natura day 2010 finance - natura | relações com...

TRANSCRIPT

Roberto Pedote Vice President, Finance,

IT and Legal Affairs

Finance

Natura Day 2010

Agenda

• Schedule

• Value Proposition

• Value Chain

• Results

2

Schedule

3

Schedule

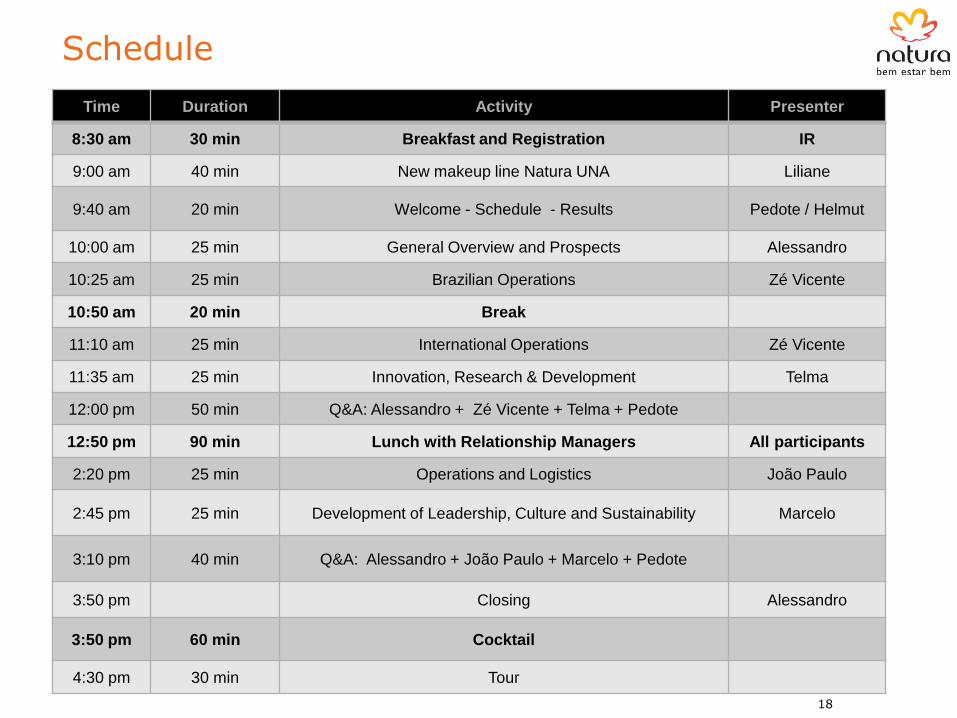

Time Duration Activity Presenter

8:30 am 30 min Breakfast and Registration IR

9:00 am 40 min New makeup line Natura UNA Liliane

9:40 am 20 min Welcome - Schedule - Results Pedote / Helmut

10:00 am 25 min General Overview and Prospects Alessandro

10:25 am 25 min Brazilian Operations Zé Vicente

10:50 am 20 min Break

11:10 am 25 min International Operations Zé Vicente

11:35 am 25 min Innovation, Research & Development Telma

12:00 pm 50 min Q&A: Alessandro + Zé Vicente + Telma + Pedote

12:50 pm 90 min Lunch with Relationship Managers All participants

2:20 pm 25 min Operations and Logistics João Paulo

2:45 pm 25 min Development of Leadership, Culture and Sustainability Marcelo

3:10 pm 40 min Q&A: Alessandro + João Paulo + Marcelo + Pedote

3:50 pm Closing Alessandro

3:50 pm 60 min Cocktail

4:30 pm 30 min Tour

4

Alessandro Carlucci

› CEO

› Joined Natura in 1989

› Member of the Board of Directors of the

World Federation of Direct Selling Associations

and Redecard

› BBA from FGV, Chicago’s Kellogg-Northwestern

Roberto Pedote

› Vice President of Finance, IT and Legal Affairs

› Joined Natura in 2008

› BA in Public Administration from FGV and Law

from USP, MBA from Michigan University

› 16 years experience at Unilever (Brazil, UK and

LatAm), Nokia in Brazil

João Paulo Ferreira

› Vice President, Operations and Logistics

› Joined Natura in 2009

› Engineering (USP), MBA (Michigan)

› 20 years experience at Unilever, with local,

regional and global roles. Vice President,

Supply Chain

José Vicente Marino

› Business Vice President

› Joined Natura in 2008

› BBA and MBA from FGV, MBA in Retail

(USP)

› Served as executive VP of hygiene and

personal care division of Johnson & Johnson

in Brazil

Marcelo Cardoso

› Vice President, Organizational Development

and Sustainability

› Joined Natura in 2008

› BBA

› MBA in Retail (USP), Chicago’s Kellogg-

Northwestern

› Served at GP Investimentos (HopiHari,

Playcenter, Método Engenharia), Regional DBM

› President

Telma Sinicio

› Vice President, Innovation

› Joined Natura in 2009

› BS and Masters in Engineering ESALQ (USP),

Wharton Business School

› 26 years at Johnson & Johnson Consumer Products

Companies Worldwide in R&D

Executive Committee

5

Our Relationship Managers invite you all for lunch...

Glaucilene

Vanessa

Andreia

Eliana

Roseli

Sandra

Cintia

Julia

Monica

Gilseia

Patricia

Mara Lucia

Ivani

Rita

6

Value Proposition

7

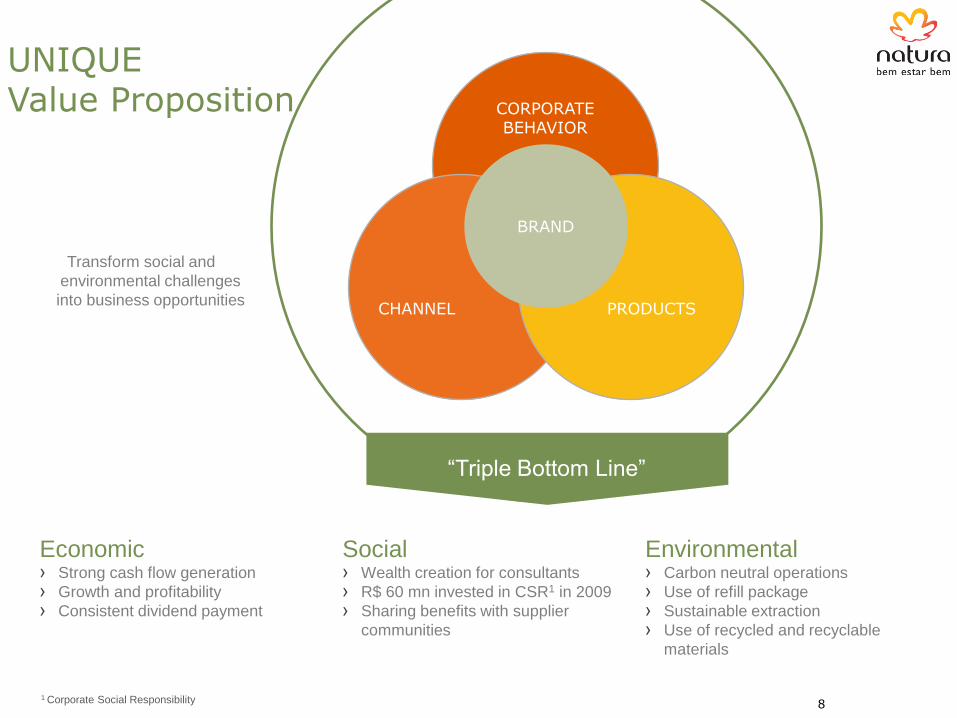

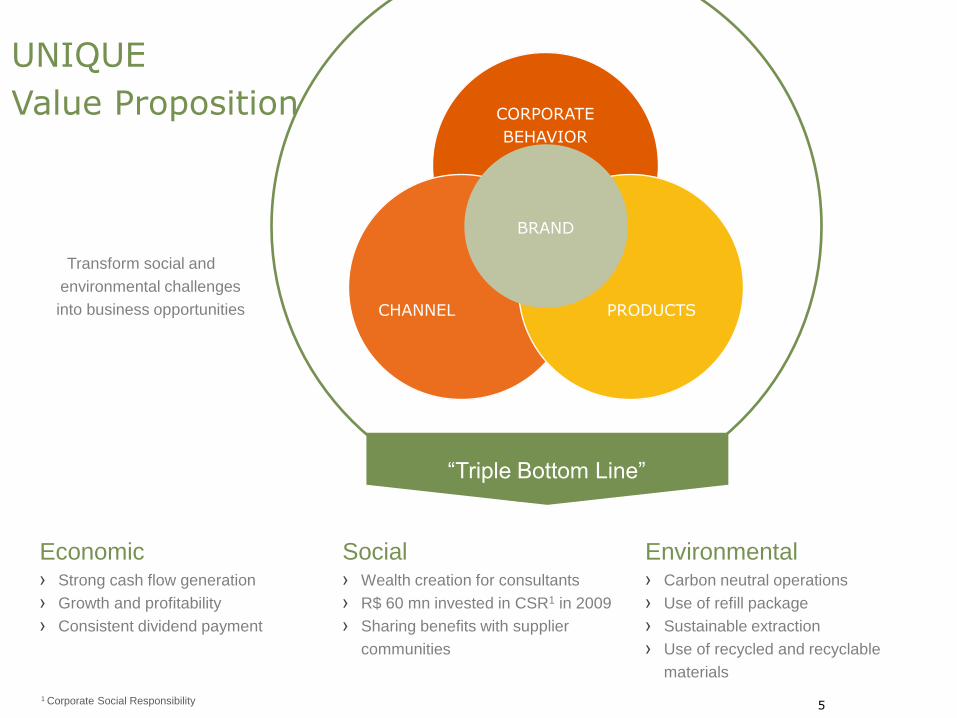

UNIQUE Value Proposition

CHANNEL PRODUCTS

CORPORATE BEHAVIOR

BRAND

“Triple Bottom Line”

Social › Wealth creation for consultants

› R$ 60 mn invested in CSR1 in 2009

› Sharing benefits with supplier

communities

Economic › Strong cash flow generation

› Growth and profitability

› Consistent dividend payment

Environmental › Carbon neutral operations

› Use of refill package

› Sustainable extraction

› Use of recycled and recyclable

materials

1 Corporate Social Responsibility

Transform social and

environmental challenges

into business opportunities

8

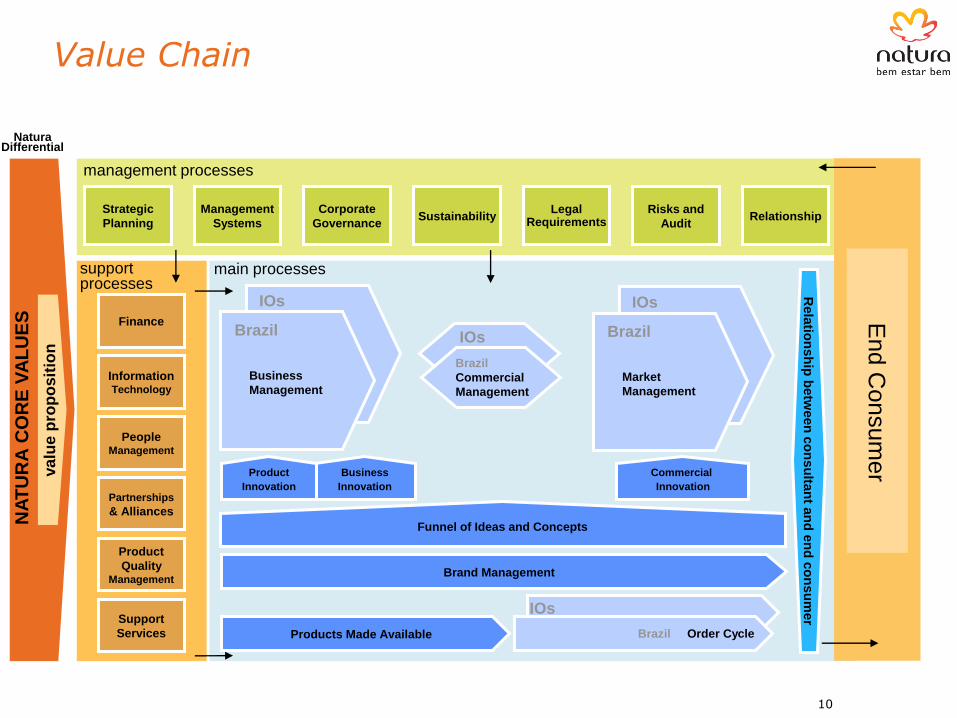

Value Chain

9

Value Chain

support processes

management processes

Natura Differential

NA

TU

RA

CO

RE

VA

LU

ES

va

lue

pro

po

sit

ion

People Management

Finance

main processes

Information Technology

Strategic

Planning

Corporate

Governance

IOs

IOs

Brazil

Commercial

Management

Market

Management

Brazil

Business

Management

Brazil

IOs

Management

Systems

Partnerships

& Alliances

Product

Quality Management

Support

Services

Relationship Sustainability Risks and

Audit

Legal

Requirements

Rela

tion

sh

ip b

etw

een

co

nsu

ltan

t an

d e

nd

co

nsu

mer

Brand Management

Products Made Available

IOs

Brazil Order Cycle

Business

Innovation

Product

Innovation

Commercial

Innovation

End C

onsum

er

Funnel of Ideas and Concepts

10

support processes

management processes

Natura Differential

NA

TU

RA

CO

RE

VA

LU

ES

va

lue

pro

po

sit

ion

People Management

Finance

main processes

Information Technology

Strategic

Planning

Corporate

Governance

IOs

IOs

Brazil

Commercial

Management

Market

Management

Brazil

Business

Management

Brazil

IOs

Management

Systems

Partnerships

& Alliances

Product

Quality Management

Support

Services

Relationship Sustainability Risks and

Audit

Legal

Requirements

Rela

tion

sh

ip b

etw

een

co

nsu

ltan

t an

d e

nd

co

nsu

mer

Brand Management

Products Made Available

IOs

Brazil Order Cycle

Business

Innovation

Product

Innovation

Commercial

Innovation

End C

onsum

er

Funnel of Ideas and Concepts

11

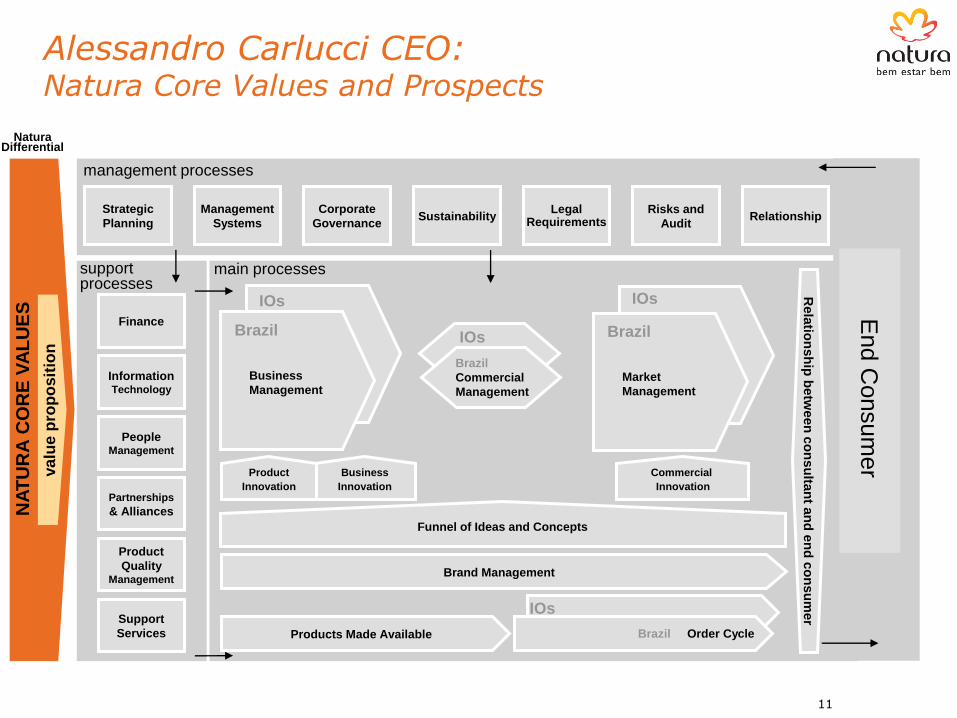

Alessandro Carlucci CEO: Natura Core Values and Prospects

support processes

management processes

Natura Differential

NA

TU

RA

CO

RE

VA

LU

ES

va

lue

pro

po

sit

ion

People Management

Finance

main processes

Information Technology

Strategic

Planning

Corporate

Governance

IOs

IOs

Brazil

Commercial

Management

Market

Management

Brazil

Business

Management

Brazil

IOs

Management

Systems

Partnerships

& Alliances

Product

Quality Management

Support

Services

Relationship Sustainability Risks and

Audit

Legal

Requirements

Rela

tion

sh

ip b

etw

een

co

nsu

ltan

t an

d e

nd

co

nsu

mer

Brand Management

Products Made Available

IOs

Brazil Order Cycle

Business

Innovation

Product

Innovation

Commercial

Innovation

End C

onsum

er

Funnel of Ideas and Concepts

12

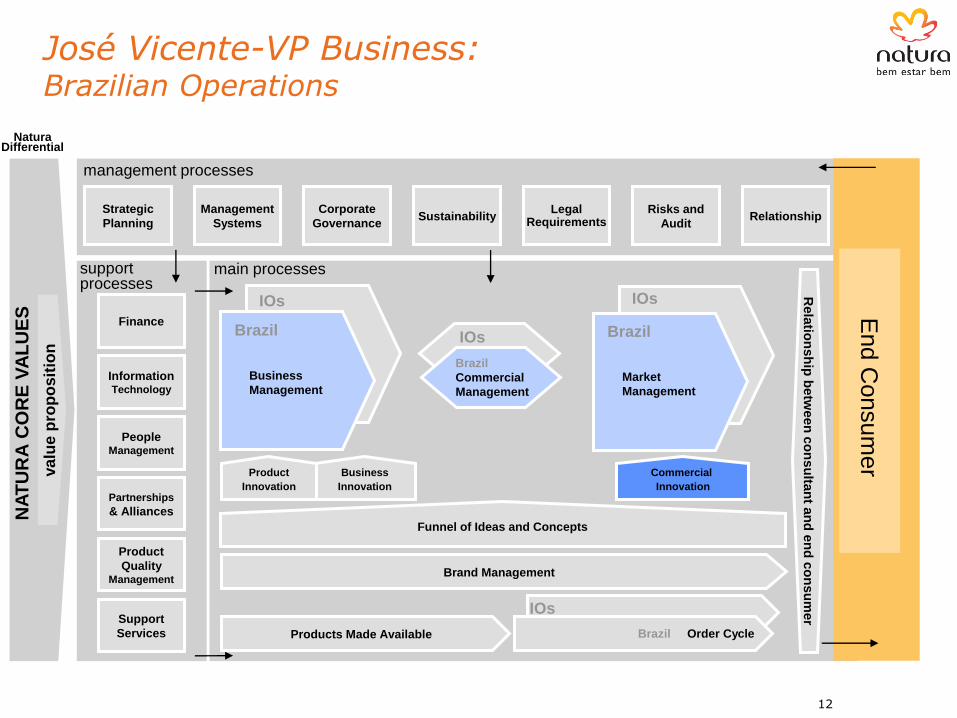

José Vicente-VP Business: Brazilian Operations

support processes

management processes

Natura Differential

va

lue

pro

po

sit

ion

People Management

Finance

main processes

Information Technology

Strategic

Planning

Corporate

Governance

IOs

IOs

Brazil

Commercial

Management

Market

Management

Brazil

Business

Management

Brazil

IOs

Management

Systems

Partnerships

& Alliances

Product

Quality Management

Support

Services

Relationship Sustainability Risks and

Audit

Legal

Requirements

Rela

tion

sh

ip b

etw

een

co

nsu

ltan

t an

d e

nd

co

nsu

mer

Brand Management

Products Made Available

IOs

Brazil Order Cycle

Business

Innovation

Product

Innovation

Commercial

Innovation

End C

onsum

er

Funnel of Ideas and Concepts

13

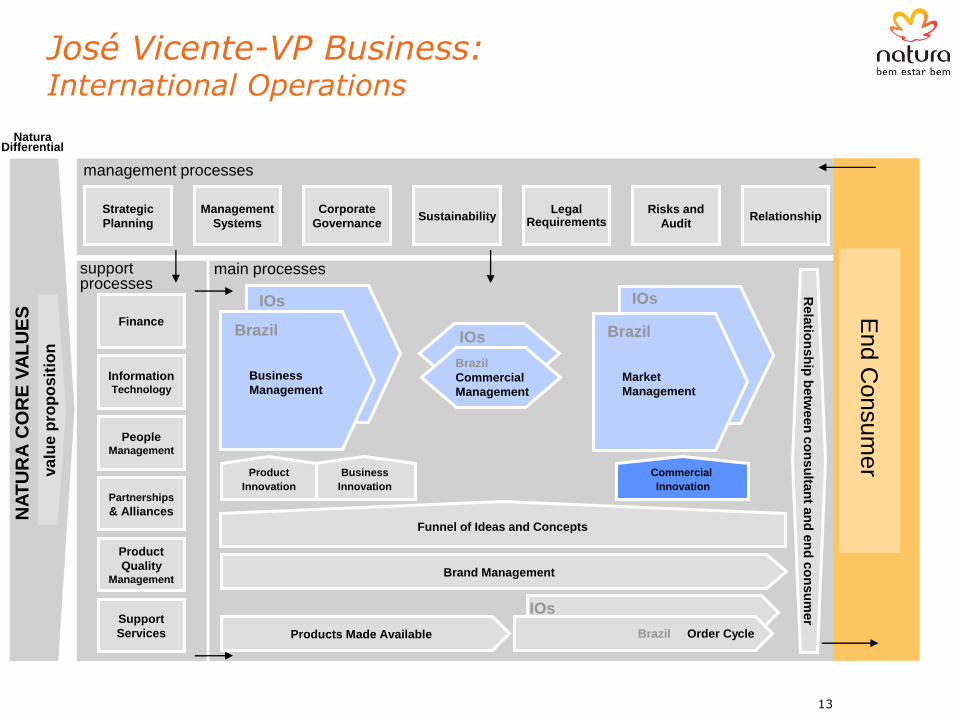

José Vicente-VP Business: International Operations

NA

TU

RA

CO

RE

VA

LU

ES

support processes

management processes

Natura Differential

va

lue

pro

po

sit

ion

People Management

Finance

main processes

Information Technology

Strategic

Planning

Corporate

Governance

IOs

IOs

Brazil

Commercial

Management

Market

Management

Brazil

Business

Management

Brazil

IOs

Management

Systems

Partnerships

& Alliances

Product

Quality Management

Support

Services

Relationship Sustainability Risks and

Audit

Legal

Requirements

Rela

tion

sh

ip b

etw

een

co

nsu

ltan

t an

d e

nd

co

nsu

mer

Brand Management

Products Made Available

IOs

Brazil Order Cycle

Business

Innovation

Product

Innovation

Commercial

Innovation

End C

onsum

er

Funnel of Ideas and Concepts

14

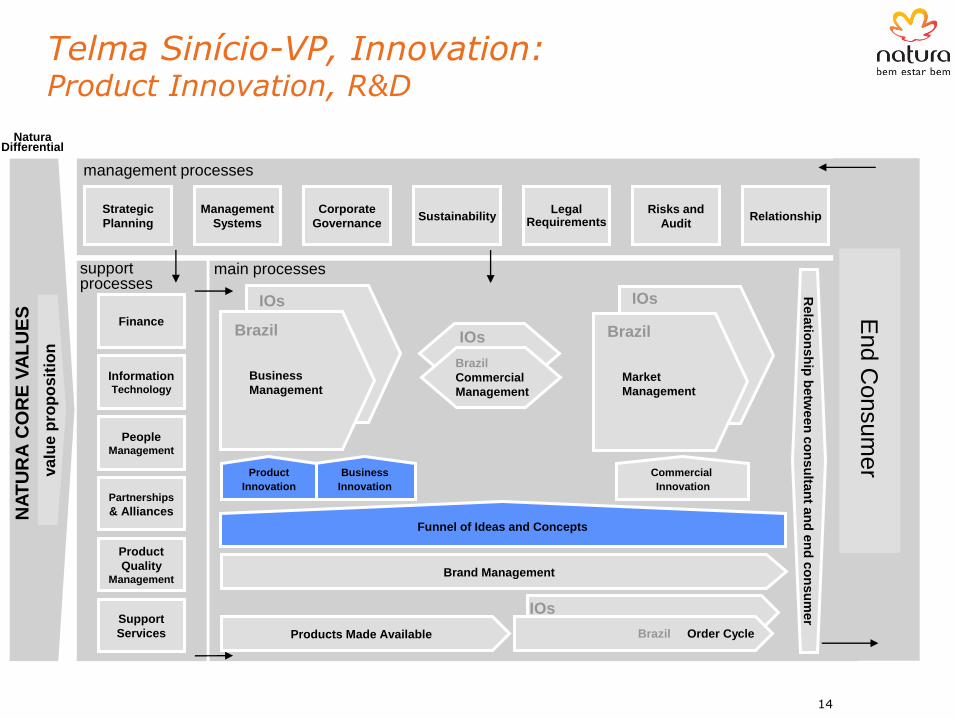

Telma Sinício-VP, Innovation: Product Innovation, R&D

NA

TU

RA

CO

RE

VA

LU

ES

support processes

management processes

Natura Differential

va

lue

pro

po

sit

ion

People Management

Finance

main processes

Information Technology

Strategic

Planning

Corporate

Governance

IOs

IOs

Brazil

Commercial

Management

Market

Management

Brazil

Business

Management

Brazil

IOs

Management

Systems

Partnerships

& Alliances

Product

Quality Management

Support

Services

Relationship Sustainability Risks and

Audit

Legal

Requirements

Rela

tion

sh

ip b

etw

een

co

nsu

ltan

t an

d e

nd

co

nsu

mer

Brand Management

Products Made Available

IOs

Brazil Order Cycle

Business

Innovation

Product

Innovation

Commercial

Innovation

End C

onsum

er

Funnel of Ideas and Concepts

15

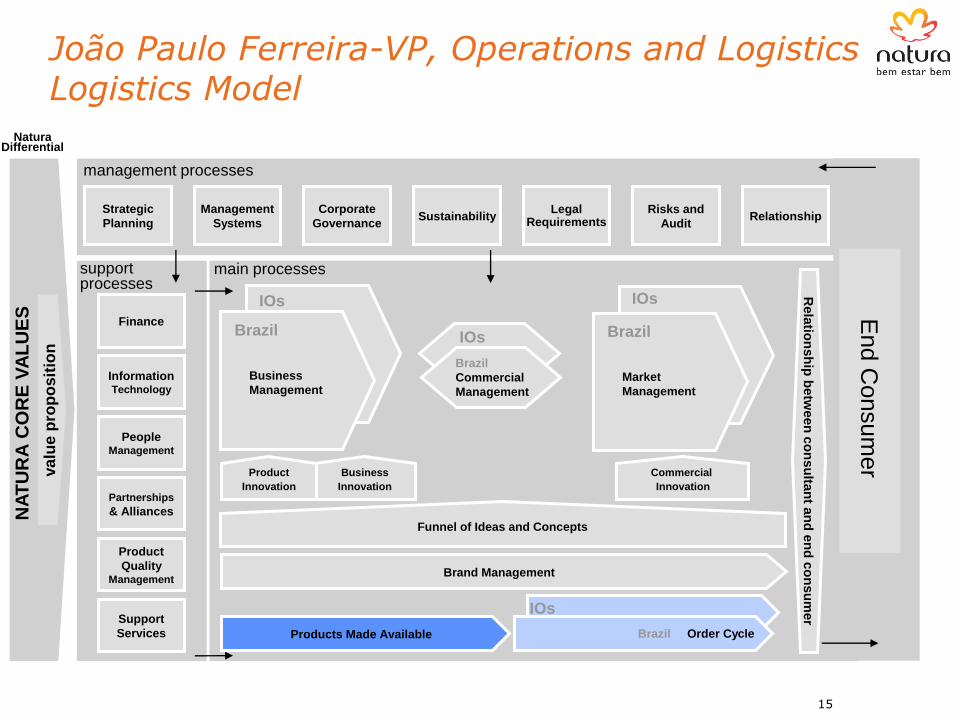

João Paulo Ferreira-VP, Operations and Logistics Logistics Model

NA

TU

RA

CO

RE

VA

LU

ES

support processes

management processes

Natura Differential

va

lue

pro

po

sit

ion

People Management

Finance

main processes

Information Technology

Strategic

Planning

Corporate

Governance

IOs

IOs

Brazil

Commercial

Management

Market

Management

Brazil

Business

Management

Brazil

IOs

Management

Systems

Partnerships

& Alliances

Product

Quality Management

Support

Services

Relationship Sustainability Risks and

Audit

Legal

Requirements

Rela

tion

sh

ip b

etw

een

co

nsu

ltan

t an

d e

nd

co

nsu

mer

Brand Management

Products Made Available

IOs

Brazil Order Cycle

Business

Innovation

Product

Innovation

Commercial

Innovation

End C

onsum

er

Funnel of Ideas and Concepts

16

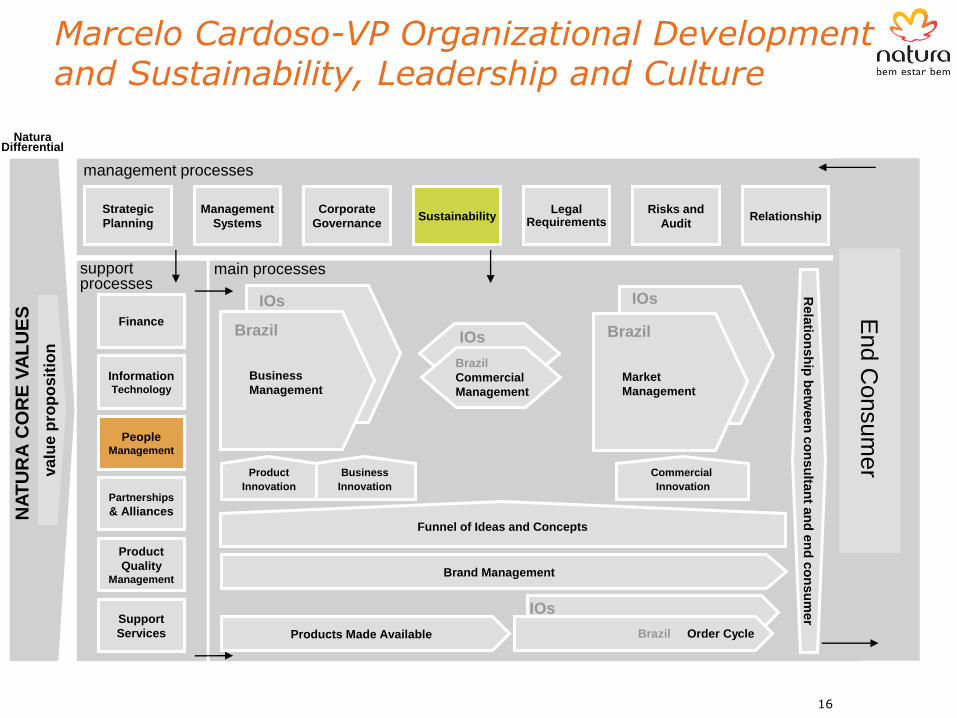

Marcelo Cardoso-VP Organizational Development and Sustainability, Leadership and Culture

NA

TU

RA

CO

RE

VA

LU

ES

support processes

management processes

Natura Differential

va

lue

pro

po

sit

ion

People Management

Finance

main processes

Information Technology

Strategic

Planning

Corporate

Governance

IOs

IOs

Brazil

Commercial

Management

Market

Management

Brazil

Business

Management

Brazil

IOs

Management

Systems

Partnerships

& Alliances

Product

Quality Management

Support

Services

Relationship Sustainability Risks and

Audit

Legal

Requirements

Rela

tion

sh

ip b

etw

een

co

nsu

ltan

t an

d e

nd

co

nsu

mer

Brand Management

Products Made Available

IOs

Brazil Order Cycle

Business

Innovation

Product

Innovation

Commercial

Innovation

End C

onsum

er

Funnel of Ideas and Concepts

17

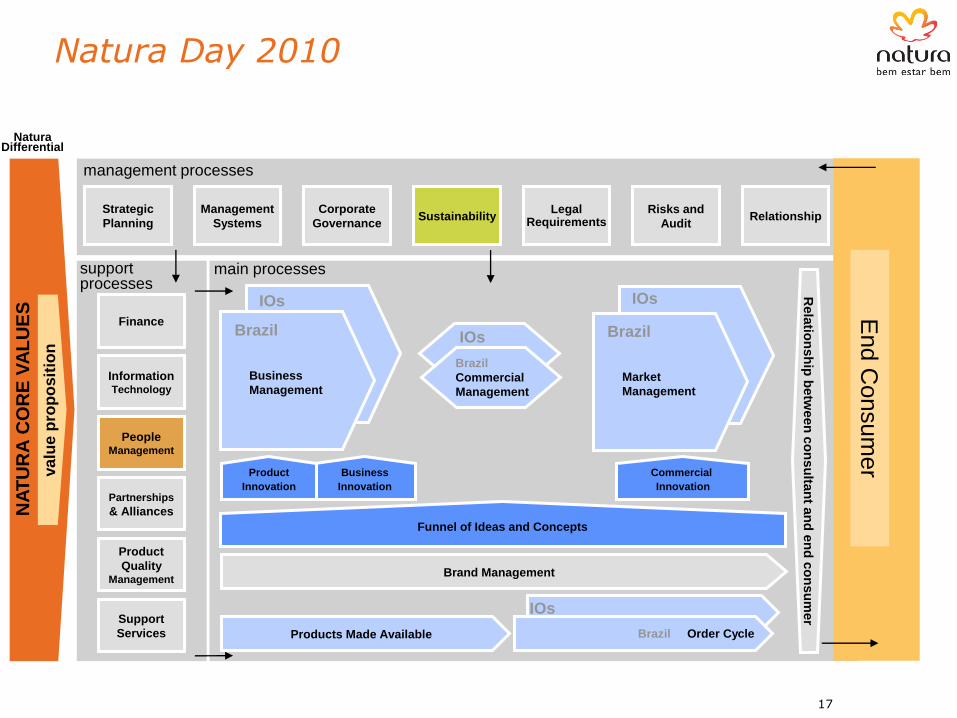

Natura Day 2010 N

AT

UR

A C

OR

E V

AL

UE

S

Schedule

18

Time Duration Activity Presenter

8:30 am 30 min Breakfast and Registration IR

9:00 am 40 min New makeup line Natura UNA Liliane

9:40 am 20 min Welcome - Schedule - Results Pedote / Helmut

10:00 am 25 min General Overview and Prospects Alessandro

10:25 am 25 min Brazilian Operations Zé Vicente

10:50 am 20 min Break

11:10 am 25 min International Operations Zé Vicente

11:35 am 25 min Innovation, Research & Development Telma

12:00 pm 50 min Q&A: Alessandro + Zé Vicente + Telma + Pedote

12:50 pm 90 min Lunch with Relationship Managers All participants

2:20 pm 25 min Operations and Logistics João Paulo

2:45 pm 25 min Development of Leadership, Culture and Sustainability Marcelo

3:10 pm 40 min Q&A: Alessandro + João Paulo + Marcelo + Pedote

3:50 pm Closing Alessandro

3:50 pm 60 min Cocktail

4:30 pm 30 min Tour

Consistent Results Since IPO

19

53

55

60

2007 2008 2009

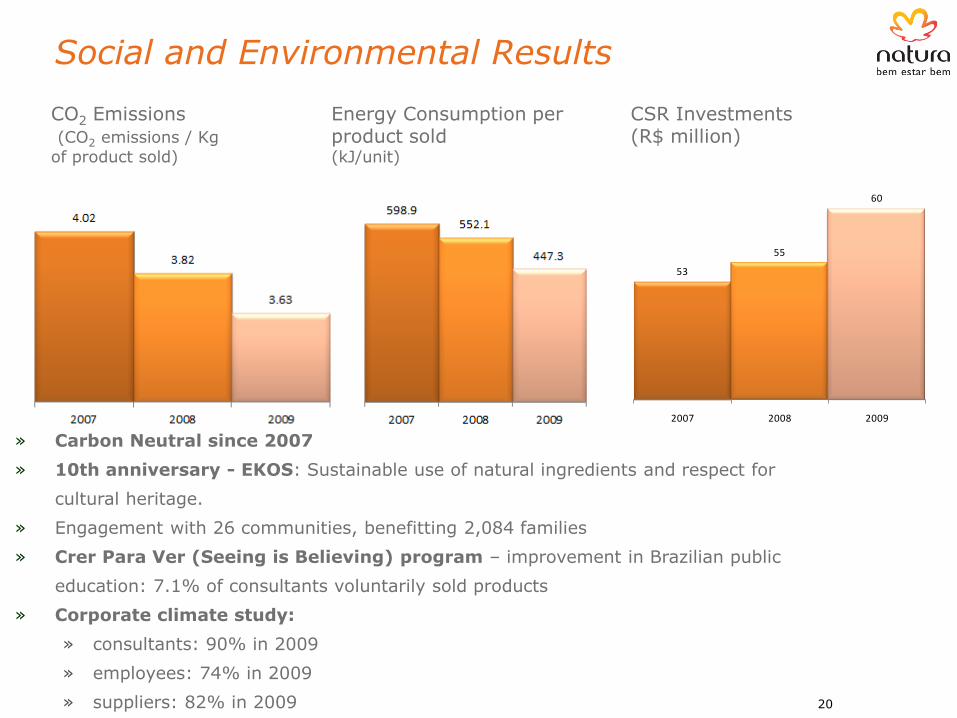

Social and Environmental Results

CO2 Emissions (CO2 emissions / Kg

of product sold)

» Carbon Neutral since 2007

» 10th anniversary - EKOS: Sustainable use of natural ingredients and respect for

cultural heritage.

» Engagement with 26 communities, benefitting 2,084 families

» Crer Para Ver (Seeing is Believing) program – improvement in Brazilian public

education: 7.1% of consultants voluntarily sold products

» Corporate climate study:

» consultants: 90% in 2009

» employees: 74% in 2009

» suppliers: 82% in 2009

CSR Investments (R$ million)

20

Energy Consumption per product sold (kJ/unit)

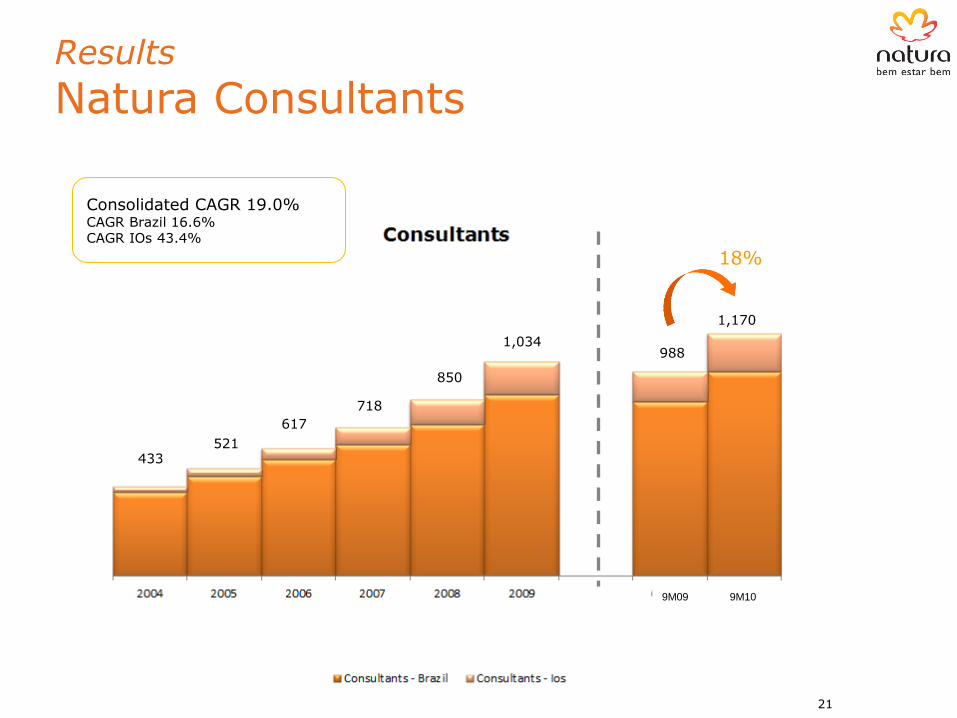

433

1,170

1,034

850

718

617

521

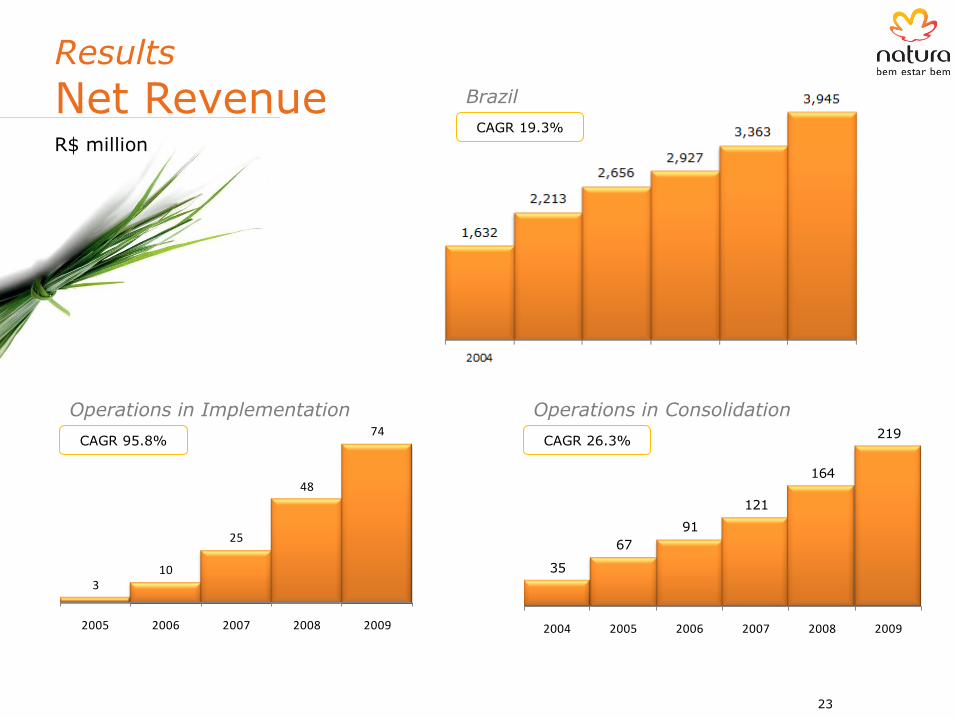

Consolidated CAGR 19.0% CAGR Brazil 16.6% CAGR IOs 43.4%

Results

Natura Consultants

18%

988

21

9M09 9M10

Results

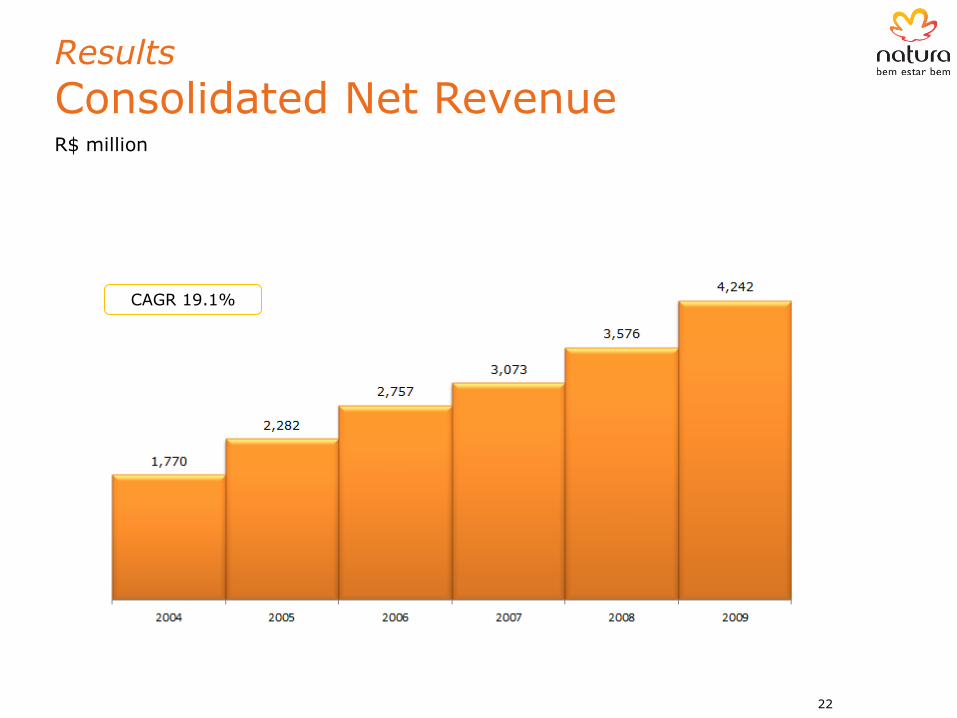

Consolidated Net Revenue R$ million

CAGR 19.1%

22

35

67

91

121

164

219

2004 2005 2006 2007 2008 2009

Receita Líquida Op. Consolidação

3 10

25

48

74

2005 2006 2007 2008 2009

Receita Líquida Op. Implantação

Results

Net Revenue CAGR 19.3%

23

R$ million

Brazil

CAGR 95.8%

Operations in Implementation

CAGR 26.3%

Operations in Consolidation

Results

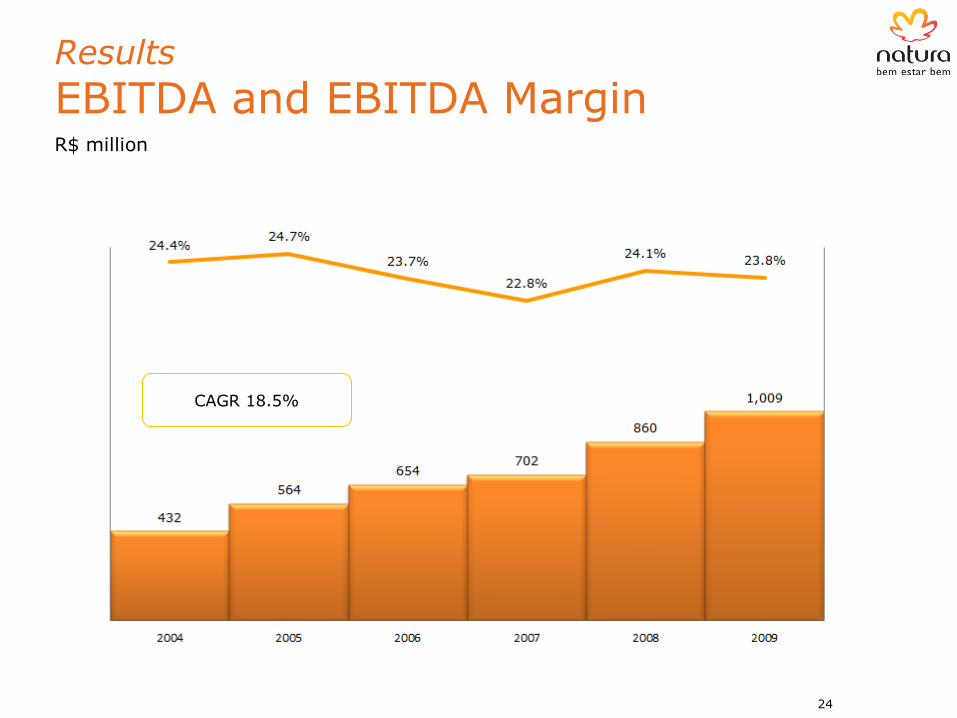

EBITDA and EBITDA Margin

CAGR 18.5%

24

R$ million

Results

International Investments

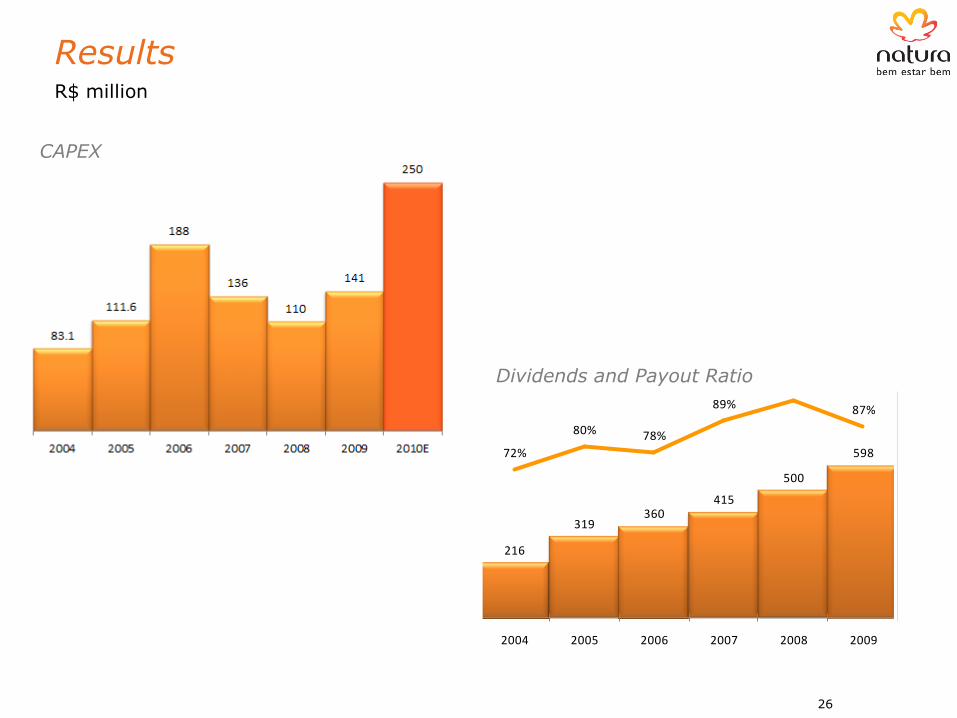

25

CAGR 20.4%

Brazil

Operations in Implementation Operations in Consolidation

R$ million

216

319360

415

500

59872%

80% 78%

89%

96%

87%

2004 2005 2006 2007 2008 2009

Dividendos

Dividendos Pay Out Ratio

Results

26

Dividends and Payout Ratio

CAPEX

R$ million

Results

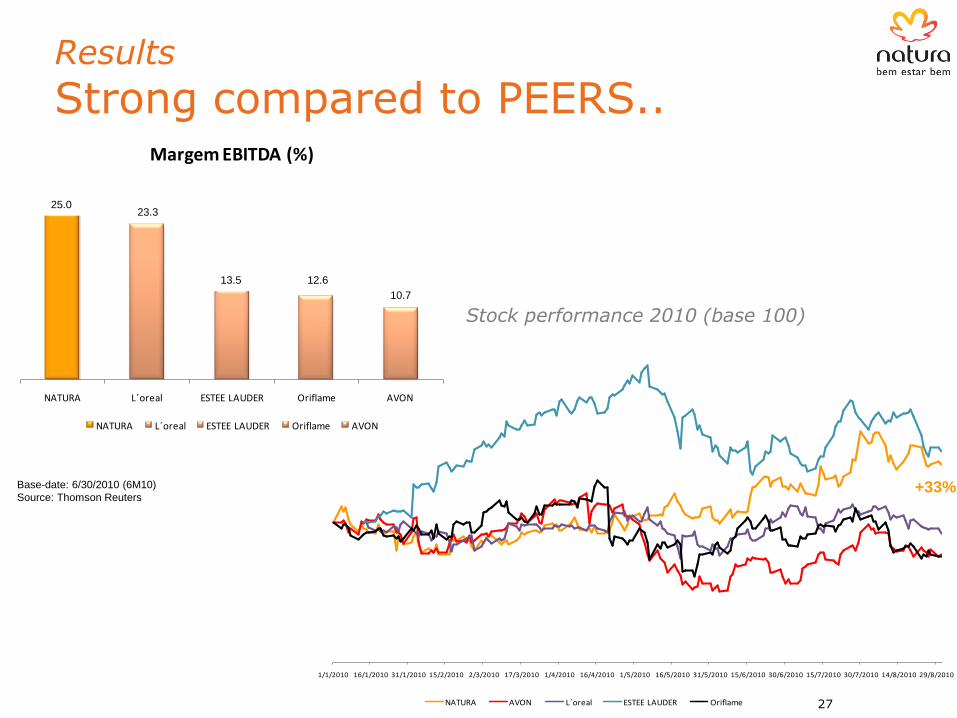

Strong compared to PEERS..

Desempenho Ações 2010 (Base 100)

Base-date: 6/30/2010 (6M10)

Source: Thomson Reuters

1/1/2010 16/1/2010 31/1/2010 15/2/2010 2/3/2010 17/3/2010 1/4/2010 16/4/2010 1/5/2010 16/5/2010 31/5/2010 15/6/2010 30/6/2010 15/7/2010 30/7/2010 14/8/2010 29/8/2010

NATURA AVON L´oreal ESTEE LAUDER Oriflame

+33%

25,023,3

13,512,6

10,7

NATURA L´oreal ESTEE LAUDER Oriflame AVON

Margem EBITDA (%)

NATURA L´oreal ESTEE LAUDER Oriflame AVON

27

Stock performance 2010 (base 100)

25.0 23.3

13.5 12.6

10.7

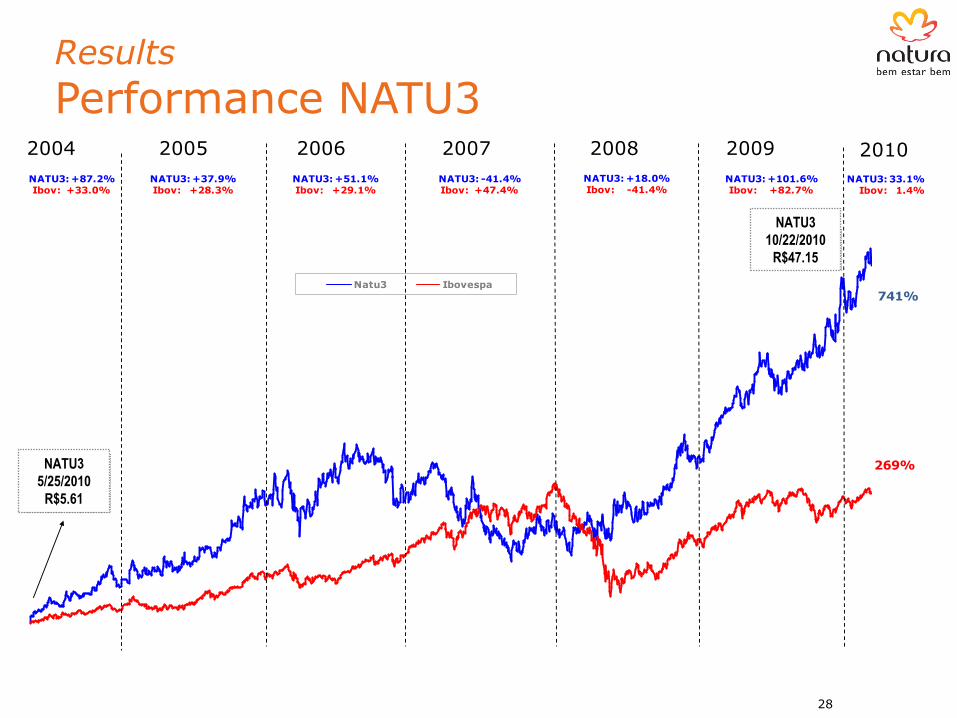

Results

Performance NATU3

Natu3 Ibovespa

NATU322/10/2010

R$47,15

NATU325/05/2004

R$5,61

2004 2005 2006 2007 2008 2009

NATU3: +87.2%Ibov: +33.0%

NATU3: +37.9%Ibov: +28.3%

NATU3: +51.1%Ibov: +29.1%

NATU3: -41.4%Ibov: +47.4%

NATU3: +18.0%Ibov: -41.4%

NATU3: +101.6%Ibov: +82.7%

2010

NATU3: 33.1%Ibov: 1.4%

741%

269%

28

NATU3

5/25/2010

R$5.61

NATU3

10/22/2010

R$47.15

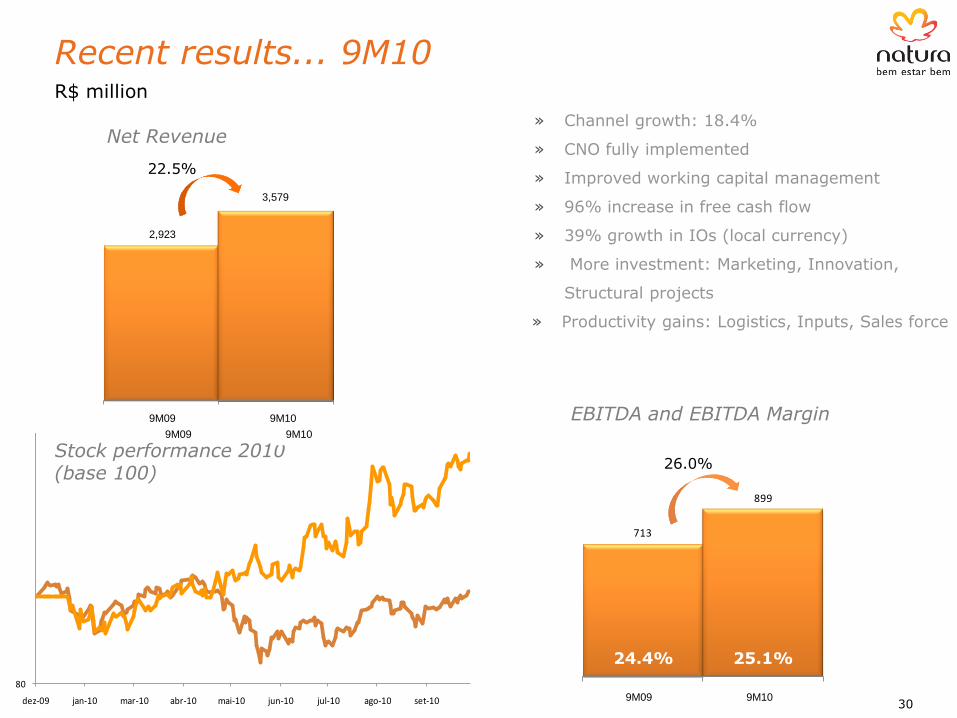

Recent Results

29

713

899

09M09 09M10

EBITDA

2.923

3.579

09M09 09M10

Receita Líquida

Recent results... 9M10

80

dez-09 jan-10 mar-10 abr-10 mai-10 jun-10 jul-10 ago-10 set-10

Ibovespa

NATU3

» Channel growth: 18.4%

» CNO fully implemented

» Improved working capital management

» 96% increase in free cash flow

» 39% growth in IOs (local currency)

» More investment: Marketing, Innovation,

Structural projects

» Productivity gains: Logistics, Inputs, Sales force

22.5%

26.0%

25.1% 24.4%

30

R$ million

Net Revenue

EBITDA and EBITDA Margin

Stock performance 2010 (base 100)

2,923

3,579

9M09 9M10

9M09 9M10

9M09 9M10

end.thank you

Alessandro Carlucci CEO

Natura’s strategy

NATURA DAY 2010

natura

HISTORY PRESENCE VALUE PROPOSITION

2

3

70s 80s 90s 00s Today

170

657

4,700

Sales Volume (retail) in US$ million

5

A small lab and

two passions:

cosmetics and

relationships

(1969)

Natura opts for

direct sales

system (1974)

High growth based

on regional

expansion and

product portfolio

Commitment to

social and

environmental

responsibility

Pursuit of

management

excellence

Corporate

governance

initiatives and

publication of GRI

Annual Report

Sustainable

development

Natura Ekos line

(2000)

Natura Plant in

Cajamar (2001)

IPO on Bovespa

(2004)

Increasing

leadership in the

Brazilian market

New growth cycle

in other Latin

American

countries

Evolution of the

management

model

OUR HISTORY

3

4

CF&T Market, 2009 (US$ billion)

Source: Euromonitor

Peru

Chile

Argentina

France

Mexico

Colombia

7.4

3.0

1.4

1.7

2.9

Brazil

28.4

OUR PRESENCE

UNIQUE

Value Proposition

CHANNEL PRODUCTS

CORPORATE

BEHAVIOR

BRAND

“Triple Bottom Line”

Social › Wealth creation for consultants

› R$ 60 mn invested in CSR1 in 2009

› Sharing benefits with supplier

communities

Economic › Strong cash flow generation

› Growth and profitability

› Consistent dividend payment

Environmental › Carbon neutral operations

› Use of refill package

› Sustainable extraction

› Use of recycled and recyclable

materials

1 Corporate Social Responsibility

Transform social and

environmental challenges

into business opportunities

5

STRATEGY

6

Investments and Structural Projects:

CAPEX (IT, production capacity and logistics)

New logistical model (New DCs, HUBs, production abroad)

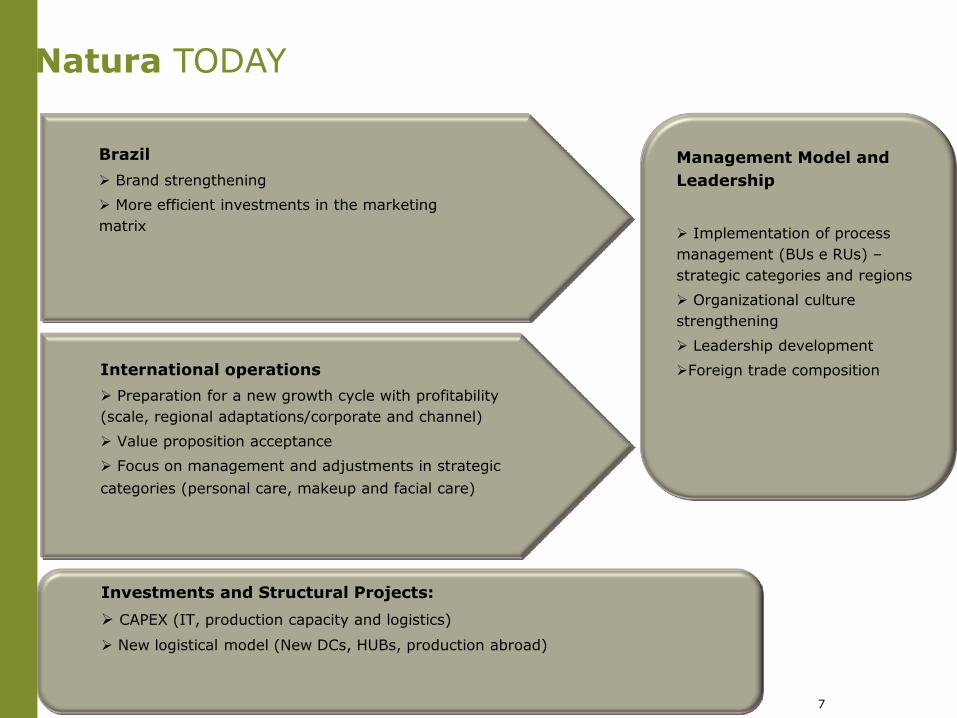

Natura TODAY

Management Model and

Leadership

Implementation of process

management (BUs e RUs) –

strategic categories and regions

Organizational culture

strengthening

Leadership development

Foreign trade composition

International operations

Preparation for a new growth cycle with profitability

(scale, regional adaptations/corporate and channel)

Value proposition acceptance

Focus on management and adjustments in strategic

categories (personal care, makeup and facial care)

Brazil

Brand strengthening

More efficient investments in the marketing

matrix

7

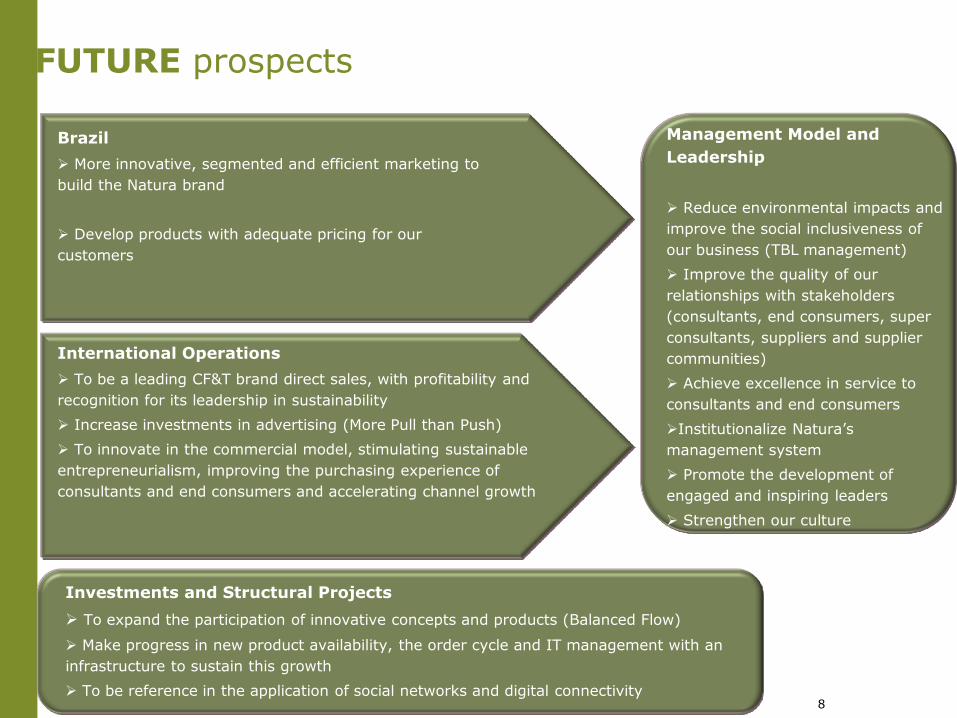

FUTURE prospects

Management Model and

Leadership

Reduce environmental impacts and

improve the social inclusiveness of

our business (TBL management)

Improve the quality of our

relationships with stakeholders

(consultants, end consumers, super

consultants, suppliers and supplier

communities)

Achieve excellence in service to

consultants and end consumers

Institutionalize Natura’s

management system

Promote the development of

engaged and inspiring leaders

Strengthen our culture

International Operations

To be a leading CF&T brand direct sales, with profitability and

recognition for its leadership in sustainability

Increase investments in advertising (More Pull than Push)

To innovate in the commercial model, stimulating sustainable

entrepreneurialism, improving the purchasing experience of

consultants and end consumers and accelerating channel growth

Brazil

More innovative, segmented and efficient marketing to

build the Natura brand

Develop products with adequate pricing for our

customers

Investments and Structural Projects

To expand the participation of innovative concepts and products (Balanced Flow)

Make progress in new product availability, the order cycle and IT management with an

infrastructure to sustain this growth

To be reference in the application of social networks and digital connectivity 8

end.thank you

José Vicente Marino

Business Vice President

Brazilian Operations

Natura Day 2010

Agenda

• CF&T Market Overview

• Business Proposition

• BUs and RUs • Categories and sub-brands • Marketing Matrix

CF&T Market Overview

4

Countries 2009 CAGR % „04- „09

United States 59 1.6%

Japan 40 0.7%

Brazil 28 14.1%

Mexico 7 7.4%

Argentina, Chile, Colombia and Peru

9 10.8%

Countries with Natura operations 44 12.2%

World 351 5.1%

CF&T market size (US$ billion)

Source: Euromonitor 2009

Brazil is the third largest

CF&T market in the world

Direct sales in CF&T market

Region Direct Sales (%)

Latin America 27.3%

Brazil 24.4%

Argentina 23.8%

Chile 19.5%

Colombia 38.5%

Mexico 31.6%

Peru 28.0%

Asia Pacific 11.7%

North America 8.5%

Western Europe 3.2%

Australasia 9.2%

Africa / Middle East 2.3%

Source: Euromonitor 2009

Large market Exceptional growth Direct sales

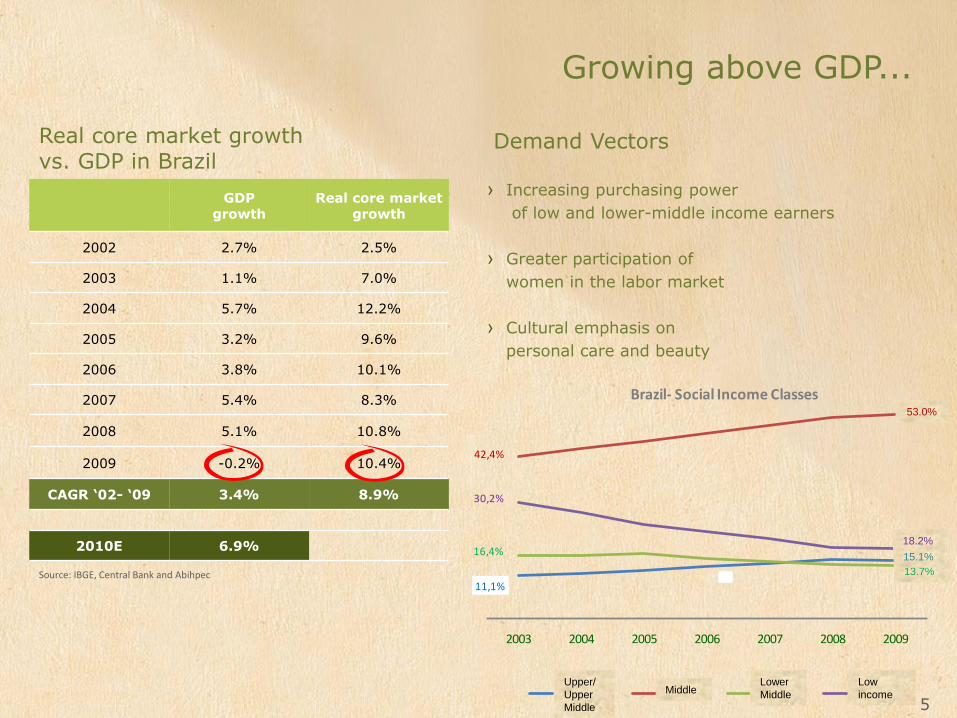

Growing above GDP...

GDP growth

Real core market growth

2002 2.7% 2.5%

2003 1.1% 7.0%

2004 5.7% 12.2%

2005 3.2% 9.6%

2006 3.8% 10.1%

2007 5.4% 8.3%

2008 5.1% 10.8%

2009 -0.2% 10.4%

CAGR ‘02- ‘09 3.4% 8.9%

2010E 6.9%

Real core market growth vs. GDP in Brazil

Source: IBGE, Central Bank and Abihpec

Demand Vectors

› Increasing purchasing power

of low and lower-middle income earners

› Greater participation of

women in the labor market

› Cultural emphasis on

personal care and beauty

5

11,1%

15,1%

42,4%

53,0%

16,4%

13,7%

30,2%

18,2%

2003 2004 2005 2006 2007 2008 2009

Brazil- Social Income Classes

Class AB Class C Class D Class EUpper/

Upper

Middle

Middle Lower

Middle

Low

income

53.0%

18.2%

13.7%

15.1%

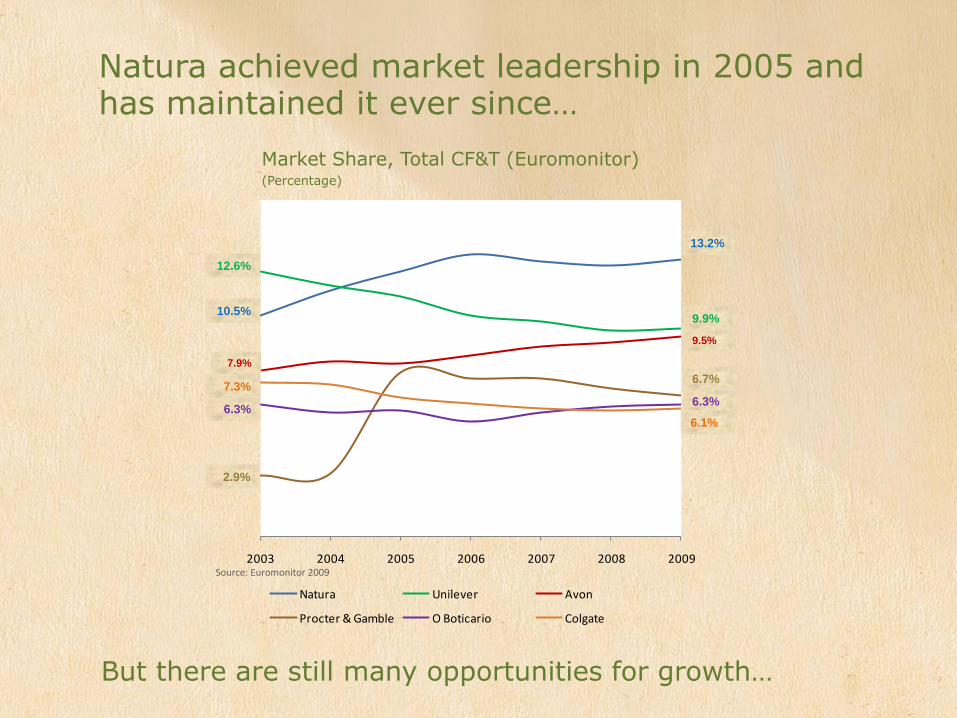

10,5

13,212,6

9,9

7,9

9,5

2,9

6,7

6,3 6,37,3

6,1

2003 2004 2005 2006 2007 2008 2009

Natura Unilever Avon

Procter & Gamble O Boticario Colgate

Natura achieved market leadership in 2005 and has maintained it ever since…

Market Share, Total CF&T (Euromonitor)

(Percentage)

Source: Euromonitor 2009

But there are still many opportunities for growth…

9.5%

6.3%

9.9%

6.1% 6.3%

6.7%

13.2%

7.9%

12.6%

7.3%

2.9%

10.5%

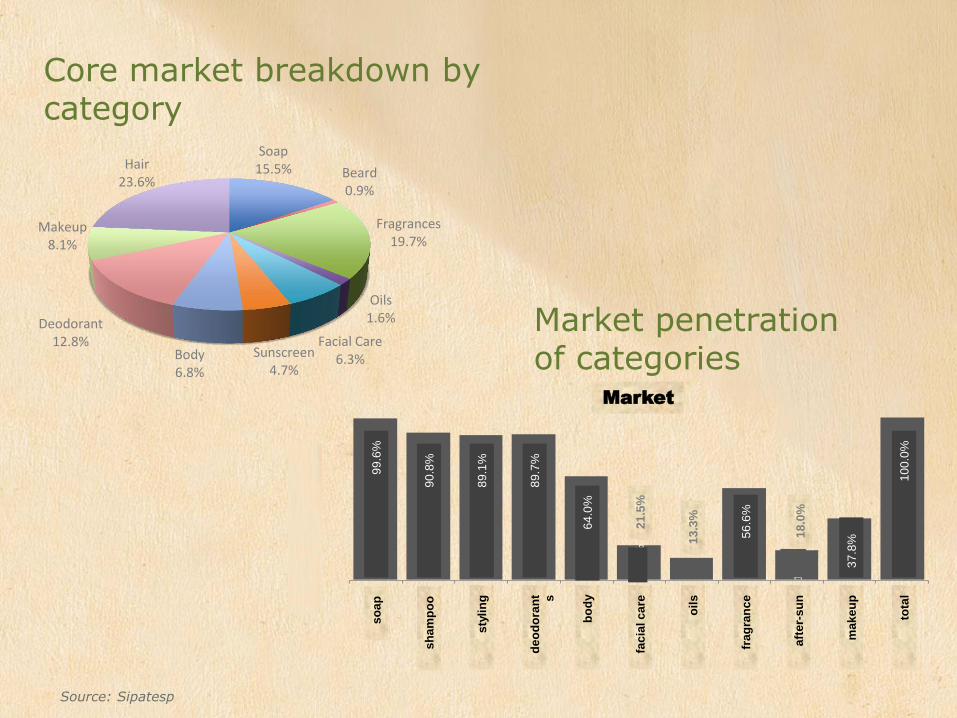

Categories

Core market breakdown by category

Source: Sipatesp

Market penetration of categories

99,6

%

90,8

%

89,1

%

89,7

%

64,0

%

21,5

% 13,3

%

56,6

%

18,0

%

37,8

%

100,0

%

sabonete

sham

poo

pos s

ham

poo

desodora

nte

s

corp

o

rosto

óle

os

perf

um

es

pro

t sola

r

maquia

gem

tota

l

MercadoMarket

so

ap

sh

am

po

o

sty

lin

g

de

od

ora

nt s

bo

dy

fac

ial c

are

oil

s

fra

gra

nc

e

aft

er-

su

n

ma

ke

up

tota

l

99

.6%

90

.8%

89

.1%

89

.7%

64

.0%

13

.3%

21

.5%

56

.6%

18

.0%

37

.8%

10

0.0

%

Soap 15.5% Beard

0.9%

Fragrances 19.7%

Oils 1.6%

Facial Care 6.3% Sunscreen

4.7% Body 6.8%

Deodorant 12.8%

Makeup 8.1%

Hair 23.6%

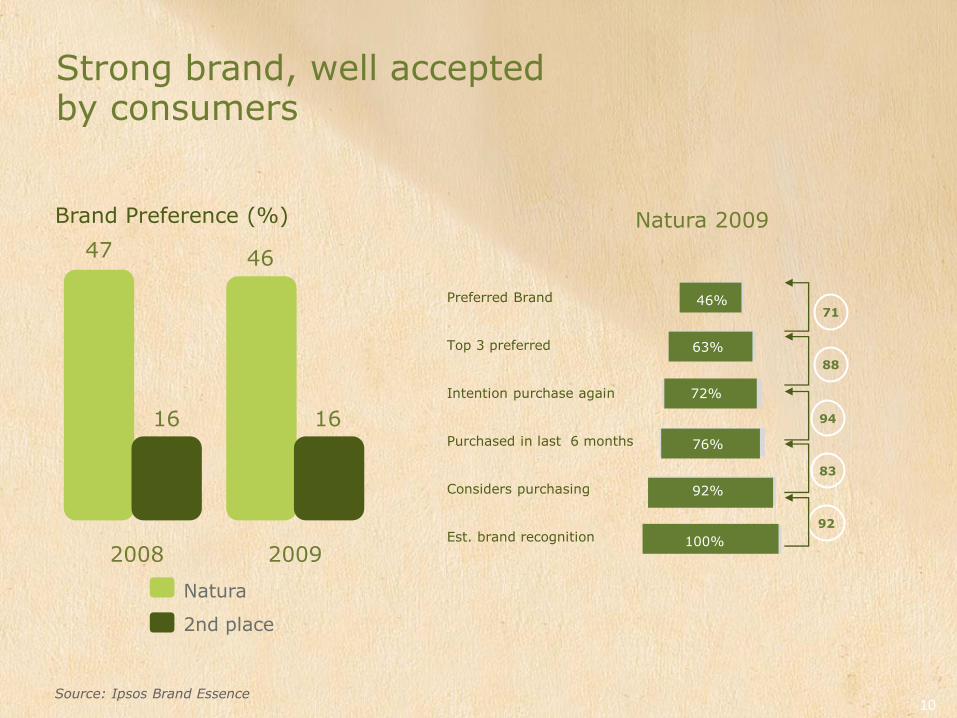

Brand strength

10

Strong brand, well accepted by consumers

Source: Ipsos Brand Essence

Brand Preference (%)

Preferred Brand

Top 3 preferred

Intention purchase again

Purchased in last 6 months

Considers purchasing

Est. brand recognition

Natura 2009

83

92

94

88

71

100%

92%

76%

72%

63%

46%

2008 2009

47 46

16 16

Natura

2nd place

Business Proposition

Business Proposition

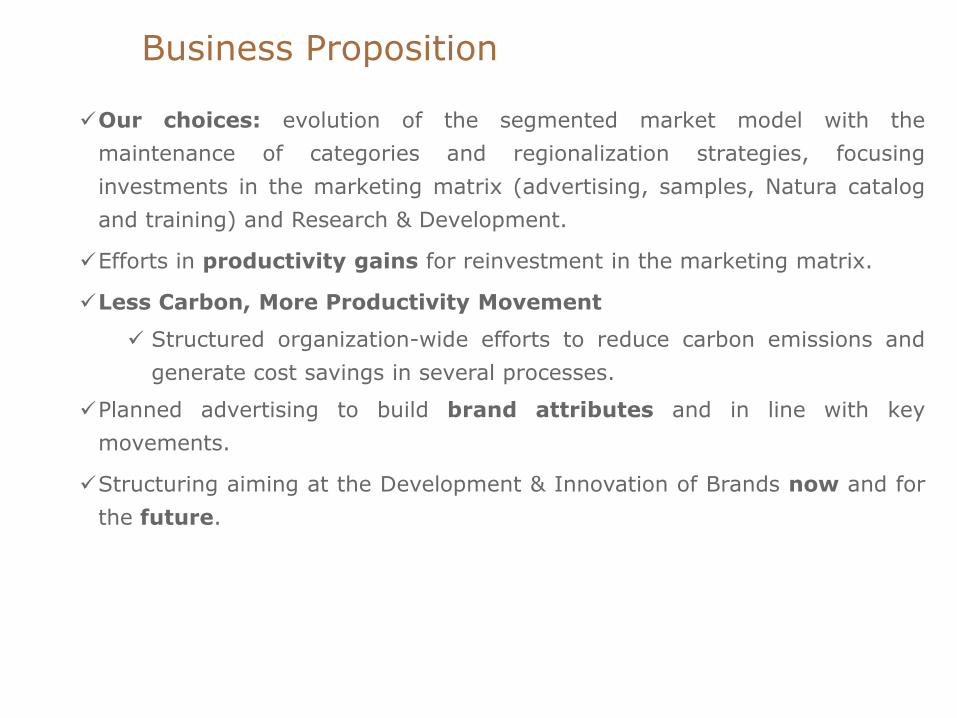

Our choices: evolution of the segmented market model with the

maintenance of categories and regionalization strategies, focusing

investments in the marketing matrix (advertising, samples, Natura catalog

and training) and Research & Development.

Efforts in productivity gains for reinvestment in the marketing matrix.

Less Carbon, More Productivity Movement

Structured organization-wide efforts to reduce carbon emissions and

generate cost savings in several processes.

Planned advertising to build brand attributes and in line with key

movements.

Structuring aiming at the Development & Innovation of Brands now and for

the future.

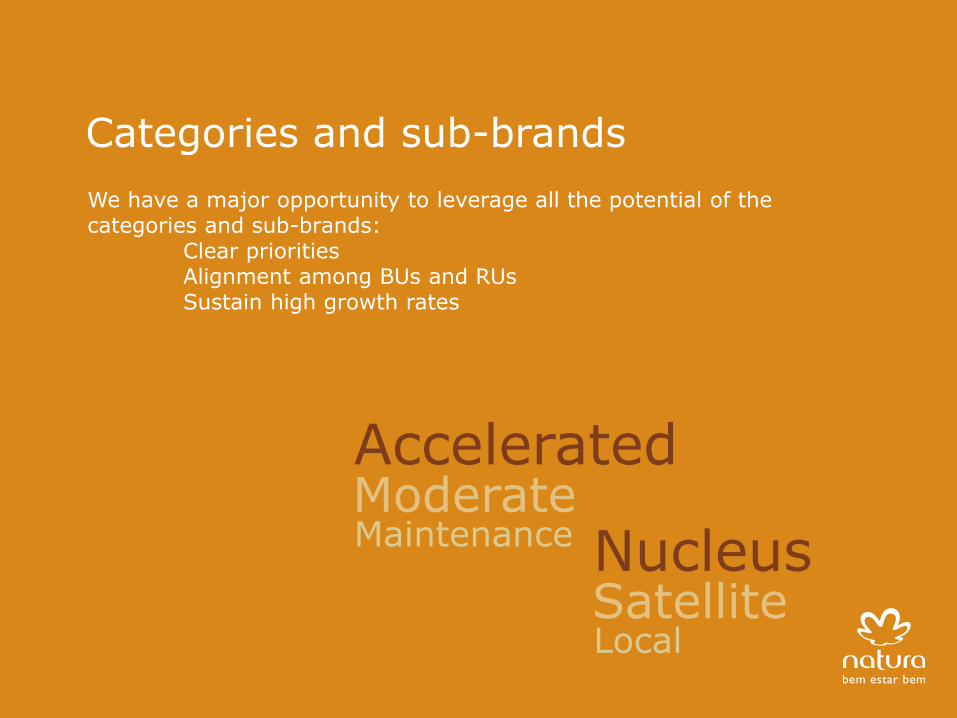

We have a major opportunity to leverage all the potential of the categories and sub-brands: Clear priorities Alignment among BUs and RUs Sustain high growth rates

Categories and sub-brands

Accelerated

Maintenance Moderate

Nucleus

Local Satellite

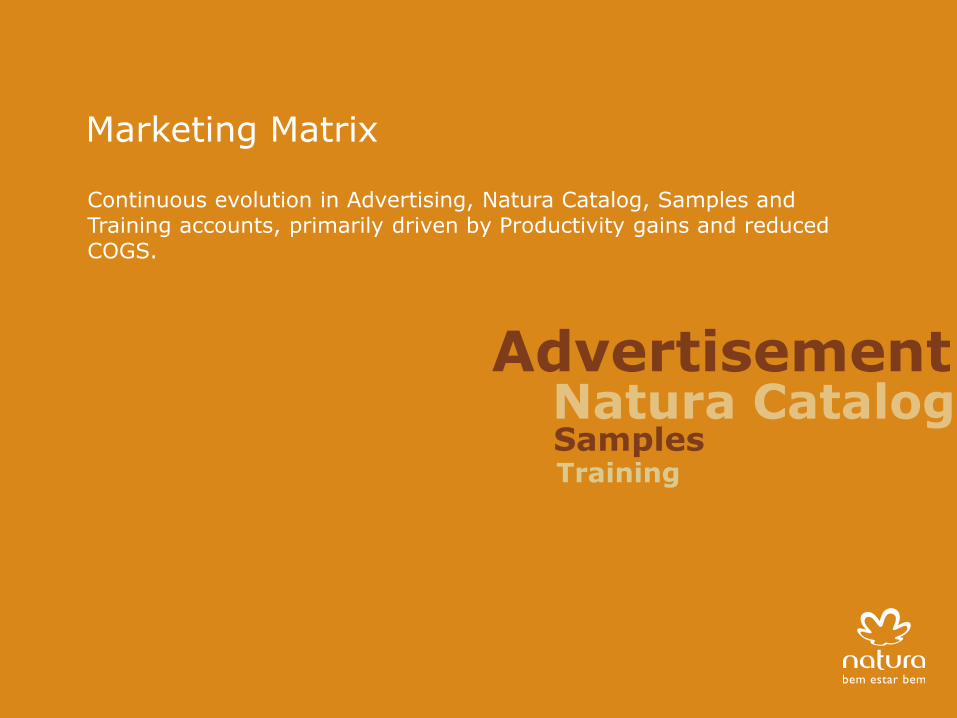

Continuous evolution in Advertising, Natura Catalog, Samples and Training accounts, primarily driven by Productivity gains and reduced COGS.

Marketing Matrix

Advertisement

Samples Natura Catalog

Training

BUs and RUs

BU Leader

Categories and Strategies

Key brands

Main BU goals

Inspiration

Oils Soaps

Ekos Amor América Sève

Gilberto Baptista

Face Makeup Sunscreen

Chronos UNA Aquarela Faces/Faces ZIP Fotoequilíbrio

Mônica Gregori

Body, Hair, Beard and Deodorants

Tododia Erva Doce Natura Homem Plant

Guto Pedreira

- Competition with retail products (price repositioning) - Daily use products

-Technological innovation (protection, sensations) - “Beauty” products

Give new meaning to routines

Reveal beauty Appreciate diversity

- Use of natural ingredients - Innovation in sensations and textures - Sustainable and recyclable packaging

Fragrance Children‟s Vertical Strategies

Amó Humor Kaiak Natura Águas Naturé Mamãe e Bebê CPV

Denise Figueiredo

-Fragrance and sample innovation - Regionalized fragrances

Strengthen relationships

BU B BU D BU C BU A

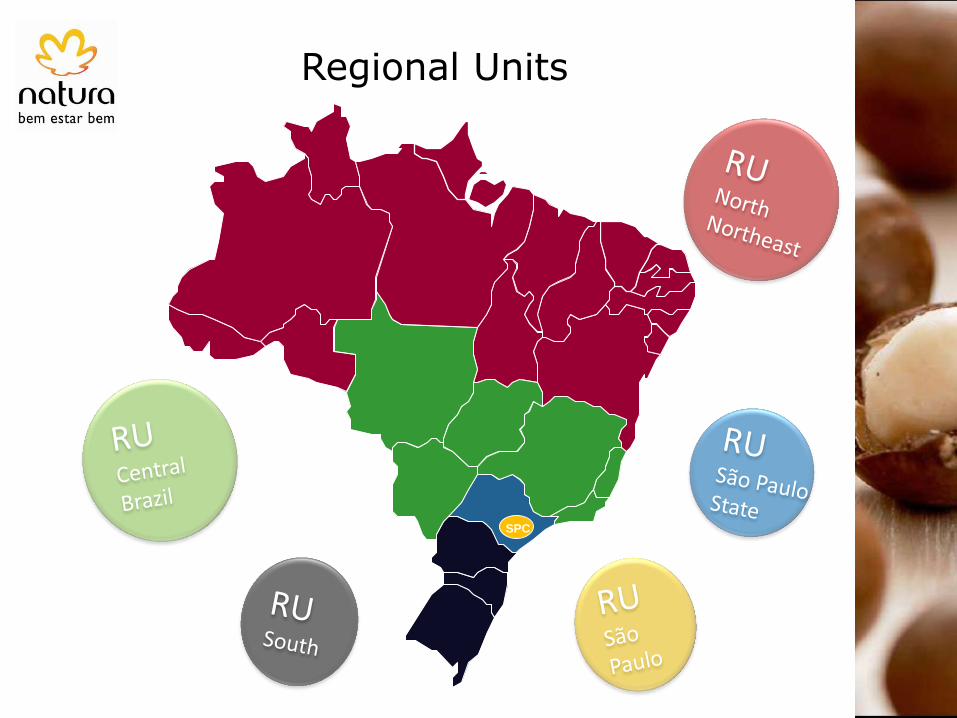

Regional Units

SPC

With the operations in progress, regionalization initiatives are already functional...

» Regionalized product launches

» Targeted catalogs for different regions

» Promotions adapted to regional opportunities

09-2010 Cycle Central Brazil

Cover Inside cover - sales Back cover

09-2010 Cycle São Paulo, São Paulo State, South

Cover Inside cover Back cover

09-2010 Cycle North/Northeast

Cover Inside cover Back cover

11-2010 Cycle Central Brazil

Cover Inside cover - sales Back cover

11-2010 Cycle São Paulo, São Paulo State, South

Cover Inside cover Back cover

11-2010 Cycle North/Northeast

Cover Inside cover Back cover

... And we will implement new initiatives in the coming years.

» Regionalized product portfolio

» Intersecting regional and category strategies targeted to

meet regional opportunities

» Increased understanding of local consumption habits

» Transformation of social challenges to establish an

inclusive, sustainable business model that can be

replicated in all regions

end.thank you

Natura Day 2010

International Operations

José Vicente Business Vice President

AGENDA

» Market & Competition

» International Operating Proposition

» International Strategy

2

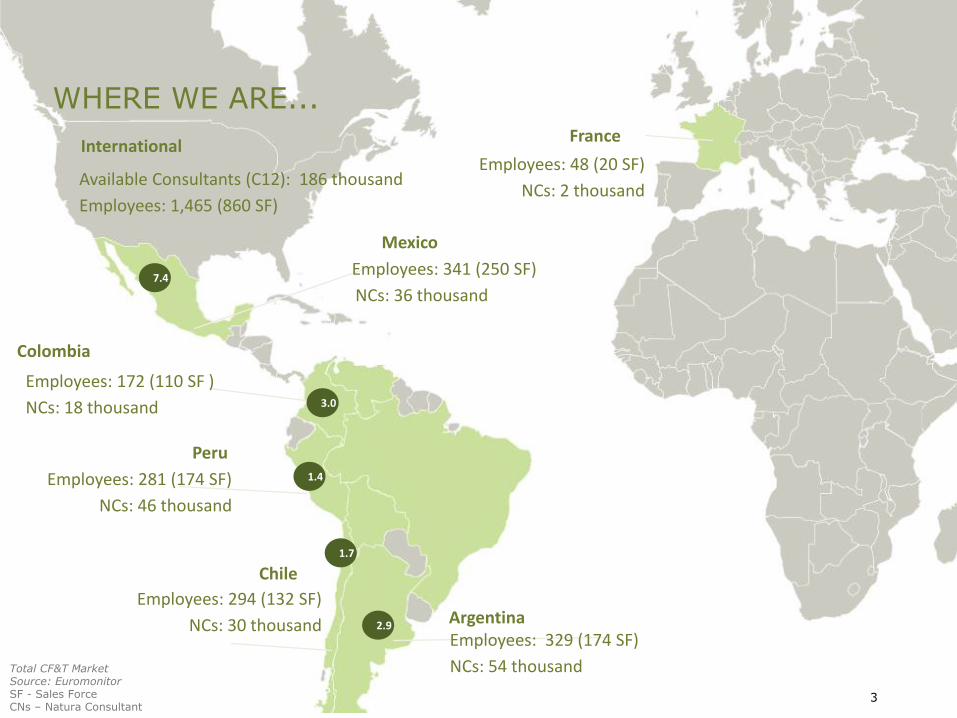

WHERE WE ARE...

Argentina Employees: 329 (174 SF)

NCs: 54 thousand

Chile

Employees: 294 (132 SF)

NCs: 30 thousand

Peru

Employees: 281 (174 SF)

NCs: 46 thousand

Mexico

Employees: 341 (250 SF)

NCs: 36 thousand

Colombia

Employees: 172 (110 SF )

NCs: 18 thousand

Available Consultants (C12): 186 thousand

Employees: 1,465 (860 SF)

International France

Employees: 48 (20 SF)

NCs: 2 thousand

7.4

3.0

1.4

1.7

2.9

Total CF&T Market Source: Euromonitor SF - Sales Force CNs – Natura Consultant

3

Core market size

2009 (US$ million) 5,456 2,271 2,254 1,263 998

Direct sales 2009

(US$ million)

CFT growth 01-09

(%) CAGR 7% 9% 21% 8% 8%

% Direct sales 2009 32% 38% 24% 19% 28%

• P&G •P&G • Unilever • Unilever • P&G

• Unilever •Unilever •P&G •L´Oréal • Unilever

•Colgate-Palm. •Colgate-Palm. •L´Oréal •P&G •Colgate-Palm.

•Avon • Avon •Avon •Avon • Belcorp

•Jafra • Belcorp •Natura •Belcorp • Unique

•Fuller •Yanbal •Tsu •Natura •Avon

• Fragrance • Fragrance • Hair • Hair • Hair

• Hair • Hair • Deodorants • Deodorants • Fragrances

• Facial care • Body • Fragrances • Fragrances • Makeup

• Fragrances • • Fragrances • •

• Makeup • • Body • •

• Facial care • Body • Makeup • Face • Face

Main competitors

Retail

874 1.724 536 246 279

Top 3 Categories

Total market

Top 3 Categories Direct sales

Direct sales

MARKET & COMPETITION LatAm CFT market presents country-specific challenges

Mercado Alvo Fonte: Euromonitor 4

Main competitors

Fragrances

Makeup

Fragrances

Makeup

Fragrances

Makeup

INTERNATIONAL OPERATING PROPOSITION

To be among the leading brands in direct CF&T sales

in all Latin America countries where we operate in and to be recognized

for its leadership in sustainability and with

profitability.

5

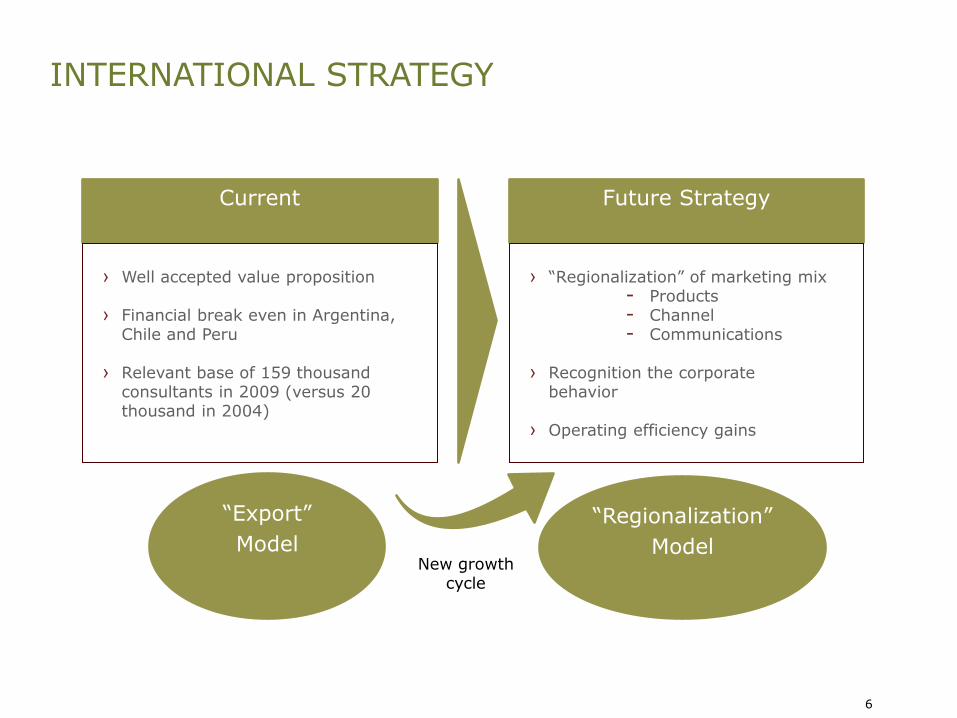

INTERNATIONAL STRATEGY

› Well accepted value proposition

› Financial break even in Argentina, Chile and Peru

› Relevant base of 159 thousand

consultants in 2009 (versus 20 thousand in 2004)

› “Regionalization” of marketing mix - Products - Channel - Communications

› Recognition the corporate

behavior

› Operating efficiency gains

Current Future Strategy

New growth cycle

“Export”

Model

“Regionalization”

Model

6

BASED ON VALUE PROPOSITION

CHANNEL PRODUCTS

CORPORATE

BEHAVIOR

ESSENCE

“Triple Bottom Line”

7

BRAND

» Well-accepted brand, although still little-known

» Marketing matrix: + push - pull

» Increased investments in advertising and samples

8

PRODUCTS

» Focus resources in regionally strategic categories (Personal care, Makeup and Facial care) and core brands (Ekos, Tododia, Chronos and UNA)

» Develop technologies and products that incorporate local biodiversity

» More efficient portfolio management: › Quantity of SKUS › Product Regionalization › Price Positioning › Promotions › Local Production

9

CHANNEL

» NEW COMMERCIAL MODEL

» To promote accelerated growth

» More levels

» To stimulate economic, social and environmental entrepreneurship

IMPLEMENTATION TIMELINE

Mexico

1H11

Colombia

2H11

Argentina, Chile and Peru

2012

10

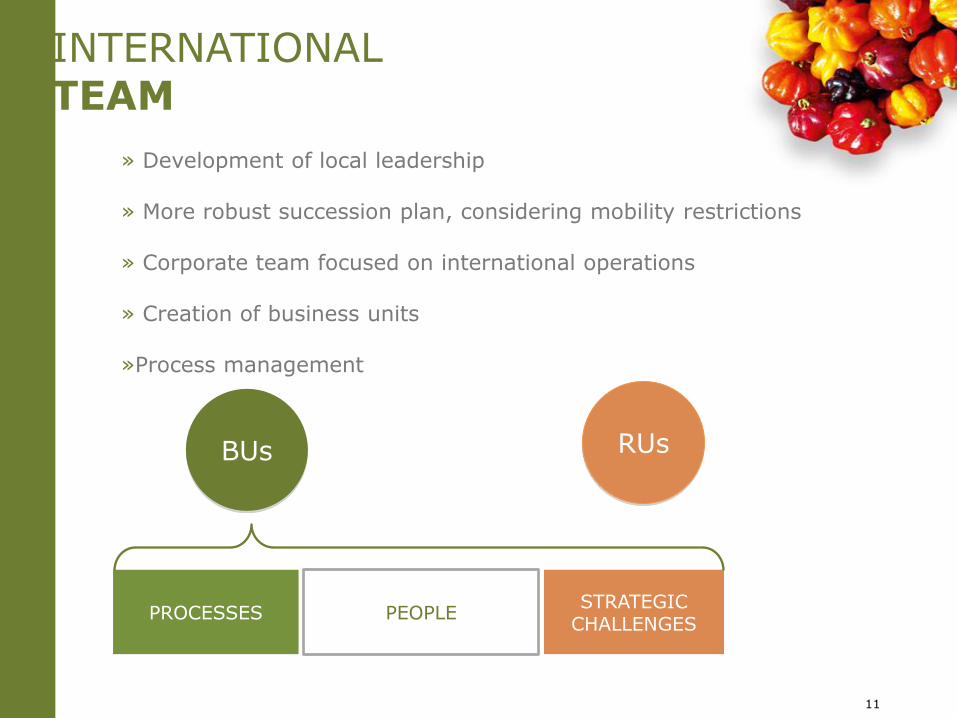

INTERNATIONAL TEAM

» Development of local leadership

» More robust succession plan, considering mobility restrictions

» Corporate team focused on international operations

» Creation of business units

»Process management

RUs

PROCESSES STRATEGIC

CHALLENGES PEOPLE

BUs

11

effective management of impacts related to water, carbon and waste

significant changes in relationship quality through education and global dialogue

consistent communications and promotion of joint initiatives

CORPORATE BEHAVIOR

12

Create an identity that distinguishes our corporate performance based on

Social and environmental

entrepreneurialism of our channel Sustainable use of regional biodiversity

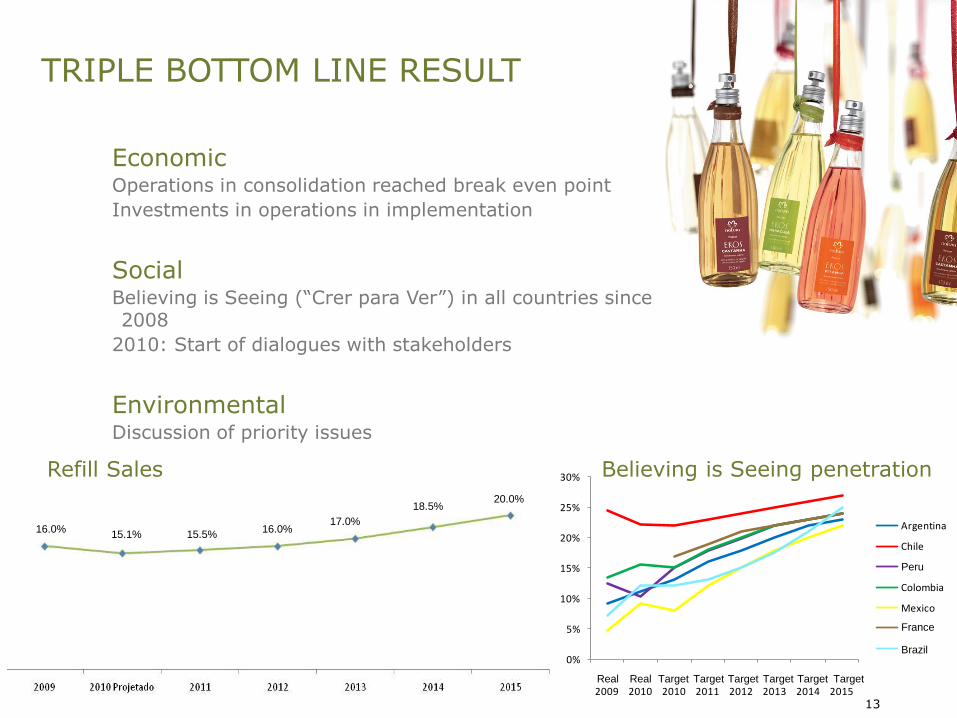

TRIPLE BOTTOM LINE RESULT

Economic Operations in consolidation reached break even point

Investments in operations in implementation

Social Believing is Seeing (“Crer para Ver”) in all countries since 2008

2010: Start of dialogues with stakeholders

Environmental Discussion of priority issues

0%

5%

10%

15%

20%

25%

30%

Ac. 2009

Ac. 2010

Meta 2010

Meta 2011

Meta 2012

Meta 2013

Meta 2014

Meta 2015

Argentina

Chile

Perú

Colombia

Mexico

Francia

Brasil

Refill Sales Believing is Seeing penetration

13

16.0% 15.1% 15.5%

16.0% 17.0%

18.5% 20.0%

Peru

France

Brazil

Real Real Target Target Target Target Target Target

end.thank you

Telma Sinicio

Innovation Vice President

Innovation

Natura Day 2010

Agenda

Innovation

• What is innovation at Natura?

• Natura’s Vision of Innovation

• Organizational Structure

• New Abilities

• Innovation Processes

What is innovation at Natura?

Starting point

What is innovation at Natura?

Starting point

Create Flow

Experience

Natura’s Vision of Innovation

To create an innovative experience flow of well being well

to exceed the expectations of our relationship network

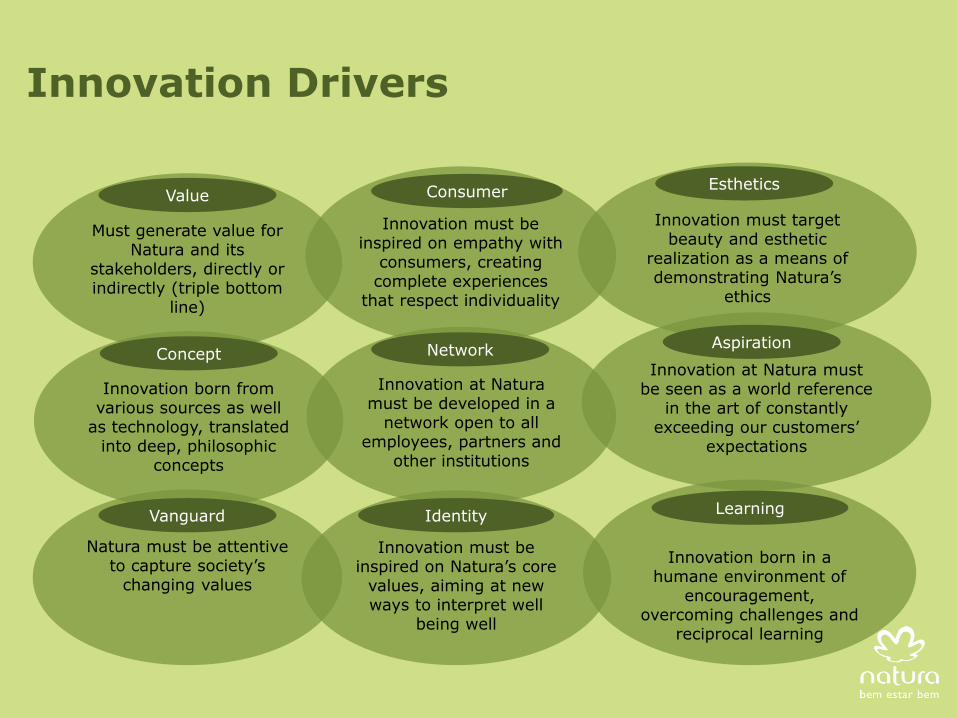

Innovation Drivers

Must generate value for

Natura and its stakeholders, directly or indirectly (triple bottom

line)

Innovation must target

beauty and esthetic realization as a means of demonstrating Natura’s

ethics

Natura must be attentive

to capture society’s changing values

Innovation born from

various sources as well as technology, translated

into deep, philosophic concepts

Innovation must be

inspired on empathy with consumers, creating complete experiences

that respect individuality

Innovation at Natura

must be developed in a network open to all

employees, partners and other institutions

Innovation must be

inspired on Natura’s core values, aiming at new ways to interpret well

being well

Innovation born in a humane environment of

encouragement, overcoming challenges and

reciprocal learning

Vanguard

Value Esthetics

Concept

Consumer

Identity

Network Innovation at Natura must

be seen as a world reference in the art of constantly

exceeding our customers’ expectations

Learning

Aspiration

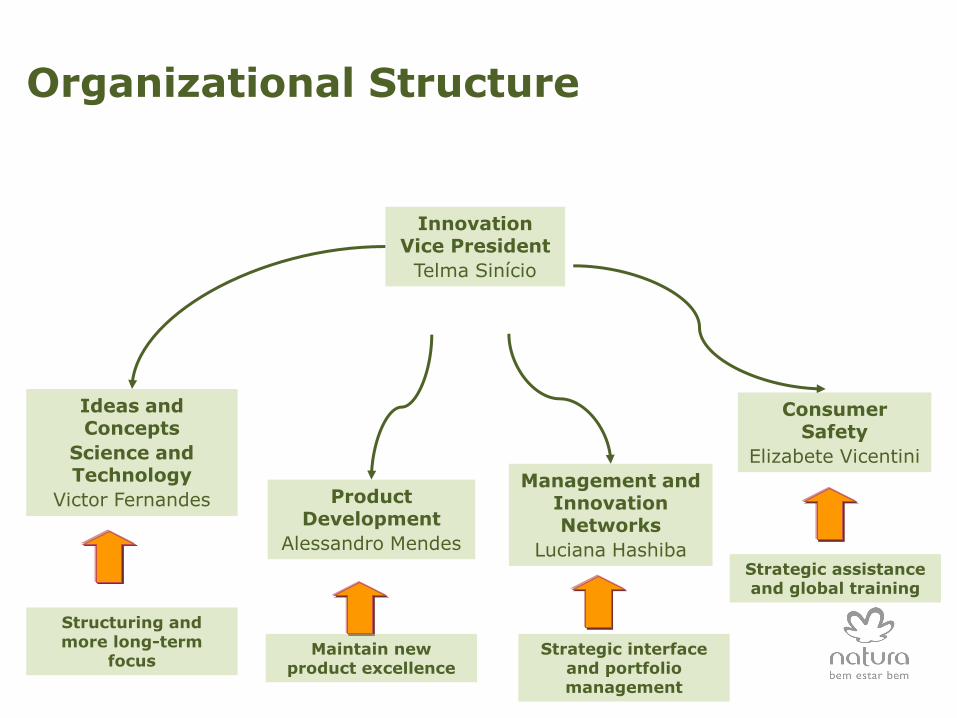

Organizational Structure

Ideas and Concepts

Science and Technology

Victor Fernandes

Consumer Safety

Elizabete Vicentini

Product Development

Alessandro Mendes

Management and Innovation Networks

Luciana Hashiba

Innovation Vice President

Telma Sinício

Structuring and more long-term

focus Maintain new

product excellence Strategic interface

and portfolio management

Strategic assistance and global training

Ideas and Concepts

_Flow that feeds all innovative processes

_Long term platform for conception of innovative ideas

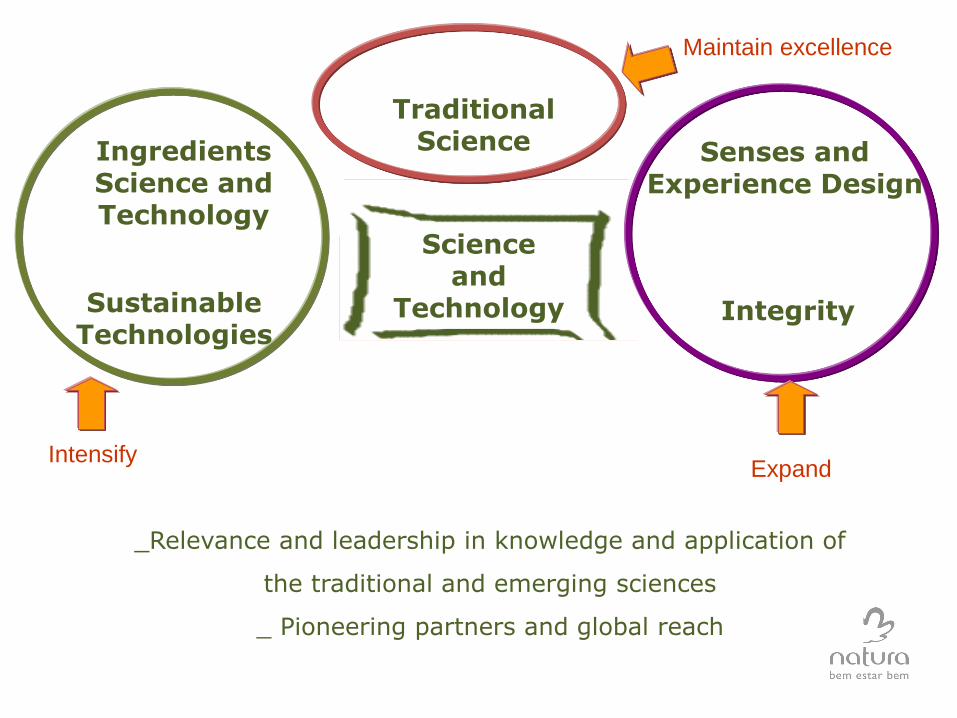

Science and

Technology Integrity

Senses and Experience Design

Traditional Science Ingredients

Science and Technology

Sustainable Technologies

_Relevance and leadership in knowledge and application of

the traditional and emerging sciences

_ Pioneering partners and global reach

Intensify

Maintain excellence

Expand

Ciência e Tecnologia

Senses and Experience Design

Ciência Clássica

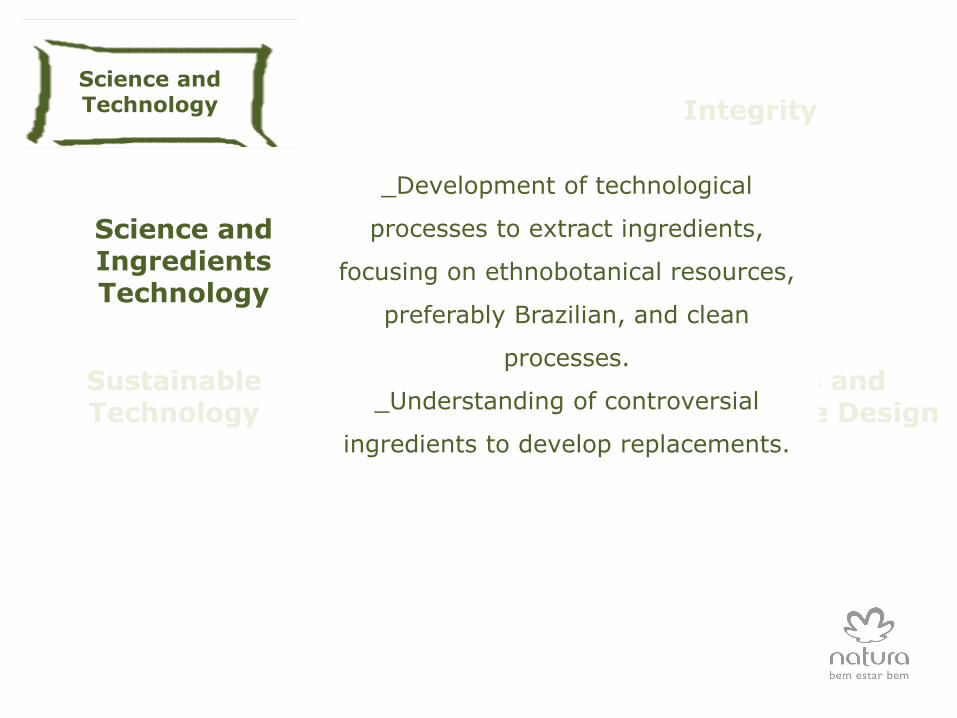

Science and Ingredients Technology

Sustainable Technology

_Development of technological

processes to extract ingredients,

focusing on ethnobotanical resources,

preferably Brazilian, and clean

processes.

_Understanding of controversial

ingredients to develop replacements.

Science and Technology Integrity

Ciência e Tecnologia

Integralidade

Sentidos e Design de

Experiências

Traditional Science

Science and Ingredients Technology

Sustainable Technologies

Science and Technology

_Relevance and leadership in traditional and emerging

sciences, with the capacity to choose the most

appropriate partners with international reach,

interaction models and pioneering partnerships

_Transformation social and environmental

challenges into business and product

opportunities, including the sustainable use of

natural resources, biodiversity, ecodesign and

environmental indicators.

_Development of packages, formats and

materials to bring new benefits to customers

with minimum environmental impact.

Integrity

Senses and Experience Design

Classical Science

Science and Ingredient Technology

Tecnologias Sustentáveis

__Relevance and leadership in traditional and

emerging sciences, with the capacity to choose the

most appropriate partners with international reach,

interaction models and pioneering partnerships

_Development of new ingredients from Brazilian ethnobotany to

create products with new and different benefits for skin, the

scalp and hair

_Development of the basic scientific, biological and physical-

chemical processes related to skin, scalp and hair, in line with

consumers’ cosmetic needs

_Non-invasive methods for treating human skin, scalp and hair

conditions

Science and Technology

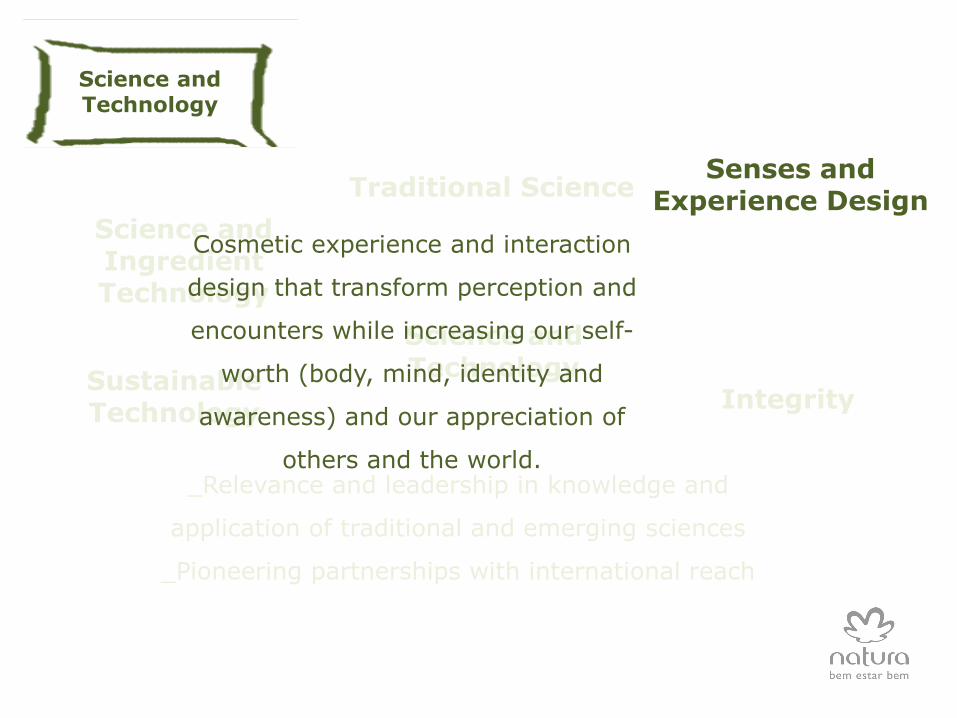

Science and Technology

Integrity

Senses and Experience Design

Traditional Science

Science and Ingredient Technology

Sustainable Technology

_Relevance and leadership in knowledge and

application of traditional and emerging sciences

_Pioneering partnerships with international reach

Cosmetic experience and interaction

design that transform perception and

encounters while increasing our self-

worth (body, mind, identity and

awareness) and our appreciation of

others and the world.

Science and Technology

Science and Technology

Science and Technology

Integrity

Senses and Experience Design

Traditional Science

Science and Ingredient Technology

Sustainable Technology

_Relevance and leadership in knowledge and

application of traditional and emerging sciences

_Pioneering partnerships with international reach

_Holistic understanding of well being and its

correlation to the physical, emotional,

cultural and social aspects.

Product Development

_Formula and packaging

_Raw materials

_Open Innovation for formulation and packaging

_Environmental impact

_Indicators management

Consumer Safety

_Ingredient safety

_Safety and effectiveness of products

_Integration and intelligence of product information and ingredients

_New testing methods

_Post-sales consumer safety

_Excellence in international legal and regulatory aspects

Management and Innovation

Network

_Innovation Networks expansion: ICTs and Companies

_Innovation Incentive Management

_Integrated Innovation Management – processes, strategies,

projects, portfolio, pipeline and knowledge

_Intellectual Property Management

_Innovation Communication

Innovative Processes

_Evolution of the ideas and concepts pipeline

_Optimization of the alignment between the technology pipeline and

business strategy

_Short-, medium-, and long-term idea, concept and product

development pipeline

_Portfolio management using world-class tools

end.thank you

João Paulo Ferreira VP Operatio e Logística

Strategy O&L

NATURA DAY 2010

João Paulo Ferreira VP, Operations & Logistics

our

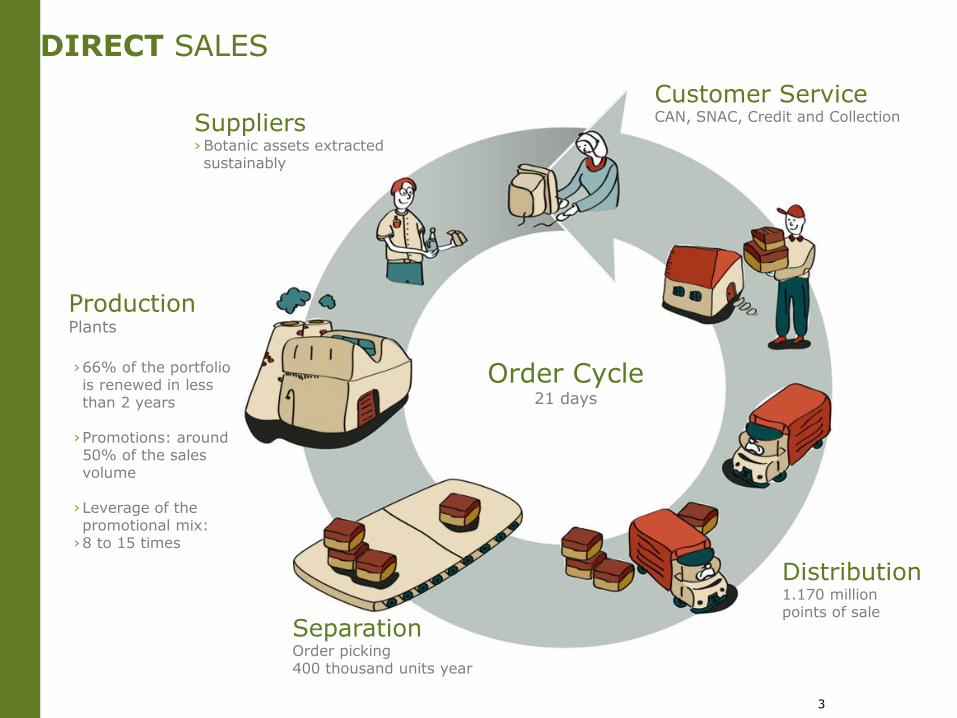

LOGISTIC NETWORK

2

Order Cycle 21 days

Distribution 1.170 million points of sale

Customer Service CAN, SNAC, Credit and Collection

Separation Order picking 400 thousand units year

Production Plants

DIRECT SALES

Suppliers › Botanic assets extracted sustainably

›66% of the portfolio is renewed in less than 2 years

›Promotions: around 50% of the sales volume

›Leverage of the promotional mix:

›8 to 15 times

3

our

SUPPLY CHAIN

4

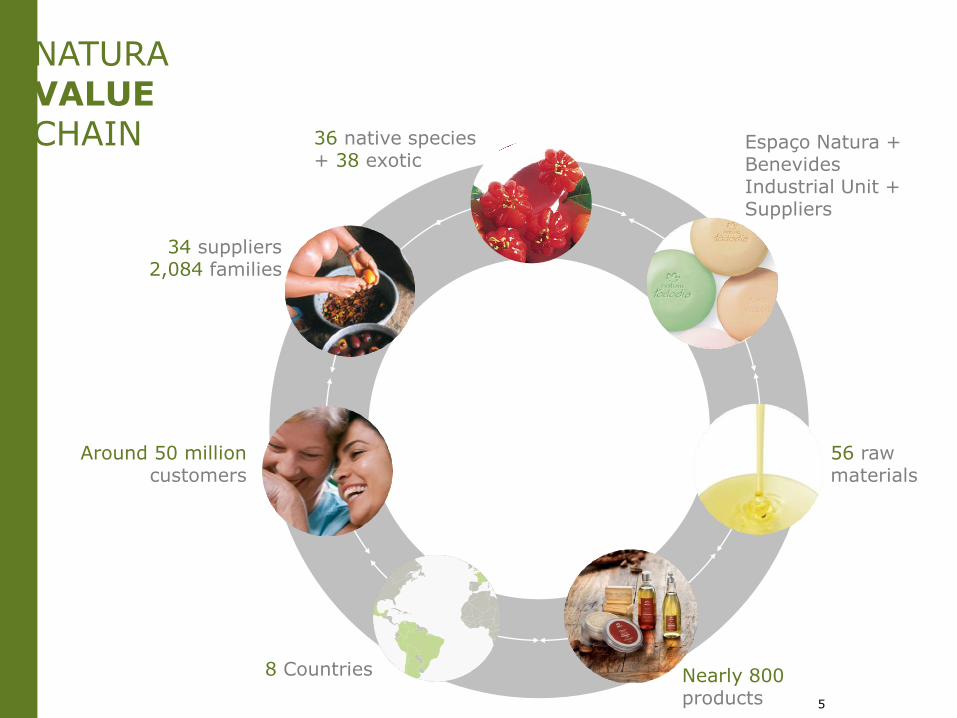

36 native species + 38 exotic

Nearly 800 products

Around 50 million customers

8 Countries

56 raw materials

34 suppliers 2,084 families

Espaço Natura + Benevides Industrial Unit + Suppliers

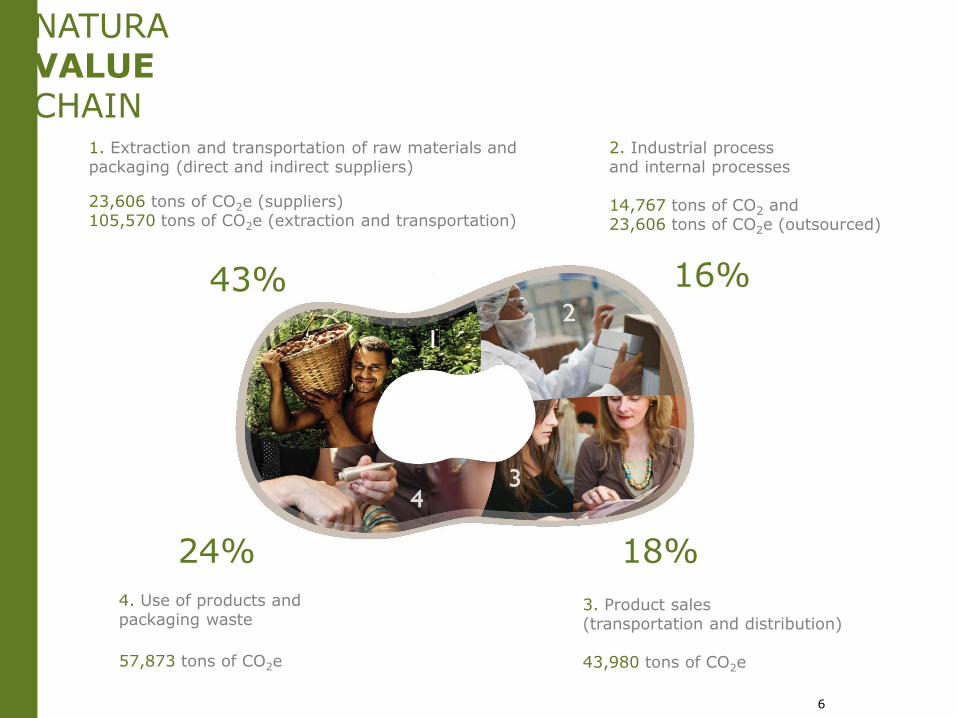

NATURA VALUE CHAIN

5

1. Extraction and transportation of raw materials and packaging (direct and indirect suppliers) 23,606 tons of CO2e (suppliers) 105,570 tons of CO2e (extraction and transportation)

43%

2. Industrial process and internal processes 14,767 tons of CO2 and 23,606 tons of CO2e (outsourced)

16%

4. Use of products and packaging waste

57,873 tons of CO2e

24%

3. Product sales (transportation and distribution) 43,980 tons of CO2e

18%

6

NATURA VALUE CHAIN

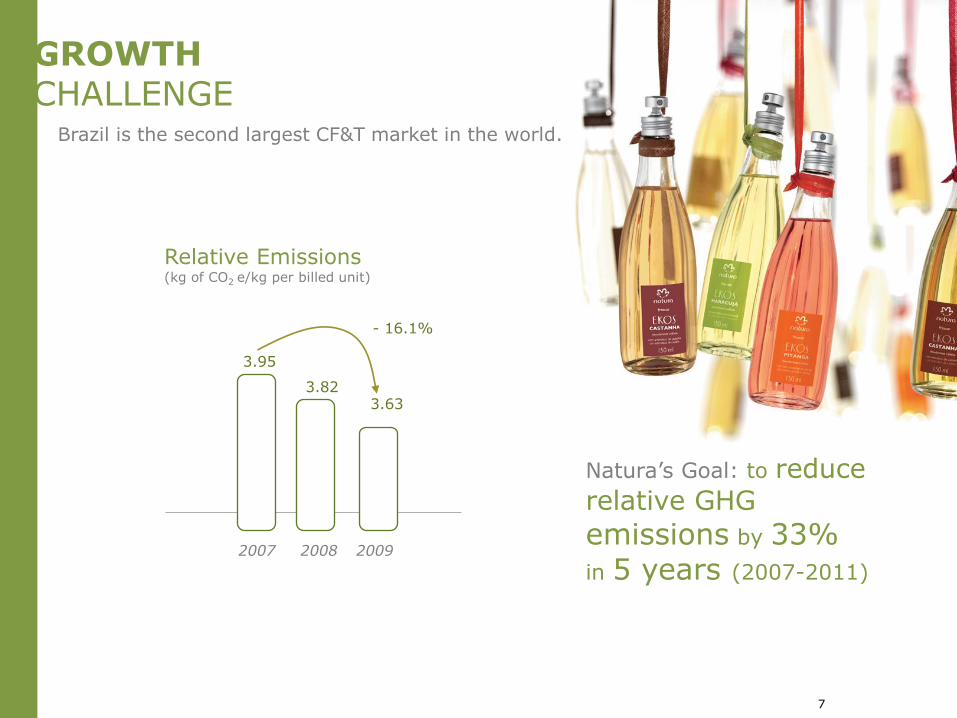

Brazil is the second largest CF&T market in the world.

Natura’s Goal: to reduce relative GHG

emissions by 33%

in 5 years (2007-2011)

GROWTH CHALLENGE

2007 2008 2009

- 16.1%

Relative Emissions (kg of CO2 e/kg per billed unit)

3.95

3.82 3.63

7

new

LOGISTICAL MODEL

8

Argentina

Brazil

Chile

Peru

Mexico

Colombia

France

DC

Production

› Plants: 4

› Hubs: 1

› Distribution Centers: 11

› Delivery Points: 1 million

› Billed units: 384 million

› Total km traveled per year: 1.6 million

› Total orders/year: 12.8 million

› SKUS: 1200

› Employees: 6260

› Raw material and packaging suppliers: 200

› Outsourced (co-producers): 20

*Data as of 2009 – source: Natura Annual Report

our CURRENT NETWORK

9

Production

International Production

Hubs

› Fábricas: 4

› Hubs: 6

› Centros de Distribuição: 14

› Terceiristas (co-makers): 24

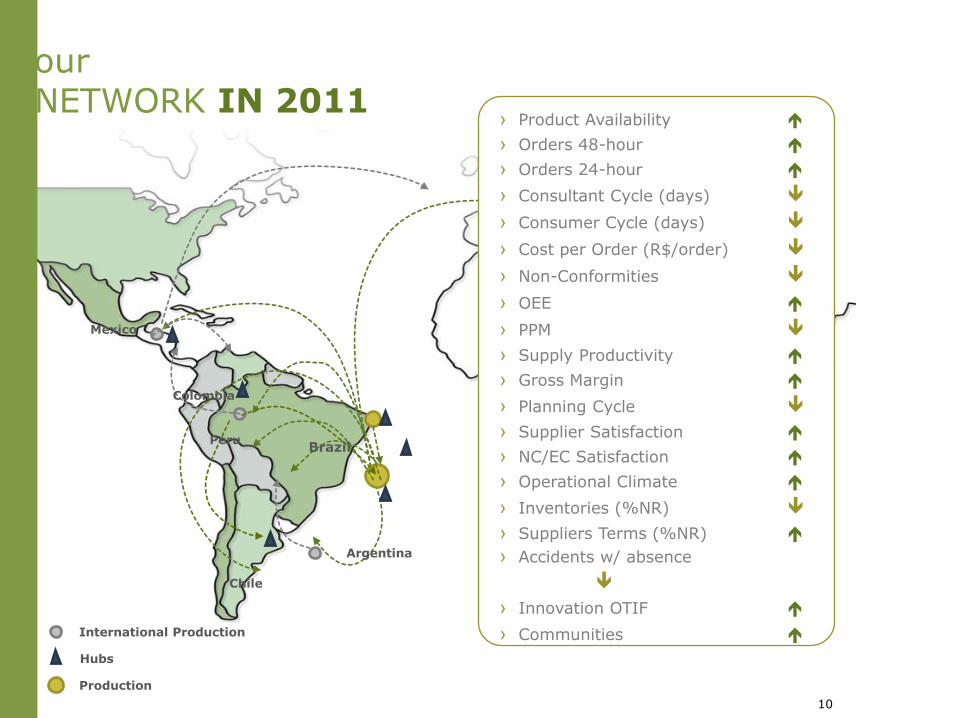

our NETWORK IN 2011

Argentina

Brazil

Chile

Peru

Mexico

Colombia

França

› Product Availability

› Orders 48-hour

› Orders 24-hour

› Consultant Cycle (days)

› Consumer Cycle (days)

› Cost per Order (R$/order)

› Non-Conformities

› OEE

› PPM

› Supply Productivity

› Gross Margin

› Planning Cycle

› Supplier Satisfaction

› NC/EC Satisfaction

› Operational Climate

› Inventories (%NR)

› Suppliers Terms (%NR)

› Accidents w/ absence

› Innovation OTIF

› Communities

10

Argentina

Brazil

Chile

Peru

Mexico

Colombia

França

› New service policy

› Revision of the global distribution network

› Order Tracking

› New customer/consultant service system

› Reconfiguration of production in Brazil

› International production

› Global Sourcing

› Operating and strategic integration with suppliers

› Risk Management

› Initial Control - agility and precision in innovation

› Elimination of losses and quality management (TPM/

6σ)

› Safety- management by behaviors

› Integrated and global network planning (DRP, MPS,

MRP)

› S&OP

11

Production

International Production

Hubs

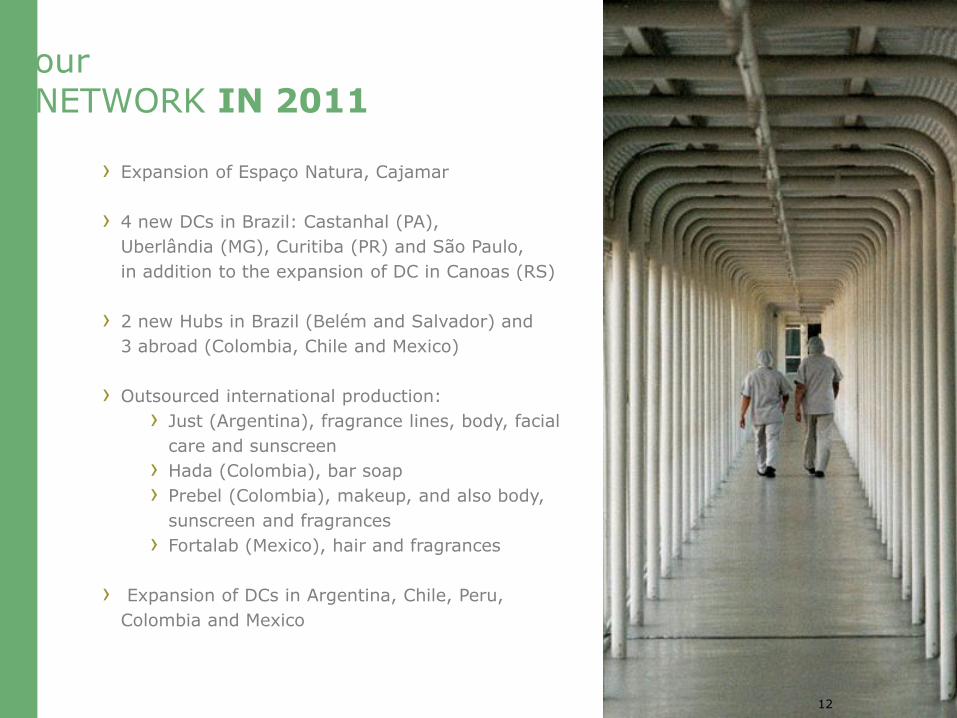

our NETWORK IN 2011

› Expansion of Espaço Natura, Cajamar

› 4 new DCs in Brazil: Castanhal (PA),

Uberlândia (MG), Curitiba (PR) and São Paulo,

in addition to the expansion of DC in Canoas (RS)

› 2 new Hubs in Brazil (Belém and Salvador) and

3 abroad (Colombia, Chile and Mexico)

› Outsourced international production:

› Just (Argentina), fragrance lines, body, facial

care and sunscreen

› Hada (Colombia), bar soap

› Prebel (Colombia), makeup, and also body,

sunscreen and fragrances

› Fortalab (Mexico), hair and fragrances

› Expansion of DCs in Argentina, Chile, Peru,

Colombia and Mexico

our NETWORK IN 2011

12

VISION FOR THE FUTURE

13

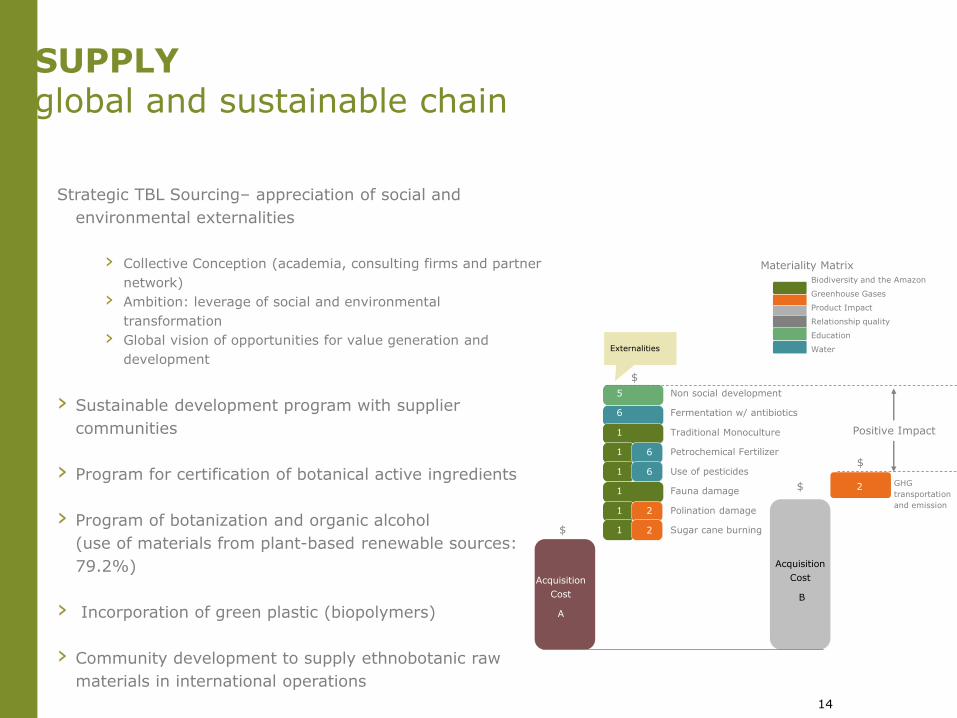

Strategic TBL Sourcing– appreciation of social and

environmental externalities

› Collective Conception (academia, consulting firms and partner

network)

› Ambition: leverage of social and environmental

transformation

› Global vision of opportunities for value generation and

development

› Sustainable development program with supplier

communities

› Program for certification of botanical active ingredients

› Program of botanization and organic alcohol

(use of materials from plant-based renewable sources:

79.2%)

› Incorporation of green plastic (biopolymers)

› Community development to supply ethnobotanic raw

materials in international operations

SUPPLY global and sustainable chain

Non social development

Fermentation w/ antibiotics

Traditional Monoculture

Petrochemical Fertilizer

Use of pesticides

Fauna damage

Polination damage

Sugar cane burning

Biodiversity and the Amazon

Greenhouse Gases

Product Impact

Relationship quality

Education

Water

5

6

1

1

1

1

1

1

6

6

2

2

2

Acquisition

Cost

A

Acquisition

Cost

B

Externalities

Positive Impact

GHG

transportation

and emission

$

$

$

$

Materiality Matrix

14

› Construction of an international network of

production partners aligned with the Triple Bottom

Line

› Eco-efficiency in internal processes

› New technologies for effluent treatment and

energy generation

PRODUCTION global and sustainable network

15

› Redesign of the global distribution network with CO2

optimization (25%) and improved service

› New order picking technologies to increase

productivity, reduce errors and promote social inclusion

› Secondary packaging optimization program

› Reverse Logistics: recycling program

› Order tracking through the end consumer

16

DISTRIBUTION

optimizing costs and

reducing GHG emissions

› Green S&OP

› Integration and colaboration through tier

2

› Global visibility in real time

› New IT tools, ex. GHG optimizer

› Integrated international work and

decision making processes

PLANNING global footprint

17

› Integration with suppliers: innovation, strategic and long-term relationships, social and environmental chains

› Entrepreneurialism together with the chain

› New distribution network: 25% decrease in CO2 emissions per order at the distribution

› Positive social impact considering social development indexes

› Increased response capacity: flexibility and reliability for the end consumer

› Improved service: broader availability and faster delivery

› Optimized working capital: integrated global planning

› Global presence: international production footprint, intensive use of partners, global supply management

› New TBL processes within Supply Chain Management

EXPECTED RESULTS

18

› Social and environmental guidelines as part of

the decision making processes and of Supply Chain modeling

› Value creation for the business as from a sustainable supply network

› Sustainability as a strength to redefine service and collaboration standards

› Dichotomy between global presence and relationship with local communities – cultural diversity

› Training and development of employees with TBL abilities

SUPPLY NETWORK global and sustainable

19

end.thank you

Marcelo Cardoso

Vice President, Organizational Development and Sustainability

Leadership, Culture and Management

NATURA DAY 2010

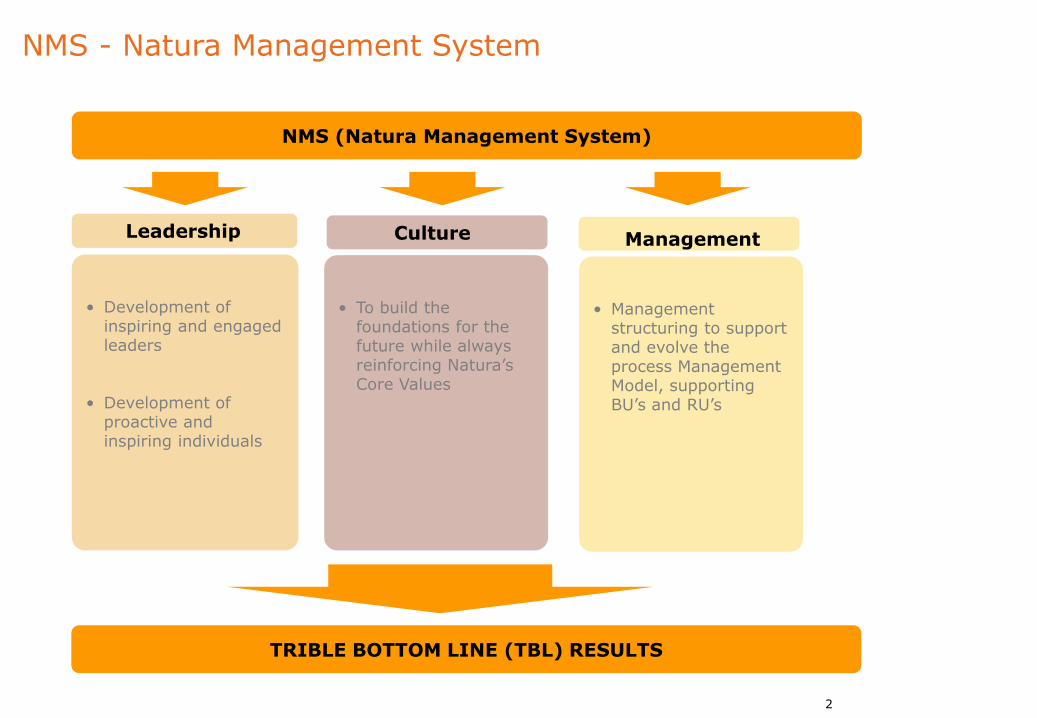

NMS - Natura Management System

• To build the foundations for the future while always reinforcing Natura’s Core Values

• Development of inspiring and engaged leaders

• Development of proactive and inspiring individuals

Leadership Culture

NMS (Natura Management System)

• Management structuring to support and evolve the process Management Model, supporting BU’s and RU’s

Management

TRIBLE BOTTOM LINE (TBL) RESULTS

2

NMS - Natura Management System

Building a System that expresses our Core Values

“Establish and institutionalize the Natura Management System, aligning strategy, process management, people development and culture building,

making it replicable in other business lines and operations.”

- Natura Management System

3

Leadership Development Strategic Priority

Inspiring and engaged leadership development

“Leaders engaged with Natura’s purpose, who share its

values and are exemplars of Natura’s desired behavior,

inspiring, mobilizing and improving our relationship network to seek individual and collective highlighted results and to act as real agents for social change.”

- Leadership is one of Natura’s strategic priorities

4

Inspiring leadership

• Agent of change in all aspects of his or her life

• Mobilizes people in favor of the common good

• Shares Natura’s beliefs and values

• Consonance between talk and action

• Builds quality relationships

• Innovation capacity

• Global perspective

• Constantly seeks high performance

Engaged Leadership

• Committed to Natura’s purpose based on personal projects

• Takes responsibility for decision-making

• Constantly seeks new challenges

• Trains his or her successors

• Delivers better triple bottom line results

• Seeks personal and professional growth

Well being Being well

Natura’s Leadership Development Program:

Leadership office (“Foco”) creation

Carry out the chain of succession for critical positions

Increase the number of leaders developed in-house

Inspiring and engaged leadership development

5

Leadership Development Strategic Priority

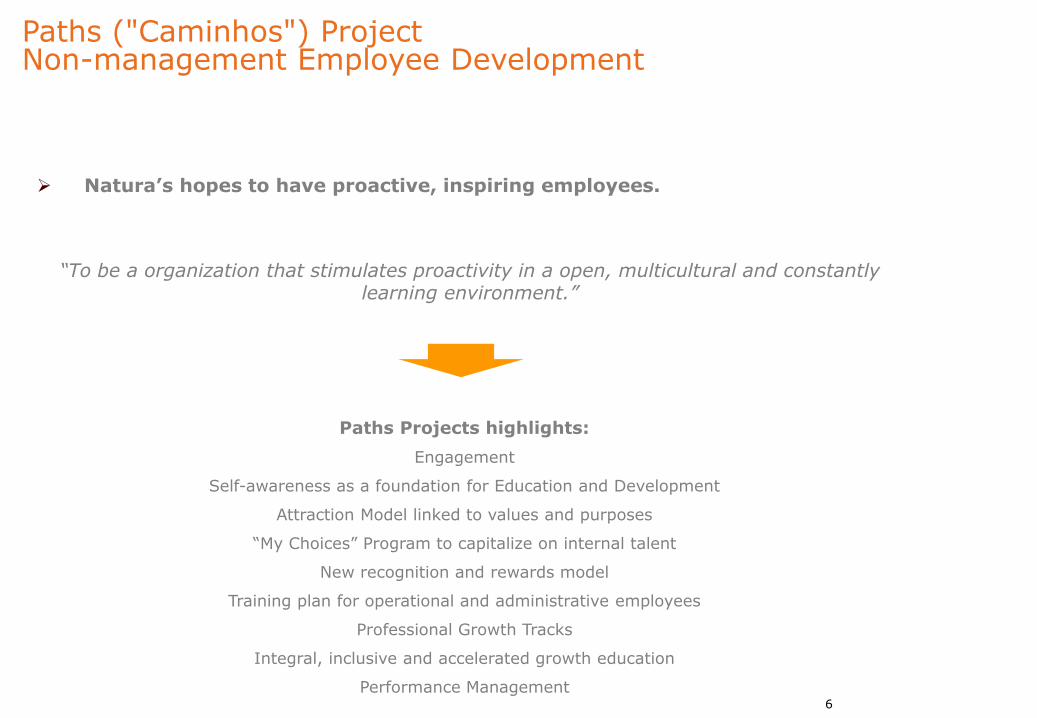

Paths ("Caminhos") Project Non-management Employee Development

“To be a organization that stimulates proactivity in a open, multicultural and constantly learning environment.”

Natura’s hopes to have proactive, inspiring employees.

Paths Projects highlights:

Engagement

Self-awareness as a foundation for Education and Development

Attraction Model linked to values and purposes

“My Choices” Program to capitalize on internal talent

New recognition and rewards model

Training plan for operational and administrative employees

Professional Growth Tracks

Integral, inclusive and accelerated growth education

Performance Management 6

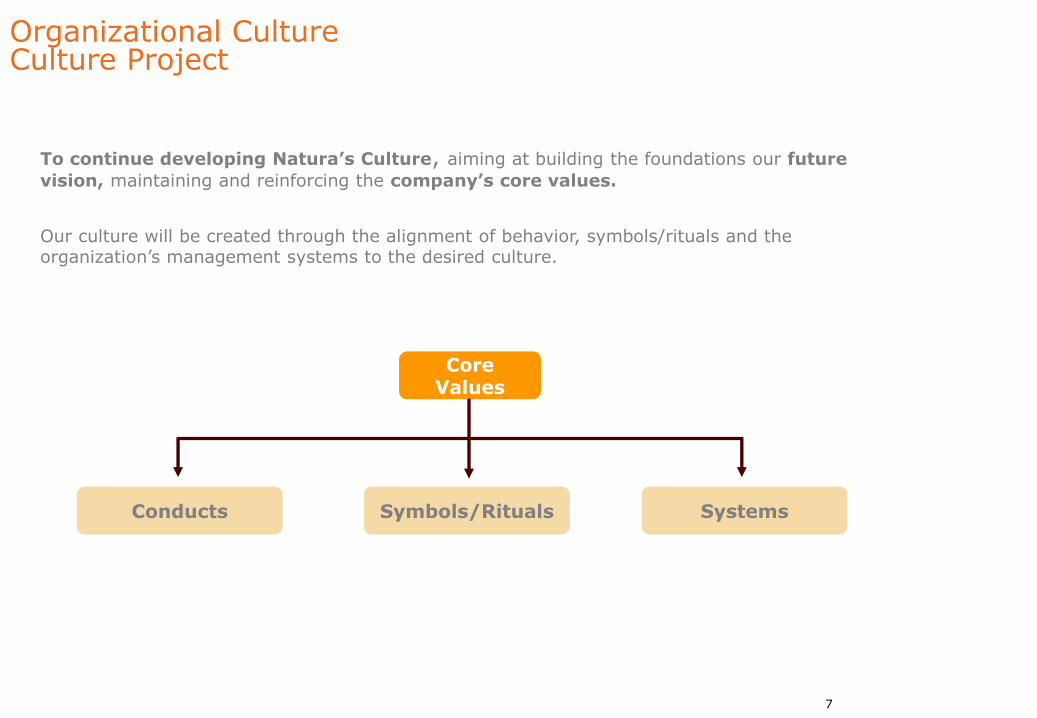

To continue developing Natura’s Culture, aiming at building the foundations our future

vision, maintaining and reinforcing the company’s core values.

Our culture will be created through the alignment of behavior, symbols/rituals and the organization’s management systems to the desired culture.

Organizational Culture Culture Project

Core Values

Conducts Symbols/Rituals Systems

7

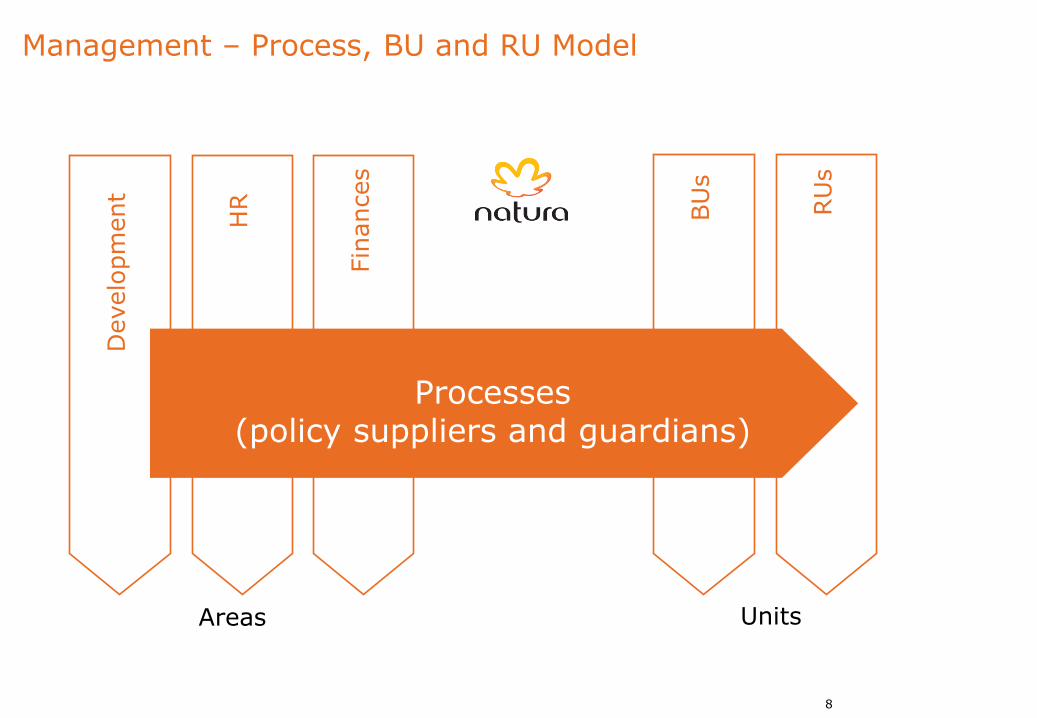

Management – Process, BU and RU Model

BU

s

RU

s

Areas

Develo

pm

ent

HR

Fin

ances

Units

Processes (policy suppliers and guardians)

8

9

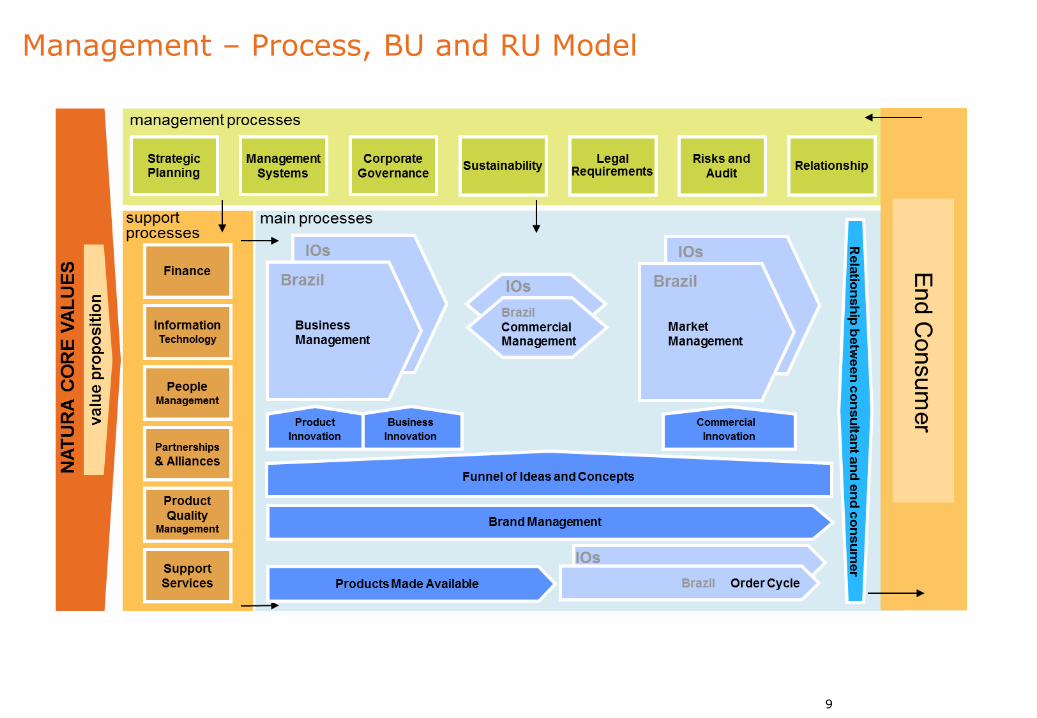

Management – Process, BU and RU Model

end.thank you