netwealth educational webinar - the 5 deadly sins of smsfs

TRANSCRIPT

The five deadlysins of SMSFs

Presented byKeat Chew, Head of Technical ServicesNigel Smith, Technical Services Consultant

| Netwealth The five deadly sins of SMSFs2

Disclaimer

This information has been prepared and issued by Netwealth Investments Limited (netwealth), ABN 85 090 569 109, AFSL 230975, RSEL0000192). It contains factual information and general financial product advice only and has been prepared without taking into account your individual objectives, financial situation or needs. The information provided is not intended to be a substitute for professional financial product advice and you should determine its appropriateness having regard to your particular circumstances and seek any independent financial or other professional advice you may require. The relevant disclosure document should be obtained from netwealth and considered before deciding whether to acquire, dispose of, or to continue to hold, an investment in any netwealth product.

While all care has been taken in the preparation of this document (using sources believed to be reliable and accurate), no person, including netwealth, or any other member of the netwealth group of companies, accepts responsibility for any loss suffered by any person arising from reliance on this information.

| Netwealth

1. Being a bad trustee

2. Dying without a plan

3. Leaving the country

4. Borrowing blindly

5. Being greedy

The five deadly sins of SMSFs3

The five deadly sins

| Netwealth

Sin No.1Being a bad trustee

The five deadly sins of SMSFs4

| Netwealth

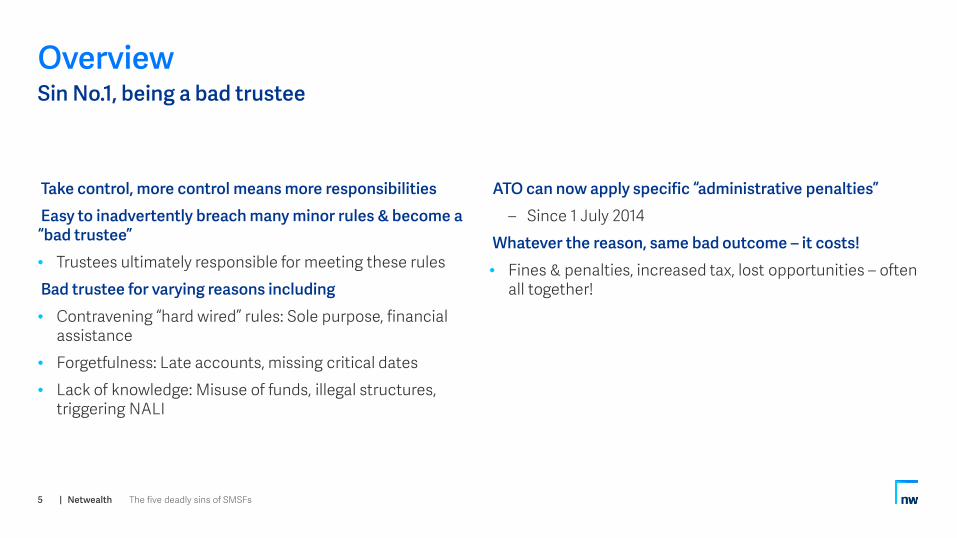

Take control, more control means more responsibilitiesEasy to inadvertently breach many minor rules & become a

“bad trustee” • Trustees ultimately responsible for meeting these rules

Bad trustee for varying reasons including• Contravening “hard wired” rules: Sole purpose, financial

assistance

• Forgetfulness: Late accounts, missing critical dates

• Lack of knowledge: Misuse of funds, illegal structures, triggering NALI

ATO can now apply specific “administrative penalties”– Since 1 July 2014

Whatever the reason, same bad outcome – it costs!• Fines & penalties, increased tax, lost opportunities – often

all together!

The five deadly sins of SMSFs5

OverviewSin No.1, being a bad trustee

| Netwealth

3 regulatory directives and penalties on SMSF trustees • Education – forced education at trustee expense

• Rectification – directed actions to resolve issues (do this or else!)

• Administrative ($) penalties – for specific breaches & payable by trustees

Penalties on each trustee• 60 penalty units ($10,800#) breaching:

– the lending rules

– the borrowing rules, or

– the in-house asset rules

• 20 penalty units ($3,600) for breaching operating standards

• 10 penalty units ($1,800) for:

– not keeping proper minutes and records,

– Fail to inform regulator/keep record of changes in trustees

• 5 penalty units ($900) for non compliance with education direction

# If 4 individual trustees could be $43,200 v 4 members with corporate trustee = $10,800

## Over 70% of SMSFs (and 90% new SMSF established) with individual trustees

The five deadly sins of SMSFs6

For our No.1 sinners…ATO penalties

| Netwealth

DCT V Rodriguez (2016): Fined $40,000 (+ $14,000 costs) for 30 breaches (1)Over a number of years• The Trustee borrowed, repaid & then re-borrowed

• Effectively the SMSF was his personal ATM

• Attempted to disguise some of the borrowings

Caught via an ACR, the ATO & Court identified the following contraventions• s62 (sole purpose)

• s65 (lending) and in-house asset provisions

Relevant factors taken into account by the Court• repetition and consistency of the contraventions

• attempt to disguise some of the borrowings, and the

• Trustee’s awareness of borrowings to be in breach of the SIS Act

The trustee (not the fund) is liable and must pay the fine

(1) Under the Administrative Penalties could have been 30 x $10,800 = $324,000 per trustee

The five deadly sins of SMSFs7

A new benchmark for trustee fines

| Netwealth

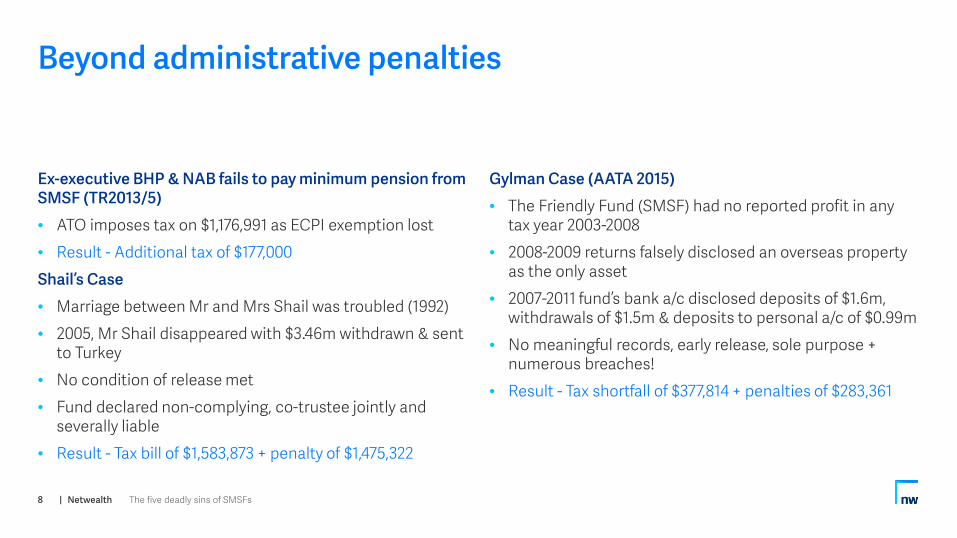

Ex-executive BHP & NAB fails to pay minimum pension from SMSF (TR2013/5)• ATO imposes tax on $1,176,991 as ECPI exemption lost

• Result - Additional tax of $177,000

Shail’s Case• Marriage between Mr and Mrs Shail was troubled (1992)

• 2005, Mr Shail disappeared with $3.46m withdrawn & sent to Turkey

• No condition of release met

• Fund declared non-complying, co-trustee jointly and severally liable

• Result - Tax bill of $1,583,873 + penalty of $1,475,322

Gylman Case (AATA 2015)• The Friendly Fund (SMSF) had no reported profit in any

tax year 2003-2008

• 2008-2009 returns falsely disclosed an overseas property as the only asset

• 2007-2011 fund’s bank a/c disclosed deposits of $1.6m, withdrawals of $1.5m & deposits to personal a/c of $0.99m

• No meaningful records, early release, sole purpose + numerous breaches!

• Result - Tax shortfall of $377,814 + penalties of $283,361

The five deadly sins of SMSFs8

Beyond administrative penalties

| Netwealth

SMSF lose majority of cases against ATO – (SPAA 2016)• … of 32 cases looked at, ATO won 28 of them ….pretty

clear weight is very much in commissioner's hand, … cards very much stacked in the commissioner's favour.”

• Avoid being spotted and confrontation with ATO

Those on ATO radar (Kasey Macfarlane, Assistant Commissioner, SMSF Unit)• individuals with poor personal tax lodgement histories

and no or limited income

• SMSFs with overdue annual returns

• breaches reported in auditor contravention reports that have not been rectified

• SMSFs that have significant changes in assets and income, outside the previous pattern of the fund and without obvious reason

• possible non-commercial related-party investments or transactions

• non-compliance with pension rules

• inappropriate claiming of tax deductions in pension phase

The five deadly sins of SMSFs9

Don’t get on the ATO $@&# list!

| Netwealth

• Be good and be a responsible trustee

• Only do it if you are not going to be sinner no.1

• Always time to repent, ATO can be forgiving

• If you want to be a trustee, be a good one!

• Take advice and avoid being in the spotlight

The five deadly sins of SMSFs10

Final messages for sinner No.1

| Netwealth The five deadly sins of SMSFs11

Sin No.2Dying without a plan

| Netwealth

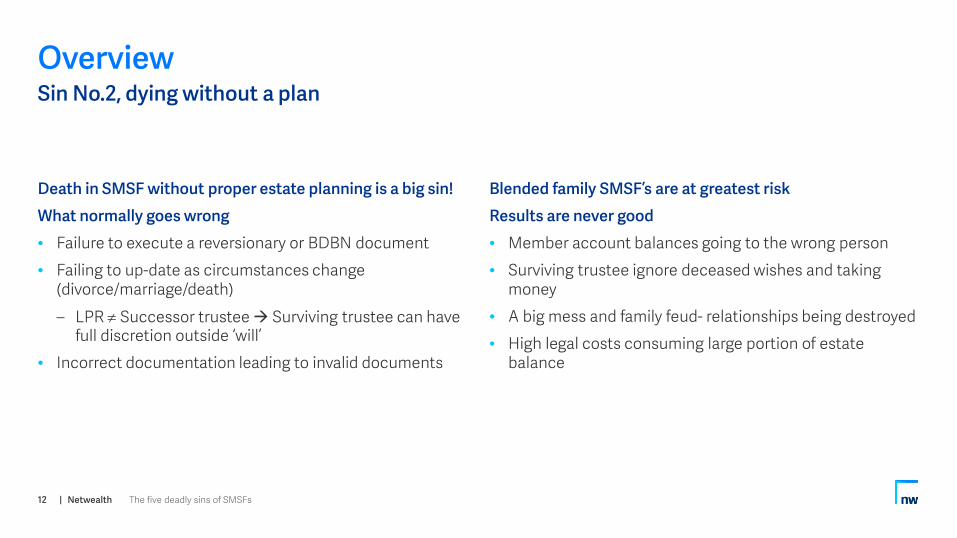

Death in SMSF without proper estate planning is a big sin!What normally goes wrong• Failure to execute a reversionary or BDBN document

• Failing to up-date as circumstances change (divorce/marriage/death)

– LPR ≠ Successor trustee Surviving trustee can have full discretion outside ‘will’

• Incorrect documentation leading to invalid documents

Blended family SMSF’s are at greatest riskResults are never good• Member account balances going to the wrong person

• Surviving trustee ignore deceased wishes and taking money

• A big mess and family feud- relationships being destroyed

• High legal costs consuming large portion of estate balance

The five deadly sins of SMSFs12

OverviewSin No.2, dying without a plan

| Netwealth

Facts of the case• Husband (Augusto) and wife (Francesca), wife passed away

• No binding nomination

• Her will specifies none of her super to go to husband, but to be paid to her kids

• Kids act as executors for her estate

• Individual trustees at date of death

• Augusto resigned as individual trustee and appoint corporate trustee

• Corporate trustee (Augusto) exercise discretion to pay all to himself

The five deadly sins of SMSFs13

Failure to appoint a successor trusteeIoppolo & Hesford v Conti (Supreme Court Australia)

| Netwealth

Issues and court’s findings• Kids as executors brought action against trustee of SMSF

• Kids argued that they have right to be appointed as co trustee of fund

• Court held that although SIS allows appointment of co-trustee, no legal requirement

• Executors argued that trustee did not act in ‘bona fide’ manner

• Court rejected the argument, confirming that trustee if no binding nomination, can apply discretion and entitled to ignore direction of the Will

Important lessons• Non binding nomination is exactly that!

• Need to think careful about binding, non binding and reversionary and implications

The five deadly sins of SMSFs14

Ioppolo & Hesford v Conti (Supreme Court Australia)

| Netwealth

Summary• Mr & (the 2nd) Mrs Morris were only members &

individual trustees

• Mr Morris died Feb 2010, with BDBN in favour of his two daughters from first marriage

• Mrs Morris’ legal advice (poor in hindsight!) said that the BDBN was ineffective

• The trustee (now a corporate trustee with Mrs Morris as the sole director) used discretion to pay all of the deceased’s benefits to (surprise!!) – herself

• Daughters objected saying BDBN was valid – long legal battle followed

• 2013 - SC agreed BDBN valid and ordered payment to daughters + daughters costs to be paid by the Mrs Morris

– BUT Mrs Morris had died prior to judgement & her estate was bankrupt!

• The daughters won BUT there was a $324,000 shortfall + costs & incidentals that unlikely to be recovered from bankrupt estate

• Adding insult to injury – his estate was subject to a separate action and a $1.8m estate had reduced to $200k by the date of the hearing

The five deadly sins of SMSFs15

Legal costs mean you can win but you loseWooster v Morris (2010)

| Netwealth

Summary• Mr Munro, a solicitor, had an SMSF with his (2nd) wife at

time of death

• Exec of his estate - his two biological daughters and Mrs Munro#2.

• After his death, Mrs Munro’s appointed her daughter (not related to Mr Munro) as 2nd t/tee to SMSF

• Mr Munro had made a BDBN for super to go to his Estate (Will) to be split b/w his natural daughters and 2nd Mrs Munro.

• The nominated beneficiary was the “trustee of (the) deceased estate”

• 2nd Mrs Munro argued the BDBN was invalid and trustees (Mrs M#2 & her daughter) decided to pay 100% super to the 2nd Mrs Munro as dependent (by-passed will)

• Mr. Munro’s natural daughters argued the BDBN was valid and should be paid to the executors - to be dealt with by the Will (so they would get their share)

• Court said: The nomination of ‘Trustee of Deceased Estate’ was insufficient to direct the trustee to pay the benefits to Mr Munro’s ‘LPR’, being his executors.

• Result: Natural daughters missed out, deceased wishes not carried out & 2nd wife got everything!

The five deadly sins of SMSFs16

Invalid documents executedMunro v Munro

| Netwealth

• It is a big sin to build up lifetime wealth to lose it on death

• Don’t leave an estate planning mess

• Realise perhaps when your time may be up, and do something

• Be prepared for the inevitable

• Be even more prepared if part of a blended family

• Take advice and avoid dying without a plan!

The five deadly sins of SMSFs17

Final messages for sinner No.2

| Netwealth The five deadly sins of SMSFs18

Sin No.3Leaving the country

| Netwealth

To maintain tax concessions and avoid massive tax penalties an SMSF must be a resident fund at all times during the yearThere are 3 tests that the fund must continuously meet during the year1. Fund established in Australia, or any asset of fund is

situated in Australia at that time; and

2. At that time, the central management and control of the fund is ordinarily in Australia; and

3. At that time either the fund had no active member(#) or at least 50% of:

– the total market value of the fund's assets attributable

to superannuation interests held by active members; or

– the sum of the amounts that would be payable to or in respect of active members if they voluntarily ceased to be members;

is attributable to superannuation interests held by active members who are Australian residents.

# An active member is essential a member who is making, or having contributions – including rollovers - made on their behalf.

The five deadly sins of SMSFs19

OverviewSin No.3, leaving the country

| Netwealth

Test 1 – Established in Australia• Both SMSF & Retail can pass with ease

Test 2 – Central management and control ordinarily in Australia

• SMSF trustees overseas high level decisions o/seas TEST FAILED

– 2 year period is a guideline depending on facts – don’t assume always applicable

• Trustees must show absence is short term/defined in advance/have a passing purpose

• SMSF trustees may be able to delegate/EPoA but give up all control

• Retail trustees in Aust high level decisions in Aust TEST PASSED

• Retail: Member investment decisions continue as normal while overseas

Test 3 – Active member

• SMSF member contributes active member

• If has more than 50% of fund assets TEST FAILED

• Retail: Member contributes while overseas becomes active member

• Retail: Irrelevant as no way overseas member has 50%+ of total fund assets

Retail fund allows overseas member to contribute and manage without fear

The five deadly sins of SMSFs20

Going overseas - SMSF vs RetailWhy an SMSF is at risk when trustees move O/S but a retail fund is not

| Netwealth

Failure of any one of the tests at any time = notice of non-compliancePenalty is very high!• 1st year: (Market Value of Fund assets – non-

concessional) x 47% (Highest MTR)

• Thereafter: Assessable income x 47% (Highest MTR)

CBNP Superannuation Fund v Commissioner of Taxation• Mrs M established an SMSF (Corporate Trustee) and was

the only member

• 6 years later moved to NZ and ceased being an Australian Tax resident

• This was the case for more than 2 years

• Non-residency issue discovered as a result of “in-house asset” contravention

• ATO issued a notice of non-compliance – taxed at 45% -trustees appealed

The court held• Not a resident super fund at all times during the year, as

CMC was not in Australia;

• Mrs M was not 'temporarily absent from Australia'

• It was an SMSF but was not a complying fund, because it was not a resident SF

• ATO discretion not available to a non-resident fund

Assessed on amended taxable income of $302,313 ($136,040 additional tax)

The five deadly sins of SMSFs21

SMSF and overseas nightmares

| Netwealth

• Do not set up SMSF if there is any itch of going overseas

• Could be unforgiveable sin, no amount of confession may be able to help

• If already set up, going overseas requires planning

– Change to small APRA fund

– Wind up and transfer to retail fund

– Have the necessary trusteeship taken over

• Take advice and avoid a very expensive one way ticket

The five deadly sins of SMSFs22

Final messages for sinner No.3

| Netwealth The five deadly sins of SMSFs23

Sin No.4Borrowing blindly

| Netwealth

LRBAs are best suited to SMSF• Provides a number of opportunities to:

– Boost fund asset/performance via gearing;

– By-pass limiting contribution caps

– Greater access to lumpy high value assets – usually real property

BUT, it can go horribly wrong very easily & not easily rectified• Legally complex to structure

• Gearing can be equally powerful on the downside

• Not appropriate for the fund and members

Very high on the ATO “watch list”• The ATO is pursuing a case involving hundreds of

"bungled" LRBAs and clients wrongly advised to invest in property – ATO Director of Super May 2015

The five deadly sins of SMSFs24

OverviewSin No.4, borrowing blindly

| Netwealth

Location A/c from which deposit should come

Can Holding T/tee be incorporated after contract Signed?

Description of purchaser oncontract

Must Bare Trust be signed before purchase contract?

Is an agency agreement required?

NSW SMSF's A/c No <holding T/tee> No NoQLD SMSF's A/c No <holding T/tee> YES YES

VIC

SMSF's A/c YES

<holding t/tee> ATF <trustee of SMSF> ATF <name of SMSF> or <t/tee of SMSF> ATF <name of SMSF> and/or nominee No No

The five deadly sins of SMSFs25

LRBA’s – what could possibly go wrong?An example (different States have different documentation requirements)

Deposit paid by member personally & later characterized as contribution• Property initially in wrong name

• Possible acquisition issues to correct as now being acquired from a member

• If you can correct, possibly 2nd round of stamp duty (CGT?) to transfer to SMSF

| Netwealth

Changing legislation – e.g. related party loan arrangements interpretation • PCG 2016/5 – LRBA Safe Harbour Guidelines

• Need to unwind prematurely

• Need to restructure

• Income received treated as NALI (Non Arms Length Income)

– NALI taxed at highest MTR

• Possible unintended tax and stamp duty consequences

Incorrect structure – e.g. not a bare trust / multiple assets• At best – costly legal advise to correct

• Most likely – forced to prematurely unwind arrangement with uncertain consequences

• At worst – forced to unwind, additional stamp duty, unplanned CGT & ATO fines

The five deadly sins of SMSFs26

LRBA’s – more that could possibly go wrong

| Netwealth

Not understanding the key principals – e.g. single asset/ same asset rules• Building on vacant land = different asset = breach

• Undertake property development (strata title a big block) = breach

• Buy different shares under single LRBA = multiple assets = breach

• Buy single company (BHP) & need to sell some = different asset = breach

Death with large single asset• Reduced contributions = inadequate cash flow to

continue LRBA = forced early sale;

• Forced early sale to pay benefits to deceased beneficiaries

– May be able to postpone problem by paying income stream to beneficiaries

• Cross insurance no longer allowed to cover debt on premature death

The five deadly sins of SMSFs27

LRBA’s – even more that could possibly go wrong

| Netwealth

• Only for those who understand gearing

– Fit the right risk profile to borrow

• If get it wrong, costly to unwind

• Specialist professional legal advice all the way

– Get it right first time

• Take advice and avoid costly borrowing!

The five deadly sins of SMSFs28

Final messages for sinner No.4

| Netwealth The five deadly sins of SMSFs29

Sin No.5Don’t be greedy!

| Netwealth

Yes it’s your money BUT just not yet!!Tempted to use SMSF for other purposes that may be within letter of the law but not in the spirit of the lawThe ATO has regularly taken a narrower interpretation to stop such practicesExamples could include• Loan to related company

• Personal use assets

• Early release of benefits

Such arrangements can fail at many different levels• Specific sections of the law

• General provisions – “Sole purpose test”

• Related legislation provisions – Part IVA

The five deadly sins of SMSFs30

OverviewSin No.5, don’t be greedy!

| Netwealth

Loans to members and related party • SISA S65: (1) A trustee … of a regulated superannuation

fund must not lend or give financial assistance to a member or a relative of a member of a fund;

• Does not say that a SMSF cannot lend to a company!

R Ali Super Fund (SMSF) v Commissioner of Taxation• Trustee lent money to a company that then on lent the

money to members of the fund and businesses controlled by the trustees

• Technically not in breach of sec 65 as money lent to a company

CoT declared the SMSF non-complying• Breach of Sec 65 - money lent to the company was

immediately on lent to members the ATO “looked through” the company to ultimate use/reason for the arrangements and deemed it financial assistance;

• Other related breaches included:

– S62 Sole purpose; S84 in-house asset limit; s109 dealing at arms length.

The five deadly sins of SMSFs31

Don’t lend to members

| Netwealth

Personal use assets (SISA 62A & SISR 13.18AA)• SMSF are not prohibited form holding collectables and personal use assets BUT very strict guidelines apply

• Trustee’s applying a wider/different interpretation can lead to trouble:

– 13.18AA(3) - prohibits SMSF trustees from storing collectables and personal use assets in the private residence of related parties

– What about storing them in a related party business premises – hang paintings on the boardroom wall all properly insured, alarmed, climate controlled etc.?

ATO’s interpretation• You can store (but not display) in premises owned by a related party that is not their private residence - artwork can’t be

hung where it is visible to clients and employees.

The five deadly sins of SMSFs32

Don’t enjoy your personal assets

| Netwealth

Early release of member benefits is illegal Must meet a condition of release before accessing your super• Few exceptions with strict conditions & small amounts (Financial Hardship/Compassionate)

Heavy penalties apply to members & trustees & promoters (includes financial planners)• No deduction for any fee/commission a promoter takes from your super

• Illegally accessed super is included in your taxable income, even if returned to fund

• SMSF trustees can also incur higher taxes, additional penalties, & disqualification

• Trustees may also incur a fine of up to $340,000 and a jail term of up to five years or fines of up to $1.1 million for corporate trustees

• Promoters face civil & criminal penalties with some already jailed

The five deadly sins of SMSFs33

Don’t get your money early

| Netwealth

Facts• Vuong, aged 49 & a member of the Equipsuper fund

• Vuong met Phuong who said he could be paid his super early subject to a 29% fee

• Vuong signed blank form and roll-over to Nguyen SMSF

• Equipsuper paid $114,697 by cheque to Nguyen SMSF (fraudulently used by Phuong)

• Vuong subsequently received $81,434 in a series of payments ($114,697 net of fee)

• Vuong ran this past his tax agent in relation to the preparation of his FY2009 tax return who ‘smelled a rat’ saying it was improbable it would be super

In July 2011, the ATO undertook an auditResult was that the ATO imposed• $45,300 primary tax on total $114,697 withdrawal

• $11,325 fine being a 25% administrative penalty (Later remitted by AAT on appeal)

• $2,900 in shortfall interest charge (Later remitted by AAT on appeal)

The five deadly sins of SMSFs34

A greedy sinnerVuong and FCT

| Netwealth

• There is a price for tax concessions

• Got to do your time

• If you are easily tempted, don’t have one

• Take advice and avoid being a sinner

The five deadly sins of SMSFs35

Final messages for sinner No.5

Contact

Thank you

Keat ChewHead of Technical Services1800 555 [email protected]

Nigel SmithTechnical Services Consultant1800 555 [email protected]

| Netwealth The five deadly sins of SMSFs37

Disclaimer

This information has been prepared and issued by Netwealth Investments Limited (netwealth), ABN 85 090 569 109, AFSL 230975, RSEL0000192). It contains factual information and general financial product advice only and has been prepared without taking into account your individual objectives, financial situation or needs. The information provided is not intended to be a substitute for professional financial product advice and you should determine its appropriateness having regard to your particular circumstances and seek any independent financial or other professional advice you may require. The relevant disclosure document should be obtained from netwealth and considered before deciding whether to acquire, dispose of, or to continue to hold, an investment in any netwealth product.

While all care has been taken in the preparation of this document (using sources believed to be reliable and accurate), no person, including netwealth, or any other member of the netwealth group of companies, accepts responsibility for any loss suffered by any person arising from reliance on this information.