neogen mich tech finish

TRANSCRIPT

1

Michigan Tech University Student Research

This report is published for educational purposes only by students competing in the CFA Institute Research

Neogen

Date: January 19, 2015 Ticker: NEOG Recommendation: Sell Exchange: Nasdaq Current Price: $48.16 Industry: Animal and Food Safety Target Price: $21.20 (Premium: -‐56%) Sector: Healthcare Figure 1: Forecast Summary

2012 2013 2014 2015F 2016F 2017F 2018F

Total Revenue $184,046 $207,528 $247,405 $280,418 $315,447 $352,745 $387,986

Gross Profit Margin 92,425 109,494 122,598 147,119 165,930 185,698 202,363

Net Income 22,389 27,041 28,031 35,961 40,959 45,907 49,506

Basic EPS 0.64 0.76 0.77 0.97 1.08 1.20 1.28

Gross Profit Margin 50% 53% 50% 52% 53% 53% 52%

Statistics as of Jan 19, 2015

Figure 2: Issue Data

Last Px 47.96

P/E ttm 57.29

P/B 5.42

P/S 6.7

Mkt Cap 1772.5M

Curr Ev 1678.2M

Cur EV/ T12M EBITDA

29

Source: Bloomberg

1

Summary

Neogen Corporation is a well-‐managed and financially sound corporation, which is heavily overvalued. Neogen’s current share price is not justified based on neither fundamental valuation nor relative valuation.

Fundamental valuation: Discounted cash flow valuation, employing reasonable growth rates and cost of equity, indicates a target price of $19.07 or a market cap of $710 million. At a current market cap of $1.77 billion, Neogen is significantly overvalued. Reasonable growth projections versus explosive: Neogen’s management expects industry sales to grow between 5% and 8% annually. Further, Neogen management predicts their firm’s organic sales growth to be between 8%-‐10% annually, with an additional 3%-‐5% sales growth through acquisitions. We believe these growth rates represent an upper bound. We believe the market is expecting explosive growth rates that are unlikely to be achieved without a major catalyst event (e.g., a terror attack via the food chain.) Relative valuation: Relative valuation, based on a variety of metrics and a richly-‐valued peer group, indicates a target price of $27.59 or a market cap of $1.01 billion. Again, Neogen is significantly overvalued.

2

2

Strong financial health and quality corporate management: With no long-‐term debt, positive cash flow to support acquisitions, and strong liquidity, Neogen is a financially healthy company. Additionally, Neogen has a business model that provides consistent revenue with established customer relationships. The management has been very tactful in their ability to integrate acquired businesses into their corporate framework.

Business Description Neogen Corporation develops, manufactures and markets a variety of products and services targeted for the food and animal safety markets worldwide. Products extend into acumedia, genomics, life sciences and toxicology. The company was founded in 1982 and has three main points of operation in Michigan, Kentucky, and Nebraska.

Reportable Segments Food Safety This segment represents 54% of the company’s revenues. Products within this space include diagnostic test kits and a variety of complementing products to identify potentially dangerous or undesired substances in both human and animal feed. Examples include pathogens, spoilage organisms, drug and pesticide residues, and general sanitation concerns. Animal Safety This segment represents 46% of the company’s revenues. Products include pharmaceuticals, rodenticides, disinfectants, vaccines, veterinary instruments, diagnostics products, and genetic testing. Company Strategy Neogen focuses on building trust with its distributors and customers, while continuously offering a wider range of products and improving its existing lines. While the company is committed to internal research and development, Neogen also expands its product offerings through serial acquisitions. Neogen’s 28 acquisitions since 2000 incorporate proven technologies into their global distribution network. Rather than acquiring major competitors, Neogen has had a track record of acquiring smaller companies, which provide growth opportunities via new product lines. These acquisitions create a level of synergy, yet can be assimilated into their corporate structure. Typically, Neogen pays 1.1x to 1.3x sales for its acquisitions.

CFA Research Institute Research Challenge January 19, 2015

Figure 3: Growth Potential

Dil EPS from Cont Op

1.7%

Cap – 1 yr Gr 18.6%

BVS – 1 yr Gr 16.5%

R&D to Sales 3.4%

Retention Ratio 100.0%

Rev – 1 yr Gr 19.2%

Empl 1yr Gr 18.6%

Assets – 1 yr Gr 18.8%

Source: Bloomberg

Figure 4: Profitability

EBITDA 52.6M

EBIT 43.4M

OPM 17.5%

Pretax Margin 17.4%

ROA 9.0%

ROE 10.1%

ROC N.A.

Asset Turnover 0.8

Source: Bloomberg

3

-‐30

-‐20

-‐10

0

10

20

-‐10 0 10

Residuals

SPX Index -‐ Percent

Figure 6: SPX Index-‐ Percent Residual Plot

Source: Bloomberg, Team Calculations

Alpha 1.304

Beta 1.001

R^2 0.205

Source: Bloomberg, Team Calculations

-‐20

-‐10

0

10

20

-‐20 0 20

% Change in s&

P 500

% Change in NEOG

Figure 5: Beta Calculation

3

It is important to note that while Neogen has been paying cash for these acquisitions, management is not opposed to larger acquisitions requiring debt financing. The major consideration would be Neogen’s ability to successfully incorporate the acquired company into its existing business framework and corporate culture.

Industry Overview and Competitive Positioning Industry Growth The primary markets demanding food and animal safety products are developed nations and supply chains serving middle and high income classes within developing nations. As reported in the 2013 annual report by Neogen, the global middle class is expected to grow from 1.8 billion to 4.9 billion by 2030. This growth in income will mean a continued expansion in the demand for animal and food safety products as this segment will demand higher quality food. With the highest potential for industry growth outside the United States, Neogen has been building its corporate footprint internationally. Indeed, management believes that 67% of future growth opportunities lie beyond the United States. However, the company has experienced its challenges gaining a foothold in international markets. Neogen is committed to being a forefront player, as the potential for new regulations and consumer demand in these regions provide a significant demand for food and animal safety products. Through strategic acquisitions, Neogen has been able to tap into new distribution networks bringing its range of products to China, Brazil, Latin America, Europe, and shortly India. Neogen currently sells products in 110 countries serving 123 distributors. As of 2014, international sales accounted for 38% of revenues for Neogen. Apart from an increased growth in the demand for quality food, the corporations in the supply chain have been shifting to a reduced number of suppliers. In response, Neogen has been offering a broader selection of product lines, thus providing a “one stop shop” for all food and animal safety needs. Indeed, Neogen has the largest selection of products within the industries it serves. Product Segments Food Safety: The food safety testing industry consists of both the process of testing and the subsequent required treatment to ensure the safety of food throughout the supply chain from production, processing, to end consumer. This market segment is expected to

CFA Research Institute Research Challenge January 19, 2015

4

CFA Research Institute Research Challenge January 19, 2015

4

grow to $15 billion by 2019. The largest market will remain to be North America followed by Europe. Asia-‐Pacific is expected to be the largest driver of growth in the industry. Animal Safety: Although there are many products sold by Neogen within the animal safety industry, the intervention products market provides Neogen with niche access to a $1+ billion addressable market of which they have a 12% share. This market is expected to grow at 5-‐7% moving forward. Competitors Charm Sciences is a privately held firm that is a world leader in food safety, water quality, and environmental diagnostic tests. The company segments its products based on target use. Charm Sciences uses the following categories for its products: dairy, food and grain, food and beverage, water, healthcare solutions, products and instruments. Charm Sciences prides itself on its quality of products, continuous innovation, excellent customer support, and scientific merit. Furthermore, Charm Sciences has a current customer base in more than 100 countries all over the world. Charm Sciences achieves its superiority through extensive and thorough research and development.

Idexx Laboratories is a publicly traded firm and poses the biggest competitive threat to Neogen due to its substantial relative size. Idexx Laboratories employs more than six times as many employees as Neogen, and has a market cap four and half times larger. Idexx Laboratories’ products are sold to customers in more than 175 countries around the world. Idexx Laboratories focuses its line of products around animal, milk, and water safety. Idexx Laboratories also markets products in communications, practice efficiency, diagnostics, information technology, and veterinary medicine. Idexx Laboratories also engages and expends many of their usable resources on research and development. Each of the aforementioned companies, Charm Sciences and Idexx Laboratories, pose significant competitive threats to Neogen, although in varying ways. Charms Sciences is much more closely related to Neogen in terms of offered products and the target customer base of these products. It poses the bigger threat in the product competition and having the most innovative, valued products. Idexx Laboratories, however, is the bigger threat in terms of sheer size. Theoretically, if desired and advantageous, Idexx Laboratories could further challenge

-‐20 -‐15 -‐10 -‐5 0 5 10 15 20 25

-‐10 -‐5 0 5 10

NEOG US Equity -‐ Percent

SPX Index -‐ Percent

NEOG US Equity -‐ Percent

Predicted NEOG US Equity -‐ Percent

Figure 7: SPX Index -‐ Percent Line Fit Plot

Source: Bloomberg, Team Calculations

Figure 8: Structure

Curr Ratio 7.6

Quick Ratio 5.1

Debt/Assets 0.0%

Debt/Com Eq 0.0%

A/R Turnover 5.4

Inv Turnover 2.7

GM 0.496

EBIT/Int Exp N.A.

Source: Bloomberg

5

Figure 10: Correlation of NEOG to S&P 500

Correlation: 2000-‐2015

S&P NEOG

S&P 1 0.350

NEOG 0.350 1

Correlation: 2010-‐2015

S&P NEOG

S&P 1 0.453

NEOG 0.453 1

Source: Bloomberg, Team Calculations

CFA Research Institute Research Challenge January 19, 2015

5

the specific product lines of Neogen even more so. All three companies spend a lot of their valuable resources on research and development.

Corporate Governance and Social Responsibility Neogen prides itself on being able to save thousands of people from becoming sick or potentially worse each day through the distribution of their products. As stated by Neogen’s founder, “we don’t make the food you eat, but we make it safer.” The company focuses on building a devoted workforce that is passionate about influencing positive change in the food and animal safety industry. The company stresses values like honesty, integrity, ethical responsibility, and respect. The social policies of Neogen are governed by the Corporate Governance Committee which provides oversight for management succession, human resources practices, risk management, and environment and health safety issues.

Investment Risks Government Standards Neogen’s product lines help businesses ensure they are meeting government standards for food and animal safety. With this said, Neogen benefits as governments increase standards within the industries served. Europe, Canada and the United States have some of the strictest standards for food and animal safety in the world which has allowed Neogen to prosper within their markets. A concern within these markets includes changes in requirements for approval to sell certain products, or existing regulations which would affect current product lines. As emerging markets increase safety standards Neogen will be in a prime position to capitalize. However, if emerging markets don’t enact increased standards Neogen could face significant challenges as they push to expand their global footprint. Quality and Litigation The manufacturing and distribution of Neogen’s products are subject to inherent risk of product liability claims. Although the company carries liability insurance, there is the potential that its insurance policies wouldn’t adequately cover potential claims against Neogen. Pricing and Competition The food and animal safety/diagnostics markets are extremely competitive. While there are a number of major competitors in the space, this market has a multitude of small “mom and pop”

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

$3.50

$4.00

NEOG SPX Index

Figure 9: Growth of $1 since January 2010

Source: Bloomberg, Team Calculations

6

6

competitors that are able to build market share for niche product lines. This creates a unique operating environment that requires upper management to be tactful in their strategic approach. Integration of Acquisitions Based on Neogen’s growth strategy, management must excel at evaluating and integrating acquisitions into the existing sales and distributions models. This process requires existing management to work closely with the acquired business units often pulling them from other duties. It is a significant challenge to retain and motivate quality management, who can successfully integrate acquisitions with Neogen.

Financial Analysis Earnings Historically, Neogen has been posting significant year over year gains across multiple revenue segments, partially driven by acquisitions. Both their food safety and animal safety segments have had continuous growth since 2012. For example, their acquisitions with SyrVet Inc. in July 2013 and Prima Tech Inc. in November 2013, which are both veterinary instrument companies. These acquisitions have helped increase revenue within their animal safety segment by 29%, especially the veterinary instruments and disposables segment by 70%. Cash & Cash Flows Based on forecasts, Neogen is expected to see increases in net changes in cash due to increases in cash from operating activities exceeding cash used in investing activities. This expansion of cash flow of Neogen will have spillover effects into the Balance Sheet strength.

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

FY 2010

FY 2011

FY 2012

FY 2013

FY 2014

FYE 2015

FYE 2016

FYE 2017

FYE 2018

Figure 13: Return on Assets

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

FY 2010

FY 2011

FY 2012

FY 2013

FY 2014

FYE 2015

FYE 2016

FYE 2017

FYE 2018

Figure 12: Return on Equity

CFA Research Institute Research Challenge January 19, 2015

Figure 11: FY 2012 Revenue by Segment

Natural Toxins, Allergens and Drug Residues

Bacterial and General Sanitajon

Dehydrated Culture Media and Other

Life Sciences

Veterinary Instruments and Disposables

Animal Care and Other

Rodenjcides, Insecjcides and Disinfectants

Source: Bloomberg, Team Eshmates

Source: Bloomberg, Team Estimates

Source: Bloomberg, Team Estimates

7

CFA Research Institute Research Challenge January 19, 2015

7

Balance Sheet Strength One of Neogen’s practices is to fund operations and acquisitions without the use of debt. As a result of their positive cash flows from operations, cash balances will be strong into the future, which provides Neogen with the opportunity to pay dividends, repurchase stock or expand their acquisition program.

Valuation Free Cash Valuation Overview We employed a three-‐stage free cash flow to equity valuation model. Revenues were modeled by individual sectors and then grouped into Neogen’s reporting segments (either product revenues or service revenues). Individual sector revenues were modeled based on the sector outlooks, while keeping historical revenue growth rates in mind. Given Neogen is a serial acquirer, the model incorporated additional revenues via acquisitions. The acquisition costs were treated as capital expenditures in the calculation of free cash flow and the effect of acquisitions were included in the perpetual growth rate. Free cash flows were calculated explicitly for the upcoming four periods. A transitional period was included, where growth was linearly adjusted downward to the terminal growth rate. Cost of equity was estimated using an adjusted beta and the CAPM model. Shares outstanding were grown based on the employee stock options currently held, assuming a 100% rate of exercise. The balance sheet and statement of cash flows reflect the exercise of these options. Relative Valuation Using a peer group of companies in the Diagnostics Testing industry, a relative valuation was conducted on the basis of the P/E, P/CF, P/B, and P/S ratios. As seen in Figure 14, Neogen’s value for each of these metrics exceeds the peer group median. Next, the median ratio from the peer group for each metric was used to imply a valuation for Neogen. As seen in Figure 14, Neogen had an implied price of $27.98, $25.09, $27.13, and $30.16, based on the P/E, P/CF, P/B, and P/S ratios, respectively. These implied prices are consistent in value. An average of the four implied valuations produced a target price of $27.59 for Neogen. This share price equates to a market cap of $1.01 billion compared to their current market cap of $1.77 billion.

$-‐ $20 $40

P/S

P/B

P/CF

P/E

Figure 14: NEOG Stock Implied Price

0 20 40 60

P/S

P/B

P/CF

P/E

Figure 15: Relahve Valuahon

Peer Group Median

NEOG US Equity

Source: Bloomberg, Team Estimates

Source: Bloomberg, Team Estimates

8

CFA Research Institute Research Challenge January 19, 2015

8

Inherently, what can be derived from the relative valuation method is that Neogen is richly valued relative to its peers. Furthermore, these peers appear to be overvalued, based on the same overconfidence in future growth rates and industry performance.

INVESTMENT SUMMARY Our final target price was computed using a weighted average of both our discounted cash flow fundamental valuation as well as our relative valuation analysis. Given the peer group used to conduct the relative valuation was richly valued, a weight of only 25% was applied to the relative valuation method and the remaining 75% was applied to the discounted cash flow valuation.

(25% x $27.59) + (75% x $19.07) = $21.20

In summary, Neogen is a financially stable firm with experience and proven management. However, the current market price exceeds a justifiable a level. Only a major catalyst event, such as a terror attack via the food chain, could support the current market price.

0

1

2

3

4

5

Threat of New Entrants

Bargaining Power of Suppliers

Bargaining Power of Customers

Compejjve Rivalry

Threat of Subsjtute

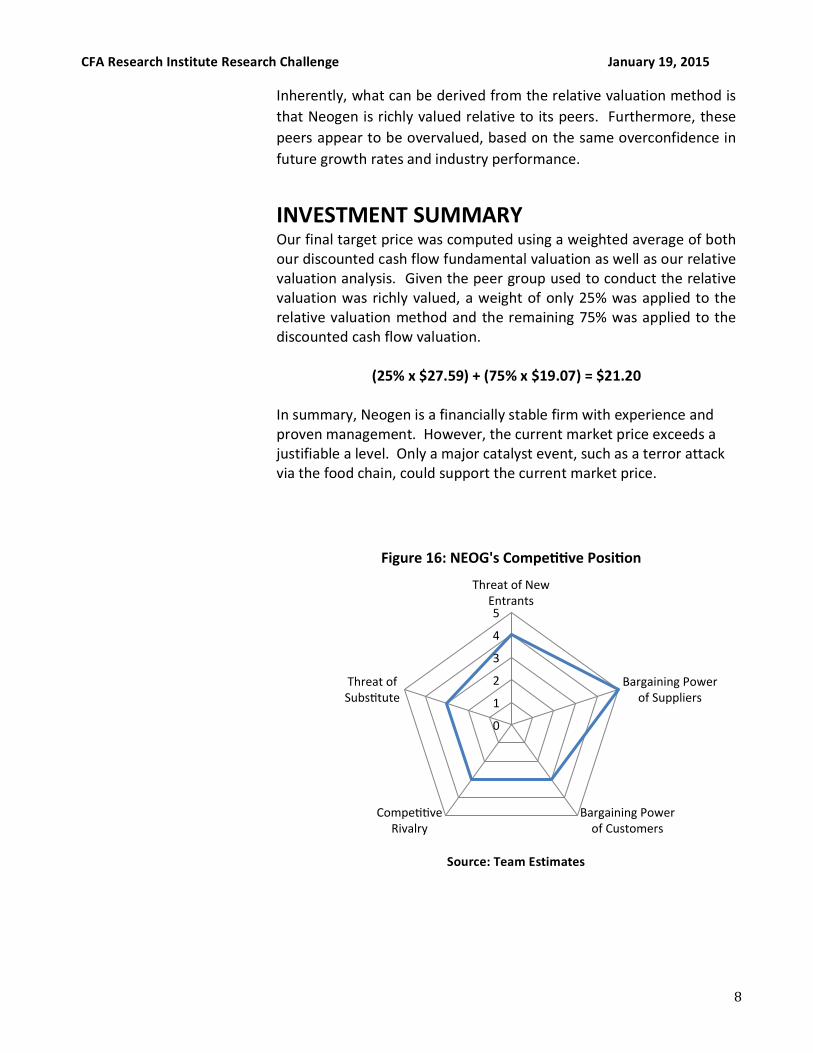

Figure 16: NEOG's Compehhve Posihon

Source: Team Estimates

9

CFA Research Institute Research Challenge January 19, 2015

Disclosures: Ownership and material conflicts of interest:

The author(s), or a member of their household, of this report does not hold a financial interest in the securities of this company.

The author(s), or a member of their household, of this report does not know of the existence of any conflicts of interest that might bias the content or publication of this report.

Receipt of compensation:

Compensation of the author(s) of this report is not based on investment banking revenue.

Position as a officer or director:

The author(s), or a member of their household, does not serves as an officer, director or advisory board member of the subject company.

Market making:

The author(s) does not act as a market maker in the subject company’s securities.

Ratings guide: Banks rate companies as either a BUY, HOLD or SELL. A BUY rating is given when the security is expected to deliver absolute returns of 15% or greater over the next twelve month period, and recommends that investors take a position above the security’s weight in the S&P 500, or any other relevant index. A SELL rating is given when the security is expected to deliver negative returns over the next twelve months, while a HOLD rating implies flat returns over the next twelve months.

Disclaimer:

The information set forth herein has been obtained or derived from sources generally available to the public and believed by the author(s) to be reliable, but the author(s) does not make any representation or warranty, express or implied, as to its accuracy or completeness. The information is not intended to be used as the basis of any investment decisions by any person or entity. This information does not constitute investment advice, nor is it an offer or a solicitation of an offer to buy or sell any security. This report should not be considered to be a recommendation by any individual affiliated with Michigan Technological University. CFA Institute or the CFA Institute Research Challenge with regard to this company’s stock.