nasscom bpm summit 2016 session i : it's the idea that matters

TRANSCRIPT

NAME : Gautam AhujaDESIGNATION : Professor

COMPANY: University of Michigan

It’s the idea that counts…

IT’S THE IDEA THAT COUNTS: THE BPM INDUSTRY IN 2016

AN OUTSIDER’S VIEW Gautam AhujaUniversity of Michigan

A BPM WORD CLOUD IN 2016

Digital Transformation Automation RPA Cognitive Intelligence Social, Mobile, Analytics, Cloud New Business Models Outcome based pricing BPaaS Multichannel Integration Domain Specialists and SME …………Clearly for the BPM Decision-maker there are many competing dimensions on which major decisions have to be made… Yet resources, time and attention are limited, so what do we do? …..when the entire industry is in ferment..rather than jumping to action and execution, it makes sense to focus on conceptual clarity to pick the right investments to back

AN INDUSTRY IN FERMENT It turns out that “an industry in ferment” is a fairly common occurrence among industries Indeed almost every industry known has followed a cycle where after a period of foundation, emergence, growth, comes disruption as the industry matures, new challenges and opportunities arise and so on..

When one examines the BPM business from this broader historical perspective and focus on the underlying economic dimensions, this past history provides guidance…as they say… the past is prologue

Strategy and resource commitment in such a context implies a Four Step Sense-making Process

1. Structure the environmental context to obtain a clear mental model or picture of the key issues in the industry, collectively

2. Collate and use the data “tea leaves” to see the emerging trends3. Identify the implications of these trends 4. Devise an appropriate strategy and make investments in “ideas” consistent with that strategy

Note that this approach suggests that a critical attribute of a good idea is that is drawn from a serious study of the external environment in which it will be played out.

It also suggests that the past experience of other industry’s lifecycles can be informative in making sense of the BPM business

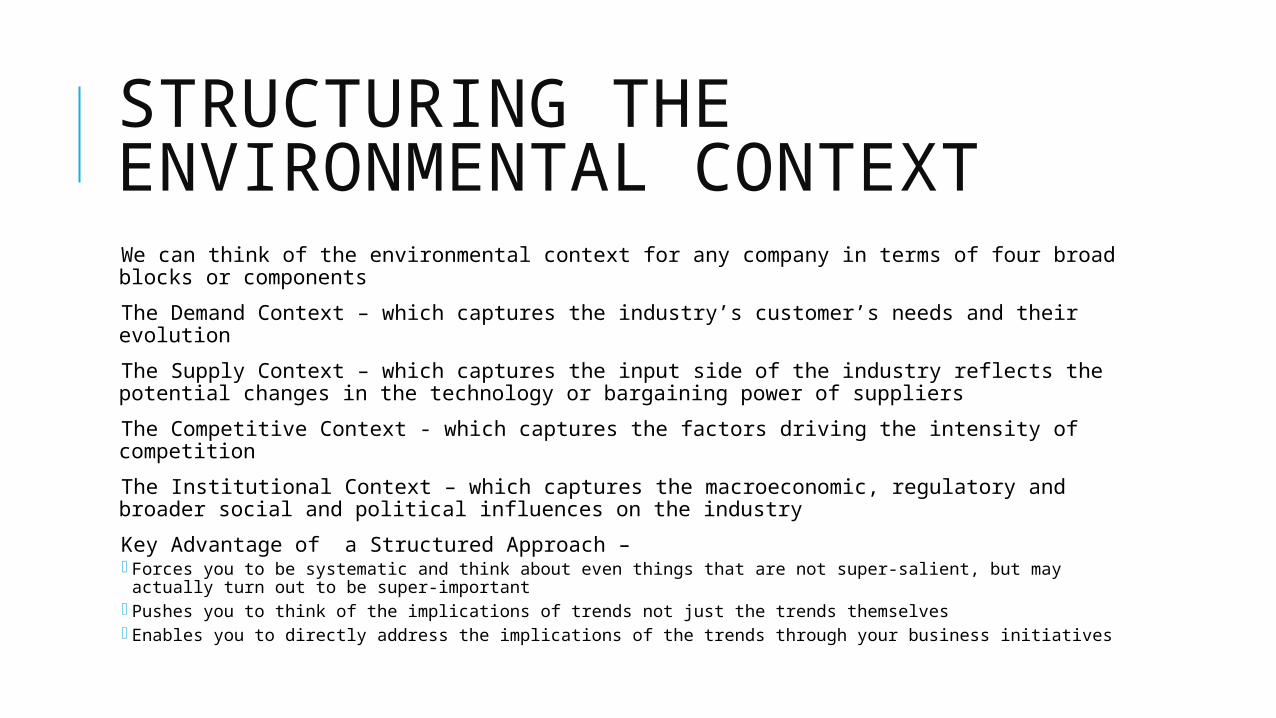

STRUCTURING THE ENVIRONMENTAL CONTEXT We can think of the environmental context for any company in terms of four broad blocks or components

The Demand Context – which captures the industry’s customer’s needs and their evolution The Supply Context – which captures the input side of the industry reflects the potential changes in the technology or bargaining power of suppliers

The Competitive Context - which captures the factors driving the intensity of competition The Institutional Context – which captures the macroeconomic, regulatory and broader social and political influences on the industry

Key Advantage of a Structured Approach – Forces you to be systematic and think about even things that are not super-salient, but may actually turn out

to be super-important Pushes you to think of the implications of trends not just the trends themselves Enables you to directly address the implications of the trends through your business initiatives

THE DEMAND CONTEXT (SELECTIVE ENUMERATION) Customers increasingly want not just productivity and cost improvements but also fundamental insights into improving their business (analytics)

They want to enable transactional ease for their customers, enable access across platforms and channels and want to use the information so generated (integrated multichannel access, social, mobile, big data analytics)

They want to be able to connect to their customers and suppliers seamlessly and conduct their operations efficiently and effectively… i.e. improve productivity and cost (end to end solution, digital transformation)

And they want to do this with the minimum hassle (cloud, BPaaS etc. ) These new models and technology infusion encourage BPM providers to have “skin in the game” (new business and revenue models, outcome based pricing)

And customers usually want ALL OF THE ABOVE TOGETHER

THE SUPPLY CONTEXT New technologies have emerged that promise multiple exciting features to enhance and make more efficient the delivery of business processes RPA Cognitive Intelligence Technologies – Machine learning, AI, pattern recognition, neural networks

New vendors have emerged that specialize in these technologies, along with industry participants who are also building capabilities in these areas or partnering

Labor attrition rates continue to increase (NASSCOM, 2016) Shortage of domain specialists, SMEs Computing technologies that are simultaneously enabling higher standards of service and customer contact but also increasing the demands for technological competence in both the BPM firms as well as the clients

THE COMPETITIVE CONTEXT Extremely fragmented industry - many firms already in the industry (NASSCOM 2016 provides an estimate of 2500)

With heterogenous profiles and capabilities (IT+BPM, BPM, RPA+BPM, etc.) Limited barriers to entry historically Increase in M&A activity Number of deals declining sharply (almost 40% decline in 2015), as also TCV (almost 36% decline in 2015) of the deals (in aggregate)

Average TCV (of individual deals) though is increasing Average scope (of individual deals) is increasing Revenue / employee is almost stagnant (0.6% increase in 2015)

THE INSTITUTIONAL CONTEXT

Global Macroeconomic Uncertainty (negative interest rates, huge budget deficits, significant increases in financial leverage of corporations)

Anxiety about globalization and automation (eg. US) Since the mid 1980’s productivity has increased but not wages – gap has widened especially since 2000

GDP per capita has increased but median household income has stagnated with a significant and growing gap between

Benefits have gone to “mobile” capital, but labor’s share of income has declined, enhancing income inequality

Significant anxiety about the role of technology Fears that the pattern noted above may only worsen as automation hits services

Reflected in political volatility, uncertainty and potential turbulence

STEP 2: IDENTIFYING ECONOMIC IMPLICATIONS OF THE TRENDS

Will focus on some of the trends in each of the four boxes for reasons of time, not all trends covered

THE DEMAND CONTEXT (SELECTIVE ENUMERATION) They want to be able to connect to their customers and suppliers seamlessly and conduct their operations efficiently and effectively… i.e. improve productivity and cost (end to end solution, digital transformation) . Customers increasingly want not just productivity and cost improvements but also fundamental insights into improving their business (analytics) => To provide customer insights and end-to-end solutions there needs to be close integration between BPM and

complementary offerings such as analytics and automation; hence the best service providers are the ones that will seamlessly integrate multiple services (perhaps eventually into an integrated BPM system )

=> Favors broader vertical scope companies (those able to provide integrated services) with deep domain knowledge (narrower horizontal scope)

They want to enable transactional ease for their customers, enable access across platforms and channels and want to use the information so generated (integrated multichannel access, social, mobile, big data analytics) => Higher technological capabilities required – which involves more investment in technology development => More investments in technology implies that fixed-cost intensity of the industry has increased

And they want to do this with the minimum hassle (cloud, BPaaS etc., flexibility of on-demand BPM models) => The flexibility of variable usage through BPaaS etc. makes BPM costs variable for the client but again increase the fixed cost intensity of the BPM service providers

New models encourage BPM providers to have “skin in the game” (new business and revenue models, outcome based pricing)

=> Outcome based pricing requires greater risk-bearing ability and productization again enhancing the scale requirements of the industry

And they want ALL OF THE ABOVE TOGETHER => A major segment of the industry will increasingly favor larger, technology intensive, broader service scope, domain specialist providers

=> Increases in scale, scope and technology requirements will increase barriers to entry, foster consolidation and domain specialization, and reduce fragmentation – thus enhancing industry profit potential

THE SUPPLY CONTEXT New technologies have emerged that promise multiple exciting features to enhance and make more efficient the delivery of business processes RPA Cognitive Intelligence Technologies – Machine learning, AI, pattern recognition, neural networks

New vendors have emerged that specialize in these technologies, along with industry participants who are also building capabilities in these areas or partnering

Labor attrition rates continue to increase (NASSCOM, 2016) Shortage of domain specialists, SMEs Computing technologies that are simultaneously enabling higher standards of service and customer contact but also increasing the demands for technological competence in both the BPM firms as well as the clients

Will focus on RPA here as that helps us open up the discussion later

ROBOTICS PROCESS AUTOMATION: KEY ECONOMIC IMPLICATIONS

Immediate benefits – productivity increases, error reduction, quick ROI, compatibility with legacy infrastructure, etc. margin improvements, non-linear growth Potential longer term manifestationsDeep embedding of RPA will probably increase switching costs - the greater the number of automation-human handovers in a given process, the higher the costs of switching that process to another RPA vendor

“Per license” pricing schemes for robots will likely foster even greater BPM / IT provider interest in developing their own RPA platforms and products (or acquiring RPA firms)

May reduce off-shoring and potentially even outsourcing (but only in limited, specific domains)If a process can be half-automated, and the cost of automation is 1/3 a human FTE the economics of outsourcing weakens sharply. A job costing 60k onshore and 20k offshore has a savings potential of 40k. With automation the savings drop to 20k (and possibly less given transition and ongoing coordination costs)

RPA success will probably incentivize development of integrated BPMS – after all the use of robotics interventions itself signals that the underlying business processes (or more accurately IT infrastructure) were poorly compatible and hence may be worth redesigning

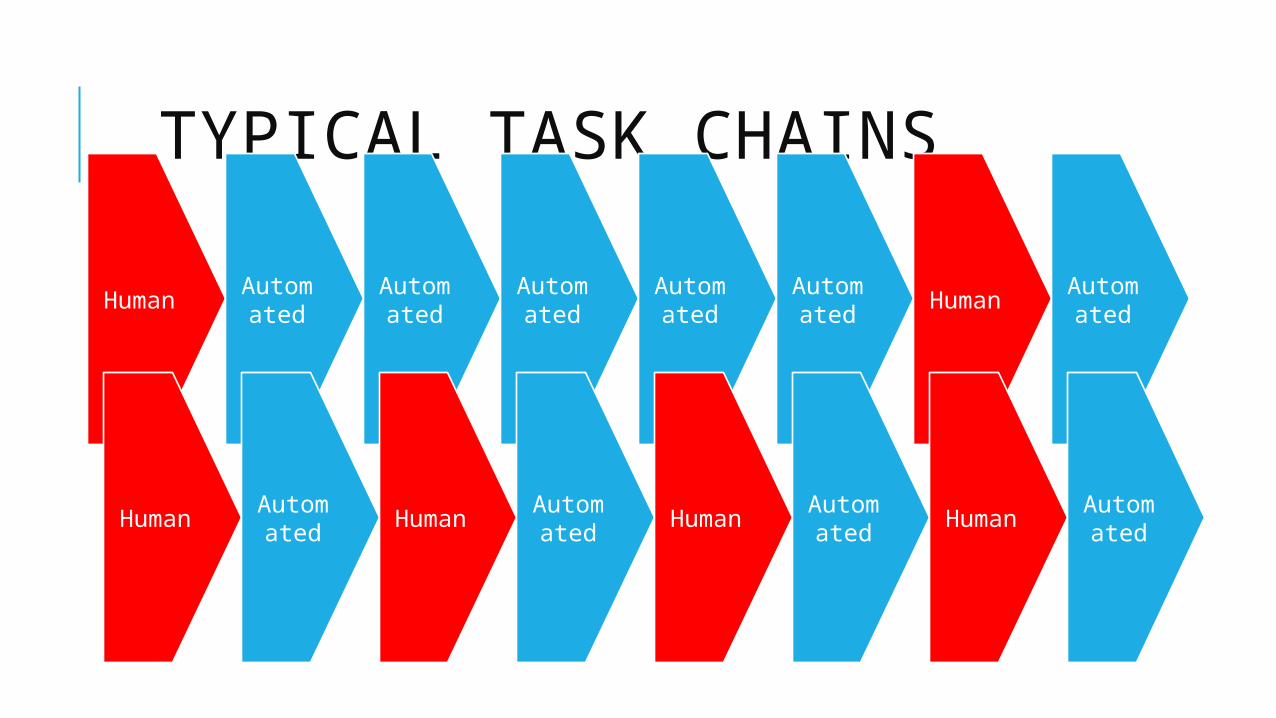

TYPICAL TASK CHAINSHuma

nAutomated

Automated

Automated

Automated

Automated

Human

Automated

Human

Automated

Human

Automated

Human

Automated

Human

Automated

THE COMPETITIVE CONTEXT Extremely fragmented industry - too many firms already in the industry (NASSCOM 2016 provides an estimate of 2500)

With heterogenous profiles and capabilities (IT+BPM, BPM, RPA+BPM, etc.) Limited barriers to entry historically Current Trends Increase in M&A activity Number of deals declining sharply (almost 40% decline in 2015), as also TCV (almost 36% decline in 2015) of the deals (in

aggregate) Average TCV (of individual deals) though is increasing Average scope (of individual deals) is increasing Revenue / employee is almost stagnant (0.6% increase in 2015)

TCV trends suggest that consolidation is going to increase (likely significantly) as the industry becomes more fixed cost intensive, technology intensive, and the average contract is increasingly a bundled offering of BPM plus complementary services (eg. analytics, IT)

With fewer contracts available to bid on some form of a “rich become richer” dynamic forms leading to increasing consolidation of the industry. Failing to get a contract leaves one with far fewer chances to catch up. And size will have become even more important in a technology and fixed cost intensive world

Note that there will still remain segments in the industry that won’t require all of this technology and scale so the above dynamics may only play in specific segments of the industry

THE INSTITUTIONAL CONTEXT Global Macroeconomic Uncertainty (negative interest rates, huge budget deficits, significant increases in financial leverage of corporations)

=> Non-trivial risk of business volatility, at the same time as industry pressures require investments in technology and fixed costs are increasing (higher operating leverage) Fixed costs are good as long as volume growth occurs, else… Some financial flexibility would be valuable

Anxiety about globalization and automation (eg. US) Since the mid 1980’s productivity has increased but not wages – gap has widened especially since 2000 GDP per capita has increased but median household income has stagnated with a significant and growing gap between the two for the last two decades

Benefits have gone to “mobile” capital, but labor’s share of income has declined, enhancing income inequality

Anemic job growth Significant anxiety about the role of technology

Fears that the pattern noted above may only worsen as automation hits services

=> BPM service providers as well as automation may face significant concerns. Clearly defined social value propositions may become almost as important as customer value propositions

SO WHAT DOES THIS READING OF THE EXTERNAL CONTEXT SUGGEST ABOUT THE SHAPE OF WINNING IDEAS AND BUSINESSES?

LIKELY ATTRIBUTES OF IDEAS AND BUSINESSES THAT WIN

Domain Clarity (and Refinement) and Sharp Targeting of Chosen Domain Without a narrow specific domain cannot really develop deep domain expertise. Without domain expertise providing end-to-end business-insight-rich performance is unlikely. Can’t be all things to all people

A “Completed” Product or Service Offering Will think of the complementary services required by the client to fully benefit from the provided service and ensure that such complements are simultaneously provided to the client For example, RPA is good – it enhances productivity and makes available humans for better work; however successful RPA-embedded solutioning will also include the most effective way of utilizing these newly “created” human resources as well. Think in terms of the system, and the client’s full problem not just the single process that is being automated

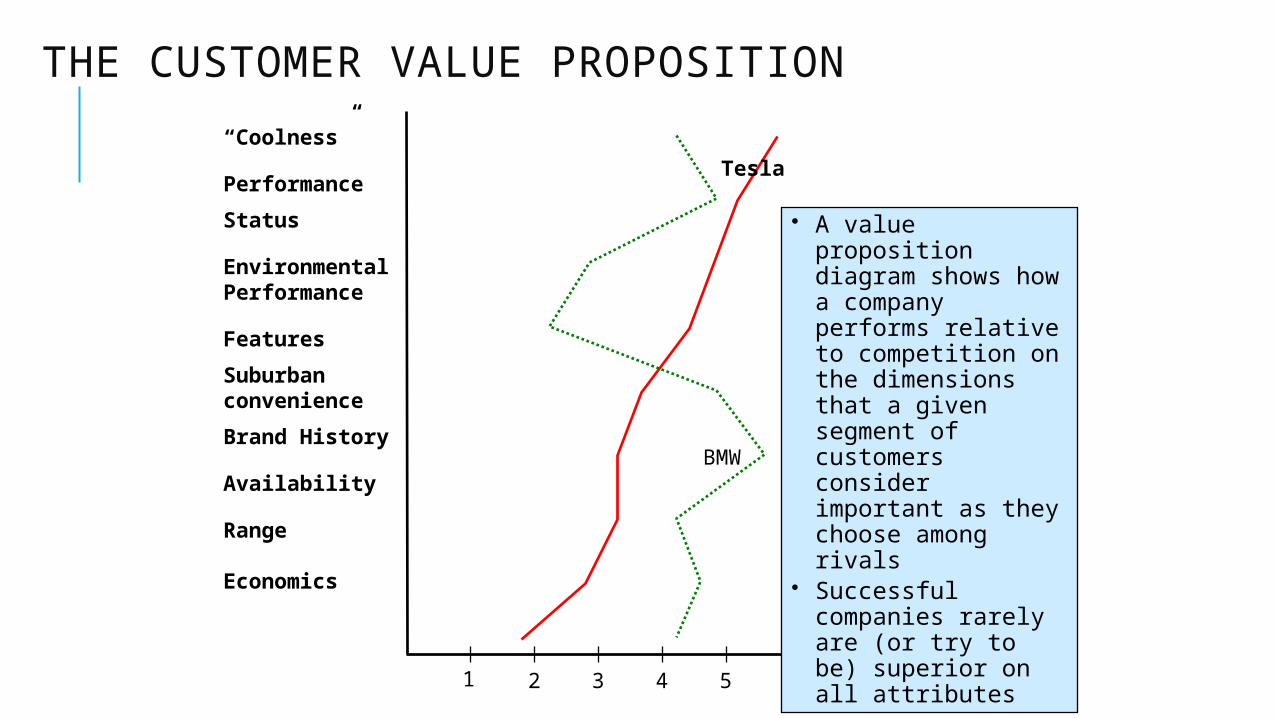

Clearly Conceptualized and Effectively Executed Value Proposition Customer Value Proposition

Deep domain expertise must be translated into a clear and refined understanding of what the client truly values in specific attributes

Simple Test: If your sales team can take the same Customer Value Proposition slide and use it in another domain the slide is too generic to truly capture domain expertise

“Coolness”

PerformanceStatus

Environmental Performance

FeaturesSuburban convenienceBrand History

Availability

Range

Economics

THE CUSTOMER VALUE PROPOSITION

1 2 3 4 5

Tesla

BMW

• A value proposition diagram shows how a company performs relative to competition on the dimensions that a given segment of customers consider important as they choose among rivals

• Successful companies rarely are (or try to be) superior on all attributes

LIKELY ATTRIBUTES OF IDEAS AND BUSINESSES THAT WIN(CONTINUED) Will likely redesign the entire organization and functional activities of the BPM service provider to effectively reflect the external context described earlier. For instance, Technology => increased investments in analytics, product and platform development Finance: Will recognize that these investments in technology are prospective and hence riskier investments and need to be monitored differently than traditional BPM investments

Marketing: With analytics-embedded services likely need a different pricing model (eg. outcome based)

Sales: Retraining (or additional hiring) to ensure effective selling of technology embedded services and platform products, or outcome-based revenue models

HR: Need to build domain expertise, technology expertise, implies may have to look beyond traditional recruiting platforms, venues and practices; may also need to enhance training to meet the new marketing, sales etc. needs