new fasab technical guidance for environmental … fasab technical guidance for environmental...

TRANSCRIPT

New FASAB Technical Guidance for

Environmental Liabilities Reporting

Patricia Huheey

ODUSD(I&E)/EM

June 14, 2010

Department of Defense

Report Documentation Page Form ApprovedOMB No. 0704-0188

Public reporting burden for the collection of information is estimated to average 1 hour per response, including the time for reviewing instructions, searching existing data sources, gathering andmaintaining the data needed, and completing and reviewing the collection of information. Send comments regarding this burden estimate or any other aspect of this collection of information,including suggestions for reducing this burden, to Washington Headquarters Services, Directorate for Information Operations and Reports, 1215 Jefferson Davis Highway, Suite 1204, ArlingtonVA 22202-4302. Respondents should be aware that notwithstanding any other provision of law, no person shall be subject to a penalty for failing to comply with a collection of information if itdoes not display a currently valid OMB control number.

1. REPORT DATE 14 JUN 2010 2. REPORT TYPE

3. DATES COVERED 00-00-2010 to 00-00-2010

4. TITLE AND SUBTITLE New FASAB Technical Guidance for Environmental Liabilities Reporting

5a. CONTRACT NUMBER

5b. GRANT NUMBER

5c. PROGRAM ELEMENT NUMBER

6. AUTHOR(S) 5d. PROJECT NUMBER

5e. TASK NUMBER

5f. WORK UNIT NUMBER

7. PERFORMING ORGANIZATION NAME(S) AND ADDRESS(ES) Office of the Deputy Under Secretary of Defense (Installations &Environment),ODUSD(I&E)/EM,3400 Defense Pentagon, Room 3B856A,Washington,DC,20301-3400

8. PERFORMING ORGANIZATIONREPORT NUMBER

9. SPONSORING/MONITORING AGENCY NAME(S) AND ADDRESS(ES) 10. SPONSOR/MONITOR’S ACRONYM(S)

11. SPONSOR/MONITOR’S REPORT NUMBER(S)

12. DISTRIBUTION/AVAILABILITY STATEMENT Approved for public release; distribution unlimited

13. SUPPLEMENTARY NOTES Presented at the NDIA Environment, Energy Security & Sustainability (E2S2) Symposium & Exhibitionheld 14-17 June 2010 in Denver, CO.

14. ABSTRACT

15. SUBJECT TERMS

16. SECURITY CLASSIFICATION OF: 17. LIMITATION OF ABSTRACT Same as

Report (SAR)

18. NUMBEROF PAGES

21

19a. NAME OFRESPONSIBLE PERSON

a. REPORT unclassified

b. ABSTRACT unclassified

c. THIS PAGE unclassified

Standard Form 298 (Rev. 8-98) Prescribed by ANSI Std Z39-18

Acquisition, Technology and Logistics

Agenda

• Environmental Closure Liabilities

– What are they?

– What are the standards?

• FASAB AAPC PP&E Disposals Task Force

• TR 11 - AAPC Implementation Guidance for

Cleanup Costs Associated with Equipment

• EL vs Ongoing operations

• Asbestos TB 2006/9 – 1 Requirements

• Implementation Issues

• TR 10 - AAPC Implementation Guidance on

Asbestos Cleanup Costs

Acquisition, Technology and Logistics

Today’s Topic is Closure Liabilities

Note 14. Environmental Liabilities and Disposal Liabilities

E:n..n.-onrnental Liabi lities and Dispos.al Liabilities Dottars m 1.4J]Iions I

1 A.5MS~30

I Envi.-onmenul Uabilit ies-Nonfed-al I 200r9 2008

Acc r ued Envi ronn1ental Resto•atio n Liabililii e-s

Acfilo'e ln sta la1fon s-lnstallafion Resfo~a1ion Program ( IRP) .and B uilding Demolffion .and Debris Removal ( BDIO R ) $ 7 . 957.4 $ 8 . 873.5

Acfio,oe ln stalla1fons.-M ilifa.r:,o M u n itions Respon se Program (MM R P ) 5.223.5 5 . 035.1

Former l:,o U sed [)efense S ites-IR P & B DJD R 3.452.9 3 .233.2

F o rme.-l:,o Used Defense S ites - M M.RP 1 3, 545 .9 14 . 859 .0

Oth .e.- Accrued E n v i ro:n m.e n,tal ILia b i l iti es-No n>-BRAC

.:::·. ~ - "' ., .. ., <> 0.1 .,. .C>

Em.rfT I Closure Rec-u~em.enfs 2 . 193.7 1 _868. 1

Enviromnenfa~ Response at Oper.afion.al R a nges 1 6 4 .0 204 .1'

A sbestos 1.183.3 42s.e

Non-M ilitary Eq lrlp:ment 1 14 .4 8 9.2

I.J[rer 1 .,£..<:.0::.~ . n ~ . ...: Base Riealig:n m;ent and C l·o sure Inst a ll a-ti o n s (BRAC)

Installation R es1oration P\rogr.am 3 . 684.7 3 . 772 .6

M :ili la.r:,o M unitions Respon se Prog;ram 1.0 6 3 .6 1 . 075.0

Environm~ental Corrective A ct ion I C lo s u re !Requirements 34 4-.0 372.8 IE n vironm e n·lal D ispo-sa.ll f o r M ilita ry E q uipmen t I Weapon s P r ogram s

N u c le a:r P o ·t.--ered M i lltary !Equipment I S pen t N uclear e=u e l 1 2,672.4 12.255.7

I Non>-N u c lea:r PowerediiMilltary Eq;uip ment 36.4 39.1

O ther N a t ional D e f en se ~.•eapons Sys"fem.s 194.4 1Q7.4

O h.em'icall W eapons D isposal P1ro[J1r aJn

I Chemical Agents a nd Munitions Destruction (CAM D ) 6 . 956.0 10 . 636.7

I CM.£0 Assem'bfedl Chemical 'INeapons A ssessmen! (ACWA)

- 1-5.~47.8 5 . 634.2

i T otal Envi.-onm @n tal U a.bilities $ 66,.230.0 $ 70, M5.9

Acquisition, Technology and Logistics

Accounting Standards - Definitions

• SFFAS 5 - Liabilities

– Liability: Probable future outflow or other sacrifice of

resources as a result of past transactions or events…

recognized when the event occurs.

• SFFAS 6 – PP&E

– Cleanup costs are the costs of removing, containing, and/or

disposing of (1) hazardous waste from property, or (2)

material and/or property that consists of hazardous waste

at permanent or temporary closure or shutdown of

associated PP&E.

– Cleanup costs shall be estimated when the associated

PP&E is placed in service…recognized over the asset life.

Acquisition, Technology and Logistics

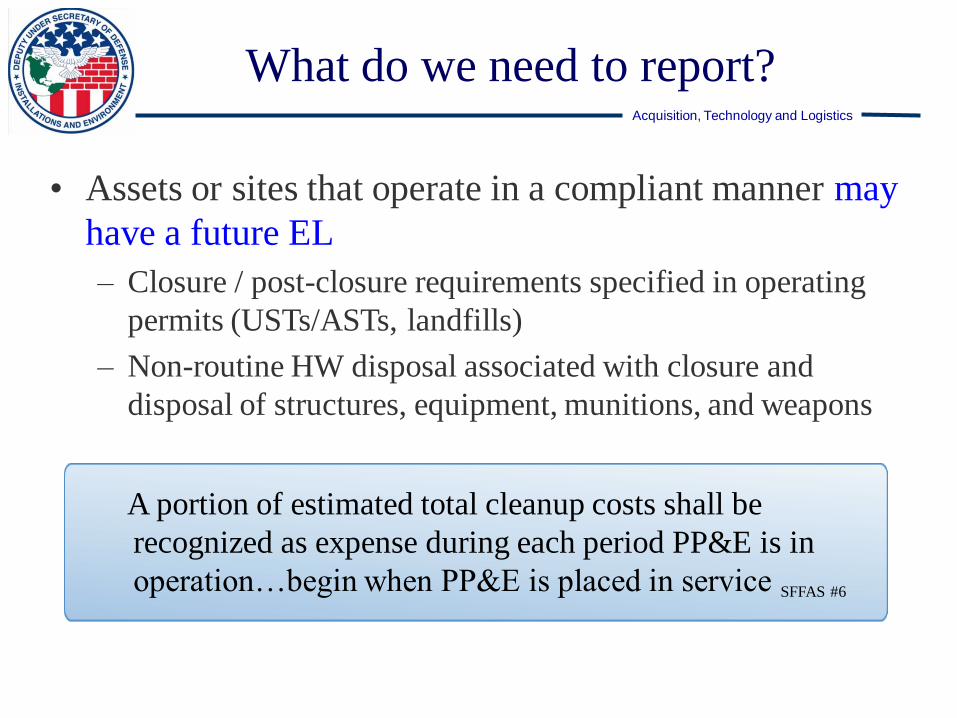

What do we need to report?

• Assets or sites that operate in a compliant manner may

have a future EL

– Closure / post-closure requirements specified in operating

permits (USTs/ASTs, landfills)

– Non-routine HW disposal associated with closure and

disposal of structures, equipment, munitions, and weapons

A portion of estimated total cleanup costs shall be

recognized as expense during each period PP&E is in

operation…begin when PP&E is placed in service SFFAS #6

Acquisition, Technology and Logistics

(Future) Expense Recognition in

Current Period

• Information Needed

– Placed in Service Date

– Useful Life for tanks, facilities

– Total and Used Capacity for Landfills

• Calculating the amount to be recognized in current period

– Tanks, Facilities:

• Closure cost * (yrs in service / total useful life) – amt prev. recognized

– Landfills:

• Closure cost * (capacity used / total est capacity) - amt prev. recognized

• Disclosure: Method for assigning est total cleanup costs

to current operating periods – Useful Life or Capacity

Acquisition, Technology and Logistics

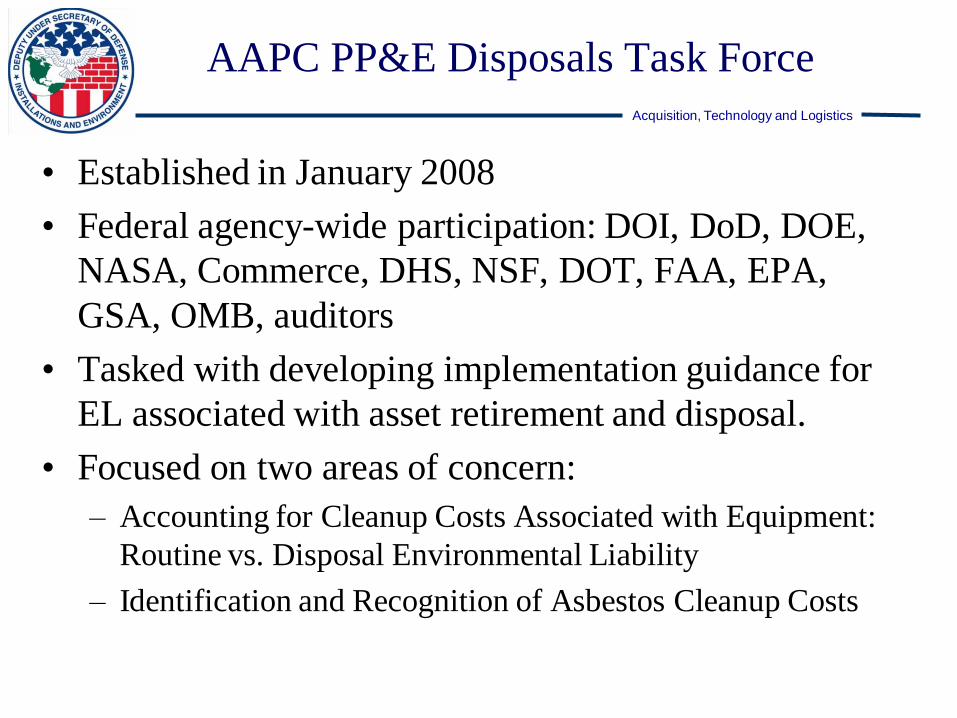

AAPC PP&E Disposals Task Force

• Established in January 2008

• Federal agency-wide participation: DOI, DoD, DOE,

NASA, Commerce, DHS, NSF, DOT, FAA, EPA,

GSA, OMB, auditors

• Tasked with developing implementation guidance for

EL associated with asset retirement and disposal.

• Focused on two areas of concern:

– Accounting for Cleanup Costs Associated with Equipment:

Routine vs. Disposal Environmental Liability

– Identification and Recognition of Asbestos Cleanup Costs

Acquisition, Technology and Logistics

Implementation Guidance on Cleanup Costs

Associated with Equipment - Background

• Environmental liabilities are defined by cleanup costs

and hazardous waste in SFFAS 6.

• Cleanup costs that occur when operations cease are

recognized over the life of the asset.

• However, “…. ...cleanup that is part of “ongoing part

of operations are accounted for in accordance with

liability standards…”

What constitutes “ongoing part of operations”?

What are the “liability standards”?

Acquisition, Technology and Logistics

Implementation Guidance on Cleanup Costs

Associated with Equipment - Technical Guidance

• Cleanup associated with “ongoing operations” are

operating expenses, not an accrued environmental

liability.

– Immediate cleanup (e.g., spill)

– Routine HW disposal (part of “ongoing operations”)

• What do they mean by “liability standards”? (SFFAS 1)

– Liabilities that routinely recur in normal operations and are

due within a fiscal year

– Accounts Payable: When an entity accepts title to goods (or

service), it recognizes a liability for the unpaid amount

Acquisition, Technology and Logistics

EL vs Ongoing Operations

– When is cleanup the same as ongoing (day-to-day) operations?

– Considerations include:• Regulatory requirements - Is it the same waste code as routinely disposed waste?

• Method of managing the waste - Does it go to the same place as routinely

disposed waste?

• Ongoing contract - Is this activity non-routine, requiring a special contract?

Common Operational Waste Environmental Liability

• Ship scrapping operations

• Nuclear waste

• Asbestos

• Permitted unit closures

• Batteries, cleaning solvents,

motor oil

• Wastewater from equipment

cleaning

• Certain sludges, residues

characteristic of operational waste

• Product or waste recovered for

reuse: fuel, used oil

Acquisition, Technology and Logistics

Recognizing EL for Equipment

YES Example:

YES Example: • Disposal Plan

• W<iste Disposal C<:ntract

Rtc0{11tZII! Esttmltefa Environmental Liabilh on

financ ial st~emertsin accordance with

SFFAS ft! . §

E)(pense t n a ~anee wtth SFEAS No.1

YES

Otsclose Huarcbys Wute e•tstence 1n financi~ statement

nctes.

ft!t Rnsona~y Estim!ble. Estim~e Cost of Future Stl..dy

ttlt Reasona~y Estimable . EsttmJte Cost to ContitnVKi

Requrtd Shoes

Recognze Estimated Cost of Stu:iy or Ccnhtn~nt tn

Accordance With SFFA S ft! 6

Acquisition, Technology and Logistics

Technical Bulletin 2006/9-1: Asbestos

• Estimate all asbestos-related cleanup (i.e., disposal)

costs; not just asbestos that requires immediate

cleanup.

• Both friable and non-friable

• No asset lasts forever; must assume future repair,

removal, renovation, or demolition.

• Recognize liability for costs that are probable and

reasonably estimable.

• Recognize liability when asset is placed in service.

• Effective for reporting period after Sept 30, 2011.

Acquisition, Technology and Logistics

Implementation Issues

• Agencies are not required to track non-friable asbestos

• Removal of non-friable asbestos not always required

• State regulation results in decentralized data collection

• Contingent nature of the cleanup requirements:

– Location and quantity

– Condition

– Disposal methodology (e.g., bull-doze, hand removal)

– State regulation

Acquisition, Technology and Logistics

Can we Make Assumptions?

• Where is the non-friable asbestos?

• Destructive Testing not required

• Assumptions based on: year built, use/application (fire

retardant), similar assets

• How will the asset be disposed?

• Current condition of asbestos may indicate future

condition.

• What is the State regulation (asbestos tile removal

required prior to demolition?)

Reasonable assumptions can be made in some cases to make

up for a lack of actual data (FASAB TR 10)

Acquisition, Technology and Logistics

Implementation Guidance on

Asbestos Cleanup Costs

• Review inventory listing of all real property

• Identify and eliminate all real property or group of real

properties on the list that are not expected to contain

asbestos – document!

• For remaining assets, determine:

– Scope of asbestos removal required based on

• Method of renovation or demolition

• Applicable regulatory requirements

– Amount, type, location, and expected condition of asbestos

Acquisition, Technology and Logistics

Implementation Guidance on

Asbestos Cleanup Costs

• If the information is either not available or not

sufficient to support assumptions, then cleanup is not

reasonable estimable at that time.

• Still recognize any other identifiable costs (e.g.,

asbestos survey).

• Prepare appropriate narrative disclosure.

• Revise estimates as additional information becomes

available.

Acquisition, Technology and Logistics

Acceptable Estimating Methodologies

• A property-specific cost estimate based on

survey data (most accurate, if available);

• An extrapolation of historical cost or cost

estimates for asbestos cleanup of similar real

property(ies);

• A cost model used for an individual real

property or group of similar real properties;

• Other reasonable methodologies.

As additional information becomes available, key assumptions

should be re-evaluated, cost estimates revised, and necessary

adjustments made….

Acquisition, Technology and Logistics

Summary of General Approach

Review tac;i les in real properly

IIIYOniOry

Yes

No

Co:o1 are probable, but not

roasonably e:o11mable

Yes

ES1imale and reoogr.le any t:::::\ identifiable costs (e.g . survey ~ costs) and ct~Scloso e>~.iStenco

ot i!$bes!O$ In note:> to financial s1aternents

~------------~ ~ Estima1e ooSl of

removal. oonlalnmont or~S<t1end

reccJgJ'IZB in accoroanc.e with

SFFAS 61

Estunate and teoognlze any Q

ldelllifiable oos.ts 1e.g. V survoycosQ

Acquisition, Technology and Logistics

EL Policy and Guidance

• Statement of Federal Financial Accounting Standard 6

(SFFAS 5) – Accounting for Liabilities of the Federal

Government

• SFFAS 6 – Plant, Property & Equipment

• DoD Financial Management Regulation, 7000.14-R,

Volume 4, Chapter 13

• OUSD(C) EL Best Practices Guide

• DUSD (I&E) Management Guidance for Recognizing,

Measuring, and Reporting Non-DERP Environmental

Disposal and Closure Liabilities (October 2005)

Acquisition, Technology and Logistics

Summary

• Two FASAB Implementation Guides issued

– Technical Release 10 (Asbestos) and 11 (Equipment)

• Provides additional framework

• Still leaves some implementation issues for the

financial reporting entities to resolve:

– Based on framework and examples, determine specifically

what is operational vs accrued liability for equipment

– Determine specific cost estimating approach for asbestos based

on methodologies from the guidance

• Document and share your process with other Financial

Reporting Entities!

Acquisition, Technology and Logistics

Questions

?