new and future business models for energy utilities

TRANSCRIPT

© 2015 Frost & Sullivan. All rights reserved. This document contains highly confidential information and is the sole property of

Frost & Sullivan. No part of it may be circulated, quoted, copied or otherwise reproduced without the written approval of Frost & Sullivan.

New and Future Business Models forEnergy Utilities

Thomas Houareau, Consulting Director

Energy & Environment

1 July 2015

2

Now Available On Demand

Listen On Demand

https://www.brighttalk.com/webcast/5563/160745

Or

www.frost.com/ab

Today’s Presenter

• Over 10 years with Frost & Sullivan in Energy & Environment and related

industries

• Leader in more than 70 consulting engagements in the power generation and

transmission sector

• Extensive track record working with leading power utilities and global power

equipment manufacturers

Thomas Houareau, Director, Frost & Sullivan

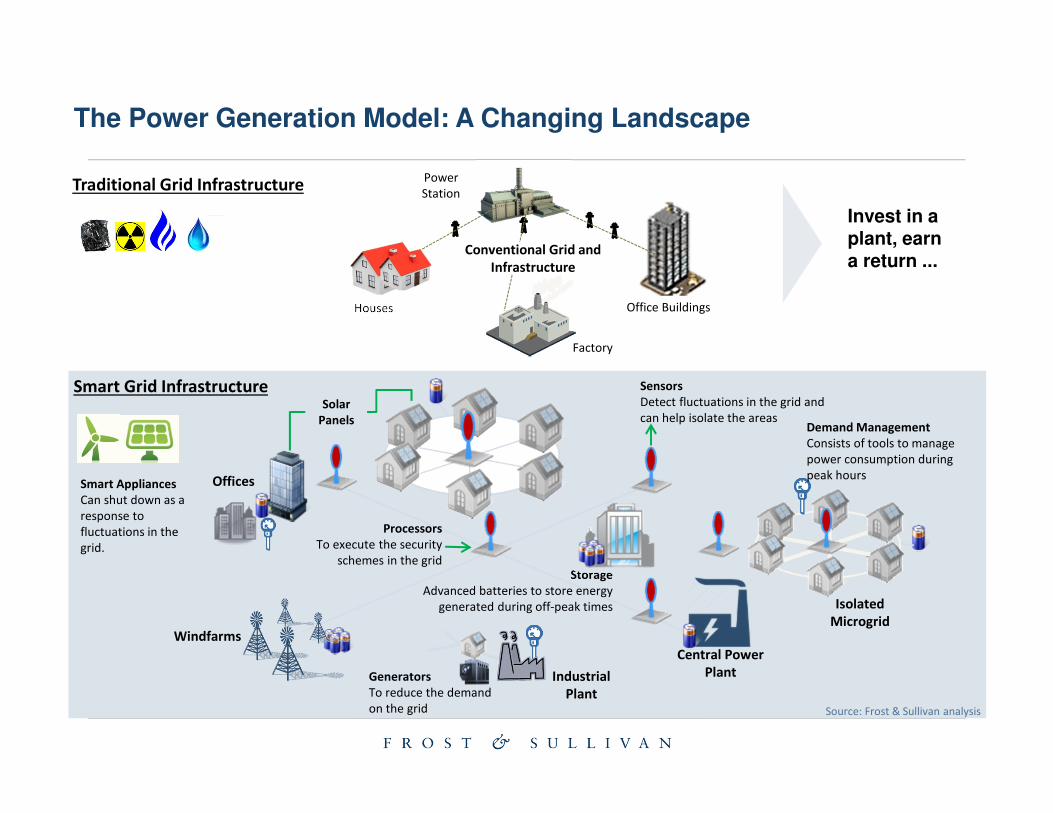

The Power Generation Model: A Changing Landscape

Traditional Grid Infrastructure

Smart Grid Infrastructure

Offices

Isolated

Microgrid

Central Power

PlantIndustrial

Plant

Windfarms

Storage

Advanced batteries to store energy

generated during off-peak times

Sensors

Detect fluctuations in the grid and

can help isolate the areasDemand Management

Consists of tools to manage

power consumption during

peak hours

Generators

To reduce the demand

on the grid

Solar

Panels

Processors

To execute the security

schemes in the grid

Smart Appliances

Can shut down as a

response to

fluctuations in the

grid.

Source: Frost & Sullivan analysis

Power

Station

Houses Office Buildings

Conventional Grid and

Infrastructure

Factory

Invest in a plant, earn a return ...

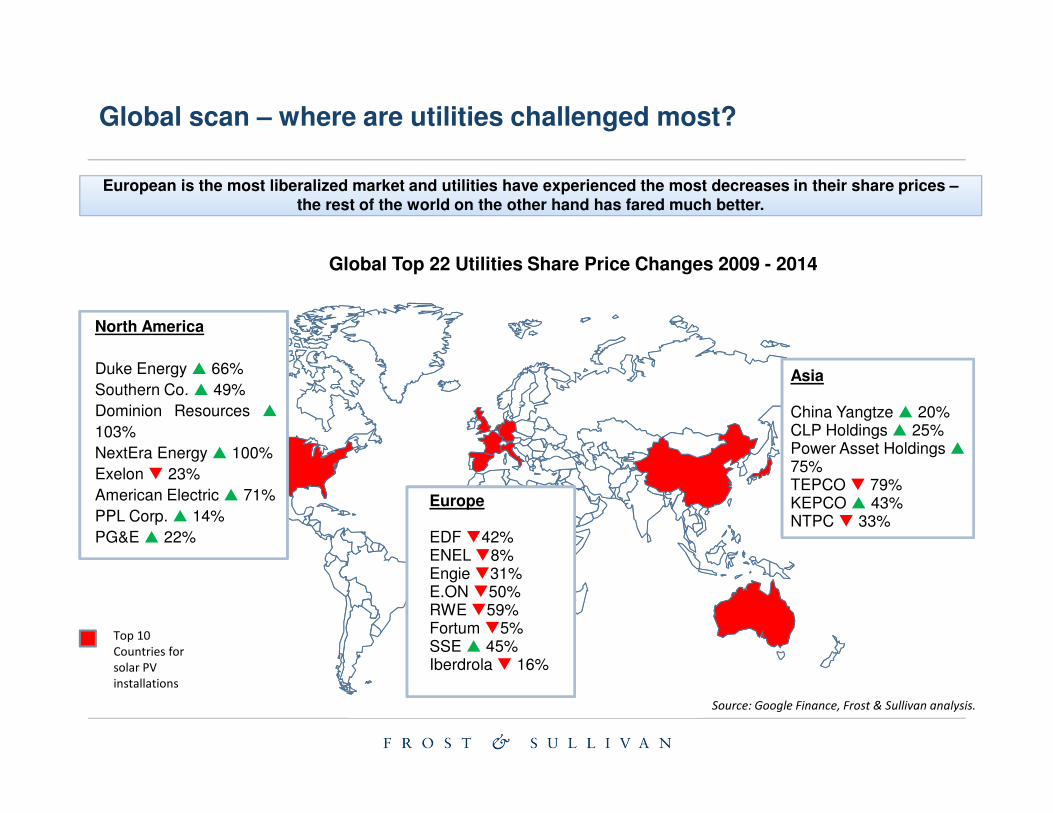

Global scan – where are utilities challenged most?

Source: Google Finance, Frost & Sullivan analysis.

Europe

EDF �42%ENEL �8%Engie �31%E.ON �50%RWE �59%Fortum �5%SSE � 45%Iberdrola � 16%

North America

Duke Energy � 66%

Southern Co. � 49%

Dominion Resources �

103%

NextEra Energy � 100%

Exelon � 23%

American Electric � 71%

PPL Corp. � 14%

PG&E � 22%

Asia

China Yangtze � 20%CLP Holdings � 25%Power Asset Holdings �75%TEPCO � 79%KEPCO � 43%NTPC � 33%

European is the most liberalized market and utilities have experienced the most decreases in their share prices –the rest of the world on the other hand has fared much better.

Global Top 22 Utilities Share Price Changes 2009 - 2014

Top 10

Countries for

solar PV

installations

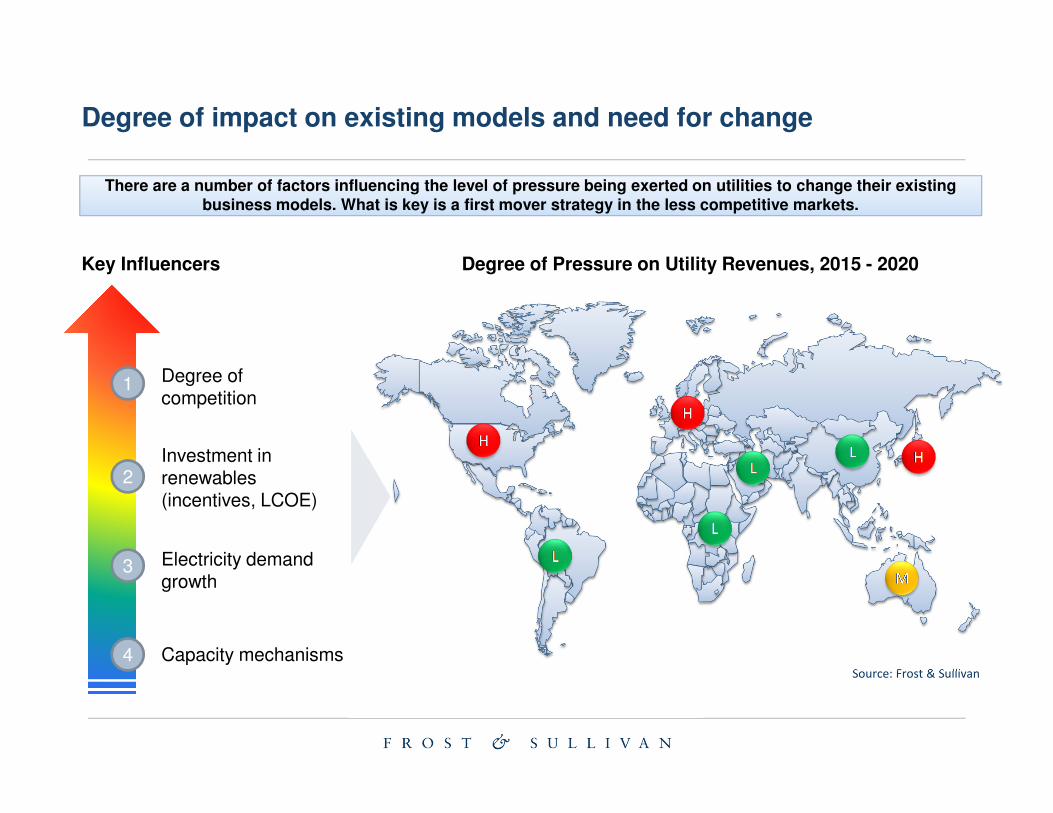

Degree of impact on existing models and need for change

Source: Frost & Sullivan

There are a number of factors influencing the level of pressure being exerted on utilities to change their existing business models. What is key is a first mover strategy in the less competitive markets.

Degree of Pressure on Utility Revenues, 2015 - 2020

Degree of competition

Investment in renewables (incentives, LCOE)

Electricity demand growth

1

2

3

Key Influencers

Capacity mechanisms4

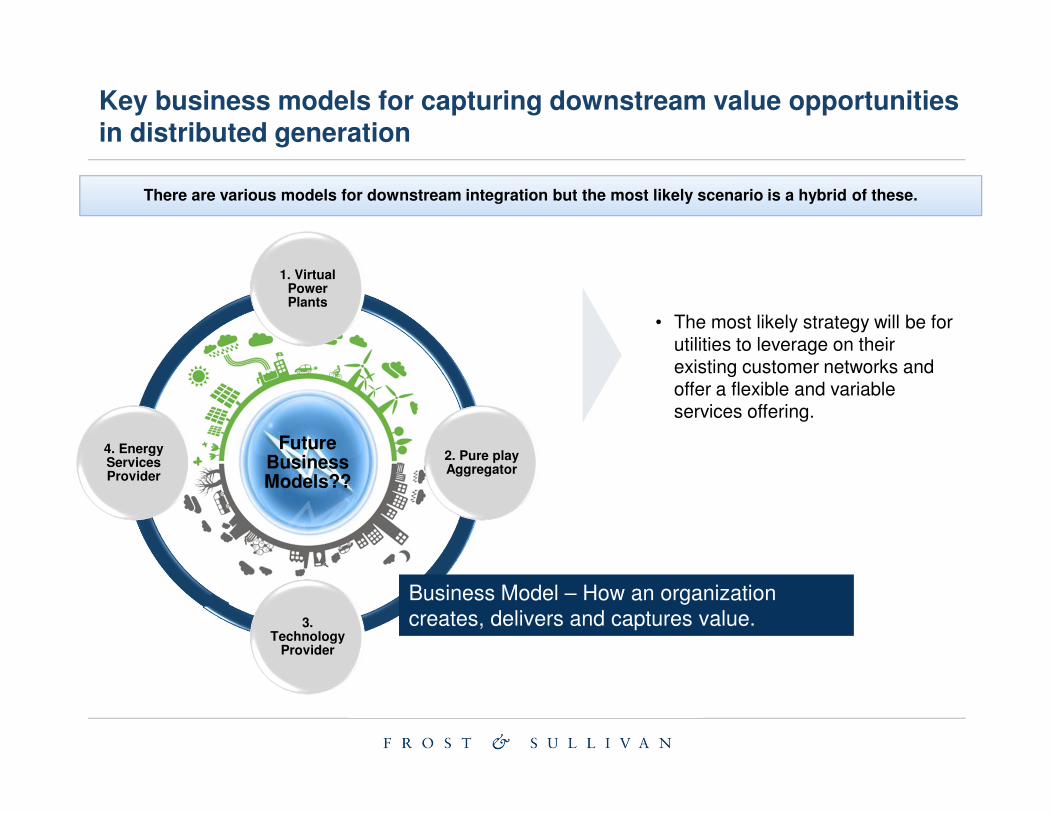

Future Business Models??

1. Virtual Power Plants

2. Pure play Aggregator

3. Technology

Provider

4. Energy Services Provider

Key business models for capturing downstream value opportunities in distributed generation

• The most likely strategy will be for utilities to leverage on their existing customer networks and offer a flexible and variable services offering.

There are various models for downstream integration but the most likely scenario is a hybrid of these.

Business Model – How an organization

creates, delivers and captures value.

8

http://twitter.com/frost_sullivan

Follow Frost & Sullivan on Facebook, LinkedIn, SlideShare, and Twitter

http://www.facebook.com/FrostandSullivan

https://www.linkedin.com/groups/Future-Energy-4727266

http://www.slideshare.net/FrostandSullivan

9

For Additional Information

Chiara Carella

Head of Corporate Communications

Europe, Israel and Africa

+44 (0) 207 343 8314

Cyril Cromier

Vice President - Sales

Energy & Environment

+33 1 42 81 22 44

Thomas Houareau

Director

Energy and Environment

+44 (0)20 7343 8329