mse608c – engineering and financial cost analysis the income statement

Post on 21-Dec-2015

216 views

TRANSCRIPT

MSE608C – Engineering and Financial Cost Analysis

The Income Statement

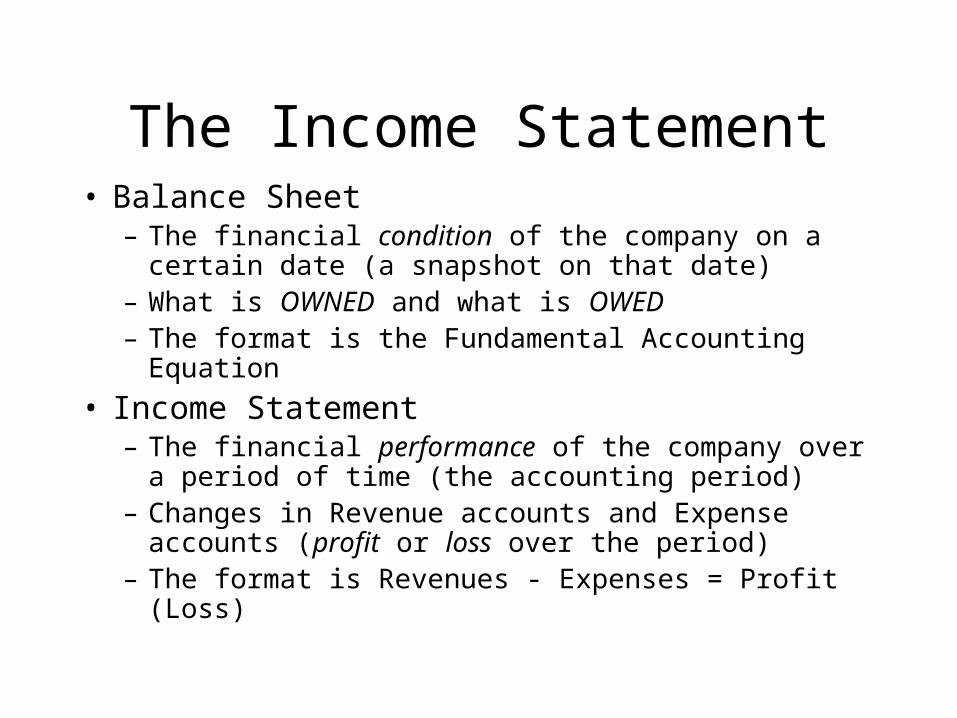

The Income Statement• Balance Sheet

– The financial condition of the company on a certain date (a snapshot on that date)

– What is OWNED and what is OWED– The format is the Fundamental Accounting Equation

• Income Statement– The financial performance of the company over a

period of time (the accounting period)– Changes in Revenue accounts and Expense accounts

(profit or loss over the period)– The format is Revenues - Expenses = Profit (Loss)

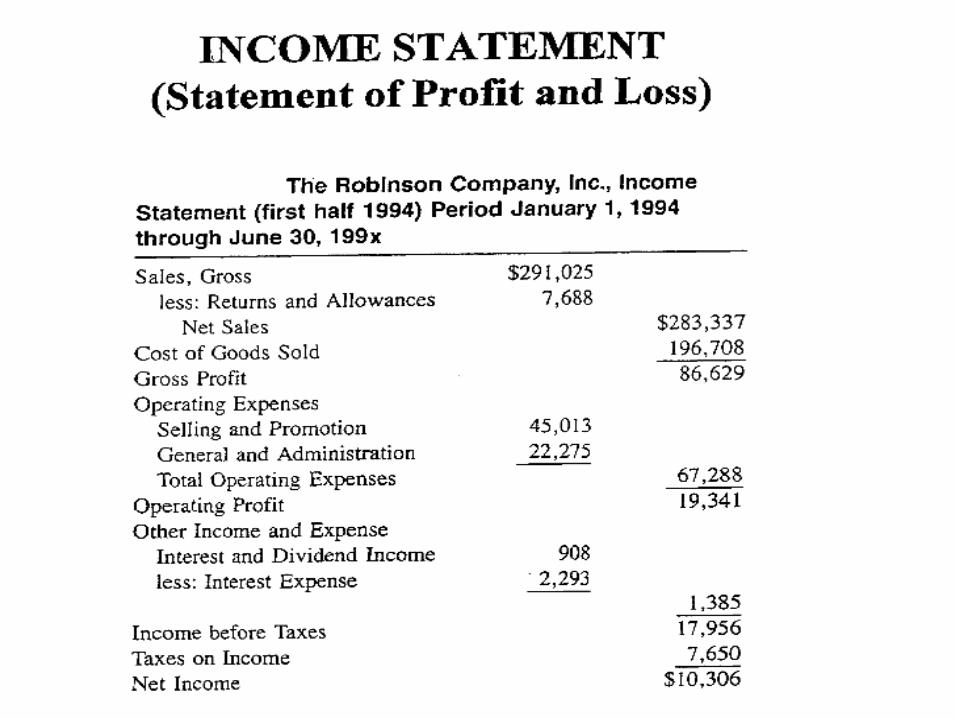

Revenues and Gross Profit

REVENUES – COGS = GROSS PROFIT

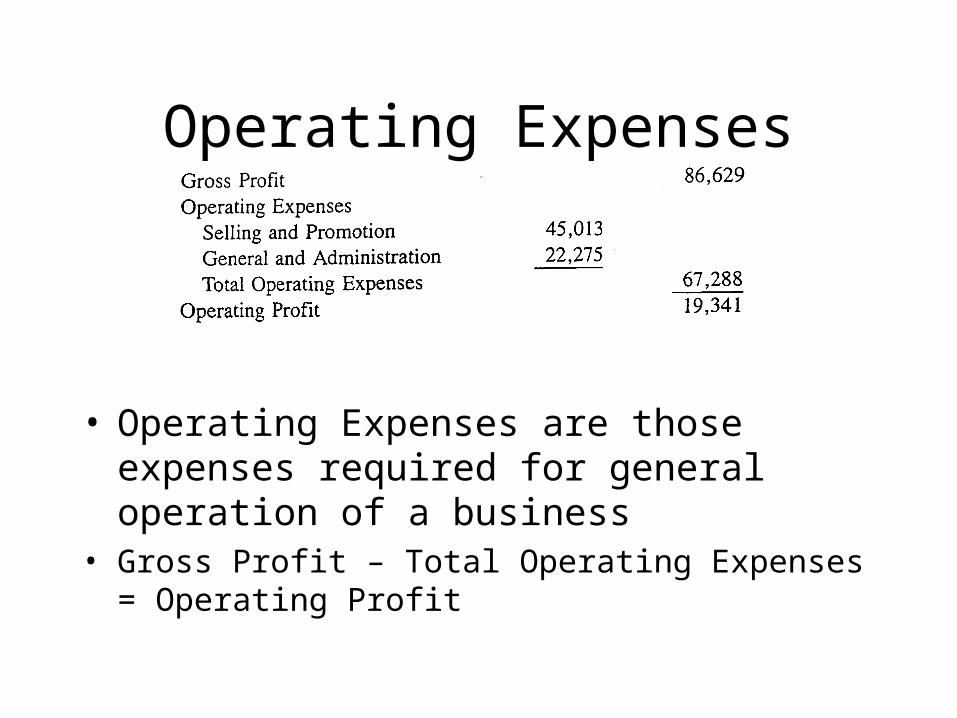

Operating Expenses

• Operating Expenses are those expenses required for general operation of a business

• Gross Profit – Total Operating Expenses = Operating Profit

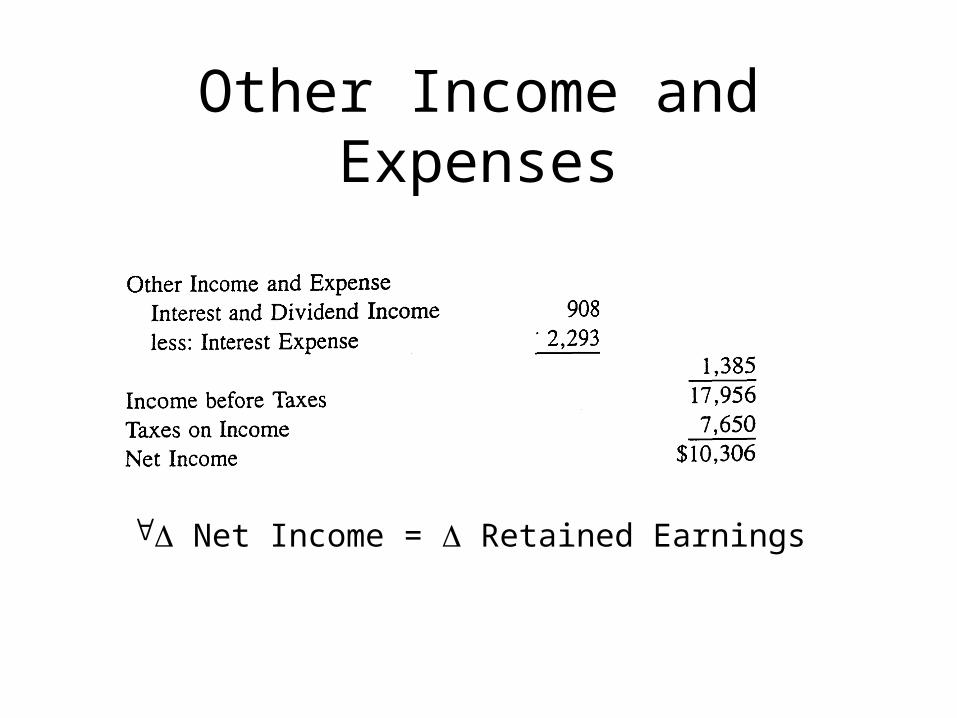

Other Income and Expenses

Net Income = Retained Earnings

What are Revenues and Expenses?

Asset

+ - =Liabilities

- +

Owners’ Equity

- ++

A = L + OE

- + - +

+-

INVESTED CAPITAL RETAINED EARNINGS

EXPENSES REVENUES

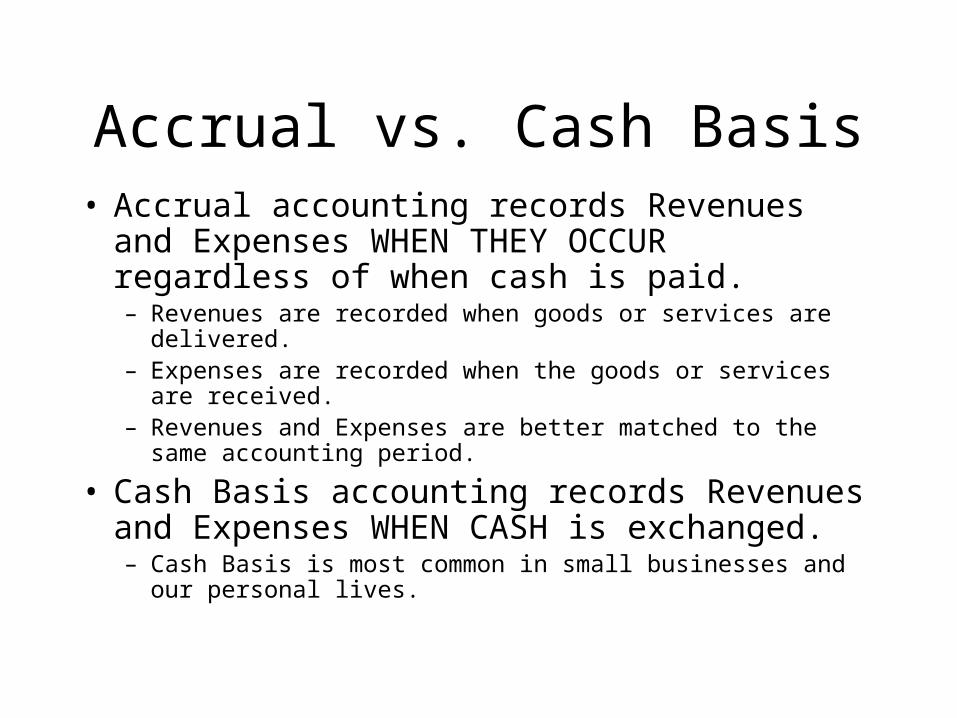

Accrual vs. Cash Basis• Accrual accounting records Revenues and

Expenses WHEN THEY OCCUR regardless of when cash is paid.– Revenues are recorded when goods or services are delivered.– Expenses are recorded when the goods or services are received.– Revenues and Expenses are better matched to the same accounting

period.

• Cash Basis accounting records Revenues and Expenses WHEN CASH is exchanged.– Cash Basis is most common in small businesses and our personal

lives.

Who Can Use the Cash Method?

• Although the IRS allows all businesses to use the accrual method of accounting, most small businesses can instead use the cash method for tax purposes. The cash method can offer more flexibility in tax planning because you can sometimes time your receipt of revenue or payments of expenses to shift these items from one tax year to another.

• However, some businesses must use the accrual method: corporations that are not S corporations and partnerships that have at least one corporation (other than an S corporation) as a shareholder. There are some exceptions to these restrictions — the cash method is available for farming businesses and entities (including corporations) with average annual gross receipts of less than five million dollars for all prior years.

• Tax shelters may never use the cash method. If your business has inventories, you must use the accrual method, at least for sales and merchandise purchases.

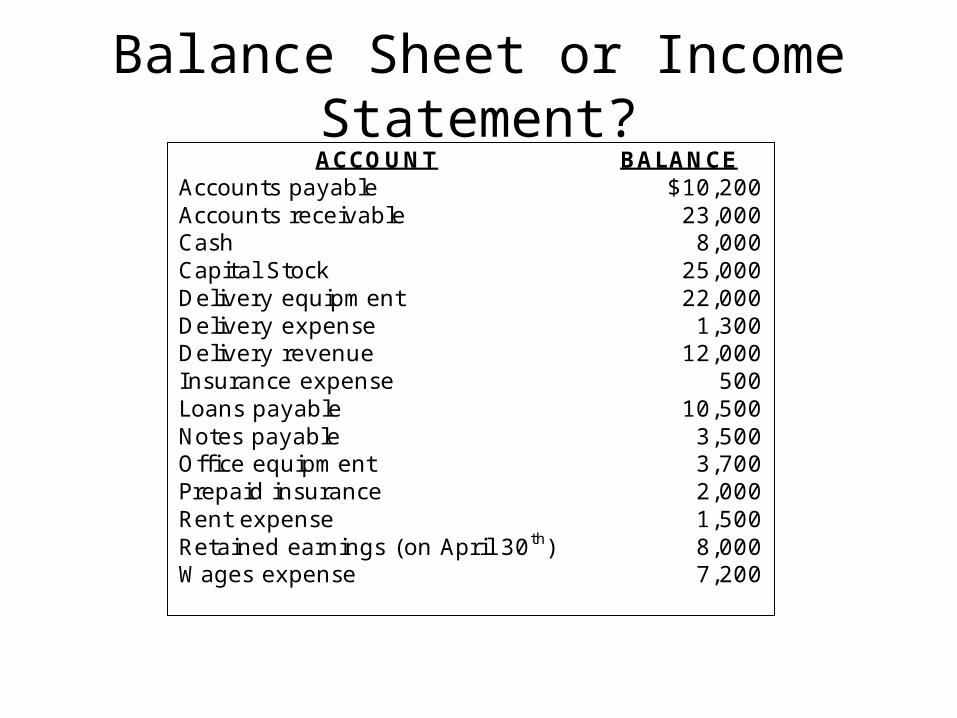

ACCOUNT BALANCE Accounts payable $10,200 Accounts receivable 23,000 Cash 8,000 Capital Stock 25,000 Delivery equipment 22,000 Delivery expense 1,300 Delivery revenue 12,000 Insurance expense 500 Loans payable 10,500 Notes payable 3,500 Office equipment 3,700 Prepaid insurance 2,000 Rent expense 1,500 Retained earnings (on April 30th) 8,000 Wages expense 7,200

Balance Sheet or Income Statement?

What are the Accounting Transactions?

1. You purchase 6 months of prepaid rent at $1000 per month.

2. At end of accounting period (month) you account for rent.

Balance Sheet or Income Statement?

What are the Accounting Transactions?

1. You purchase $500 of supplies for your business.

2. You consume $100 of supplies during the accounting period.

Balance Sheet or Income Statement?

What are the Accounting Transactions?

1. You purchase a motor for $500 which you will eventually modify (labor only) and sell as the product of your business.

2. You modify a motor, using $100 of labor only, and put it into finished goods waiting to be sold.

3. You sell a modified motor for $1000.

Balance Sheet or Income Statement?

Assessment

• What is the primary difference between the Balance Sheet and the Income Statement?

• Owners Equity is comprised of what two components?

• What is the bottom line of the Income Statement?

• Net Income is the same as __________ ?