nepal macroeconomic update, august 2015

DESCRIPTION

Nepal Macroeconomic Update, August 2015, Vol.3, No.2TRANSCRIPT

2015-09-03 1

Nepal Macroeconomic Update August 2015, Vol.3, No.2

Chandan Sapkota

Asian Development Bank

Nepal Resident Mission

Press briefing at Nepal Resident Mission, 03 September 2015

2015-09-03 2

The views expressed in this document are those of the author and do not necessarily reflect the views and policies of the Asian Development Bank, or its Board of Governors, or the governments they represent.

2015-09-03 3

Presentation Outline

1. Macroeconomic overview

2. Performance in FY2015

Real sector

Fiscal sector

Monetary sector

External sector

3. FY2016 growth outlook

4. FY2016 inflation outlook

5. Fiscal sustainability and reconstruction

• The April 25 Gorkha earthquake and subsequent aftershocks affected

GDP growth & per capita income

Absolute poverty level

Progress on achieving some of the MDGs

Expenditure performance

Revenue mobilization

Financial sector

Migration & remittance inflows

Exports

Imports

Balance of payments

2015-09-03 4

Macroeconomic overview

2015-09-03 5

Real Sector

2015-09-03 6

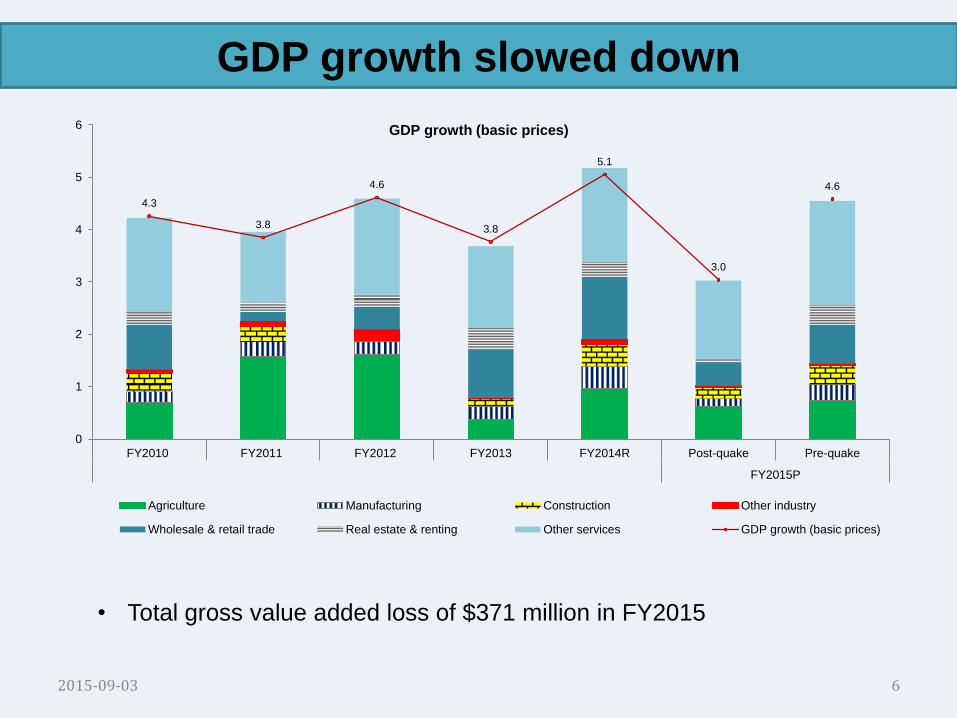

GDP growth slowed down

4.3

3.8

4.6

3.8

5.1

3.0

4.6

0

1

2

3

4

5

6

FY2010 FY2011 FY2012 FY2013 FY2014R Post-quake Pre-quake

FY2015P

GDP growth (basic prices)

Agriculture Manufacturing Construction Other industry

Wholesale & retail trade Real estate & renting Other services GDP growth (basic prices)

• Total gross value added loss of $371 million in FY2015

2015-09-03 7

Services sector was hit the hardest

• 62% of total gross value added loss accounted for by services sector

-1 1 3 5 7 9 11

Health & social work

Fishing

Public administration & defence

Community, social & personal services

Transport, storage & communications

Education

Hotels & restaurants

Construction

Wholesale & retail trade

Manufacturing

Agriculture & forestry

Financial intermediation

Electricty, gas & water

Mining & quarrying

Real estate, renting & business activities

Sub-sectoral growth in FY2015

FY2015 post-quake growth

Decline in growth due to the Aprilearthquake

2015-09-03 8

Domestic investment commitment went down

Commitment (% of GDP): • FY2015: 6.3% of GDP

• FY2014: 14.9% of GDP

0

10

20

30

40

50

60

70

80

FY2010 FY2011 FY2012 FY2013 FY2014 FY2015

FDI commitment & actual inflows (NRS billion)

Energy Service

Manufacturing Tourism

Agriculture Mineral

Construction Total FDI commitment

Actual FDI inflows

27 39

90 84

120

289

133

0

50

100

150

200

250

300

350

FY2009 FY2010 FY2011 FY2012 FY2013 FY2014 FY2015

Domestic Investment commitment (NRs billion)

Energy Manufacturing Service

Tourism Agriculture Mineral

Construction Total

• Commitment in FY2015: 3.2% of GDP

• Actual inflows in FY2015: 0.21 % of GDP

2015-09-03 9

Fiscal Sector

2015-09-03 10

Public expenditure performance remained sluggish

• Actual capital spending was about 70% of planned capital spending

0

20

40

60

80

100

120 Expenditure growth

Recurrent Capital Total expenditure

71.8 71.6 70.8

82.6

78.4

69.9

0

20

40

60

80

100

120

FY2009 FY2010 FY2012 FY2013 FY2014 FY2015R

Absorption capacity

Recurrent (% of allocation) Capex (% of allocation)

2015-09-03 11

Capital spending is too slow and too low

0.0 1.0 2.0 3.0 4.0

Civil works

Building

Research andconsultancy

Capitalcontingencies

Plant andmachinery

Land

Vehicles

Furniture andfittings

Capital budget (% of GDP)

FY2014

FY2015R

15.4 15.9

14.6 15.6 15.9

20.0

3.5 3.4 3.2 3.4 3.8

8.6

0

5

10

15

20

25

30Public expenditure (% of GDP)

Total Recurrent Capital

2015-09-03 12

High bunching of spending

• One-fourth of total spending done in last month; 45% in last three months

• 44% of actual capex in the last month; 63% in last three months

0

20

40

60

80

100

120

140

Aug-14 Sep Oct Nov Dec Jan-14 Feb Mar Apr May Jun Jul-15

SAARC Summitpreparation/Dashain/Tihar

SAARCSummit

Normal budget execution Post April 25 earthquake

Recurrent Capital Financing Total expenditure

2015-09-03 13

Revenue mobilization slowed, but remains robust

9.8 10.5 11.9

13.4 13.0 13.9

15.3 16.1 16.8

2.1 1.8

2.1

1.5 1.5

2.1

2.2

2.3 2.3

0

5

10

15

20

25 Tax and nontax revenue (% of GDP)

Tax revenue Non-tax revenue

0

10

20

30

40

50

Valueadded tax

Income tax Customs Excise Landregistration

fee

Vechile tax Educationalservice tax

Revenue growth

FY2014R FY2015P

2015-09-03 14

Primary surplus and a marginal fiscal deficit

-5

0

5

10

15

20

25

FY'2009 FY'2010 FY'2011 FY'2012 FY'2013 FY2014 FY2015R

Fiscal indicators (% of GDP)

Domestic revenue Grants Recurrent expenditure

Capital expenditure Fiscal balance

-3

-2

-1

0

1

2

3

FY2010 FY2011 FY2012 FY2013 FY2014 FY2015R

Primary and fiscal balance (% of GDP)

Primary balance Fiscal balance

2015-09-03 15

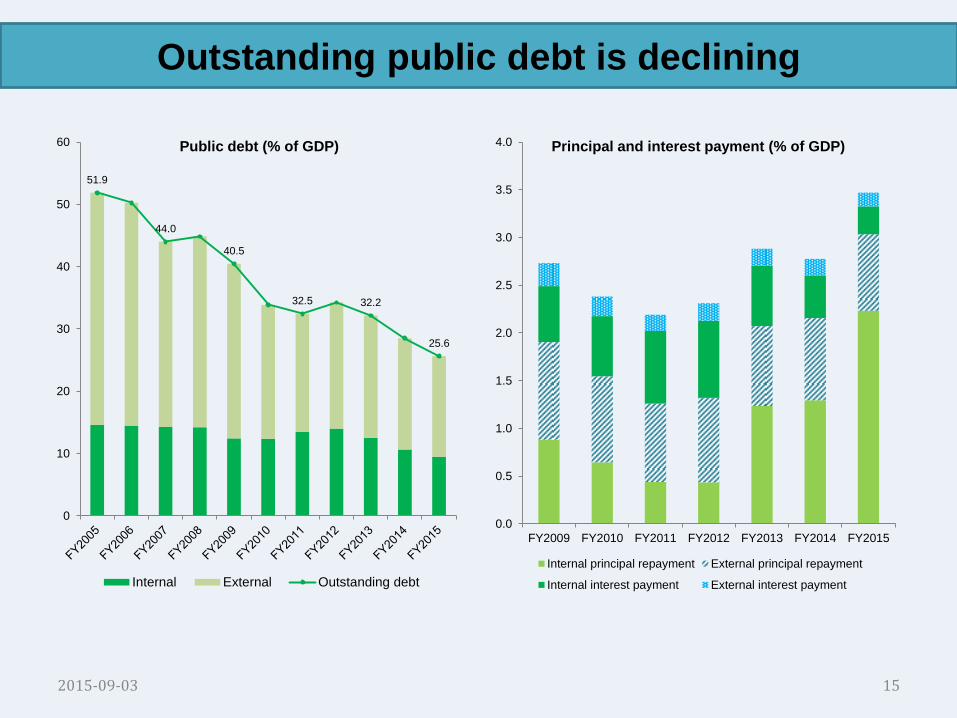

Outstanding public debt is declining

51.9

44.0

40.5

32.5 32.2

25.6

0

10

20

30

40

50

60 Public debt (% of GDP)

Internal External Outstanding debt

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

FY2009 FY2010 FY2011 FY2012 FY2013 FY2014 FY2015

Principal and interest payment (% of GDP)

Internal principal repayment External principal repayment

Internal interest payment External interest payment

2015-09-03 16

Monetary Sector

2015-09-03 17

Inflation moderated to 7.2%

0

2

4

6

8

10

12

14

16

Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul

Food inflation

FY2013 FY2014 FY2015

0

2

4

6

8

10

12

14

Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul

Non-food inflation

FY2013 FY2014 FY2015

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul

Overall inflation

FY2013 FY2014 FY2015

Inflation (Y-o-Y)

Year Average Food Non-food

FY2010 9.6 15.1 4.9

FY2011 9.6 14.6 5.3

FY2012 8.3 7.7 9.0

FY2013 9.9 9.7 10.1

FY2014 9.1 11.6 6.8

FY2015 7.2 9.6 5.2

2015-09-03 18

Money supply and deposit growth up

-20

-15

-10

-5

0

5

10

15

20

25

30

M2 Net foreignassets

Net domesticassets

Credit toprivate sector

Net claims onGovernment

Monetary sector (% change)

FY2013 FY2014 FY2015

-15

-10

-5

0

5

10

15

20

25

30

35

40

FY2011 FY2012 FY2013 FY2014 FY2015

Growth rate of deposit

Commerical banks Development banks

Finance companies Total deposit

2015-09-03 19

Credit growth picked up (mostly to services sector)

-15

-10

-5

0

5

10

15

20

25

30

FY2011 FY2012 FY2013 FY2014 FY2015

Growth rate of credit

Commerical banks Development banks

Finance companies Total credit-15

-10

-5

0

5

10

15

20

25

30

35

40

FY2007FY2008FY2009FY2010FY2011FY2012FY2013FY2014FY2015

Annual change in credit (NRs billion)

Construction Real estate

2015-09-03 20

Low short-term interest rates & stable policy rates

0.00

0.50

1.00

1.50

2.00

2.50

Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul

Interbank rate 91-day treasury bills rate

FY2014 FY2015

Interbank rate 91-day treasury bills rate

0

2

4

6

8

10

Jun

-13

Jul

Au

g

Se

p

Oct

Nov

Dec

Jan

-14

Fe

b

Ma

r

Ap

r

Ma

y

Jun

Jul

Au

g

Se

p

Oct

Nov

Dec

Jan

-15

Fe

b

Ma

r

Ap

r

Ma

y

Jun

Jul

Policy rates (%)

CRR-Commerical banksCRR-Development banksCRR-Finance companiesBank rate and Standing Liquidity Facility rate

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

0

2

4

6

8

10

12

14

Au

g-1

1

No

v

Fe

b

Ma

y

Au

g-1

2

No

v

Fe

b

Ma

y

Au

g-1

3

No

v

Fe

b

Ma

y

Au

g-1

4

No

v

Fe

b

Ma

y

NP

L (

Non

pe

rfo

rmin

g lo

an

/To

tal

loa

n)

CA

R (

To

tal ca

pita

l fu

nd

/ T

ota

l ri

sk

we

igh

ted

exp

osu

res)

CAR and NPL

Capital adequacy ratio Min CAR + buffer

Non-performing loan

2015-09-03 21

Stock market volatility persists

10.3

22.0

77.3

65.3

0

10

20

30

40

50

60

70

80

90

FY2012 FY2013 FY2014 FY2015

Turnover (NRs billion)

Trading

Preferred Stock

Manufacturing &Processing

Mutual Fund

Others

Hotel

FinanceCompanies

Promoter Share

DevelopmentBanks

Hydropower

InsuranceCompanies

Commercial Banks

Total

0

200

400

600

800

1000

1200

FY2011 FY2012 FY2013 FY2014 FY2015

Stock market performance

Market capitalization (NRs billion)

Number of listed companies

NEPSE index (closing)

2015-09-03 22

External Sector

2015-09-03 23

Trade deficit marginally up: Growth of imports > exports

Share of GDP FY2013 FY2014 FY2015

TOTAL EXPORTS 4.5 4.7 4.0

To India 3.0 3.1 2.6

To China 0.1 0.1 0.1

To Other Countries 1.4 1.5 1.3

TOTAL IMPORTS 32.8 36.8 36.5

From India 21.7 24.6 23.1

From China 3.7 3.8 4.7

From Other Countries 7.5 8.4 8.6

TOTAL TRADE BALANCE -28.3 -32.1 -32.4

With India -18.6 -21.5 -20.5

With China -3.6 -3.6 -4.6

With Other Countries -6.1 -6.9 -7.3

2015-09-03 24

Overseas migration slowed down, but remittance accelerated

294,094

354,716

384,665

453,543

527,814 512,887

0

100,000

200,000

300,000

400,000

500,000

600,000

FY2010 FY2011 FY2012 FY2013 FY2014 FY2015

Migrants & destination Malaysia

Qatar

SaudiArabia

UAE

Others

Kuwait

SouthKorea

Bahrain

Oman

Japan

Afghanistan

Lebanon

Israel

Total

0

5

10

15

20

25

30

35

0

100,000

200,000

300,000

400,000

500,000

600,000

Work

ers

' rem

itta

nces (

% o

f G

DP

)

Num

ber

of

overs

eas m

igra

nt w

ork

ers

Migration & remittances

Overseas migrant workers

Workers' remittances (% of GDP)

• Remittance inflows reached a record 29.1% of GDP in FY2015

2015-09-03 25

High remittance inflows buoyed external stability

• CAB: 5.1% of GDP and BOP 6.8% of GDP

• Gross forex: $8.3 billion (import cover of 11.2 months)

-40

-30

-20

-10

0

10

20

30

40

50

FY2010 FY2011 FY2012 FY2013 FY2014 FY2015

Balance of payments (% of GDP)

Export (fob) Oil import Non-oil import (cif)

Net services balance Net income balance Grants

Workers remittances Net transfers excl grants & remittances Capital account

Financial account Current account balance Balance of payments

2015-09-03 26

Exchange rate remains weak

• Depreciation of Nepalese rupee 15 July 2011-15 July 2012: 19.9%

15 July 2012- 15 July 2013: 6.7%

15 July 2013- 15 July 2014: 0.9%

15 July 2014- 15 July 2015: 5.4%

70.2

108.4

106.4

60

65

70

75

80

85

90

95

100

105

110

1-J

an-1

14

-Feb

-11

10-M

ar-…

13

-Ap

r-1

117-M

ay-…

20

-Ju

n-1

12

4-J

ul-

11

27-Aug-…

30

-Sep

-11

3-N

ov

-11

7-D

ec-1

11

0-J

an-1

21

3-F

eb-1

218-M

ar-…

21

-Ap

r-1

225-M

ay-…

28

-Ju

n-1

21

-Au

g-1

24

-Sep

-12

8-O

ct-1

211-Nov-…

15

-Dec

-12

18

-Jan

-13

21

-Feb

-13

27-M

ar-…

30

-Ap

r-1

33

-Ju

n-1

37

-Ju

l-1

39

-Au

g-1

31

2-S

ep-1

31

6-O

ct-1

319-Nov-…

23

-Dec

-13

26

-Jan

-14

1-M

ar-1

44

-Ap

r-1

48

-May

-14

11

-Ju

n-1

41

5-J

ul-

14

18-Aug-…

21

-Sep

-14

25

-Oct

-14

28-Nov-…

1-J

an-1

54

-Feb

-15

10-M

ar-…

13

-Ap

r-1

517-M

ay-…

20

-Ju

n-1

52

4-J

ul-

15

27-Aug-…

Exchange rate (NRs/USD)

2015-09-03 27

FY2016 Growth and Inflation Forecast

2015-09-03 28

Cautiously optimistic on growth outlook

• Late and subnormal monsoon

• Scope and pace of post-earthquake reconstruction

• Political uncertainties and supply disruptions

• Net migration, remittances inflows and services sector growth

4.6

3.8

5.1

3.0

4.5

5.5

0

1

2

3

4

5

6

FY2012 FY2013 FY2014R FY2015P FY2016_s1 FY2016_s2

CBS NRM forecast as of Aug 2015

Supply-side contributions to growth

Agriculture Industry Services GDP growth (basic prices)

2015-09-03 29

Inflation to be elevated levels

• Expected low agricultural harvest

• Higher demand for reconstruction materials and workers

• Supply disruptions, including distribution networks

• Political strikes

• Depreciation of Nepalese rupee

9.6 9.6

8.3

9.9

9.1

7.2

8.5

9.5

0

2

4

6

8

10

12

FY2010 FY2011 FY2012 FY2013 FY2014 FY2015 FY2016_s1 FY2016_s2

NRM forecast as of Aug 2015

Contributions to inflation

Food and beverage Non-food and services Nepal-CPI India-CPI

2015-09-03 30

Fiscal Sustainability and Reconstruction

• Funds for

reconstruction is not an

issue

– Pledged amount > public

sector needs

• Capacity to accelerate

reconstruction projects

within the given

timeframe is an issue

Adequate fiscal space to

finance (through

borrowing) post-

earthquake reconstruction

2015-09-03 31

Dearth of capacity but not funds!

Debt stabilizing primary balance

Initial debt to GDP level 25.6%

Weighted real interest rate -0.1%

GDP growth rate 5.0%

Required primary balance -1.2%

2015-09-03 32

Fiscal sustainability even with a primary deficit

-5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Public debt and primary balance estimate (% of GDP)

Public debt_s1 Public debt_s2 Public debt_s3

Primary balance_s1 Primary balance_s2 Primary balance_s3

2015-09-03 33

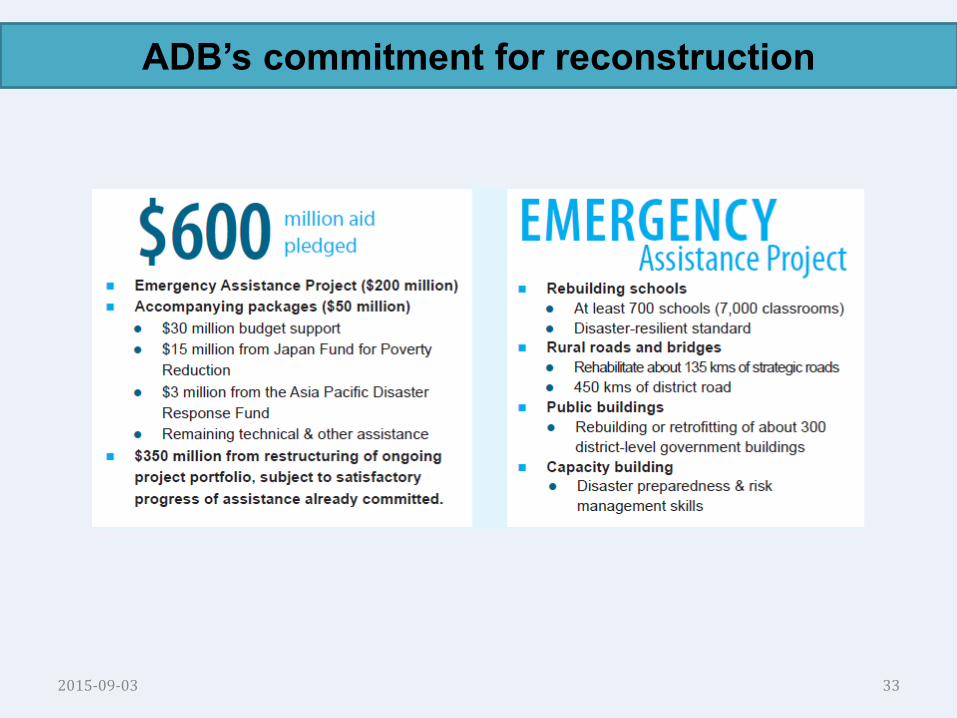

ADB’s commitment for reconstruction

2015-09-03 34

Thank You!

2015-09-03 35