needles powers crosson financial and managerial accounting 10e uses of accounting information and...

TRANSCRIPT

NeedlesPowersCrosson

Financial and Managerial Accounting

10e

Uses of Accounting Information and the Financial Statements1

C H A P T E R

© human/iStockphoto©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Concepts Underlying Accounting Measurement

Accounting is an information system that measures, processes, and communicates financial information about a business or other economic entity.– An economic entity is a unit that exists independently,

such as a business, hospital, or governmental body.– Bookkeeping is the process of recording financial

transactions and keeping financial records. It is mechanical and repetitive and is usually handled by computers.

– Management information systems (MIS) consist of the interconnected business subsystems, including accounting, that provide the information needed to run a business.

– For accounting purposes, a business organization is a separate entity, distinct not only from its creditors and customers but also from its owners.

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Financial and Managerial Accounting

- External decision makers use financial accounting to evaluate how well a business has achieved its goals.

These reports, called financial statements, are a central feature of accounting. They report on a business’s financial performance.

- Internal decision makers use information provided by managerial accounting about operating, investing, and financing activities.

It provides managers and employees with information about how they have done in the past and what they can expect in the future.

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Accounting is usually divided into financial accounting and managerial accounting.

Business Transactions

Business transactions are economic events that affect a business’s financial position.

All business transactions are recorded in terms of money. This concept is called money measure.

In international transactions, exchange rates must be used to translate from one currency to another. An exchange rate is the value of one currency in terms of another.

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Forms of Business Organization

There are three basic forms of business organization that are recognized as separate entities.– Sole proprietorship—a business owned by 1

person The owner takes all the profits or losses of the

business and is liable for all its obligations.

– Partnership—a business that has 2 or more owners The partners share the profits or losses according to a

prearranged formula.

– Corporation—a business unit chartered by the state and legally separate from its owners The owners, called stockholders, have limited

liability—their risk of loss is limited to the amount they paid for their shares.

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Formation and Organization of a Corporation

To form a corporation, most states require incorporators to sign an application and file it with the proper state official.– This application contains the articles of

incorporation, which form the company charter.

– The authority to manage a corporation is delegated by its stockholders to a board of directors and by the board of directors to the corporation’s officers, as shown below.

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Stockholders

A unit of ownership in a corporation is called a share of stock.– The articles of incorporation state the maximum

number of shares that a corporation is authorized to issue.

– The number of shares held by stockholders is the outstanding stock.

– To invest in a corporation, a stockholder transfers cash or other resources to the corporation and receives shares of stock in return.

– Corporations may have more than one kind of stock, but here we refer only to common stock.

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Board of Directors

A corporation’s board of directors decides on major business policies, authorizes contracts, sets executive salaries, and arranges major loans with banks.– The oversight of a corporation’s management

and ethics by its board of directors is known as corporate governance. To strengthen corporate governance, the Sarbanes-

Oxley Act requires boards of directors to establish an audit committee made up of the independent directors (those directors who do not directly participate in managing the business) who have financial expertise.

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

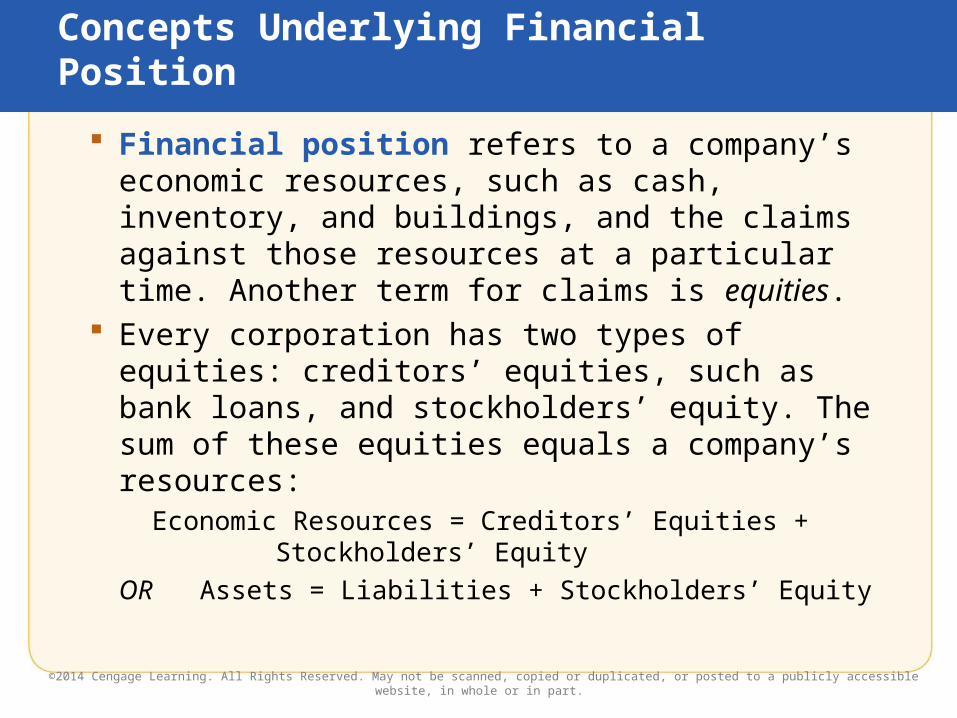

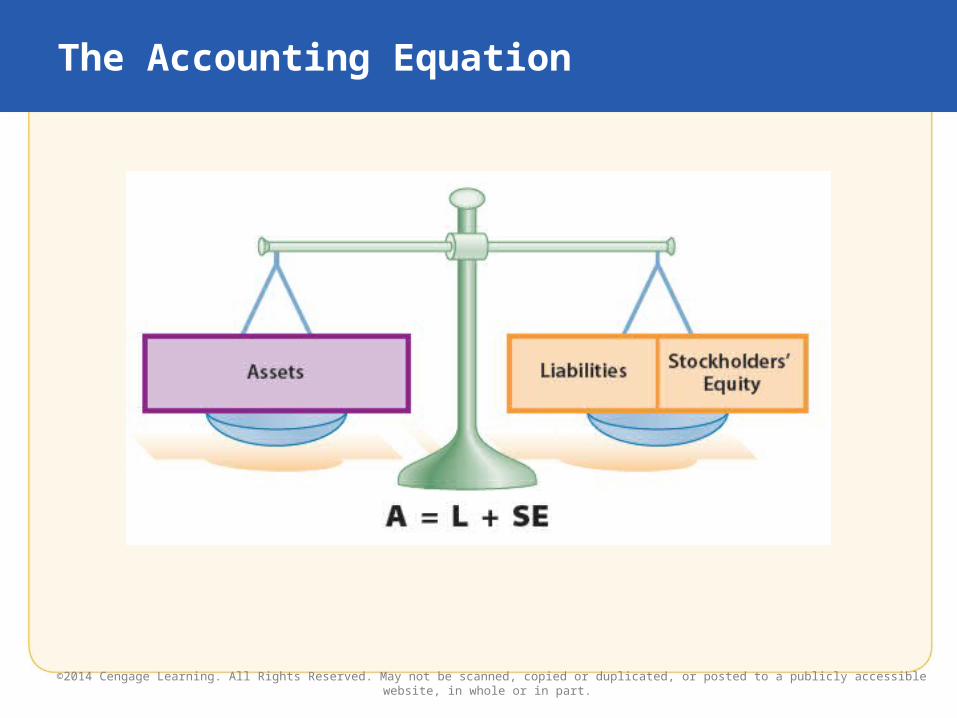

Concepts Underlying Financial Position

Financial position refers to a company’s economic resources, such as cash, inventory, and buildings, and the claims against those resources at a particular time. Another term for claims is equities.

Every corporation has two types of equities: creditors’ equities, such as bank loans, and stockholders’ equity. The sum of these equities equals a company’s resources:

Economic Resources = Creditors’ Equities + Stockholders’ Equity

OR Assets = Liabilities + Stockholders’ Equity

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

The Accounting Equation

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Assets

Assets are the economic resources that are expected to benefit the company’s future operations. They include:– monetary items (cash and money owed to

the company by customers)– nonmonetary, physical items (inventories,

land, buildings, equipment)– nonphysical items (rights granted by

patents, trademarks, and copyrights)

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Liabilities

Liabilities are a business’s present obligations to pay cash, transfer assets, or provide services to other entities in the future. They include:– amounts to suppliers for goods or services

bought on credit– borrowed money such as bank loans– salaries and wages owed to employees– taxes owed to the government– services to be performed

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Stockholders’ Equity(slide 1 of 3)

Stockholders’ equity represents the claims by the owners of a corporation (the stockholders) to the assets of the business.– Theoretically, stockholders’ equity is what

would be left if all liabilities were paid. – It is sometimes said to equal net assets.– We can define stockholders’ equity this

way: Stockholders’ Equity = Assets − Liabilities

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

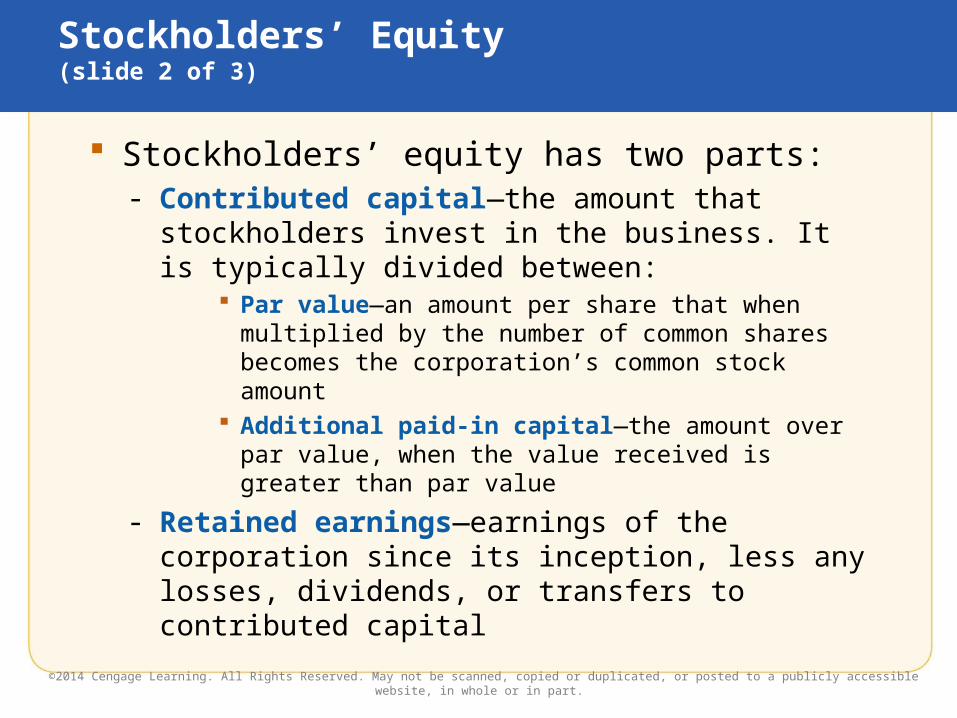

Stockholders’ Equity(slide 2 of 3)

Stockholders’ equity has two parts:- Contributed capital—the amount that

stockholders invest in the business. It is typically divided between:

Par value—an amount per share that when multiplied by the number of common shares becomes the corporation’s common stock amount

Additional paid-in capital—the amount over par value, when the value received is greater than par value

- Retained earnings—earnings of the corporation since its inception, less any losses, dividends, or transfers to contributed capital

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Stockholders’ Equity(slide 3 of 3)

Revenues and expenses are the increases and decreases in stockholders’ equity that result from operating a business.- When revenues exceed expenses, the difference

is called net income.- When expenses exceed revenues, the difference

is called net loss.- Retained earnings is the accumulated net

income minus dividends over the life of a business.

Dividends are distributions of resources, generally in the form of cash, to stockholders.

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Financial Statements

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Four major financial statements are used to communicate accounting information: the income statement, the statement of retained earnings, the balance sheet, and the statement of cash flows.

Income Statement

The income statement summarizes the revenues earned and expenses incurred by a business over an accounting period.

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Statement of Retained Earnings

The statement of retained earnings shows the changes in retained earnings over an accounting period.

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Balance Sheet

The purpose of a balance sheet is to show the financial position of a business on a certain date, usually the end of a month or year.

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Statement of Cash Flows

The statement of cash flows focuses on liquidity, that is, balancing the inflows and outflows of cash to enable the business to operate and pay its bills when they are due.– Cash flows are the inflows and outflows of

cash into and out of a business.– The statement of cash flows is organized

according to three major business activities: Cash flows from operating activities Cash flows from investing activities Cash flows from financing activities

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

GAAP and the Independent CPA’s Report

To ensure that financial statements are understandable to their users, a set of generally accepted accounting principles (GAAP) has been developed to provide guidelines for financial accounting.

Many companies of all sizes have their financial statements audited by an independent certified public accountant (CPA). – An audit is an examination of a company’s financial

statements and the accounting systems, controls, and records that produced them. It ascertains that the statements were prepared in accordance with GAAP.

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Organizations That IssueAccounting Standards

Two organizations issue accounting standards that are used in the United States:– The Financial Accounting Standards Board

(FASB) has been designated by the Securities and Exchange Commission (SEC) to issue Statements of Financial Accounting Standards.

– The International Accounting Standards Board (IASB) issues international financial reporting standards (IFRS). The SEC allows foreign companies to use these standards in the United States.

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Other Organizations That Influence GAAP

The Public Company Accounting Oversight Board (PCAOB) has wide powers to determine the standards that auditors must follow.

The American Institute of Certified Public Accountants (AICPA) is the primary professional organization of CPAs.

The Securities and Exchange Commission (SEC) is a governmental agency that has the legal power to set and enforce accounting practices for companies whose securities are offered for sale to the general public.

The Governmental Accounting Standards Board (GASB) issues accounting standards for state and local governments.

The Internal Revenue Service (IRS) interprets and enforces the tax laws that specify the rules for determining taxable income.

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Professional Conduct

The code of professional ethics of the American Institute of Certified Public Accountants governs the conduct of CPAs. The code requires CPAs to act with:– Integrity—be honest and candid and subordinate

personal gain to service and the public trust.– Objectivity—be impartial and intellectually honest.– Independence—avoid all relationships that impair

or appear to impair objectivity.– Due care—carry out professional responsibilities

with competence and diligence. The Institute of Management Accountants (IMA),

the primary professional association of managerial accountants, also has a code of professional conduct.

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Decision Makers: The Users of Accounting Information

The people who use accounting information to make decisions fall into three categories: managers (internal users), outsiders who have a direct financial interest in the business, and outsiders who have an indirect financial interest.

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Management, Investors, and Creditors

Management is responsible for ensuring that a company meets its goals of profitability and liquidity.

Investors—stockholders who have invested in a company—have a direct financial interest in the success of their companies.

Creditors—those who lend money or deliver goods or services before being paid—are interested mainly in whether a company will have the cash to pay interest charges and to repay the debt on time.

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Business Goals and Activities(slide 1 of 2)

A business is an economic unit that aims to sell goods and services at prices that will provide an adequate return to its owners.

The two major goals of all businesses are:– Profitability—the ability to earn enough

income to attract and hold investment capital– Liquidity—the ability to have enough cash to

pay debts when they are due

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Business Goals and Activities(slide 2 of 2)

All businesses pursue their goals by engaging in the following activities:– Operating activities—buying, producing, and

selling goods and services; hiring managers and other employees; paying taxes

– Investing activities—buying resources for operating the business, such as land, buildings, and equipment; selling those resources when no longer needed

– Financing activities—obtaining capital from creditors and from the company’s stockholders; repaying creditors; paying a return to stockholders

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Financial Analysis

Financial analysis is the use of financial statements to determine that a business is well managed and is achieving its goals.

The effectiveness of financial analysis depends on:– Performance measures: Profitability is

commonly measured in net income, and liquidity is commonly measured by cash flows.

– Financial ratios: The ratio of earnings to total assets can be used to assess profitability, and the ratio of cash flows to total assets can be used to assess liquidity.

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Ethical Financial Reporting

Ethics is a code of conduct that addresses the question of whether actions are right or wrong.– The intentional preparation of misleading

financial statements is called fraudulent reporting and can result from distortion of records, falsified transactions, and misapplication of various accounting principles.

– In response to the accounting scandals at Enron Corporation and WorldCom, the Sarbanes-Oxley Act of 2002 was passed. It regulates the financial reporting of public

companies and their auditors.

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.