mutual fund fragility - wharton financefinance.wharton.upenn.edu/~itayg/files/cme group-msri.pdf ·...

TRANSCRIPT

Mutual Fund FragilityNon-bank Runs and Financial Crises

CME GROUP-MSRI SEMINAR

Itay Goldstein, Wharton

Overview

The way investors get paid upon redemption in open-end mutual funds might create a first-mover advantage or strategic complementarities

This can amplify redemptions following adverse shocks

The problem gets more severe when the fund holds more illiquid assets

Implications for fund policies and possibly also for regulation

2

Bank Runs

Bank runs have plagued the financial system for many years

The concern of bank runs is a source of vast government intervention and regulation Deposit insurance Bank regulation (capital, liquidity, etc.) Various government authorities

involved: FDIC, Federal Reserve System, etc.

3

Economic Force behind Runs

Basic economic force behind runs is based on (Diamond and Dybvig, 1983): Strategic complementarities

Banks create liquidity by holding illiquid assets and liquid liabilities (deposits)

Depositors are promised a fixed amount if they want to withdraw

If many withdraw, the bank will have to liquidate assets at a loss, hurting those who don’t withdraw

Run arises as a self-fulfilling belief: People run because they think others will do so

4

What about Non-Bank Institutions?

Strategic complementarities and run-type behavior are not limited to banks

Recent Example provided by money-market funds

One feature that is common to money-market funds and banks is that they have fixed claims

This clearly enhances the first-mover advantage contributing to run dynamics

New thinking following the crisis involves moving away from the fixed-NAV model to a floating-NAV model as in other mutual funds

5

Run Dynamics in a Floating-NAV Model

However, moving to a floating-NAV model does not eliminate the first-mover advantage and the potential for run-like behavior

In a floating-NAV environment, investors can redeem shares and get the NAV as of the day of redemption

But, their redemptions will affect fund trading going forward hurting remaining investors in illiquid funds

This is the source of the first-mover advantage (or strategic complementarities)

6

7

Complementarities in Mutual Funds Redemptions

Day 1 Day 2 Day 3 Day 4 …

At 3:59pm, investor i submits redemption

NAV determined by the closing price at 4:00pm

Mutual fund trades to raise the cash or to restore cash balance.

• Source for complementarities: • Redemptions impose costs on remaining investors: • Costs include: commissions, bid-ask spread, price

impact, forced deviation from desired portfolio, liquidity-based trading.

Empirical Analysis of Flows in Equity Mutual Funds

Chen, Goldstein and Jiang (2010) Study flows in 4,393 actively-managed equity

funds from 1995-2005 Find stronger sensitivity of outflows to negative

performance in illiquid funds These funds generate greater complementarities Illiquid funds are: small-cap & mid-cap equity

funds (domestic or international), or single-country funds excluding US, UK, Japan and Canada. Or continuous measure of liquidity of portfolio

Pattern is weaker in funds that are mostly held by institutional investors Externalities are better internalized

8

Evidence from Chen, Goldstein, and Jiang (2010)

9

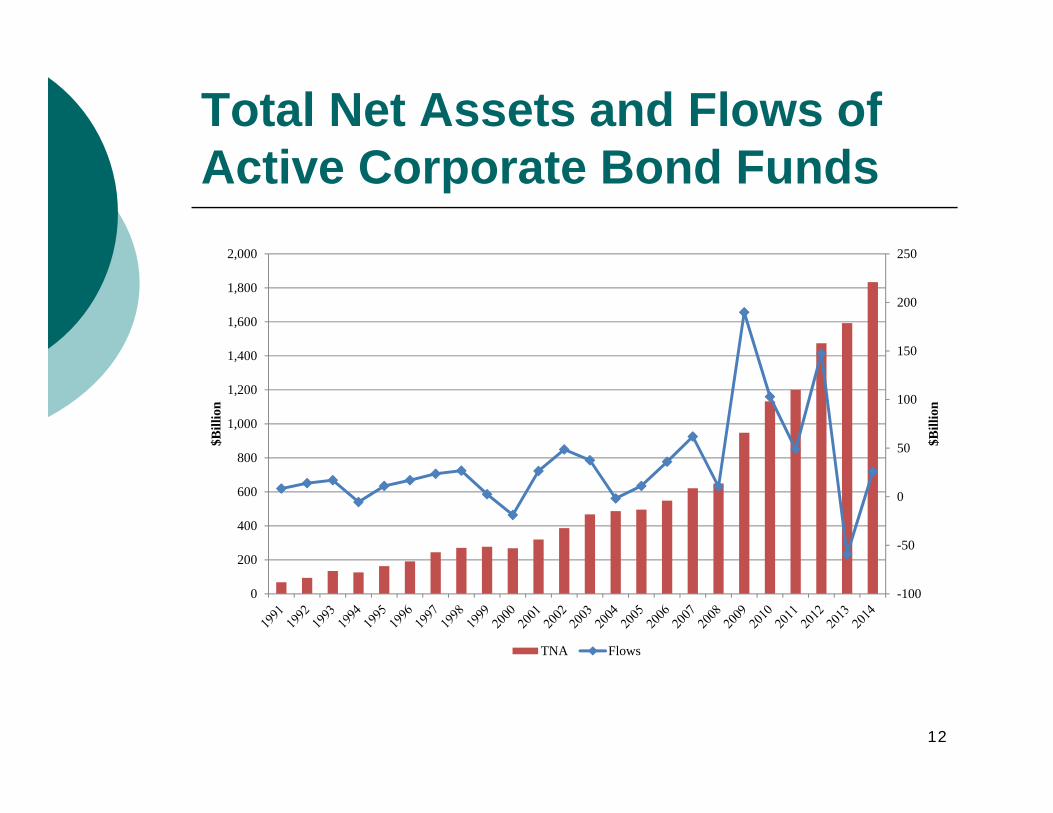

Corporate Bond Funds

Recently, there is growing interest in Corporate bond mutual funds in this context They are growing fast Their assets can be very illiquid and so

they generate stronger complementarities

Concern for fragility: Investors will pull their money out following signs of bad performance, amplified by the strategic complementarities

10

Distribution of Bond Fund Assets

11

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Corporate World Government Multisector State muni National muni

Total Net Assets and Flows of Active Corporate Bond Funds

12

-100

-50

0

50

100

150

200

250

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

$Bill

ion

$Bill

ion

TNA Flows

Empirical Analysis of Flows in Corporate Bond Mutual Funds

Goldstein, Jiang and Ng (2015) Study flows in 1,660 actively-managed corporate bond

funds from 1992-2014 Compare the pattern with that of equity funds Link pattern to illiquidity

Large literature on the flow-to-performance relation in equity funds, finding convex relation (greater sensitivity on upside than on downside)

We find that corporate bond funds are different: flow-to-performance relation tends to be concave

(greater sensitivity on downside than on upside) Pattern strengthens with illiquidity

Funds that hold less cash or periods with greater aggregate illiquidity

13

Flow Performance Relation of Corporate Bond Funds vs. Equity Funds

14

-0.1 -0.05 0 0.05 0.1-0.025

-0.02

-0.015

-0.01

-0.005

0

0.005

0.01

0.015

Performance

Flow

sBond Funds

-0.1 -0.05 0 0.05 0.1-0.02

-0.01

0

0.01

0.02

0.03

0.04

0.05

Performance

Flow

s

Stock Funds

Does redemption sensitivity disappear in aggregation?

15

-0.05 0 0.05-0.03

-0.025

-0.02

-0.015

-0.01

-0.005

0

0.005

0.01

0.015

Performance

Flow

s

Bond funds

-0.05 0 0.05-0.03

-0.025

-0.02

-0.015

-0.01

-0.005

0

0.005

0.01

0.015

Performance

Flow

s

Stock funds

Economic impact of Corporate Bond Fund Flows

Do outflows in bond funds have significant implications on market prices and the real economy?

Exploratory evidence Evaluate how corporate bond fund flows are related to Gilchrist

and Zakrajsek (2012)’s excess bond premium. Conduct a bivariate VAR with quarterly corporate bond fund

outflows and excess bond premium on a quarterly basis, and estimate the response of EBP to shocks to the corporate bond fund outflow.

Estimate the effect of corporate bond fund outflows on real-economy variables.

Sample period is from 1991Q1 to 2010Q3 with two lags of the endogenous variables.

16

Impact of Corporate Bond Fund Outflows on Excess Bond Premium

-.05

0.0

5.1

.15

% Im

pact

on

Exc

ess

Bond

Pre

miu

m

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20Quarters after the Outflows shock

Following 1% increase in corporate bond fund outflows during a quarter, the excess bond premium rises during the contemporaneous quarter, and jumps up further by 9.2 and 7.6 basis points in next two quarters.

17

Impact of Corporate Bond Fund Outflows on GDP growth

-.15

-.1-.0

50

.05

% Im

pact

on

Log

GD

P G

row

th R

ates

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20Quarters after the Outflows shock

18

Some Lessons

We need to pay attention to the liquidity mismatch created by mutual funds

Measures to reduce ‘first-mover advantage’ should be considered/implemented more prominently: Fund holding more liquidity/cash reserves (but, costly

to performance) Restriction on redemption frequency (but,

compromising liquidity to investors) Emergency rules: suspension of redemption;

redemption in kind…(but, seldom used, hard to implement)

Forward looking NAV calculation, e.g., swing pricing (but, hard to implement)

19

Some Lessons – Cont’d

Regulation may be needed if there are externalities going beyond the individual fund Fire-sale pricing leading to real implications

More broadly, regulating one part of the financial system will change the operation of other parts and create new risks Money market funds were largely a response to

tightened bank regulation Large activity in bond markets and bond funds is also

motivated by the need that cannot be easily filled by traditional banks

‘Shadow banking’ more generally

20