multifamily market overview - f.tlcollect.com · multifamily market overview 2019. macro-level...

TRANSCRIPT

g r e a t e r d a y t o n a p a r t m e n t a s s o c i a t i o n

presented by:

Kurt shoemaKer | First Vice president

multifamily m arke t overv ie w 2019

macro-leveleconomicindicators

01micro-leveleconomicindicators

022018 cBre rent & occupancy

survey results

03investment

markethighlights

2019Forecast

multiFamilydevelopment

04 0605

agenda

01 macro-level economic

indicators

greater dayton apartment association | 2019 multiFamily marKet oVerView |

greater dayton apartment association | 2019 multiFamily marKet oVerView |

source: u.s. bureau oF labor statistics, seasonally-adJusted data through January 2018. wage growth is based on aVerage hourly earnings.

CYCLICAL DRIVER - U.S. ECONOMY

Despite 3.7% unemployment, job creation maintaining pace; 2.5 million jobs added in past year

Historical Employment Growth Rate Year-over-Year

1.7

-5-4-3-2-10123

Oct-08 Oct-10 Oct-12 Oct-14 Oct-16 Oct-18

%

Wage GrowthOctober 2018 y-o-y

+3.1%

Jobs + 1.7% | Wages + 3.1% | 220,000 Monthly Job Growth

cyclical driversU.S . economy

DESPITE 3.9% UNEMPLOYMENT, JOB CREATION MAINTAINING PACE

0 4

JoBS

+1.7%waGeS

+3.1%monthlyJoB Growth

220,000

greater dayton apartment association | 2019 multiFamily marKet oVerView |

source: bloomberg.com, accessed 1/22/2019

key r ateshiStorical

05

Prime Rate

1/2015 1/2016 1/2017 1/2018 1/20192.00%

2.50%

3.50%

3.00%

4.00%

4.50%

5.00%

5.50%

3.25%3.50%

3.75%

4.50%

5.50%

5-Year Treasury

1/2015 1/20171/2016 1/2018 1/20190.50%

1.00%

2.00%

1.50%

2.50%

3.00%

1.33% 1.45%

1.89%

2.60%2.45%

10-Year Treasury3.00%

2.60%

2.20%

1.80%

1.40%

1.00%

1/2015 1/2016 1/2017 1/2018 1/2019

1.80%2.02%

2.39%2.65% 2.75%

LIBOR (3 mo)2.00%

1.60%

1.20%

0.80%

0.40%

0.00%

1/2015 1/2016 1/2017 1/2018 1/2019

0.26%0.61%

1.01%

2.40%

2.80% 2.78%

1.73%

greater dayton apartment association | 2019 multiFamily marKet oVerView |

interest r ates10-year treaSUry | 2 year hiStory

THREE POTENTIAL TWEAKS TO FEDERAL FUNDS RATE IN 2019

06

source: marKetwatch.com

ma

y-17

no

V-17

au

g-1

7

Feb-1

8

Jul-

18

J un

-17

dec

-17

sep-

17

ma

r-18

au

g-1

8

ma

y-18

oc

t-18

Jul -

17

Jan

-18

oc

t-17

apr

-18

sep-

18

Jun

-18

no

V-18

dec

-18

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

Jan

-19

8-YEARHIGH AT

3.22%

source: tradingeconomics.com | dow Jones

DOW JONES INDUSTRIAL AvERAGE

07

greater dayton apartment association | 2019 multiFamily marKet oVerView |

2008 2010 2012 2014 2016 2018

5000

10000

15000

20000

25000

30000-7.31% firSt neGative year Since 2009

Growth in 2018

TAx & TRADE REFORMWHAT’S IMPACTING OUR ECONOMY

08

greater dayton apartment association | 2019 multiFamily marKet oVerView |

greater dayton apartment association | 2019 multiFamily marKet oVerView |

BUyinG a hoUSe may not Be financially attainaBle

DemoGraphicS remain favoraBle

lifeStyle chanGeS favor mUltifamily

DEMOGRAPHICSanD a chanGinG mentality

SECULAR DEMAND DRIvERS

09

greater dayton apartment association | 2019 multiFamily marKet oVerView |

source: cbre research, cbre econometric adVisors, national association oF realtors, u.s. bureau oF labor statistics, Q3 and Q4 2018. home price, earnings and inFlation data through october 2018.

+37% rent growth since recession; yet affordability is not just a multifamily problem

Historical Multifamily Effective Rent ($/Month/Unit)

1,190

1,634

1,100

1,200

1,300

1,400

1,500

1,600

1,700

Q3 2006 Q3 2008 Q3 2010 Q3 2012 Q3 2014 Q3 2016 Q3 2018

Comparative Price Changes Since Recession

% Change Total Annual

Multifamily Rent 37.5 3.7

Single-Family HomeMedian Sales Price 57.4 5.3

Average Hourly EarningsAll Workers 22.0 2.3

Average Hourly Earnings Production & Non-Supervisory Workers

21.5 2.2

Inflation - CPI All Cities 16.3 1.7

AFFORDABILITYU.S. mUltifamily rentS

+37% RENT GROWTH SINCE RECESSION; YET AFFORDABILITY IS NOT JUST A MULTIFAMILY PROBLEM.

10

greater dayton apartment association | 2019 multiFamily marKet oVerView |

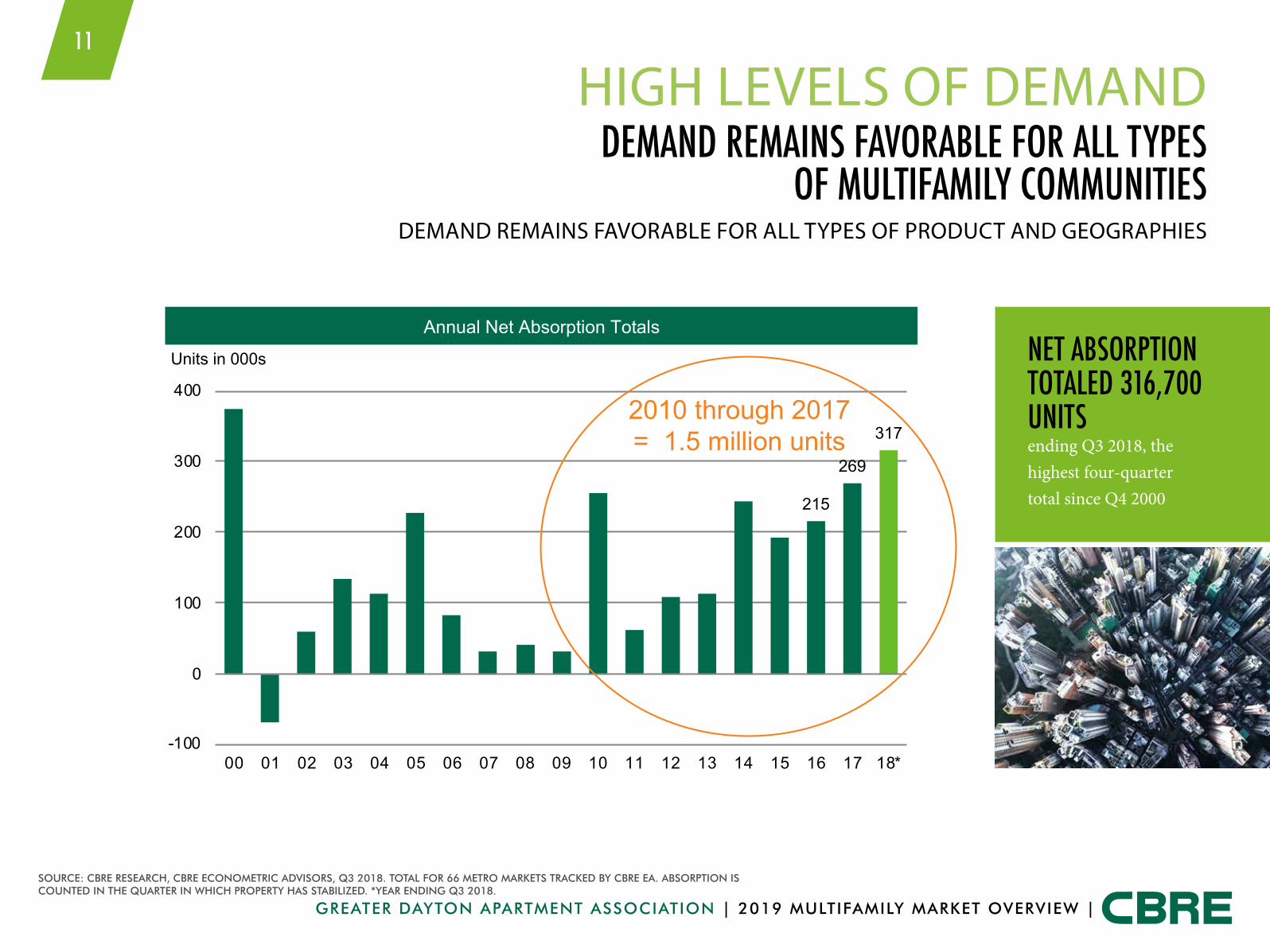

source: cbre research, cbre econometric adVisors, Q3 2018. total For 66 metro marKets tracKed by cbre ea. absorption is counted in the Quarter in which property has stabilized. *year ending Q3 2018.

Annual Net Absorption Totals

215

269

317

-100

0

100

200

300

400

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18*

Units in 000s

2010 through 2017= 1.5 million units

HIGH LEvELS OF DEMANDDemanD remainS favoraBle for all typeS

of mUltifamily commUnitieSDEMAND REMAINS FAvORABLE FOR ALL TYPES OF PRODUCT AND GEOGRAPHIES

11

net aBSorption totaleD 316,700 UnitS

ending Q3 2018, the highest four-quarter total since Q4 2000

greater dayton apartment association | 2019 multiFamily marKet oVerView |

source: cbre research, cbre econometric adVisors, Q3 2018.

Historical Vacancy Rate and Year-over-Year Change

0

1

2

3

4

5

6

7

-150

-100

-50

0

50

100

150

200

Q3 2006 Q3 2008 Q3 2010 Q3 2012 Q3 2014 Q3 2016 Q3 2018

Y-o-Y Vacancy Change (bps) Vacancy Rate (%)

U.S. MULTIFAMILY vACANCYvacancy incheD Up in 2017, BUt Still healthy

vACANCY FELL IN BOTH 2Q AND 3Q, REvERSAL OF FORMER TWO-YEAR TREND OF MODEST INCREASES

12

Same for both “baseline” and “Moody’s Analytics” forecasts

Down 40 bps year-over-year

Outlook over next year: +40 bps rise to 4.4% in Q3 2019

Q3 2018 = 4.0%

02 micro-level economic

indicators

greater dayton apartment association | 2019 multiFamily marKet oVerView |

greater dayton apartment association | 2019 multiFamily marKet oVerView |

source: esri

AREA DEMOGRAPHICSDayton ohio mSa

14

eDUcation | popUlation 25+

popUlation

hoUSeholD income

2 0 1 8 8 0 5 , 7 4 62 0 1 8 - 2 0 2 3 P R O J . G R O W T H 0 . 1 5 %U S A V G : 0 . 8 3 %

A S S O C I AT E S D E G R E E 9 . 8 %B A C H E L O R ’ S D E G R E E + 2 9 . 1 %C O M B I N E D 3 9 %U S A V G : 4 0 %

2 0 1 8 A V E R A G E $ 7 0 , 5 1 8 U S A V E R A G E $ 8 3 , 6 9 4H O U S E H O L D S E A R N I N G $ 2 5 K - $ 3 4 . 9 K 1 0 . 4 %H O U S E H O L D S E A R N I N G $ 3 5 K - $ 4 9 . 9 K 1 3 . 8 %H O U S E H O L D S E A R N I N G $ 5 0 K - $ 7 4 . 9 K 1 8 . 7 %H O U S E H O L D S E A R N I N G + 7 5 K 3 4 %

greater dayton apartment association | 2019 multiFamily marKet oVerView |

OHIO 4.6%KENTUCKY 4.5%INDIANA 3.6%NATIONAL 3.9%

source: bureau oF labor statistics

DAYTON MSA 4%

UNEMPLOYMENTSeaSonally aDJUSteD Unemployment

rateS aS of novemBer, 2018

15

source: united states census bureau > building permits surVey > permits by metropolitan area

JAN-NOV 2018 MLS SINGLE-FAMILY & CONDO SALES

LISTING

SOLDS

TOTAL SALE PRICE

% SALE/L IST PRICE

2018 2017 % Change

MEDIAN SALES PRICE

19,834 19,617 1.11%

15,195 15,036 1.06%

$2.52B $2.34B 7.49%

98.5 98.1 0.41%

$142,000 $134,000 5 .97%

AVERAGE SALES PRICE $165,733 $155,822 6 .36%

SINGLE FAMILY SALESDayton mSa SaleS

16

greater dayton apartment association | 2019 multiFamily marKet oVerView |

25%overall increaSeSince the receSSion

greater dayton apartment association | 2019 multiFamily marKet oVerView |

source: cbre

WHAT IS AN OPPORTUNITY zONE?Definition

THE DEPLOYMENT OF DEBT & EQUITY IN ECONOMICALLY CHALLENGED COMMUNITIES TO SUPPORT LONG-TERM, SUSTAINABLE GROWTH

17

of census tracts in a state could be designated as

“opportunity zones”

census tract must have at least 20%

poverty rate

of median income must not exceed 80% of metro or state level

designation of opportunity zone remains in effect

through the end of 2028

greater dayton apartment association | 2019 multiFamily marKet oVerView |

OPPORTUNITY zONEStax aDvantaGeS

18

KEY BENEfITS• Temporary Deferral of Capital Gains Taxes• Step up Basis• Tax-Free Earnings after Year 10

investors can defer taxes on capital gains

until 2026

capital must be placed in an opportunity fund

within 180 days

unlimited amount of capital can be reinvested into an opportunity fund

source: cbre

greater dayton apartment association | 2019 multiFamily marKet oVerView |

source: bureau oF labor statistics

SKILLED LABOR SHORTAGEinDUStry trenDS

19

80% of conStrUction firmS report havinG a harD time fillinG craft poSitionS

conStrUction JoBS are expecteD to Grow By 11% Until 2026, exceeDinG the averaGe for all other occUpationS

greater dayton apartment association | 2019 multiFamily marKet oVerView |

source: http://Fox45now.com/news/local/dayton-and-cincinnati-metroplex-within-the-decade

. . . w i l l c o m e t o f r u i t i o n w i t h i n t h e n e x t d e c a d e a n d t h e t i m i n g i s r i p e

- J i l l M e y e r, Pr e s i d e n t & C E O C i n c i n n a t i U S A R e g i o n a l C h a m b e r

18thlargest

CINCINNATI DAYTON

metroplexCOMBINED MSA’S ESTIMATED TO BECOME:

20

greater dayton apartment association | 2019 multiFamily marKet oVerView |

MULTIFAMILY MARKET CYCLEmarket poSition aS of q3 2018

21

source: cbre

82 JEANETTE I. RICE | STATE OF U.S. MULTIFAMILY MARKETCBRE

Source: CBRE Research, Q3 2018.

STABILIZATIONRents still declining or stable,

vacancy increasing, or decreasing slowly and limited

or new supply additions

EXPANSIONRents rising at faster pace, vacancy declining, and new supply additions underway

or on the horizon

MATURATIONRents increasing at slower pace, vacancy stable, and

increased new supply additions

CONTRACTIONRents declining, vacancy increasing, and excess new supply additions

MULTIFAMILY MARKET CYCLEMARKET POSITION AS OF Q3 2018

AlbuquerqueAustinChicagoClevelandDallasLexingtonNashvilleNew YorkSan AntonioSeattleSt. LouisTulsaU.S. Infill Multifamily

AtlantaBaltimoreCharlotteColorado Sprs.DenverFt. WorthKansas CityLouisvilleMiamiMinneapolisNewarkNorfolkOaklandOklahoma CityOmahaOrange CountyPortlandRaleighWashington, D.C.West Palm Beach

Inland EmpireJacksonvilleLas VegasLong IslandOrlandoPhoenixProvidenceRichmondTampa

BirminghamBostonCincinnatiColumbusDaytonDetroitEl PasoFt. LauderdaleGreensboroGreenvilleHartfordHonoluluHoustonIndianapolis

Los AngelesMemphisPhiladelphiaPittsburghSacramentoSalt Lake CitySan DiegoSan FranciscoSan JoseTucsonVenturaU.S. Suburban Multifamily

Dayton

03 2018 cBre rent and

occupancy survey

greater dayton apartment association | 2019 multiFamily marKet oVerView |

greater dayton apartment association | 2019 multiFamily marKet oVerView |

source: cbre

CBRE SURvEY RESULTS5-year occUpancy hiStory

23

NORTH

89.5%

94.0% 95.3%93.0%

201475.0%

80.0%

85.0%

90.0%

95.0%

100.0%

2015 2016 2017 2018

CENTRAL

201475.0%

80.0%

85.0%

90.0%

95.0%

2015 2016 2017 2018

84.3%

95.3% 96.4%

91.4%

100.0%

EAST

201475.0%

80.0%

85.0%

90.0%

95.0%

2015 2016 2017 2018

93.1%95.2% 94.2% 93.6%

100.0%

SOUTH

201475.0%

80.0%

85.0%

90.0%

95.0%

2015 2016 2017 2018

93.9% 95.0%93.5% 94.2%

100.0%

94.2%

95.5%93.3%

94.1%

greater dayton apartment association | 2019 multiFamily marKet oVerView |

source: cbre

CBRE SURvEY RESULTS5-year occUpancy hiStory

24

Greater Dayton MSA, Overall

201475.0%

80.0%

85.0%

90.0%

95.0%

100.0%

2015 2016 2017 2018

91.9%94.9% 94.2% 93.6% 94.4%

greater dayton apartment association | 2019 multiFamily marKet oVerView |

source: cbre

CBRE SURvEY RESULTSye 2018 averaGe effective rent

25

$805 / UNITAVERAGE ASKING RENT

$667 / UNITAVERAGE ASKING RENT

$837 / UNITAVERAGE ASKING RENT

$825 / UNITAVERAGE ASKING RENT

$827 / UNITAVERAGE ASKING RENT

$700 1 Bed / 1 Bath

$703 2 Bed / 1 Bath

$971 2 Bed / 2 Bath

$987 3 Bed average

}

$581 1 Bed / 1 Bath

$670 2 Bed / 1 Bath

$709 2 Bed / 2 Bath

$809 3 Bed average

} }

$693 1 Bed / 1 Bath

$666 2 Bed / 1 Bath

$1,012 2 Bed / 2 Bath

$1,100 3 Bed average

} }OVERALL NORTH SOUTH EAST CENTRAL

$748 1 Bed / 1 Bath

$743 2 Bed / 1 Bath

$969 2 Bed / 2 Bath

$1,110 3 Bed average

$714 1 Bed / 1 Bath

$683 2 Bed / 1 Bath

$1,367 2 Bed / 2 Bath

$1,300 3 Bed average

+ 10.7%+ 5.3%+ 5.5% + 5.2% + 4.3%

YOY 2017 - 2018 AvERAGE EFFECTIvE RENT GROWTH

greater dayton apartment association | 2019 multiFamily marKet oVerView |

CBRE SURvEY RESULTSkey take awayS

26

Downtown Dayton iS on fire

occUpancieS improveD

rent increaSeS city wiDe

reSUltS SUrpaSSinG moSt SUBmarketS

04 investment market

HigHligHts

greater dayton apartment association | 2019 multiFamily marKet oVerView |

greater dayton apartment association | 2019 multiFamily marKet oVerView |

source: real capital analytics, cbre research, Q4 2018, 2018 estimate is For all types oF transactions

U.S. MULTIFAMILY ACQUISITIONS2018 hiGheSt volUme in rca

hiStory at roUGhly $175 Billion

28

• 2017’s $154 billion total investment volUme waS Down 3.2% from the prior year

• total volume was second highest in the paSt 17 yearS (anD likely all hiStory)

• 2018 total is estimate based on mid JanUary total of $165 Billion. eStimate iS $175 Billion which woUlD Be a 14% Gain over 2017

• 2019 investment - a modest decline of 8% to 12% eStimateD

JEANETTE I. RICECBRE

–

–

• 2017’s $154 billion total

•

•

•

greater dayton apartment association | 2019 multiFamily marKet oVerView |

source: cbre

ANNUAL HISTORICAL TRANSACTION vOLUME

2018 mUltifamily SaleSGREATER DAYTON MSA | MULTIFAMILY SALES $1M+ OR 100 UNITS+

29

yoy 2017-2018 percentaGe chanGe:

total conSiDeration: $141 million

no. tranSactionS: 19 | UnitS: 2,509

- 12.5%Consideration

+ 26% Transactions

- 9.7% Units

greater dayton apartment association | 2019 multiFamily marKet oVerView |

2018 MULTIFAMILY SALESGREATER DAYTON MSA | MULTIFAMILY SALES $1M+ OR 100 UNITS+

30

source: cbre

10-YEAR HISTORY | TRANSACTION SALE VOLUME

2009 2010 2012 2014 2016 20182011 2013 2015 2017$0

$20$40$60$80

$100$120$140$160$180

mill

ions

greater dayton apartment association | 2019 multiFamily marKet oVerView |

2018 MULTIFAMILY SALESGREATER DAYTON MSA | MULTIFAMILY SALES $1M+ OR 100 UNITS+

31

source: cbre

10-YEAR AVERAGE / SALE PRICE PER UNIT

2009 2010 2012 2014 2016 20182011 2013 2015 2017$0

$10

$20

$30

$40

$50

$60

$70

thou

sand

s

2018 avG.

$53,000per Unit

greater dayton apartment association | 2019 multiFamily marKet oVerView |

source: cbre research, cbre econometric adVisors, ncreiF, u.s. department oF the treasury, Q3 2018.

INTEREST RATES & CAP RATESintereSt rateS & cap rateS not

alwayS trenDinG toGether

32

other factorS to conSiDer for cap rate pricinG• mortgage rates

• spreads between interest rateS anD mortGaGe rateS

• overall investment volume

• cross-border buying activity

• availability of debt capital

• product availability

• economic performance

• market fundamentals

• actual/potential tax changes

Historical Treasury Rates and Multifamily Cap Rates

2.92

4.21

0

2

4

6

8

Q3 2002 Q3 2004 Q3 2006 Q3 2008 Q3 2010 Q3 2012 Q3 2014 Q3 2016 Q3 2018

10-Year Treasury Multifamily Cap Rate

Historical Spread Between Interest Rates and Cap Rates

356

129

-100

0

100

200

300

400

Q3 2002 Q3 2004 Q3 2006 Q3 2008 Q3 2010 Q3 2012 Q3 2014 Q3 2016 Q3 2018

Average (197) Spread (BPs)

greater dayton apartment association | 2019 multiFamily marKet oVerView |

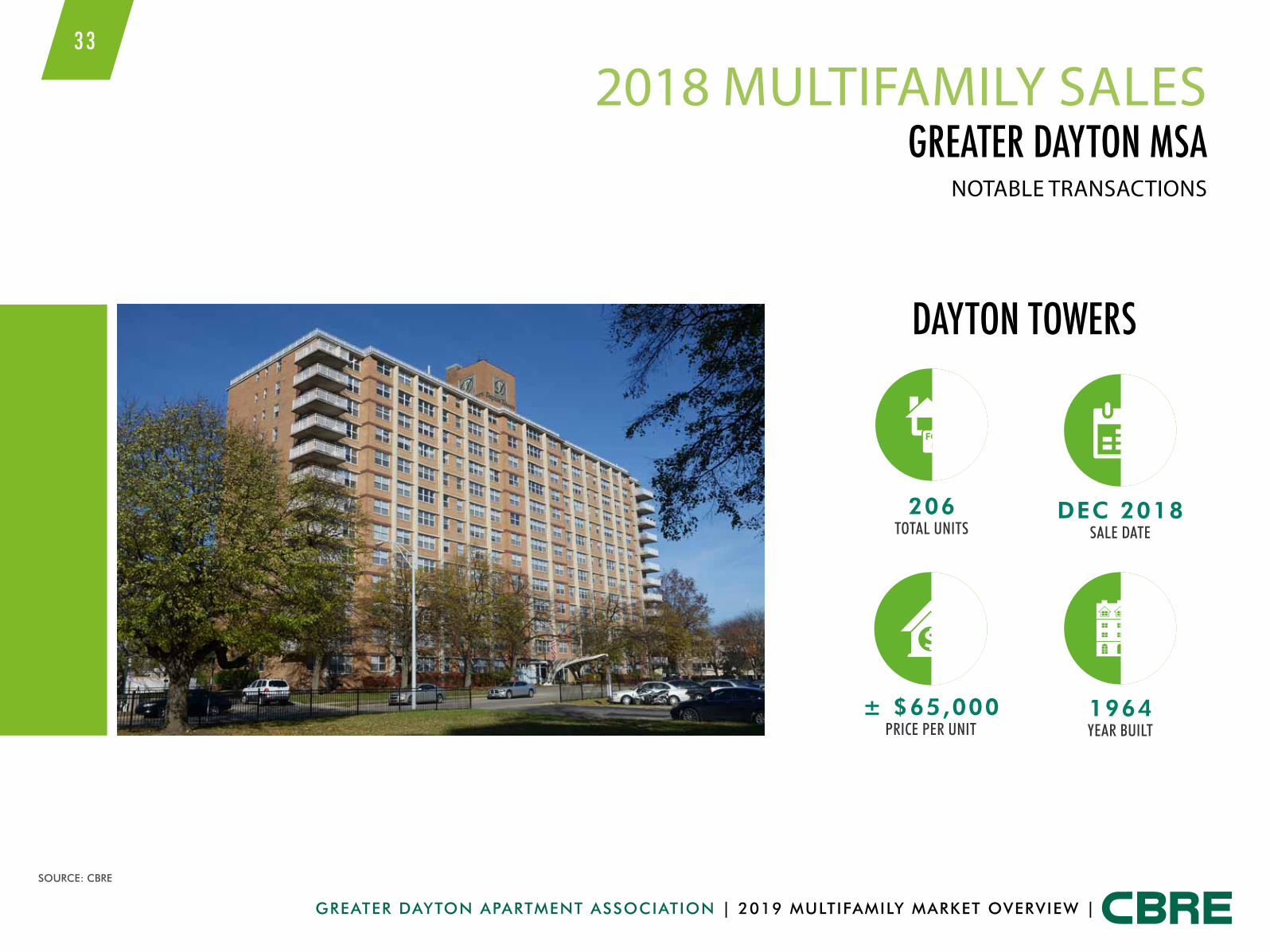

source: cbre

2018 MULTIFAMILY SALESGreater Dayton mSa

NOTABLE TRANSACTIONS

33

Dayton towerS

206TOTAL UNITS

DEC 2018SALE DATE

± $65,000PRICE PER UNIT

1964YEAR BUILT

05 multifamilydevelopment

greater dayton apartment association | 2019 multiFamily marKet oVerView |

greater dayton apartment association | 2019 multiFamily marKet oVerView |

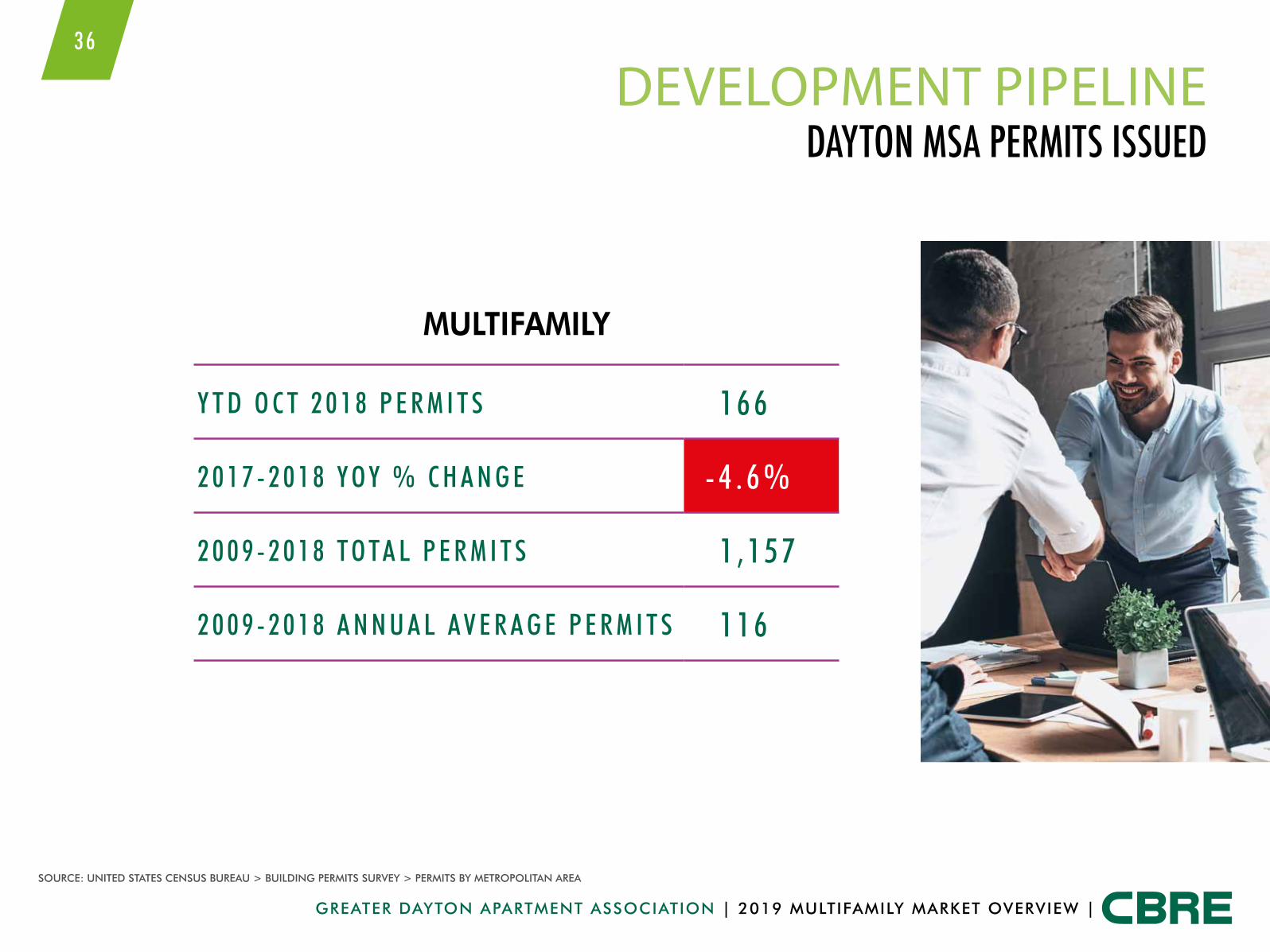

source: united states census bureau > building permits surVey > permits by metropolitan area

DEvELOPMENT PIPELINEDayton mSa permitS iSSUeD

35

SINGLE-FAMILY PERMITS

Y T D O C T 2 0 1 8 P E R M I T S 1 , 0 8 3

2 0 1 7 - 2 0 1 8 Y O Y % C H A N G E + 1 8 . 1 %

2 0 0 9 - 2 0 1 8 T O TA L P E R M I T S 8 , 1 0 9

2 0 0 9 - 2 0 1 8 A N N U A L A V E R A G E P E R M I T S 8 1 1

greater dayton apartment association | 2019 multiFamily marKet oVerView |

source: united states census bureau > building permits surVey > permits by metropolitan area

36

DEvELOPMENT PIPELINEDayton mSa permitS iSSUeD

MuLTIFAMILY

Y T D O C T 2 0 1 8 P E R M I T S 1 6 6

2 0 1 7 - 2 0 1 8 Y O Y % C H A N G E - 4 . 6 %

2 0 0 9 - 2 0 1 8 T O TA L P E R M I T S 1 , 1 5 7

2 0 0 9 - 2 0 1 8 A N N U A L A V E R A G E P E R M I T S 1 1 6

greater dayton apartment association | 2019 multiFamily marKet oVerView |

DEvELOPMENT PIPELINEDayton mSa cBre proJecteD mUltifamily DeliverieS

37

3-YEAR Mf UNIT DELIVERY PROJECTION

20190

200

400

600

800

1,000

1,200

2020 2021

1,013

494

source: cbre

322

greater dayton apartment association | 2019 multiFamily marKet oVerView |

DEvELOPMENT PIPELINE mUltifamily proJectS UnDer conStrUction

38

WATERfORD AT SUGAR CREEKSouth Submarket: Sugarcreek Township

MILLER VALENTINE GROUP & ACKERMANN GROUP

231 Units

MARCH 2018 - fIRST UNITS Final units being delivered Spring 2019

greater dayton apartment association | 2019 multiFamily marKet oVerView |

39

DEvELOPMENT PIPELINE mUltifamily proJectS UnDer conStrUction

ALLURESouth Submarket: Centerville

HILLS PROPERTIES312 Units

LEASINGStarted Leasing December 2018

Summer 2019 Stabilization

greater dayton apartment association | 2019 multiFamily marKet oVerView |

40

DEvELOPMENT PIPELINE mUltifamily proJectS UnDer conStrUction

ELEMENT OAKWOODSouth Submarket: Oakwood

HILLS PROPERTIES84 Units

LEASINGExpected to

start leasing in March 2019

greater dayton apartment association | 2019 multiFamily marKet oVerView |

41

DEvELOPMENT PIPELINE mUltifamily proJectS UnDer conStrUction

CENTERfIELD fLATSCentral Submarket: CBD

CRAWfORD HOYING112 units with

First Floor Retail

LEASINGExpected to start leasing in

March 2019, Occupying in September 2019

06 2019 forecast

greater dayton apartment association | 2019 multiFamily marKet oVerView |

greater dayton apartment association | 2019 multiFamily marKet oVerView |

43

2019 APARTMENT MARKETkurt shoemaker’s forecast

•Rents up by 1.5%• Cap rates compress

even further•Development pipeline

will slow •fundamentals will

remain solid

•Overall rents will slow to 2%• CBD rents and occupancies will have

growing pains with new product•Development pipeline will be very thin•fundamentals will continue to

remain solid•Sales Volume will decrease •Opportunity Zone to replace Value Add

as most used brokerage term

2018 recap 2019 forecaSt

greater dayton apartment association | 2019 multiFamily marKet oVerView |

4 4

Dave lockarD, ccimSenior Vice President+1 513 369 [email protected]

emily cantleySr. Capital Mkts Ops Analyst+1 513 369 [email protected]

kUrt Shoemakerfirst Vice President+1 513 369 [email protected]

To download today’s presentation: www.cbre.com/invcmmultifamily

CBRE TEAMcentral miDweSt mUltifamily |

cincinnati team memBerS

katlyn GeiGerCapital Mkts Ops Analyst+1 513 369 [email protected]