out through HSBC Bank plc or J. DaviesBuildings Insurance

Reference: 1000400244 Page 5 of 8 Prepared By Training 249

Index & Fact Find Information

Mortgage Suitability Letter

Sourcing List & Research Mortgage KFI

1.Summary 2.Suitabilty 3.AlternativesConsidered

4.PossibleDisadvantages 5.Affordability 6.Protection 7.Keeping in

touch

10. What happens if you do not want this mortgage any more?Early repayment chargesThe figures assume a start date for the mortgage of 1st July 2017.Early repayment charges are payable on this mortgage until 30th September 2020 as follows.

Early Repayment Charges on your mortgage Cash Examples(amount you would repay if the loan is

redeemed during the date rangesbelow)

Loan Amount Start ofchargeperiod

Basis of charge 01/07/2017to

30/09/2018

01/10/2018to

30/09/2019

01/10/2019to

30/09/2020£192,999.00 01/07/2017 3% of outstanding loan £5,789.97

01/10/2018 2% of outstanding loan £3,859.9801/10/2019 1% of outstanding loan £1,929.99

Total £5,789.97 £3,859.98 £1,929.99Should you repay your mortgage, the maximum charge you could pay is £5,789.97.

NotesThe charge is 1% of the amount repaid early for each remaining year of the fixed rate period,reducing on a daily basis. The maximum charge will vary depending on the completion date of yourmortgage. Please refer to lenders KFI on www.hsbc.co.uk on completion for the maximum figure.What happens if you move house?If you move house and buy another house during the fixed rate period we may agree to lend you upto the same amount as the balance of your existing loan at the same fixed rate for the remainder ofthe fixed rate period, provided that you meet the conditions stated in the Offer Document that we willprovide to you if you proceed with this Mortgage. If we agree to lend you more than the balance ofyour existing Mortgage, we'll offer to do so at the rates we have available at that time.For full details of the conditions that apply, please consult the product literature.

11. What happens if you want to make overpayments?During the fixed rate period, up to 10% of your annual remaining mortgage balance can be overpaidwithout an early repayment charge. Additional payments can be made over the internet, over thecounter or on the phone. Any amount above that would incur an early repayment charge described inSection 10. Once the fixed rate period ends, early repayment charges do not apply. Following receiptof any capital repayment or overpayment, we will immediately recalculate the amount that you oweand the amount of interest that you pay. This means that you will get the benefit straight away.

12. Additional featuresIncentivesFree Legals

Reference: 1000400244 Page 6 of 8 Prepared By Training 249

Index & Fact Find Information

Mortgage Suitability Letter

Sourcing List & Research Mortgage KFI

1.Summary 2.Suitabilty 3.AlternativesConsidered

4.PossibleDisadvantages 5.Affordability 6.Protection 7.Keeping in

touch

13. Interest rate and other costsThe APRC is the total cost of the mortgage expressed as an annual percentage. The APRC isprovided to help you to compare different illustrations.

Because your mortgage is a variable interest rate mortgage, the actual APRC could bedifferent from this APRC if the interest rate for your mortgage changes. For example,if the interest rate rose to 10.94% the APRC could increase to 11.67% and yourmortgage payments could increase to £2,087.25.Please make sure that you are aware of all other taxes and costs associated with your mortgage.

14. Other rights of the borrowerYou have 7 days after being given a binding mortgage offer to reflect before committing yourself totaking out this loan.

15. Using a mortgage intermediaryHSBC Bank plc will pay Intrinsic Financial Services an amount of £768.00 in cash or in benefits if youtake out this mortgage.

16. Where can you get more information about mortgages?The Money Advice Service publishes useful guides on choosing a mortgage. These are availablefree through its website: www.moneyadviceservice.org, or by calling 0300 500 5000. The websitealso provides Comparative Tables to help you shop around.

Contact detailsIf you wish to discuss this mortgage illustration please contact:Training 249J. Davies9 Poplar RoadOr Phone 01276 583423

YOUR HOME MAY BE REPOSSESSED IF YOU DO NOT KEEP UP REPAYMENTS ON YOURMORTGAGE

Reference: 1000400244 Page 7 of 8 Prepared By Training 249

Index & Fact Find Information

Mortgage Suitability Letter

Sourcing List & Research Mortgage KFI

1.Summary 2.Suitabilty 3.AlternativesConsidered

4.PossibleDisadvantages 5.Affordability 6.Protection 7.Keeping in

touch

Summary of mortgage paymentsMonth / Year Interest

rate %Type of

ratePayment

£Total sum

paid todate £

Totalinterestchargedto date £

Total debtrepaid to

date £

Remainingdebt £

Jul 1.89 Fixed 1106.92 1106.92 303.97 802.95 192196.05Aug 1.89 Fixed 1106.92 2213.84 606.68 1607.16 191391.84Sep 1.89 Fixed 1106.92 3320.76 908.12 2412.64 190586.36Oct 1.89 Fixed 1106.92 4427.68 1208.29 3219.39 189779.61Nov 1.89 Fixed 1106.92 5534.60 1507.19 4027.41 188971.59Dec 1.89 Fixed 1106.92 6641.52 1804.82 4836.70 188162.30Jan 1.89 Fixed 1106.92 7748.44 2101.18 5647.26 187351.74Feb 1.89 Fixed 1106.92 8855.36 2396.26 6459.10 186539.90Mar 1.89 Fixed 1106.92 9962.28 2690.06 7272.22 185726.78Apr 1.89 Fixed 1106.92 11069.20 2982.58 8086.62 184912.38May 1.89 Fixed 1106.92 12176.12 3273.82 8902.30 184096.70Jun 1.89 Fixed 1106.92 13283.04 3563.77 9719.27 183279.731 1.89 Fixed 13283.04 13283.04 3563.77 9719.27 183279.732 1.89 Fixed 13283.04 26566.08 6942.26 19623.82 173375.183 1.89 Fixed 13283.04 39849.12 10131.92 29717.20 163281.804 (Jul - Sep) 1.89 Fixed 3320.76 43169.88 10899.41 32270.47 160728.534 (Oct - Jun) 3.69 Variable 11191.59 54361.47 15264.04 39097.43 153901.575 3.69 Variable 14922.12 69283.59 20785.07 48498.52 144500.486 3.69 Variable 14922.12 84205.71 25953.28 58252.43 134746.577 3.69 Variable 14922.12 99127.83 30755.41 68372.42 124626.588 3.69 Variable 14922.12 114049.95 35177.74 78872.21 114126.799 3.69 Variable 14922.12 128972.07 39205.99 89766.08 103232.9210 3.69 Variable 14922.12 143894.19 42825.39 101068.80 91930.2011 3.69 Variable 14922.12 158816.31 46020.60 112795.71 80203.2912 3.69 Variable 14922.12 173738.43 48775.69 124962.74 68036.2613 3.69 Variable 14922.12 188660.55 51074.13 137586.42 55412.5814 3.69 Variable 14922.12 203582.67 52898.79 150683.88 42315.1215 3.69 Variable 14922.12 218504.79 54231.92 164272.87 28726.1316 3.69 Variable 14922.12 233426.91 55055.06 178371.85 14627.1517 3.69 Variable 14921.15 248348.06 55349.06 192999.00 0.00

THE TOTAL AMOUNT THAT MUST BE PAID COULD BE CONSIDERABLY DIFFERENT FROMTHAT SHOWN, DUE TO VARIABLE INTEREST RATES.

Reference: 1000400244 Page 8 of 8 Prepared By Training 249

Index & Fact Find Information

Mortgage Suitability Letter

Sourcing List & Research Mortgage KFI

1.Summary 2.Suitabilty 3.AlternativesConsidered

4.PossibleDisadvantages 5.Affordability 6.Protection 7.Keeping in

touch