mp dec2012

Post on 19-Oct-2014

403 views

DESCRIPTION

TRANSCRIPT

Monthly Perspectives

For important disclosures, refer to the Disclosure Section, located at the end of this report.

n

Decembe

r201

2

In Europe, the Eurogroup and the IMF finallyagreed on a deal to allow the release of the nexttranche of Greece’s second bail‐out programme.The deal sends a signal as to the willingness of corecountries to support the periphery. Moreover, TheGreece package has raised the issue of whetherconcessions may also be made for other countrieswith a bailout programme, such as Portugal andIreland.

President Obama has won re‐election, with a statusquo outcome in Congress. Congress has alreadybegun work toward a compromise to avoid the taxincreases and spending cuts scheduled to take effectat the start of 2013. In the US and in China, the dataremains relatively resilient, while in Europe datasuggest that the region is stuck in a recession.

The Portuguese parliament approved the 2013budget. Despite some austerity fatigue, thePortuguese government seems determined to carry

on with the reforms.

The US fiscal negotiations will probably continueto drive the market in December. The news flowis supportive of a compromise before year‐end,although the progress in the negotiations has sofar been limited.

This month, political decisions should be again atthe top of agenda. In the Eurozone, anotherEurogroup meeting starts today, followed by anEU finance ministers meeting tomorrow. In theUS, news on the fiscal front will be decisive formarkets. Markets appear to believe that much ofthe fiscal cliff will be avoided before year‐end. InJapan, elections will be held on December 16th.

In December, we will have an ECB rate‐settingmeeting in Europe, and a two‐day FOMC policymeeting in the US.

November’s Highlights

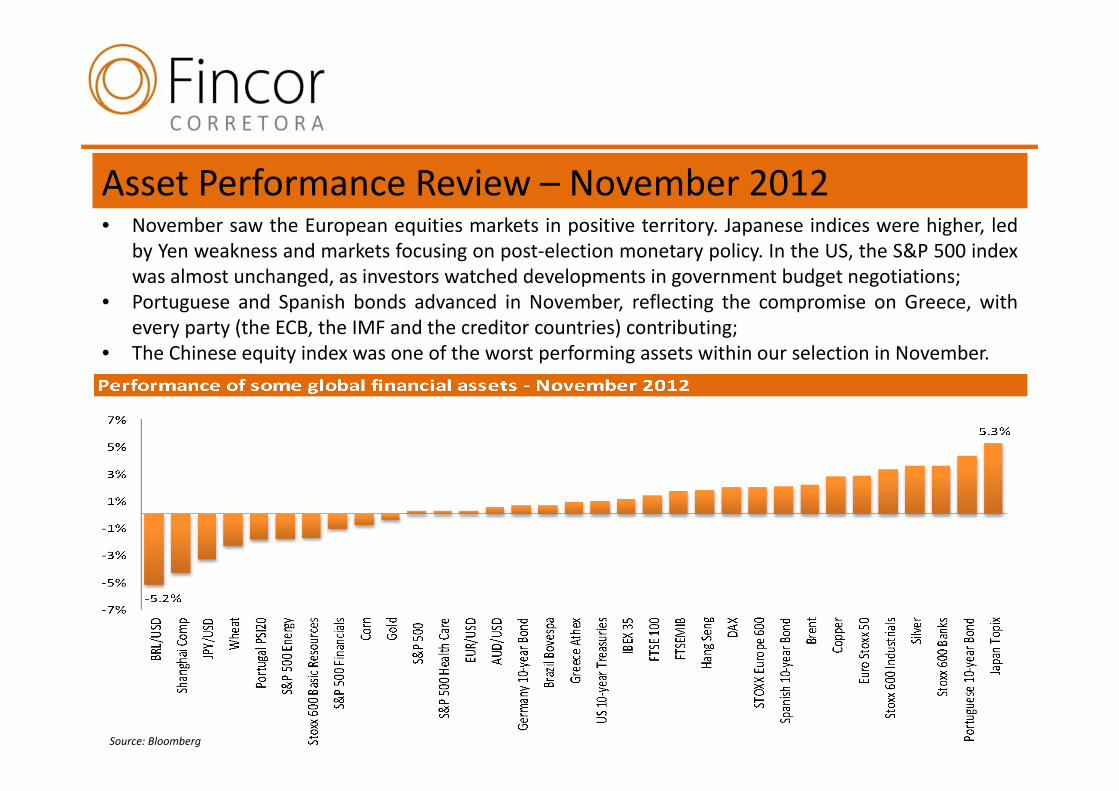

Asset Performance Review – November 2012• November saw the European equities markets in positive territory. Japanese indices were higher, led

by Yen weakness and markets focusing on post‐election monetary policy. In the US, the S&P 500 indexwas almost unchanged, as investors watched developments in government budget negotiations;

• Portuguese and Spanish bonds advanced in November, reflecting the compromise on Greece, withevery party (the ECB, the IMF and the creditor countries) contributing;

• The Chinese equity index was one of the worst performing assets within our selection in November.

Source: Bloomberg

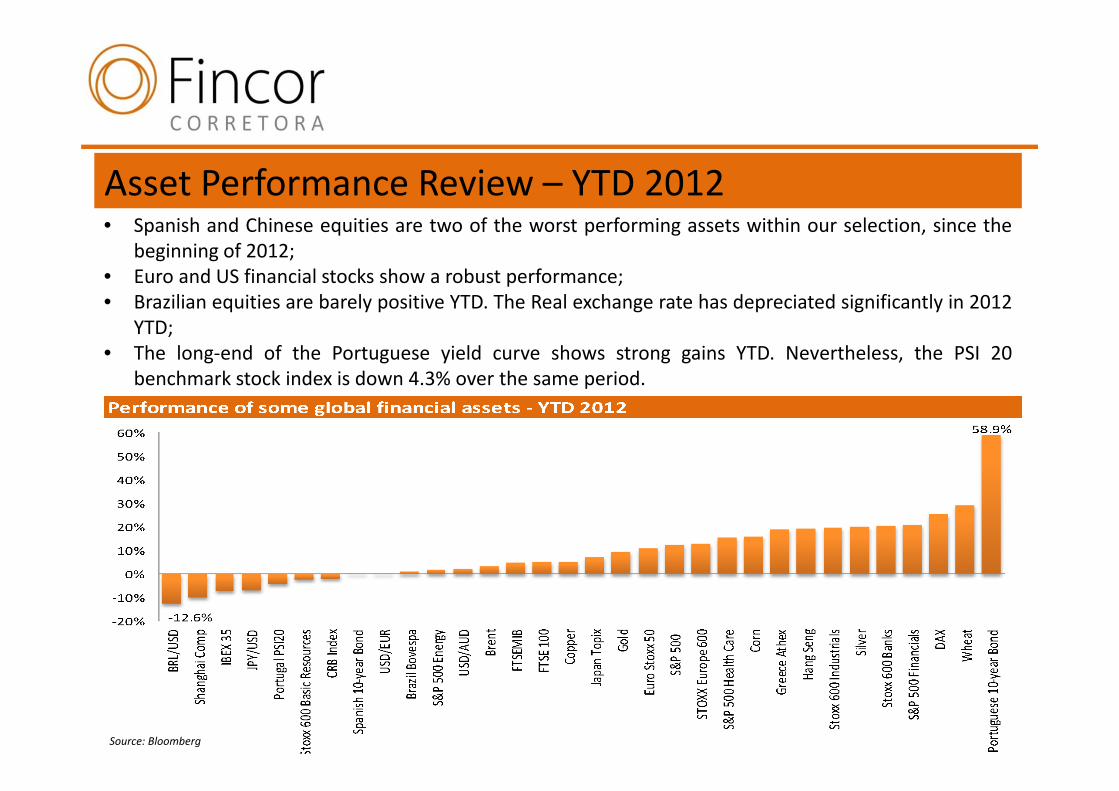

Asset Performance Review – YTD 2012• Spanish and Chinese equities are two of the worst performing assets within our selection, since the

beginning of 2012;• Euro and US financial stocks show a robust performance;• Brazilian equities are barely positive YTD. The Real exchange rate has depreciated significantly in 2012

YTD;• The long‐end of the Portuguese yield curve shows strong gains YTD. Nevertheless, the PSI 20

benchmark stock index is down 4.3% over the same period.

Source: Bloomberg

‐15%

‐10%

‐5%

0%

5%

10%

15%

Aug‐11 Oct‐11 Dec‐11 Feb‐12 Apr‐12 Jun‐12 Aug‐12 Oct‐12

Portugal Deposits Flows(from households and non‐financial corporations, y/y)

‐15% ‐10% ‐5% 0% 5% 10% 15%

Staff costs

Purchase of goods ans services

Current transfers

Interest payments

Portuguese Expenditure (Jan to Oct 2012, y/y)

85

90

95

100

105

110

2008 2009 2010 2011 2012

Portugal Average Value of Housing Bank Appraisals

Sep 08= 100

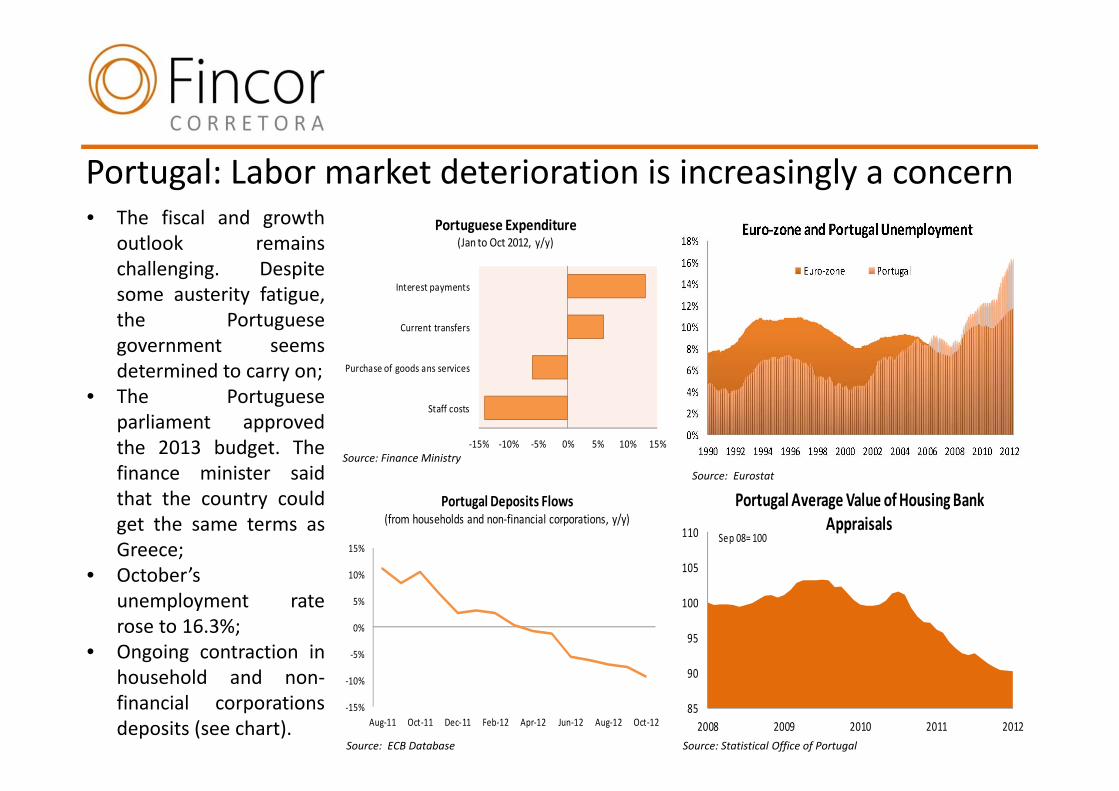

Portugal: Labor market deterioration is increasingly a concern• The fiscal and growth

outlook remainschallenging. Despitesome austerity fatigue,the Portuguesegovernment seemsdetermined to carry on;

• The Portugueseparliament approvedthe 2013 budget. Thefinance minister saidthat the country couldget the same terms asGreece;

• October’sunemployment raterose to 16.3%;

• Ongoing contraction inhousehold and non‐financial corporationsdeposits (see chart).

Source: Finance MinistrySource: Eurostat

Source: ECB Database Source: Statistical Office of Portugal

‐14%

‐12%

‐10%

‐8%

‐6%

‐4%

‐2%

0%

2%

4%

Aug‐11 Oct‐11 Dec‐11 Feb‐12 Apr‐12 Jun‐12 Aug‐12 Oct‐12

Spain Deposits Flows(from households and non‐financial corporations, y/y)

0.717

0.0

1.0

2.0

3.0

4.0

Jul‐11 Sep‐11 Nov‐11 Jan‐12 Mar‐12 May‐12 Jul‐12 Sep‐12 Nov‐12

Bankia Share Price (€)

0%

2%

4%

6%

8%

10%

12%

5%

10%

15%

20%

25%

30%

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

Unemployment vs. Non‐Performing Loans

Unemployment Rate (LHS)

NPL Ratio (RHS)

4%

5%

6%

7%

8%

Oct‐11 Jan‐12 Apr‐12 Jul‐12 Oct‐12

Spain 10‐year Government Bonds Yield

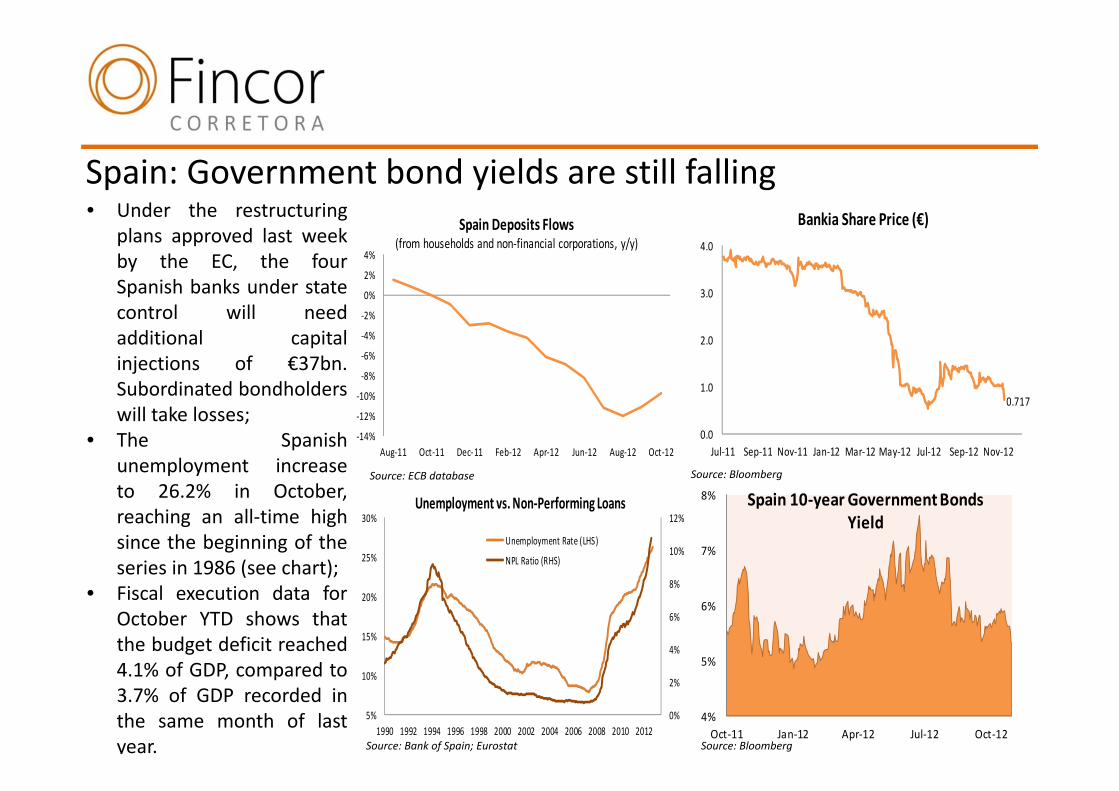

Spain: Government bond yields are still falling • Under the restructuring

plans approved last weekby the EC, the fourSpanish banks under statecontrol will needadditional capitalinjections of €37bn.Subordinated bondholderswill take losses;

• The Spanishunemployment increaseto 26.2% in October,reaching an all‐time highsince the beginning of theseries in 1986 (see chart);

• Fiscal execution data forOctober YTD shows thatthe budget deficit reached4.1% of GDP, compared to3.7% of GDP recorded inthe same month of lastyear.

Source: ECB database Source: Bloomberg

Source: Bank of Spain; Eurostat Source: Bloomberg

60%

80%

100%

120%

140%

160%

180%

200%

60%

80%

100%

120%

140%

160%

180%

200%

03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18 19 20

Greek Public Debt (% of GDP)

MoU forecast (Mar 2012)

New Targets (Nov 2012)

‐12%

‐8%

‐4%

0%

4%

8%

12%

65

80

95

110

125

2001 2003 2005 2007 2009 2011 2013

Greek GDP and Economic Sentiment

EC Economic SentimentIndicator (LHS)

GDP (% y/y, RHS)

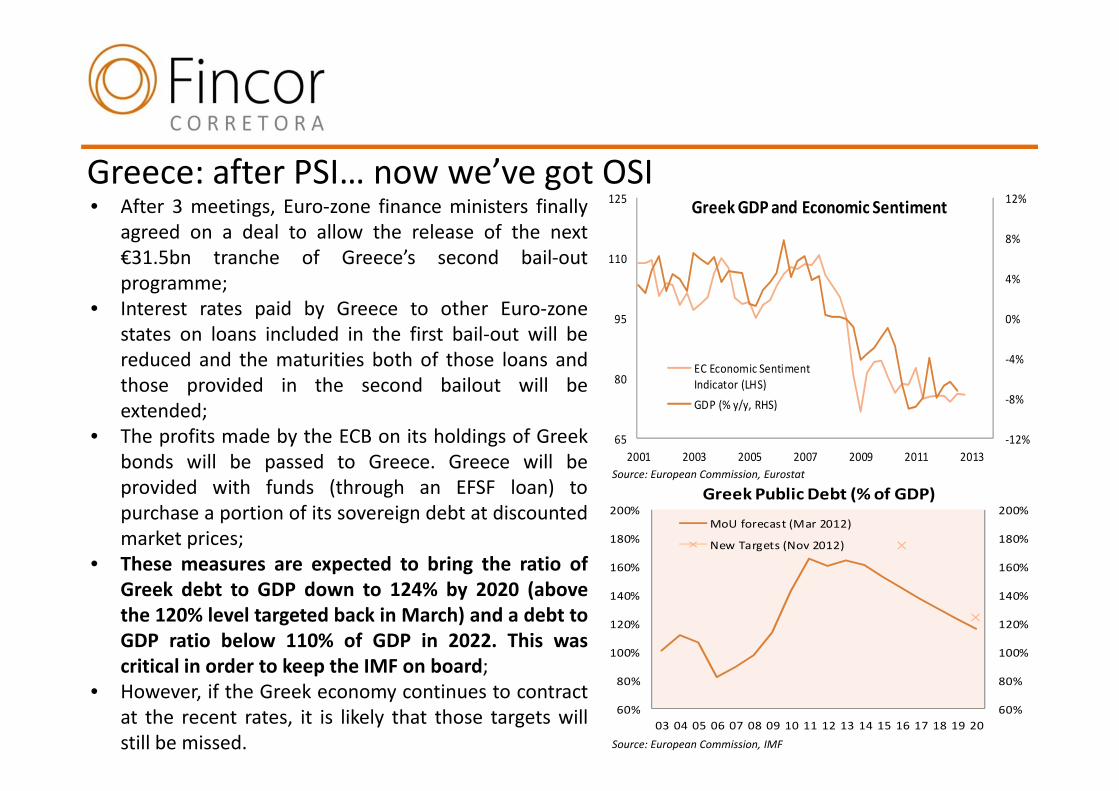

Greece: after PSI… now we’ve got OSI• After 3 meetings, Euro‐zone finance ministers finally

agreed on a deal to allow the release of the next€31.5bn tranche of Greece’s second bail‐outprogramme;

• Interest rates paid by Greece to other Euro‐zonestates on loans included in the first bail‐out will bereduced and the maturities both of those loans andthose provided in the second bailout will beextended;

• The profits made by the ECB on its holdings of Greekbonds will be passed to Greece. Greece will beprovided with funds (through an EFSF loan) topurchase a portion of its sovereign debt at discountedmarket prices;

• These measures are expected to bring the ratio ofGreek debt to GDP down to 124% by 2020 (abovethe 120% level targeted back in March) and a debt toGDP ratio below 110% of GDP in 2022. This wascritical in order to keep the IMF on board;

• However, if the Greek economy continues to contractat the recent rates, it is likely that those targets willstill be missed.

Source: European Commission, Eurostat

Source: European Commission, IMF

‐8%

‐6%

‐4%

‐2%

0%

2%

4%

6%

8%

10%

‐8%

‐6%

‐4%

‐2%

0%

2%

4%

6%

8%

10%

2000 2002 2004 2006 2008 2010 2012

GDP (y/y)

Switzerland

Euro‐zone

Sweden

‐6%

‐4%

‐2%

0%

2%

4%

6%

65

75

85

95

105

115

125

1995 1997 1999 2001 2003 2005 2007 2009 2011 2013

Euro‐zone Economic Sentiment Indicator and GDP Growth

Euro‐zone GDP (y/y)Euro‐sone Economic Sentiment Indicator

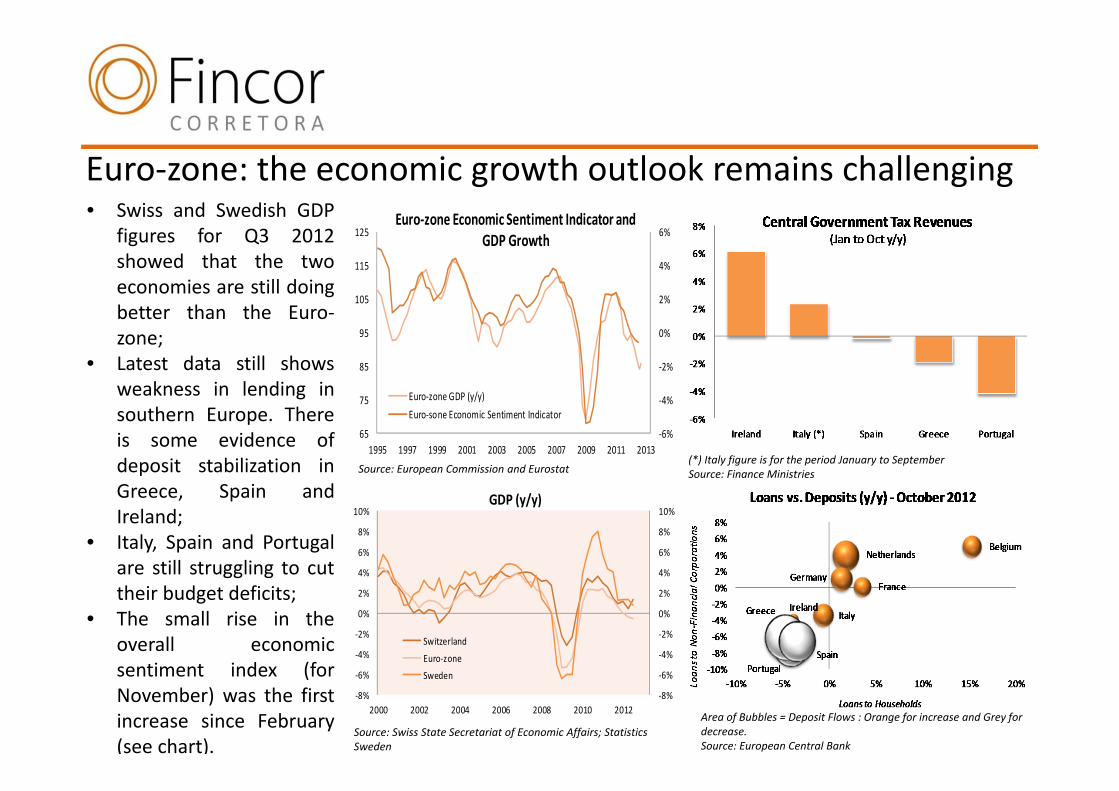

Euro‐zone: the economic growth outlook remains challenging• Swiss and Swedish GDP

figures for Q3 2012showed that the twoeconomies are still doingbetter than the Euro‐zone;

• Latest data still showsweakness in lending insouthern Europe. Thereis some evidence ofdeposit stabilization inGreece, Spain andIreland;

• Italy, Spain and Portugalare still struggling to cuttheir budget deficits;

• The small rise in theoverall economicsentiment index (forNovember) was the firstincrease since February(see chart).

Source: European Commission and Eurostat(*) Italy figure is for the period January to September Source: Finance Ministries

Source: Swiss State Secretariat of Economic Affairs; Statistics Sweden

Area of Bubbles = Deposit Flows : Orange for increase and Grey for decrease.Source: European Central Bank

‐35%

‐25%

‐15%

‐5%

5%

15%

25%

‐25%

‐20%

‐15%

‐10%

‐5%

0%

5%

10%

15%

2006 2008 2010 2012

Non‐Defence Capital Goods (Ex. Air.) (y/y)

Shipments

Orders

0

50

100

150

200

250

300

350

0

50

100

150

200

250

300

350

Oct‐10 Feb‐11 Jun‐11 Oct‐11 Feb‐12 Jun‐12 Oct‐12

Change in Private Payroll Employment (000s)

Change in Private Payroll EmploymentThree Month Average

‐4%

‐2%

0%

2%

4%

6%

8%

‐0.4%

‐0.2%

0.0%

0.2%

0.4%

0.6%

0.8%

Jan‐11 May‐11 Sep‐11 Jan‐12 May‐12 Sep‐12

Real Personal Disposable Incomem/m (LHS)3m/3m Ann. (RHS)

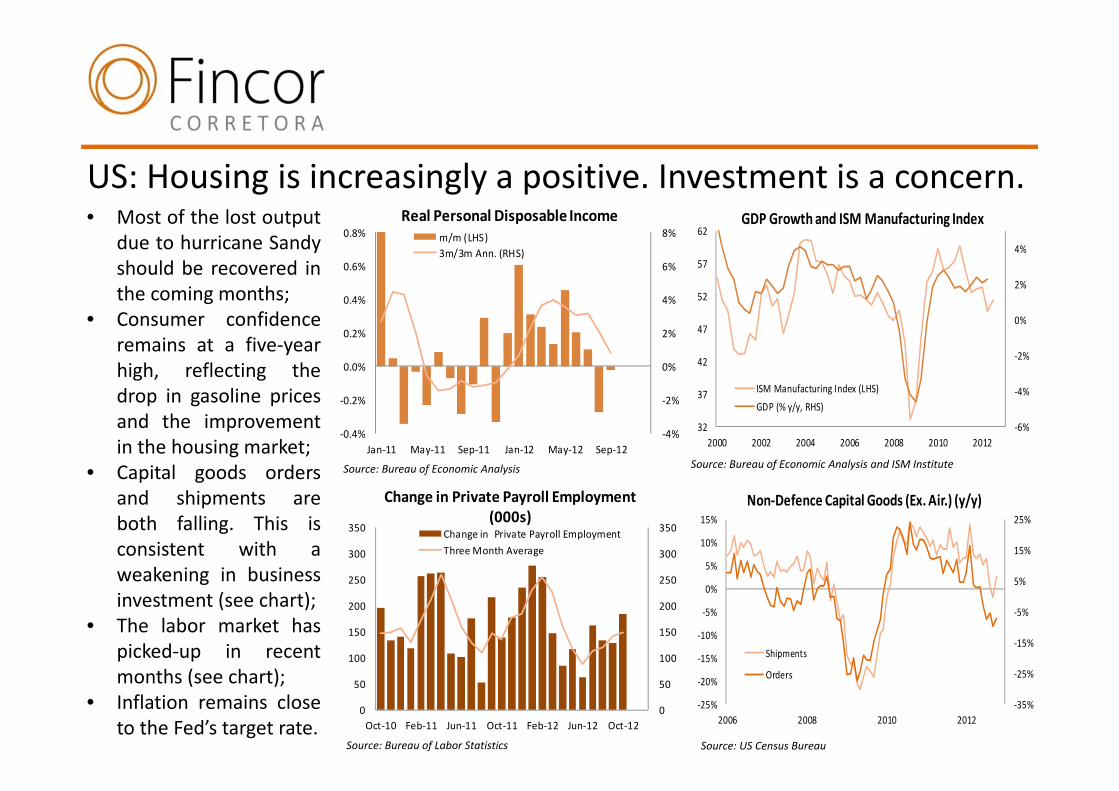

US: Housing is increasingly a positive. Investment is a concern. • Most of the lost output

due to hurricane Sandyshould be recovered inthe coming months;

• Consumer confidenceremains at a five‐yearhigh, reflecting thedrop in gasoline pricesand the improvementin the housing market;

• Capital goods ordersand shipments areboth falling. This isconsistent with aweakening in businessinvestment (see chart);

• The labor market haspicked‐up in recentmonths (see chart);

• Inflation remains closeto the Fed’s target rate.

Source: Bureau of Economic Analysis Source: Bureau of Economic Analysis and ISM Institute

Source: Bureau of Labor Statistics Source: US Census Bureau

‐6%

‐4%

‐2%

0%

2%

4%

32

37

42

47

52

57

62

2000 2002 2004 2006 2008 2010 2012

GDP Growth and ISM Manufacturing Index

ISM Manufacturing Index (LHS)

GDP (% y/y, RHS)

LHS)

11.6%

2.4%

‐40%

‐20%

0%

20%

40%

60%

80%

100%

‐30%

‐10%

10%

30%

50%

2007 2008 2009 2010 2011 2012 2013

China Exports and Imports

Exports (y/y, RHS) Imports (y/y, LHS)

50.6

‐4%

‐2%

0%

2%

4%

6%

8%

10%

35

40

45

50

55

60

65

2005 2007 2009 2011 2013

China NBS Manufacturing Index and CPI

NBS Manufacturing PMI (LHS) CPI (y/y, RHS)

uction (y/y, LHS)

5%

6%

7%

8%

9%

10%

11%

12%

13%

0%

5%

10%

15%

20%

25%

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

China GDP and Industrial Production

Industrial Production(y/y, LHS)

GDP Growth (y/y, RHS)

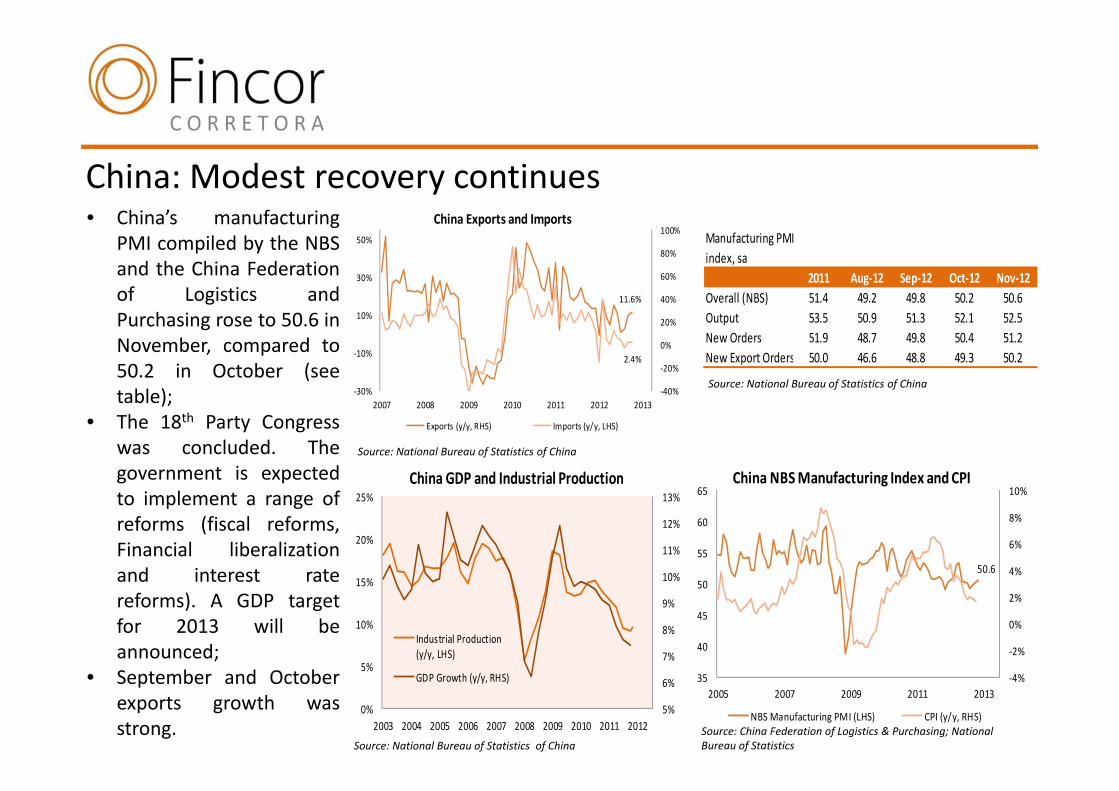

China: Modest recovery continues• China’s manufacturing

PMI compiled by the NBSand the China Federationof Logistics andPurchasing rose to 50.6 inNovember, compared to50.2 in October (seetable);

• The 18th Party Congresswas concluded. Thegovernment is expectedto implement a range ofreforms (fiscal reforms,Financial liberalizationand interest ratereforms). A GDP targetfor 2013 will beannounced;

• September and Octoberexports growth wasstrong.

Source: National Bureau of Statistics of China

Source: China Federation of Logistics & Purchasing; NationalBureau of StatisticsSource: National Bureau of Statistics of China

Manufacturing PMIindex, sa

2011 Aug‐12 Sep‐12 Oct‐12 Nov‐12Overall (NBS) 51.4 49.2 49.8 50.2 50.6Output 53.5 50.9 51.3 52.1 52.5New Orders 51.9 48.7 49.8 50.4 51.2New Export Orders 50.0 46.6 48.8 49.3 50.2

Source: National Bureau of Statistics of China

7.7%

6.3%

2.5%

2.3%

‐1.9%

‐6.1%

‐7.2%

‐8.0%

‐14.0%

‐20% ‐15% ‐10% ‐5% 0% 5% 10%

Zon

Jerónimo Martins

EDP Renováveis

BES

PSI 20

BPI

EDP

Portugal Telecom

Sonae Indústria

PSI 20 Selected Members Ranked Returns

70

80

90

100

110

120

130

Jan‐12 Mar‐12 May‐12 Jul‐12 Sep‐12 Nov‐12

Galp Share Price vs. PSI 20 Index

PSI20

GALP

Jan 12 = 100

• ENI (ENI IM) raised €1.4bn from the sale of shares andconvertible bonds in Galp Energia (GALP PL). Followingthe sale of 5% to Amorim Energia at €14.25, ENI had28.34% of Galp. Now, after the two operations andconsidering that Amorim Energia holds pre‐emptiverights over 10.34% of Galp, ENI still holds at least 5% ofthe company. Drilling is undergoing in Jupiter and resultsare expected to be announced before year‐end. Its E&Pportfolio and earnings growth profile still makes GALPone of most interesting stories in the Portuguese Market;

• Jerónimo Martins (JMT PL) rose 6.3% in November. Theretail company provided some visibility on the number ofstores to be opened in 2013 in Colombia (30‐40).Jerónimo Martins will held its Investor’s day onDecember 11th, a long awaited event in which investorsare willing to get news from Poland and furtherinformation on the company’s venture in Colombia;

• Energias de Portugal (EDP PL) fell 7.2% in November. Thestock has underperformed the European Utilities sectorthis year. Regulatory receivables have taken EDP’sleverage up and become a concern for investors.

PSI20 monthly review

Source: Bloomberg

Source: Bloomberg

The fiscal cliff remains the biggest uncertainty in the US• Another Eurogroup meeting starts today

and an EU finance ministers meeting isscheduled for tomorrow. They willprobably continue to work on the finalshape of the Greek agreement. TheCypriot rescue programme will probablyalso be discussed;

• At this month’s ECB meeting (December6th), new staff projections on growthand inflation will be published, including2014 forecasts for the first time. Nopolicy action is expected;

• In the US, the FOMC will end 2012 witha two‐day policy meeting on December11th‐12th. With Operation Twistexpected to finish by the end of 2012,investors will look for forward guidanceand more clarity on further assetpurchases;

• Fiscal cliff discussions are expected tointensify in December.

What we are watching in December:Date Region Event

1‐Dec‐12 China PMI Manufacturing3/4 ‐Dec‐12 Europe Eurogroup and EcoFin meetings3‐Dec‐12 UK PMI Manufacturing3‐Dec‐12 US ISM Manufacturing

5/7 ‐Dec‐12 Germany Merkel attends CDU Annual Party Crongress5‐Dec‐12 Europe PMI Manufacturing5‐Dec‐12 US ISM Non‐Manufacturing6‐Dec‐12 Europe ECB Governing concil policy meeting and press conference6‐Dec‐12 UK BoE Meeting7‐Dec‐12 Europe 7th review of Irish aid programme7‐Dec‐12 US Unemployment rate7‐Dec‐12 US Nonfarm Payrolls7‐Dec‐12 US University of Michigan Confidence9‐Dec‐12 China Industrial Production

11/15 ‐Dec‐12 China Money Supply (New Loans)11‐Dec‐12 Europe Zew Survey12‐Dec‐12 US FOMC Meeting

13/14 ‐Dec‐12 Europe EU Leaders hold Summit in Brussels13/14 ‐Dec‐12 Europe IMF and EC hold joint conference on Fiscal Governance13‐Dec‐12 Switzerland SCB holds monetary policy assessment13‐Dec‐12 US Advance Retail Sales14‐Dec‐12 US Industrial Production18‐Dec‐12 US NAHB Housing Market Index19‐Dec‐12 Germany IFO Survey19‐Dec‐12 US Housing Starts20‐Dec‐12 Japan BOJ Target Rate

21/24 ‐Dec‐12 Europe PMI Manufacturing24‐Dec‐12 US S&P/Case Shiller Home Price Index1‐Jan‐13 Ireland EU Council Presidency

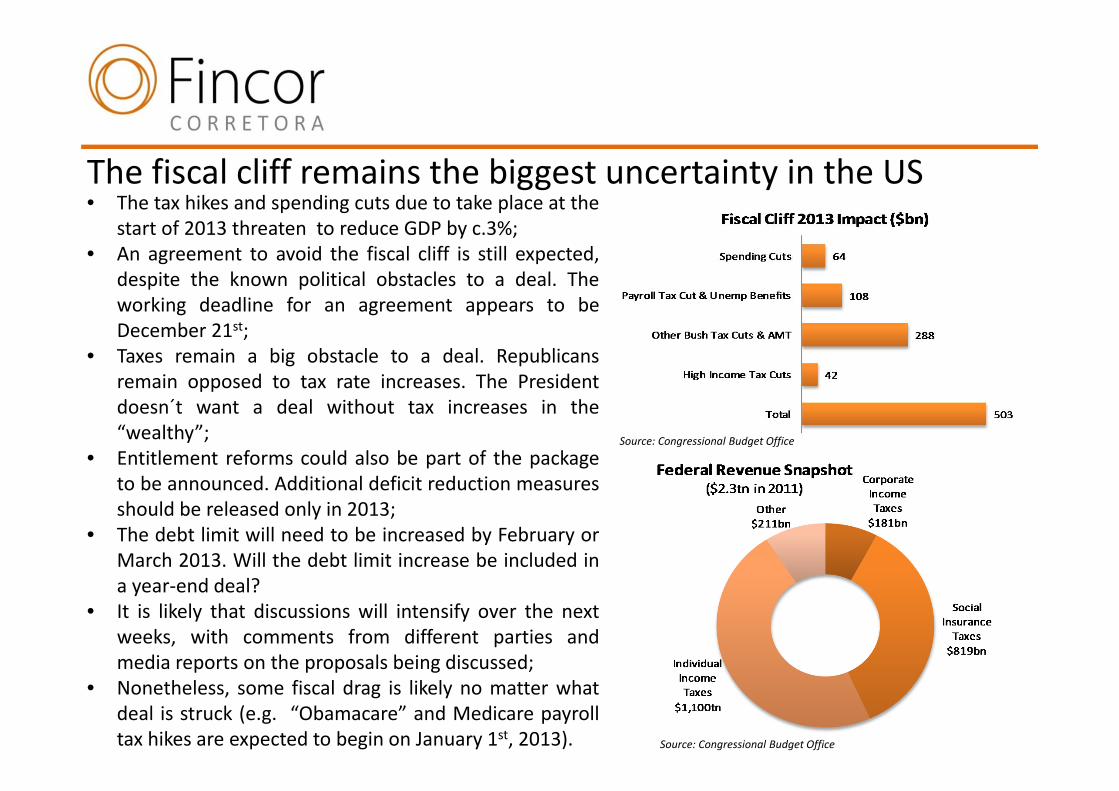

The fiscal cliff remains the biggest uncertainty in the US• The tax hikes and spending cuts due to take place at the

start of 2013 threaten to reduce GDP by c.3%;• An agreement to avoid the fiscal cliff is still expected,

despite the known political obstacles to a deal. Theworking deadline for an agreement appears to beDecember 21st;

• Taxes remain a big obstacle to a deal. Republicansremain opposed to tax rate increases. The Presidentdoesn´t want a deal without tax increases in the“wealthy”;

• Entitlement reforms could also be part of the packageto be announced. Additional deficit reduction measuresshould be released only in 2013;

• The debt limit will need to be increased by February orMarch 2013. Will the debt limit increase be included ina year‐end deal?

• It is likely that discussions will intensify over the nextweeks, with comments from different parties andmedia reports on the proposals being discussed;

• Nonetheless, some fiscal drag is likely no matter whatdeal is struck (e.g. “Obamacare” and Medicare payrolltax hikes are expected to begin on January 1st, 2013).

Source: Congressional Budget Office

Source: Congressional Budget Office

4%

5%

6%

7%

8%

4%

5%

6%

7%

8%

Jan‐11 Apr‐11 Jul‐11 Oct‐11 Jan‐12 Apr‐12 Jul‐12 Oct‐12

Italian and Spanish 10‐year Bond Yields

ItalySpain

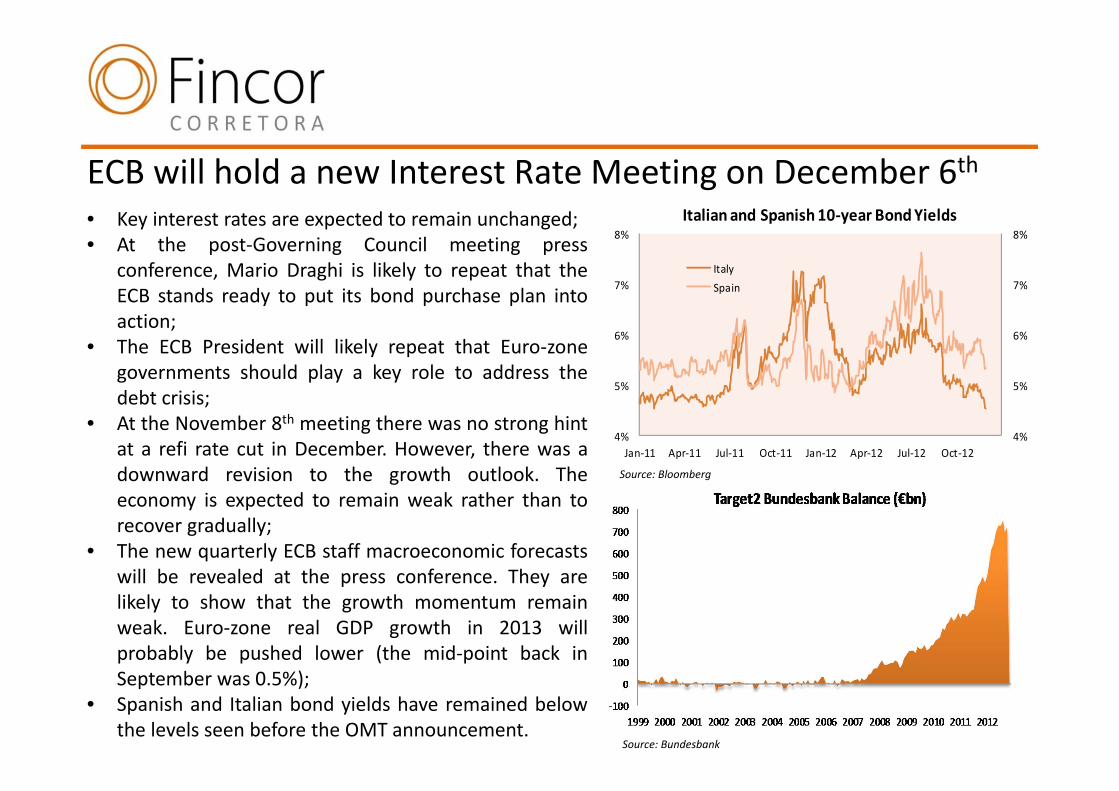

ECB will hold a new Interest Rate Meeting on December 6th• Key interest rates are expected to remain unchanged;• At the post‐Governing Council meeting press

conference, Mario Draghi is likely to repeat that theECB stands ready to put its bond purchase plan intoaction;

• The ECB President will likely repeat that Euro‐zonegovernments should play a key role to address thedebt crisis;

• At the November 8th meeting there was no strong hintat a refi rate cut in December. However, there was adownward revision to the growth outlook. Theeconomy is expected to remain weak rather than torecover gradually;

• The new quarterly ECB staff macroeconomic forecastswill be revealed at the press conference. They arelikely to show that the growth momentum remainweak. Euro‐zone real GDP growth in 2013 willprobably be pushed lower (the mid‐point back inSeptember was 0.5%);

• Spanish and Italian bond yields have remained belowthe levels seen before the OMT announcement.

Source: Bloomberg

Source: Bundesbank

2%

4%

6%

8%

10%

63%

64%

65%

66%

67%

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012Oct

US Employment Rate and Participation Rate

Unemployment Rate (RHS) Participation Rate in the Labour Force (LHS)

0

500

1,000

1,500

2,000

2,500

3,000

2007 2008 2009 2010 2011 2012

Total Reserve Assets ($bn)

FOMC will hold a policy meeting on December 11th and 12th• FED Chairman, Ben Bernanke, at his recent

speech in the New York Economic Club,underlined the disappointing growth of the USeconomy. Although the job market has recentlylooked healthier, the unemployment rate remainsat a high level;

• The minutes of the October FOMC meetingsuggested that the committee is likely to shift theforward guidance from the current mid‐2015formulation to a threshold rule (in terms of theunemployment rate and inflation). Will it happenat the December meeting?

• Operation Twist will finish by the end of 2012.Additional asset purchases when the twist comesto an end remain probable. According to theminutes of the October FOMC meeting: "anumber of participants indicated that additionalasset purchases would likely be appropriate nextyear after the conclusion of the maturityextension program“. An announcement at theDecember meeting is possible.

Source: US Federal Reserve

Source: Bureau of labor and Statistics

70

80

90

100

110

120

130

0.0%

0.1%

0.2%

0.3%

0.4%

0.5%

0.6%

2007 2008 2009 2010 2011 2012

BoJ Target Rate andJPY/USD Exchange Rate (JPY per USD)

BoJ Target Rate (LHS)JPY/USD Exchange Rate (RHS)

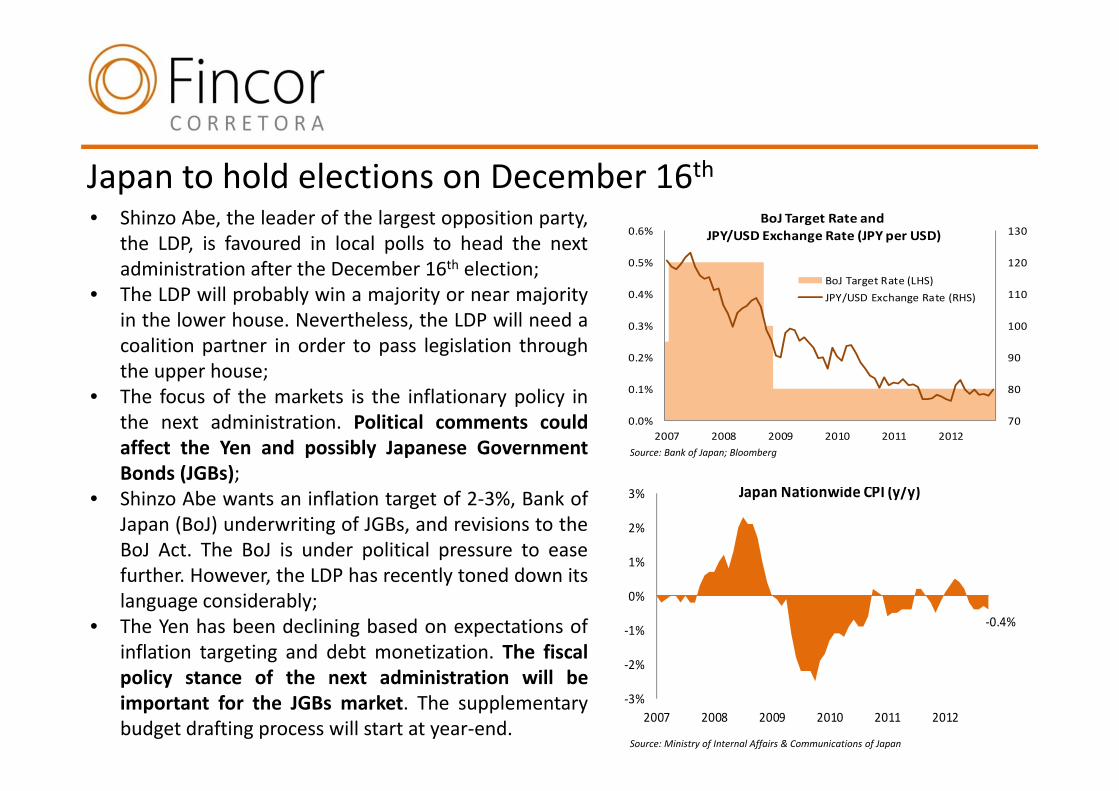

Japan to hold elections on December 16th• Shinzo Abe, the leader of the largest opposition party,

the LDP, is favoured in local polls to head the nextadministration after the December 16th election;

• The LDP will probably win a majority or near majorityin the lower house. Nevertheless, the LDP will need acoalition partner in order to pass legislation throughthe upper house;

• The focus of the markets is the inflationary policy inthe next administration. Political comments couldaffect the Yen and possibly Japanese GovernmentBonds (JGBs);

• Shinzo Abe wants an inflation target of 2‐3%, Bank ofJapan (BoJ) underwriting of JGBs, and revisions to theBoJ Act. The BoJ is under political pressure to easefurther. However, the LDP has recently toned down itslanguage considerably;

• The Yen has been declining based on expectations ofinflation targeting and debt monetization. The fiscalpolicy stance of the next administration will beimportant for the JGBs market. The supplementarybudget drafting process will start at year‐end.

Source: Bank of Japan; Bloomberg

Source: Ministry of Internal Affairs & Communications of Japan

‐0.4%

‐3%

‐2%

‐1%

0%

1%

2%

3%

2007 2008 2009 2010 2011 2012

Japan Nationwide CPI (y/y)

6,092

1,980

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2006 2008 2010 2012

China's Shanghai Composite Index

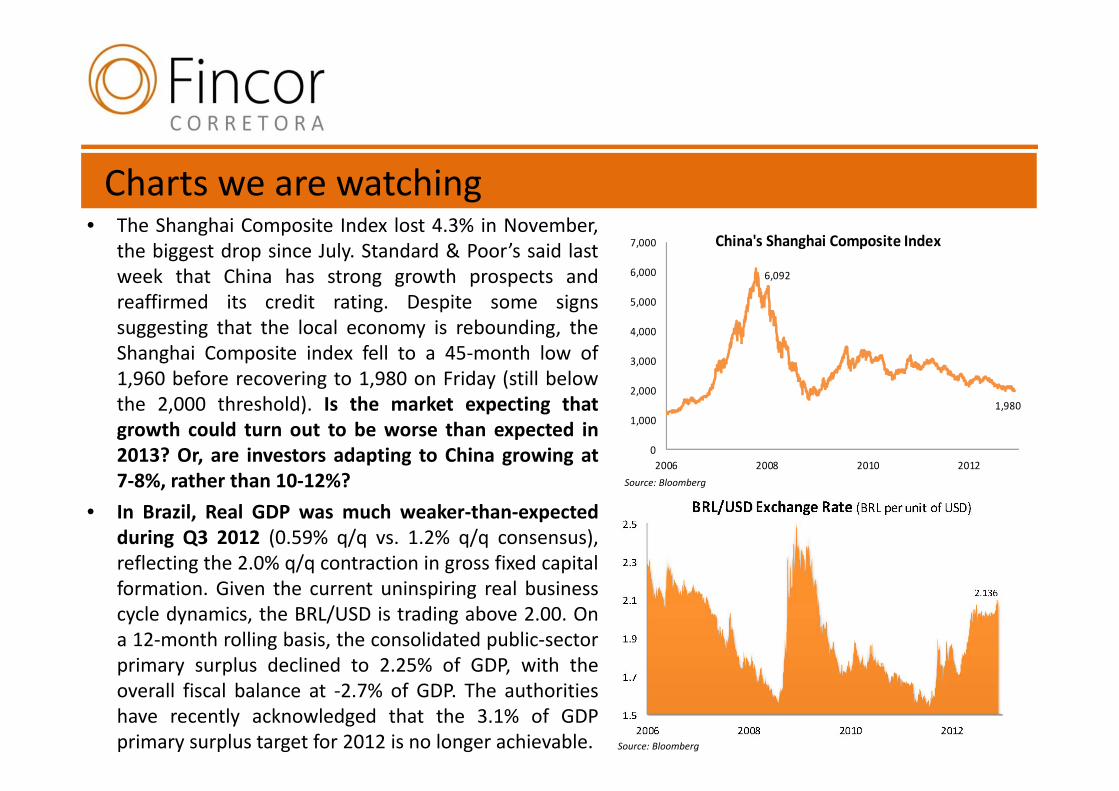

Charts we are watching• The Shanghai Composite Index lost 4.3% in November,

the biggest drop since July. Standard & Poor’s said lastweek that China has strong growth prospects andreaffirmed its credit rating. Despite some signssuggesting that the local economy is rebounding, theShanghai Composite index fell to a 45‐month low of1,960 before recovering to 1,980 on Friday (still belowthe 2,000 threshold). Is the market expecting thatgrowth could turn out to be worse than expected in2013? Or, are investors adapting to China growing at7‐8%, rather than 10‐12%?

• In Brazil, Real GDP was much weaker‐than‐expectedduring Q3 2012 (0.59% q/q vs. 1.2% q/q consensus),reflecting the 2.0% q/q contraction in gross fixed capitalformation. Given the current uninspiring real businesscycle dynamics, the BRL/USD is trading above 2.00. Ona 12‐month rolling basis, the consolidated public‐sectorprimary surplus declined to 2.25% of GDP, with theoverall fiscal balance at ‐2.7% of GDP. The authoritieshave recently acknowledged that the 3.1% of GDPprimary surplus target for 2012 is no longer achievable.

Source: Bloomberg

Source: Bloomberg

Disclosure Section

This research report is based on information obtained from sources which we believe to be credible and reliable, but isnot guaranteed as to accuracy or completeness. All the information contained herein is based upon informationavailable to the public.The recipient of this report must make its own independent assessment and decisions regarding any securities orfinancial instruments mentioned herein.This report is not, and should not be construed as an offer or a solicitation to buy or sell any securities or relatedfinancial instruments. The investment discussed or recommended in this report may be unsuitable for investorsdepending on their specific investment objectives and financial position.The material in this research report is general information intended for recipients who understand the risks associatedwith investment. It does not take account of whether an investment, course of action, or associated risks are suitablefor the recipient.Investors should seek financial advice regarding the appropriateness of investing in any securities or investmentstrategies discussed or recommended in this research report and should understand that the statements regardingfuture prospects may not be realized. Investors may receive back less than initially invested. Past performance is not aguarantee for future performance.Fincor – Sociedade Corretora, S.A. accepts no liability of any type for any indirect or direct loss arising from the use ofthis research report.Recommendations and opinions expressed are our current opinions as of the date referred on this research report.Current recommendations or opinions are subject to change as they depend on the evolution of the company or maybecome outdated as a consequence of changes in the environment.Fincor ‐ Sociedade Corretora, S.A. provides services of reception, execution, and transmission of orders.

Fincor – Sociedade Corretora, S.A.

Rua Castilho, 44 4º Andar1250‐071 LisboaPortugal