mthius ecomony axys report

TRANSCRIPT

8/7/2019 mthius ecomony axys report

http://slidepdf.com/reader/full/mthius-ecomony-axys-report 1/10

The Mauritian Economy

AXYS Stockbroking Ltd July 2010 1

Executive Summary

Eye of the storm

The Mauritian economy in 2009 proved relatively resilient to the global

recession by recording a GDP growth rate of 2.2% (at market prices). Theeconomy derived its strength both from the bold package of policies and

reforms initiated in 2006, and from a timely fiscal stimulus. The worst

affected sectors were textiles and tourism which both recorded contractions

due to a fall in demand; and construction grew at a reduced rate because of

project delays and postponements.

Lying ahead

The July CSO forecast revises the GDP growth rate down from 4.3% to 4.0%

in 2010. Owing to our less optimistic stance on tourism, we expect the figure

to be closer to 3.5%. It is possible for both Textiles and Tourism to record

slight growth due to the statistical effect of a low base, in spite of a double

whammy: weakened EUR and GBP, and slower rate of recovery in theEurozone. The construction sector – boosted by a massive government

infrastructure programme (PSIP) which is facing delays – is set to grow at a

subdued rate for the second straight year. The emerging real estate sector is

a cause for concern with the drying out of buyers for IRS/RES developments

coupled with an unsettling rush into commercial real estate. However, we

expect the financial sector to continue growing at a stable pace driven by

stable banks and global businesses. The sugar industry is expected to record

no growth with harvest at par with the preceding year.

The current account deficit is set to widen due to decreasing export

revenue, and the re-emergence of inflation. According the last monetary

policy committee, inflation has bottomed out and will return to its

historically high levels. As a result, the Bank of Mauritius kept its Repo Rate

unchanged at 5.75%. We believe that unemployment, which stood at 8.3%

in Q1 2010, will hover around the 8.5% mark.

Vicious circle

Export dependent sectors are faced with structural issues that can no longer

be resolved via depreciation. Depreciation results in increased inflation

which leads to demands for wage increase which ultimately results

increased production costs, thereby not resolving the issue. Mauritius needs

to adapt and re-invent itself – as it has done, more than once, in past – in

order to return to sustainable growth path.

CSO (Apr) CSO (Jul)

2007 2008 2009 2010F 2010F

GDP Growth @ Mkt 5.5% 5.1% 2.2% 4.3% 4.0%

Sugar -13.6% 3.7% 15.0% 8.9% 2.3%

Manufacturing 2.2% 3.2% 1.1% 2.1% 1.9%

Textiles 8.5% 0.0% -2.9% 1.0% 1.0%

Financial Intermediation 7.5% 10.8% 4.9% 5.9% 5.9%

Real Estate 7.6% 7.6% 5.9% 5.8% 5.6%

Construction 15.2% 11.1% 6.5% 8.0% 5.0%

Hotels & Restaurants 14.0% 2.7% -5.3% 5.1% 5.1%

Country Information

Appellation: Republic of Mauritius

Independence/Rep.: March 12, 1968/1992

Government: Westminster Dem.

President: Sir Jugnauth, A.

Prime Minister: Dr Ramgoolam, N.

Suffrage: Universal, >18yrs

Off. & Biz. Language: English, French

Geography

Area: 2,040 km2

Excl. economic zone: 1.9M km2

Capital: Port-Louis

Location: 20° 10' S; 57° 30' E

Time Zone: GMT +4 hrs

Climate: Sub-tropical

Tel. country code: 230

Intnet country code: .mu

Demographics

Population: 1,275,000Popn growth rate: 0.5%

Median age: 32 yrs

Life expectancy: 74 yrs

Workforce: 594,000

Unemployment: 8.3%

Literacy: 84.4% (2000)

Poverty: 8% (2006)

Currency

Currency: Mauritian Rupee

Symbol/code: Rs / MUR

Exchange rate: Rs 33 per USD

Rs 41 per EUR

Economy (2009)

GDP growth rate: 2.2%

GDP: Rs 274.8bn

GDP per capita: Rs 215,500

GDP ppp: $ 15.9bn (133rd

)

GDP ppp per capita: $ 12,400 (91st)

Budget deficit: 4.5% of GDP

Public debt: 58.7% of GDP

Current A/C deficit: 7.5% of GDP

Headline Inflation: 2.5%

Net intl reserves: 8.3% of GDP

8/7/2019 mthius ecomony axys report

http://slidepdf.com/reader/full/mthius-ecomony-axys-report 2/10

The Mauritian Economy

AXYS Stockbroking Ltd July 2010 2

Mauritius: A bird’s eye view

Economy

Mauritius is an upper-middle-income (UMI) small-island-

state. From a monocrop-sugar based economy at

independence in 1968, Mauritius has steadily diversified

and opened up its export oriented economy. In 2006,

bolder ongoing economic reforms were initiated in the

wake of the erosion of trade preferences; namely the

Sugar Protocol and the Multi-Fibre Agreement (MFA). The

fruits of these reforms are evidenced by the successful

economic growth and diversification as well as the

improvement in business climate. In just a few years, the

island state sky rocketed to 17th

in 2010 on the World

Bank’s Doing Business Report; thereby making Mauritius1st in Sub-Saharan Africa (ahead of South Africa), and 1st

amongst UMI countries (ahead of Malaysia).

Figure 1. Sectoral breakdown of the Mauritian economy

Government

Mauritius acceded to the status of republic in 1992,

resulting in a president replacing the Queen of England as

the head of state. The president is elected quinquennially

by the National Assembly (Parliament); however all

executive powers reside in the prime minister (PM), who

is elected via universal suffrage for five year terms as per

the Westminster model.

Policy

Recent administrations – including the newly elected one

– have traditionally adopted social agendas, albeit with agradual liberalisation of the economy. The re-elected

government has stated its intention to pursue reforms;

nevertheless, it will back peddle on a couple of unpopular

fiscal measures taken during its previous mandate.

Judicial

The Mauritian legal system was instituted using elements

of both British common law and French civil codes. The

highest institution for judicial proceedings is the Supreme

Court, however the highest court of appeals has remained

the Privy Council of England. The chief justice is appointed

by the president in consultation with the PM.

Developments

In 2009, a specialised Commercial Court was established

for the purpose of expediting the settlement of

commercial disputes.

The Mauritian Economy:

Sector by Sector

Sugar

The Sugar industry is of

paramount historical

importance to the

development of Mauritius. It

was the only pillar of the

domestic economy pre-

independence. Today it

represents a mere 2% of GDP

and employs almost 10% of

the workforce.

The wake-up call

Sugar estates, protected by

trade preferences (Sugar Protocol, Lomé Convention) and

impeded by imposed structural constraints, did not

improve their business model. Precipitated by World

Trade Organisation (WTO) rulings, the European Union

(EU), decided to abolish trade preferences and cease the

purchase of sugar at a hefty premium to market prices.

Reforms

Upon assessment, Mauritius found itself amongst the

least competitive, inefficient, and ineffective sugar

producing countries. Nevertheless the Illovo deal paved

the way for reforms, and it was found that exporting

refined sugar and special sugars moved Mauritius up the

competitive ladder helped by its logistical advantage: anefficient seaport, and short land-base journeys.

8/7/2019 mthius ecomony axys report

http://slidepdf.com/reader/full/mthius-ecomony-axys-report 3/10

The Mauritian Economy

AXYS Stockbroking Ltd July 2010 3

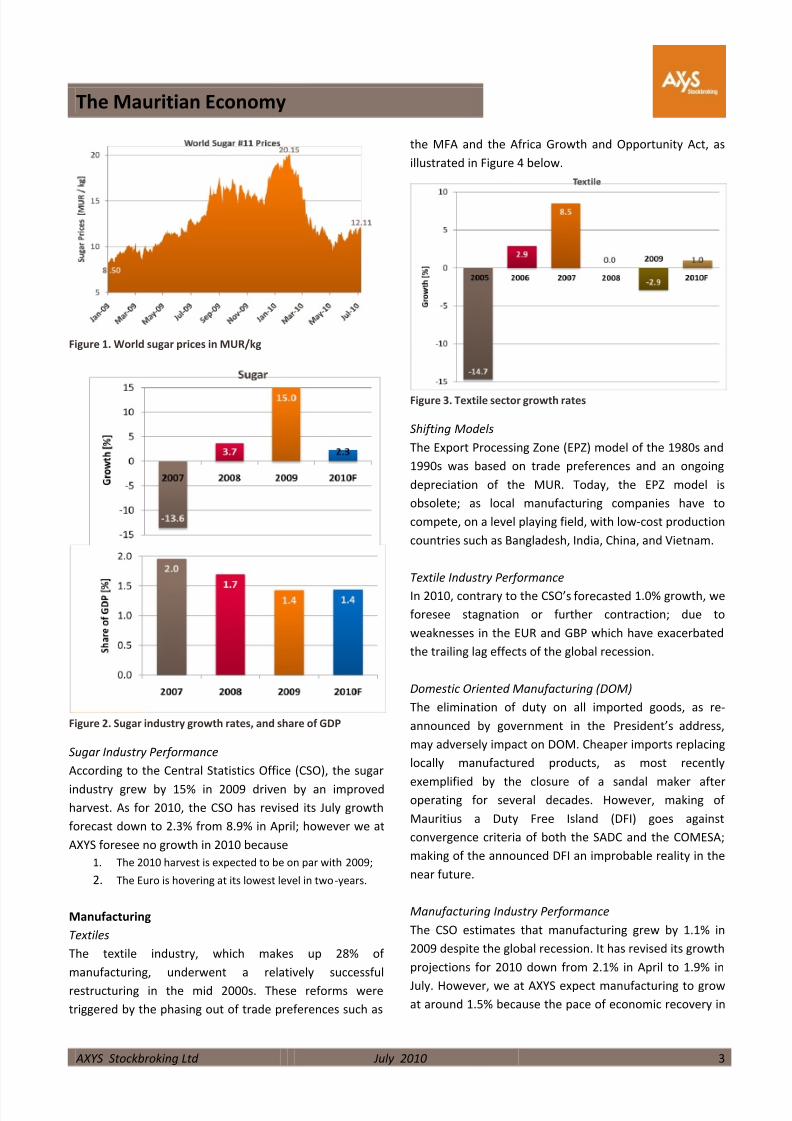

Figure 1. World sugar prices in MUR/kg

Figure 2. Sugar industry growth rates, and share of GDP

Sugar Industry Performance

According to the Central Statistics Office (CSO), the sugar

industry grew by 15% in 2009 driven by an improved

harvest. As for 2010, the CSO has revised its July growth

forecast down to 2.3% from 8.9% in April; however we at

AXYS foresee no growth in 2010 because

1. The 2010 harvest is expected to be on par with 2009;

2. The Euro is hovering at its lowest level in two-years.

Manufacturing

Textiles

The textile industry, which makes up 28% of

manufacturing, underwent a relatively successful

restructuring in the mid 2000s. These reforms were

triggered by the phasing out of trade preferences such as

the MFA and the Africa Growth and Opportunity Act, as

illustrated in Figure 4 below.

Figure 3. Textile sector growth rates

Shifting Models

The Export Processing Zone (EPZ) model of the 1980s and

1990s was based on trade preferences and an ongoing

depreciation of the MUR. Today, the EPZ model is

obsolete; as local manufacturing companies have to

compete, on a level playing field, with low-cost production

countries such as Bangladesh, India, China, and Vietnam.

Textile Industry Performance

In 2010, contrary to the CSO’s forecasted 1.0% growth, we

foresee stagnation or further contraction; due to

weaknesses in the EUR and GBP which have exacerbated

the trailing lag effects of the global recession.

Domestic Oriented Manufacturing (DOM)

The elimination of duty on all imported goods, as re-

announced by government in the President’s address,

may adversely impact on DOM. Cheaper imports replacing

locally manufactured products, as most recently

exemplified by the closure of a sandal maker afteroperating for several decades. However, making of

Mauritius a Duty Free Island (DFI) goes against

convergence criteria of both the SADC and the COMESA;

making of the announced DFI an improbable reality in the

near future.

Manufacturing Industry Performance

The CSO estimates that manufacturing grew by 1.1% in

2009 despite the global recession. It has revised its growth

projections for 2010 down from 2.1% in April to 1.9% in

July. However, we at AXYS expect manufacturing to grow

at around 1.5% because the pace of economic recovery in

8/7/2019 mthius ecomony axys report

http://slidepdf.com/reader/full/mthius-ecomony-axys-report 4/10

The Mauritian Economy

AXYS Stockbroking Ltd July 2010 4

Mauritius’ primary export markets has slowed down since

the Greek bail-out.

Figure 4. Manufacturing sector growth and share of GDP

Financial Intermediation

Over the past decade, Mauritius has slowly but surelydeveloped into a reputable financial centre; albeit, a

conservative one. This traditionalism was demonstrated

by the local banks which did not indulge into asset classes

like the mortgaged-backed securities being at the heart of

Wall Street’s meltdown. A main line of business, other

than banking, is the offshore sector which was recently

renamed the Global Business (GB) sector. Having

graduated to the OECD’s white list , government finds

calling Mauritius a tax haven derogatory.

Global Business

The Mauritian Global Business industry derives its

advantage from the various multilateral, and bilateral

Double Taxation Avoidance (DTA) treaties. Additionally,

fortunate geographical positioning allows Mauritius to

conduct business with Tokyo, Mumbai, London, and New

York, all on the same business day.

DTA with India

Following recent financing scandals in the high-profile

money-minting Indian Premier League (IPL – India’scricket top flight), there was public outcry in India to

review its DTA with Mauritius, as it is believed that some

of the tainted money transited in the domestic GB. If this

DTA were to be amended, it would have a negative impact

on this sector. However, we do not expect any changes in

the DTA with India in the near future because Mauritius

and India share strong diplomatic ties; and also because

Mauritius is a key investment vehicle into India.

Figure 5. Finance growth and share of GDP

Financial Industry Performance

Banking, the financial industry’s primary driver, came out

of the global financial crisis virtually unscathed. The

industry recorded a subdued 4.9% growth rate in 2009,

compared to 10.8% in 2008. With respect to 2010, the

CSO expects a 5.9% growth rate, but we believe the

growth will be similar to 2009 levels due to the reduced

loan book and deposit base growth as recorded by MCB

and SBM.

Real Estate

Real estate has emerged as one of the new pillars of the

economy. The sector took off following the introduction

of Integrated Resort (IRS) and Real Estate Schemes (RES),

where for the first time non citizens were allowed to

purchase property. Additionally, the reduction in sugar

production from over 600kT to about 450kT, has freed up

land for the development of gated communities,

apartments, business parks, and shopping malls. Over the

past three years, the industry has grown at an average of

7.0%.

8/7/2019 mthius ecomony axys report

http://slidepdf.com/reader/full/mthius-ecomony-axys-report 5/10

The Mauritian Economy

AXYS Stockbroking Ltd July 2010 5

Figure 6. Real Estate growth rate and share of GDP

IRS/RES

The über-luxurious IRS/RES property developments are

out of reach for over 99% of the Mauritian population.

Several projects have been placed on hold – following the

collapse of this very sector both in Europe and USA –

because buyers have dried out. A key drawback faced in

selling a luxury villa in Mauritius to a European buyer is

distance; not many are willing to take twelve hour flights

to spend a few days at their vacation home. Proximity to

South Africa is a likely explanation for the high proportion

of South Africans buying such properties. IRS/RES is

unlikely to grow much further, unless high net worth

Asians or Middle Easterners can be attracted.

Business Parks

The emergence of business parks has been a welcomeaddition to the domestic landscape. However, unless the

big banks, major conglomerates, and government services

start relocating outside of Port-Louis, there will be no

momentum for decentralisation. Another factor resides in

the absence of urban planning. Ebène with its awkwardly

designed narrow roads, and a mere few dozen parking

spaces per 10-15 storey skyscrapers is perhaps a wasted

opportunity.

Residential and Commercial Properties

In Mauritius, Singapore or Hong Kong, land is very limited.

It is thus quite natural for property prices to rise as the

island develops. The construction frenzy and boom in

sales of property in the recent past – fuelled by

expatriates being allowed to own property after meeting

select criteria – as well as the soaring prices is reason for

anxiety.

Figure 7. Existing malls depicted in red, & planned malls in blue

Malls in Mauritius

There presently is a commercial property craze. For

instance in the short distance between Phoenix and

Trianon, there already exists three shopping centres, each

with a grocery store, food court and boutiques; yet, there

is

1. a new mall (Centre Point) under construction at

Trianon;

2. a shopping centre planned 0.5km down the M1

towards Ebène; and

3. foundation works have begun on the Mall of Mauritius,

4km down the M1 at Bagatelle.

In addition, malls are being planned at

4. Cascavelle in the west;

5. La Croisette (cost of Rs 2bn) in the north at Grand-

Baie; and a6. Government mandated Waterfront is to be built at Les

Salines (Port-Louis) by an Indian engineering company.

A key question to be asked is whether the Mauritian

consumer has an exponentially expanding purchasing

power; or will these malls further split the existing pie?

Sector Performance

The Real Estate sector grew at a subdued 5.8% in 2009,

with a revised July CSO forecast for 2010 at 5.6%.

However, we anticipate a lower growth of around 5.1% in2010, on the back of fears that the supply/demand

imbalance will be reached sooner rather than later.

8/7/2019 mthius ecomony axys report

http://slidepdf.com/reader/full/mthius-ecomony-axys-report 6/10

The Mauritian Economy

AXYS Stockbroking Ltd July 2010 6

Construction

Construction, so long as government spends as per its

ambitious Public Sector Investment Programme (PSIP),

will grow at an excellent rate, irrespective of the

prevailing economic environment. Thus far, the usual

government-related delays, and complacency have led to

lower than budgeted expenditure. Additionally, the July

CSO national accounts state delays in the PSIP as the

reason for lowering the 2010 growth rate from 8.0% to

5.0%; thereby re-enforcing our views.

Figure 8. Construction growth rate and share of GDP

Road Decongestion Programme

A significant subset of the PSIP involves projects aimed at

road decongestion, most of which were restated during

the President’s Address. These include the extension of

the M2 to Grand Baie, the addition of lanes to the M1between Phoenix and Caudan, the Ring Road, the harbour

(or dream) bridge, and several by-passes including a

highway to circumnavigate Port-Louis. The program

should in theory alleviate traffic, however several hurdles

remain:

The issue is not the number of lanes on the M1 or M2,

but the limited number entry/exit points in and out of

Port-Louis;

There exist squatters connected to the electricity,

water, and sewage grids living on the path of the Ring

Road, ie political will is needed to address theproblem;

Charging toll to use the highways, imply toll plazas

which lead to increased bottle-necks.

Sector Performance

The construction sector has grown at double digit rates in

the recent past driven by the real estate boom and doped

by government spending. Having grown at a reduced 6.5%

in 2009, the CSO has revised the growth rate from 8.0% to

5.0% citing government delays. We concur provided

government does not further delay the PSIP.

Tourism

When supply exceeds demand

The tourism industry currently suffers from a

supply/demand imbalance. Comparing 2009 and 2007

statistics, we observe that arrivals dropped by 4% whilst

bed places increased by 7%. Consequently, lowered room

rates are likely to become a new norm for the medium

term. In addition, a pronounced shift in clientèle away

from 5-Star hotels towards cheaper alternatives has been

reported by all major hotel groups. It is time for the

industry to adapt and adjust, since depreciating the Rupee

is a short-sighted and temporary solution.

Figure 9. Hotels & Restaurants growth and share of GDP

Industry Performance

In 2009, the tourism sector experienced recession

shrinking by 5% due to its vulnerability to exogenous

shocks, as well as its over-concentration on the European

market. The CSO have forecast a 5.1% growth rate in

2010; however we believe it is premature to revise our

tourism paper forecasts (arrivals at 907k, receipts at Rs35bn) upwards until we have seen the results from CY Q2

which englobe the effects of the Icelandic volcanic ash

eruptions, and the low season on the industry.

8/7/2019 mthius ecomony axys report

http://slidepdf.com/reader/full/mthius-ecomony-axys-report 7/10

The Mauritian Economy

AXYS Stockbroking Ltd July 2010 7

Mauritian Economy: macroeconomic issues

Tax Policy

In the recent past, Mauritius has moved towards a low

taxation regime. Corporate, Income, and Value Added(VAT) taxes have all been set at a flat 15%. In spite of

lowered taxes, as a result of improved efficiencies and

reduced tax truancy, fiscal revenue from taxes (both

direct and indirect) have increased.

Revisions

The re-elected government has stated its intent to abolish

two highly unpopular taxes: the first on property and the

second on interest. Contrary to popular belief, the

removal of taxes on interest will not increase savings, as

the deposit base had continued to increase. The heart of

the ‘low-savings’ issue lies with the fact that the CSOamalgamates SMEs and Households into a single entity.

Nonetheless, as a means to make up for lost revenue, the

re-introduction of progressive tax rates is a possibility.

Current Account

Mauritius being a small country, both by surface area, and

domestic market size, it is almost inevitable – because

several specialised industries focused solely on the

domestic market would not be sustainable – that the

country operates under a current account deficit.

Figure 10. Key balances as % of GDP

Expectedly, Mauritian imports exceed exports leading to a

substantial current account deficit. The present current

account deficit is likely to become larger due to the global

recessionary environment affecting key Mauritian export

markets for both exports and tourism. Additionally,

Mauritius as witnessed a steady decline in the level of

exports of goods and services from about 60% of GDP in

the 1990s to under 50% in 2009. Further, imports are due

to become more expensive because of the re-emergence

of inflation.

Foreign Direct Investment (FDI)

FDI levels sky rocketed following reforms leading to the

improvement in business climate, and ease of access to

residency permits. The FDI has been mainly geared

towards Real Estate (IRS/RES), Hotels & Restaurants, and

Financial intermediation.

Figure 11. Evolution of FDI distribution

Figure 12 above suggests that the construction, banking

and tourism sectors have all been doped by FDI during the

last few years, which led to the duly noted high growth

rates. The Rs 8.8bn reached in 2009, compared to the

record Rs 11bn levels reached in 2007 and 2008, is

commendable given the fact that FDI fallout globally was

much more pronounced.

Figure 12. FDI evolution in Mauritius

Monetary Policy

The central bank’s objectives include the promotion of

orderly, balanced development, and monetary policy.

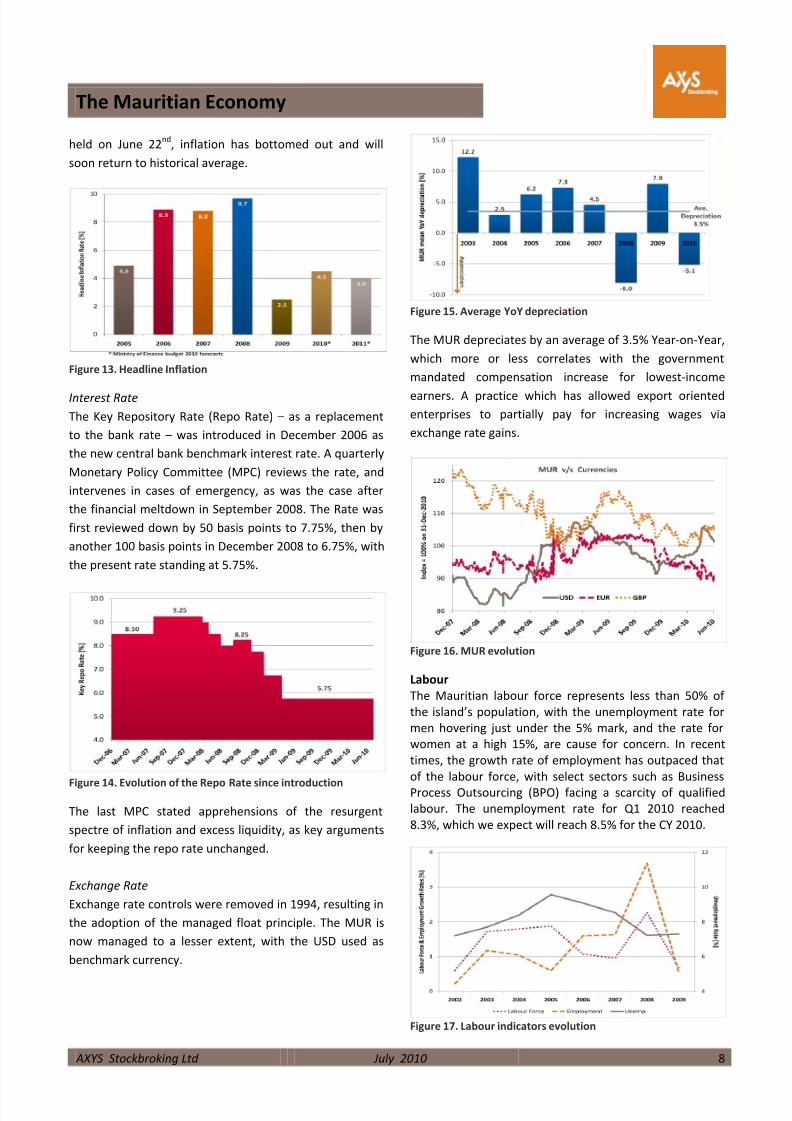

Inflation

The largest driver of domestic inflation is the price of oil;

implying that a shift away from fossil fuels would be a

fundamental way to reduce inflation. The current inflation

rate of 1.8% is at an all time low because the global

recession led to a dramatic fall in commodity prices.

According to the last Monetary Policy Committee (MPC),

8/7/2019 mthius ecomony axys report

http://slidepdf.com/reader/full/mthius-ecomony-axys-report 8/10

The Mauritian Economy

AXYS Stockbroking Ltd July 2010 8

held on June 22nd

, inflation has bottomed out and will

soon return to historical average.

Figure 13. Headline Inflation

Interest Rate

The Key Repository Rate (Repo Rate) – as a replacement

to the bank rate – was introduced in December 2006 as

the new central bank benchmark interest rate. A quarterly

Monetary Policy Committee (MPC) reviews the rate, and

intervenes in cases of emergency, as was the case after

the financial meltdown in September 2008. The Rate was

first reviewed down by 50 basis points to 7.75%, then by

another 100 basis points in December 2008 to 6.75%, with

the present rate standing at 5.75%.

Figure 14. Evolution of the Repo Rate since introduction

The last MPC stated apprehensions of the resurgent

spectre of inflation and excess liquidity, as key arguments

for keeping the repo rate unchanged.

Exchange Rate

Exchange rate controls were removed in 1994, resulting in

the adoption of the managed float principle. The MUR is

now managed to a lesser extent, with the USD used as

benchmark currency.

Figure 15. Average YoY depreciation

The MUR depreciates by an average of 3.5% Year-on-Year,

which more or less correlates with the government

mandated compensation increase for lowest-income

earners. A practice which has allowed export oriented

enterprises to partially pay for increasing wages via

exchange rate gains.

Figure 16. MUR evolution

Labour

The Mauritian labour force represents less than 50% of

the island’s population, with the unemployment rate for

men hovering just under the 5% mark, and the rate for

women at a high 15%, are cause for concern. In recent

times, the growth rate of employment has outpaced that

of the labour force, with select sectors such as Business

Process Outsourcing (BPO) facing a scarcity of qualified

labour. The unemployment rate for Q1 2010 reached

8.3%, which we expect will reach 8.5% for the CY 2010.

Figure 17. Labour indicators evolution

8/7/2019 mthius ecomony axys report

http://slidepdf.com/reader/full/mthius-ecomony-axys-report 9/10

The Mauritian Economy

AXYS Stockbroking Ltd July 2010 9

Drawing Conclusions

The Mauritian economy is dependent on the heath of its

primary export markets for both goods and services,

which are the Eurozone and the UK. Given that their rate

of economic recovery has slowed down following the

sovereign debt problem, coupled with a weakened EUR

and GBP, the local economy is being hit by a double

whammy.

Figure 18. Mauritian GDP growth

The Mauritian economy proved relatively resilient to the

global recession due to the combined effects of the

economic reforms since 2006, and timely policies which

included a stimulus package worth about 4.5% of GDP

that led to a V-shape recovery as evidenced by the SEM-7.

Figure 19. A V-Shaped recovery can be seen on local bourse

Consequently, the economy grew at a reduced 2.2% in

2009, and is expected to grow at 4.0% according to CSO’s

latest forecast. Though, this is a downward revision from

4.3% in April’s projections, we believe this growth rate to

be optimistic because the sugar industry’s woes are not

over, the manufacturing industry’s production costs are

higher than in Asia, and the tourism industry is faced witha lasting supply/demand imbalance.

The above sectors need to make structural changes, as

depreciating the MUR only postpones the problem. In

fact, a weaker MUR would lead to more expensive

imports which in turn lead to high inflation. High inflation

triggers union demands for wage increases which in turn

drive up production costs. Thereby leading to a vicious

circle of depreciation-inflation-compensation without

resolving the initial problem.

Ironically, in the Mauritian context, the financial sector is

presently the healthiest, whilst the emerging Business

Process Outsourcing sector is facing a shortage of skilled

labour, and the commercial real estate sector is in a

frenzy.

The second half of 2010 is expected to remain difficult.

The absence of a clear and coherent economic policy from

the re-elected government may become a hindrance as

simultaneously cutting taxes, increasing spending and

reducing deficit/debt are incompatible. Therefore we

believe that the real GDP growth rate for 2010 will be

closer to 3.5%.

8/7/2019 mthius ecomony axys report

http://slidepdf.com/reader/full/mthius-ecomony-axys-report 10/10

The Mauritian Economy

AXYS Stockbroking Ltd July 2010 10

References

International Monetary Fund, World Economic Outlook ,

April 2010.

World Bank, Mauritius at a Glance, Dec 2009.

African Development Bank, Country Strategy Paper:

Mauritius, May 2009.

Central Intelligence Agency, The World factbook:

Mauritius, June 2010.

US Department of State, 2010 Investment Climate –

Mauritius, March 2010.

Office of the President of the Republic of Mauritius,

Government Programme 2010-2015, June 2010.

Ministry of Finance, Programme Based Budget 2010,

November 2009.

Sithanen, R., Budget Speech 2010, November 2009.

Bank of Mauritius, Monthly Statistical Bulletin, June 2010.

Central Statistical Office, Quarterly National Accounts,

June 2010.

Central Statistical Office, Quarterly National Accounts,

March 2010.

Central Statistical Office, Labour force, Unemployment &Employment , June 2010.

Central Statistical Office, International Travel & Tourism,

May 2010.

Central Statistical Office, External Trade Statistics, June

2010.

Bhavik Desai [email protected]

Vikash Tulsidas [email protected]

AXYS Stockbroking Ltd

Bowen Square, Dr Ferrière Street, Port Louis

Tel: (230) 213 3475 Fax: (230) 213 3478

Email: [email protected]

Url: http://www.axysstockbroking.com

AXYS Stockbroking Ltd has issued this document without consideration of the investment objectives, financial situation or particular needs of any individual recipient.

Recipients should not act or rely on any recommendation in this document without consulting their financial adviser to determine whether the recommendation is

appropriate to their investment of this document. This document is not, and should not be construed as, an offer to sell or the solicitation of an offer to purchase or

subscribe for any investment. This document has been based on information obtained from sources believed to be reliable but which have not been independently

verified. AXYS Stockbroking Ltd makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness. AXYS

Stockbroking Ltd and its officers, directors and representatives may have positions in securities mentioned in this document, or in related investments, and may from time

to time add to or dispose of such securities or investments. AXYS Stockbroking Ltd is a member of the Stock Exchange of Mauritius and is licensed by the Financial Services

Commission.