mukesh kolhe - suzlon energy - experiences with australia-india trade covering goods, services and...

TRANSCRIPT

1 1

Suzlon Energy Ltd.

Mukesh Kolhe

May 16

2

Disclaimer

• This presentation and the accompanying slides (the “Presentation”), which have been prepared by Suzlon Energy Limited (the “Company”), have beenprepared solely for information purposes and DOES not constitute any offer, recommendation or invitation to purchase or subscribe for any securities,and shall not form the basis OF or be relied on in connection with any contract or binding commitment whatsoever. The Presentation is not intended toform the basis of any investment decision by a prospective investor. No offering of securities of the Company will be made except by means of astatutory offering document containing detailed information about the Company.

• This Presentation has been prepared by the Company based on information and data which the Company considers reliable, but the Company makes norepresentation or warranty, express or implied, whatsoever, and no reliance shall be placed on, the truth, accuracy, reliability or fairness of the contentsof this Presentation. This Presentation may not be all inclusive and may not contain all of the information that you may consider material. Any liability inrespect of the contents of or any omission from, this Presentation is expressly excluded. In particular, but without prejudice to the generality of theforegoing, no representation or warranty whatsoever is given in relation to the reasonableness or achievability of the projections contained in thePresentation or in relation to the bases and assumptions underlying such projections and you must satisfy yourself in relation to the reasonableness,achievability and accuracy thereof.

• Certain matters discussed in this Presentation may contain statements regarding the Company’s market opportunity and business prospects that areindividually and collectively forward-looking statements. Such forward-looking statements are not guarantees of future performance and are subject toknown and unknown risks, uncertainties and assumptions that are difficult to predict. These risks and uncertainties include, but are not limited to, theperformance of the Indian economy and of the economies of various international markets, the performance of the wind power industry in India andworld-wide, the Company’s ability to successfully implement its strategy, the Company’s future levels of growth and expansion, technologicalimplementation, changes and advancements, changes in revenue, income or cash flows, the Company’s market preferences and its exposure to marketrisks, as well as other risks. The Company’s actual results, levels of activity, performance or achievements could differ materially and adversely fromresults expressed in or implied by this Presentation. The Company assumes no obligation to update any forward-looking information contained in thisPresentation. Any forward-looking statements and projections made by third parties included in this Presentation are not adopted by the Company andthe Company is not responsible for such third party statements and projections.

• No responsibility or liability is accepted for any loss or damage howsoever arising that you may suffer as a result of this Presentation and any and allresponsibility and liability is expressly disclaimed by the Management, the Shareholders and the Company or any of them or any of their respectivedirectors, officers, affiliates, employees, advisers or agents.

• No offering of the Company’s securities will be registered under the U.S. Securities Act of 1933, as amended (the “Securities Act”). Accordingly, unless anexemption from registration under the Securities Act is available, the Company’s securities may not be offered, sold, resold, delivered or distributed,directly or indirectly, into the United States or to, or for the account or benefit of, any U.S. Person (as defined in regulation S under the Securities Act).

• The distribution of this document in certain jurisdictions may be restricted by law and persons into whose possession this presentation comes should inform themselves about and observe any such restrictions

3

Contents

Suzlon Introduction

Industry Opportunities – Wind and Solar

Products & Technology

Suzlon in Australia

4

Suzlon – A global powerhouse

End to End service provider with strong presence across value chain

Installation of ~15,000 MW majority in India, USA, China, Brazil, Australia

Installed ~ 10,000 wind turbines globally

> 30,000 GHz power generated per year

Across 19 countries in 6 CONTINENTS

4200 MW manufacturing facilities spread across India, China (JV)

Workforce of over 7,000

5

Manufacturing Capacity

Manufacturing Capacity

India based ~3,600 MW

China JV* ~600 MW

Total ~4,200 MW

*Holds 25% stake in China JV

Fully vertically integrated manufacturing

Installed Capacity (MW) - spread across 15 manufacturing locations in India

Foundry

Forging

Mould

Generator

Control Panel

Transformer

Nacelle and Hub

Tubular Tower

Rotor Blade

6

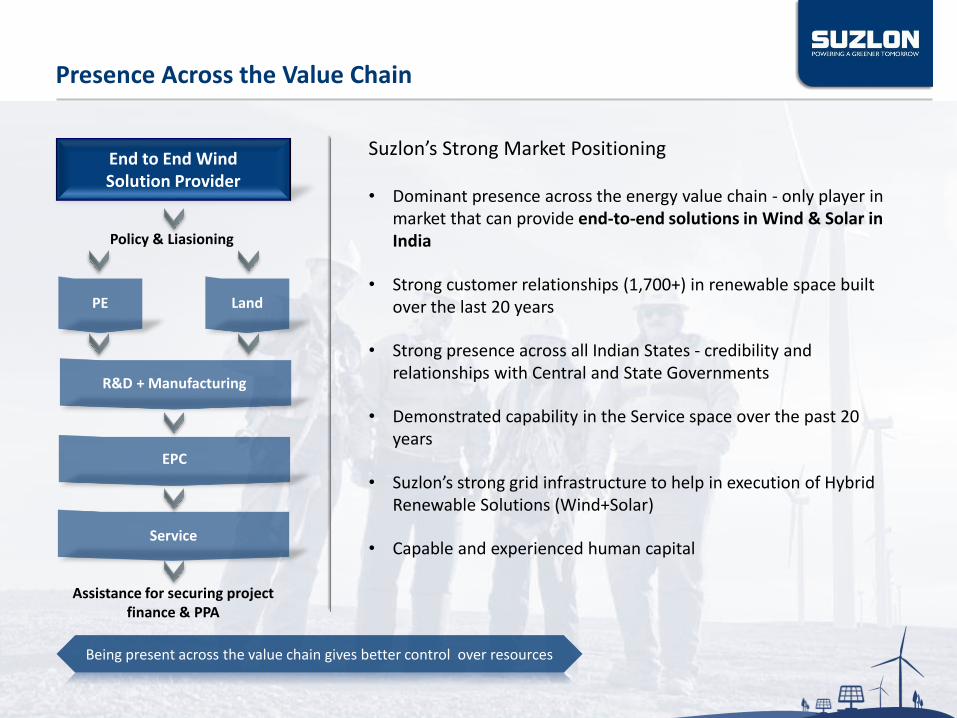

Presence Across the Value Chain

End to End Wind Solution Provider

Policy & Liasioning

Suzlon’s Strong Market Positioning

• Dominant presence across the energy value chain - only player in market that can provide end-to-end solutions in Wind & Solar in India

• Strong customer relationships (1,700+) in renewable space built over the last 20 years

• Strong presence across all Indian States - credibility and relationships with Central and State Governments

• Demonstrated capability in the Service space over the past 20 years

• Suzlon’s strong grid infrastructure to help in execution of Hybrid Renewable Solutions (Wind+Solar)

• Capable and experienced human capital

PE Land

R&D + Manufacturing

EPC

Service

Assistance for securing project finance & PPA

Being present across the value chain gives better control over resources

7

~15 GW of Worldwide Installations

12

34

5

6

5

1

6

3

2North

America2718 MW

USA 2687 | Canada 31

South America869 MW

Brazil 741 | Nicaragua 63Uruguay 65

SouthAfrica

139 MW

Europe487 MW

Spain 233 | Portugal 103Turkey 88 | Others 63

4

Australia764 MW

Asia9877 MW

India 8917 | China 929Sri Lanka 31

(Figures in MW)

Asia 9877 | North America 2718 | South America 869 | Australia 764 | Europe 487 | South America 139

Data as on 31st March 2015

8

Global R&D Centers

R&D expenditure constitutes ~2-3% of the topline

12

2 1Europe Asia

Denmark (Aarhus, Vejle)SCADA | Blade Science Center

Germany (Hamburg, Rostock)Development and Integration | Certification | Design & Product Engineering | Innovation & Strategic Research

The Netherlands (Hengelo)Blade Design and Integration

India (Pune, Vadodara, Hyderabad, Chennai)

Design & Product EngineeringTurbine Testing & MeasurementTechnical Field SupportBlade EngineeringBlade Testing Center

9

Top Global Customers

Supplied more than 4 GW to renowned marquee customers worldwide

10

Contents

Suzlon Introduction

Industry Opportunities - Wind and Solar

Products & Technology

Suzlon in Australia

11

Bloomberg Projections based on Revised LRET

1

1

BNEF validates our Market Projections of 4-5 GW for the Australia Wind

Market

12

Solar Energy Development Trend-India

*Cumulative installation till FY10 – 10MW, FY11- 35MW

5 10 16

23 31

40

1 2 3 4 6

13

23

33

43

52

61

33

FY19e

66

FY18e

0

49

FY20e

+61%

83

101

FY21eFY16

18

FY17e FY22e

6

FY15FY14FY13FY12

Roof Top

Ground MountedIn GW

Strong Policy & Economy driving future growth towards 100 GW milestone by 2022

13

Solar Business to leverage Suzlon's end to end solution offering in Indian Market

13

Solar irradiance Assessment

Land Acquisition

and Approvals

Infrastructure &

Power Evacuation

Supply Chain

Installation

&

Commissioning

Value Added Service

Life Cycle Asset

Management

• Long term Comprehensive OMS Solution offering

• Experienced team of professionals

• In-house and World-class SCADA

• Assistance in Regulatory Approval

• Assistance in REC, 3rd party PPA, Group Captive, CDM, CSR etc.

• Assist in organising Debt

• Design & Engineering

• Project management with on-site quality plan for installation & commissioning

• Strong SCM and global vendor base

• Selection of Modules, Inverters / Transformers & Trackers

• EPC experience of ~20 yrs

• Developed Substations / Line

• Development of allied infra

• Acquisition of land

• Getting statutory approvals and clearances

• Data collection for potential sites

Wind and Solar complementary to Suzlon’s strengths in India

14

Contents

Suzlon Introduction

Industry Opportunities – Wind and Solar

Products & Technology

Suzlon in Australia

15

S52 – 600 kW S66 – 1.25 MW S82 – 1.5 MW S88 – 2.1 MW S95 – 2.1 MW S97 – 2.1 MW S111 – 2.1 MW

Wind Class II A III A III A II A II A IEC III A III A

Hub Height 75 m 64.5 m, 74.5 m 78.8 m 80 m, 100 m 80m, 90, 100m 90 m / 120 m 90 m

Power regulation

Active Pitch regulated

Special features of product

– –STV, LTV, SFS

controlSTV, LTV, PIT, SFS

controlHTV, Lightning protection class-I, Lift, PIT, compliance to

international standards like CE, UL, CSA

Productpresence

AsiaAsia, North

AmericaAsia

Asia, North & South America,

Australia, Europe, Africa

Asia, South America

Australia, Europe

Asia, North & South America,

Australia, Europe

Asia, USA, Australia, Europe

Rotor Diameter52 m

Rotor Diameter66 m

Rotor Diameter82 m

Rotor Diameter88 m

Rotor Diameter95 m

Rotor Diameter97 m

Rotor Diameter111.8 m

Hub Height75 m

Hub Height74.5 m

Hub Height78.8 m

Hub Height100 m

Hub Height100 m

Hub Height120 m

Hub Height90 m

Comprehensive Product Portfolio - 600 kW to 2.1 MW

Current market offerings

16

Contents

Suzlon Introduction

Industry Opportunities – Wind and Solar

Products & Technology

Suzlon in Australia

17

Suzlon Australia – key factsBusiness and trade contribution > 2 bAUD

• 182-184, Stawell street, Burnley, MelbourneHeadquarter

•Established in June 2004 with two employees

•Secured first deal with AGL for the Hallet wind farm in 2005

•Rapid growth 2005-2011- constructed 9 wind farms across Australia

•Peak capacity – 350 employees in 2011

Key milestones

•AGL

• Infigen Energy

•Trustpower Ltd.

•Pacific Hydro

Customer base

•South Australia: 6 Wind farms,-508 MW

•New South Wales : 2 Wind farms – 190 MW

•Victoria :1 Wind farm- 67 MWWindfarms

•S88

•S95, S97Products installed

• “Easy to do Business with”

•Workforce of more than 12 nationalities

•Global organisation – easy to mobilise internal skilled supportIdentity

•Strong on-ground servcie crew trained by international experts

•Local 24/7 monitoring centre

•Tailored servcie packagesCustomer care

18

Factors that have helped us -Legal, Commercial, Policy, relationship management, etc.

• Expansion of the Renewable Energy Target(‘RET’) particularly in earlier years from 2001-2009

Legal

• Commitment and expansion of parentcompany, Suzlon Energy Limited, to growinginternational subsidiaries

– Competitive pricing strategy and supportof research and development and after-care functions

– Establishment of through-life capabilityfrom turbine sales, project execution tooperations and maintenance

• Suzlon as a growing company was able togrow with the Australian market not hinderedby outdated processes and procedures

– As an early entrant to the Australianmarket, ability to create foundationrelationships and grow with customers

• Ability to utilize knowledge of the RET towork with customers and meet timelines.

– Interaction with policymakers has enabledthe company to be heard on importantissues shaping the industry.

Relationship Management

Commercial Policy

19

Policy matters that we have capitalized on

• RET - capitalized on building a name when the RET was developing in early stages

• Visa policies - have allowed Suzlon to bring international experience to Australia

20

Enablers that can grow Indo-Australia trade

• Exchange of skillsets - making it easier for workers of both countries to work between countries by facilitating worker exchanges

• Knowledge-sharing–chance for both countries to learn from each other not only in respect of the renewable energy industry but also in terms of trade generally

Skills and workforce

• Increased certainty of the RET beyond 2020 until at least 2030 and beyond.

• Clarity on carbon policy and how this is to be managed and the opportunities it will create for the renewables industry.

• Fixed travel visas to encourage exchange of skills between the countries

Policy matters

• Established working groups on Wind and Solar energy growth

• Focus on Research and development

• Exchange of skills and knowhow

• Establish offshore Research and training facilities

Focussed working groups

•Australia is naturally blessed with renewable resources- Wind and Solar

•Capitalise on the established cost-effective manufacturing base in India

•Leverage Research in Solar technology in Australia – establish offshore centres, manufacturing in India

•Set-up “ renewables corridor” to enhance trade

Opportunities

21

THANK YOU