neuland labs limited

TRANSCRIPT

RC Capital Management is an Investment Advisory Firm specializing in identifying and investing in high quality companies that trade at a substantial discount to our conservative estimates of Intrinsic Value.

This report is a compilation of our analysis of Financial / Business performance “Neuland Labs Limited” from an investment perspective The report is meant for subscribers of RC Capital Management Investment Advisory only. Unauthorized circulation of this report is prohibited

RC Capital Management is a SEBI Registered Investment Advisor

Registration Number – INA000004088

RC Capital Management Neuland Labs Limited

Page. 1 www.rccapitalmanagement.com Confidential

Company Analysis: Neuland Labs Limited

Posted on 19th May 2021

About

The company was established in 1994 as an API manufacturer by Dr. Davuluri Rama Mohan Rao. The company started business in generic APIs such as Ciproflaxin which are commodity in nature and have low margins. Over the years, it developed capabilities in niche/ complex API such as Levetiracetam, Mirtazapine, Salmeterol and Salbutamol which have lower competition and higher margins

The following slide from the investor presentation gives a good overview of the GDS (API) business

The GDS division produces API for customers and has two sub-segments. The prime segment produces mature APIs which have higher competition. The other sub-segment, called the specialty segment produces APIs with complex processes (and are niche in nature).

The prime segment is a high volume, lower margin business. In the prime segment, the company is focused on process optimization and yields for select molecules to establish a leadership position in these molecules and thus earn an above average ROC.

RC Capital Management Neuland Labs Limited

Page. 2 www.rccapitalmanagement.com Confidential

The specialty segment involves high end complex chemistry skills and R&D support. This involves niche molecules with specialized skills and higher margins. At the same time, the volume per molecule is much lower than the prime segment

In 2013, the company refocused their business towards niche API and the Custom manufacturing business. These two businesses have grown since then and are scaling up.

The CMS segment is summarized below

The CMS segment is the custom manufacturing business which produces APIs to customer’s specifications. The CMS segment has scaled from around 50 Crs in 2014 to 270 crs in FY21. This segment has much higher margins and ROC due to the long gestation period and stickiness of customers (similar to the CRAMs business of PI industries and Laurus labs)

Industry review and Competitive analysis:

The evolution of the company and its business model is similar to Laurus labs. Of course, the product range and the trajectory is different. Laurus labs is a 4800 Cr revenue company with substantial scale in the ARV product range.

Neuland labs has started growing, but has yet to hit a similar scale of operations

RC Capital Management Neuland Labs Limited

Page. 3 www.rccapitalmanagement.com Confidential

Financials

The company reported a revenue of 953 Crs and net profit of 80 Crs for FY21. The company grew its topline by 24.3%, operating profit by 54.3% and net profit by 405%. Operating margin improved from 13.7% to 17.1% during this period. The company improved its ROC to 15.1%

The company generated an operating cash flow of 189.4 Crs which was invested in capex of 105 Crs and the rest was used to pay down debt

The company has grown its topline from 223 Crs in FY08 to 953 Crs in the current fiscal at 12% CAGR. This growth was initially driven by APIs which is a low return business. The company pivoted to high value API and CMS in 2013 which led to an improvement in operating margin to 15-18% till 2017

The company has had patchy performance in the past few years due to various issues. Management’s efforts in the specialty and CMS segments started bearing fruit by 2017 when it was hit by RM supply issues from china. At the same time, the CMS segment also saw a drop in topline due to the lumpy nature of contracts.

The company has since then reduced import dependence on china from 40% to around 10% this year. In addition to that, the CMS business has a much bigger pipeline and scale due to which the volatility in performance has reduced (though not eliminated)

The topline has been growing since 2019 and operating margins which bottomed out at 9% in 2019, has improved to 17% for the year

Positives

The company started life as an API manufacturer in the mid-80s when it was founded by the Chairman Dr. Davuluri Rama Mohan Rao. Sucheth and Saharsh Davuluri, who are his sons joined the business in mid 2000s. Both the sons are engineers and MBA and have experience in other companies too. They were inducted into the company in operational roles and have since then taken over the day to day management of the company.

The company started pivoting to niche API and CMS business in 2013. Both segments are complex businesses with high entry barriers. Niche API products are complex products which require specialized skills, are difficult to produce and need a high level of compliance. As a result, these products have few manufacturers globally with few Chinese producers. This allows companies such as Neuland to charge higher margins than commodity APIs

The CMS/CRAMS business is similar to that of PI industries or Laurus labs. The company provides custom manufacturing services for niche API during research, development and finally

RC Capital Management Neuland Labs Limited

Page. 4 www.rccapitalmanagement.com Confidential

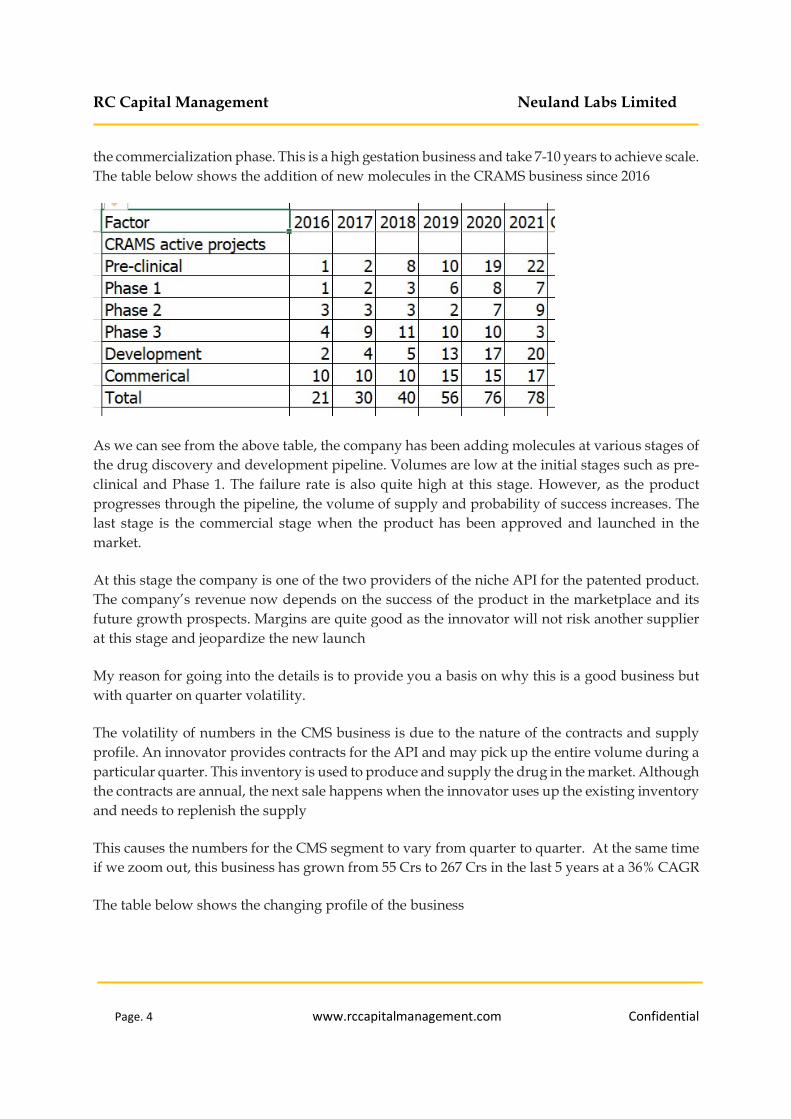

the commercialization phase. This is a high gestation business and take 7-10 years to achieve scale. The table below shows the addition of new molecules in the CRAMS business since 2016

As we can see from the above table, the company has been adding molecules at various stages of the drug discovery and development pipeline. Volumes are low at the initial stages such as pre-clinical and Phase 1. The failure rate is also quite high at this stage. However, as the product progresses through the pipeline, the volume of supply and probability of success increases. The last stage is the commercial stage when the product has been approved and launched in the market.

At this stage the company is one of the two providers of the niche API for the patented product. The company’s revenue now depends on the success of the product in the marketplace and its future growth prospects. Margins are quite good as the innovator will not risk another supplier at this stage and jeopardize the new launch

My reason for going into the details is to provide you a basis on why this is a good business but with quarter on quarter volatility.

The volatility of numbers in the CMS business is due to the nature of the contracts and supply profile. An innovator provides contracts for the API and may pick up the entire volume during a particular quarter. This inventory is used to produce and supply the drug in the market. Although the contracts are annual, the next sale happens when the innovator uses up the existing inventory and needs to replenish the supply

This causes the numbers for the CMS segment to vary from quarter to quarter. At the same time if we zoom out, this business has grown from 55 Crs to 267 Crs in the last 5 years at a 36% CAGR

The table below shows the changing profile of the business

RC Capital Management Neuland Labs Limited

Page. 5 www.rccapitalmanagement.com Confidential

The high margin/high ROC business of Niche API and CMS have increased from 40% to 50% in contribution to the topline

As we discussed in the Laurus labs analysis, the numbers for the company have been suppressed in the last few years as the company has investing 5-7% in R&D for these high margin businesses. The company has also invested 270 Crs in a new manufacturing unit (unit III) which has been operationalized recently

These investments in R&D and manufacturing, such as manpower and overheads, are being passed through the P&L which has suppressed the operating margin. As these businesses scale, we should see an improvement in the margins and ROC numbers

Finally, there is a large optionality built into the business – namely peptides drugs. The company has been investing in this complex and niche space for last 10 years and could launch 1/2 products in the next 1-2 years. These are highly complex and high margin products. The company plans to use these capabilities in the GDS segment to manufacture APIs and in the CMS segment to offer these services to customers

Risks

The top risk faced by the company is Audit risk. The company has been focused on managing quality and clearing regulatory audits. The company has cleared all the FDA audits till date (15 audits) including two audits last year.

The second risk for the company is the commoditization risk / price competition for its products (Prime API in this case). I personally think this is not a risk for pharma companies. Price competition and pricing pressure is a fact of life in competitive and commodity type business such as Generics.

Generics are not as commoditized as steel or sugar, but the high competitive intensity means that there will always be pricing pressure on generic products. Companies such as Neuland labs are dealing with these pressures by achieving cost leadership in the generic API and expanding into niche API which have lower competition due to entry barriers

RC Capital Management Neuland Labs Limited

Page. 6 www.rccapitalmanagement.com Confidential

The next risk for the company is key man risk. I think this has been mitigated as the two sons of the Chairman have been running the Business for the last 10+ years and are now the face of the company

The final risk is execution of business plans by the management. Till date, execution has been good but sometimes patchy. If we dig deeper, it becomes clear that when a particular problem or risk such as RM shortage from china surfaced, management was transparent about it and persistent in solving the issue

Management quality checklist

Management compensation: appears reasonable

Capital allocation record: Management has invested into niche API and CMS business. Although these are high ROC businesses, we are yet to see the full result of these investments. Management is also using excess cash flow to reduce debt and thus de-risk the balance sheet

Shareholder communication: Adequate. Annual report has sufficient details and management shares updates via quarterly reports and conference calls

Accounting practice: Appears conservative

Related party transactions: nothing concerning for now

Scenario analysis

It is crucial to understand that valuation of a company is based on which scenario plays out in the future. Although we put a single number for intrinsic value which matches the high probability scenario, it is not a given that this is the only scenario which will play out.

Scenario 1 involves a topline growth of around 20% due to above average growth in the prime API and CMS segment. The company improves margins from 17-21% levels. As I have shared earlier, most API companies at scale have 18-22% operating margins. The CMS business has

RC Capital Management Neuland Labs Limited

Page. 7 www.rccapitalmanagement.com Confidential

higher margins than the API business and hence the company should be able to achieve these margins at scale

Scenario 2 is a pessimistic scenario. The company misses its topline targets completely due to FDA compliance issues, inability to scale up unit III and slower CMS growth in single digits. Operating margins remain at the current levels and valuations drop as a result

Scenario 3 is the best-case scenario. Topline more than doubles as the Prime and GDS businesses scale at unit 3. Due to the economies of scale and normalization of overheads and Manpower costs (which are being incurred in advance ), operating margins reach the industry average of similar businesses – 30%. Valuation reflects the high ROC and growth numbers of the company

The Market cap numbers represent the range of value for the company depending on which scenario plays out. As the results come in, we will know which scenario is playing out and will adjust accordingly

Another notable point – Listed CRO/CMS businesses sell for around 10 times sales. If we take that metric, the entire market cap for Neuland labs is accounted by the CMS division. However, this segment has yet to achieve scale and hence we cannot consider such a high valuation for now. If management continues to scale this segment as planned, we can expect the market to adjust the valuations accordingly

Conclusion

This position is part of the pharma basket as shared earlier here. I shared the thesis for this basket at that point of time. Neuland labs has benefits of the same tailwinds in the Industry and seems to be positioned to take advantage of them. It has multiple growth drivers in the form of growth in the API – specialty segment and scaling up of the CMS segment

We started the Pharma basket with three companies – Laurus Labs, Alembic pharma and Biocon ltd. We have exited Alembic Pharma and Biocon ltd at roughly break even and Laurus labs is up 2.5X since the purchase. We have replaced these positions with Neuland labs. We created the pharma basket to take advantage of the tailwinds in the sector. I shared last year that if companies in the basket do not perform as per expectations, we will exit them and not agonize over the decision. We have followed that thinking

Neuland labs has good growth prospects, but as I shared in the earlier section, numbers will be lumpy due to the CMS business. This happened in the recent quarter and will recur in the future till the CMS business has a large base of clients and molecules. This lumpiness in the numbers could cause the stock price to swing from quarter to quarter

In the recent quarter, growth appeared to slow down due to a drop in the CMS revenue on a q-o-q basis (though it grew on a y-o-y basis). This will happen again in the future. As long as the

RC Capital Management Neuland Labs Limited

Page. 8 www.rccapitalmanagement.com Confidential

company is adding new products in the API segment and projects to the CMS segment, the long-term thesis remains intact

There is no change to fair price, buy price and position size in the model portfolio

RC Capital Management Neuland Labs Limited

Page. 9 www.rccapitalmanagement.com Confidential

Q1- 2022 Results Analysis

Posted on 5th August 2021

The company reported a 2.5% drop in the topline and 43% drop in profits. Gross margin expanded during the quarter due to higher contribution from CMS and specialty products

Topline dropped as there was a delay in some projects in the pipeline due to which the company was not able to bill/ship to the customer. In addition to that, there was some level of destocking at the customer level in the GDS segment, due to which the numbers were flat.

The company is operationalizing unit III due to which it is incurring higher manpower and operative expenses without a contribution to the topline. This has resulted in negative operating leverage penalizing the current quarter profits

Market reaction

This is a small cap stock and it has been stuck on the lower circuit since the announcement of the result. I had written about the following risk in the company note

The final risk is execution of business plans by the management. Till date, execution has been good but sometimes patchy. If we dig deeper, it becomes clear that when a particular problem or risk such as RM shortage from china surfaced, management was transparent about it and persistent in solving the issue

And described this as a probable scenario

Scenario 2 is a pessimistic scenario. The company misses its topline targets completely due to FDA compliance issues, inability to scale up unit III and slower CMS growth in single digits. Operating margins remain at the current levels and valuations drop as a result

When I share a downside scenario in the analysis, it may appear hypothetical in nature, but can play out. It is important to be aware of them so that we can manage the risk in the position

The market had high expectation from the company due to which the stock was up 5X in the last one year. The last two quarter results have disappointed the market and it is now extrapolating the current problems as permanent

Plan of action

Let me share my view point and action plan on the position

RC Capital Management Neuland Labs Limited

Page. 10 www.rccapitalmanagement.com Confidential

Management repeatedly mentioned that the current delays are temporary in nature and the company is adding new projects in the development and commercial stage of the GDS and CMS business. There is no drop in the demand or pipeline of its products

The company expects to catch up on the performance in the coming quarters and is still on target for the year

In the CMS business, results are often lumpy (till it reaches scale) and projects do face unexpected delays especially if there is complex, multi-step chemistry involved in it. As a result, I am inclined to trust the management.

That said, I have been burnt several times in the past on taking management speak on face value. Neuland labs does have a history of patchy execution and these delays could continue for longer.

As result we are putting the position on hold for now

We will wait for the management to start delivering as per plans, before a change in our stance

If you have not started a position, please do not do so now. For the rest, I am in the same boat as you. As I noted in this update for Neuland labs, we will buy with you and exit with you. We continue to hold the position.

At a personal level, I am still optimistic that management will fix the issues and deliver better performance. However, the timing is uncertain, and I don’t want to put any more capital at risk to be proven right.

Copyright © R C Capital Management. All rights reserved.

RC Capital Management is a partnership firm registered with SEBI as an Investment Adviser

(Registration no. INA000004088). This should not be considered as an offer to buy or sell any securities.

RC Capital Management and its partners and associates will not be liable or responsible for any direct

or indirect loss or liability incurred to any user on account of actions taken or decisions made by the

user based of the information, views and analysis provided in this newsletter. Past performance does

not guarantee future results. The information and data mentioned herein are from reliable source, but

RC Capital Management does not warrant its completeness and accuracy. This information is made

available for personal and non-commercial use only. Use of the information is at user’s own risk. Any

act of copying, reproducing or distributing this newsletter, whether wholly or in part, for any purpose

without the permission of RC Capital Management is strictly prohibited and will be considered as

RC Capital Management Neuland Labs Limited

Page. 11 www.rccapitalmanagement.com Confidential

copyright infringement. As a condition to accessing the contents of this newsletter, you agree to the

terms of use of the website.

RC Capital Management – SEBI registered Investment Advisor

Type of Registration: Non-Individual Reg. No. : INA000004088, Valid till : Perpetual

Address: B-101, Chinar Soc., Behind Subway, Kothrud, Pune-411038 / +918806058625

Principal Officer – Rohit Chauhan ( 91-8806058625 / [email protected])

Corresponding SEBI Regional Office – SEBI Bhavan BKC, Plot No.C4-A, ‘G’ Block, Bandra-Kurla Complex, Bandra (East), Mumbai – 400051