netflix.a new power player in the italian media landscape

TRANSCRIPT

Claudio Cammarano, London EMBA 2014

A new power player in the Italian media landscapeMarketing strategy and tactical plan

Shanghai, August 5th 2014

Agenda• Executive summary• Analytical summary

Category: demand attractivenessCategory: market attractivenessCompany & competitive positionGE/McKinsey’s matrixCompetitive perceptual positioningCompetitors’ brand attributesCompetitors triage of valueBrand meaning mapPositioning mapMDI vs. SDI dimensionsBrand Asset EvaluatorCenters of influence & PESTLE

• Strategic opportunity & marketing strategy • Decision tree & strategic alternatives evaluation• Strategic recommendation• Tactical marketing plan: S_IVAR

MDI vs. SDI projectionsDesired brand objectivesMarket share performance treeThe core conceptBudget, cost, benefitsExamples of creativity

• Brand management Brand attributesBrand personalityThe 4 pillars of brand equityDesired outcome on positioning mapDesired outcome on Brand asset evaluatorValue proposition evaluation matrix

• Exhibits

Executive Summary• The strategic opportunity is to enter the Italian market with

possible $ 846m revenue by 2017

• We can grab this opportunity by considering competition within the entire E&M category and differentiating our product in order to better reach unmet consumer needs

• The strategic alternatives are: (1) entering the Italian market with our efforts alone, (2) entering the Italian market in partnership with a relevant Italian player, or (3) entering the Italian market as a part of a wider European strategy for the company

• We recommend to enter the Italian market in synergy with Netflix European strategy because we can generate total revenue $ 397m in 2 years and $ 846 by 2017

In Italy, in 2017, spending for Internet accesswill have grown from € 7,3b to € 12b with+10% year-on-year growth. Digital productswill be 31% of E&M total spending.

Category: Demand Attractiveness

Implication: Internet access will drive consumersdemand and the entire category growth within 2017.

E&M Consumer Spending* In 2013 In 2017

CategoryEntertainment & Media

€ 48b (+2,3% y-o-y)

€ 56b (+3,5% y-o-y)

Segment Home video€ 1.069b(-1.6% y-o-y)

€ 1.145b(+1,4% y-o-y)

Sub-segmentDigital home-video

5% of the total home video sub-seg

35-40% of the total home video sub-seg

*Source: PwC 2013, “Entertainment & Media Outlook in Italy”.

Italian E&M industry is risky on overall, with a medium-low degree of market attractiveness.

Market Risk Attractiveness: Italian media

Forces Reasons Mitigating Factors

Italian Entertainment & Media industry

Rivalry(MEDIUM)

Risk of triggering a price war amongcompetitors.

Focusing on add-on servicesand premium prices.

Supplier Power (HIGH)

Huge negotiation power for stars, authors & agents; now they can skiptraditional intermediation and ask for different revenue stream model.

Differentiating through tailored services to suppliers (e.g. multichannel publishing).

New entrants(MEDIUM)

Risk of product comoditization and/or price war can let new player enter the game.

Only big players with huge technologic assets and Government endorsement can realistically enter the market.

Substitute power(HIGH)

Technological convergence brings all entertainment consumes into a unique device. All entertainment segments compete for customers’ disposable time. Piracy is a potential substitute.

In Italy technological convergence is not accomplished yet: first mover will have huge advantages.

Buyer Power (MEDIUM)

Greater freedom of choice among media.

Freedom always requires sophisticated consumers.

We have high strengths and opportunities in Italy

Company & Competitive Position:

STRENGTHSuperior brand, offering & positioning

Superior operations and customer preferences insight

Superior organization agility & HR management

OPPORTUNITYAn entire customer segment up to now ignored

A legal full-service and tailor-made product can compete both with mass market home video and piracy

WEAKNESSESNot influential in Italian system of regulations and governmental authorizations

THREATSRequirement of products cultural adaptation in the target market

Some major traditional competitors are trying to fill the gap

Implication: There are unmet customer needs; traditionalplayers didn’t fill the gap in order to protect their currentleadership position.

Considering Netflix not only as part of home videosegment but of E&M on overall, we might considerinvestments for growth.

GE Matrix: Italian E&M Industry

New Market Entry Improve Position

Invest to Grow Improve Position Protect Position

Invest to GrowProtect Position

Improve PositionOptimize Position

Harvest

Improve Position Optimize Position

Invest to GrowProtect Position

Optimize Position

Harvest or Divest

MonetizeHarvest or

Divest

MonetizeHarvest or

Divest

Mar

ket A

ttrac

tiven

ess

Competitive Position

Consumer: Competitive Perceptual PositionIn consumers’ mind, competition is not only within home videoplayers, but also involves broad- and narrowcast tv channels.

Home video distributors

Warner Bros Universal Medusa Niche competitors

SegmentationAdults 18-50, with a male skew. Younger people more skewed to lower prices and purchases on mass markets.

Teenagers to adults (14-45), with niche consumepatterns: science fiction, Japanese anime etc.

Frame of referenceDistributors are not visible by themselves: its product brand that drives the offer.

Same, but with slightly more focus on Italian production.

Collection. Doesn't matter if they have already a digital version.

DifferentiationA vast portfolio of titles leaded by brands (actors, directors, series), with different price level.

Same, but with Italian blockbuster successes used as a vessil of overall quality.

In-group and out-group dynamics: followers are a community.

Broadcast tv RAI Mediaset La7 Minor competitors

SegmentationPotentially the widest audience possible: adults 19-75, with a female skew. Both targeting exactly the same audience. Losing teenagers on the way.

Adults 20-50, with a slight male skew. For newspaper and book regular readers.

People 15-60, who use these channel as a second screen.

Frame of referenceThe public free broadcasting service.

The main private broadcaster. In the last 30 years completetly substituted RAI's role.

Quality entertainment & news. Here's what public opinion says.

My own local world on tv.

Differentiation

Supposed to provide quality and experimentation. Totally disrupted.

On degree of visibility: it's what is left of mass communication in Italy today.

On quality. On geographical basis.

Consumer: Competitive Perceptual Position

Pay tv Sky Mediaset Premium Fastweb TV Vodafone Infinity & similar

Segmentation

Adults 30-60, with a male skew. Affluent, successful, willing to pay for high quality content.

Families with extended consumes of broadcast tv (especially Mediaset).

Families or adults with extended consumes of Internet bandwidth.

Mobile connectivity providers' clients.

Frame of referenceDistinction. Broadcast tv is cheap; narrowcasting is something worth to pay for.

Undefined. Leveraging Mediaset brand alone as a differentiation factor is not enough to trigger a frame of reference.

All the content with my Fastweb connection, the fastest in the market.

Content I love right here on my mobile device with a little mark-up.

DifferentiationPremium price. Quality of news (the only one with a global focus).

Quality products from Mediaset portfolio at a premium price. Poor efficacy.

An add-on service for Fastweb clients. A small niche, but technologically enabled.

An add-on service for mobile device users, but 3G is not quick enough yet and wifi not so spreaded.

Digital terrestrial tv (DDTV)

Cielo Rai 4, Rai 5, RaiNews24 & similar Real Time & similar Boing & similar

SegmentationAdults 18-50, with a female skew.

Audience highly segmented on the basis of content: Rai 4 for quality entertainment, Rai5 for documentaries, RaiNews24 for news etc.

Teenagers and adults, 15-45 years old with a female skew.

Children, teenagers and their parents.

Frame of referenceA selection of unexclusive free content form Sky payed channel.

Audience deluded by Rai broadcast tv can find refuge here.

Reality-based entertainment: low-cost reality shows, talents etc.

Children entertainment.

DifferentiationQuality nonetheless, but on a delayed time compared to Sky.

It is where Rai experiments and seeks for quality. On the basis of content. On the basis of content.

Implications:• For consumers market, what leads differentiation is not

driven by distribution channels, but product brands(e.g. authors, actors, directors, movies, series etc.).

• Distributors credibility and differentiation is derived bytheir brand portfolio.

Consumer: Competitive Perceptual Position• Home video segment players are not differentiated per

se: it is their product brand portfolio that counts• On broadcast side, the historical role of Rai as quality

content provider has been heavily disrupted in the last25-30 years

• The unique leader of pay tv segment is Sky, whileMediaset Premium failed to gain a real differentiation

• Fastweb and Vodafone are trying to leverage their techsavvy niche consumers, but their content offer ispoor, not exclusive and narrow

Consumers: Competitors Brand Attributes

Main attribute Secondaryattribute Brand persona

RAI Classic Friendly A 60 year old mother and grand-mother, attended secondary schools, not many interests except family.

Mediaset Fun Accessible A 55 year old male, father, not very cultured, loves cars, sports and easy entertainment.

Sky Sophisticated/ Upscale Modern

A 45 year old professional, with high education and net income above average, speaks a good English, enjoys smart

entertainment, has only one child.

La7 Competent ModernA 50 year old man, cultured, employed in services, intellectual,

sophisticated, a bit snobbish, probably close to Italian labor party.

Fastweb Modern RuggednessA 35 year old man, not married, still living as a teenager,

probably imployead as a web developer in one of the main cities of the country.

Vodafone Personable Spontaneous A 35 year old lady, easy-going and beautiful, very connected with peers, colleagues and friend.

Among all players, only six have a defined set of brand attributes.

Newcomers (Sky, Fastweb, Vodafone, La7 target specific segments of customers,even though with different business models (e.g. subscription vs. advertising).

Consumer: Competitors Triage of Value

Mainstream media brands:• In the last 25 years, RAI has lost its

differentiation, pointing to function,emotion and experience at the same time

• Mediaset is not functional any longer,after its prestiged anchorman EnricoMentana left the company to start a newnewscast up for La7

• Sky’s approach is the most focused onfunctional benefits («the best newscast +the greatest shows») and on watchingexperience.

Rai

Sky

MediasetFUNCTION

EMOTION EXPERIENCE

FUNCTION

EMOTION EXPERIENCE

FUNCTION

EMOTION EXPERIENCE

The triage of value model shows how mainstream and target market mediapromote their benefit to the customers.

Consumer: Competitors Triage of Value

Target market media brands:• La7 is a mainstream media, but it is

targeted on a narrow segment of Italianpopulation, more interested in the qualityof services.

• Fastweb’ communication is entirelyfocused on fast traffic data stream (itstestimonial is the motorbike worldchampion Valentino Rossi).

• Vodafone communication is centered onconsumers feelings and entertainment.

La7

Vodafone

FastwebFUNCTION

EMOTION EXPERIENCE

FUNCTION

EMOTION EXPERIENCE

FUNCTION

EMOTION EXPERIENCE

Consumer: Brand meaning map

A culture crisis implies media crisis: The traditional role of Rai and Mediaset asmainstream cultural mediators has failed. This void has been only in part filled byniche players such are now La7 and Sky.

Within the competitive scenario, only Rai, Mediaset, La7 and Sky havesuccessfully positioned as content providers, while the others (Fastweb,Vodafone) are considered as technology add-on services.

Main meanings Insights

Rai

Tradition - Family - Education - Entertainment - Who holds the remote control? - Authority - (Official) truth -

Semplification - News - Media events (undisputed) -"Nazional-popolare"

In the last 10 years, Rai failed to define and identify events of

national interest. End of Italian spirit of "nazional-popolare".

MediasetEntertainment - Leisure - Easy - Sport - Extreme -

Excitement - News - Semplification - Prime time - Media events (pop)

More and more difficult to find new popular events to vehicle throur

mainstream tv.

La7Quality news - Critic - Independent - Intellectual - Quality entertainment - Media event (disputed) - Substitutive of

public service

La7 comes when here Rai and Mediaset fail in their mission.

SkyGlobal - Quality news - Quality entertainment - Exclusivity -

Convenient (SkyGo) - Expensive - Updated - TechnologicMain traits are “mass distinction”

and exclusivity.

Consumer: Positioning map

Upscale

Modern

Accessible

Cielo

Distributor differentiation is key: brand with focus only on content (e.g. anime,science fiction, reality) are confined to niches in the middle of the 4 quadrants.

Mediaset

Sky

3

2

4

1

Mediaset Premium

La7

Rai

Rai DDTV Channels

Fastweb

Vodafone

Niche players

In the last 10 years, as a result of their business and communicationactivities, content providers have positioned their brands asupscale/accessible or modern/classic.

Classic

Consumer: MDI vs. SDI dimensions

Share GrowthOpportunity

Limited Growth

Very High GrowthPotential

Growth With MarketDevelopment

Mark

et

Develo

pm

en

t In

dex (

MD

I)

Share Development Index (SDI)Low High

Low

Hig

h

With the end (or the update) of “mainstream media” concept, formermainstream media are declining, leaving space for newcomers.

In this scenario, Sky and La7 can gain market share left behind by Raiand Mediaset, while Fastweb and Vodafone are growing in proportion withmarket growth (where their market of reference is digital media).

Mediaset

Sky

Rai

Fastweb

La7

Consumer: Brand Asset Evaluator

Brand Status

Bran

d St

reng

th

Currently, power brands are competing in E&M market. Marketis mature, but there seems to be some space for new brands.

Niche players

Mediaset

Rai

Sky

Fastweb

VodafoneMediaset PremiumCielo

La7

Leader product brands (Rai + Mediaset) are being eroded, while Skyhas just started to shift from high-end niche to mainstream. All otherbrands are sharing a fragmented space.From mainstream media to a scenario of mass fragmentation.

Italy is a highly regulated country, with a high degree of culturalcomplexity and bureaucracy. However, there are conditions for awarm reception of Netflix novelty.

• Opinion leaders: Media have already covered Netflix, with muchinterest. Most intellectuals and opinion leaders are looking forwardto its arrival, since in Italy it is common sense that broadcast tv is“cheap”.

• Policy makers: Mainstream media are heavily connected withpolitical power. It is unlikely for a newcomer to enter and disrupt themarket without assuring that the Italian media landscape won’tchange in its substance.

• Trade unions: Netflix HR standard policies are unlikely to be appliedin Italy, since labor market is heavily regulated.

• Digital divide: wifi, 3G and 4G are not as spread as in other Westerncountries. So far, governments haven’t invested in it because theyconceived Internet as a disruptor for mainstream media landscape.

Centers of Influence & PESTLE

Italy is a high-context type of country: technology, currentpolicies and, most of all, culture are the main factors that makeinvestments in media sector so risky.

The strategic opportunity is to enter Italian E&M market inorder to gain by 2017 6m new subscribers and $ 846mrevenue in three years, with a contribution margin of-39% in 2017 (a standard for a tree-year launch).

Strategic Opportunity

Vision To become the next global leader in E&M and TV industry for the next decades.

Goals Leading the way in replacing globally the traditional “linear TV” with multi-screen Internet TV.

Objectives Entering Italian market as a part of a strategy for Western Continental Europe. More specifically for Italy:

In 2015,achieve 1m subscriber with a total amount of $ 72m revenue, reducing marketing expenses through economies of scope.

In 2017,achieve 6m subscribers and $ 846m revenue ($ 450 in 2017 only) with a -39% contribution margin.

Marketing StrategyCompetitive advantage

Our competitive advantage lays in our superior HR, our ability to extract customer insight from raw traffic data and our superior brand.

Resource strategy

In order to enter the Italian market, which has a huge potential but is also risky, we will need to use our resources (capital and labor), expecting positive return in a 5-year time.

Degree of intensity

The effort will have to be intense, but since we have already launched Netflix in other countries in Western Europe and we’re planning to do that in others, we have chance to use economies of scope.

Focus Our target is the Italian cultured middle class at first, aiming to extend to a larger audience within 2017.

• Best product performance leadership

• Best customer relationship

Decision Tree: Strategic alternatives

Enter Italy

Not enter Italy:• Customer base: +0 units• Revenue: $ 0m• Δ margin: $ 0m Enter Italy as a part of a

Western European Strategy.By 2007:• Customer base: +6m units• Revenue: $ 846m• Δ margin: $ -0.4b

Enter Italy in partnership with a major Italian player.By 2017:• Customer base: +6m units• Revenue: $ 846m• Δ margin: $ -0.3b

Enter Italy alone,By 2017:• Customer base: +6m units• Revenue: $ 846m• Δ margin: $ -1.1b

Strategic Alternatives Evaluation:Alternatives

Not enter Italy

Enter Italy alone

Enter Italy with as an Italian tech partner

(e.g. Fastweb)

Enter Italy as a part of an European strategy

Pros

No risks

Total autonomy of decision. No need to share customer info.

Fastweb can foster technology

habilitation of Italian

consumers.

Action better concerted with other European

HQs.

Cons

After 2017 it willbe difficult (and costly) to enterwith a relevantmarket share.

Acting in isolationraises the degree

of risk.

Need to share analytics

expertise with Fastweb.

Difficult to drive change with

several people involved in

decision-making.

Cost

Not gaining new customer base,

relevantinformation, revenues.

Δ margin:

$ -1,1b

Δ margin:

$ -0.3b

Δ margin:

$ -0.4b.

Benefit

Not suffering for that profit loss in the next 5 years.

Revenue:

$ 846m

Revenue:

$ 846m

Revenue:

$ 846m

Our recommendation:

Enter Italy

Not enter Italy:• Customer base: +0 units• Revenue: $ 0m• Δ margin: $ 0m

Enter Italy as a part of aWestern European Strategy:• Customer base: +6m units• Revenue: $ 500m• Δ margin: $ -0.6b

Enter Italy in partnership with a major Italian player:• Customer base: +6m units• Revenue: $ 500m• Δ margin: $ -0.8b

Enter Italy alone:• Customer base: +6m units• Revenue: $ 500m• Δ margin: $ -1.5b

We recommend to enter Italian market as a part of Europeanstrategy, in order to gain effectiveness and efficiency througheconomies of scope.

Tactical Marketing Plan: S_IVARChina

Solutions Shifting linear TV for Neflix means total customization: • Quality, “exactly how you mean it”.• Convenience, that is your favorite show on your favorite display at your

favorite time.• Discover, offering is not only “pull”: we know you best and we will make

you new product offerings you will adore. Information & Incentives

Traditional activities:• Media advertising, online adverstising, DEM and newsletters. • Limited partnership with 3G and wifi providers in order to have access to

technologically enabled customers.TV series production:• Production of a brand new TV series set in most European cities, delivered

to new customers, whose costs can be shared among all European HQs.• Alternative reality game teasing campaign to launch the series.• The teasing campaign will be focus on the main concept: “This story tells

about your story”.

Value For streaming, € 9,99 per month in 2015 and 2016; € 12,99 in 2017.Access &Relationship

Some special content about the series will be shared with customers online. Also a prequel web series will be realized as a teaser.Careful selection of product brand portfolio.

Consumer: MDI vs. SDI projections

Share GrowthOpportunity

Limited Growth

Very High GrowthPotential

Growth With MarketDevelopment

Mark

et

Develo

pm

en

t In

dex (

MD

I)

Share Development Index (SDI)Low High

Low

Hig

h

With the end (or the update) of “mainstream media” concept, formermainstream media are declining, leaving space for newcomers.

Especially Netflix can shift from “cozy clubs” to achieving a dominantplace in mainstream media landscape, considering the new, emerging &unmet consumer needs inside the Italian E&M segment.

Mediaset

Sky

Rai

NetflixFastweb

Netflix Italy: Desired brand objectives

The hitchhikers: ROS 14-20%

The high-power brands: ROS >20%

Dead-end brands: ROS <5%

The low-road brands:ROS 5-10%

«P

rem

ium

» d

eg

ree

of

cate

go

ry

Relative market shareLow High

Low

Hig

h

With the end (or the update) of “mainstream media” concept, formermainstream media are declining, leaving space for newcomers.

With different positioning (not to harm each other), Netflix and Sky canshift from “cozy clubs” to achieving a dominant place in mainstreammedia landscape, taking up a role of cultural mediation.

MediasetSkyRai

Netflix

Market share performance tree:

Aware

Press coverage: $ 0 (labor cost)

Attracted PriceIntend to buy Purchase

Expected SOM in 2017:14% in TV segment

no no no no no

Buzz on TV series with Entertainment42 :$ 10m agency cost

Online and ATL advertising: $ 15 media planning cost

TV series “Path of glory”: $ 300m production cost

Monthly fee at $ 9.99 for 2015 and 2016: $ 0 cost (but less revenues)

DEM & Remarketing: $ 1m advcost

Costs will be sharedamong European HQs.

The TV series: “Paths of glory”As it happened before with “House of Cards”, Netflixwill produce an original TV series refined on the basisof their unique customer insight.

• Based on Stanley Kubrick’s masterpiece on 1st World War

• Directed by Luc Besson

• Starring Ralph Fiennes

• Also starring Franka Potente

• 12 episodes

• Set in Western Europe

• Can follow 1st World War anniversary celebrations

The teaser campaign: “Paths of glory”Set an alternate reality game to promote “Paths of glory”before the launch. The best agency in that specific field isprobably Entertainment42, founded by Jordan Weisman.

• Whysoserious.com, alternative reality campaign for Christopher Nolan’s “Dark knight”

• Nine Inch Nails “Year zero” launch

• Participated for the launch of James Cameron’s “Avatar”

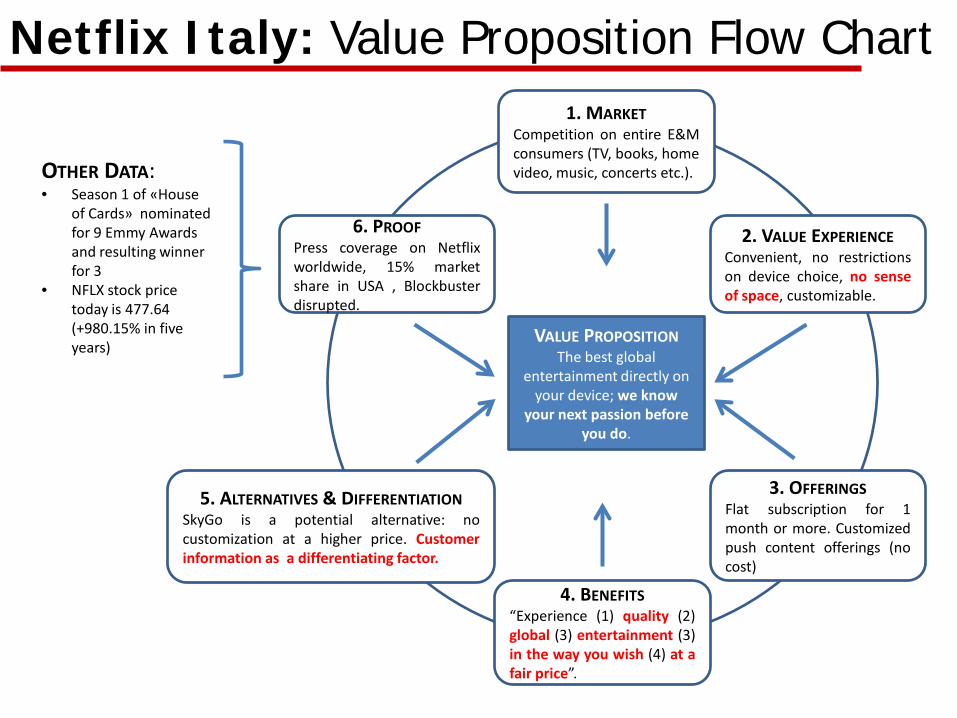

Netflix Italy: Value Proposition Flow Chart

1

VALUE PROPOSITIONThe best global

entertainment directly on your device; we know

your next passion beforeyou do.

1. MARKETCompetition on entire E&Mconsumers (TV, books, homevideo, music, concerts etc.).

5. ALTERNATIVES & DIFFERENTIATIONSkyGo is a potential alternative: nocustomization at a higher price. Customerinformation as a differentiating factor.

3. OFFERINGSFlat subscription for 1month or more. Customizedpush content offerings (nocost)

6. PROOFPress coverage on Netflixworldwide, 15% marketshare in USA , Blockbusterdisrupted.

2. VALUE EXPERIENCEConvenient, no restrictionson device choice, no senseof space, customizable.

4. BENEFITS“Experience (1) quality (2)global (3) entertainment (3)in the way you wish (4) at afair price”.

OTHER DATA:• Season 1 of «House

of Cards» nominatedfor 9 Emmy Awards and resulting winnerfor 3

• NFLX stock pricetoday is 477.64 (+980.15% in fiveyears)

Netflix Italy: Perceptual position & personality

Desidered Perceptual Positioning

SegmentationAdults 25-50, with a male skew. Emerging middle class. Cultured, willing to pay for high quality content. Knowledge and services workers strong skewness.

Frame of referenceCustomized offer, with greater convenience than watching content on PCs. Even possible to share the same room with your family and still watching different programmes.

Differentiation Premium price for a digital distribution services. Very convenient (more convenient than piracy). Technologic but easy. Personal media.

Main attribute Secondaryattribute Brand persona

Modern SpontaneousA 35 year old young man, working as a creative worker in an advertisingagency. Cultured, tech savvy but not interested in technology per se, witha rich and various social life.

Netflix Italy: Brand meaning

Main meanings Insights

Entertainment - Convenience - Customization - Media events (global/ entertainment) - Family - Technology - Updated - Global -Quality service - Quality content

Death of the concept of "second screen".

Netflix formula is the best to meet Italian family unmet needs inmainstream media landscape: quality, security (in terms of privacy andcontent), convenience.

Consumer: Competitors Triage of Value

Compared to other «modern»brands, Netflix is the only oneso tightly focused onexperience. This is certainly adifferentiating factor.

Sky

NetflixItaly

FastwebFUNCTION

EMOTION EXPERIENCE

FUNCTION

EMOTION EXPERIENCE

FUNCTION

EMOTION EXPERIENCE

Netflix Italy: Positioning map

Upscale

Modern

Accessible

Cielo

Mediaset

Sky

3

2

4

1

Mediaset Premium

La7

Rai

Rai DDTV Channels

Fastweb

Vodafone

Niche players

In terms of positioning, Netflix will be positioned as definitely “modern”,but also as “accessible”, because of its flexibility and convenience.

Classic

Netflix

LEGENDA:• Pink is the unfriendly area• Yellow is the niche area• Green is the culture area• Orange is the fail area• Grey is the new frontier area

Consumer: Brand Asset Evaluator

Brand Status

Bran

d St

reng

th

Niche players

Mediaset

Rai

Sky

Fastweb

VodafoneMediaset PremiumCielo

La7

In a scenario of mass fragmentation, Netflix will start itsbrand history as a niche brand, but its purpose it tobecome the next mainstream media.

Our aim is to transform Netflix in Italy from a nichebrand into the new premium mainstream media.

Value Proposition Evaluation MatrixEx

clus

ivity

Desire

IN 2017

NEXT

Claudio Cammarano, London EMBA 2014

Thank you

Exhibit 1: Netflix result on operations in 2013

Revenues derived from our DVD-by-mail membershipservices. The price varies from according to the planchosen by the member.

• DVD-by-mail membership fee = from $ 4.99 to $ 43.99• Contribution margin = 48%

Exhibit 2: Netflix result on operations in 2013

Revenues derived from monthly membership fees forservices consisting solely of streaming content offeredthrough a membership plan.

• Monthly membership fee = $ 7.99 (1 device); $ 11.99 (4 devices)• Contribution margin = 23%

Exhibit 3: Netflix result on operations in 2013

Revenues derived from monthly membership fees forservices consisting solely of streaming content offeredthrough a membership plan.

• Monthly membership fee = from $ 7.00 to $ 14.00• Contribution margin = (39%) • 25% of total streaming memberships

Exhibit 4: Projected result on operations 2015-17

As of /Year Ended December 31 Change

2016 projected: Italy

2016 projected: Italy

2015 projected: Italy

2015 projected: Current markets

2014 projected: Current markets 2013 2012 2013 vs. 2012

(in thousands, except percentages)Members (units):

Net additions 2,760 2,300 1,000 6,249 5,530 4,809 4,263 13%

Members at end of period 6,060 3,300 1,000 22,710 16,460 10,930 6,121 79%

Paid members at end of period 5,757 2,970 0,890 22,255 16,296 9,722 4,892 99%

Contribution loss ($):

Revenues $449,046 $326,700 $71,200 $2,473,418 $1,766,727 $712,390 $287,542 148%

Cost of revenues $100,000 $150,000 $250,000 $1,767,986 $1,262,847 $774,753 $475,570 63%

Marketing $500,000 $500,000 $500,000 $500,000 $215,000 $211,969 $201,115 5%

Contribution loss -$150,954 -$323,300 -$678,800 $205,432 $288,880 -$274,332 -$389,143 -30%

Contribution margin -34% -99% -2,358% 8% 16% -39% -135%

Revenues derived from monthly membership fees in Italyfor services consisting solely of streaming content offeredthrough a membership plan.

• Monthly membership fee = by 2017, 6m subscribers for $ 500m revenues• Contribution margin = (34%)