mtn group limited€¦ · 2 financial review 3 2016 guidance ... nigerian regulatory fine and tower...

TRANSCRIPT

MTN Group Limited

Results presentation for the six month period ended 30 June 2016

AGENDA

1 Strategic and

operational update

2 Financial review

3 2016 Guidance

4 Key matters and

immediate priorities

Strategic and operational update

4

Performance reflects a confluence of material issues which created a ‘perfect storm’

Group financial results for the six months ended 30 June 16

On 10 June MTN settled Nigerian regulatory fine with Federal Government of Nigeria

MTN to pay 330 billion naira (USD 1.67 billion) over three years in full and final settlement, in addition

to complying with certain other regulatory conditions

50 billion naira (USD 250 million) paid on 24 February 2016 forms part of the monetary component of

the settlement

June 2016, first schedule of 30 billion naira paid (USD 124 million)

Accrued present value of remaining, 280 billion naira (USD 1.42 billion)

Impact

- EBITDA: negative re-measurement impact of R10 499 million (provision R9 287m made in H2 15)

- Headline earnings: R8 632 million

- HEPS: 474 cents

- Cash flow: R 5 870 million

Nigeria fine

settlement;

significant

negative

impact on

results

STRATEGIC AND

OPERATIONAL UPDATE

5

A challenging operating environment

Source of GDP growth: IMF

Slowing reliant economies, regulatory pressure and tough competition

1.3 2.70.0

3.55.9

8.6

5.0

0.1

-1.8

4.0 4.5 4.9

8.5

5.3

6.5

10.48.9

15.7

2.2 2.1

6.7

-4

0

4

8

12

16

20

South Africa Nigeria Iran Ghana Cameroon Ivory Coast Uganda

The economic landscape in key MTN markets (%)

2015 GDP 2016 GDP f/c Inflation 2016 f/c

Key

challenges

impacted

growth

Depreciation in local currencies resulted in higher US dollar expenses

Forex losses of R3 606 million

Liquidity constraints impacting repatriation of funds from Nigeria

Weak macro economic conditions in most markets resulted in lower consumer spending

Negative GDP growth in South Africa and Nigeria expected in 2016, our two largest markets

Regulatory pressure, notably withdrawal of regulatory services in Nigeria until May 2016

7.5 million disconnected of subscribers – registration requirements in Nigeria, Uganda and Cameroon

(approximately 18 million since October 15)

STRATEGIC AND

OPERATIONAL UPDATE

6Note: Results are presented based on operational performance (excluding hyperinflation, Nigerian regulatory fine and tower profits)

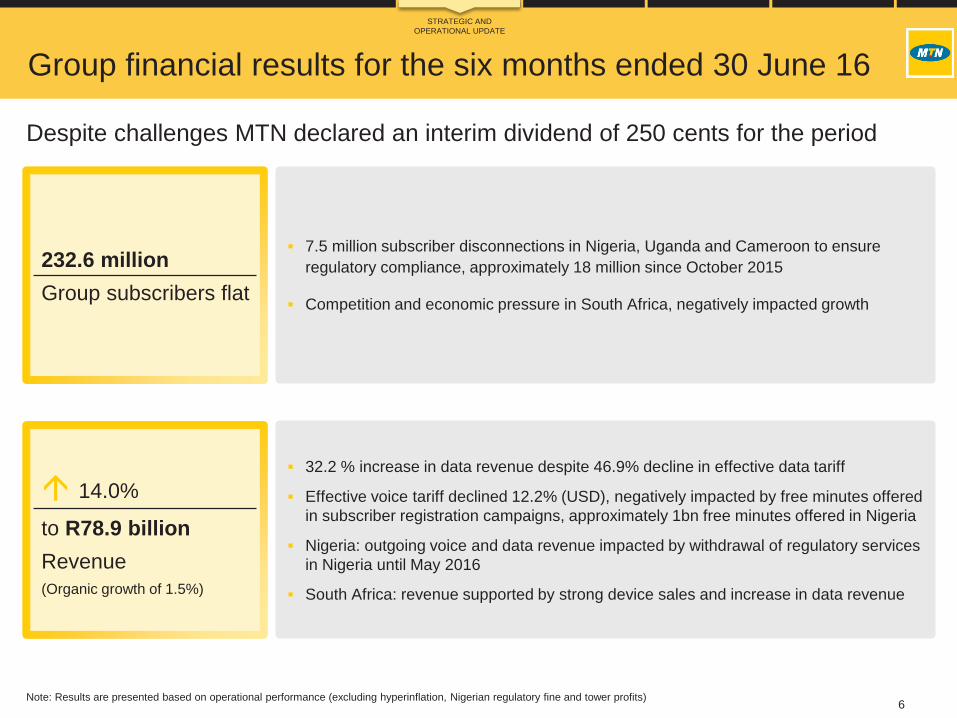

Despite challenges MTN declared an interim dividend of 250 cents for the period

Group financial results for the six months ended 30 June 16

STRATEGIC AND

OPERATIONAL UPDATE

7.5 million subscriber disconnections in Nigeria, Uganda and Cameroon to ensure

regulatory compliance, approximately 18 million since October 2015

Competition and economic pressure in South Africa, negatively impacted growth

232.6 million

Group subscribers flat

14.0%

to R78.9 billion

Revenue

(Organic growth of 1.5%)

32.2 % increase in data revenue despite 46.9% decline in effective data tariff

Effective voice tariff declined 12.2% (USD), negatively impacted by free minutes offered

in subscriber registration campaigns, approximately 1bn free minutes offered in Nigeria

Nigeria: outgoing voice and data revenue impacted by withdrawal of regulatory services

in Nigeria until May 2016

South Africa: revenue supported by strong device sales and increase in data revenue

7

Group financial results for the six months ended 30 June 16

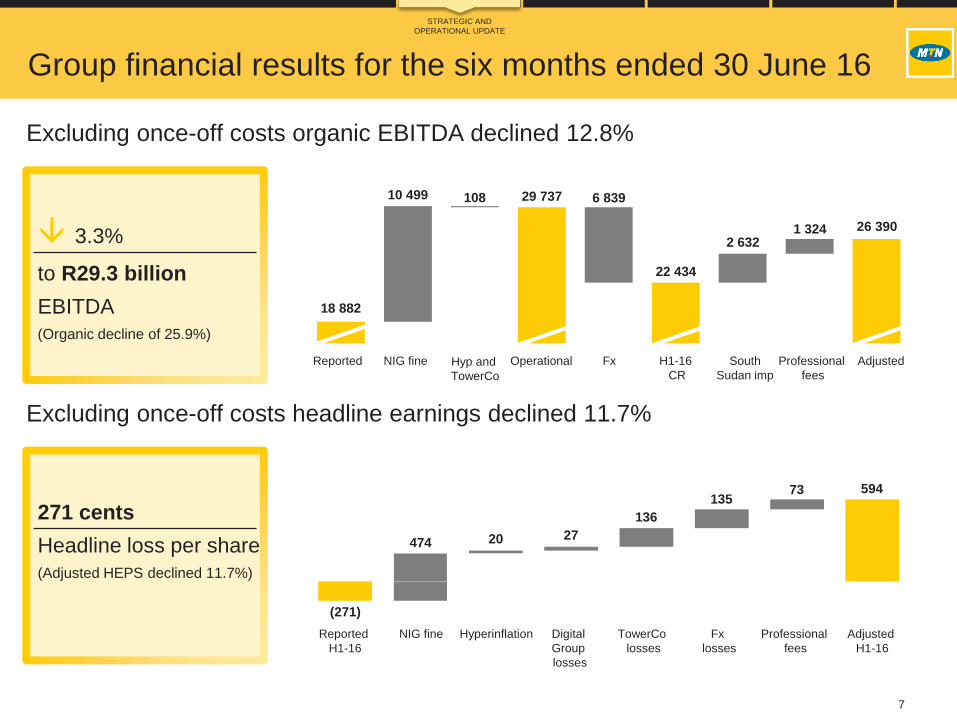

Excluding once-off costs organic EBITDA declined 12.8%

Excluding once-off costs headline earnings declined 11.7%

STRATEGIC AND

OPERATIONAL UPDATE

3.3%

to R29.3 billion

EBITDA

(Organic decline of 25.9%)

271 cents

Headline loss per share

(Adjusted HEPS declined 11.7%)

NIG fine Professional

fees

Operational AdjustedReported Fx H1-16

CR

South

Sudan imp

18 882

10 499 108 29 737 6 839

22 434

2 6321 324 26 390

NIG fine Digital

Group

losses

Adjusted

H1-16

Reported

H1-16

TowerCo

losses

Fx

losses

Professional

fees

Hyperinflation

(271)

474 20 27

136

13573 594

Hyp and

TowerCo

8

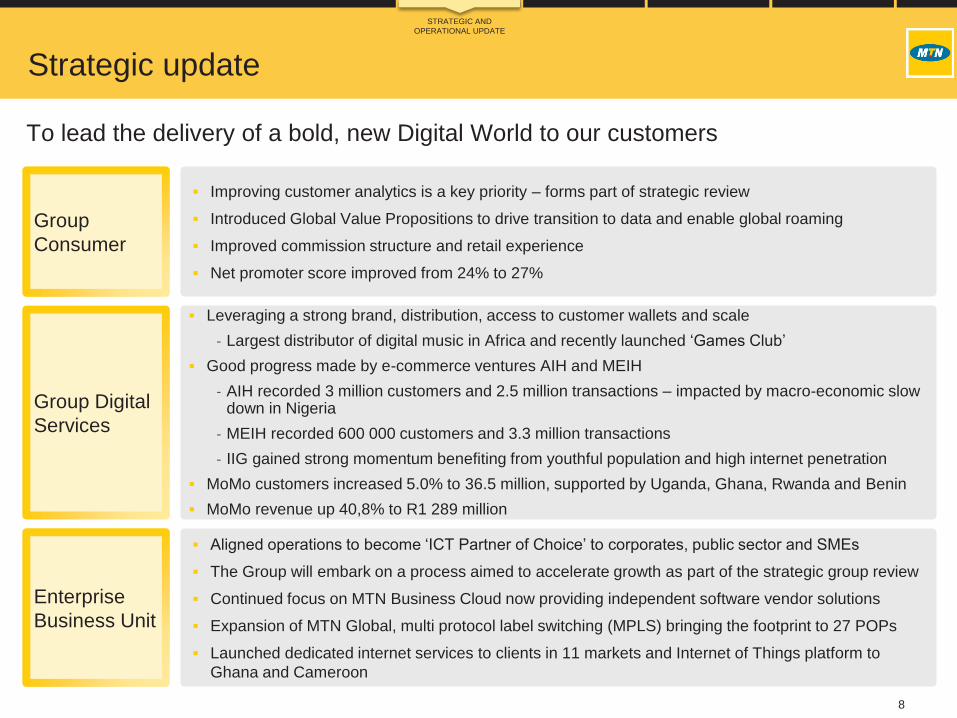

To lead the delivery of a bold, new Digital World to our customers

Strategic update

Group

Consumer

Improving customer analytics is a key priority – forms part of strategic review

Introduced Global Value Propositions to drive transition to data and enable global roaming

Improved commission structure and retail experience

Net promoter score improved from 24% to 27%

Group Digital

Services

Leveraging a strong brand, distribution, access to customer wallets and scale

- Largest distributor of digital music in Africa and recently launched ‘Games Club’

Good progress made by e-commerce ventures AIH and MEIH

- AIH recorded 3 million customers and 2.5 million transactions – impacted by macro-economic slow down in Nigeria

- MEIH recorded 600 000 customers and 3.3 million transactions

- IIG gained strong momentum benefiting from youthful population and high internet penetration

MoMo customers increased 5.0% to 36.5 million, supported by Uganda, Ghana, Rwanda and Benin

MoMo revenue up 40,8% to R1 289 million

Enterprise

Business Unit

Aligned operations to become ‘ICT Partner of Choice’ to corporates, public sector and SMEs

The Group will embark on a process aimed to accelerate growth as part of the strategic group review

Continued focus on MTN Business Cloud now providing independent software vendor solutions

Expansion of MTN Global, multi protocol label switching (MPLS) bringing the footprint to 27 POPs

Launched dedicated internet services to clients in 11 markets and Internet of Things platform to

Ghana and Cameroon

STRATEGIC AND

OPERATIONAL UPDATE

9

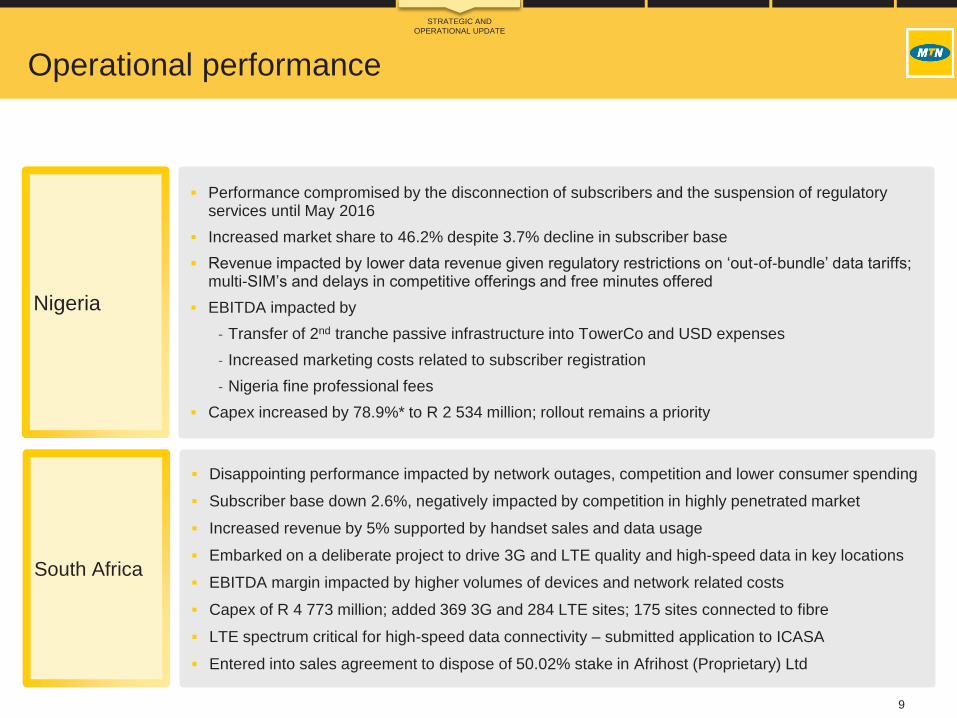

Operational performance

Performance compromised by the disconnection of subscribers and the suspension of regulatory services until May 2016

Increased market share to 46.2% despite 3.7% decline in subscriber base

Revenue impacted by lower data revenue given regulatory restrictions on ‘out-of-bundle’ data tariffs; multi-SIM’s and delays in competitive offerings and free minutes offered

EBITDA impacted by

- Transfer of 2nd tranche passive infrastructure into TowerCo and USD expenses

- Increased marketing costs related to subscriber registration

- Nigeria fine professional fees

Capex increased by 78.9%* to R 2 534 million; rollout remains a priority

Disappointing performance impacted by network outages, competition and lower consumer spending

Subscriber base down 2.6%, negatively impacted by competition in highly penetrated market

Increased revenue by 5% supported by handset sales and data usage

Embarked on a deliberate project to drive 3G and LTE quality and high-speed data in key locations

EBITDA margin impacted by higher volumes of devices and network related costs

Capex of R 4 773 million; added 369 3G and 284 LTE sites; 175 sites connected to fibre

LTE spectrum critical for high-speed data connectivity – submitted application to ICASA

Entered into sales agreement to dispose of 50.02% stake in Afrihost (Proprietary) Ltd

Nigeria

South Africa

STRATEGIC AND

OPERATIONAL UPDATE

10

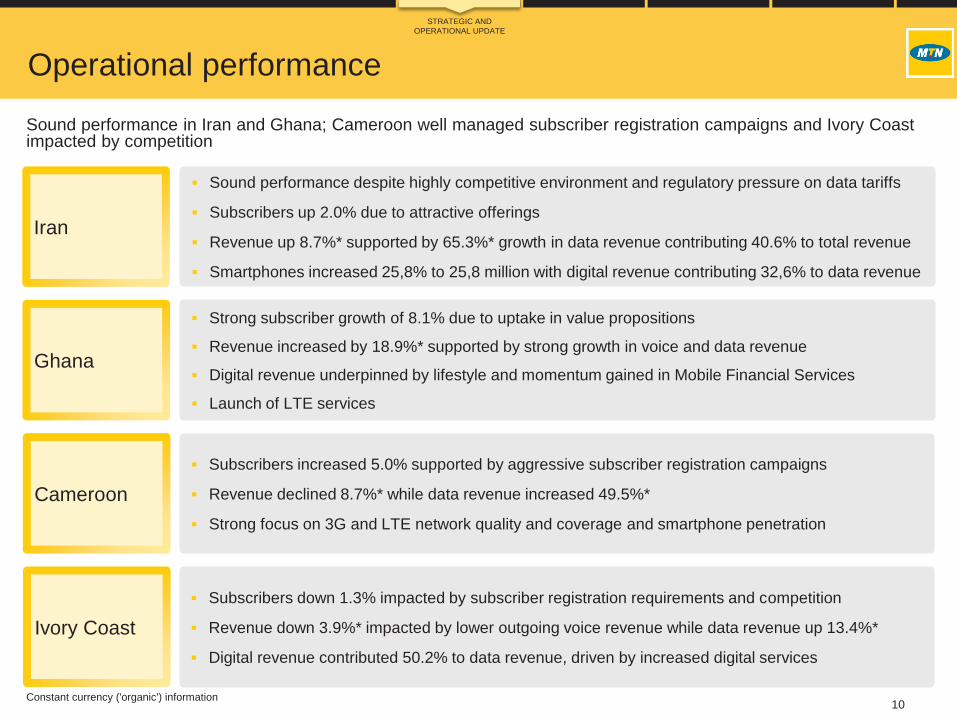

Sound performance in Iran and Ghana; Cameroon well managed subscriber registration campaigns and Ivory Coast impacted by competition

Operational performance

Sound performance despite highly competitive environment and regulatory pressure on data tariffs

Subscribers up 2.0% due to attractive offerings

Revenue up 8.7%* supported by 65.3%* growth in data revenue contributing 40.6% to total revenue

Smartphones increased 25,8% to 25,8 million with digital revenue contributing 32,6% to data revenue

Iran

Ghana

Cameroon

Ivory Coast

Strong subscriber growth of 8.1% due to uptake in value propositions

Revenue increased by 18.9%* supported by strong growth in voice and data revenue

Digital revenue underpinned by lifestyle and momentum gained in Mobile Financial Services

Launch of LTE services

Subscribers increased 5.0% supported by aggressive subscriber registration campaigns

Revenue declined 8.7%* while data revenue increased 49.5%*

Strong focus on 3G and LTE network quality and coverage and smartphone penetration

Subscribers down 1.3% impacted by subscriber registration requirements and competition

Revenue down 3.9%* impacted by lower outgoing voice revenue while data revenue up 13.4%*

Digital revenue contributed 50.2% to data revenue, driven by increased digital services

STRATEGIC AND

OPERATIONAL UPDATE

Constant currency ('organic') information

Financial review

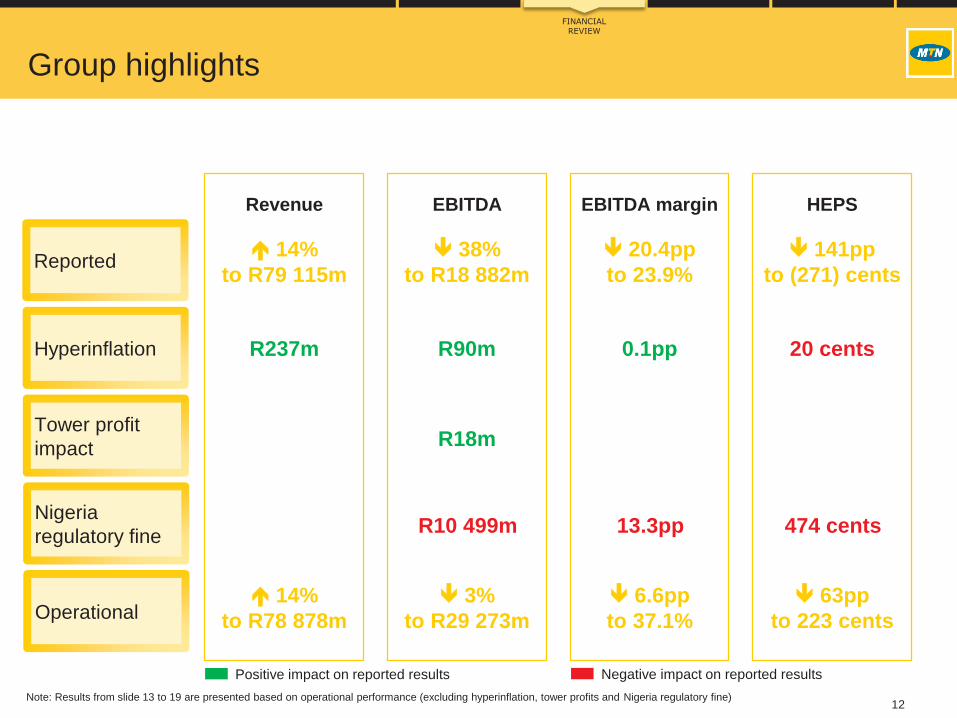

12Note: Results from slide 13 to 19 are presented based on operational performance (excluding hyperinflation, tower profits and Nigeria regulatory fine)

Group highlights

14%

to R79 115m

38%

to R18 882m

20.4pp

to 23.9%

141pp

to (271) cents

R237m R90m 0.1pp 20 cents

R18m

14%

to R78 878m

3%

to R29 273m

6.6pp

to 37.1%

63pp

to 223 cents

Revenue EBITDA EBITDA margin HEPS

Reported

Hyperinflation

Tower profit

impact

Nigeria

regulatory fine

Operational

R10 499m 13.3pp 474 cents

Positive impact on reported results Negative impact on reported results

FINANCIAL REVIEW

13

* EBITDA less capex (approximates free cash flow)

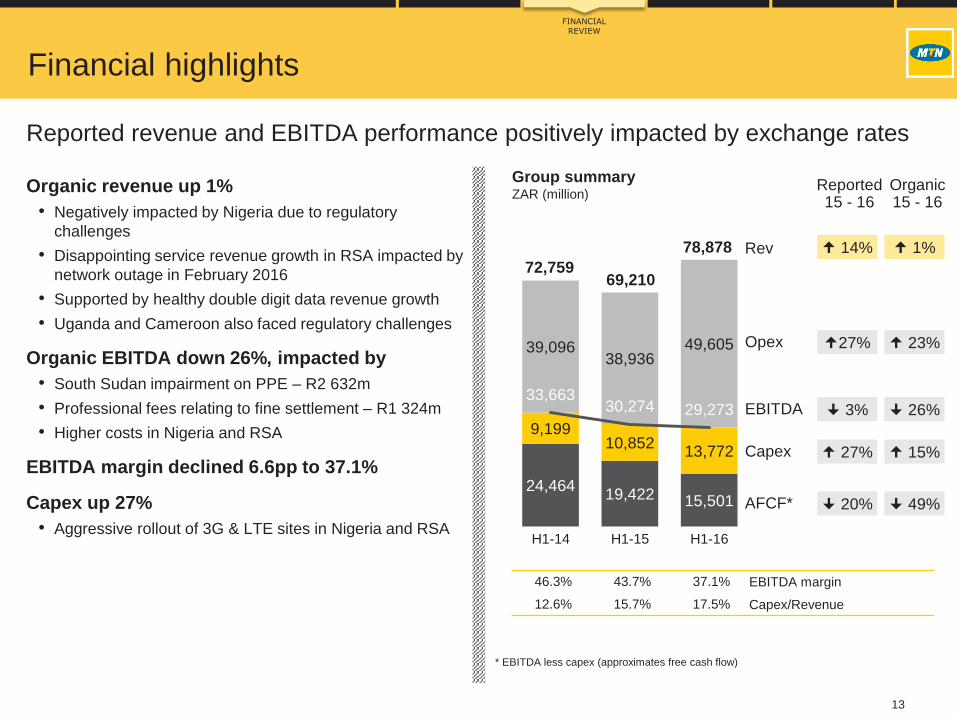

Financial highlights

Organic revenue up 1%

• Negatively impacted by Nigeria due to regulatory

challenges

• Disappointing service revenue growth in RSA impacted by

network outage in February 2016

• Supported by healthy double digit data revenue growth

• Uganda and Cameroon also faced regulatory challenges

Organic EBITDA down 26%, impacted by

• South Sudan impairment on PPE – R2 632m

• Professional fees relating to fine settlement – R1 324m

• Higher costs in Nigeria and RSA

EBITDA margin declined 6.6pp to 37.1%

Capex up 27%

• Aggressive rollout of 3G & LTE sites in Nigeria and RSA

Reported revenue and EBITDA performance positively impacted by exchange rates

24,464 19,422 15,501

9,199 10,852

13,772

39,096 38,936

49,605

72,75969,210

78,878

33,66330,274 29,273

H1-14 H1-15 H1-16

46.3% 43.7% 37.1% EBITDA margin

12.6% 15.7% 17.5% Capex/Revenue

Rev

Opex

EBITDA

Capex

AFCF*

14%

27%

3%

27%

20%

1%

23%

26%

15%

49%

Reported15 - 16

Organic15 - 16

Group summary ZAR (million)

FINANCIAL REVIEW

14

H1-16 CR is at constant prior year FX rate HOE – Head office companies and eliminations

Revenue

Impacted by a decline in outgoing voice revenue growth

Outgoing revenue up 8% (organic down 5%), negatively impacted by

• Muted subscriber growth to 232.6m – disconnections in Nigeria, Cameroon and Uganda impacted by registration requirements

• Withdrawal of regulatory services in Nigeria until May

• Network outages and increased post-paid churn in RSA

• Effective tariff down 21.7% (organic down 12.2%), impacted by competition

• Billable MOU up 8% – driven by free minutes

Data revenue up 32% (organic up 20%)

• Healthy double digit growth in majority of the markets

• Nigeria impacted by restrictions on out-of-bundle rates

Devices revenue up 34% (organic up 36%)

• RSA contributes 86%, handset revenue up 33%

• Number of prepaid handsets sold 3.2m (up 33%) post-paid 641k (up 41%)

Incoming voice revenue up 13% (organic down 3%)

• Decline in MTR

• Group incoming minutes remained flat

Revenue breakdownZAR (million)

69 210

FINANCIAL REVIEW

RSA H1-16

CR

NIG FX H1-16H1-15 Other

WECA

MENA HOEOther

SEA

959

909 1 190

215 125 12 70 240

8 638 78 878

+13%

Revenue breakdown per category(%) Data

25% Incoming voice10%

Outgoing57%

SMS2%

Devices5%

Other1%

15

H1-16 CR is at constant prior year FX rate HOE – Head office companies and eliminations

Revenue – data

Increased data revenue contribution at 25%

Data revenue up 32% (organic up 20%)

• Strong data revenue growth despite 59% decline in data

tariff (organic decline 47%)

• Continued improvements of 3G and LTE networks across

operations (data traffic up 135%)

• Increased device penetration (no. of smartphones on

network up 26%)

• Increased contribution from digital service revenue

Nigeria data revenue

• Impacted by regulatory restrictions on “out of bundle” data

tariffs

Digital and MFS services revenue contributed

32% to data revenue

• Increased up-take in lifestyle content

• Continued growth in MFS

Data revenueZAR (million)

FINANCIAL REVIEW

15 013

1 089469 125

1 071465 12 17 970

1 879 19 849

RSA H1-16

CR

NIG FX H1-16H1-15 Other

WECA

MENA HOEOther

SEA

+12.5%

Access data58%

VAS4%

ICT6%

Digital26%

MFS6%

Data breakdown per category(%)

16* Organic growth

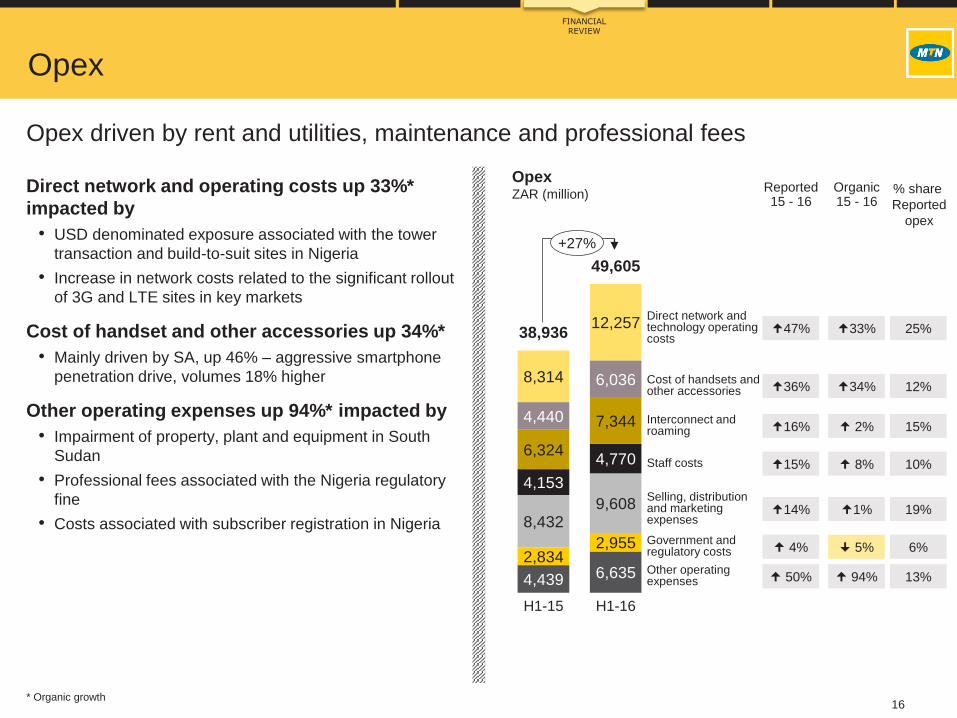

Opex

Direct network and operating costs up 33%*

impacted by

• USD denominated exposure associated with the tower

transaction and build-to-suit sites in Nigeria

• Increase in network costs related to the significant rollout

of 3G and LTE sites in key markets

Cost of handset and other accessories up 34%*

• Mainly driven by SA, up 46% – aggressive smartphone

penetration drive, volumes 18% higher

Other operating expenses up 94%* impacted by

• Impairment of property, plant and equipment in South

Sudan

• Professional fees associated with the Nigeria regulatory

fine

• Costs associated with subscriber registration in Nigeria

Opex driven by rent and utilities, maintenance and professional fees

4,439 6,635 2,834

2,955

8,432 9,608

4,153

4,770 6,324

7,344 4,440

6,036 8,314

12,257 38,936

49,605

H1-15 H1-16

Direct network and technology operating costs

Cost of handsets and other accessories

Interconnect and roaming

Staff costs

Selling, distribution and marketing expenses

Other operating expenses

+27%

OpexZAR (million)

Government and regulatory costs

FINANCIAL REVIEW

33%

34%

2%

8%

1%

5%

94%

Organic15 - 16

25%

12%

15%

10%

19%

6%

13%

% share

Reported

opex

47%

36%

16%

15%

14%

4%

50%

Reported15 - 16

17

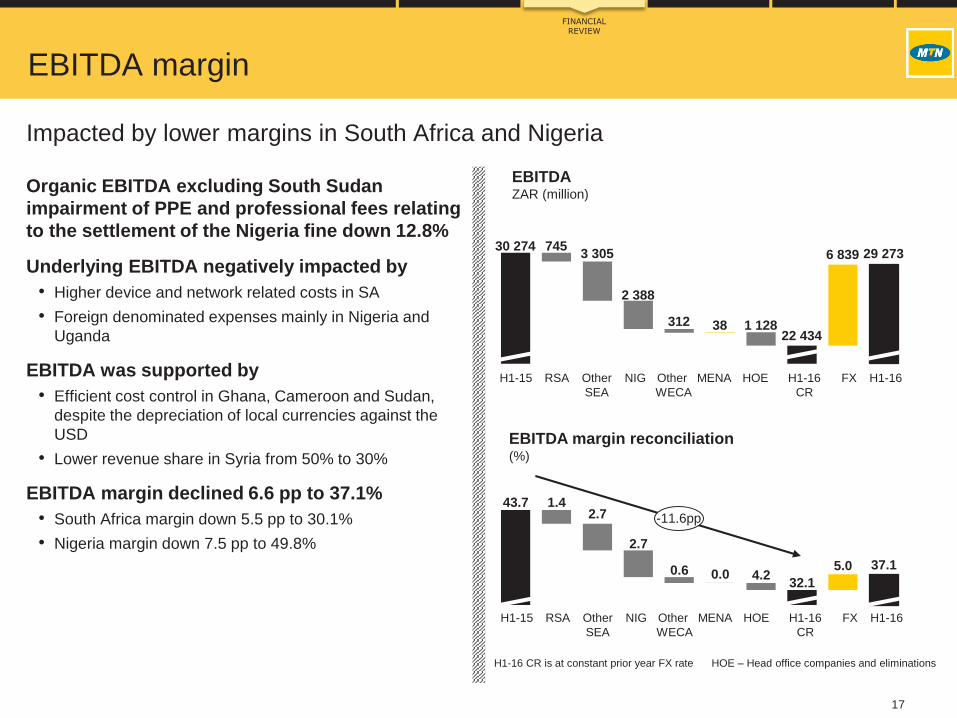

EBITDA margin

H1-16 CR is at constant prior year FX rate HOE – Head office companies and eliminations

Impacted by lower margins in South Africa and Nigeria

Organic EBITDA excluding South Sudan

impairment of PPE and professional fees relating

to the settlement of the Nigeria fine down 12.8%

Underlying EBITDA negatively impacted by

• Higher device and network related costs in SA

• Foreign denominated expenses mainly in Nigeria and

Uganda

EBITDA was supported by

• Efficient cost control in Ghana, Cameroon and Sudan,

despite the depreciation of local currencies against the

USD

• Lower revenue share in Syria from 50% to 30%

EBITDA margin declined 6.6 pp to 37.1%

• South Africa margin down 5.5 pp to 30.1%

• Nigeria margin down 7.5 pp to 49.8%

EBITDAZAR (million)

FINANCIAL REVIEW

RSA H1-16

CR

NIG FX H1-16H1-15 Other

WECA

MENA HOEOther

SEA

30 274 7453 305

2 388

312 38 1 12822 434

6 839 29 273

EBITDA margin reconciliation(%)

43.7 1.42.7

2.7

0.6 0.0 4.232.1

5.0 37.1

RSA H1-16

CR

NIG FX H1-16H1-15 Other

WECA

MENA HOEOther

SEA

-11.6pp

18

Finance cost

Net interest paid more than doubled to

ZAR 1 855m

• Increase in net debt by 187%: ZAR 49.3bn (H1-15: ZAR

17.2bn)

Forex loss ZAR 3 606m impacted by fx

movements

• Nigeria losses mainly due to USD denominated

intercompany loans and third party payables

• Mauritius forex losses mainly on Iran receivables

• South Sudan forex losses mainly on USD third party trade

payables

• Sudan forex losses on settlement of USD denominated

third party trade payables

• RSA forex losses on derivatives hedging foreign payables

Impacted by higher net interest paid and fx losses

H1-16 H1-15 H1-14

Net interest paid 1 855 839 932

Net forex losses 3 606 1 481 736

Total 5 461 2 320 1 668

H1-16 H1-15 H1-14

Nigeria 1 124 769 129

Mauritius 1 078 253 104

South Sudan 408 - 19

Sudan 395 (83) (4)

RSA 178 77 54

Manco 141 (4) (3)

Other 282 469 437

Total 3 606 1 481 736

Net finance costZAR (million)

Net forex losses/(gains)ZAR (million)

FINANCIAL REVIEW

19

Taxation

(461) (472)(1 573)

6 6725 672 5 661

1,042

1,023 606

7 253

6 2234 694

H1-14 H1-15 H1-16

Normalised Group effective tax rate of 49.2%

(H1-15: 32.9%)

• Reported group effective tax rate impacted by the Nigeria

regulatory fine and hyperinflation

• Normalised group effective tax rate impacted by lower

PBT due to

- Decrease in equity income from joint ventures and

associates

- Nigeria professional fees

- South Sudan unrealised forex losses and PPE

impairment and

- Conakry goodwill impairment

Normalised withholding tax

• 6.3% (prior year 5.4%) – WHT is lower than prior year in

absolute terms due to lower dividends up-streamed

Current tax

• Current tax largely unchanged

Deferred tax – income statement

• Nigeria unrealised forex losses on USD denominated

intercompany loans and third party payables

-14%-25%

TaxZAR (million)

Normal taxDef taxWHT

31.5% 32.9% 49.2% Eff tax rate %

FINANCIAL REVIEW

Share of

results JVs

and assoc

Forex

losses

S Sdn

Adj eff

tax rate

Eff

Tax rate

Goodwill

impairment

PPE

impairment

S Sdn

Professional

fees

NIG

49.2 9.6

3.41.3 1.2 0.7 33.0

-16.2pp

Group effective taxZAR (million)

20

ZAR (million) H1-16 H1-15 Change %

Revenue 79 115 69 304 14

Other income 367 411 (11)

COS and operating expenses 50 101 39 040 28

EBITDA before Nigeria regulatory fine 29 381 30 675 (4)

Nigeria regulatory fine 10 499 - 100

EBITDA 18 882 30 675 (38)

Depreciation, amortisation and impairment of goodwill 13 691 10 750 27

Profit from operations 5 191 19 925 (74)

Net finance cost 5 945 2 319 156

Share of results from joint ventures and associates after tax (1 692) 2 027 (184)

Net monetary gain 919 496 85

(Loss)/profit before tax (1 527) 20 129 (108)

Income tax expense 4 726 6 249 (24)

(Loss)/profit after tax (6 253) 13 880 (145)

Non-controlling interests (764) 1 980 (139)

Attributable (loss)/profit (5 489) 11 900 (146)

Income statement (IFRS)

Impacted by losses from JV’s and fx

FINANCIAL REVIEW

21

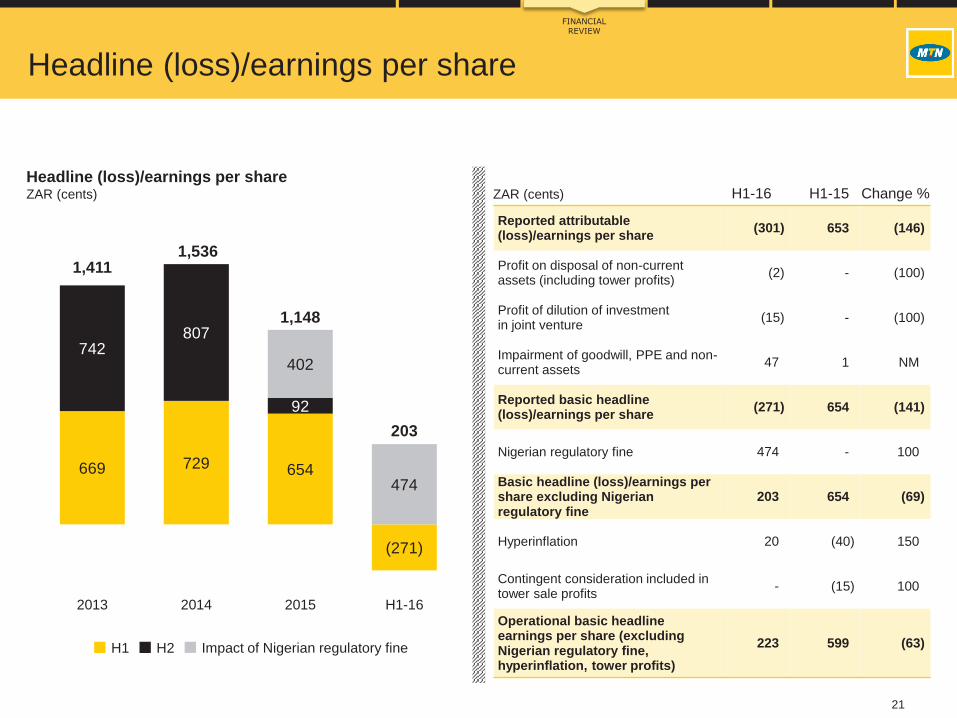

669 729 654

(271)

742807

92

402

474

1,4111,536

1,148

203

2013 2014 2015 H1-16

Headline (loss)/earnings per share

H1-16 H1-15 Change %

Reported attributable (loss)/earnings per share

(301) 653 (146)

Profit on disposal of non-current assets (including tower profits)

(2) - (100)

Profit of dilution of investment in joint venture

(15) - (100)

Impairment of goodwill, PPE and non-current assets

47 1 NM

Reported basic headline (loss)/earnings per share

(271) 654 (141)

Nigerian regulatory fine 474 - 100

Basic headline (loss)/earnings per share excluding Nigerian regulatory fine

203 654 (69)

Hyperinflation 20 (40) 150

Contingent consideration included in tower sale profits

- (15) 100

Operational basic headline earnings per share (excluding Nigerian regulatory fine, hyperinflation, tower profits)

223 599 (63)

Headline (loss)/earnings per shareZAR (cents) ZAR (cents)

FINANCIAL REVIEW

Impact of Nigerian regulatory fineH1 H2

22

5,979 6,8808,225 8,808

4,585

9,362

12,302

14,69415,2192,088

2,422

17,429

19,182

25,34124,027

4,585

2012 2013 2014 2015 H1-16

H1 H2 Share buy back

Shareholder returns

Dividends

• Interim dividend 250cps, 48% decline

Share buy-backs

• H2-11 repurchased 6.8m shares (ZAR 930m)

• H1-12 repurchased 15.6m shares (ZAR 2.1bn)

• H2-14 repurchased 10.7m shares (ZAR 2.4bn)

• Total repurchase of 1.8% of issued shares since 2011

Dividends and share buy-backsZAR (million)

FINANCIAL REVIEW

23

ZAR (million) 2016 Dec 2015

Property, plant and equipment 93 462 106 702

Goodwill and other intangible assets 52 172 55 887

Other non-current assets 54 813 55 846

Cash 26 955 34 177

Current assets* 55 513 61 255

Total assets 282 915 313 867

Total equity 119 796 151 838

Interest-bearing liabilities 81 947 75 171

Other liabilities 81 172 86 858

Total liabilities 163 119 162 029

Total equity and liabilities 282 915 313 867

Net debt 49 257 31 635

Annualised net debt/EBITDA excluding Nigerian regulatory fine 0.83 0.46

ZAR strengthened against most other African currencies (Naira 50%, Cedi 4%, Uganda Shilling 7% and Syrian Pound 52%) since Dec 2015

*Includes foreign currency deposits of ZAR 1 123m (Dec 2015 ZAR 428m), treasury bills and commercial papers of ZAR 3 926m (Dec 2015 ZAR 7 196m) and bonds of ZAR 49m (Dec 2015 ZARnil)

Statement of financial position (IFRS)

Total assets impacted by FCTR

FINANCIAL REVIEW

24

ZAR (million) H1-16 H1-15 Change %

Cash generated from operations^ 23 870 26 289 (9)

Dividends paid to equity holders of the Company (15 212) (14 697) (4)

Dividends paid to non-controlling interests (790) (3 042) 74

Dividends received from associates and joint ventures 426 285 49

Net interest paid (2 143) (934) (129)

Tax paid (6 587) (6 469) (2)

Cash (used in)/generated from operating activities (436) 1 432 (130)

Acquisition of property, plant and equipment and intangible assets (14 024) (11 830) (19)

Movement in investments and other investing activities (185) (2 641) 93

Cash used in investing activities (14 209) (14 471) 2

Cash generated by financing activities 13 608 1 558 NM

Cash and cash equivalents at the beginning of the year 34 139 43 072 (21)

Effect of exchange rates on cash and equivalents (6 272) (787) NM

Net monetary gain on cash and cash equivalents 107 134 (20)

Cash and cash equivalents at the end of the year* 26 937 30 938 (13)

^Cash generated from operations decreased by R2.4bn mainly as a result of Nigerian payments on regulatory fine (R5.9bn)* Includes bank overdraft of R18m (H1-15: R76m)

Statement of cash flows (IFRS)

Impacted by R5.9bn payment made on Nigerian regulatory fine

FINANCIAL REVIEW

2016 Guidance

26

(‘000)

Guidanceprovided

March 2016

Updated guidance

June 2016

SEA 3 515 1 850

South Africa 1 100 1 100

Uganda 1 800 950

Other 615 (200)

WECA 6 825 4 725

Nigeria 3 500 800

Ghana 1 100 1 800

Cameroon 1 000 1 000

Ivory Coast 400 475

Other 825 650

MENA 1 610 1 500

Iran 1 100 1 500

Syria - (100)

Sudan 350 400

Other 160 (300)

Total 11 950 8 075

Net additions guidance

Guidance 2016

2016

GUIDANCE

27

ZAR (million)

Authorised

2016

Capitalised

June 2016

Capitalised

June 2015

SEA 13 548 5 626 5 896

South Africa 11 280 4 773 4 678

Uganda 807 364 556

Other 1 461 489 662

WECA 16 162 6 975 3 652

Nigeria 11 130 2 534 1 172

Ghana 1 258 1 646 355

Cameroon 1 157 1 121 943

Ivory Coast 815 842 422

Other 1 802 832 760

MENA 3 539 1 064 732

Syria# 1 543 191 56

Sudan# 1 280 549 337

Other 716 324 339

Head office companies and eliminations 1 865 107 572

Total 35 114 13 772 10 852

Hyperinflation - 78 17

Total reported 35 114 13 850 10 869

Iran (49%)# 3 518 2 313 1 854

#Excluding hyperinflation

Capex guidance

2016

GUIDANCE

Key matters and immediate priorities

29

Appointment of the right CEO to take MTN forward into new growth phase

Key matters and immediate priorities

VP’s to strengthen management team, further changes to be completed by year-end

More in-depth commercial, risk and governance skills and experience

KEY MATTERS AND

IMMEDIATE PRIORITIES

New Group

CEO

Appointment of Rob Shuter, new Group president and CEO, as soon as practically possible in 2017 (no later than July 2017)

Brings extensive experience in Africa and Europe – previously CEO Vodafone Europe cluster

In the interim, Phuthuma to hand over more operational responsibility to key executives

High calibre

Management

team

Stephen van Coller, VP for M&A and strategy

Godfrey Motsa, VP for SEA region (excluding South Africa)

Gunter Engling to act as CFO, following the resignation of Brett Goschen

Babak Fouladi, Group CTIO and CTO of South Africa for 12 months

Phuthuma Nhleko to revert to non-executive Chairman role as soon as Rob Shuter joins the Group

Refreshed

composition

of the board

Stan Miller, Paul Hanratty and Nkululeko “Nkunku” Sowazi appointed to Group board

Mike Harper, Mike Bosman, Lerato Phalatse and Trudi Makhaya appointed to MTN South Africa board

30

Deep and fundamental strategic review of operations and processes to

ensure the Group is operating far more optimally

Prospects

Advanced analytics will support network quality, high speed data connectivity, improved customer

service and segmented offerings

Increased operating efficiencies and improving customer services focusing on improved service

channels productivity and MoMo as a distribution channel

Creating value through leveraging its extensive infrastructure

Embark on a process of housing new revenue streams, particularly digital services, outside the core

business enabling more agility and greater flexibility to accelerate growth

New revenue streams expected to increase contribution in next 12-18 months

Areas to be

addressed

KEY MATTERS AND

IMMEDIATE PRIORITIES

Tower

investments

Investments in towers with IHS evidenced by substantial ownership interest in INT and direct

investments in IHS

IHS is well positioned for future growth and build-out from 3G upgrades and move to LTE across its

key markets

IHS is now the largest independent tower operator in EMEA by tower count and tenth largest

independent tower company in the world with 24 000 towers

Recently led in-country consolidation through its acquisition of Helios Towers Nigeria

31

Prospects

KEY MATTERS AND

IMMEDIATE PRIORITIES

Expect improved operating conditions supported by permanent and refreshed management team

Strong operational oversight ensuring regulatory compliance across operations

Operating

conditions

Nigeria

South Africa

Iran

Aims to list MTN Nigeria on Nigeria Stock Exchange during 2017, subject to prevailing market

conditions and appropriate regulatory approval

Expect improved competitiveness and performance following reinstatement of regulatory services

Data performance to benefit from increased investment in 3G and LTE and recently acquired

spectrum

Expect improved performance supported by strong focus on customer service and improving the

network quality, capacity and speed

Data growth will benefit from significant investment and deliberate focus in 3G and LTE

Significant opportunities to expand digital services supported by easing of sanctions

Expect improvements in operating environment supported by a reduction in inflation and normalised

exchange rate

Working towards remittance of approximately R15.4 billion

Questions

thank you

Appendices

35

South Africa

Revenue growth of 5.1%

Subscribers down 2.6% to 29.8 million

• Negatively impacted by network outages in some areas,

competition and economic pressure affecting consumer

spending

• Pre-paid and post-paid segments declined by 2.7% to

24.7 million and 2.1% to 5.1 million respectively

Strong data revenue growth, supported by

smartphones

• Strong data revenue growth, up 19.2%, contributing

34.1% to total revenue attributable to

- Smartphones up 18.4% to 9.3 million

- Improved 3G and LTE network quality

- Additional services being offered in digital, including

international content

• Device sales in the previous comparable period were

impacted by the industrial strike action and supply chain

challenges

22,574 25,346 24 673

5,4195,242 5,132

27,99330,588 29 805

Dec 14 Dec 15 Jun 16

Total subscribers ‘000

Postpaid

Prepaid

19,157 18,882 19,841

19,765 21,156

38,922 40,038

19,841

Dec 14 Dec 15 Jun 16

Revenue ZAR (million)

H2

H1

Launched Jun 1994 Market share 32.3% Population 55.7m Market size 2016 96m Penetration 162% Shareholding 100%

36

South Africa

Strong focus on network experience

EBITDA margin down 5.5 pp

• Mainly due to

- Increased device costs relating to higher volumes sold

- Impact of network related costs as a result of the rollout

of 3G and LTE sites

Focus on improving network quality and capacity

• Capex of R4 773 million

• Rollout of 369 co-located 3G sites and 284 LTE sites

• 175 sites were connect to fibre

• 10 000 homes passed with fibre to the home, 40% rolled

out over the six month period

• Invitation to apply for high demand spectrum – 700MHz,

800MHz and 2.6GHz bands

12,775 12,158 13,862

13,638 14,510

26,413 26,668

13 862

Dec 14 Dec 15 Jun 16

Expenses ZAR (million)

H2

H1

2,0004,678 4,773

3,676

6,2705,676

10,948

4,773

Dec 14 Dec 15 Jun 16

Capex ZAR (million)

H2

H1

32.1% 33.4% 30.1% EBITDA margin

37

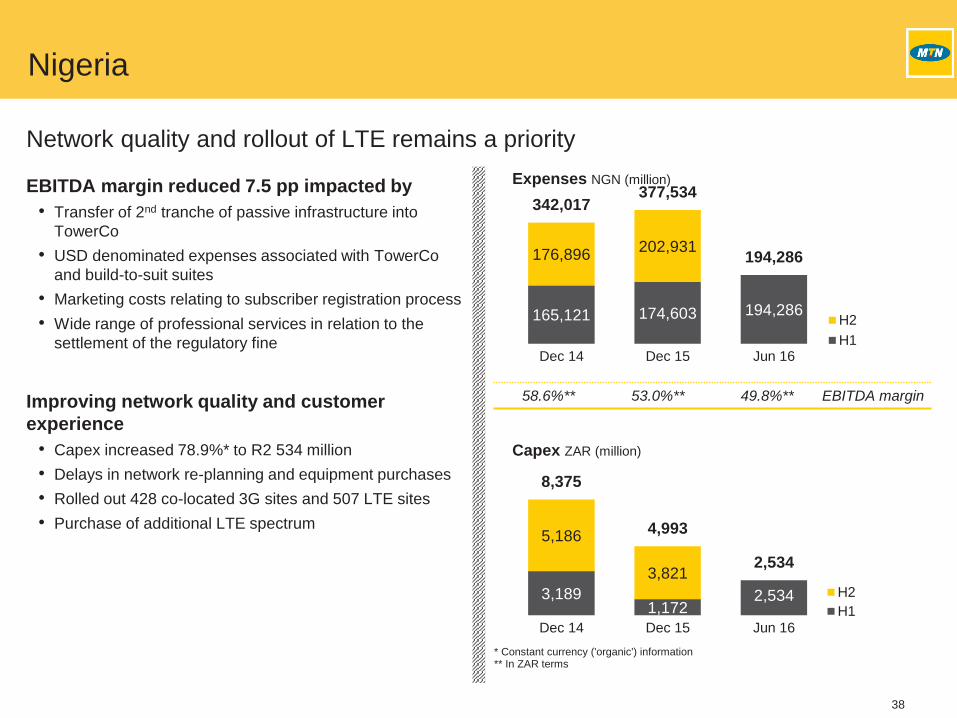

Nigeria

* Constant currency ('organic') information

Challenging operating environment

Subscriber decline of 3.7%

• Market share increased by 46.2% despite the decline in

subscriber base to 58.9 million (including 568 000

Visafone subscribers)

• Inability to offer competitive prices as a result of the

suspension of regulatory services until May 2016, when

approval was received

Revenue declined 4.8%*

• Lower outgoing voice and data revenue impacted by

regulatory requirements, multi-SIMs and tough economic

conditions

• Data revenue declined 2.7%*, contributing

19.3% to total revenue

- 11.2% increase in smartphones to 16 million

- Digital revenue continued to gain momentum – music

and lifestyle

- Diamond Yellow increased to 6.5 million registered

accounts

59,893

61,252

58 978

Dec 14 Dec 15 Jun 16

Total subscribers ‘000

413,611 408,999 389,345

411,195 398,450

824,806 807,449

389,345

Dec 14 Dec 15 Jun 16

Revenue NGN (million)

H2

H1

Launched Aug 2001 Market share 46.2% Population 174.3 m Market size 2016 133m Penetration 72% Shareholding 78.8%

38

Nigeria

* Constant currency ('organic') information** In ZAR terms

Network quality and rollout of LTE remains a priority

EBITDA margin reduced 7.5 pp impacted by

• Transfer of 2nd tranche of passive infrastructure into

TowerCo

• USD denominated expenses associated with TowerCo

and build-to-suit suites

• Marketing costs relating to subscriber registration process

• Wide range of professional services in relation to the

settlement of the regulatory fine

Improving network quality and customer

experience

• Capex increased 78.9%* to R2 534 million

• Delays in network re-planning and equipment purchases

• Rolled out 428 co-located 3G sites and 507 LTE sites

• Purchase of additional LTE spectrum

165,121 174,603 194,286

176,896202,931

342,017377,534

194,286

Dec 14 Dec 15 Jun 16

Expenses NGN (million)

H2

H1

3,1891,172

2,534

5,186

3,821

8,375

4,993

2,534

Dec 14 Dec 15 Jun 16

Capex ZAR (million)

H2

H1

58.6%** 53.0%** 49.8%** EBITDA margin

39

Iran

*Constant currency ('organic') information **In ZAR terms***Excluding hyperinflation

Revenue growth of 8.7%* supported by increased data revenue growth

Subscriber growth of 2.0% to 47.3 million

• Attractive segmented offerings, data bundles and

improved network experience

Strong data revenue

• Data revenue increased 65.3%*, contributing 40.6% to

total revenue despite regulatory pressure on data tariffs

• Smartphones increased 25.8% to 25.8 million

• Digital revenue contributed 32.6% to data revenue due to

strong growth in local lifestyle content based usage

• Outgoing voice revenue negatively impacted by the

continuous substitution of data services

EBITDA down 2.4 pp

• Mainly due to increased transmission costs associated

with the data network expansion, as well as marketing

costs related to 3G and LTE campaigns

3G and LTE networks expansion

• Added 1 783 co-located 3G sites and 851 LTE sites

27,260 31,038 33,739

29,46632,281

56,72663,319

33,739

Dec 14*** Dec 15*** Jun 16***

Revenue IRR (billion)

(100%)

H2

H1

8911,854 2,313

2,221

2,326

3,112

4,180

2 313

Dec 14*** Dec 15*** Jun 16***

Capex ZAR (million)

(49%)

H2

H1

42.8%** 41.5%** 37.7%** EBITDA margin

Launched Oct 2006 Market share 46.4% Population 80.6m Market size 2016 101m Penetration 126% Shareholding 49%

40

Ghana

*Constant currency ('organic') information**In ZAR terms

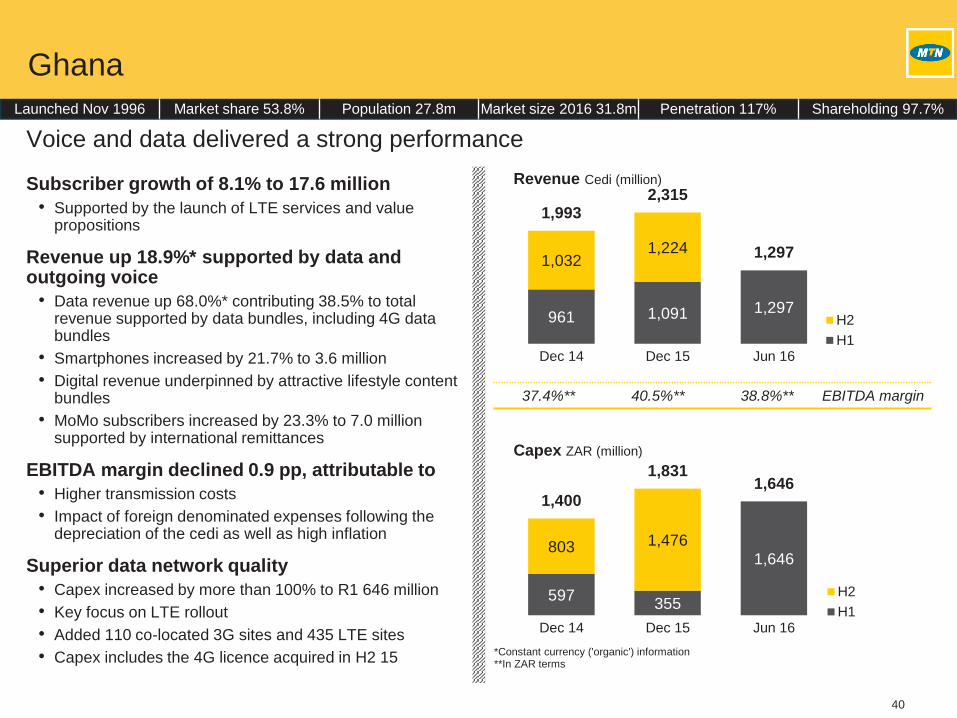

Voice and data delivered a strong performance

Subscriber growth of 8.1% to 17.6 million

• Supported by the launch of LTE services and value propositions

Revenue up 18.9%* supported by data and outgoing voice

• Data revenue up 68.0%* contributing 38.5% to total revenue supported by data bundles, including 4G data bundles

• Smartphones increased by 21.7% to 3.6 million

• Digital revenue underpinned by attractive lifestyle content bundles

• MoMo subscribers increased by 23.3% to 7.0 million supported by international remittances

EBITDA margin declined 0.9 pp, attributable to

• Higher transmission costs

• Impact of foreign denominated expenses following the depreciation of the cedi as well as high inflation

Superior data network quality

• Capex increased by more than 100% to R1 646 million

• Key focus on LTE rollout

• Added 110 co-located 3G sites and 435 LTE sites

• Capex includes the 4G licence acquired in H2 15

961 1,091 1,297

1,0321,224

1,9932,315

1,297

Dec 14 Dec 15 Jun 16

Revenue Cedi (million)

H2

H1

597355

1,646803 1,476

1,400

1,8311,646

Dec 14 Dec 15 Jun 16

Capex ZAR (million)

H2

H1

37.4%** 40.5%** 38.8%** EBITDA margin

Launched Nov 1996 Market share 53.8% Population 27.8m Market size 2016 31.8m Penetration 117% Shareholding 97.7%

41

Cameroon

*Constant currency ('organic') information**In ZAR terms

Aggressive subscriber registration campaigns

Subscribers up 5.0% to 9.6 million

• Market share growth attributable to improved network

quality, expansion of LTE footprint and increased

smartphone penetration

Revenue declined 8.7%*

• Decline in outgoing voice revenue impacted by price

competition and free minutes used as part of subscriber

registration process

• Data revenue increased 49.5%* and contributes 18.8% to

total revenue, supported by increased 3G device

penetration and network rollout

• Smartphones increased by 34.1% to 2.6 million

• Mobile Money brand campaign increased activity

EBITDA margin up 0.2 pp

• Supported by strong cost optimisation

• Reduction in transmission costs due to WACS cable

Focus on 3G and LTE network rollout and quality

• 6.9%* increase in capex to R1 121 million

• 189 co-located 3G sites and 64 LTE sites rolled out

136,593 135,986 124,152

146,776 134,244

283,369 270,230

124,152

Dec 14 Dec 15 Jun 16

Revenue CFA (million)

H2

H1

373943 1 121489

968862

1,911

1,121

Dec 14 Dec 15 Jun 16

Capex ZAR (million)

H2

H1

42.8%** 36.2%** 38.0%** EBITDA margin

Launched Feb 2000 Market share 57.4% Population 23.6m Market size 2016 18.5m Penetration 71% Shareholding 70%

42

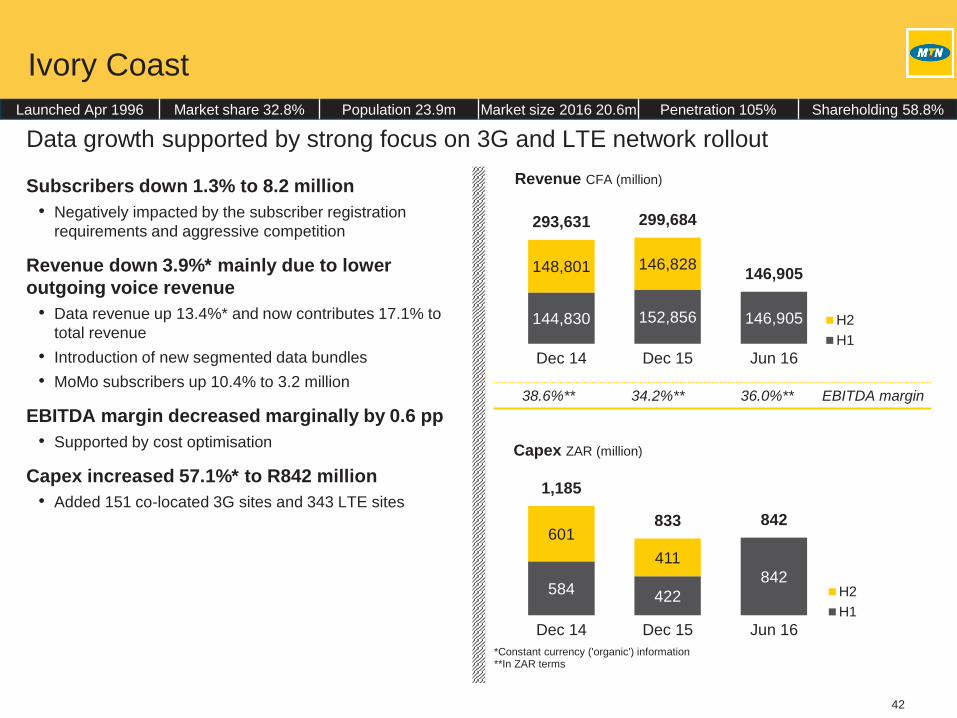

Ivory Coast

*Constant currency ('organic') information**In ZAR terms

Data growth supported by strong focus on 3G and LTE network rollout

Subscribers down 1.3% to 8.2 million

• Negatively impacted by the subscriber registration

requirements and aggressive competition

Revenue down 3.9%* mainly due to lower

outgoing voice revenue

• Data revenue up 13.4%* and now contributes 17.1% to

total revenue

• Introduction of new segmented data bundles

• MoMo subscribers up 10.4% to 3.2 million

EBITDA margin decreased marginally by 0.6 pp

• Supported by cost optimisation

Capex increased 57.1%* to R842 million

• Added 151 co-located 3G sites and 343 LTE sites

144,830 152,856 146,905

148,801 146,828

293,631 299,684

146,905

Dec 14 Dec 15 Jun 16

Revenue CFA (million)

H2

H1

584 422

842

601

411

1,185

833 842

Dec 14 Dec 15 Jun 16

Capex ZAR (million)

H2

H1

38.6%** 34.2%** 36.0%** EBITDA margin

Launched Apr 1996 Market share 32.8% Population 23.9m Market size 2016 20.6m Penetration 105% Shareholding 58.8%

43

Uganda

*Constant currency ('organic') information**In ZAR terms

Gaining momentum post subscriber registration process

Subscribers increased 10.8% to 9.9 million

• Supported by voice bundle propositions and continued

success of MTN Zone

• MoMo decreased registered subscribers by 24.4% to 7.2

million mainly due to H2 2015 disconnections during the

subscriber registration process

Revenue decreased 2.3%*

• Voice revenue impacted by One Network Area, decline in

mobile termination rates and disconnections

• Data revenue up 22.7%*, contributing 32.8% to total

revenue – supported by data bundles

• Digital revenue contributed 70.5% to data revenue

supported by local content services including MTN Play.

EBITDA margin down 6.0 pp

• Higher network operating costs and associated USD

denominated expenses

• Higher transmission costs, marketing and distribution

costs following the launch of 3G and 4G services.

Capex spend down 42.1%* to R364 million

• Delay in supply chain process

• Added 195 co-located 3G sites and 100 LTE sites

618,467 633,861 619,434

649,118 668,830

1,267,585 1,302,691

619,434

Dec 14 Dec 15 Jun 16

Revenue UGX (million)

H2

H1

407556

364

260

395667

951

364

Dec 14 Dec 15 Jun 16

Capex ZAR (million)

H2

H1

39.2%** 34.5%** 30.0%** EBITDA margin

Launched Oct 1998 Market share 52.7% Population 40.5m Market size 2016 20.3m Penetration 46% Shareholding 96%

44

Syria

*Constant currency ('organic') information**In ZAR terms***Excluding hyperinflation

Operational growth despite a challenging environment

Subscribers decreased by 2.4%

Revenue increased 10.5%*

• Supported by 16.9%* increase in data revenue,

contributing 28.8% to total revenue

EBITDA margin increased 12.3 pp

• Supported by the conversion of the BOT licence and cost

optimisation

Capex increased by 241.1% to R191 million

• Added 92 co-located 3G sites and 3 LTE sites

26,436 26,468 29,295

26,844 29,392

53,280 55,860

29,295

Dec 14*** Dec 15*** Jun 16***

Revenue SYP (million)

H2

H1

38 56 191319

918357

974

191

Dec 14*** Dec 15*** Jun 16***

Capex ZAR (million)

H2

H1

18.9%** 17.7%** 28.6%** EBITDA margin

Launched Jun 2002 Market share 40.9% Population 17.0m Market size 2016 14.8m Penetration 84% Shareholding 75%

45

Sudan

*Constant currency ('organic') information**In ZAR terms***Excluding hyperinflation

Progress in tough conditions

Subscribers increased 4.2% to 8.8 million

• Driven by targeted marketing campaigns

Revenue increased by 15.7%*

• Data revenue increased 78.3%* and contributes 27.7% to

total revenue as a result of increased data users

EBITDA margin down 1.9 pp

Capex up 62.9% to R549 million

• Added 44 co-located 3G sites

692 811 938

738830

1,4301,641

938

Dec 14*** Dec 15*** Jun 16***

Revenue SDG (million)

H2

H1

481 337549

911

482

1,392

819

549

Dec 14*** Dec 15*** Jun 16***

Capex ZAR (million)

H2

H1

33.8%** 35.0%** 35.4%** EBITDA margin

Launched Sep 2005 Market share 33.8% Population 37.6m Market size 2016 30.3m Penetration 69% Shareholding 85%

46

ZAR (million)Actual H1-16

Hyper-inflation

Tower profit*

Nigeria regulatory

fine

Actual 2016

adjustedActual H1-15

Hyper-inflation

Tower profit*

Actual 2015

adjustedAdjusted

change %

Revenue 79 115 237 - - 78 878 69 304 94 - 69 210 14

Other income 367 - 18 - 349 411 - 352 59 492

EBITDA 18 882 90 18 (10 499) 29 273 30 675 49 352 30 274 (3)

Depreciation, amortisation and impairment of goodwill 13 691 77 - - 13 614 10 750 35 - 10 715 27

Profit from operations 5 191 13 18 (10 499) 15 659 19 925 14 352 19 559 (20)

Net finance cost 5 945 32 - 452 5 461 2 319 (1) - 2 320 135

Share of results of joint ventures & associates after tax

(1 692) (1 039) - - (653) 2 027 362 - 1 665 (139)

Net monetary gain 919 919 - - - 496 496 - - NM

(Loss)/profit before tax (1 527) (139) 18 (10 951) 9 545 20 129 873 352 18 904 (50)

Income tax expense 4 726 32 - - 4 694 6 249 26 - 6 223 (25)

(Loss)/profit after tax (6 253) (171) 18 (10 951) 4 851 13 880 847 352 12 681 (62)

Non-controlling interests (764) 204 - (2 319) 1 351 1 980 105 75 1 800 (25)

Attributable (loss)/profit (5 489) (375) 18 (8 632) 3 500 11 900 742 277 10 881 (68)

EBITDA margin 23.9% 37.1% 44.3% 43.7% (6.6)pp

Effective tax rate (309.6%) 49.2% 31.0% 32.9% 16.3pp

*Tower sale profits for the period relates to Ghana release of deferred profit of R18m (H1-15: The measurement of the contingent consideration receivable relating to Nigeria tower transaction tranche 1 of R339m and the Ghana release of deferred profit of R13m)

Income statement

Hyperinflation, Nigeria regulatory fine and tower sales impact

47

ZAR (million)Cash and cash

equivalents*

Net interest-bearing

liabilities

Net debt/(cash)

H1-16

Net debt/(cash)

Dec 2015

South and East Africa 4 161 2 107 (2 054) (1 652)

South Africa 3 457 - (3 457) (1 507)

Uganda 81 1 279 1 198 (86)

Other 623 828 205 (59)

West and Central Africa 18 548 24 587 6 039 3 956

Nigeria 14 785 16 922 2 137 1 695

Ghana 223 1 141 918 15

Cameroon 745 1 483 738 118

Ivory Coast 810 2 842 2 032 2 399

Other 1 985 2 199 214 (271)

Middle East and North Africa 2 981 3 188 207 (585)

Syria 736 - (736) (1 525)

Sudan 323 2 131 1 808 1 889

Other 1 922 1 057 (865) (949)

Head office companies & eliminations 7 000 52 065 45 065 29 916

Total 32 690 81 947 49 257 31 635

* Includes restricted cash and current investments

Net debt

48

Net debt composition

Nigeria and Head office

Naira denominated

USDdenominated

ZARdenominated

Eurodenominated

Nigeria borrowings 11 331 5 591 - -

Nigeria cash 12 832 1 941 - 12

Head office borrowings - 25 700 26 365 -

Head office cash - 3 996 2 284 720

Nigeria borrowings(%)

USD33%(26%)

Naira67%(74%)

Head office borrowings(%)

Nigeria cash(%)

Head office cash(%)

USD49%(57%)

ZAR51%(43%)

USD13%(6%)

ZAR33%(44%)

USD57%(45%)

Euro10%(11%)

Naira87%(94%)

Net debt compositionZAR (million)

49

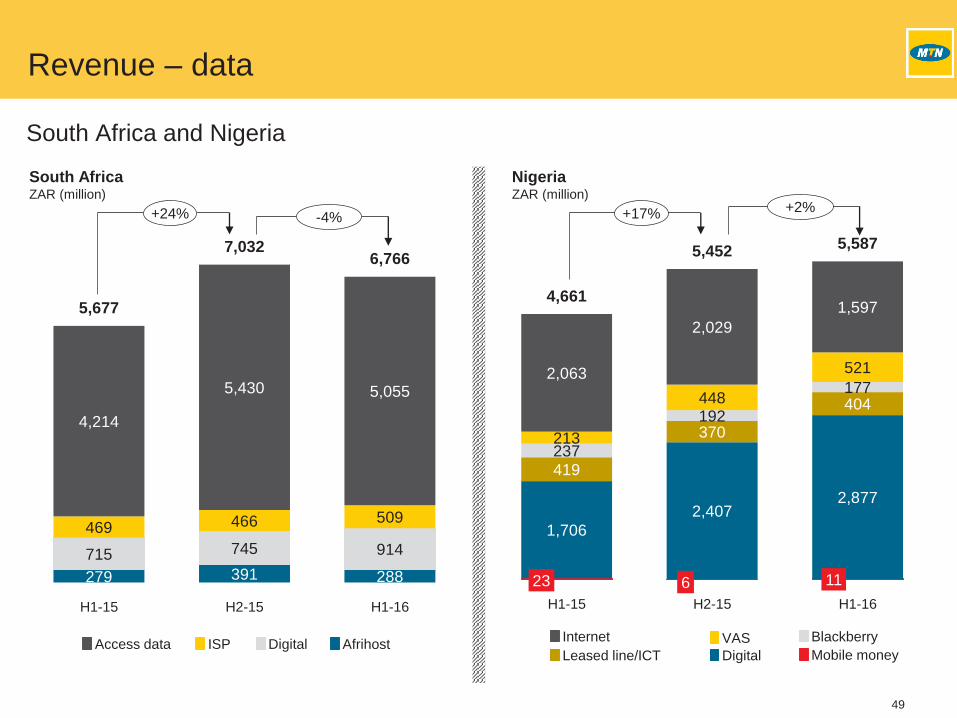

Revenue – data

South Africa and Nigeria

23 6 11

1,706

2,4072,877

419

370

404

237

192

177

213

448

5212,063

2,029

1,5974,661

5,4525,587

H1-15 H2-15 H1-16

279 391 288

715 745 914

469 466 509

4,214

5,430 5,055

5,677

7,0326,766

H1-15 H2-15 H1-16

South AfricaZAR (million)

NigeriaZAR (million)

ISP DigitalAccess data AfrihostInternet VAS Blackberry

Leased line/ICT Mobile moneyDigital

+24% -4% +17% +2%

50

ZAR (million) H1-16 H1-15 Change %

Telco joint ventures 2 198 1 935 14

Iran 1 975 1 737 14

Swaziland 50 48 4

Botswana 173 150 15

Tower companies (2 480) (64) NM

Ghana (17) 22 (177)

Uganda - (149) (100)

Nigeria * (2 463) 63 NM

BICS 123 118 4

Share of results of telco joint ventures and associates after tax excluding hyperinflation (159) 1 989 (108)

Iran – Hyperinflation (H1-16: Mainly depreciation and amortisation of assets written up) (1 039) 362 NM

Share of results of telco joint ventures & associates after tax including hyperinflation (1 198) 2 351 (151)

Digital Group (494) (324) (52)

AIH (370) (249) (49)

MEIH (69) (42) (64)

IME (55) (33) (67)

Share of results of joint ventures and associates after tax (1 692) 2 027 (183)

* Includes forex losses of R2 282m resulting from the devaluation of the Naira

Share of results of joint ventures and associates after tax (IFRS)

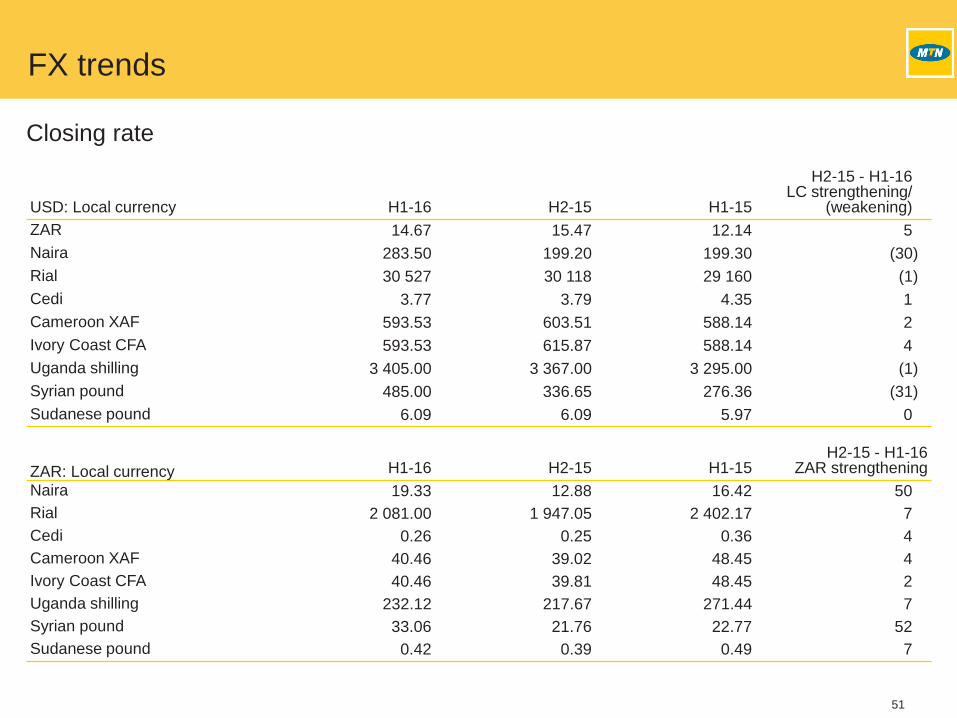

51

USD: Local currency H1-16 H2-15 H1-15

H2-15 - H1-16LC strengthening/

(weakening)

ZAR 14.67 15.47 12.14 5

Naira 283.50 199.20 199.30 (30)

Rial 30 527 30 118 29 160 (1)

Cedi 3.77 3.79 4.35 1

Cameroon XAF 593.53 603.51 588.14 2

Ivory Coast CFA 593.53 615.87 588.14 4

Uganda shilling 3 405.00 3 367.00 3 295.00 (1)

Syrian pound 485.00 336.65 276.36 (31)

Sudanese pound 6.09 6.09 5.97 0

ZAR: Local currency H1-16 H2-15 H1-15H2-15 - H1-16

ZAR strengthening

Naira 19.33 12.88 16.42 50

Rial 2 081.00 1 947.05 2 402.17 7

Cedi 0.26 0.25 0.36 4

Cameroon XAF 40.46 39.02 48.45 4

Ivory Coast CFA 40.46 39.81 48.45 2

Uganda shilling 232.12 217.67 271.44 7

Syrian pound 33.06 21.76 22.77 52

Sudanese pound 0.42 0.39 0.49 7

FX trends

Closing rate

52

USD: Local currency H1-16 H2-15 H1-15H1-15 - H1-16LC weakening

ZAR 15.26 12.77 11.85 (22)

Naira 205.83 199.34 196.49 (5)

Rial 30 271 29 831 28 024 (7)

Cedi 3.83 3.80 3.76 (2)

Cameroon XAF 590.97 596.62 587.24 (1)

Ivory Coast CFA 597.32 598.87 587.07 (2)

Uganda shilling 3 371.57 3 508.93 2 956.18 (12)

Syrian pound 418.97 312.76 237.91 (43)

Sudanese pound 6.09 6.08 5.97 (2)

ZAR: Local currency H1-16 H2-15 H1-15

H1-15 - H1-16ZAR strengthening/

(weakening)

Naira 13.52 14.62 16.59 (19)

Rial 1 984.95 2 184.00 2 364.16 (16)

Cedi 0.25 0.28 0.32 (22)

Cameroon XAF 38.79 43.83 49.58 (22)

Ivory Coast CFA 39.18 44.08 49.58 (21)

Uganda shilling 220.40 257.64 249.48 (12)

Syrian pound 27.41 23.02 20.07 37

Sudanese pound 0.40 0.45 0.50 (20)

FX trends

Average rate