msc in finance and financial information systems...

TRANSCRIPT

The harmonization of accounting practices after the mandatory adoption of IASs / IFRSs in European Union: the

case of Greece

By IOANNIDOY EVANGELIA

COORDINATOR: Dr ATHIANOS STERGIOS

MSc in Finance and Financial Information Systems

Kavala 2006

Technological Educational

Institute of Kavala

TABLE OF CONTENTS

PAGES ABSTRACT 4

1. INTRODUCTION 4

2. LITERATURE REVIEW 9

2.1 International trends in accounting 9

2.1.1 Classification 9

2.1.2 Harmonization 14

2.1.3. The difference between harmonization and standardization 17

2.1.4 Manners to measure harmonization 18

2.1.5 Approaches for assessing the effects of harmonization 22

2.1.6 Important differences between IAS and local GAAP 23

2.1.7 Differences between IAS and Greek GAAP 26

2.1.8 Into the future 28

2.1.9 Arguments in favour of and /or against complete harmonization 29

2.2 Empirical studies 32

2.2.1 The global harmonization 32

2.2.2 Herfindahl index and I harmonization 34

3. DATA 38

4. METHODOLOGY 41

5. RESULTS 42

6. CONCLUSIONS 54

REFERENCES 55

APPENDIX A 63

APPENDIX B 68

2

CONTENTS OF TABLES PAGES

Table 1: The main empirical studies on the International Accounting

Harmonization and the tests they used 21

Table 2: Differences in the terminology between US-GAAP and IAS 23

Table 3: Methods used by the companies for calculating the inventories

in 2003 42

Table 4: Methods used by the companies for calculating the depreciation

in 2003 43

Table 5: Methods used by the companies for presenting the financial

statements in 2003 44

Table 6: Methods used by the companies for calculating inventories

in 2004 45

Table 7: Methods used by the companies for calculating depreciation

in 2004 46

Table 8: Methods used by the companies for presenting the financial

statements in 2004 47

Table 9: Methods used when adopting IASs (2004) 48

Table 10: Methods used by the companies for calculating inventories

using IASs (2005) 49

Table 11: Methods used by the companies for calculating depreciation

using IASs (2005) 50

Table 12: Methods used by the companies for presenting the financial

statements using IASs (2005) 51

Table 13: Comparison of H indices Spearman correlation results 52

Table 14: H index of harmonization trend 53

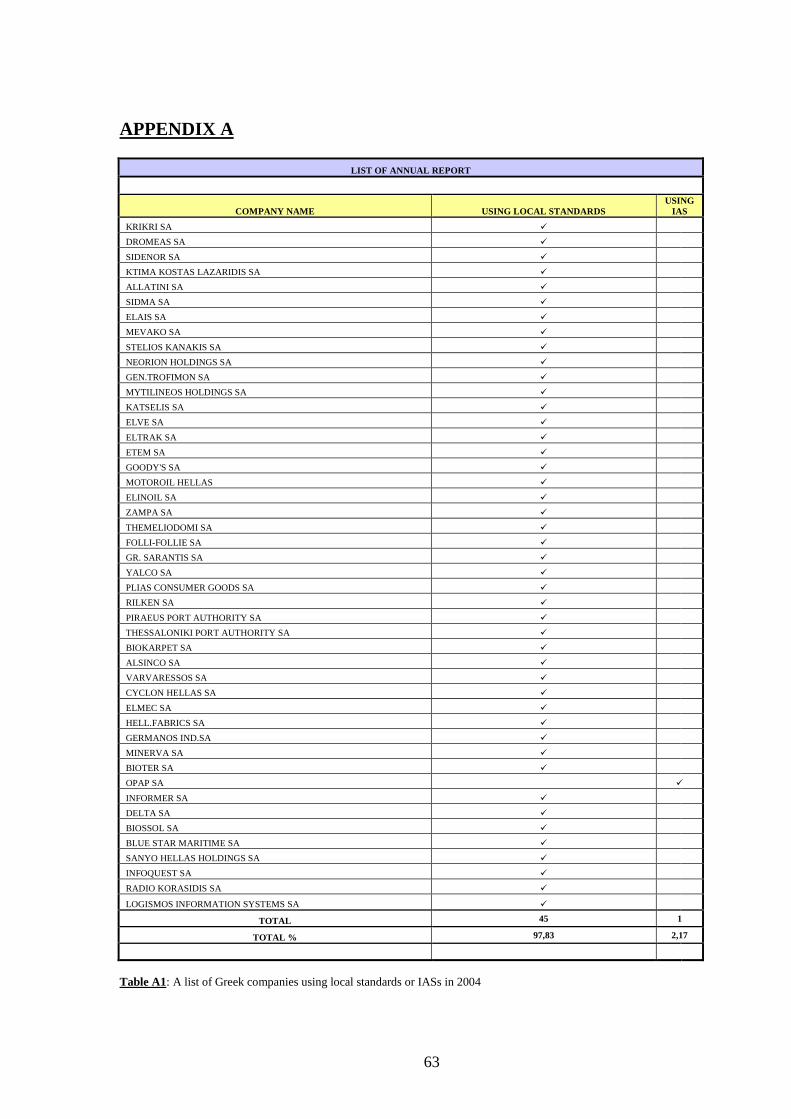

Table A1: A list of Greek companies using local standards or IASs

in 2004 63

Table A2: Listed companies per sector 64

Table A3: % participation per sector 65

3

PAGES

Table A4: Average assets and sales using local

standards (2003-2004) 66

Table A5: Average assets and sales using IASs (2005) 67

4

ABSTRACT

Many organizations have made efforts to improve the comparability of financial reporting. Many

studies have discussed the advantages and disadvantages of comparability. Our study

investigated the affect on the harmonization of accounting practices when a sample of companies

chooses to use international accounting standards (IASs) when preparing financial reports. This

study analyzed trends in the H index, a measure introduced by Van der Tas, in order to determine

if the adoption of IASs by a sample of Greek companies has increased the level of harmony. The

study included a control sample of Greek companies that did not switch from reporting using

local Greek standards during the same time period, 2003 through 2005. Three accounting

practices were included, depreciation, inventory and financial statement cost basis. The results

indicated that across the 3-year period, the majority of the H indices comparisons were positive

and statistically significant.

1. INTRODUCTION

Different countries have contributed to the development of accounting over the centuries. The

archaeologists many times discover ancient remains with writing and numbers on and they can be

sure that also those societies had the need to keep account.

The Romans developed a single-entry accounting and later Italy led to the emergence of the

double entry-system due to the increasing business. The seventeenth century, we first meet the

public subscription of share capital in Holland and next the growing separation of owner-ship

from management raised the need for audit in nineteenth century in Britain. Many European

countries have contributed to the development of accounting: France led in the development of

legal control over accounting, Scotland gave us the accountancy profession and Germany gave us

standardized formats for financial statements. From the late nineteenth century, the United States

has given us consolidation of financial statements, management accounting, and capitalization of

leases and deferred tax accounting.

Although international influences and similarities are clear, there are great differences among the

countries particularly in Europe.

Nowadays, it is known that the scenery of legal systems differs around the world and so on the

accounting principals in companies among different countries. The globalisation of markets and

the extension of enterprises is a reality. We need a method that can be used in order to eliminate

5

or reduce these “difference” problems and to provide comparability in financial information by

using the same Accounting Standards.

There are many differences among the principles that rule the financial reports in different

countries. To overcome this type of problems of dealing in an international environment, nine

countries founded and formed the International Accounting Standards Committee (IASC) in

1973 and had a based in London. The original members were the accountancy bodies of nine

countries: Australia, Canada, France, Germany, Japan, Mexico, the Netherlands, the United

Kingdom and the United States. This organization purposed to devise and spread widely

international standards in order to reduce the variation of practices in financial reporting

throughout the world. The IASC reorganized in 2001 as the IASB (International Accounting

Standards Board).

From 1973 to 1988, the IASC (International Accounting Standard Committee) formed standards

to complete the model of harmonization. The IASC formulates and publishes in the public

interest accounting standards to be observed in the presentation of financial statements and to

promote their worldwide acceptance and observance. The members agreed to support the

standards and use their best efforts to ensure that published financial statements comply with the

standards. They managed to persuade governments, stock exchanges, and other bodies to support

the IASC's standards.

Some years later, a new project named “Comparability/ Improvements” (IASC 1990) took place

to complete the formed standards and led the EC to set a new strategy for the financial reporting

in Europe. This strategy is a method which can reduce these differences. The international

competition, new investments in the world market, and the expansion in these markets have as a

result the need to compare all the data received. The aims of IASs are to determine and certify all

the above activities through their regulations, in order to achieve balance and gradual advance in

world markets. We can state that the IASs are a simple measure to interpret financial information

(FASB 1996). It is a great need that had been created in all the enterprises per the world to find a

way of common information of shareholders but also of people involved with the economic unit.

This led in new developed models, high quality, comprehensible and applicable that would be as

long as possible objective.

In many countries, IASs, are adopted as a whole and are legally obligatory. In some other

countries, the IASs are adjusted or incorporated to the local accounting standards and regulations.

Accounting standards are the regulations or rules (often including laws and statutes) that govern

the preparation of financial statements. Standard setting is the process by which accounting

6

standards are formulated. Thus, accounting standards are the products of standard setting.

However, actual practice may deviate from what the standards require. There are at least four

reasons for this.

First, in many countries the penalties for non-compliance with official accounting

pronouncements are weak or ineffective. Second, companies may voluntarily report more

information than required. Third, some countries allow companies to depart from accounting

standards if doing so will better represent a company's results of operations and financial

position. Finally, in some countries accounting standards apply only to individual company

financial statements, not to consolidated statements. In those countries, companies are free to

choose different accounting standards for their consolidated financial statements. To gain a

complete picture of how accounting works in a country, we must pay attention to the accounting

standard-setting process, the resulting accounting standards, and actual practice. Auditing adds

reliability to financial reports.

However the most important advantage of the IASs is that they are the “official language in stock

exchanges” around the world.This happens because many stock exchanges all over the world

accept IASs for cross border listing purposes. It is also important to mention that IASs aid the

harmonization process of accounting rules world-wide.

Harmonization is a process of increasing the compatibility of accounting practices by setting

bounds to their degree of variation. The term “harmonization”makes clearly the report in

accounting diversity. The harmonization of accounting standards, first at the regional level and

eventually at the global level, provides a basis for making the financial information of

multinationals more comparable. So, harmonization seems to imply coordination in the context

of a more flexible approach with acceptance of a state of harmony which may be short of total

uniformity.

According to Samuels & Piper (1985), international harmonization of accounting has been

defined as “the attempt to bring together different systems. It is the process of blending and

combining various practices into an orderly structure, which produces a synergistic result”. The

harmonisation of financial accounting and reporting standards is seen as a means of facilitating

the globalization of capital markets.

Prior research on accounting harmonisation may be characterised as either ‘‘de jure’’

harmonization, or formal harmonization, and ‘‘de facto’’ harmonization, or material

harmonization. The formal term refers to harmonization between regulations and practices

applied by companies. Some studies on the assessment of accounting harmonization have

7

focused on the investigation of material harmonization, disregarding the importance of formal

harmonization. The methodologies developed use the accounting information prepared by

companies to examine the level of harmonization among the practices and treatments applied.

This definition gives the term material harmonization.

Earlier writers have written about the benefits and costs of harmonization, obstacles and

problems that harmonization hinder, scope for harmonization, factors that are encouraging the

harmonization drive and so on. Nair and Frank (1981) and Evans and Taylor (1982) with aims

similar to those of Nair and Frank (1981), Doupnik and Taylor (1985), Van der Tas (1988) and

Tay and Parker (1990) tried to answer the question of how to measure harmonization.

‘Strong’ definitions coexist with ‘weak’ definitions. In this category (strong category), we find

Nobes and Parker (1991), who believe that harmonization is a process of reducing alternative

accounting choices and increasing the uniformity of accounting practices. Choi and Mueller

(1992) are representative of a second attitude (weak definition). They content themselves with an

absence of contradictions between accounting practices. Meek and Saudagaran (1990) belong to

this category. They argue that harmonization involves a conciliation of various points of view,

thereby avoiding logical conflict. This degree of harmonization does not prevent the existence of

choices between different accounting practices. A similar view of harmonization was expressed

by Tay and Parker (1992) who stressed that there should be flexibility within harmonization Van

der Tas (1992) occupies a middle position between the views of Nobes and Parker and, Choi and

Mueller. He recognizes the importance of a uniform set of accounting rules, but acknowledges

their ‘less strict’ character. Based on a review of the literature, our conclusion is that

harmonization should be viewed as the first stage in the overall process of International

Accounting Harmonization.

The European Union attributes great importance in the international harmonisation under the

application of accountant models because they constitute the basic condition for a fair and

effective competition. The EU recognizes that the comparability, the transparency and the

reliability of economic information constitute the fundamental condition on a single market of

capital. The lack of comparability discourages the investments because of the uncertainty. The

application of models is created acceptable accountant practices all over the world and thus we

deter an anarchy that may exist in the economic world. The solutions that will improve the

comparability should be supported internationally because the pumping of capital does not stop

in the borders of a country or in Europe. So, the international accountings standards are presented

8

as the most suitable and most acceptable solution in order to constitute the common denominator

that will lead to the collaboration of international markets.

The objective of Greek economy is the convergence with the matured economies of other

countries. The obligatory application of International Accounting Standards, at least for the

companies which their shares are negotiable in ASE (Athens Stock Exchange), contributes in the

creation of a single Stock Exchange Market. The application of International Accounting

Standards from the listed companies will improve the general picture of ASE and attract

foreigner investments what can constitute a very important lever of growth for the Greek

economy.

In Greece, the need for reliable accountant models is urgent and was voted a law that forecasts

the obligatory application of IASs from 01-01-2005 for publishing the economic situations,

especially when the company is listed in ASE. In EU exist today 7.000 listed companies, 300

companies apply the IASs and 200 companies apply the US GAAP.

In this thesis we examine the affect on the harmonization, or comparability, of accounting

practices a) when a sample of companies choose to use international accounting standards (IASs)

when preparing financial reports, b) when the sum of sample companies use local accounting

practices and c) when the total of sample companies adopt and use international accounting

practices, in our case IASs / IFRSs.

The rest of the dissertation is as follows: section 2 literature review. In section 3, it is presented

the sample of Greek firms in which we make our investigation. Section 4 mentions the

methodology which is followed for the processing of the data. Section 5 provides effects of

adopting IASs /IFRSs. On harmonization index H, reports the differences between accounting

practices that the sample companies choose to use across two accounting systems (under Greek

GAAP and IASs / IFRSs). Final section is the conclusions.

9

2. LITERATURE REVIEW

2.1 International trends in accounting

2.1.1 Classification

A critical question is why we should know how and why accounting develops. The answer is

critical, too. If we can identify what causes accounting to develop, we might be able to influence

or anticipate its direction and rate of change. It is said that we could better understand a nation's

accounting by knowing the factors that influence the development. Accounting clearly differs

around the world. In other words, these factors make us observing the differences and the

similarities between the accounting practices in different countries. Because accounting responds

to its environment, different cultural, economic, legal, and political environments produce

different accounting systems, and similar environments produce similar systems.

This leads us to classification. Classification is fundamental to understanding and analyzing why

and how national accounting systems differ. We can also analyze whether these systems are

converging or diverging. The goal of classification is to group countries according to the

distinctive characteristics of their financial accounting systems. Classifications reveal

fundamental structures that group members have in common and that distinguish the various

groups from each other. By identifying similarities and differences, we can better understand the

accounting systems. Classifications are a way of viewing the world.

International accounting classification work has been done in two ways: judgmental

classifications and empirically classifications. Although the methods of analysis for the two

approaches are different, their results are generally in agreement.

Mueller made the initial work on classification. Mueller's classification scheme was widely used

by national institutes of accountants, international organizations and multinational professional

accounting service firms. Later, the American Accounting Association's 1975-76 Committee on

International Accounting Operations and Education classified the accounting patterns of the

world into five separate ''Zones of Influence." They based their conclusions on historical, cultural

and socioeconomic sources that have influenced accounting principles of financial measurement

and reporting in different countries and regions. After Mueller, Nobes, based on these earlier

studies, showed that classification not only indicates which countries are in different categories,

but also how close or distant these categories are to one another. Further, Gray developed a

different judgmental classification scheme based on his work linking accounting and culture.

10

Another system of classification is to analyze accounting and reporting standards and practices

actually in use. Frank showed that financial accounting and environmental factors are related,

and he supported that accounting similarities can be expected among countries with similar

environments. After, a new study by Nair and Frank extended the Frank study in two ways and

the conclusion from this study is that measurement practices should be distinguished from

disclosure and that accounting measurement seems to be more stable than disclosure.

We can say that the classification has practical benefits. Due to the coexistence of certain

countries in a common group, these countries acquire common characteristics of reaction. The

differences among groups are barriers to the regional and worldwide harmonisation efforts. It is

easy to succeed, if the groups involved (such as the International Accounting Standards Board at

the international level and the European Union at the regional level) understand the differences

should overcome. Many times, developing countries can not develop their own accounting

standards. So it is frequent phenomenon copying existing standards as China and other countries

in Eastern Europe are doing now. Communication problems are often. Companies face users

(internal and external) who are unfamiliar with every company's accounting standards. All the

companies need to speak the same language.

It is known that every nation's accounting standards and practices is a result of economic,

historical, institutional and cultural factors and that is the “variety” among countries. It is

important to mention the following eight factors that have a significant influence on accounting

development. The first seven are economic, socio-historical and institutional in nature. Recently,

the relationship between culture (the eighth item) and accounting development has begun to be

explored.

In countries with strong equity markets such as the United States and United Kingdom,

accounting focuses on firms’ profitability. Company needs to meet the shareholders’ interest.

Japan and Switzerland are examples on the other side. In these countries, the credit-based system

(bank) is the dominant source of finance and accounting focuses on creditor protection through

conservative accounting measurements. The financial institutions have direct access to any

information they want so extensive public disclosures are not considered necessary.

The legal system determines how individuals and institutions have an effect on each other. The

Western world has two basic orientations: legalistic (code or civil law) and non-legalistic

(common or case law). Code law derives mainly from Roman law and the Code Napoleon. In

code law countries, laws are a set of requirements and procedures, and codification of accounting

standards and procedures is natural. By contrast, common law develops on a case-by-case basis.

11

Common law derives from English case law. Of course, statute law does exist, but it tends to be

less detailed and more flexible than in a code law system. This encourages experimentation and

permits the exercise of judgment. In most common law countries, accounting rules are

established by private sector professional organizations. This allows them to be more adaptive

and innovative.

Taxation is another critical issue. In many countries, tax legislation effectively determines

accounting standards because companies must record revenues and expenses for tax purposes

(Germany, Sweden). In other countries (Netherlands), financial and tax accounting are separate

but often tax legislation require the application of certain accounting principles.

It is known that accounting ideas and technologies are transferred through conquest, commerce,

and similar forces and the “copying” is a motivation for the harmonization of accounting.

Double-entry bookkeeping, which originated in Italy in the 1400s, gradually spread across

Europe with other ideas of the Renaissance. British colonialism exported accountants and

accounting concepts throughout the empire. Many developing economies use an accounting

system that was developed elsewhere, either because it was imposed on them (for example,

India) or by their own choice (for example, countries of Eastern Europe now modelling their

accounting systems after European Union (EU) regulations).

Another factor that affects the accounting development is the inflation. Inflation distorts

historical cost accounting and affects the prices. Israel, Mexico and certain countries of South

America use general price-level accounting because of their experiences with hyperinflation. In

the late 1970s, in response to unusually high rates of inflation, both the United States and United

Kingdom experimented with reporting the effects of changing prices.

The economic growth of a country influences the structure of the company and the way that

functions. This factor affects all the types of business transactions and determines which ones are

most prevalent. All the enterprises are adapted in the prevailing conditions because the most

important issue they face is the new accounting challenges.

The level of education is the last of the seven parameters that affect the accounting development

and belong in the sphere of economic, socio-historical and institutional factors. There are so

many terms in the economic scene that is impossible to comprehend them easily. It has no mean

if highly sophisticated accounting standards and practices are misunderstood and misused. That

is the magic. People must understand these terms in order to use them correctly and provide the

accounting principles. The only way to do so is a high educational level.

12

The new factor “culture” means the values and attitudes shared by a society. Cultural variables

underlie nations' institutional arrangements. According to Hofstede, culture is defined as

collective programming of the mind; it manifests itself not only in values, but in more superficial

ways: in symbols, heroes, and rituals (Hofstede, 2001). With the help of a model, cultural

differences and their consequences between nations, societies, and regions can be described in

detail.

There are four national cultural dimensions or societal values, the individualism, the power

distance, the uncertainty avoidance and the masculinity. His analysis is based on data from

employees of a large U.S. multinational corporation operating in forty different countries.

He said that “…individualism (versus collectivism) is a preference for a loosely knit social fabric

over an interdependent, tightly knit fabric (I versus us). Power distance is the extent to which

hierarchy and an unequal distribution of power in institutions and organizations are accepted.

Uncertainty avoidance is the degree to which society is uncomfortable with ambiguity and an

uncertain future. Masculinity (versus femininity) is the extent to which gender roles are

differentiated and performance and visible achievement (traditional masculine values) are

emphasized over relationships and caring (traditional feminine values)…”.

In this point, it is considered to report widely the theories of Mueller (1967, 1968), Nobes (1983)

and Gray (1988).

The macroeconomic pattern, the microeconomic pattern, the independent discipline approach and

the uniform accounting approach were first proposed by Mueller. Mueller’s (1967) study

identified four distinct patterns of contemporary accounting development. He believed that many

factors, such as the stage of economic development, the stage of business complexity, the shades

of political persuasion, and reliance on particular systems of law, would lead to the development

of different schemes of contemporary accounting.

The macroeconomic pattern is based on three propositions, the business enterprise is the basic

component in the national economy, the business enterprise succeed its goals best through close

coordination of its activities with national economic policies and public interest is served best if

business enterprise accounting is closely linked to national economic policies (Sweden).

Under the microeconomic approach, the individual firms are the core of business activities, the

main aim of the firm is to survive, firm’s best strategy for survival is economic optimization and

accounting derives its concepts and applications from economic analysis. The central accounting

concept here is that the accounting process must hold the amount invested in the firm constant in

real terms (Netherlands).

13

Business operates independently and produces its own concepts and methods from experience

and practice. Accounting is viewing here as a service function that derives its concepts and

principles from the business process it serves, not from a discipline such as economics (United

Kingdom, United States).

Finally, the uniform accounting approach maintains that accounting is a tool for administrative

control. This approach is used in countries with strong governmental involvement in economic

planning (France).

Nobes continued the study above adding in his classification fourteen essentially ‘‘Eurocentric’’

capitalist countries. His study was dominated by the structural constraints of the priorities of

capital. It was necessary for him to report an acceptance of the social, political and economic

arrangements, but also the belief that all self- interested economic transactions must rely on some

underlying bond to remain coherent.

Supported in previous studies, Gray suggested four accounting value dimensions that affect the

financial reporting practices. He believed that statutory control, uniformity, conservatism and

secrecy are the elements in a high power distance society. These societies are hard, there is no

trust between people, there exist null information of public and an imposition of laws and codes

is accepted. On the other hand, there are the professionalism, the flexibility, the optimism and the

transparency. In this case, people are more concern for equal rights, there is trust, they are not

scared for the future and business information move on a need-to-know basis.

On the basis of data gathered during the 1988–1992 period from 86 samples drawn from 41

cultural groups in 38 nations, Schwartz (1994) and Schwartz and Bardi (1997) divided national

cultures into seven value types. Conservatism, autonomy, hierarchy, mastery, egalitarian

commitment and harmony are the main ideas in Schwartz’s study.

Conservatism means the emphasis on the status quo and prohibits actions that might disrupt the

traditional order. Autonomy means the emphasis on the person viewed as an autonomous entity.

Hierarchy means the emphasis on how important is the hierarchical role. Mastery is the emphasis

on active mastery of the social environment through self-assertion. Egalitarian commitment is

how people can control selfish interests and harmony emphasizes on the unity with the nature.

These culture-level value types are condensed by Schwartz into two broad dimensions: autonomy

versus conservatism and egalitarian commitment and harmony versus hierarchy and mastery.

14

2.1.2 Harmonization

The big growth of international market leads us to wonder why do we need harmonization of

International Accounting Standards, what are the advantages and what are the barriers that hinder

harmonization? Although accounting may be the "language of business”, a common language has

never been necessary. This, however, is no longer true. We now face a global economy and this

affect the entire business world. Today's global corporation make the production and distribution

facilities separate widely. So, multinational corporations must prepare multiple reports for

different nations they do business in. Prices, interest rates and currency exchange values have

become internationally linked. Harmonization is necessary because standard national financial

statements are useless. There is a need for harmonization for accounting standards in order to

help the foreign investor to understand the financial statements of the foreign companies whose

shares they might want to buy. After all, financial information is a form of a language, so that

information could be comparable. The new factors of the global economy lead to the adoption of

International Accounting Standards (IASs) and the harmonization of the accounting practices.

Many writers underline the advantages of harmonization. According to Turner (1983) the

greatest benefit that would flow from harmonization would be the comparability of international

financial information. Such comparability would eliminate the current misunderstandings about

the reliability of foreign financial statements and would remove one of the most important

obstacles in the services of international investment. Choi, Frost and Meek (1999) said that

harmonization would save time and money that is currently spent to consolidate divergent

financial information when more than one set of reports is required to comply with the different

national laws or practice. They also added that harmonization improve the tendency for

accounting standards throughout the world to be raised to the highest possible level and to be

consistent with local economic, legal and social conditions. Nobes and Parker (2002) believed it

would be beneficial to countries which do not have standards of accounting and it would also

help in raising foreign capital as investors, financial analysts and foreign lenders will be able to

understand the financial statements of foreign companies. Samuels and Piper (1985) supported

that on the line of harmonization firms and users would be able to compare the investment

opportunities which will help them to make the right investment decision. As taxes exist on the

total global income of an organisation, it would be a help to the national tax authorities around

the world if they computed them on similar accounting principles and practices.

15

All the above is a small number of opinions around the advantages of harmonization and are the

prevailing opinions. Always when advantages exist, we also meet the disadvantages. Below are

presented elements that writers believed that constituted obstacles in the completion of

harmonization.

The most fundamental obstacles to harmonization are the present of differences between the

accounting practices of different countries, the lack of strong professional accountancy bodies in

some countries and the differences in the political and economic systems (Nobes and Parker

2002). Many writers mentioned that if accounting measurement rules were the only difference

among countries, then straightforward translations would be sufficient to enable reports to be

understood and interpreted. However, countries also raise substantial economic and cultural

differences that preclude simple interpretations, even when the figures are generated use the same

accounting principles.

The degree to which the government is involved also varies from country to country. Whereas

professional organizations set the standards in Britain, for example, the government assumes this

responsibility in France. Another barrier that the governments of different countries will have to

face is the coordination of their accounting policies with policies prevailing in other countries in

order to minimize negative externalities and to maximize positive externalities.

There are many barriers to harmonization as well. Users have different needs in different nations

(debtor vs creditor, countries that have very active stock markets and those where banks

primarily accumulate and invest capital) (Wyatt 1997). The existence of these barriers enforces

the belief that the public does not desire the adoption. However there are a number of benefits as

well which will come with the harmonization of international accounting standards.

It is useful in this analysis to highlight the reasons for accounting harmonisation from two view

points, the preparation of financial statements and the users.

Companies prepare financial statements for its users who are interested on the company. But it is

not the only reason. It is so hard for a company, any time making an investment in a country, to

deal with a new set of accounting standards. A uniform set of accounting standards, adopted from

all the countries, provide efficiency gains both internally and externally (Epstein and Mirza,

2001). So, preparators will best serve the client if harmonized principles and practices are

followed. A similar internal reporting system gives the chance of better comparisons, less

confusion and mistakes between the parts of the company. Cost savings can be achieved, because

the preparation of financial statements will be easier for companies. With Accounting Standards

the credibility of the externally reporting could be raised. All the reported figures would be

16

shown in the same way. The access to main financial markets will become easier for companies

and the capital would be appeared simpler for them.

At the other hand, there are users (employees, investors, banks, and owner). Harmonization

brings a lot of advantages. Investors, banks or owners are interested in obtaining information,

which enables them to take investment decisions. Financial statement based on harmonized

principles would make easier the comparison between companies because similar transactions

take place in the same way everywhere in the world. In other words, similar accounting practices

lead to a better comparability between companies. It is a major theme, the fact of better

understanding the reports because the risk is lower and the selections of investments is more

efficient. Choi et al. argue that “financial statement users have difficulty in interpreting

information produced under non-domestic accounting systems. They claim that harmonisation

will make it more likely that users will interpret the information correctly, and thus make better

decisions based on that information” (Choi et al., 2002). For the employees, we can claim

harmonised accounting standards are important because they can better understand the

development of the company they work in and operate its functions efficiently.

Harmonization is a movement away from total diversity of practice. According to Fredrick Choi

(1999), harmonization is a process of increasing the compatibility of accounting practices by

setting limits on how much they can vary. From this definition, harmonization of standards will

minimise logical conflicts and improve the comparability of financial information from different

countries. Harmonization is flexible and open. R.D. Nair and Werner G. Frank, in their article

“The Harmonization of International Accounting Standards, 1973-1979”, wrote that in the 1970s,

serious attempts were made to harmonize international accounting practices. This effort was

important because the growth of international trade and of multinational corporations

necessitated the comparison of accounting data across national boundaries.

From all the above, it is clear that international harmonization of accounting standards is vital to

promote the international capital market and it is also necessary to overcome the difficulties. In

spite of differences in international financial reporting, harmonisation of the accounting practices

were used in the preparation and presentation of financial information.

17

2.1.3. The difference between harmonization and standardization

International accounting harmonization generates interest among accounting practitioners,

academicians, investors, and other users of financial reports. Many organisations proposed the

accordance of financial reporting. In this point, it is essential to make clear the concepts of

harmonization and standardization and whether the target is harmonization or standardization.

Both ‘harmonization’ and ‘standardization’ are used in accounting practice and in the literature.

Harmonization is a movement away from total diversity of practice and standardization is a

movement toward uniformity. There is no real difference between them, perhaps, in the degree of

harmonisation they involve. In each case, they refer to the efforts required to ensure that

transactions and events are accounted in the same way wherever they took place or were

reported. “Standardisation” implies uniform standards in all the countries involved.

“Standardisation” is also a process, a movement towards uniformity, which is also a state (Tay

and Parker, 1990; Nobes and Parker, 2000). “Harmonisation” implies a reconciliation of different

points of view, and permits different requirements in individual countries to be reported in a

uniform way provided that there is no logical conflict (Canibano and Mora, 2000). Wolk et al.

describe harmonisation of Accounting Standards as “the degree of co-ordination or similarity

among the various sets of national Accounting Standards and methods and formats of financial

reporting” (Meek and Saudagaran in Wolk et al., 2001). Roberts et al. give a similar definition,

who describes harmonisation as a process by ”which accounting moves away from total diversity

of practice” (Roberts et al., 1998). Hence, international accounting harmonisation can be defined

as “the process of bringing international Accounting Standards into some sort of agreement so

that the financial statements from different countries are prepared according to a common set of

principles of measurement and disclosure” (Haskins et al. 1996).

From all the above definitions, it is clear that harmonization of standards will minimise logical

conflicts and improve the comparability of financial information from different countries. The

final end is a standardised situation, in which homogeneity and uniformity exist.

18

2.1.4 Manners to measure harmonization

The company transfer its financial position and affairs into a financial report. A financial report is

a manner of communicating. The structure of each financial report depends on the method used

by the company. As part of these policies, a company decides whether to translate an event (the

decision between alternative degrees of disclosure) and which accounting method to practice (the

choice between alternative methods of valuation, profit determination, consolidation and

presentation). Many times, the company has no choice. There are standards are settled by the

government or a private standard setting body and can refer either to the degree of disclosure or

to the accounting method to be applied. If a company desires to harmonize its financial reports,

the only way to do so is to follow these rules.

One definition about harmonization refer:”…harmonization is an increase in the degree of

comparability and means that more companies in the same circumstances apply the same

accounting method to an event or give additional information in such a way that the financial

reports of more companies can be made comparable…”.

The most popular manner measuring the degree of comparability in a financial report is the H

index (Herfindahl index). This index constitute one of a great number of statistical methods that

have been developed to measure the degree of concentration and rises when the methods of the

parties involved concentrate more on one or only a limited number of alternative methods. Its

calculation shows that high relative frequencies have a higher weighting that low relative

frequencies. The H index fluctuates between zero (0) meaning there is no harmony (with an

infinite number of alternative methods all with the same frequency), and one (1) meaning that all

the companies use the same method.

Many examples illustrate the application possibilities of Herfindahl index.

Deferred tax in the UK: A survey of Published Accounts (ICAEW, 1968-1981) showed five

different ways to present the deferred tax. When using the same standards, the result was that

harmonization took place and they could measure the provisions.

Accounting for the WIR (investment tax credit) in the Netherlands: There are three ways measure

the WIR. The results showed that the draft guideline, issued by Raad voor de Jaarverslaggeving

(1983), has a slight impact on the degree of harmony at the very time when the process of

harmonization stopped.

19

Accounting for the investment tax credit (ITC) in the US: They found two different methods for

measuring ITC but the H index showed that the degree of harmony rose during the examinant

period.

The WIR equalization account in the Netherlands: The WIR equalization could be presented in

five ways. The frequencies when adopting H index were favoring.

Valuation of land and buildings in the Netherlands: The increase in the C index was caused when

companies applied historical cost to give additional information about the current value of these

assets.

I index for the ITC in the US and the Netherlands: the method showed that the international

harmony decreased, while the two countries concentrated on a different method.

Tay (1989) briefly proposed the methodology below:

-Data on accounting methods and disclosure levels were obtained from the financial statements

of listed companies from five different countries.

- For each accounting method or disclosure item, companies were grouped according to the

practice followed.

- The chi-square test was used to assess the significance of the actual degree of harmony

demonstrated by the grouping, compared with a rectangular distribution. It was utilized by Tay

and Parker (1990) and although it is easily calculated, the chi-square has several limitations

because it does not consider the sample size and its value is not significant when the number of

observations is low or zero.

- Harmony was quantified using two different concentration measures — the H-index suggested

by van der Tas, and the entropy measure (E) — in three different forms (absolute, numbers-

equivalent and relative measures).

- Improvements in the level of disclosure and superiority of accounting method were quantified

using a disclosure index.

- The effects of disclosure of information and accounting methods on comparability were

quantified by calculating the C index.

- Changes in the values of H, E, C and the disclosure index were tested for statistical significance

by using nonparametric tests.

In general, there are three different statistical methods to measure harmonization and

standardization. These may be broadly described as descriptive statistics, non-parametric

statistics and indices.

20

The first one, descriptive statistics, is the simplest method. This method presents the calculation

of the number or percentage of companies within the sample which complied with specified

regulations. The size of the percentage described the degree of uniformity. But, these studies do

not provide completed information. Evans and Taylor (1982), McKinnon and Janell (1984) and

Nobes (1987) studied and showed that the result does not reflect general standardization of

accounting practice so much as uniformity of compliance with these IAS requirements.

The Friedman’s ANOVA test and the Mann-Whitney U test show that non-parametric statistics

may be useful in testing for evidence of harmony when data are ordinal in nature. However, they

also show that the concept must be properly defined and data properly interpreted and

appropriately categorized.

Finally, the three main indices, the H index, the I index and the C index. The first two are used

for calculating national and international harmony. The third calculates comparability of accounts

when different accounting methods are used but sufficient information is provided to show the

effect of using alternative methods.

To measure the extent of harmonization in Sweden, Cook (1989) used the V test of Cramer and

the C coefficient of contingency as a supplement to the chi-square test. Krisement (1997) also

applied the V test to measure the extent of harmonization of accounting practices for foreign

currency in nine European countries. Another statistical method used to measure the extent of

harmonization of accounting practices involves the generation of linear regression models such

as those developed by Archer, Delvaille and McLeay (1996) and McLeay et al. (1999). This

method allows a distinction to be made between the influence of normalization and the effects of

harmonization. Taplin (2003) argued that H and C indexes are not adequate to measure the level

of accounting harmonization. This is because there is a significant difference between an index

(H or C) calculated for the sample and an index created for a population and he proposed a

method to measure this difference – the standard error.

In Table 1 showed the main empirical studies on the International Accounting Harmonization

and the tests they used (Taplin 2003).

21

Authors Test used

H C Cmodified I Imodified X2 Others

Van der Tas (1988)

Tay and Parker

(1990, 1992)

Concentration

index

Van der Tas

(1992a, 1992b)

Emenyonu and Gray

(1992)

Archer, Delvaille and

McLeay (1995)

Hermann and Thomas

(1995)

Garcia-Benau

(1996)

Global

concentration

index

Archer, Delvaille and

McLeay (1996) Linear regression

Lainez, Callao and Jarne

(1996)

Friedman’s test

Wilcoxon’s test

Krisement (1997) V index

Adhikary and Emenyonu

(1997, 1998)

McLeay et al. (1999) Linear regression

Morris and Parker (1999)

Lainez, Jarne and Callao

(1999)

Canibano and Mora

(2000) Bootstrapping test

Parker and Morris (2001)

Aisbitt (2001) Wilcoxon’s test

Chen, Sun and Wang (2001)

Taplin (2003) Standard error

Ding, Stolowy and Tenenhaus

(2003)

Logistic

regression

Table 1: The main empirical studies on the International Accounting Harmonization and the tests they used (Taplin 2003).

22

2.1.5 Approaches for assessing the effects of harmonization

Many writers proposed several approaches to assess the effects of the implementation of

international standards in finance. Participants proposed that the authors need to be concentrated

on the income differences and investigate how the implementation of those standards will affect

these differences. They examined the net income across countries and they argued that there were

differences provoked by the implementation of standards. They examined depreciation, depletion

and amortization expense and operating expense and concluded that differences among countries

are relatively constant. One participant suggested that the authors must directly investigate the

potential effect of changes in accounting measurement by using an approach as in French and

Poterba (1991) who computed P/E ratios. The differences in accounting practices made difficult

to measure these ratios because there are many details in firm’s financial reports.

Authors believe that other more direct approaches used to evaluate accounting measurement

diversity have serious limitations and they view their study as an attempt to avoid some of those

studies’ problems, such as the need to observe accounting practices that many companies do not

disclose. A capital markets approach has many limitations but it may be the best approach to

address certain accounting issues.

2.1.6 Important differences between IAS and local GAAP

It is important to study the differences in the content of financial reports taking into account that

the differences vary depending on many factors as the nature of the company's operations, the

industry in which it operates, and the accounting policy choices it has made. It is also essential to

report what IAS articles mentions about the elements we are going to examine.

A great number of studies were published trying explaining the differences between the local

GAAPs and the IASs. The most popular are these explaining the differences between the US-

GAAP and the IASs (Leuz, 2003, Pacter, 2002, Street, Nichols and Gray, 2000). The most of

them are theoretical approaches.

Choi et al. (2002) has summarized the differences in the U.S., U.K., and IAS GAAPs, however,

the standards appear more similar than different. In addition to the similarities previously

discussed, IAS and U.S. GAAP are very similar in some areas such the framework and

treatments of related party transactions, post balance sheet events, contingencies and provisions.

23

The financial ratios used to analyze financial statements are also very similar under the IAS and

U.S. GAAP.

Sawabe (2002) notes a country specific difference in the Japanese banking industry. In this

example, Japanese Regulatory Accounting Principles (RAP) concurs with GAAP on inventory

valuation. Yet, corporate managers have discretion to choose between lower of cost or market

(LCM) or historical cost method, for corporate accounting principles. Another example is the

case of German banks. SFAS 131 and IAS 14R describe segment reporting requirements for

public companies. Homolle (2003) notes there are “substantial differences” between SFAS 131

and IAS 14R approaches when applied to the German banking industry, which had to be

reconciled with Germany’s GAS 3, imposed by the GASC. Furthermore, GAS 3 was then

supplemented by GAS 3-10, Segment Reporting of Banks, in an attempt to define industry

specific banking guidelines for segment reporting (Homolle, 2003). Using Securities and

Exchange Commission (SEC) form 20-F that reconciles IAS to U.S. GAAP, researchers have

identified the following practical terminology differences between the two GAAP methods

(Pacter, 2002; Sleigh-Johnson, 2002; Street et al., 2000) (Table 2):

US-GAAP terminology IAS terminology

Income statement Profit and loss accounts

Account receivable Debtors

Account payable Creditors

Capital lease Finance lease

Allowance for uncollectible accounts Provision for bad debts

Inventory Stock

Common stock Ordinary shares

Statement of cash flows Cash flow statement

Accounts receivable confirmation Debtors circularization

Table 2: Differences in the terminology between US-GAAP and IAS (Pacter, 2002; Sleigh-Johnson, 2002; Street et al., 2000).

24

Below is given concisely the content of IAS article that we are going to examine in our work

(IASB):

Summary of IAS 1

“A complete set of financial statements comprises a balance sheet, an income statement, a

statement of changes in equity, a cash flow statement and notes comprising a summary of

significant accounting policies and other explanatory notes. Financial statements present fairly

the financial position, financial performance and cash flows of an entity. Fair presentation

requires faithful representation of the effects of transactions, events and conditions in accordance

with the definitions and recognition criteria for assets, liabilities, income and expenses set out the

Framework for the Preparation and Presentation of Financial Statements. The application of

IFRSs (Standards and Interpretations), with additional disclosure when necessary, is presumed to

result in financial statements that achieve a fair presentation. An entity makes an explicit and

unreserved statement of compliance with IFRSs in the notes to the financial statements. Such a

statement is only made on compliance with all the requirement of IFRSs. A departure from

IFRSs is acceptable only in the extremely rare circumstances in which compliance with IFRSs

conflicts with providing information useful to suers in making economic decisions. IAS 1

specifies the disclosures required when an entity departs from a requirement of an IFRS.

IAS 1 specifies the following about the preparation and presentation of financial statement:

-Financial statements are prepared on a going concern basis unless management either intends to

liquidate the entity or to cease trading, or has no realistic alternative but to do so.

- Financial statements, except for cash flow information, are prepared using the accrual basis of

accounting.

- The presentation and classification of items in the financial statements are usually retained

from one period to the next.

- Each material class of similar items is presented separately. Dissimilar items are presented

separately unless they are immaterial. Omissions or misstatements of items are material if they

could, individually or collectively; influence the economic decisions of users taken on the basis

of the financial statements.

- Assets and liabilities, and income and expenses, are not offset unless required or permitted by

an IFRS.

- Comparative information is disclosed for all amounts reported in the financial statements,

unless an IFRS requires or permits otherwise.

25

-Financial statements are presented at least annually.”

Summary of IAS 2

“Inventories are measured at the lower of cost and net realisable value. Net realisable value is the

estimated selling price in the ordinary course of business less the estimated costs of completion

and the estimated costs necessary to make the sale. Cost includes all costs of purchase, costs of

conversion and other costs incurred in bringing the inventories to their present location and

condition. The cost of inventories, other than those for which specific identification of costs are

appropriate, is assigned by using the first-in, first-out (FIFO) or weighted average cost formula.

When inventories are sold, the carrying amount of those inventories is recognised as an expense

in the same period as the revenue. The amount of any write-down of inventories to net realisable

value is recognised as an expense in the period the write-down or loss occurs. The amount of any

reversal of a write-down of inventories is recognised as a reduction in the amount of inventories

recognised as an expense in the period in which the reversal occurs.”

Summary of IAS 16

“Property, plant and equipment is initially recognised at cost. Subsequent to initial recognition,

property, plant and equipment is carried either at:

-Cost, less accumulated depreciation and any accumulated impairment losses, or

-Revalued amount, less subsequent accumulated depreciation and any accumulated impairment

losses. The revalued amount is fair value at the date of revaluation.

The choice of measurement is applied consistency to an entire class of property, plant and

equipment. Any revaluation increase is credited directly to the revaluation surplus in equity,

unless it reverses a revaluation decrease previously recognised in profit or loss. Any revaluation

decrease is recognised in profit or loss. However, the decrease is debited directly to the

revaluation surplus in equity to the extent of the credit balance in revaluation surplus in respect of

that asset. Depreciation is applied on a component basis. That is to say, each part of an item of

property, plant and equipment with a cost that is significant in relation to the total cost of the item

is depreciated separately. The depreciable amount of an asset is allocated on a systematic basis

over the useful life of the asset. Impairment is recognised in accordance with IAS 36 Impairment

of Assets. The gain or losses on derecognition of an item of property, plant and equipment is the

26

difference between the net disposal proceeds, if any, and the carrying amount of the item. It is

included in profit or loss.”(www.iasplus.com)

2.1.7 Differences between IAS and Greek GAAP

Greek requirements are mainly based on Corporate Law 2190/1920, accounting standards issued

by the Ministry of National Economy, the interpretations issued by the National Accounting

Standards Board (ESYL) and the Greek General Chart of Accounts approved by Presidential

Decree 1123/80.

Greek accounting may differ from that required by IAS in the following areas:

Financial statements reports

- There is not financial report for cash flows, only for the listed companies.

- There is not report for the change on owners. It is presented in the table Earning disposal

indirectly.

Τangibles

- Revaluation of the real estate value per 4 years.

Ιntangibles

- The interest when buing fixed assets are characterized as expenses of prolonged depreciation

(5 years).

Depreciation (tangible)

- Factors of annual depreciation

Deprciation (intangible)

- Depreciation in 5-year period.

Expenses of research and growth

- The expenses of research ad growth are presented in the account of expenses of prolonged

depreciation.

Securities valuation

- It separately becomes in the lower price between price of acquisition and current value for each

element.

Deferred taxation

- It is not contented in law 2190/20

27

Forecasts for employees’ compensation

- The company is forced to make forecasts with regard to the retirement.

Consolidation

- Only the subsidiary companies with same activity.

Goodwill

It is valued with one way.

There are no specific rules requiring disclosures of:

- a primary statement of changes in equity

- the FIFO or current cost of inventories valued on a LIFO basis

- the fair values of financial assets and liabilities

- the fair values of investment properties

- related party transactions, except for balances resulting from transactions that are not in the

normal course of business

- discontinuing operations

- segment reporting, except for sales

- cash flow statements

- earnings per share

There are inconsistencies between Greek and IAS rules that could lead to differences for many

enterprises in certain areas. Under Greek rules:

- Some subsidiaries with no similar activities from the rest of the group are excluded.

- The classification of business combinations between unitings of interests and acquisitions is

made on the basis of legal form rather than on whether an acquirer can be identified.

- Gains on foreign currency monetary balances are deferred until settlement.

- Trading and derivative liabilities are not recognized at fair value.

- Research costs and pre-operating costs may be capitalized.

- Goodwill can be written off directly against equity.

- Land and buildings are revalued periodically.

- Inventories are valued at the lowest of cost, net realizable value and replacement cost.

- Investment properties are revalued every four years and depreciated.

-Costs and revenues on construction contracts are not necessarily recognized on a stage of

completion basis.

28

- Provisions are not generally discounted

- Own (treasury) shares are shown as assets and an equivalent reserve is set up through the

appropriation statement and reflected in shareholders' equity; gains and losses on their sale are

recognized as income.

2.1.8 Into the future

Decision makers recognize the need to understand financial documents with transparency and

clarity. The rapid development of economies internationally has created a lot of occasions for the

growth of enterprises. The globalisation has created powerful bonds and the new data lead to an

imperative application of international models that ensure high quality economic information that

is comparable and comprehensible, independent from the country of origin. Thus is presented

high quality, comprehensible, transparent and comparable information.

A possible future prediction is that accounting system harmonization will facilitate the

commonality for the benefit of both investors and firms. The level of investors around the world

will increase. Investors visit stock markets and become more active in markets. On the other

hand, enterprises do not desire missing great amounts and time trying to accord their financial

reports. The timing is perfect for the maturity with global investors able to access information

and conduct transactions at low cost and high speed with the term that all the procedures and

techniques are similar.

The same effect faces also the Greek market. It is considered that the application of International

Accounting Standards is essential for the modernisation of Greek market, as is ensured the

uniformity of economic situations of companies’ and consequently the better comparison with

companies abroad. The economic situations that are created based on IASs facilitate the investors

and the analysts to compare the Greek companies with other. There are a lot of profits for Greek

companies: help the investors make comparisons, transparency in the presentation of economic

situation, integration of information for the investors.

The practice showed that the passage from the national accountant models in the IASs is

particularly difficult and no a simple change in the way of presentation of financial information.

This requires a big effort, particularly in countries, as Greece that the national accountant models

are directed in the tax needs, despite in the complete and essential briefing of users of economic

reports.

29

It is true that the adoption of IASs constitutes a revolution with particularly positive results. A

simple comparison of financial reports that is drawn up based on IASs with these reports that are

drawn up based on the Greek Accountant Models shows the qualitative difference.

2.1.9 Arguments in favour of and /or against complete harmonization

One of the arguments in favour of harmonization is the high quality of standards. Many studies

published for the accounting quality states that international standards are of higher quality than

most local GAAP. These studies show that IAS-earnings have higher value relevance than

earnings based on local GAAP (Niskanen et al., 2000). Auer in1996 suggested that IAS-based

earnings convey significant higher information content when compared with Swiss GAAP

earnings. Ashbaugh and Pincus (2000) showed that financial information of companies become

more predictable after the adoption of IASs and the reduction in the variation in measurement

and disclosure practice as a consequence. In particular, they found that the accuracy of financial

analysts earnings forecasts is increasing after adoption of IASs. Leuz and Verrecchia (2000)

found that the information asymmetry component of the cost of capital decreases after IASs

implementation, because of an increase in the level and quality of disclosure. Ball et al. (2000)

found that IASs have fewer explicit accounting choices and increases the amount of financial

disclosure.

Another fact that supports the adoption of IASs is that they offer lower cost of capital. This could

be considerable by companies since as IAS is of higher quality than most local GAAP (more

disclosure, fewer choices, timely, more predictable), companies who disclose information

according to IAS could receive a higher rating and as a consequence obtain a lower cost of

capital. In addition, the comparability of economic positions between business entities

irrespective of whether they are organized as single enterprises or groups would be reached,

which could have a positive effect on the decision usefulness of the financial statements for their

users (Ballwieser, 1999, p. 441).

It is undoubtedly that the harmonization of financial accounting is the result of the adoption of

IASs. We know that the implementation of these standards is mandatory for companies, so will

not be created a risk of a wide gap between the financial statements and the individual reporting,

leading to a disharmonization within countries. The application of uniform accounting principles

and rules for individual and group accounts is practical and efficient. Implementing a complete

harmonization would mean a cost reduction for these companies.

30

All the above is the positive side of this subject. There are also many writers that are contrary

with the mandatory adoption of such standards. Their arguments are counted mainly on the

economical sphere. An example is the Belgium; the Belgian Commission of Banking, Finance

and Insurance (CBFA, 2004) has carried out a survey in 73 listed Belgian companies, which

examines the difficulties and costs in relation to convergence with IASs. Although a majority of

the firms (62 per cent) state that they have no problems in obtaining the necessary data to report

under IASs, the respondents find it costly to implement IASs. Moreover, only 22 per cent of the

respondents state that the value added of IASs financial statements is positive for the majority of

users of financial statements. It is sure that the relative implementation cost will even be larger

for smaller companies. Furthermore there are fewer potential users of the financial information

disclosed by small firms, which would result in fewer potential benefits and higher accounting

costs per users (Bollen, 1995, p. 39).

There are many prior researches that indicate the negative influence of the relationship between

tax and financial reporting on accounting harmonization (Guenther and Hussein, 1995 and Lamb

et al., 1998). The question should be asked how tax computation should be organized in the

future. What problems will be arising with the adoption of IASs? Is it fair to tax companies based

on different financial statements since the application of the standards is mandatory only for the

listed companies? On the other hand, the primary objectives of IASs are to serve the needs of the

capital markets. As investors have different information needs than the tax authorities, it is time

to recognize the diverse purposes of financial reporting and tax accounting.

A critical question is whether a large multinational company should be comparable with a small

local company and whether differences that exist between large and small businesses and among

the needs of their users are eliminated by using standards. The main user groups of financial

statements identified by the literature are ‘employees, managers, providers of loan finance, trade

creditors and the Inland Revenue’ (Page, 1984; Barker and Noonan, 1996; Collis and Jarvis,

2000). Paolini and Demartini (1997), based on an Italian survey, identify two main user groups:

tax authorities and banks (representing the public interest) and management. Riistama and

Vehmanen (2004) argue that the needs of small companies’ accounts’ users differ from user

needs in large companies. Chaveau et al. (1996) found identical evidence. They state that small

business financial reports are most relevant to internal management and external bankers and

creditors. There are diverging goals to the main users of accounts. According to John and

Healeas (2000) statutory accounts were not perceived as useful for decision making: “very few of

the owner-managers have a proper understanding of the contents of statutory accounts. … They

31

often take the view that the statutory accounts are of no practical use for decision making and

prefer to use the management accounts and a cash flow forecast”. Friedlob and Plewa (1992)

indicate that because financial information is cost-free to users of financial statements, they want

more rather than less. Certified Public Accountants contended that disclosure is more important

for public than for privately held companies, and significantly more important for large publicly

owned companies than for small publicly owned companies.

Lippitt and Oliver (1983) mention ways in which the financial information needs of small

businesses can differ from those of large businesses. First, the numbers of buyers and sellers on

the capital market of small businesses is different and changes in ownership may make financial

reports less appropriate. Second, the management of a small business is often in hands of one or a

few individuals, who perform multiple management roles. Such managers are familiar with most

aspects of the business and so on, they are more independent upon formal financial information

than the others in large businesses. Thirdly, because of the limited access of a small business to

capital markets, the role of bankers and other creditors is rather significant. A main argument is

that users of public company statements usually depend on such statements for their information.

However, owners and creditors of privately owned enterprises can often ask and receive

additional information whenever requested (Chazen and Benson, 1978, p. 49).

Harvey and Walton (1996) suggest that financial statements of larger companies reflect more

complex transactions than small companies’ accounts, which implies that more extensive

disclosures are appropriate.

Bollen (1995) said that IASs could become mandatory for all types of firms. “But the

enforcement of such regulations in the small firm sector, given the large number and

heterogeneity of firms would provide an immense task for any regulator”. A number of studies

indicate considerable non-compliance with financial disclosure regulations in the small firm

sector (Ingram et al., 1977, Robert, Ramsay and Sutcliffe, 1986). Given the relatively minor

attention paid to securing compliance with small firm accounting regulations, Bollen argues that

the usefulness of mandatory accounting disclosures by small firms can be questioned.

32

2.2 Empirical studies

2.2.1 The global harmonization

A study for harmonization was written by Jose A. Lainez, Susana Callao and Jose I Jarne

(University of Saragossa) and their main aim was to measure the degree of harmonization which

exists across each element of the different national reporting requirements. They concentrated

their research on Australia, Belgium, Canada, France, Germany, Italy, Japan, Luxembourg,

Holland, Spain, Switzerland, UK and US. The writers took the elements (the work has done by

IOSCO). They considered necessary to underline the diversity which existed among

requirements; requirements can be classified into two categories, periodical reporting

requirements and additional reporting requirements. They calculated the weighted average of all

the items aiming to obtain a numerical average. This average in accordance with a scale would

indicate the degree of requirement of the stock market regulations of the different countries for

each of the specific requirements.

Then, they performed the statistical analysis evaluating the level of requirement and

harmonization. In this step, they performed non-parametric tests as Friedman’s and Wilcoxon’s

and in the next step, they adopted an indicator known as Van der Tas C-index for quantifying the

level of harmonization. At the end, they measured the level of global harmonization that exists

between the thirteen countries.

They detected differences among the countries but they concluded that harmonization of

reporting requirement is an impulse towards the harmonization of financial information.

Emmanuel N. Emenyonu and Sidney J. Gray (1996) examined the results of an effort made to

reduce the diversity in accounting practices internationally. They examine a 20-year period from

1971/1972 to 1991/1992. Firstly, they used the Chi-square (x2) test (Siegel and Castellan, 1988)

to make an accounting measurement on practices used by companies. After that, they constructed

a harmony index which provided a range of values. This index was the I-index is stated as

follows:

I-index = )1/(121

1

)*....*.*(

mm

n

i

fififi

where fi is the relative frequency, m is the number of countries and n is the number of alternative

accounting methods.

33

The Chi-square test measures the extent to which the preferences of some independent groups

are matched and the I-index measures the extent to which the accounting practices of companies

across countries are concentrated around one or more alternatives. The results showed that the

impact of efforts to reduce international accounting diversity over the period studied have been

indifferent.

Another study examines the motivations and characteristics of firms complying with IAS. Both

International Accounting Standards Committee (IASC) and accounting researchers had a special

interest about this examination because they wanted to detect the merits of mandating IAS by

multinational firms.

The procedures that are used were the non-parametric Wilcoxon test and the Logit regression

model. The first is used to analyze the characteristics of IAS firms in comparison to those of non-

IAS firms and the Logit regression model to test the relationship between a firm's compliance