mtn nigeria communications limited. - dunn loren … nigeria... · equity research | mtn nigeria...

TRANSCRIPT

August 04, 2016 www.dunnlorenmerrifield.com Bloomberg: < DLMN> GO

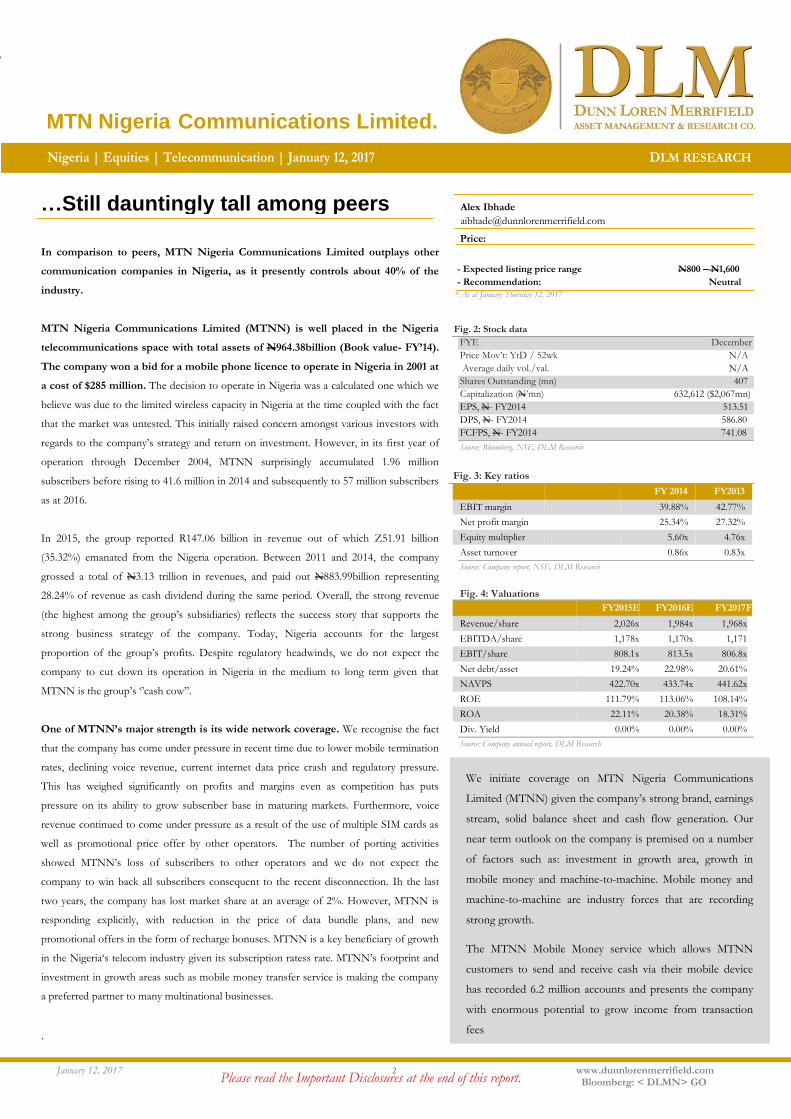

MTN Nigeria Communications Limited. Nigeria | Equities | Telecommunication | January 12, 2017 DLM RESEARCH

…Still dauntingly tall among peers

Equity Research | MTN Nigeria Communications Limited DLM RESEARCH

January 12, 2017 2 www.dunnlorenmerrifield.com

Bloomberg: < DLMN> GO

In comparison to peers, MTN Nigeria Communications Limited outplays other

communication companies in Nigeria, as it presently controls about 40% of the

industry.

MTN Nigeria Communications Limited (MTNN) is well placed in the Nigeria

telecommunications space with total assets of N964.38billion (Book value- FY’14).

The company won a bid for a mobile phone licence to operate in Nigeria in 2001 at

a cost of $285 million. The decision to operate in Nigeria was a calculated one which we

believe was due to the limited wireless capacity in Nigeria at the time coupled with the fact

that the market was untested. This initially raised concern amongst various investors with

regards to the company’s strategy and return on investment. However, in its first year of

operation through December 2004, MTNN surprisingly accumulated 1.96 million

subscribers before rising to 41.6 million in 2014 and subsequently to 57 million subscribers

as at 2016.

In 2015, the group reported R147.06 billion in revenue out of which Z51.91 billion

(35.32%) emanated from the Nigeria operation. Between 2011 and 2014, the company

grossed a total of N3.13 trillion in revenues, and paid out N883.99billion representing

28.24% of revenue as cash dividend during the same period. Overall, the strong revenue

(the highest among the group’s subsidiaries) reflects the success story that supports the

strong business strategy of the company. Today, Nigeria accounts for the largest

proportion of the group’s profits. Despite regulatory headwinds, we do not expect the

company to cut down its operation in Nigeria in the medium to long term given that

MTNN is the group’s ‘’cash cow’’.

One of MTNN’s major strength is its wide network coverage. We recognise the fact

that the company has come under pressure in recent time due to lower mobile termination

rates, declining voice revenue, current internet data price crash and regulatory pressure.

This has weighed significantly on profits and margins even as competition has puts

pressure on its ability to grow subscriber base in maturing markets. Furthermore, voice

revenue continued to come under pressure as a result of the use of multiple SIM cards as

well as promotional price offer by other operators. The number of porting activities

showed MTNN’s loss of subscribers to other operators and we do not expect the

company to win back all subscribers consequent to the recent disconnection. Ih the last

two years, the company has lost market share at an average of 2%. However, MTNN is

responding explicitly, with reduction in the price of data bundle plans, and new

promotional offers in the form of recharge bonuses. MTNN is a key beneficiary of growth

in the Nigeria‘s telecom industry given its subscription ratess rate. MTNN’s footprint and

investment in growth areas such as mobile money transfer service is making the company

a preferred partner to many multinational businesses.

.

…Still dauntingly tall among peers

Alex Ibhade

Please read the Important Disclosures at the end of this report.

Fig. 2: Stock data

FYE December

Price Mov’t: YtD / 52wk N/A

Average daily vol./val. N/A

Shares Outstanding (mn) 407

Capitalization (N’mn) 632,612 ($2,067mn)

EPS, N- FY2014 513.51

DPS, N- FY2014 586.80

FCFPS, N- FY2014 741.08

Source: Bloomberg, NSE, DLM Research

Fig. 3: Key ratios

FY 2014 FY2013

EBIT margin 39.88% 42.77%

Net profit margin 25.34% 27.32%

Equity multiplier 5.60x 4.76x

Asset turnover 0.86x 0.83x

Source: Company report, NSE, DLM Research

Fig. 4: Valuations

FY2015E FY2016E FY2017F

Revenue/share 2,026x 1,984x 1,968x

EBITDA/share 1,178x 1,170x 1,171

EBIT/share 808.1x 813.5x 806.8x

Net debt/asset 19.24% 22.98% 20.61%

NAVPS 422.70x 433.74x 441.62x

ROE 111.79% 113.06% 108.14%

ROA 22.11% 20.38% 18.31%

Div. Yield 0.00% 0.00% 0.00%

Source: Company annual report, DLM Research

Price:

- Expected listing price range N800 – N1,600

- Recommendation: Neutral

* As at January Thursday 12, 2017

We initiate coverage on MTN Nigeria Communications

Limited (MTNN) given the company’s strong brand, earnings

stream, solid balance sheet and cash flow generation. Our

near term outlook on the company is premised on a number

of factors such as: investment in growth area, growth in

mobile money and machine-to-machine. Mobile money and

machine-to-machine are industry forces that are recording

strong growth.

The MTNN Mobile Money service which allows MTNN

customers to send and receive cash via their mobile device

has recorded 6.2 million accounts and presents the company

with enormous potential to grow income from transaction

fees

MTN Nigeria Communications Limited.

Equity Research | MTN Nigeria Communications Limited DLM RESEARCH

January 12, 2017 3 www.dunnlorenmerrifield.com

Bloomberg: < DLMN> GO

Outlook.......... what does the future hold. In this section we present,

three likely scenarios which the revenue and earnings profile for MTN Nigeria

may chart, given the outlook for the Nigerian telecom industry and, in relation

to the domestic economy.

Scenario 1: Base case assumptions project a conservative growth rate.

Our base case is derived from a number of factors such as decreasing voice

revenues, hostile competition, migration to other networks and decrease in

number of subscribers.

Scenario 2: Assumes that data income grows at historical CAGR of

19.14% over the next five years with possible increase in the price of data.

Based on this assumption, revenue would increase to about N811.71billion by

2016, N833.33billion by 2017, N873.10billion by 2018 and N888.76billion by

2019. As at November 1, 2016, the industry average for data tariff floor for

major operators such as MTN, Etisalat and Airtel was N0.53k/MB. A review

of the old rate showed that Etisalat offered (N0.94k/MB), Airtel (N0.52k/MB),

MTN (N0.45k/MB) and Globacom (N0.21k/MB). As a result of the price

variation, NCC came up with an average data tariff of N0.53k/MB for

dominant operators. However, an interim price floor of 0.90k/MB was

introduced by NCC. This was later suspended with an expectation to continue

with effect from December 1, 2016. The proposed tariff seeks to increase the

industry average data tariff from N0.53k/MB to N0.90k/MB.

The implementation of the new rate is pending on the finalisation of the

study on the determination of cost based pricing for retail broadband and

data services in Nigeria. With increasing use of internet, we expect an

additional data usage on the network going forward. On the back of this growth

assumption, there’s a robust revenue upside potential for MTN Nigeria from

the medium to long term. However, despite the growth potential, MTN Nigeria

would still need to focus on cost management, albeit in the short to medium

term until a meaningful top line growth is achieved for a healthy bottom line.

By 2017 and beyond however, our forecasts imply that operating cash flow will

be healthy to accommodate dividend growth, but cost reduction would still be

necessary. However, if voice revenue continues to decrease at this rate beyond

2018 and data floor price decreases further or even remain at the current level

as opposed to the proposed data price increase, then revenue would no longer

be sufficient to boost operating and net profits. We would therefore see a

reduction in dividend pay-out albeit at a significantly reduced level, and likely

temporarily, until a sustainable growth is attained.

Scenario 3: Assumes that the company focuses on pursuing revenues in

other growth areas in line with management drive.

“ As at November 1,

2016, the industry average for data tariff

floor for major operators such as MTN, Etisalat

and Airtel was N0.53k/MB.

’’

Equity Research | MTN Nigeria Communications Limited DLM RESEARCH

January 12, 2017 4 www.dunnlorenmerrifield.com

Bloomberg: < DLMN> GO

Likely scenarios MTN Nigeria valuation or share price may chart.

Fig. 5: MTN Nigeria valuation range

We considered the main valuation criteria used in the

telecommunications industry. However, DCF is our principal method to

assess the value of MTNN as we believe the DCF model is the most

appropriate model to value companies in the telecom sector. The two key

factors which we considered will affect valuation are revenue growth and cash

flow. Typically, the telecommunications industry is considered to be slightly less

risky, hence, we used beta coefficient of 0.84, though higher than that of the

group. We used a WACC of 16.97% and cost of equity of 18.96%–and believe

a dividend yield above 10% would be appropriate to provide an adequate return

to investors. Our valuation model suggests that N800 - N1,600/share looks a

likely listing range for MTNN Nigeria, suggesting a dividend yield above 30%.

This would make dividend yield base investment on the stock attractive. The

dividend model assumes 56% average dividend pay-out of operating profit. For

EV/EBITDA model, past performance of EBITDA is positive but volatile,

and we do not expect it to grow significantly in the near term. Hence, we

forecast a maintainable normalized EBITDA of N471.40billion with

EV/EBITDA multiple of 1.93x. Our adopted EV/EBITDA multiple is lower

than those of our selected African market peers, as we applied a discount to

reflect market risks. The EV/EBITDA method suggests the shares could trade

at N1,272/share. The DCF valuation model and sensitivity analysis suggests a

price range of N804 – N1,653/share. Overall, our valuation prices places

MTNN shares on a forecast P/E of 2.72x range bound which does looks

attractive in our view and could be a very profitable long-term buy. MTN

has invested heavily in its set up and is dependent on the investments in

assets for future returns. Therefore, with higher asset base, its

depreciation and amortization is relatively higher.

Value per share: EV/EBITDA Method: N1,272/share

Value per share: DCF Sensitivity analysis: N804 – N1,653/share

Value per share: Price/Book Model: N850.10/share

Adopted EV/EBITDA multiple: 1.93x

Maintainable normalized EBITDA N471.40billion billion

Enterprise value - N1.02trillion

“ Overall, our

valuation prices place MTNN shares on a

forecast P/E of 2.72x range bound which does looks attractive in our

view and could be a very profitable long-term buy.

’’

Adopted price to book value: 1.9x

Value per share: DCF model: N1,474/share

Equity Research | MTN Nigeria Communications Limited DLM RESEARCH

January 12, 2017 5 www.dunnlorenmerrifield.com

Bloomberg: < DLMN> GO

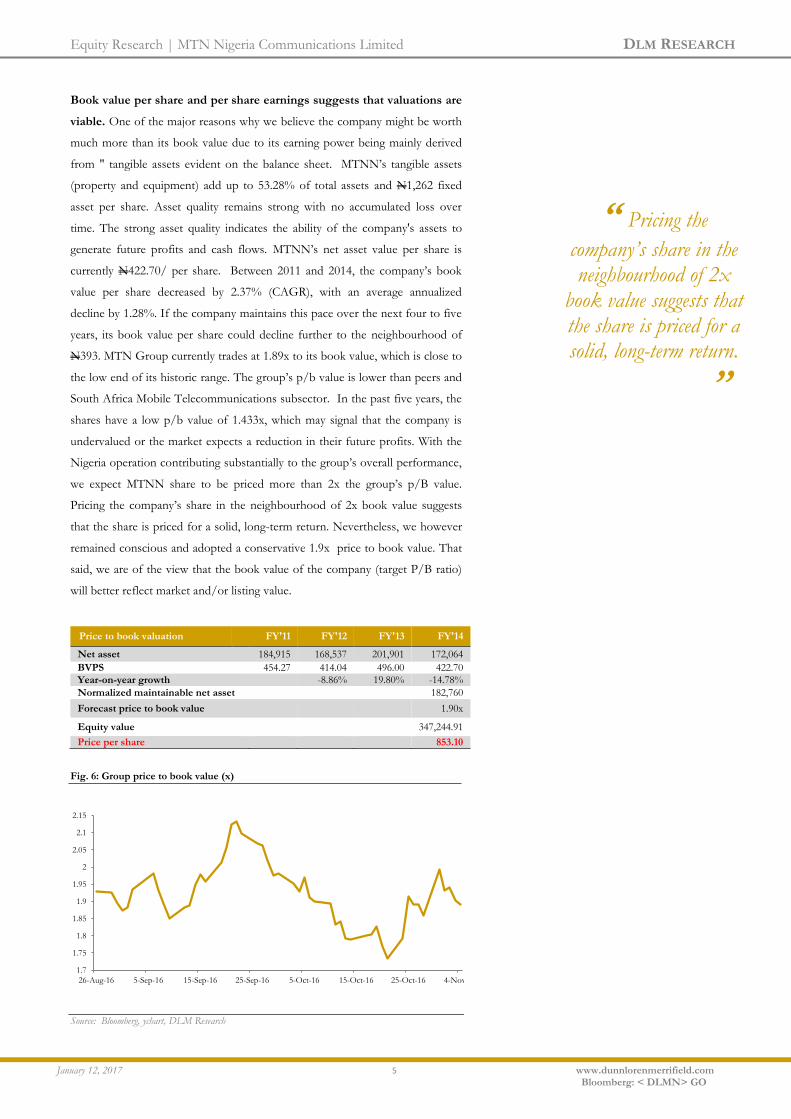

Book value per share and per share earnings suggests that valuations are

viable. One of the major reasons why we believe the company might be worth

much more than its book value due to its earning power being mainly derived

from " tangible assets evident on the balance sheet. MTNN’s tangible assets

(property and equipment) add up to 53.28% of total assets and N1,262 fixed

asset per share. Asset quality remains strong with no accumulated loss over

time. The strong asset quality indicates the ability of the company's assets to

generate future profits and cash flows. MTNN’s net asset value per share is

currently N422.70/ per share. Between 2011 and 2014, the company’s book

value per share decreased by 2.37% (CAGR), with an average annualized

decline by 1.28%. If the company maintains this pace over the next four to five

years, its book value per share could decline further to the neighbourhood of

N393. MTN Group currently trades at 1.89x to its book value, which is close to

the low end of its historic range. The group’s p/b value is lower than peers and

South Africa Mobile Telecommunications subsector. In the past five years, the

shares have a low p/b value of 1.433x, which may signal that the company is

undervalued or the market expects a reduction in their future profits. With the

Nigeria operation contributing substantially to the group’s overall performance,

we expect MTNN share to be priced more than 2x the group’s p/B value.

Pricing the company’s share in the neighbourhood of 2x book value suggests

that the share is priced for a solid, long-term return. Nevertheless, we however

remained conscious and adopted a conservative 1.9x price to book value. That

said, we are of the view that the book value of the company (target P/B ratio)

will better reflect market and/or listing value.

Price to book valuation FY'11 FY'12 FY'13 FY'14

Net asset 184,915 168,537 201,901 172,064

BVPS 454.27 414.04 496.00 422.70

Year-on-year growth

-8.86% 19.80% -14.78%

Normalized maintainable net asset

182,760

Forecast price to book value 1.90x

Equity value 347,244.91

Price per share 853.10

Fig. 6: Group price to book value (x)

Source: Bloomberg, ychart, DLM Research

1.7

1.75

1.8

1.85

1.9

1.95

2

2.05

2.1

2.15

26-Aug-16 5-Sep-16 15-Sep-16 25-Sep-16 5-Oct-16 15-Oct-16 25-Oct-16 4-Nov-16

“ Pricing the

company’s share in the neighbourhood of 2x

book value suggests that the share is priced for a solid, long-term return.

’’

Equity Research | MTN Nigeria Communications Limited DLM RESEARCH

January 12, 2017 6 www.dunnlorenmerrifield.com

Bloomberg: < DLMN> GO

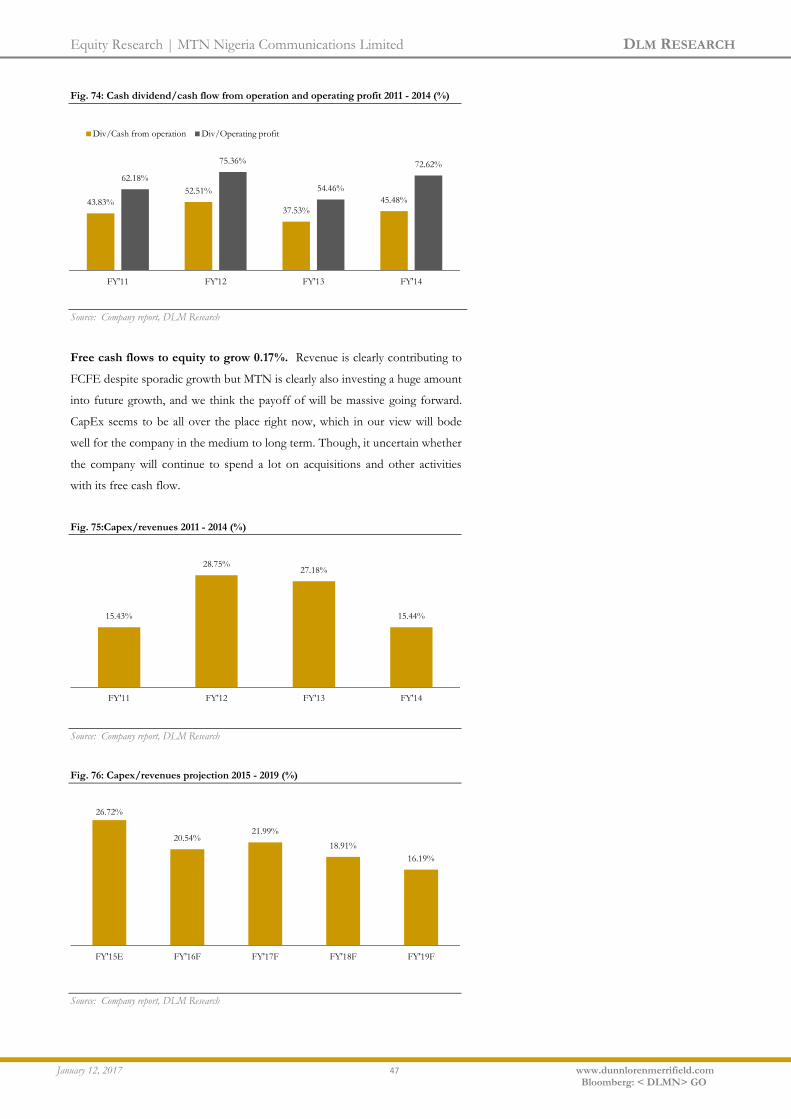

Dividend yield and dividend growth will be the main focus for investors.

The company has historically paid dividend greater than net income as

depreciation and amortization are very substantial. While the main determinant

of dividend growth in the medium to long term is earnings / free cash flow,

investors will be attracted to MTNN’s track record of paying dividend. While

our dividend forecast is based on the assumption that the current dividend

trend will be maintained, we see dividend yield ticking above inflation.

Dividend paid has increased from N220.79billion in 2011 to N238.86billion in

2014, representing a CAGR of 2.66%. The dividend paid in 2014 represents

45.48% and 72.62% of cash flow from operations and operating profit

respectively. Though, there are rooms for growth, but for FY’16, dividend

payout is forecast to moderate as a result of capex programme and regulatory

fine of N330billion unless management are able to cut some costs or capex.

Companies typically keep their pay-out ratios fairly low, such that when they

experience slowdown in cash flow and profit, they will be able to keep and

grow dividend. While a significant proportion of the company’s annual dividend

is accrued to the group due to its shareholdings status, in our view, the huge

dividend pay out to the group signals profit repatriation. Overall, we think that

balance sheet is strong enough to support future growth.

Fig. 7: Dividend operating profit (%)

Source: Company annual report, DLM Research

Costs and dividends eat up bigger slice of MTNN’s earnings. MTNN has

historically spent more of its earnings on costs of operation and dividend to

shareholders. Despite slow growth, operating costs has historically outpaced

EBITDA, while annual dividend exceeded net income except for FY’11 and

FY’13 financial year. Cash outflow for the two line items averaged 85.37% of

revenues over the past four years. While we reckon the fact that dividend-

paying stocks is among the best-performing asset classes, the high costs

underscores the intense pressure on corporate earnings. With the addition of

interest charges and income tax, MTNN seem to be paying out more than it

earns except for FY’11 and FY’13 where it posted positive net balance.

62.18%

75.36%

54.46%

72.62%

FY'11 FY'12 FY'13 FY'14

Equity Research | MTN Nigeria Communications Limited DLM RESEARCH

January 12, 2017 7 www.dunnlorenmerrifield.com

Bloomberg: < DLMN> GO

Fig. 8: Revenues and cash out flow – 2011-2014 (N’bn)

Source: Company annual report, DLM Research

With the negative net cash balance in FY12 and FY14, three scenarios

maybe playing out in our view. Annual headline revenues may be higher than

reported, while costs may be lower than reported. The third scenario is that

MTN Nigeria may be drawing from accumulated retained earnings and or profit

from sales of assets. However, with the exclusion of non-cash items such as

depreciation and amortization, net cash balance remained at a comfortable

position, which although, does not reflects on retained earnings. Erecting

network of cellular masts and towers is a costly undertaking; this has resulted in

a steady capital expenditure as a percentage of operating cash flow. However,

with the sales of 9,151 towers in 2014, we expect to see a substantial reduction

in the company’s overall cost structure going forward as the cost of tower

maintenance continues to eat into profits. Overall, reduction in overall cost

structure will provide the company an opportunity to mitigate some business

risks.

Fig. 9: Net cash balance (N’bn)

Source: Company annual report, DLM Research

750.51

772.07 761.66

854.64

757.98 753.58

793.61

824.81

FY'11 FY'12 FY'13 FY'14

Total cash out flow Revenues

7.47

-18.49

31.96

-29.83

FY'11 FY'12 FY'13 FY'14

“ However, with the

exclusion of non-cash items such as

depreciation and amortization, net cash balance remained at a comfortable position,

which although, does not reflects on retained

earnings.

’’

Equity Research | MTN Nigeria Communications Limited DLM RESEARCH

January 12, 2017 8 www.dunnlorenmerrifield.com

Bloomberg: < DLMN> GO

Retained Earnings FY'11 FY'12 FY'13 FY'14

Share capital 646.51 646.51 646.51 646.51

Share premium 64,498.50 64,498.50 64,498.50 64,498.50

Retained Earnings 119,770 103,392 135,851 106,017

Increase/Decrease in retained earnings (16,378) 32,459 (29,834)

Annual revenues utilization FY'11 FY'12 FY'13 FY'14

Total costs 402,879 435,804 454,160 495,876

Net interest expenses 17,841 14,033 28,608 38,324 Income tax 108,998 82,749 94,024 81,579

Dividends 220,789 239,480 184,863 238,861

Total cash out flow 750,507 772,066 761,656 854,640 Headline revenues 757,978 753,578 793,614 824,807 Net cash balance 7,471 (18,488) 31,958 (29,833)

Annual inflow and out flow FY'11 FY'12 FY'13 FY'14

Total costs 402,879 435,804 454,160 495,876

Less Dep & Amortization 111,836 119,790 141,187 150,418

Total costs 291,043 316,014 312,973 345,458

Interest received 13,314 34,039 13,673 22,575

Interest Paid 32,879 46,526 42,336 48,391

Net interest Paid 19,565 12,486 28,662 25,815 Tax paid 60,833 103,487 87,412 66,744 dividends 220,789 239,480 184,863 238,861

Total cash out flow 592,230 671,467 613,911 676,878

Headline revenues 757,978 753,578 793,614 824,807 Net cash balance 165,748 82,111 179,703 147,929

Total costs (Excl Dep & Amort) to headline revenues 38.40% 41.94% 39.44% 41.88% Total cash out flow to headline revenues 78.13% 89.10% 77.36% 82.07%

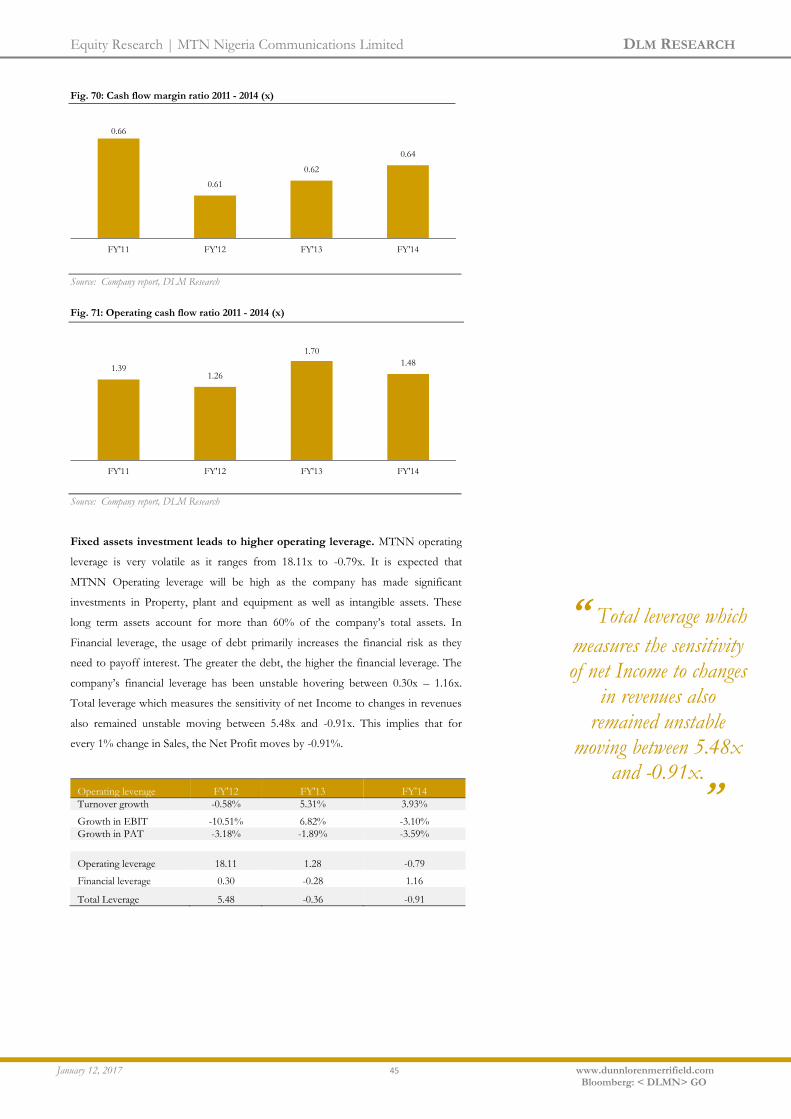

MTN has a positive free cash flow but not strong enough to support

substantial increase in dividend payout when adjusted for interest

payment. Cash Flow from Operation was mostly strong except for a decline

in FY’12 and FY’14 due largely to higher operating costs. While EBITDA level

is strong, EBITDA is only a proxy, particularly when dealing with capital

intensive companies like MTN. Hence, we relied more on free cash flow to the

firm. The reason we need FCF instead of EBITDA and operating cash flow is

the capex adjustment. Nevertheless, we think that balance sheet strength is

sufficient to support current dividend trend out to 2019E and even beyond.

Though, the company is expected to have a greater amount of free cash flow in

the near term as its expenditure on the major initiative winds down.

Fig. 10: Free Cash Flow

(FCF) FY'11 FY'12 FY'13 FY'14

Tax rate 30.7% 26.0% 27.7% 24.8%

EBITDA 466,935 437,564 490,640 479,349

EBIT 355,099 317,774 339,453 328,931

Tax on EBIT (108,998) (82,749) (94,024) (81,579)

Capital expenditures (126,556) (228,134) (229,814) (139,362)

Depreciation & Amort. 111,836 119,790 151,187 150,418

Unlevered free cash flow 231,380 126,681 166,802 258,408

\

“ Cash Flow from

Operation was mostly strong except for a

decline in FY’12 and FY’14 due largely to higher operating costs..

’’

Equity Research | MTN Nigeria Communications Limited DLM RESEARCH

January 12, 2017 9 www.dunnlorenmerrifield.com

Bloomberg: < DLMN> GO

Cash flow adjusted for interest FY'11 FY'12 FY'13 FY'14

EBITDA 466,935 437,564 490,640 479,349

Capex 126,556 228,134 229,814 139,362

Net interest expense 17,841 14,033 28,608 38,324

Cash flow adjusted for interest 322,538 195,397 232,218 301,663

Fig. 11: Cash flow margin ratio (%)

Source: Company annual report, DLM Research

We do not see signs of stabilisation in the pricing environment in Nigeria

that will drive a recovery in revenue growth in FY’16. Revenue growth

slowed in FY’14 and FY’15 and our forecasts anticipate revenue decline at 0.8%

in FY’16 before gradually recovering in the years ahead. We also expect post

2019E earnings CAGR of 1.78%. With the general economic slowdown and

industry headwinds remaining a drag on overall profitability, in the medium

term, we are of the view that MTNN’s investment in capacity and growth areas

will contribute significantly to the bottom line as data segment and e-commerce

will act as key catalysts. With increasing use of data for file sharing, video app

downloads, and web browsing, MTNN is focusing on broadband investment

even as it has invested $94 million in renewing its 2G licences and acquired

Visafone, to boost broadband services and revenue from the segment which

has been relatively low. That said, the strong outlook of broadband and

expanding geographical footprint will sustain revenue and profitability.

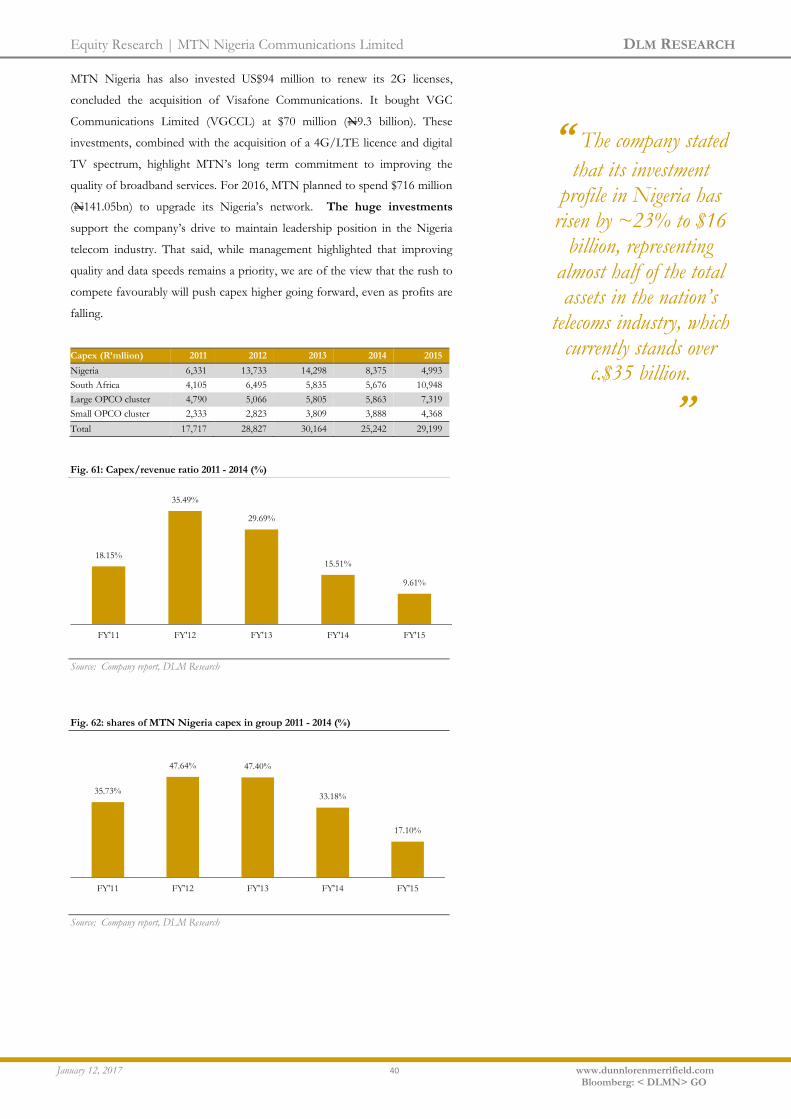

MTNN continues to maintain a significant level of investment to extend

high speed network and mobile data coverage. Given that MTN is a

capital intensive company, it spends substantial amount on a regular

basis to buy/upgrade/replace assets or equipment. It spent R47.73 billion

in last five year (2011-2015) on acquiring and renewing spectrum. While the

company maintains an average capex/revenue ratio of 23.21%, capex represent

a significant reduction in cash flow. Since capex as a percentage of revenue stay

low, we think the company will continue to spend a lot on acquisitions to

maintain its market leadership even as it is planning to double capital spending

in Nigeria in the 2016 fiscal year to $730 million. MTN Nigeria has already

indicated desire for business expansion; hence, we can expect moderate capital

commitment going ahead.

66.47%

60.52%

62.07%

63.68%

FY'11 FY'12 FY'13 FY'14

“ Revenue growth

slowed in FY’14 and FY’15 and our forecasts anticipate revenue decline

at 0.8% in FY’16 before gradually

recovering in the years ahead...

’’

Equity Research | MTN Nigeria Communications Limited DLM RESEARCH

January 12, 2017 10 www.dunnlorenmerrifield.com

Bloomberg: < DLMN> GO

Fig. 12: Capex/revenue ratio (%)

Source: Company annual report, DLM Research

The capital expenditures to depreciation ratio indicate the growth phase

of the company. Between 2011 and 2014, MTNN’s capital expenditures to

depreciation ratio averaged 1.52 which is relatively strong in our view. The high

ratio shows that MTNN has been investing in long-term assets on expectation

of future growth. However, 2014 saw a decline to 1.01 which in our view

reflects slowdown in capex and may affect its future ability to compete

successfully with other operators. This is particularly true as revenues of

companies with high capital expenditures to depreciation ratios grow more

quickly than those with low capital expenditures to depreciation ratios.

Fig. 13: Capex/Depreciation ratio (%)

Source: Company annual report, DLM Research

The Nigerian Communication Commission fine has led to a material

cash outflow, but MTN has the option to alter its dividend policy to

reduce leverage and manage its credit profile to ensure its ability to

service debt. The company uses more payables which are not matched by

receivables and inventories combined. Net debt/EBITDA has already come

down from a high of 0.47x in FY13 to 0.39x in FY14. As the company further

increases its borrowings to fund growth, the ratio may see an increase in FY16.

As at FY’14, MTN Nigeria had gross debt and cash & cash equivalent of

N393.19billion and N207.69billion respectively, implying a net debt figure of

N185.51billion. 71.72% of the gross debt was in naira, and the balance 28.28%

in USD. Given the decision to borrow $1.30billion to pay the regulatory fine

16.70%

30.27% 28.96%

16.90%

FY'11 FY'12 FY'13 FY'14

1.22

2.08

1.79

1.01

FY'11 FY'12 FY'13 FY'14

“ Between 2011 and

2014, MTNN’s capital expenditures to

depreciation ratio averaged 1.52 which is relatively strong in our

view..

’’

Equity Research | MTN Nigeria Communications Limited DLM RESEARCH

January 12, 2017 11 www.dunnlorenmerrifield.com

Bloomberg: < DLMN> GO

and fund capex needs, we estimate that the company’s net debt would increase

by over 40%, with significant exposure to exchange rate risk.

Capitalization FY'11 FY'12 FY'13 FY'14

Total debt 262,626 233,011 376,924 393,192

Net debt 156,086 197,255 232,052 185,505

Senior debt – – – –

Preferred stock 239,420 239,420 239,420 239,420

Total capitalization 502,046 472,431 616,344 632,612

Leverage FY'11 FY'12 FY'13 FY'14

Net debt / total capitalization 31.09% 41.75% 37.65% 29.32%

Total debt / EBITDA 0.56x 0.53x 0.77x 0.82x

Net debt / EBITDA 0.33x 0.45x 0.47x 0.39x

Net debt + preferred / EBITDA 0.85x 1.00x 0.96x 0.89x

Coverage FY'11 FY'12 FY'13 FY'14

EBITDA / cash interest expense 26.2x 31.2x 17.2x 12.5x

EBITDA / total interest expense 12.6x 8.8x 10.7x 7.2x

(EBITDA – capex) / cash interest expense 19.1x 14.9x 9.1x 8.9x

(EBITDA – capex) / total interest expense 9.2x 4.2x 5.7x 5.1x

DSCR 10.4x 6.5x 7.5x 6.5x

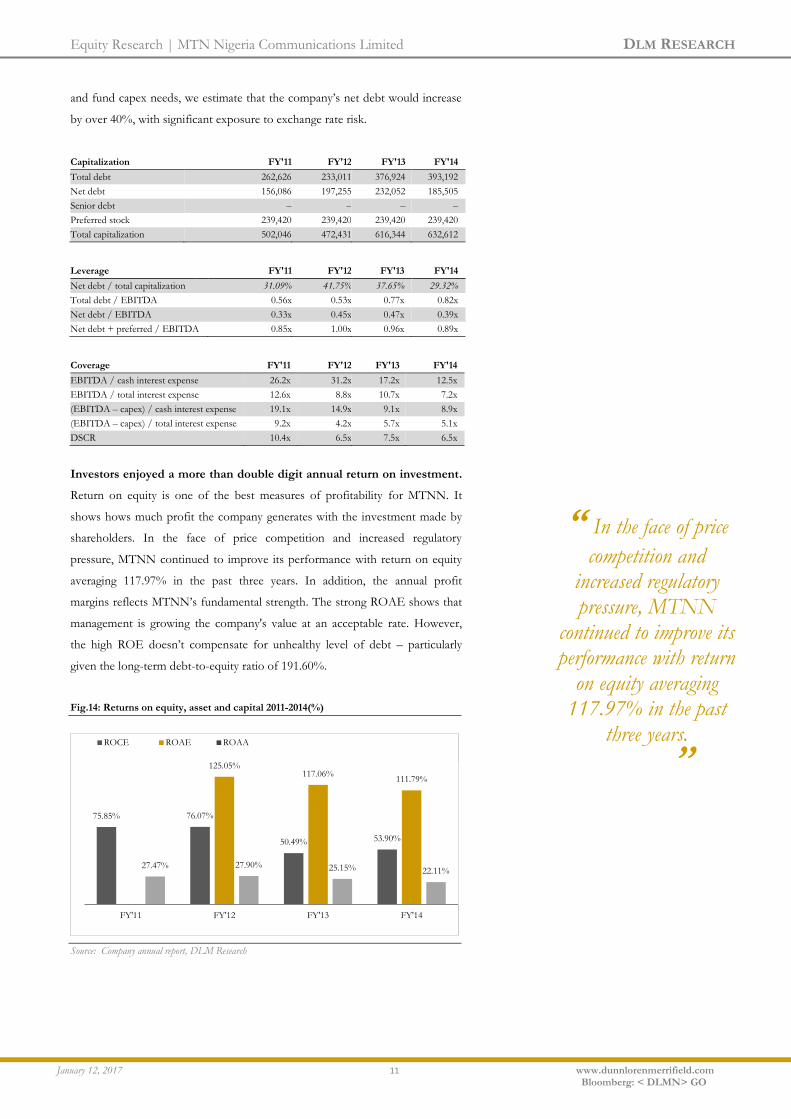

Investors enjoyed a more than double digit annual return on investment.

Return on equity is one of the best measures of profitability for MTNN. It

shows hows much profit the company generates with the investment made by

shareholders. In the face of price competition and increased regulatory

pressure, MTNN continued to improve its performance with return on equity

averaging 117.97% in the past three years. In addition, the annual profit

margins reflects MTNN’s fundamental strength. The strong ROAE shows that

management is growing the company's value at an acceptable rate. However,

the high ROE doesn’t compensate for unhealthy level of debt – particularly

given the long-term debt-to-equity ratio of 191.60%.

Fig.14: Returns on equity, asset and capital 2011-2014(%)

Source: Company annual report, DLM Research

75.85% 76.07%

50.49% 53.90%

125.05% 117.06%

111.79%

27.47% 27.90% 25.15% 22.11%

FY'11 FY'12 FY'13 FY'14

ROCE ROAE ROAA

“ In the face of price

competition and increased regulatory pressure, MTNN

continued to improve its performance with return

on equity averaging 117.97% in the past

three years. ’’

Equity Research | MTN Nigeria Communications Limited DLM RESEARCH

January 12, 2017 12 www.dunnlorenmerrifield.com

Bloomberg: < DLMN> GO

Fig. 15: Profitability margins 2011-2014(%)

Source: Company annual report, DLM Research

Current ratio increased steadily to 1.13 in 2014 as there was a growth in

borrowing which caused an increase on total current liabilities and a

rapid increase on the current ratio in 2014. The ratios have consistently

remained under 1.00 before 2014 which generally highlighted the company ‘s

negative working capital and probably suggests some liquidity crisis. However,

given the low inventory in the telecommunication industry, the low current

ratio of the company can be accepted. This in our view reflects that the majority

of the company’s assets can be categorized as non-current assets like property,

plant and equipment (PP&E) and intangible.

Fig. 16: Liquidity ratios 2011-2014 (x)

Source: Company annual report, DLM Research

Fig. 17: Working capital 2011-2014 (N’bn)

Source: Company annual report, DLM Research

61.60% 58.06%

61.82% 58.12%

46.85% 42.17% 42.77%

39.88%

30.11% 29.33% 27.32% 25.34%

FY'11 FY'12 FY'13 FY'14

EBITDA margin EBIT margin Net Profit Margin

0.91

0.43

0.85

1.13

0.92

0.44

0.85

1.13

FY'11 FY'12 FY'13 FY'14

Quick ratio Current ratio

-28.36

-203.98

-42.06

47.66

FY'11 FY'12 FY'13 FY'14

Equity Research | MTN Nigeria Communications Limited DLM RESEARCH

January 12, 2017 13 www.dunnlorenmerrifield.com

Bloomberg: < DLMN> GO

The Company

Equity Research | MTN Nigeria Communications Limited DLM RESEARCH

January 12, 2017 14 www.dunnlorenmerrifield.com

Bloomberg: < DLMN> GO

The company

MTN Nigeria Communications Limited MTNN, is a leading provider of

telecoms services to both the consumer- and the business sector in

Nigeria. The company was founded in 2001 after it secured one of the four

available licenses to operate digital Global System for Mobile

Telecommunications (GSM) with a licence fee of US$285 million for an initial

15 year period, allowing MTNN to provide and operate a 900 and 1800 MHz

second-generation digital mobile service. MTNN commenced commercial

operations in Nigeria with three cities, Lagos, Abuja and PortHarcourt.

In the absence of sufficient transmission capacity in Nigeria, MTN

embarked on the construction of a microwave transmission backbone at

a cost of US$120 million. The company offers an extensive range of services

including: cellular network access and ICT solutions. It also provides internet

services, such as video calling through its 3G network, data services mobile

internet, and mobile WiFi services. In addition, it offers international roaming

services, including data roaming, in-flight roaming, and WiFi roaming services.

It provides voice SMS, fashion and lifestyle tips, mobile TV, bulk SMS service,

mobile newspaper, conference call. Beside being the first GSM network to

make a call in Nigeria, MTNN was also the first to launch its service across

major Nigerian cities, and currently has the most expansive network coverag

across overall 3,340 cities, towns and villages in all the 36 states including the

Federal Capital Territory. In 2013, MTNN became the first telecom operator to

build a 10,000 base transceiver stations (BTS) in Nigeria. Since inception

MTNN has led the growth in the Nigeria telecom market to become the biggest

mobile operator in Nigeria with millions of subscribers joining its network. AS

at FY’15, MTNN’s subscribers’ base totalled 61.25 million subscribers before

decline to 58.4 million in the first half of 2016. The company’s subsidiary is XS

Broadband Limited, which provide broadband fixed wirless access.

MTNN’s main focus is to keep its current subscribers while also looking

to tap the growth opportunities in broaband and ICT space – both in the

consumer and business segment with the view to maximising avverge

revenue per user. Hence, this strategy has aided the achievement of its set

objectives of developing a telecommunication in emerging markets and

realizing a good return on investment (ROI).

“ MTNN commenced

commercial operations in Nigeria with three cities,

Lagos, Abuja and PortHarcourt.

’’

Equity Research | MTN Nigeria Communications Limited DLM RESEARCH

January 12, 2017 15 www.dunnlorenmerrifield.com

Bloomberg: < DLMN> GO

The shareholding structure showed that MTNN is 75.81% owned by

MTN international (Mauritius) Limited which itself operates as a

subsidiary of MTN Group Ltd; 18.7% held by Nigerian shareholders through

special purpose vehicles; 2.78% owned by Mobile Telephone Networks NIC

B.V and 2.71% owned by Shanduka Telecommunication (Mauritius) Limited.

The current shareholding structure would give MTN the clout to alienate

minority shareholders. MTN Nigeria’s issued share capital comprises

402,590,263 Ordinary Shares, 4,500,000 ‘B’ Ordinary Shares which was issued

to MTN international (Mauritius) Limited. Each Ordinary Share is linked to one

Preference Share (402,590,263 Preference Shares) thereby constituting

402,590,263 Linked Units. From the above, we estimate the outstanding shares

to be 407,063,044. That said, there is possibility for further capital raising, as the

company is looking to raise c.$1 billion from the planned listing of its Nigerian

unit.

Fig. 18: Shareholding structure (%)

Source: Company website, DLM Research

MTN Nigeria takes step towards listing on the Nigerian Stock

Exchange. The optimistic expectations from the market showed great

appetite for Telecoms. While we believe the listing will have a positive impact

on the market, giving the anticipated substantial boost to the market

capitalization, we think that the listing is part of government strategy to allow

Nigerians to hold its shares amongst others. The listing will also have positive

impacts on the company among which are; 1) creates a market valuation for the

business and enables MTN the opportunity to raise capital to fund future

growth. 2) Creates a public profile and improves the ability to attract high

profile board members. 3) Improve investor & customer confidence and

corporate governance structure. However, this positivity must be balanced

against the disadvantages among which are accountability, strong regulatory

scrutiny, higher professional fees and the need for transparency.

75.81%

18.70%

2.78% 2.71%

MTN Int'l Ltd Nig shareholders NIC B.V Shanduka Telcos

“ That said, there is

possibility for further fund raising, as the

company is looking to raise c.$1 billion from

the planned listing of its Nigerian.

’’

Equity Research | MTN Nigeria Communications Limited DLM RESEARCH

January 12, 2017 16 www.dunnlorenmerrifield.com

Bloomberg: < DLMN> GO

The listing is part of MTNN’s negotiation strategy with Nigerian

Communication Commission (NCC). While MTNN has begun initiating

procedures for the listing, it is uncertain at this time the numbers of shares to

be put on the stock exchange from the outstanding shares for public investors.

Post listing, we believe there will be more financial disclosures giving more

clarity on its business operations. That said, there are chances the listing will be

delayed for a number of reasons with market timing a major factor to be

considered. in addition, though the bulk of the share is held by its subsidiary,

we anticipate a scenario of limited float and the shares being tightly held by a

few investors.

Post listing we are of the view that the company may carefully consider

issue of capital management and would most likely buy back shares in

line with the group’s capital management strategy. Though, buying back

shares could push the company’s EPS and RoE higher than the company-wide

earnings. This will effectively reduce the company’s shares in existence. One of

the major reasons for this will be to fuel dividend growth. If the company

maintain the current dividend pay-out each year, and the number of total shares

is decreased, shareholder will be receiving a larger dividend each year– with the

group maintaining significant advantage over other investors due to its

shareholding status. The success of this if considered, will depend largely on

The Nigerian Stock Exchange regulation on listing

MTNN to raise funds through Initial Public Offer for multiple payments.

The company is targeting about $1billion to settle the regulatory fine of N330

billion which has not been fully settled. The second which is very vital is the

company’s quest to invest in capex. Though the company has not announced

any guidance on the planned IPO, we believe MTN may offer a small portion

of its stake in the business as minority shareholders will be unwilling to sell

down their holdings or exit. With the current shareholding’s structure, we do

not envisage a scenario for hostile takeover by any single investors or

divestment by majority owners aimed at dispersing its stock among high net-

worth Nigerians. On the other hand, with ownership dilution protection in

mind, we anticipate a scenario where treasury stock will be created to keep a

controlling interest within the treasury with the view to ward off hostile

takeovers by any single investors.

“ The company is

targeting about $1billion to settle the

regulatory fine of N330 billion which has not been fully

settled ’’

Equity Research | MTN Nigeria Communications Limited DLM RESEARCH

January 12, 2017 17 www.dunnlorenmerrifield.com

Bloomberg: < DLMN> GO

SWOT Analysis

Strength and Opportunities

1. Good access to funding

2. Strong market position

3. The MTN brand enjoys a high level of consumer awareness and

attraction as a result of strong advertising and sponsorship activities

4. Information on competitor's activities

5. Growing mobile and internet market

6. Low mobile penetration rates in some markets

Weakness &Threat Weakness &Threat 1. Increasing cost of operation

2. Intense price competition in the market

3. Corporate governance, regulatory and political uncertainties

4. General slowdown in economic activities which may affect earnings

growth.

5. The uprising insecurity on network facility.

6. Too many expansions can lead to loss of focus

7. Mobile number portability may impact growth

Equity Research | MTN Nigeria Communications Limited DLM RESEARCH

January 12, 2017 18 www.dunnlorenmerrifield.com

Bloomberg: < DLMN> GO

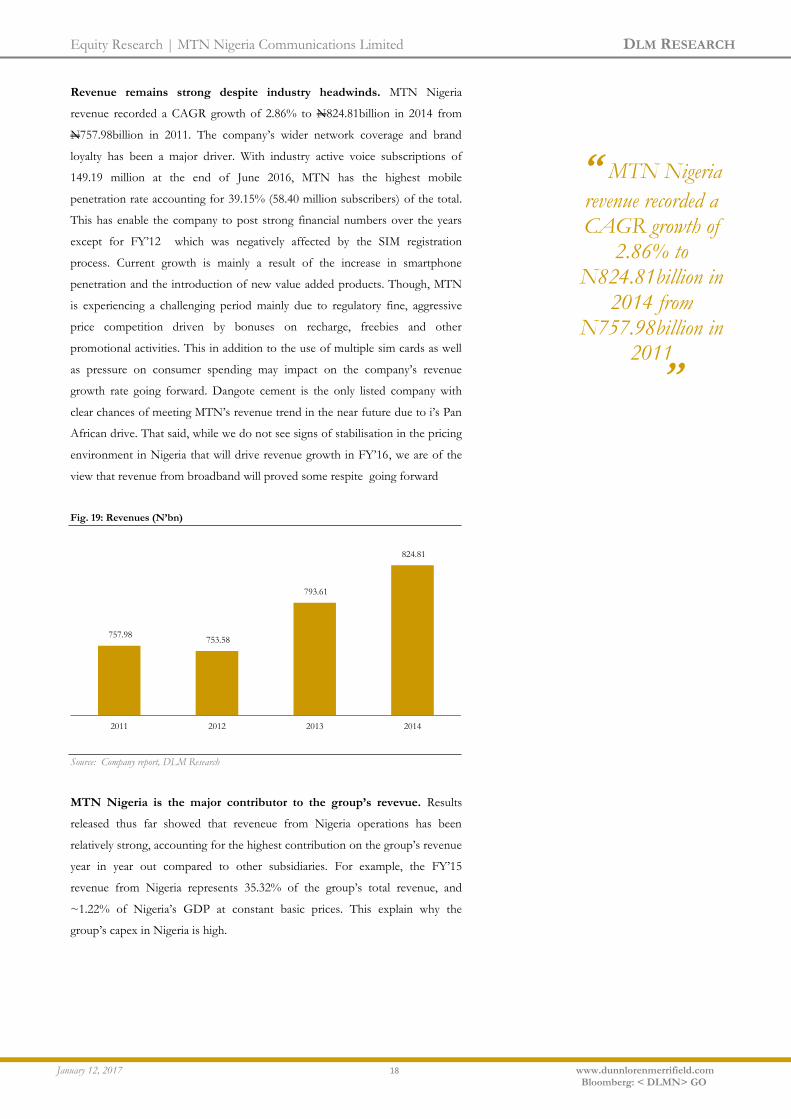

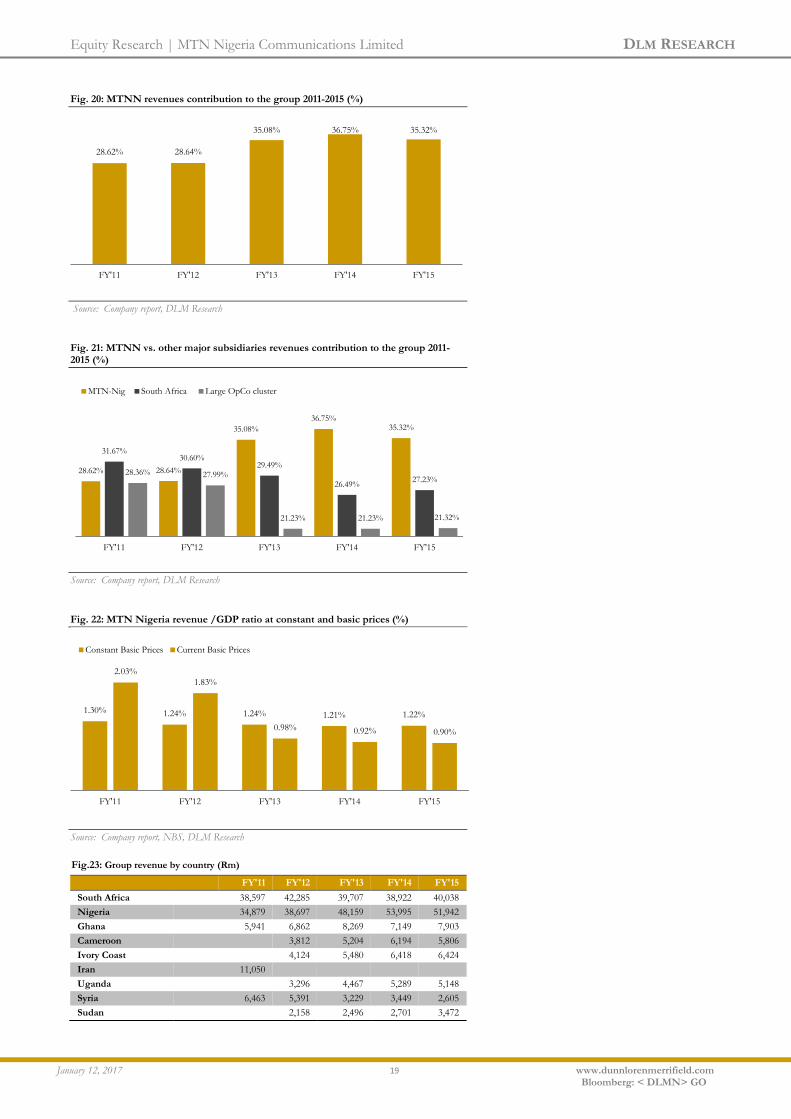

Revenue remains strong despite industry headwinds. MTN Nigeria

revenue recorded a CAGR growth of 2.86% to N824.81billion in 2014 from

N757.98billion in 2011. The company’s wider network coverage and brand

loyalty has been a major driver. With industry active voice subscriptions of

149.19 million at the end of June 2016, MTN has the highest mobile

penetration rate accounting for 39.15% (58.40 million subscribers) of the total.

This has enable the company to post strong financial numbers over the years

except for FY’12 which was negatively affected by the SIM registration

process. Current growth is mainly a result of the increase in smartphone

penetration and the introduction of new value added products. Though, MTN

is experiencing a challenging period mainly due to regulatory fine, aggressive

price competition driven by bonuses on recharge, freebies and other

promotional activities. This in addition to the use of multiple sim cards as well

as pressure on consumer spending may impact on the company’s revenue

growth rate going forward. Dangote cement is the only listed company with

clear chances of meeting MTN’s revenue trend in the near future due to i’s Pan

African drive. That said, while we do not see signs of stabilisation in the pricing

environment in Nigeria that will drive revenue growth in FY’16, we are of the

view that revenue from broadband will proved some respite going forward

Fig. 19: Revenues (N’bn)

Source: Company report, DLM Research

MTN Nigeria is the major contributor to the group’s revevue. Results

released thus far showed that reveneue from Nigeria operations has been

relatively strong, accounting for the highest contribution on the group’s revenue

year in year out compared to other subsidiaries. For example, the FY’15

revenue from Nigeria represents 35.32% of the group’s total revenue, and

~1.22% of Nigeria’s GDP at constant basic prices. This explain why the

group’s capex in Nigeria is high.

757.98 753.58

793.61

824.81

2011 2012 2013 2014

“ MTN Nigeria

revenue recorded a CAGR growth of

2.86% to N824.81billion in

2014 from N757.98billion in

2011 ’’

Equity Research | MTN Nigeria Communications Limited DLM RESEARCH

January 12, 2017 19 www.dunnlorenmerrifield.com

Bloomberg: < DLMN> GO

Fig. 20: MTNN revenues contribution to the group 2011-2015 (%)

Source: Company report, DLM Research

Fig. 21: MTNN vs. other major subsidiaries revenues contribution to the group 2011-2015 (%)

Source: Company report, DLM Research

Fig. 22: MTN Nigeria revenue /GDP ratio at constant and basic prices (%)

Source: Company report, NBS, DLM Research

28.62% 28.64%

35.08% 36.75% 35.32%

FY'11 FY'12 FY'13 FY'14 FY'15

28.62% 28.64%

35.08%

36.75% 35.32%

31.67% 30.60%

29.49%

26.49% 27.23%

28.36% 27.99%

21.23% 21.23% 21.32%

FY'11 FY'12 FY'13 FY'14 FY'15

MTN-Nig South Africa Large OpCo cluster

1.30% 1.24% 1.24% 1.21% 1.22%

2.03%

1.83%

0.98% 0.92% 0.90%

FY'11 FY'12 FY'13 FY'14 FY'15

Constant Basic Prices Current Basic Prices

Fig.23: Group revenue by country (Rm)

FY'11 FY'12 FY'13 FY'14 FY'15

South Africa 38,597 42,285 39,707 38,922 40,038

Nigeria 34,879 38,697 48,159 53,995 51,942

Ghana 5,941 6,862 8,269 7,149 7,903

Cameroon

3,812 5,204 6,194 5,806

Ivory Coast

4,124 5,480 6,418 6,424

Iran 11,050

Uganda

3,296 4,467 5,289 5,148

Syria 6,463 5,391 3,229 3,449 2,605

Sudan

2,158 2,496 2,701 3,472

Equity Research | MTN Nigeria Communications Limited DLM RESEARCH

January 12, 2017 20 www.dunnlorenmerrifield.com

Bloomberg: < DLMN> GO

The majority (68.42%) of MTN’s revenue comes from selling mobile

voice (airtime) and subscription, a decrease of 9.02% from 77.44% in

2011. With some markets almost at maturity, the relative share of voice and

messaging revenue is likely to decline, but demand for communication services

is still strong. The popularity of over-the-top services such as Skype, Facebook,

WhatsApp, Messenger, Viber, WeChat, 2go, BBM, Netflix among others for

internet calls, means that subscribers are gradually moving away from voice

centric to data centric as it offers a cheaper means of communication. This is

even through as these platforms are gradually eroding revenue that GSM

operators are making from short message service (SMS).

Revenue from airtime & subscription recorded a decline of 3.87% from

N587.01billion in 2011 to N564.30billion in 2014, which in our view is a direct

reflection of loss of market share, and reduction in voice termination rates.

Mobile subscription in Nigeria is mainly prepaid by topping up airtime in

advance of usage with an insignificant monthly payment via fixed term

contracts. As competition persists, MTN is responding with various

promotions, new tariff plans and bundled offerings. The termination rates for

voice services provided by new entrants and small operators in Nigeria

irrespective of the originating network was set at ₦6.40 from April 1, 2013;

₦5.20 from April 1, 2014; and ₦3.90 from April 1, 2015. The termination rates

for voice services provided by other operators irrespective of the originating

network were set at ₦4.90 from April 1, 2013; ₦4.40 from April 1, 2014; and

₦3.90 from April 1, 2015.

Fig. 24: Revenue from airtime & subscription (million)

Source: Company annual report, DLM Research

587.01

530.32

569.17 564.3

2011 2012 2013 2014

“ Revenue from

airtime & subscription recorded a decline of

3.87% from N587.01billion in

2011 to N564.30billion in

2014, which in our view is a direct reflection of loss of market share, and reduction in voice

termination rates.

’’

Equity Research | MTN Nigeria Communications Limited DLM RESEARCH

January 12, 2017 21 www.dunnlorenmerrifield.com

Bloomberg: < DLMN> GO

Fig. 25: Airtime & subscription contribution to revenue (%)

Source: Company annual report, DLM Research

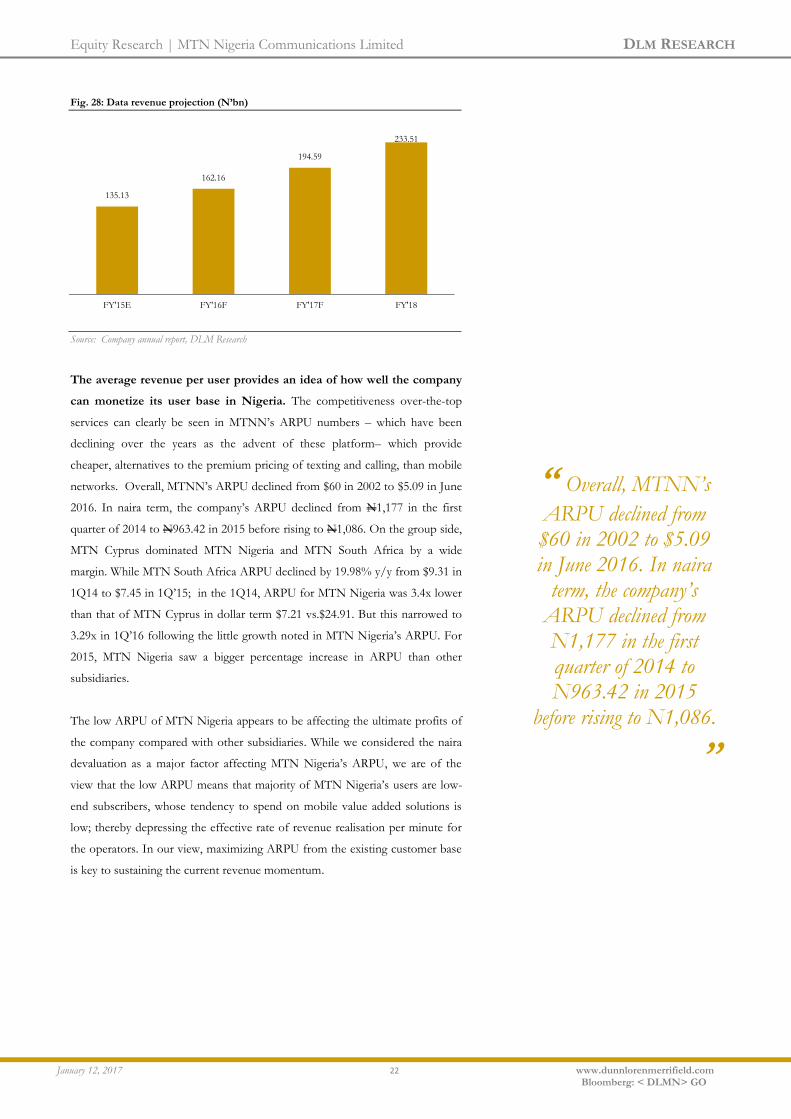

Data revenue is growing and is expected to hit the N150 billion mark by

the end of 2016 as data usage increases. This is part of the company’s

strategy to boost the declining average revenues per user (ARPU).following the

acquisition of Visafone with focus on enhancing data and internet services.

MTN strategy is to tap into the growth opportunities in the e-commerce field,

expand its product offering outside of traditional voice, increase presence in the

digital space by leveraging technologies and taking advantage of low levels of

internet penetration in a bid to generate a substantial amount of income from

the sector. With increasing use of data for over-the-top services, video and app

download; we see e-commerce and data income as a good long-term bet for

MTN’s endeavours to diversify revenue to cushion the effect of low ARPU in

Nigeria.

Fig. 26: Income contribution

Airtime & Subscription 587,011 530,316 569,168 564,301

Data 37,889 80,788 93,566 105,572

SMS 22,474 31,313 19,338 15,823

Interconnect & Roaming 91,705 92,334 77,173 86,846

Handset & Accessories 1,701 2,439 1,705 223

Others 17,199 26,388 32,664 52,041

Total 757,979 763,578 793,614 824,806

Fig. 27: Data contribution to revenue (%)

Source: Company annual report, DLM Research

77.44%

70.37%

71.72%

68.42%

FY'11 FY'12 FY'13 FY'14

5.00%

10.72%

11.79% 12.80%

FY'11 FY'12 FY'13 FY'14

“ With increasing use

of data for over-the-top services, video and app

download; we see e-commerce and data

income as a good long-term bet for MTN’s

endeavours to diversify revenue to cushion the effect of low ARPU in

Nigeria

’’

Equity Research | MTN Nigeria Communications Limited DLM RESEARCH

January 12, 2017 22 www.dunnlorenmerrifield.com

Bloomberg: < DLMN> GO

Fig. 28: Data revenue projection (N’bn)

Source: Company annual report, DLM Research

The average revenue per user provides an idea of how well the company

can monetize its user base in Nigeria. The competitiveness over-the-top

services can clearly be seen in MTNN’s ARPU numbers – which have been

declining over the years as the advent of these platform– which provide

cheaper, alternatives to the premium pricing of texting and calling, than mobile

networks. Overall, MTNN’s ARPU declined from $60 in 2002 to $5.09 in June

2016. In naira term, the company’s ARPU declined from N1,177 in the first

quarter of 2014 to N963.42 in 2015 before rising to N1,086. On the group side,

MTN Cyprus dominated MTN Nigeria and MTN South Africa by a wide

margin. While MTN South Africa ARPU declined by 19.98% y/y from $9.31 in

1Q14 to $7.45 in 1Q’15; in the 1Q14, ARPU for MTN Nigeria was 3.4x lower

than that of MTN Cyprus in dollar term $7.21 vs.$24.91. But this narrowed to

3.29x in 1Q’16 following the little growth noted in MTN Nigeria’s ARPU. For

2015, MTN Nigeria saw a bigger percentage increase in ARPU than other

subsidiaries.

The low ARPU of MTN Nigeria appears to be affecting the ultimate profits of

the company compared with other subsidiaries. While we considered the naira

devaluation as a major factor affecting MTN Nigeria’s ARPU, we are of the

view that the low ARPU means that majority of MTN Nigeria’s users are low-

end subscribers, whose tendency to spend on mobile value added solutions is

low; thereby depressing the effective rate of revenue realisation per minute for

the operators. In our view, maximizing ARPU from the existing customer base

is key to sustaining the current revenue momentum.

135.13

162.16

194.59

233.51

FY'15E FY'16F FY'17F FY'18

“ Overall, MTNN’s

ARPU declined from $60 in 2002 to $5.09 in June 2016. In naira

term, the company’s ARPU declined from N1,177 in the first quarter of 2014 to N963.42 in 2015

before rising to N1,086.

’’

Equity Research | MTN Nigeria Communications Limited DLM RESEARCH

January 12, 2017 23 www.dunnlorenmerrifield.com

Bloomberg: < DLMN> GO

Fig. 29: MTN Nigeria ARPU ($)

Source: Company annual report, DLM Research

Fig. 30: MTN Nigeria ARPU (Naira)

Source: Company annual report, DLM Research

Fig. 31: MTN Nigeria ARPU Trend ($)

Source: Company annual report, DLM Research

Fig. 32: MTNN ARPU vs. other subsidiaries ($)

Source: Company annual report, DLM Research

7.21

6.92 6.91

6.47

5.68

5.25

4.99 4.87

5.4

5.09

1Q14 1Q15 1Q16 2Q16

1,177.82

1,124.34 1,123.29 1,118.11 1,102.59

1,046.45

994.44

963.42

1,078.00 1,086

1Q14 1Q15 1Q16 2Q16

60

57

51

2002 2003 2004

7.21 6.92 6.91 6.47 5.68 5.25 4.99 4.87 5.4

9.31 8.86

8.34 8.21 7.45 7.46 7.22 6.4 3.32

24.91

27.35 25.39

21.99

19.35 19.37 19.8 18.38 17.78

11.46 11.21 12.06 10.54

9.14 9.02 9.48 9.0 8.0

1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16

Nigeria SA Cyprus Congo.B

Equity Research | MTN Nigeria Communications Limited DLM RESEARCH

January 12, 2017 24 www.dunnlorenmerrifield.com

Bloomberg: < DLMN> GO

Fig. 33: MTN Nigeria vs. other subsidiaries ARPU growth trend analysis (Rebased)

Source: Company annual report, DLM Research

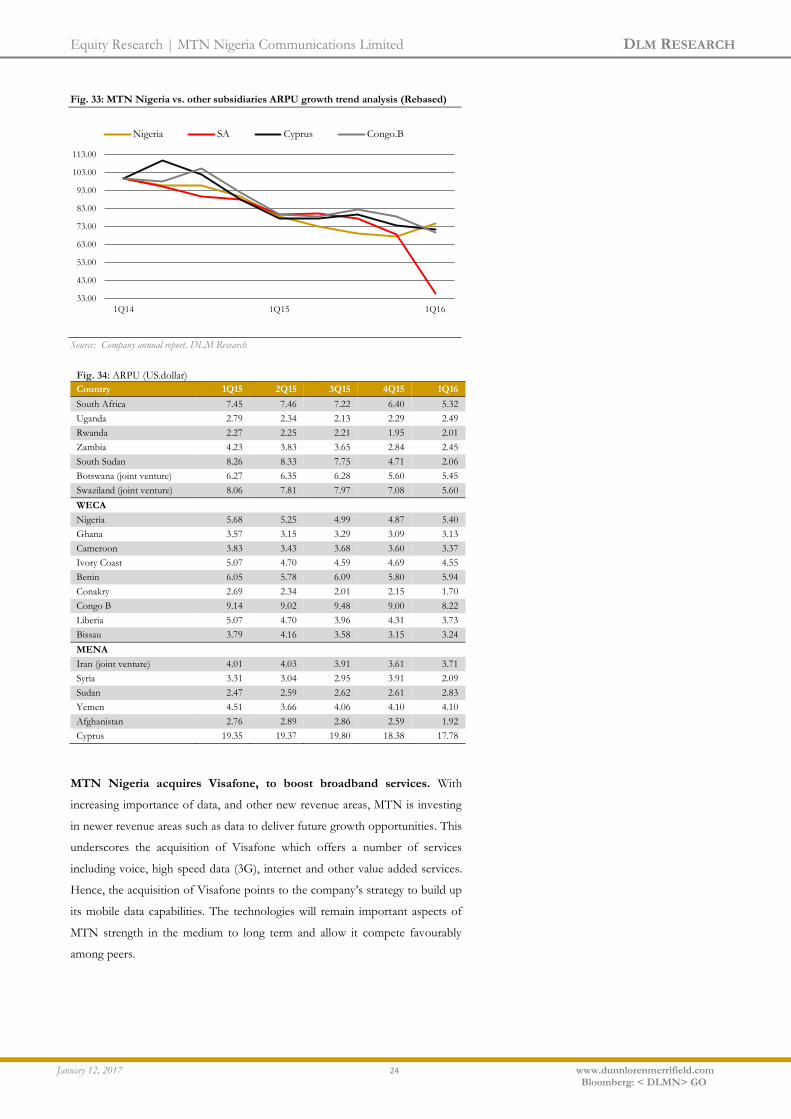

Fig. 34: ARPU (US.dollar) Country 1Q15 2Q15 3Q15 4Q15 1Q16

South Africa 7.45 7.46 7.22 6.40 5.32

Uganda 2.79 2.34 2.13 2.29 2.49

Rwanda 2.27 2.25 2.21 1.95 2.01

Zambia 4.23 3.83 3.65 2.84 2.45

South Sudan 8.26 8.33 7.75 4.71 2.06

Botswana (joint venture) 6.27 6.35 6.28 5.60 5.45

Swaziland (joint venture) 8.06 7.81 7.97 7.08 5.60

WECA

Nigeria 5.68 5.25 4.99 4.87 5.40

Ghana 3.57 3.15 3.29 3.09 3.13

Cameroon 3.83 3.43 3.68 3.60 3.37

Ivory Coast 5.07 4.70 4.59 4.69 4.55

Benin 6.05 5.78 6.09 5.80 5.94

Conakry 2.69 2.34 2.01 2.15 1.70

Congo B 9.14 9.02 9.48 9.00 8.22

Liberia 5.07 4.70 3.96 4.31 3.73

Bissau 3.79 4.16 3.58 3.15 3.24

MENA

Iran (joint venture) 4.01 4.03 3.91 3.61 3.71

Syria 3.31 3.04 2.95 3.91 2.09

Sudan 2.47 2.59 2.62 2.61 2.83

Yemen 4.51 3.66 4.06 4.10 4.10

Afghanistan 2.76 2.89 2.86 2.59 1.92

Cyprus 19.35 19.37 19.80 18.38 17.78

MTN Nigeria acquires Visafone, to boost broadband services. With

increasing importance of data, and other new revenue areas, MTN is investing

in newer revenue areas such as data to deliver future growth opportunities. This

underscores the acquisition of Visafone which offers a number of services

including voice, high speed data (3G), internet and other value added services.

Hence, the acquisition of Visafone points to the company’s strategy to build up

its mobile data capabilities. The technologies will remain important aspects of

MTN strength in the medium to long term and allow it compete favourably

among peers.

33.00

43.00

53.00

63.00

73.00

83.00

93.00

103.00

113.00

1Q14 1Q15 1Q16

Nigeria SA Cyprus Congo.B

Equity Research | MTN Nigeria Communications Limited DLM RESEARCH

January 12, 2017 25 www.dunnlorenmerrifield.com

Bloomberg: < DLMN> GO

The acquisition gives MTN edge over other mobile operators as the first major

operator to introduce 4G voice telephony which would improve e-commerce

sector, banking; insurance and financial services, software and IT enabled

services and widens the revenue base of the company. We think that MTN will

integrate the operation of Visafone into its GSM operation, and run it as voice

over its 4G Long Term Evolution (LTE) technology network as against the

initial plans to run Visafone as a Code Division Multiple Access. The new

800MHz frequency band will enable MTN to compete effectively with

Globacom which has 700 MHz spectrum.

MTN Nigeria account for the highest subscribers in the group’s total

subscribers. Despite the growing competition in the industry, MTNN

recorded 22.6 million net additional subscribers in the last 5years (2010-2015)

following regulatory approval of select promotional offerings from October

2014. As at December 2015, MTNN recorded 61.3 million subscribers,

representing 58.40% growth between 2010 and 2015, and accounted for

26.37% of the group’s total subscribers. In 2015 alone, MTN Nigeria recorded

a 2.34% growth by ramping up 1.4 million customers in a year that saw its

parent company also increasing customer base by 9.1million to 232.5 million

subscribers, representing 4.07% growth y-o-y.

Fig. 35: MTNN subscribers’ vs. Group subscribers 2010-2015 (million)

Source: Company annual report, DLM Research

Fig. 36: MTNN subscribers’ contribution to group’s total subscribers’ (%)

Source: Company annual report, DLM Research

38.7 41.6 47.4 56.8 59.9 61.3

141.6

164.5

189.3 207.8

223.4 232.5

FY'10 FY'11 FY'12 FY'13 FY'14 FY'15

MTN Nig MTN Group

27.33%

25.29% 25.04%

27.33%

26.81%

26.37%

FY'10 FY'11 FY'12 FY'13 FY'14 FY'15

“ Despite the growing

competition in the industry, MTNN

recorded 22.6 million net additional

subscribers in the last 5years (2010-2015) following regulatory approval of select

promotional offerings from October 2014

’’

Equity Research | MTN Nigeria Communications Limited DLM RESEARCH

January 12, 2017 26 www.dunnlorenmerrifield.com

Bloomberg: < DLMN> GO

Fig. 37: MTN Nigeria subscribers’ vs. other major subsidiaries FY 2015 (million)

Source: Company annual report, DLM Research

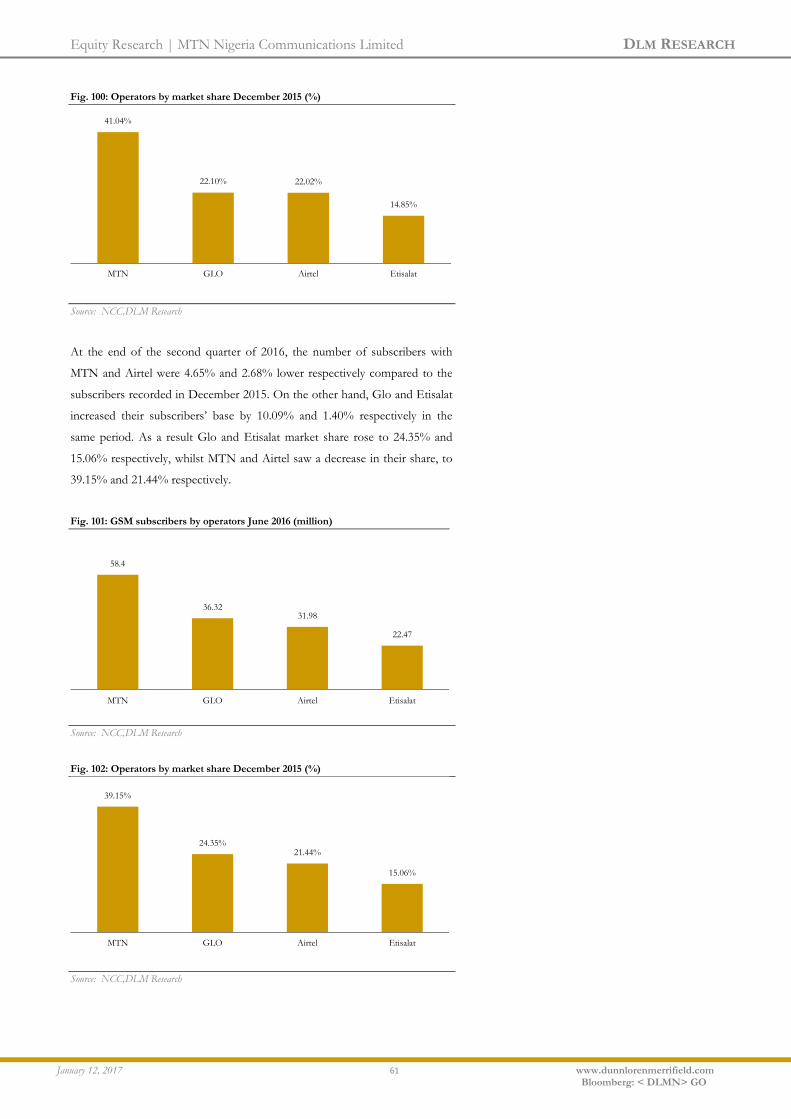

MTN’s market share is beginning to wane as more subscribers switches

to other operators. Though it reported a 2.3% increase in subscribers to 61.25

million in FY’15, its market share declined to 41.04%. According to data from

the Nigerian Communications Commission (NCC), Globacom recorded 68% of

all additional GSM lines in Nigeria between June 2015 – June 2016. Specifically,

a total of 7,477,977 new lines were activated between period, with Globacom

adding 5,063,895 new susbcribers, while Airtel added 2,414,082 new customers.

On the other hand, MTN and Etisalat experienced a reduction of 4,403,344 and

382,336 subscribers respectively. Hence, MTN’s market declined to 39.15% by

the end of June, 2016. In spite of the reduction, however MTN’s average size of

transaction is almost twice that of peers. While we see this as a drag on MTN’s

overall performance, we think that the malaise stemmed from heightened

regulatory pressure, which led to the disconnection of 6.7 million subscribers in

compliance with the subscriber registration process. While MTN has intensified

effort to complete the registration process with the disconnected subscribers,

there are chances that some of the subscriibers have migrated to other service

providers. A major strategy the company have deploy to increase its subscriber

base is to offer competitive pricing plans and promotions offer.

Fig.38: Industry subscribers- June 2016 (million)

Source: Company report NCC, DLM Research

61.3

30.6

46.1

57.1

37.4

Nig SA IRAN Large OPCO Cluster Small OPCO Cluster

58.4

36.32 31.98

22.47

MTN GLO Airtel Etisalat

“ Though it reported a

2.3% increase in subscribers to 61.25 million in FY’15, its

market share declined to 41.04%.

’’

Equity Research | MTN Nigeria Communications Limited DLM RESEARCH

January 12, 2017 27 www.dunnlorenmerrifield.com

Bloomberg: < DLMN> GO

Fig. 39: Market share –June 2016 (million)

Source: Company report NCC, DLM Research

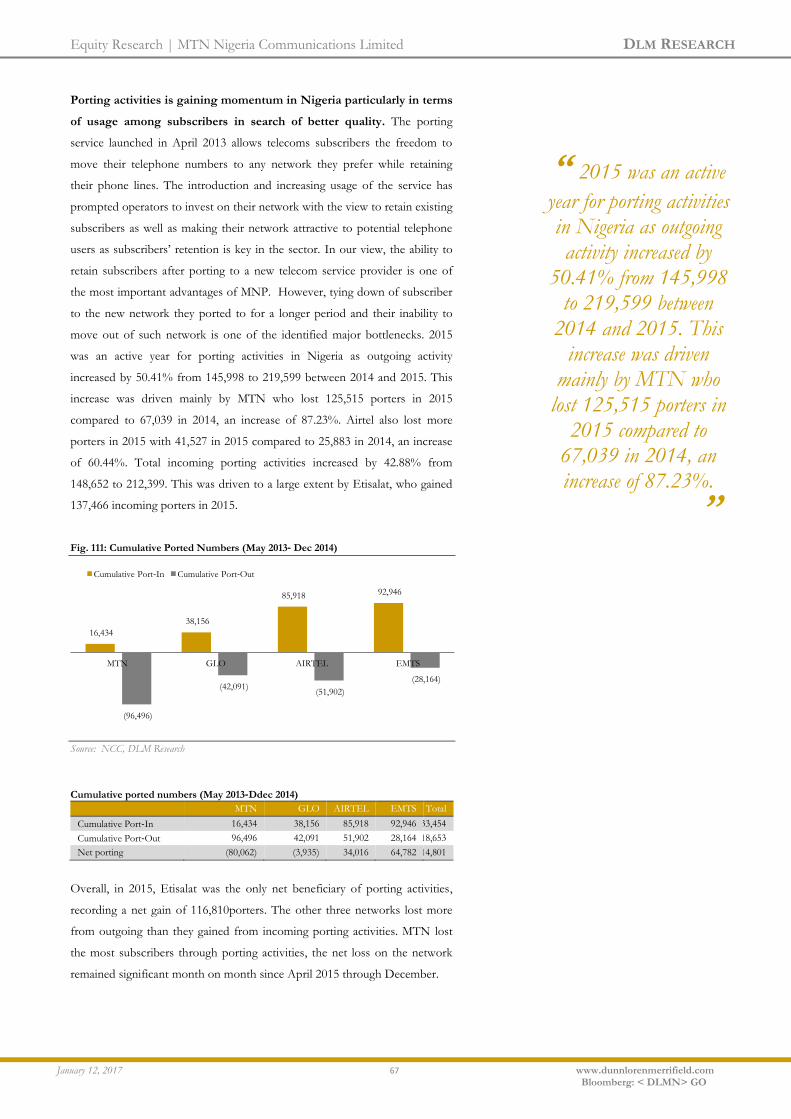

The mobile number portability process has had its heaviest negative

impact on MTNN. The porting service launched in April 2013 allows

telecoms subscribers the freedom to move their telephone numbers to any

network of their preference while retaining their phone lines. Since its

introduction, MTNN has lost the most subscribers as its share of outgoing

porting activity remains high. This in our view reflects changes in subscribers

network preference for a number of reasons among which are network

quality, tarriff and promotional tarriff offer by competitors. For example, in its

first year of introduction (May 2013- December 2014), MTNN recorded

96,496 representing 44.13% of the 218,653 outging porting activities. On the

other hand, the company’s incoming porting remained relatively low at 16,434,

representing 7.04% of the total. Further more, in 2015, while the industry

recorded outgoing porting activitis of 219,599, MTNN’s share of the industry

stood at 125,515, representing 57%. MTNN’s incoming porting for 2015

remained low at 10,936, representing 5.15% of the total. In the first half of

2016, there were a total of 112,875 incoming porters, of which MTN recorded

the smallest share of the incoming porting accounted for 4,231 or 3.75%. On

the other hand, there were a total of 113,329 outgoing porters in the half of

2016, MTN recorded the largest of 57,933 and accounted for 51.12% of the

total outgoing porting activity for the period.

Fig. 40: MTNN porting activities Jan –June 2016

Source: NCC, DLM Research

42.88%

21.34% 20.18%

15.60%

39.15%

24.35% 21.44%

15.06%

MTN GLO Airtel Etisalat

2015 2016

450 542 361 547 990 1,341

-8,430

-10,562 -12,044

-8,115

-10,189

-8,593

Jan-16 Feb Mar Apr May Jun-16

Port-in Port-out

“ The mobile number

portability process has had its heaviest negative

impact on MTNN

’’

Equity Research | MTN Nigeria Communications Limited DLM RESEARCH

January 12, 2017 28 www.dunnlorenmerrifield.com

Bloomberg: < DLMN> GO

Fig. 41: MTNN porting activities 2015

Source: NCC, DLM Research

Higher operating cost holding back operating profits. MTN has been

unable to increase operating profits by as much as 2% CAGR since 2011

as operating costs continues to exert pressure on operating profits and

margins. Operating overhead in Nigeria appears high with very wide cost

structure which comprises of NCC levies, site maintenance cost, leased capacity

cost, diesel cost, high valued equipment maintenance contracts, and community

relation costs. The upsurge in these costs has given way to decline in operating

profit. MTN’s operating expenses rose from N402.88 billion in 2011 to

N495.88billion. On the other hand, operating profit declined from N355.01

billion in 2011 to N328.93 billion in 2014. Despite the increase in general cost

level, we believe MTN needs to be cost efficient to address this negative trend

going forward. The major drivers of costs are depreciation, and direct network

operation costs. While tower maintenance is one of the biggest costs, MTN sold

9,151 of its Nigerian cell towers to infrastructure company IHS in order to drive

down its operating costs as the towers were expensive to maintain. Some of the

underlined challenges were; inaccessible roads to some of the tower, high

security costs and weak power supply. The lack of stable power supply in

Nigeria has meant MTNN run up high operating costs that affect its profit level.

For instance, in 2014, MTN Nigeria spent c.N30.5billion on the purchase of

diesel. The company’s high power bill accounts for over 50% of its operating

costs.

Fig. 42: Operating cost and cost to revenue ratio 2011-2014 (Billion, %)

Source: Company annual report, DLM Research

1,186 1,478 1,559 994 657 536 951 737 599 1,068 735 436

(6,571) (6,951) (7,439) (8,161) (9,558)

(11,918)

(19,214)

(11,218) (12,259)

(10,073) (11,414) (10,739)

Jan-15 Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec-15

Port-in Port-out

50.00%

52.00%

54.00%

56.00%

58.00%

60.00%

62.00%

350.00

400.00

450.00

500.00

550.00

600.00

2011 2012 2013 2014

Operating costs Cost to revenue

“ MTN’s operating

expenses rose from N402.88 billion in

2011 to N495.88billion. On

the other hand, operating profit declined from N355.01 billion in 2011 to N328.93 billion in 2014.

’’

Equity Research | MTN Nigeria Communications Limited DLM RESEARCH

January 12, 2017 29 www.dunnlorenmerrifield.com

Bloomberg: < DLMN> GO

Fig.43: Operating profit , OP. cost/profit ratios and OP. margins (Billion, %)

Source: Company annual report, DLM Research

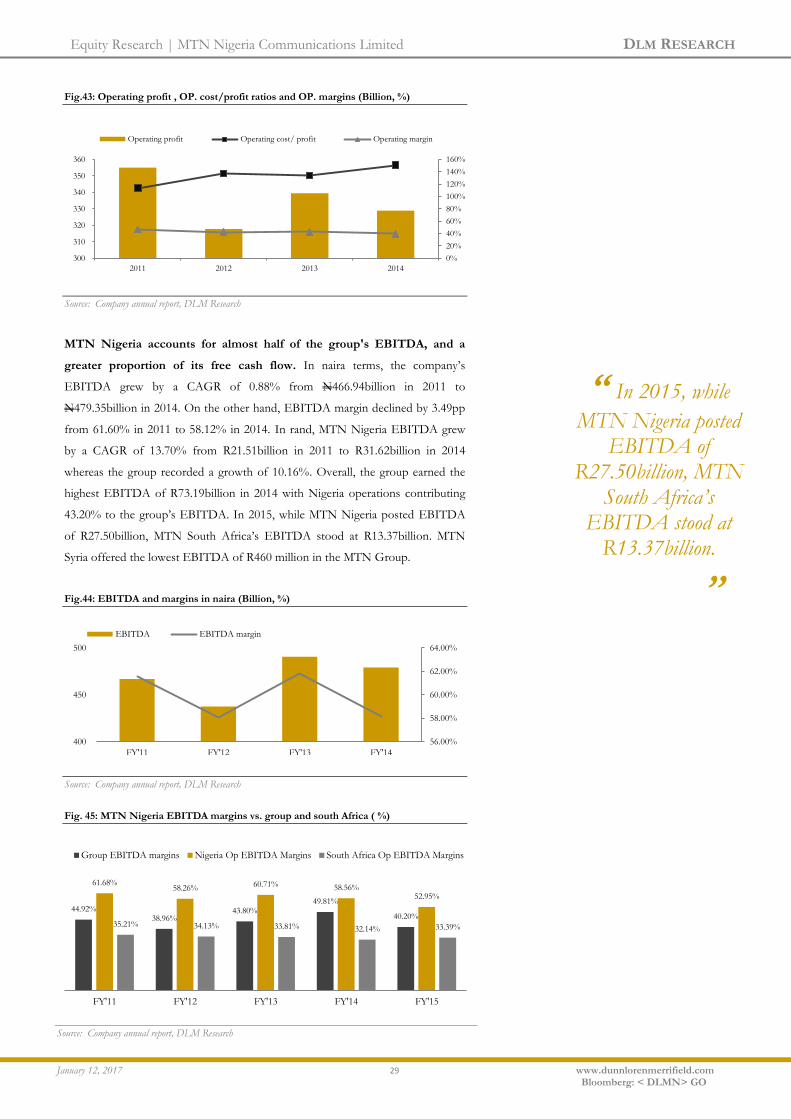

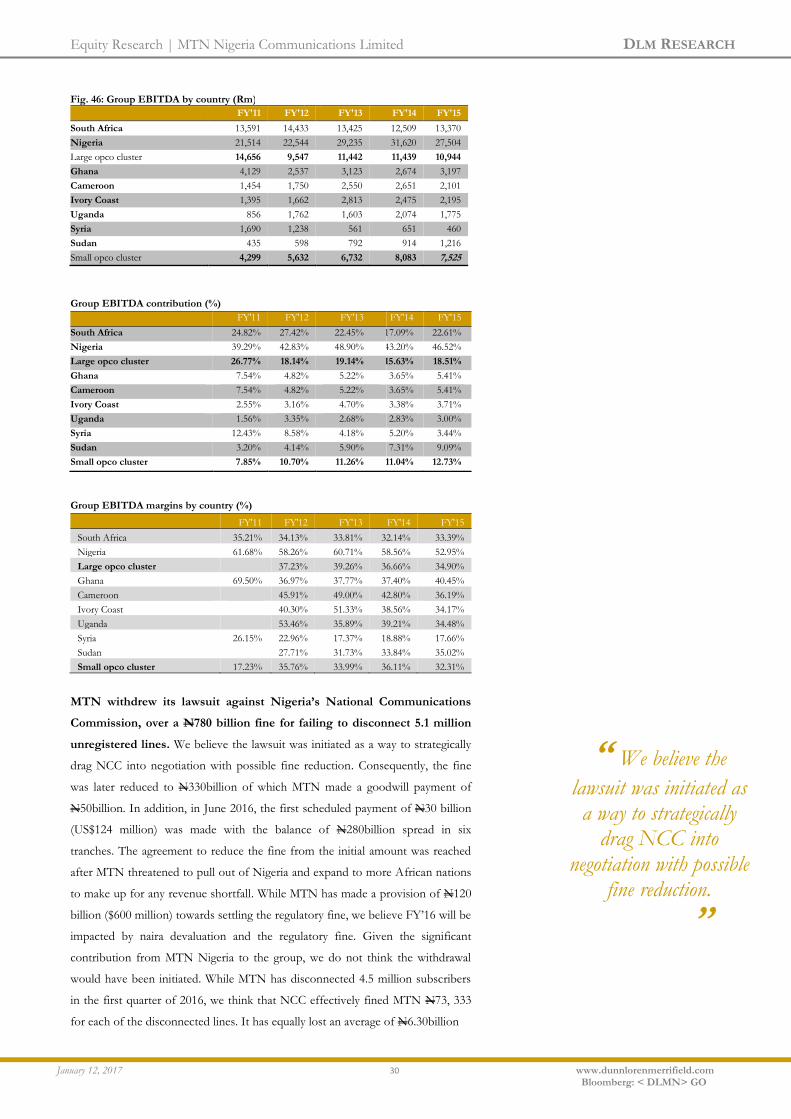

MTN Nigeria accounts for almost half of the group's EBITDA, and a

greater proportion of its free cash flow. In naira terms, the company’s

EBITDA grew by a CAGR of 0.88% from N466.94billion in 2011 to

N479.35billion in 2014. On the other hand, EBITDA margin declined by 3.49pp

from 61.60% in 2011 to 58.12% in 2014. In rand, MTN Nigeria EBITDA grew

by a CAGR of 13.70% from R21.51billion in 2011 to R31.62billion in 2014

whereas the group recorded a growth of 10.16%. Overall, the group earned the

highest EBITDA of R73.19billion in 2014 with Nigeria operations contributing

43.20% to the group’s EBITDA. In 2015, while MTN Nigeria posted EBITDA

of R27.50billion, MTN South Africa’s EBITDA stood at R13.37billion. MTN

Syria offered the lowest EBITDA of R460 million in the MTN Group.

Fig.44: EBITDA and margins in naira (Billion, %)

Source: Company annual report, DLM Research

Fig. 45: MTN Nigeria EBITDA margins vs. group and south Africa ( %)

0%

20%

40%

60%

80%

100%

120%

140%

160%

300

310

320

330

340

350

360

2011 2012 2013 2014

Operating profit Operating cost/ profit Operating margin

56.00%

58.00%

60.00%

62.00%

64.00%

400

450

500

FY'11 FY'12 FY'13 FY'14

EBITDA EBITDA margin

44.92% 38.96%

43.80% 49.81%

40.20%

61.68% 58.26% 60.71% 58.56%

52.95%

35.21% 34.13% 33.81% 32.14% 33.39%

FY'11 FY'12 FY'13 FY'14 FY'15

Group EBITDA margins Nigeria Op EBITDA Margins South Africa Op EBITDA Margins

Source: Company annual report, DLM Research

“ In 2015, while

MTN Nigeria posted EBITDA of

R27.50billion, MTN South Africa’s

EBITDA stood at R13.37billion.

’’

Equity Research | MTN Nigeria Communications Limited DLM RESEARCH

January 12, 2017 30 www.dunnlorenmerrifield.com

Bloomberg: < DLMN> GO

Fig. 46: Group EBITDA by country (Rm)

FY'11 FY'12 FY'13 FY'14 FY'15

South Africa 13,591 14,433 13,425 12,509 13,370

Nigeria 21,514 22,544 29,235 31,620 27,504

Large opco cluster 14,656 9,547 11,442 11,439 10,944

Ghana 4,129 2,537 3,123 2,674 3,197

Cameroon 1,454 1,750 2,550 2,651 2,101

Ivory Coast 1,395 1,662 2,813 2,475 2,195

Uganda 856 1,762 1,603 2,074 1,775

Syria 1,690 1,238 561 651 460

Sudan 435 598 792 914 1,216

Small opco cluster 4,299 5,632 6,732 8,083 7,525

Group EBITDA contribution (%)

FY'11 FY'12 FY'13 FY'14 FY'15

South Africa 24.82% 27.42% 22.45% 17.09% 22.61%

Nigeria 39.29% 42.83% 48.90% 43.20% 46.52%

Large opco cluster 26.77% 18.14% 19.14% 15.63% 18.51%

Ghana 7.54% 4.82% 5.22% 3.65% 5.41%

Cameroon 7.54% 4.82% 5.22% 3.65% 5.41%

Ivory Coast 2.55% 3.16% 4.70% 3.38% 3.71%

Uganda 1.56% 3.35% 2.68% 2.83% 3.00%

Syria 12.43% 8.58% 4.18% 5.20% 3.44%

Sudan 3.20% 4.14% 5.90% 7.31% 9.09%

Small opco cluster 7.85% 10.70% 11.26% 11.04% 12.73%

Group EBITDA margins by country (%)

FY'11 FY'12 FY'13 FY'14 FY'15

South Africa 35.21% 34.13% 33.81% 32.14% 33.39%

Nigeria 61.68% 58.26% 60.71% 58.56% 52.95%

Large opco cluster

37.23% 39.26% 36.66% 34.90%

Ghana 69.50% 36.97% 37.77% 37.40% 40.45%

Cameroon 45.91% 49.00% 42.80% 36.19%

Ivory Coast 40.30% 51.33% 38.56% 34.17%

Uganda 53.46% 35.89% 39.21% 34.48%

Syria 26.15% 22.96% 17.37% 18.88% 17.66%

Sudan 27.71% 31.73% 33.84% 35.02%

Small opco cluster 17.23% 35.76% 33.99% 36.11% 32.31%

MTN withdrew its lawsuit against Nigeria’s National Communications

Commission, over a N780 billion fine for failing to disconnect 5.1 million

unregistered lines. We believe the lawsuit was initiated as a way to strategically

drag NCC into negotiation with possible fine reduction. Consequently, the fine

was later reduced to N330billion of which MTN made a goodwill payment of

N50billion. In addition, in June 2016, the first scheduled payment of N30 billion

(US$124 million) was made with the balance of N280billion spread in six

tranches. The agreement to reduce the fine from the initial amount was reached

after MTN threatened to pull out of Nigeria and expand to more African nations

to make up for any revenue shortfall. While MTN has made a provision of N120

billion ($600 million) towards settling the regulatory fine, we believe FY’16 will be

impacted by naira devaluation and the regulatory fine. Given the significant

contribution from MTN Nigeria to the group, we do not think the withdrawal

would have been initiated. While MTN has disconnected 4.5 million subscribers

in the first quarter of 2016, we think that NCC effectively fined MTN N73, 333

for each of the disconnected lines. It has equally lost an average of N6.30billion

“ We believe the

lawsuit was initiated as a way to strategically

drag NCC into negotiation with possible

fine reduction.

’’

Equity Research | MTN Nigeria Communications Limited DLM RESEARCH

January 12, 2017 31 www.dunnlorenmerrifield.com

Bloomberg: < DLMN> GO

in month (N18.83bn in the first quarter) using $4.5 average revenue per

subscriber in a month. MTN Nigeria has always been fine for a number of

offences. For example, in 2014, NCC imposed quality of service fine of

N185million on the company which was duly paid. The fine underlines some of

the wider risks associated with emerging markets.

Fig. 47: MTN Nigeria regulatory fines 2012 - 2015 ( N’bn)

Source: Company annual report, DLM Research

H1’16 performance negatively impacted by regulatory pressure. For H1

2016, MTN Nigeria’s revenue declined by 4.80% to N389.35billion from

N408.99billion in the prior year. Revenue growth for the period was impacted

by a number of factors such as; 1) disconnection of the final batch of

subscribers in compliance with the subscriber registration process. 2) The

suspension of regulatory services until May 2016 when the operation attained

the necessary approvals to introduce market-related pricing plans and

promotions. 3) The introduction of regulatory restrictions on “out-of-bundle”

data tariffs which impacted MTN Nigeria’s data revenue growth. 4) Multiple

SIM usage. Digital revenue gained contributed 51.7% to data revenue

supported by growth in music and other lifestyle content services. EBITDA

margin declined by 7.5 pp to 49.8%, impacted by the transfer of the second

tranche of passive infrastructure into the TowerCo as well as US dollar-

denominated expenses associated with the TowerCo and build-to-suit sites.

This was supported by 13.8% increase in marketing costs relating to the

subscriber registration process.

Fig. 48: MTN Nigeria interim revenues 2013 - 2016 ( N’bn)

Source: Company report, DLM Research

0.360 0.131 0.185

330

2012 2013 2014 2015

383.06 413.61 408.99 389.35

410.56 411.20 398.45

2013 2014 2015 2016

H1 H2

“ For the half year

2016, MTN Nigeria’s revenue declined by

4.80% to N389.35billion from N408.99billion in the

prior year.

’’

Equity Research | MTN Nigeria Communications Limited DLM RESEARCH

January 12, 2017 32 www.dunnlorenmerrifield.com

Bloomberg: < DLMN> GO

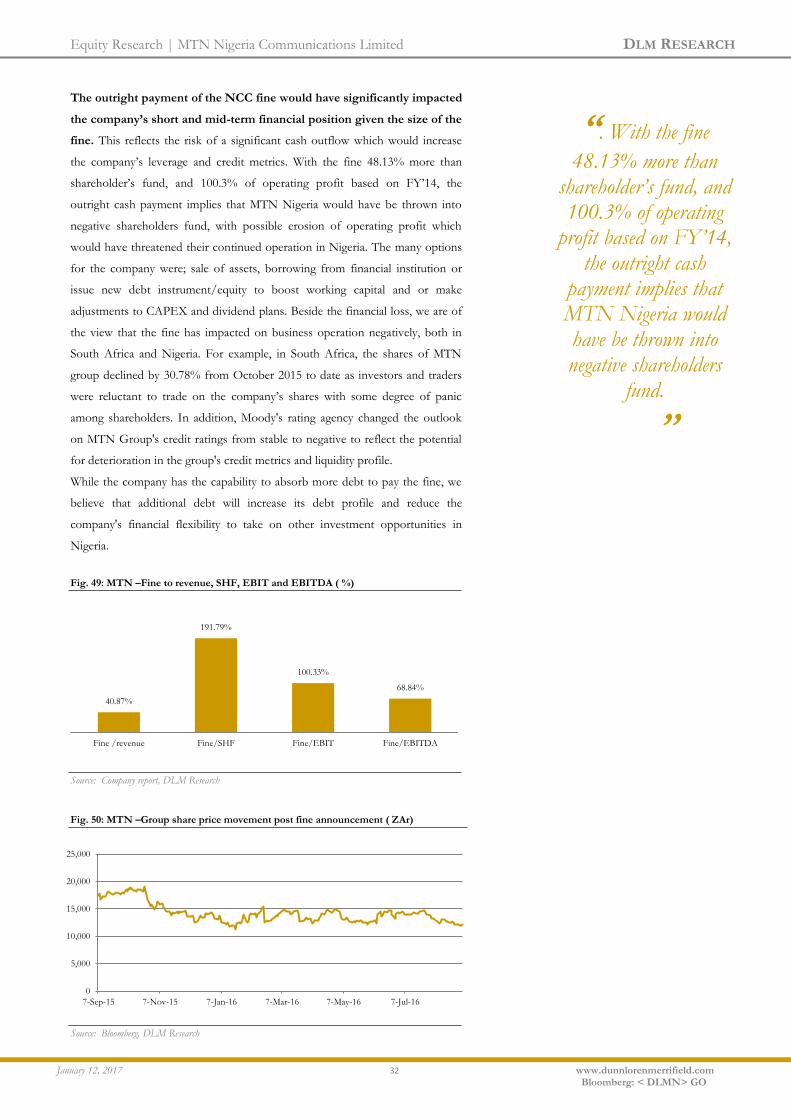

The outright payment of the NCC fine would have significantly impacted

the company’s short and mid-term financial position given the size of the

fine. This reflects the risk of a significant cash outflow which would increase

the company’s leverage and credit metrics. With the fine 48.13% more than

shareholder’s fund, and 100.3% of operating profit based on FY’14, the

outright cash payment implies that MTN Nigeria would have be thrown into

negative shareholders fund, with possible erosion of operating profit which

would have threatened their continued operation in Nigeria. The many options

for the company were; sale of assets, borrowing from financial institution or

issue new debt instrument/equity to boost working capital and or make

adjustments to CAPEX and dividend plans. Beside the financial loss, we are of

the view that the fine has impacted on business operation negatively, both in

South Africa and Nigeria. For example, in South Africa, the shares of MTN

group declined by 30.78% from October 2015 to date as investors and traders

were reluctant to trade on the company’s shares with some degree of panic

among shareholders. In addition, Moody's rating agency changed the outlook

on MTN Group's credit ratings from stable to negative to reflect the potential

for deterioration in the group's credit metrics and liquidity profile.

While the company has the capability to absorb more debt to pay the fine, we

believe that additional debt will increase its debt profile and reduce the

company's financial flexibility to take on other investment opportunities in

Nigeria.

Fig. 49: MTN –Fine to revenue, SHF, EBIT and EBITDA ( %)

Source: Company report, DLM Research

Fig. 50: MTN –Group share price movement post fine announcement ( ZAr)

Source: Bloomberg, DLM Research

40.87%

191.79%

100.33%

68.84%

Fine /revenue Fine/SHF Fine/EBIT Fine/EBITDA

0

5,000

10,000

15,000

20,000

25,000

7-Sep-15 7-Nov-15 7-Jan-16 7-Mar-16 7-May-16 7-Jul-16

“. With the fine

48.13% more than shareholder’s fund, and 100.3% of operating

profit based on FY’14, the outright cash

payment implies that MTN Nigeria would have be thrown into negative shareholders

fund.

’’

Equity Research | MTN Nigeria Communications Limited DLM RESEARCH

January 12, 2017 33 www.dunnlorenmerrifield.com

Bloomberg: < DLMN> GO

MTN group to issue dollar denominated bond to pay regulatory fine. The

decision to raise fund came after the company reported H1’16 loss pressured by

Nigeria operation regulatory fine. Since 2010, the group have issued a number

of bonds to fund business expansion. For example, in 2010, the group issued a

R1.25billion which matures in 2017. In 2014, the group also issued another

$750million note which matures in 2024. While the new bond when issued will

increase the group’s leverage profile and ratios, we think that it’s a right decision

for the company given that MTN Nigeria credit limit with Nigerian banks is

already high therefore limiting its borrowing capacity from Nigerian banks due

largely to CBN’s regulation that Nigerian banks cannot lend more than 20% of

their capital to one single company (single obligor limits). For example, in

2013, the company secured a 7-year loan worth $3 billion -N470 billion (which

consists of $1.8 billion in additional facilities and $ 1.2 billion in restructuring of

existing local facility loan) from a consortium of local and international financial

institutions to upgrade its network, which include; Zenith Bank Plc N55 billion;

FCMB N15 billion; Guaranty Trust Bank Plc N40 billion; United Bank for

Africa, N25 billion and Fidelity Bank N26.2 billion. Others local financiers are

Access Bank Plc with N35 billion; Diamond Bank Plc N5 billion; Citibank N5

billion; Ecobank, N15 billion; First Bank of Nigeria Limited N40 billion, FSDH

N3billion; Keystone Bank N5 billion; Mainstreet Bank N5 billion, Rand

Merchant Bank N3 billion; Stanbic IBTC, N15 billion; Standard Chartered N7

billion; and Union Bank of Nigeria N20 billion, totalling N329.25 billion.

Hence, MTN will have to look outside Nigeria possibly South Africa for

borrowings for business expansion.

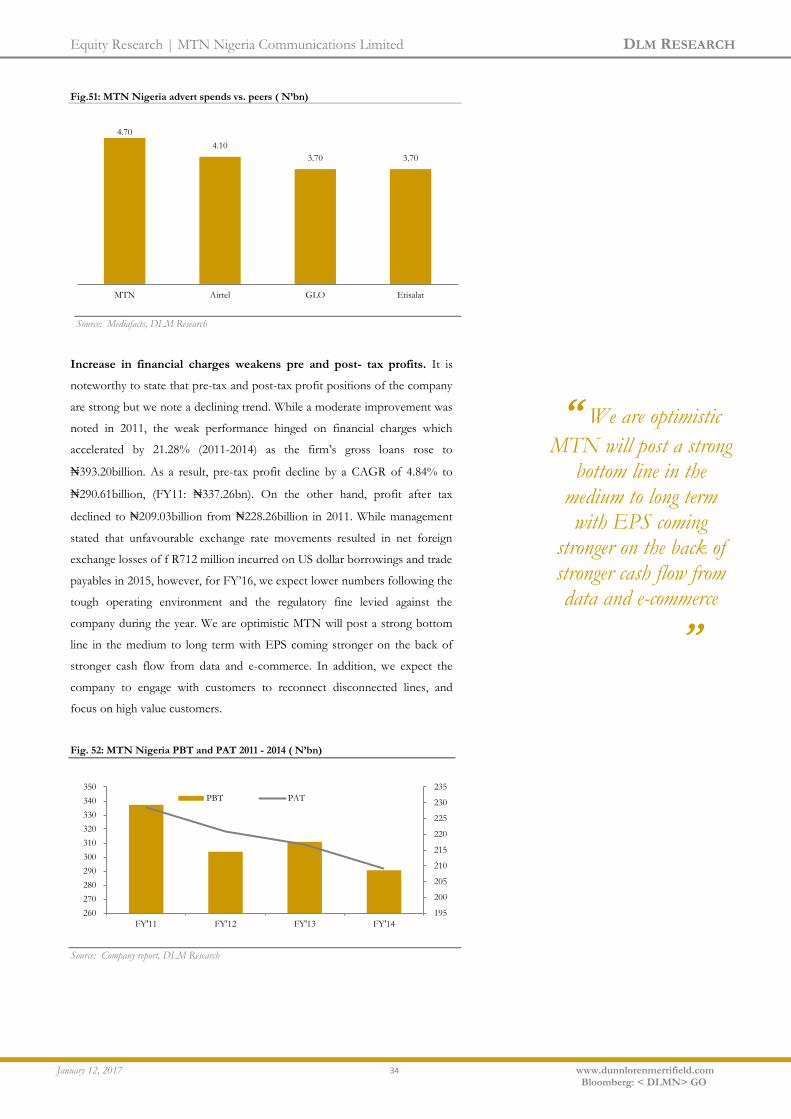

MTN is the biggest advertisement spender in the sector. Advertisement

is a major force to reckon with in the telecom industry. In the sector, a

successful marketing campaign can lead to increase sales, better name

recognition and a wider customer base. Hence, MTN Nigeria continuously

engage in aggressive marketing strategy ranging from traditional print media to

social network marketing, large scale TV and print advertising. In the past five

years, MTN has spent a substantial budget of its adspend on publicising its

products. For example, with the quest for a bigger share of the market and

outdo other competitors, MTN spent c.N4.7billion on advertising in 2015 and

was closely followed by Airtel which spent N4.10billion. Though, 2015 MTN’s

advert spends represents a decline when compared with the period 2011 when

advertising spend was N6.38billion. The company also frequently uses

celebrities who endorse the services as brand ambassadors.

“ The decision to raise

fund came after the company reported

H1’16 loss pressured by Nigeria operation

regulatory fine. The bond issuing is to enable the company raise fund

to offset the N330billion Nigerian fine, and address capex

needs ’’

Equity Research | MTN Nigeria Communications Limited DLM RESEARCH

January 12, 2017 34 www.dunnlorenmerrifield.com

Bloomberg: < DLMN> GO

Fig.51: MTN Nigeria advert spends vs. peers ( N’bn)

Source: Mediafacts, DLM Research

Increase in financial charges weakens pre and post- tax profits. It is

noteworthy to state that pre-tax and post-tax profit positions of the company

are strong but we note a declining trend. While a moderate improvement was

noted in 2011, the weak performance hinged on financial charges which

accelerated by 21.28% (2011-2014) as the firm’s gross loans rose to

₦393.20billion. As a result, pre-tax profit decline by a CAGR of 4.84% to

₦290.61billion, (FY11: ₦337.26bn). On the other hand, profit after tax

declined to ₦209.03billion from ₦228.26billion in 2011. While management

stated that unfavourable exchange rate movements resulted in net foreign