nestlé, mobilising people to implement change dealing with ... · pdf filerwanda -...

TRANSCRIPT

Rwanda

Consulting Abroad Program

Spring 2012

By John Brittell

Agenda

• MacroView

• Agricultural Sector

Overview

• Value Chain

Analysis – Kenya

• Value Chain

Analysis – Rwanda

• Appendix

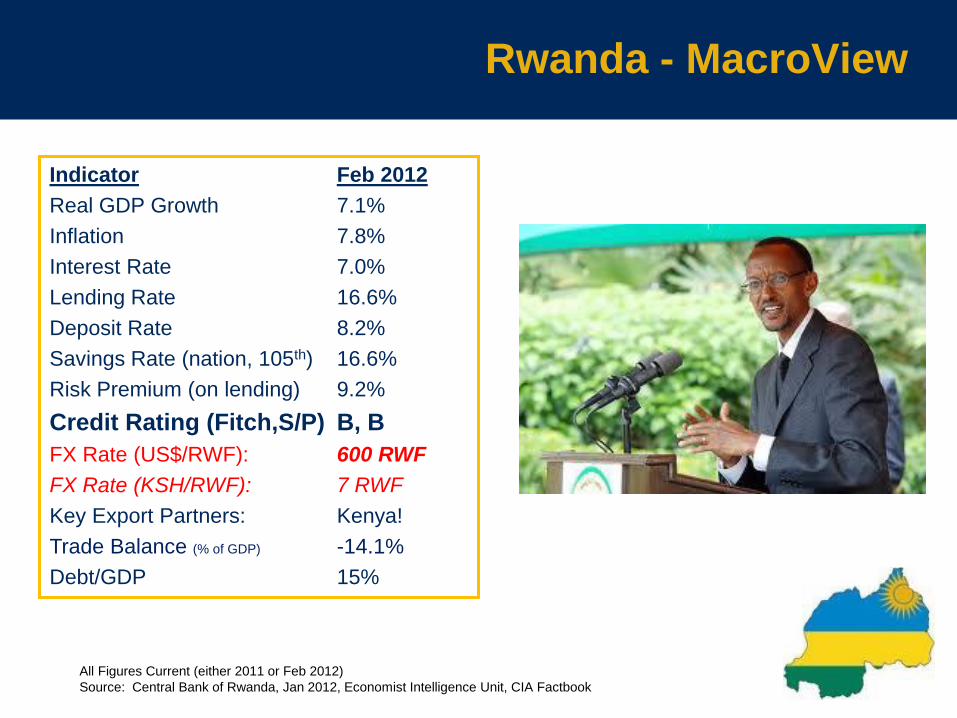

Rwanda - MacroView

All Figures Current (either 2011 or Feb 2012)

Source: Central Bank of Rwanda, Jan 2012, Economist Intelligence Unit, CIA Factbook

Indicator Feb 2012

Real GDP Growth 7.1%

Inflation 7.8%

Interest Rate 7.0%

Lending Rate 16.6%

Deposit Rate 8.2%

Savings Rate (nation, 105th) 16.6%

Risk Premium (on lending) 9.2%

Credit Rating (Fitch,S/P) B, B

FX Rate (US$/RWF): 600 RWF

FX Rate (KSH/RWF): 7 RWF

Key Export Partners: Kenya!

Trade Balance (% of GDP) -14.1%

Debt/GDP 15%

Rwanda – MacroView FX Rates

Source: EIU Rwanda 2012, Oanda.com

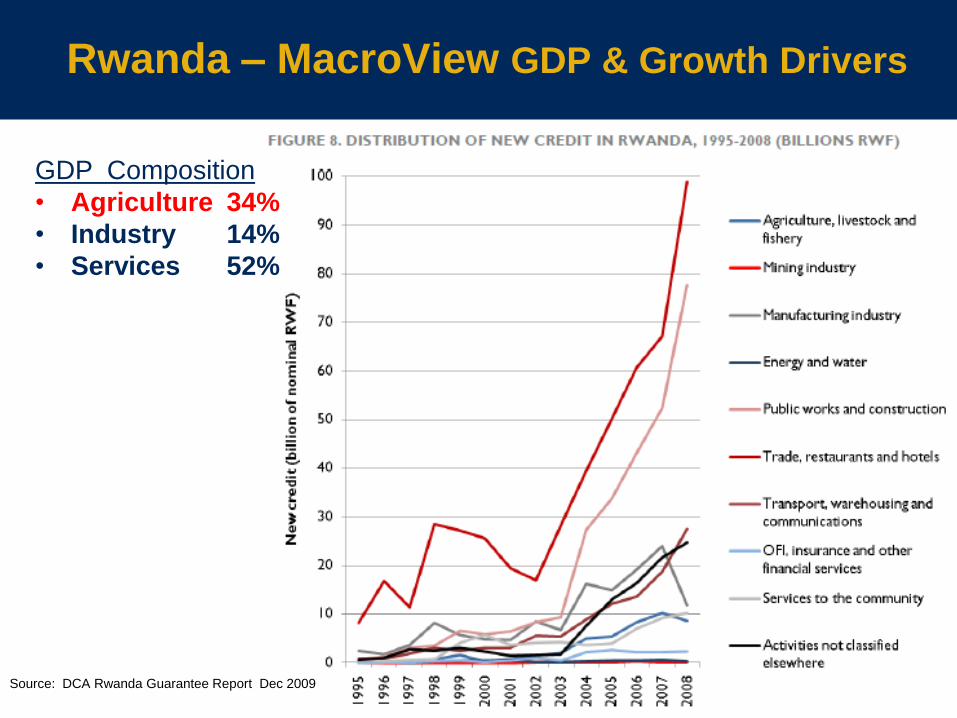

Rwanda – MacroView GDP & Growth Drivers

GDP Composition

• Agriculture 34%

• Industry 14%

• Services 52%

Source: DCA Rwanda Guarantee Report Dec 2009

Rwanda – MacroView Exports

Source: EIU Rwanda 2012

Rwanda – MacroView Social

• Population (2009 Census) *11.4 million people, 81% rural, 2.8% growth rate

overall, 8.2% urban growth rate; *400 pple/sqkm! The

most dense country in Africa…

• Age Demographic: youth < 14yrs are

> 41% of population

• Labor: xx% unemployment rate. xx% of formal

employment and more than xx% of informal

employment in agriculture

• Income distribution:

• Education: Mostly agrarian. 70% literacy rate

(men 76%, women 64%), 96% primary school

enrollment

• Societies: cooperatives limited

Agriculture Sector Overview

Agricultural Sector Overview

• Agriculture Products: coffee, tea, pyrethrum

(insecticide made from chrysanthemums), bananas,

beans, sorghum, potatoes; livestock

• Challenges: land degradation, overuse, and

fragmentation

Kenyan Value Chain Analysis

USAID’s Value Chain Analysis

What Does Value Chain Analysis Entail Per USAID?

• In identifying opportunities for upgrading and the constraints to these

opportunities, the analysis should focus on answering the following

questions:

• What and where are the market opportunities?

• What upgrading is needed to exploit them?

• Who will benefit from this upgrading?

• Who has the resources, skills and incentives to drive upgrading?

• Why has it not happened already?

• What will it take to make it happen?

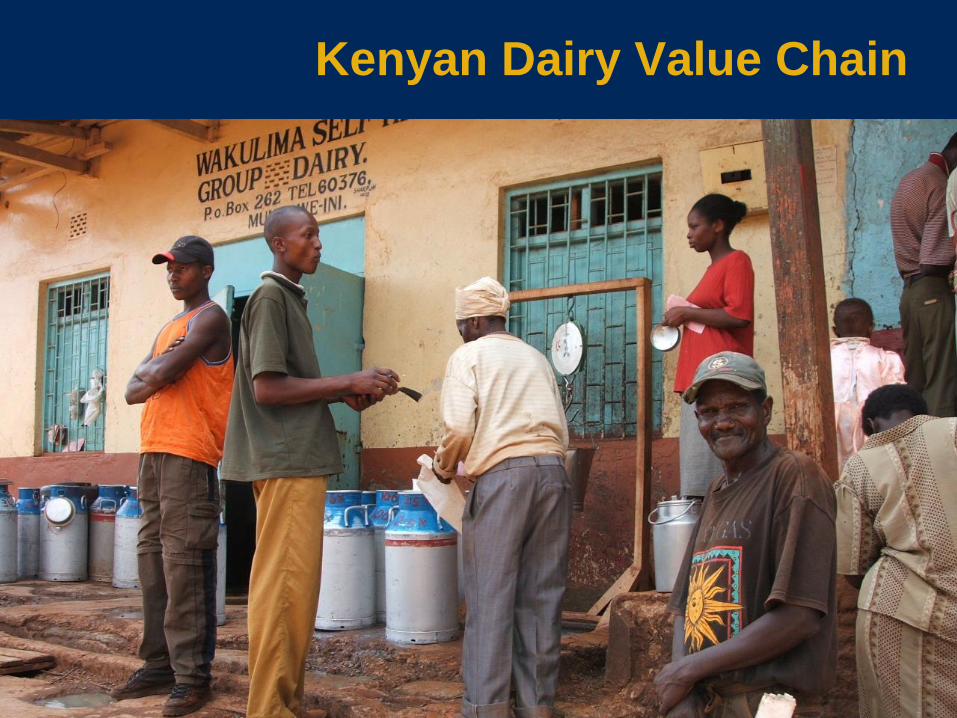

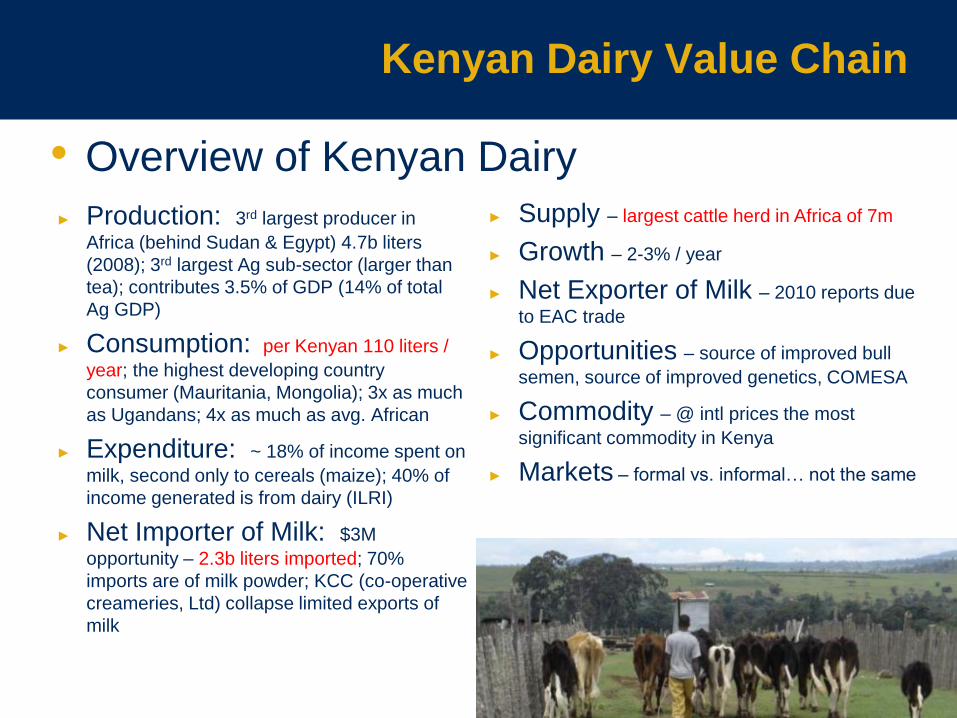

Kenyan Dairy Value Chain

Kenyan Dairy Value Chain

► Production: 3rd largest producer in

Africa (behind Sudan & Egypt) 4.7b liters

(2008); 3rd largest Ag sub-sector (larger than

tea); contributes 3.5% of GDP (14% of total

Ag GDP)

► Consumption: per Kenyan 110 liters /

year; the highest developing country

consumer (Mauritania, Mongolia); 3x as much

as Ugandans; 4x as much as avg. African

► Expenditure: ~ 18% of income spent on

milk, second only to cereals (maize); 40% of

income generated is from dairy (ILRI)

► Net Importer of Milk: $3M

opportunity – 2.3b liters imported; 70%

imports are of milk powder; KCC (co-operative

creameries, Ltd) collapse limited exports of

milk

► Supply – largest cattle herd in Africa of 7m

► Growth – 2-3% / year

► Net Exporter of Milk – 2010 reports due

to EAC trade

► Opportunities – source of improved bull

semen, source of improved genetics, COMESA

► Commodity – @ intl prices the most

significant commodity in Kenya

► Markets – formal vs. informal… not the same

• Overview of Kenyan Dairy

Kenyan Dairy Value Chain

► Employment: husbandry skills low; but

milk bars, mini-dairies, processors, cooling

plants, cottage industries all offer employment

(account for 3.5% of GDP); 1.8m dairy farms

or 35% of rural households

► Efficiency of local production

compared to global averages

(yield gap): yields per cow in US ~

9,000 kg / year; SA & Argentina ~ 2,500 to

3,500 kg / year; Kenya ~ 670 kg / year

(NewKCC) ~ 564 kg / year by FAO

► Geography of production: 53% in

Rift Valley, 25% in Central Province

► Major players: NewKCC, Brookside

Dairy, SpinKnit, Githunguru account for 92%

of market

• Constraints ► Regulation – heavy with very low support

for artificial insemination (improved bull

semen) and veterinary services

► Capacity - smallholder (2-3 cows) farms

produce 80% supply, low per farmer

production – supply to processors shady

► Quality – is poor; adoption of technology

low

► Costs – high production costly, processing

and packaging costs high and preclude

investment

► Investments – weather to volatile; price

premium for chilled milk

• Overview of Kenyan Dairy

Kenyan Dairy Value Chain

VC Point Inputs Production Transport / Bulking / Cooling

Distribution / Processing

Marketing / Distribution

Stakeholders Who is doing this?

- Cows, Goats, Camels of good breed

- Land & Water - Limited feed supply (no

napier grass), - Little vet services, - Structure/ housing - Waste management

- 80% from small (1-4 cows) holder farmers

- Produce 3.2b liters (2005) ~32% of this enters formal market (based on rainy seasons x2)

- Zero grazing = lower production due to feed

- Semi and Open range grazing offer 15-30liters per day

- milk marketed (2005)increased by 21.2% to over 1 billion liters

- Low technology adoption

- 85% milk is fresh, 3% yogurt, fermented 7%, 2% value added products (cheese, butter)

- 75% of total costs of production; 90% variable costs

- ~ 20-25% of total marketed milk sold through formal processors; remainder goes through informal sector

- 34 registered processors (>80% market controlled by 3 companies NewKCC (39%), Brookside (31%), SpinKnit (13%)

- Kakuzi (largest one) - New packaging brings

price point lower (250ml and 500ml = 25% lower price point)

- Sustainable Distribution system: via bikes!

Financing Needs that have/have not been met

- Feeding (nutrient intake) - Purchase of land to

prevent Common land grazing; also to seed feed (napier grass)

- Access to water

- Access to improved breeding (AI – artificial insemination); lower costs to semen

- Transportation from Farmer to Cooler/Processor

- Cooling centers a must in bank loans to farmers; largest problem in supply chain

- Large players only utilize 30-40% capacity; Brookside the exception @ 70% capacity utilization

- Consumption happens in small quantities, typically for tea drinking

- Raw milk ‘better’ for Kenyans

- Boiling is ‘good enough’ over pasteurized milk

- Transportation

Additional Info/Notes

- Fodder preservation smoothens milk flows

- New technology (by ICIPE) controls crop pests affecting dairy

Suppliers - Animal feed - Breeding / Vets - Dairy Equip - Farm Equip - Livestock Insurance

Other uses - Compost Manure - Biogas

- Center for Development Enterprises

- EADD Kenya (east Africa dairy development)

- Heifer Intl.

Kenyan Dairy Value Chain

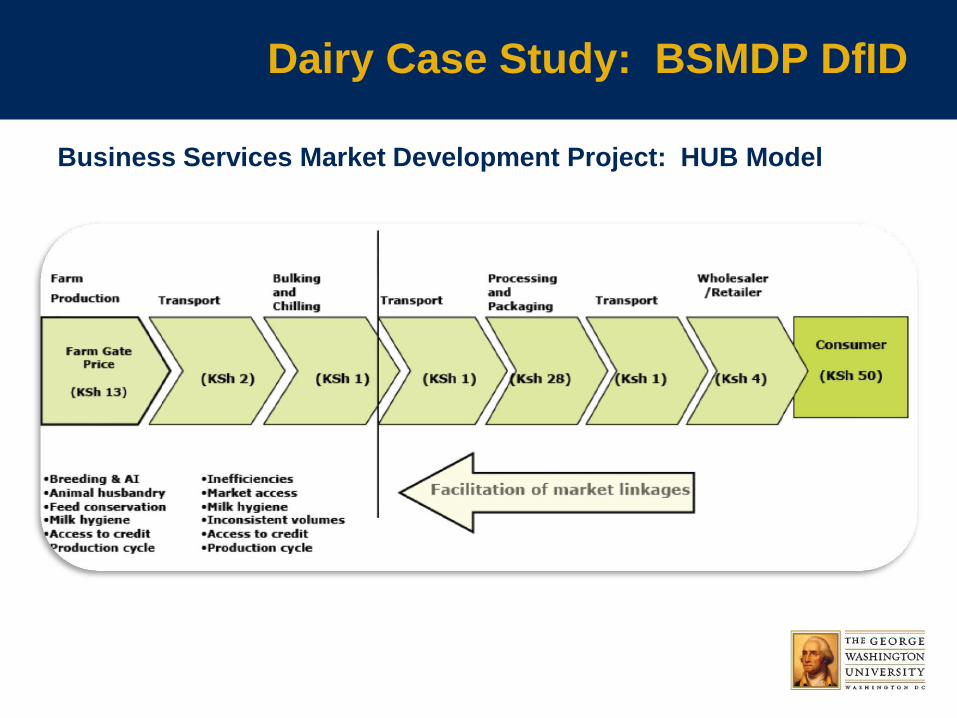

Farmer (Producer)

• Spread: 13-20 Ksh / lliter

Transporter or Hawker

• Spread: 4-5 Ksh / liter

Bulking & Cooling

• Spread: 2 Ksh / liter

Distribution

• Spread: n/a

Processing

• Spread: 14-25 Ksh / liter

Marketing & Distribution

• Spread: 1-2 Ksh / liter

Consumption

• Price: 30-60 Ksh / liter

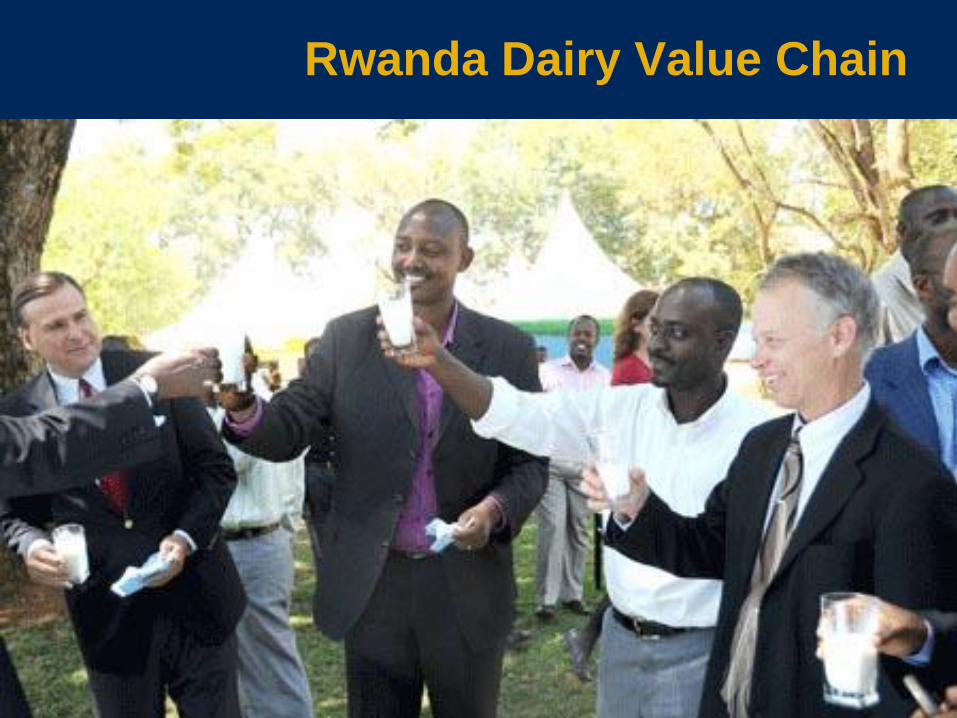

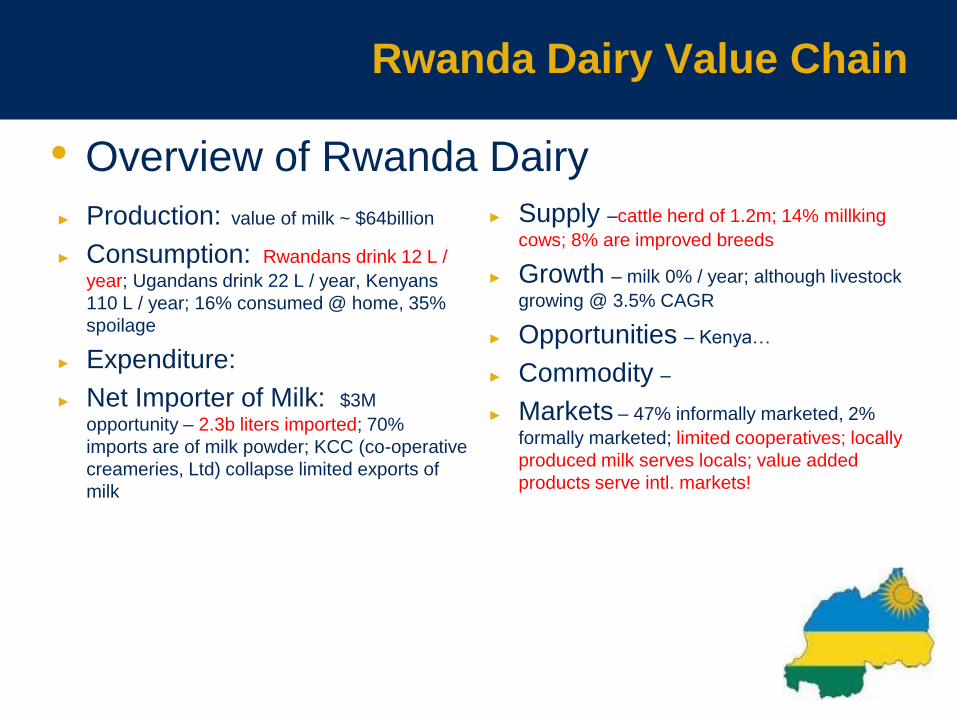

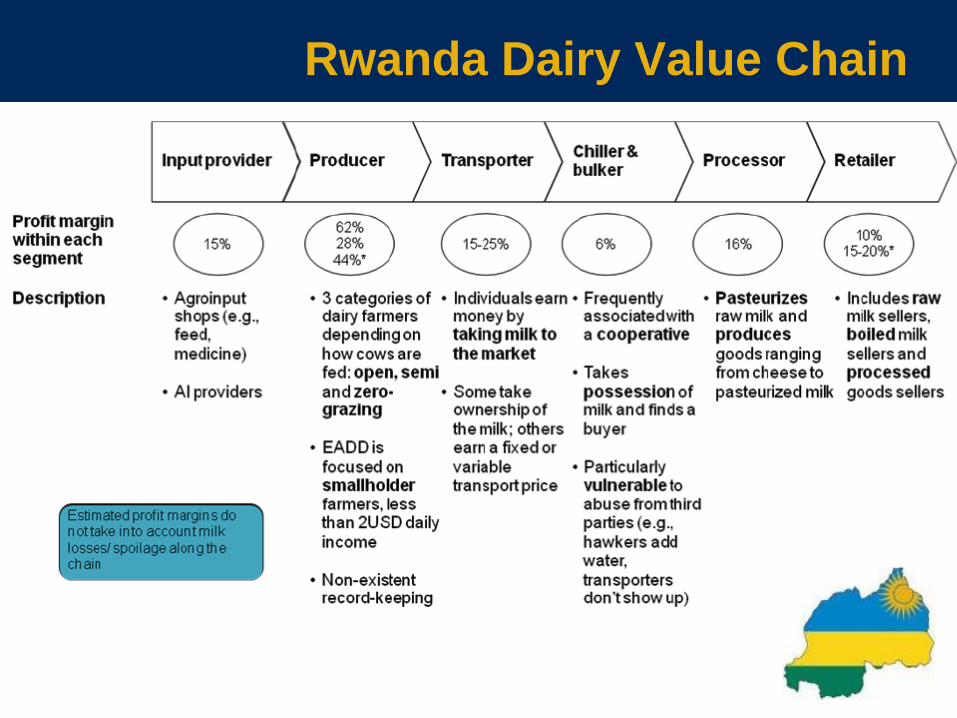

Rwanda Dairy Value Chain

Rwanda Dairy Value Chain

► Production: value of milk ~ $64billion

► Consumption: Rwandans drink 12 L /

year; Ugandans drink 22 L / year, Kenyans

110 L / year; 16% consumed @ home, 35%

spoilage

► Expenditure:

► Net Importer of Milk: $3M

opportunity – 2.3b liters imported; 70%

imports are of milk powder; KCC (co-operative

creameries, Ltd) collapse limited exports of

milk

► Supply –cattle herd of 1.2m; 14% millking

cows; 8% are improved breeds

► Growth – milk 0% / year; although livestock

growing @ 3.5% CAGR

► Opportunities – Kenya…

► Commodity –

► Markets – 47% informally marketed, 2%

formally marketed; limited cooperatives; locally

produced milk serves locals; value added

products serve intl. markets!

• Overview of Rwanda Dairy

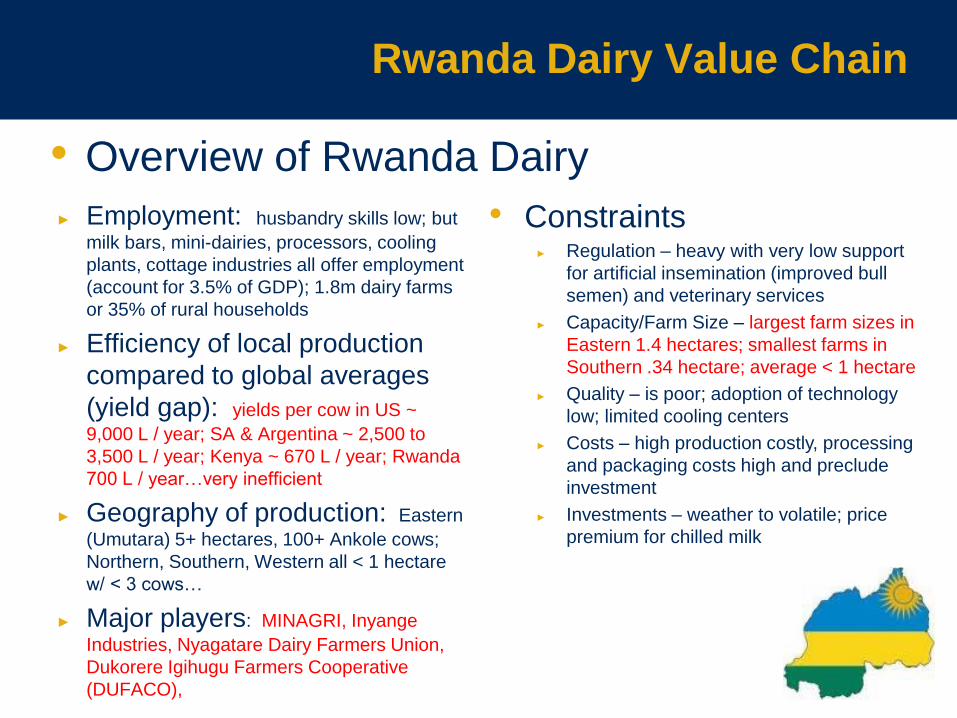

Rwanda Dairy Value Chain

► Employment: husbandry skills low; but

milk bars, mini-dairies, processors, cooling

plants, cottage industries all offer employment

(account for 3.5% of GDP); 1.8m dairy farms

or 35% of rural households

► Efficiency of local production

compared to global averages

(yield gap): yields per cow in US ~

9,000 L / year; SA & Argentina ~ 2,500 to

3,500 L / year; Kenya ~ 670 L / year; Rwanda

700 L / year…very inefficient

► Geography of production: Eastern

(Umutara) 5+ hectares, 100+ Ankole cows;

Northern, Southern, Western all < 1 hectare

w/ < 3 cows…

► Major players: MINAGRI, Inyange

Industries, Nyagatare Dairy Farmers Union,

Dukorere Igihugu Farmers Cooperative

(DUFACO),

• Constraints ► Regulation – heavy with very low support

for artificial insemination (improved bull

semen) and veterinary services

► Capacity/Farm Size – largest farm sizes in

Eastern 1.4 hectares; smallest farms in

Southern .34 hectare; average < 1 hectare

► Quality – is poor; adoption of technology

low; limited cooling centers

► Costs – high production costly, processing

and packaging costs high and preclude

investment

► Investments – weather to volatile; price

premium for chilled milk

• Overview of Rwanda Dairy

Rwanda Dairy Value Chain

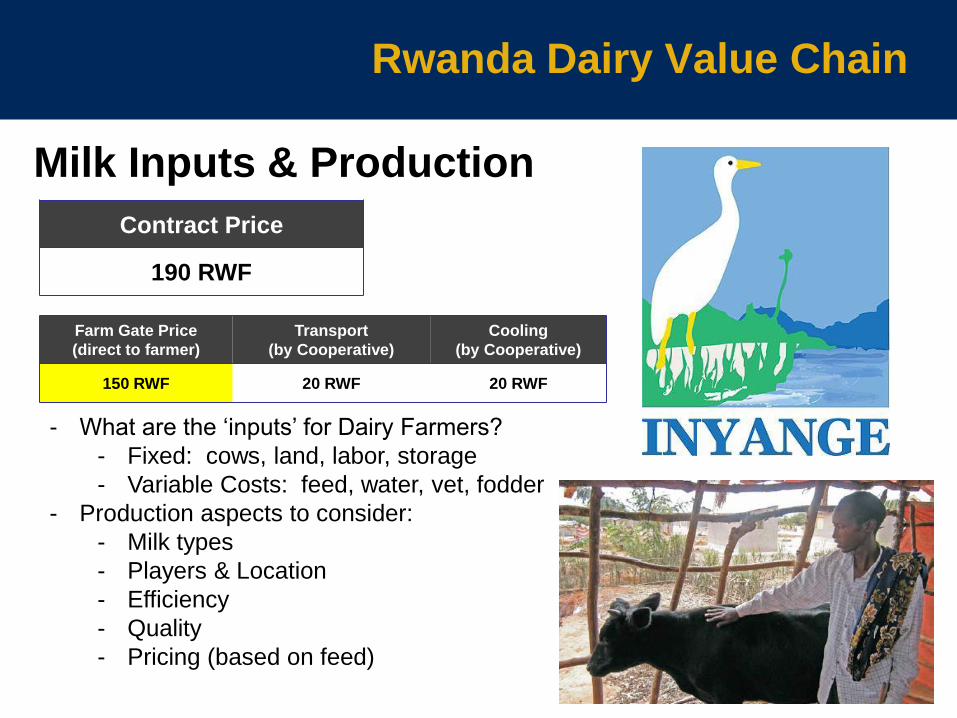

Rwanda Dairy Value Chain

Farm Gate Price

(direct to farmer)

Transport

(by Cooperative)

Cooling

(by Cooperative)

150 RWF 20 RWF 20 RWF

Contract Price

190 RWF

Milk Inputs & Production

- What are the ‘inputs’ for Dairy Farmers?

- Fixed: cows, land, labor, storage

- Variable Costs: feed, water, vet, fodder

- Production aspects to consider:

- Milk types

- Players & Location

- Efficiency

- Quality

- Pricing (based on feed)

Rwanda Dairy Value Chain

Transportation (I) – bicycle vs…

Rwanda Dairy Value Chain

Transportation (I) – …commercial

Rwanda Dairy Value Chain

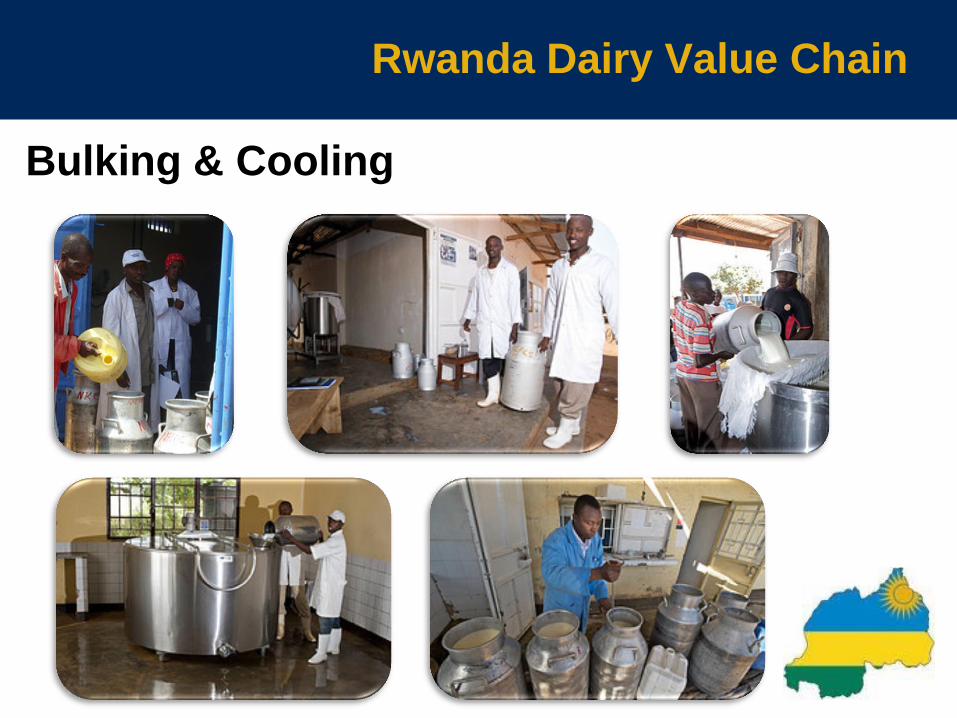

Bulking & Cooling

Rwanda Dairy Value Chain

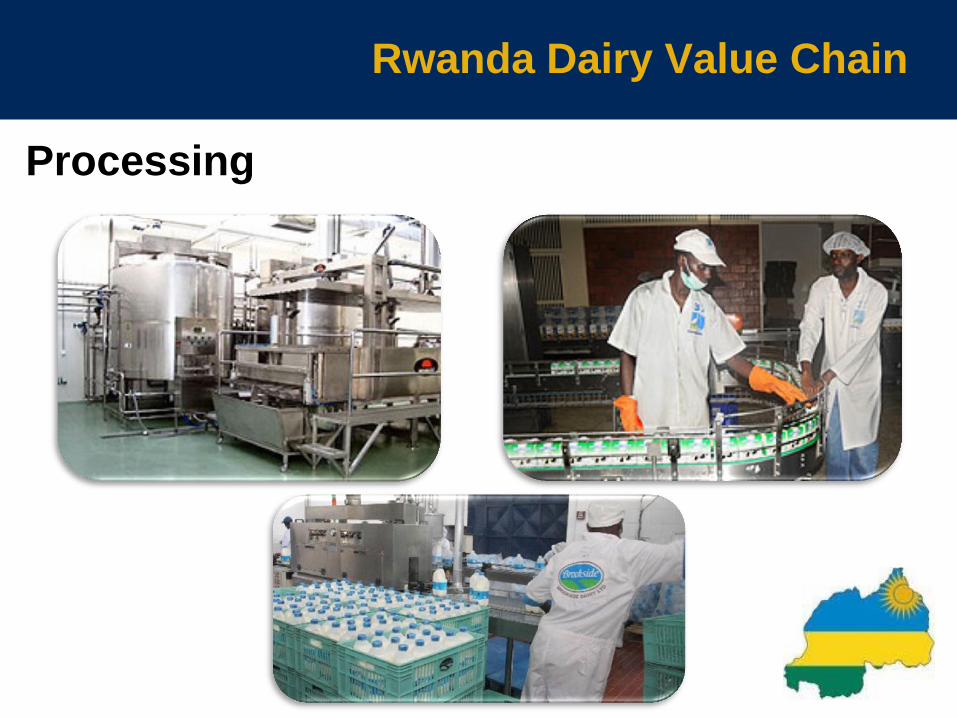

Processing

Rwanda Dairy Value Chain

Milk Vendor Location ?

Retail Vendors

Rwanda Dairy Value Chain

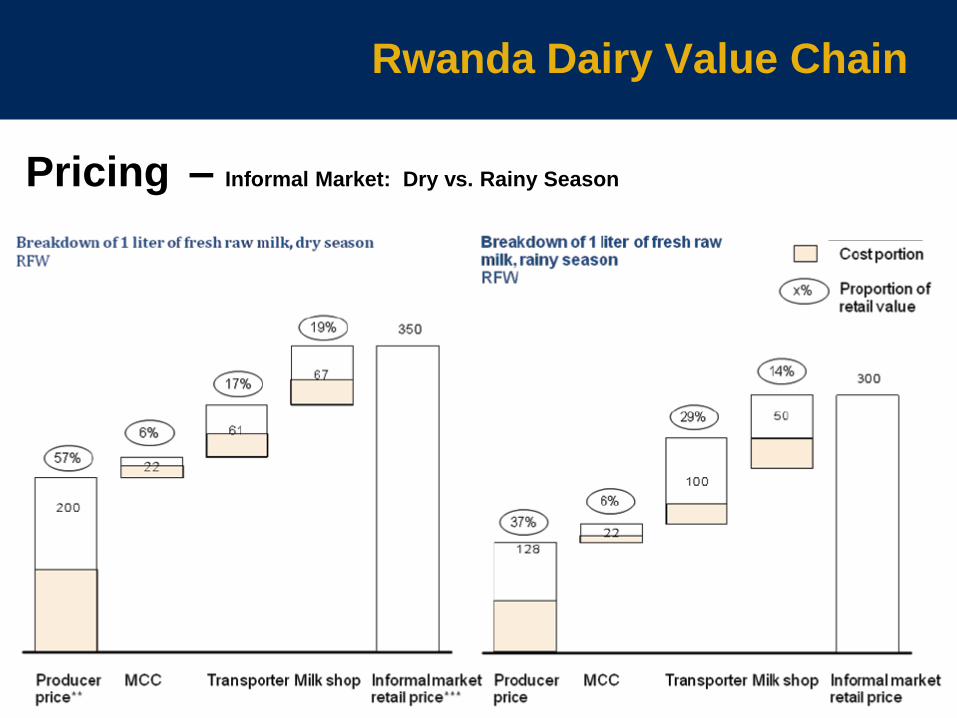

Pricing – Informal Market: Dry vs. Rainy Season

Rwanda Dairy Value Chain

Pricing – Formal Market: All Seasons

Rwanda Dairy Value Chain

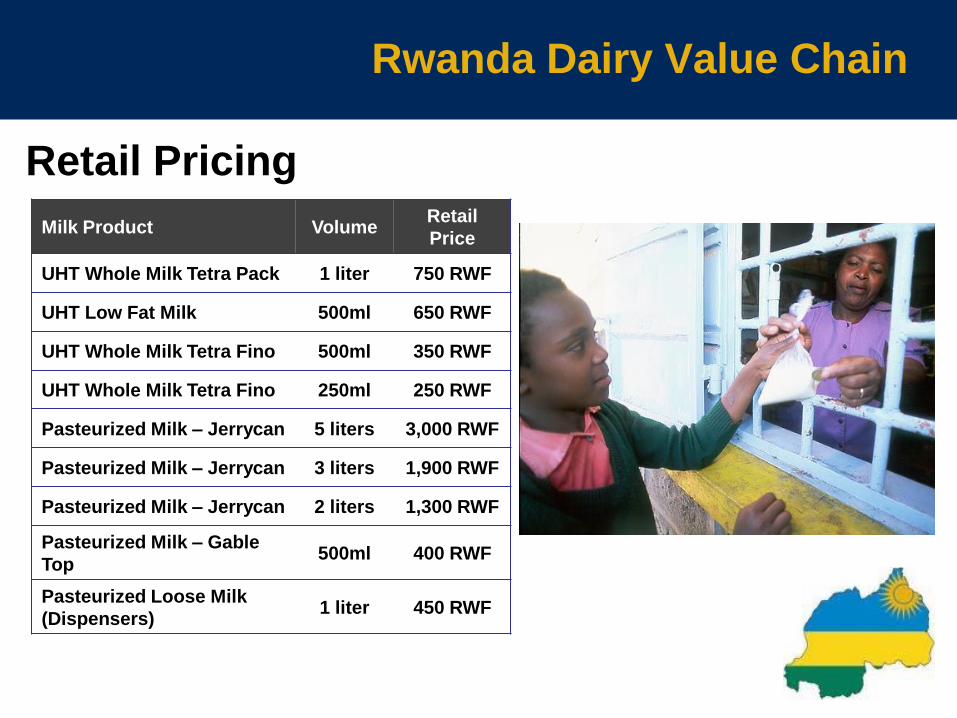

Milk Product Volume Retail

Price

UHT Whole Milk Tetra Pack 1 liter 750 RWF

UHT Low Fat Milk 500ml 650 RWF

UHT Whole Milk Tetra Fino 500ml 350 RWF

UHT Whole Milk Tetra Fino 250ml 250 RWF

Pasteurized Milk – Jerrycan 5 liters 3,000 RWF

Pasteurized Milk – Jerrycan 3 liters 1,900 RWF

Pasteurized Milk – Jerrycan 2 liters 1,300 RWF

Pasteurized Milk – Gable

Top 500ml 400 RWF

Pasteurized Loose Milk

(Dispensers) 1 liter 450 RWF

Retail Pricing

Questions

Appendix

Kenyan Dairy Value Chain

Kenyan Dairy Value Chain

Margins Analysis

Dairy Case Study: BSMDP DfID

Business Services Market Development Project: Local Model

Dairy Case Study: BSMDP DfID

Business Services Market Development Project: HUB Model