new ifrs standards and...

TRANSCRIPT

New IFRS standards and interpretations

Warsaw, December 2012

Page 2

Agenda

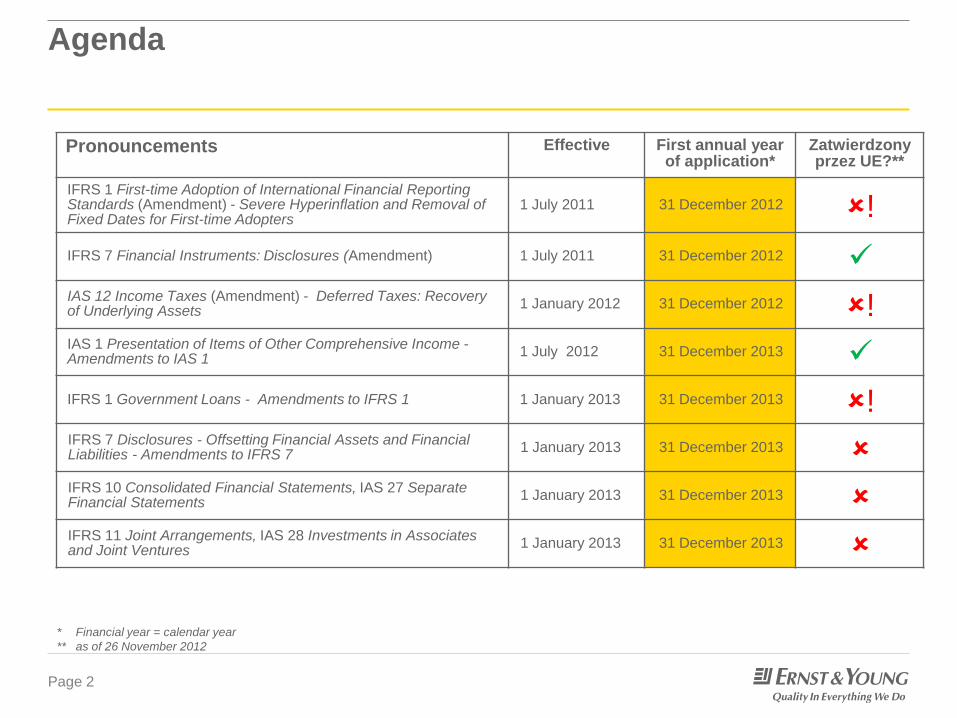

Pronouncements Effective First annual year of application*

Zatwierdzony przez UE?**

IFRS 1 First-time Adoption of International Financial Reporting Standards (Amendment) - Severe Hyperinflation and Removal of Fixed Dates for First-time Adopters

1 July 2011 31 December 2012 !

IFRS 7 Financial Instruments: Disclosures (Amendment) 1 July 2011 31 December 2012 IAS 12 Income Taxes (Amendment) - Deferred Taxes: Recovery of Underlying Assets

1 January 2012 31 December 2012 ! IAS 1 Presentation of Items of Other Comprehensive Income - Amendments to IAS 1

1 July 2012 31 December 2013

IFRS 1 Government Loans - Amendments to IFRS 1 1 January 2013 31 December 2013 ! IFRS 7 Disclosures - Offsetting Financial Assets and Financial Liabilities - Amendments to IFRS 7

1 January 2013 31 December 2013 IFRS 10 Consolidated Financial Statements, IAS 27 Separate Financial Statements

1 January 2013 31 December 2013 IFRS 11 Joint Arrangements, IAS 28 Investments in Associates and Joint Ventures

1 January 2013 31 December 2013

* Financial year = calendar year

** as of 26 November 2012

Page 3

Agenda (contd.)

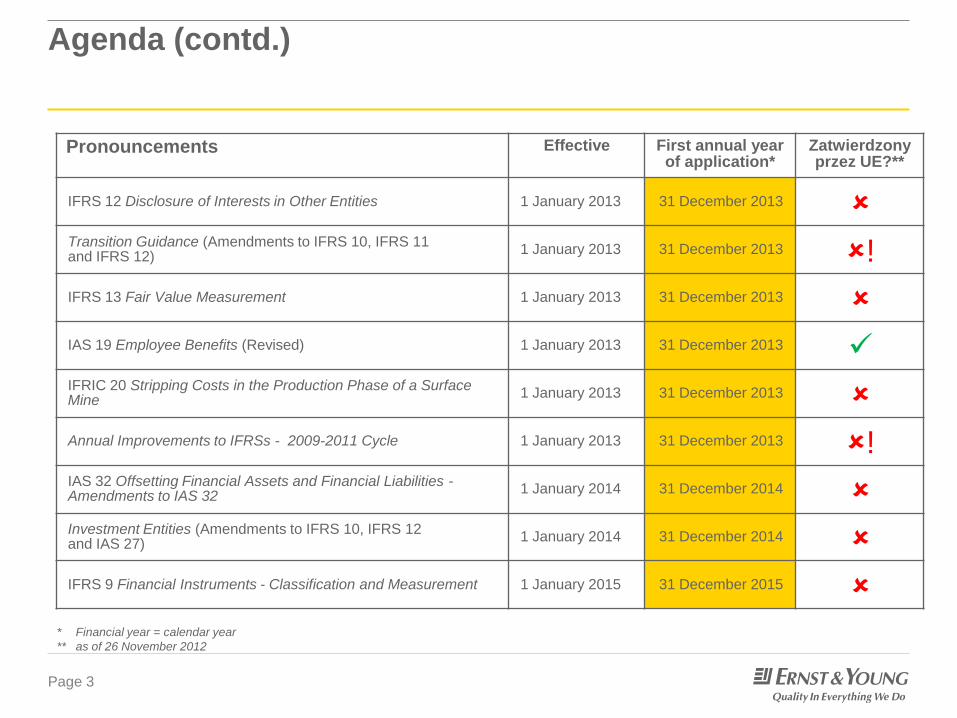

Pronouncements Effective First annual year of application*

Zatwierdzony przez UE?**

IFRS 12 Disclosure of Interests in Other Entities 1 January 2013 31 December 2013 Transition Guidance (Amendments to IFRS 10, IFRS 11 and IFRS 12)

1 January 2013 31 December 2013 !

IFRS 13 Fair Value Measurement 1 January 2013 31 December 2013

IAS 19 Employee Benefits (Revised) 1 January 2013 31 December 2013 IFRIC 20 Stripping Costs in the Production Phase of a Surface Mine

1 January 2013 31 December 2013

Annual Improvements to IFRSs - 2009-2011 Cycle 1 January 2013 31 December 2013 ! IAS 32 Offsetting Financial Assets and Financial Liabilities - Amendments to IAS 32

1 January 2014 31 December 2014 Investment Entities (Amendments to IFRS 10, IFRS 12 and IAS 27)

1 January 2014 31 December 2014

IFRS 9 Financial Instruments - Classification and Measurement 1 January 2015 31 December 2015

* Financial year = calendar year

** as of 26 November 2012

Page 4

IFRS 1 First-time Adoption of IFRS (Amendment) - Severe

Hyperinflation and Removal of Fixed Dates for First-time Adopters

► Provides guidance on how an entity

should resume presenting IFRS

financial statements when its functional

currency ceases to be subject to severe

hyperinflation

► Creates new exemption on transition to

IFRS on or after the functional currency

normalisation date

► Allows the use of fair value as

deemed cost of assets and liabilities

► Provides relief from the requirement

to provide comparative information

Transition

► Earlier application permitted, which must be disclosed

► Requires source

and documentation of the

fair value estimation if the

new deemed cost

exemption availed

Effective for annual periods beginning on or after 1 July 2011

Key requirements Financial statement impact Considerations

► Allows entities that were

subject to severe

hyperinflation in the past to

recommence reporting

under IFRS

► Removes legacy fixed dates relating to

derecognition and day one gain or loss

transactions; replaced with the date of

transition to IFRS

► Relief to first-time adopters

by reducing the cost and

resources required to

retrospectively restate past

transactions

Page 5

IFRS 7 Financial Instruments: Disclosures (Amendment)

► Additional quantitative and

qualitative disclosures relating to

transfers of financial assets when:

► Financial assets are

derecognised in their entirety,

but there is a continuing

involvement in them (e.g.,

options or guarantees on the

transferred assets)

► Financial assets are not

derecognised in their entirety

► More extensive disclosures, e.g.,

estimated maximum exposure to

loss arising from continuing

involvement

Transition

► No comparative disclosures required for any period beginning before the effective date

► Earlier application permitted, which must be disclosed

► May require modification

of management information

systems and internal

controls to obtain the

necessary quantitative

information to make the

disclosures

Effective for annual periods beginning on or after 1 July 2011

Key requirements Financial statement impact Considerations

Page 6

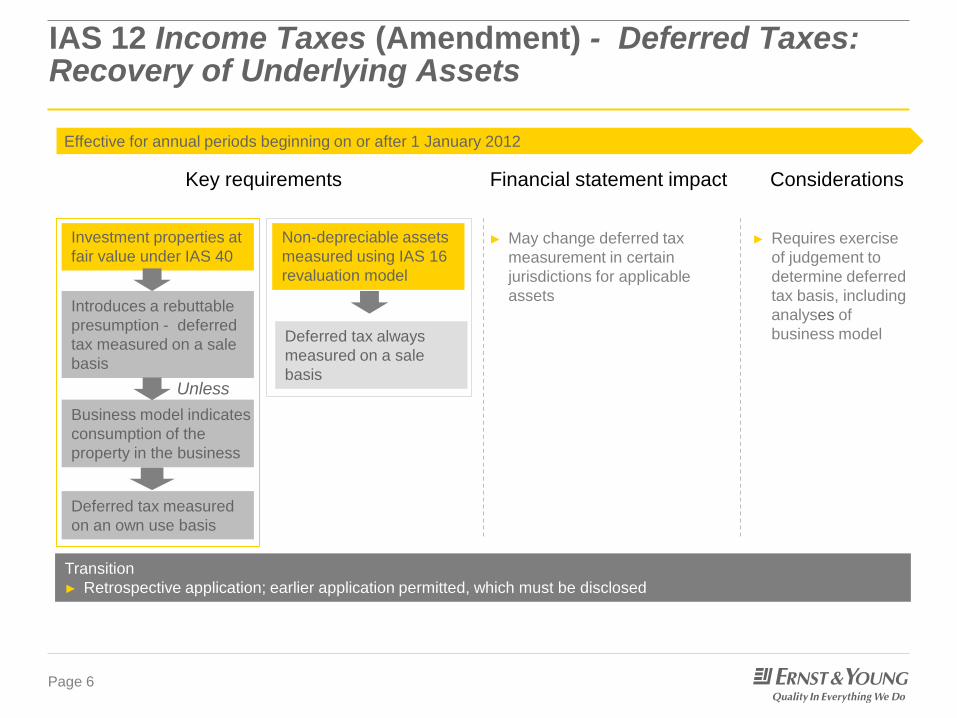

IAS 12 Income Taxes (Amendment) - Deferred Taxes: Recovery of Underlying Assets

► May change deferred tax

measurement in certain

jurisdictions for applicable

assets

Transition

► Retrospective application; earlier application permitted, which must be disclosed

► Requires exercise

of judgement to

determine deferred

tax basis, including

analyses of

business model

Effective for annual periods beginning on or after 1 January 2012

Key requirements Financial statement impact Considerations

Investment properties at

fair value under IAS 40

Non-depreciable assets

measured using IAS 16

revaluation model

Introduces a rebuttable

presumption - deferred

tax measured on a sale

basis

Business model indicates

consumption of the

property in the business

Deferred tax always

measured on a sale

basis Unless

Deferred tax measured

on an own use basis

Page 7

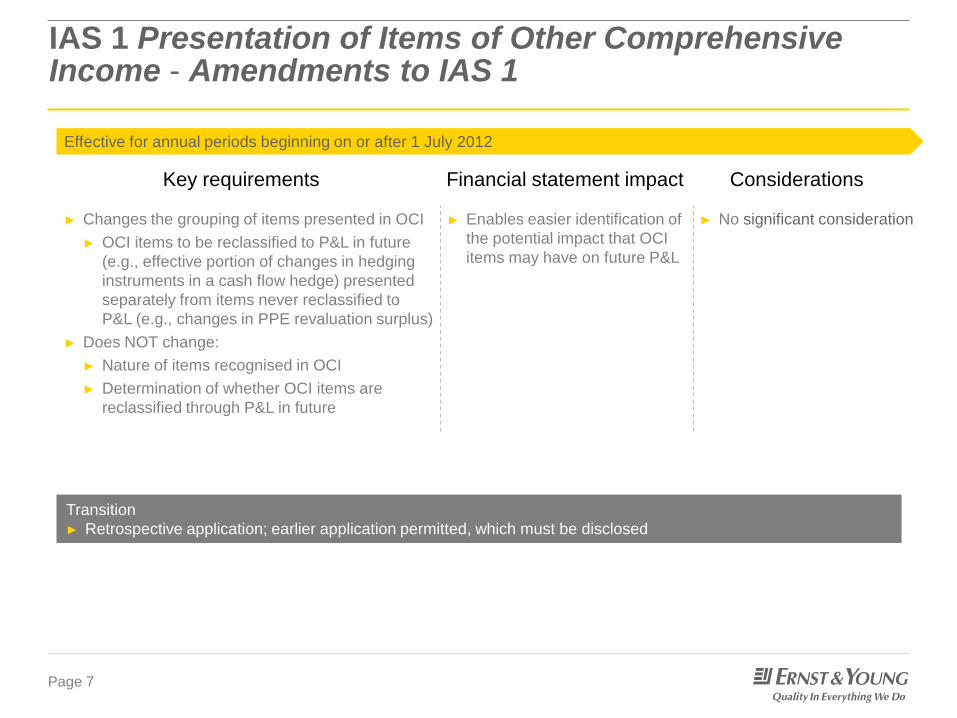

IAS 1 Presentation of Items of Other Comprehensive Income - Amendments to IAS 1

► Changes the grouping of items presented in OCI

► OCI items to be reclassified to P&L in future

(e.g., effective portion of changes in hedging

instruments in a cash flow hedge) presented

separately from items never reclassified to

P&L (e.g., changes in PPE revaluation surplus)

► Does NOT change:

► Nature of items recognised in OCI

► Determination of whether OCI items are

reclassified through P&L in future

► Enables easier identification of

the potential impact that OCI

items may have on future P&L

Transition

► Retrospective application; earlier application permitted, which must be disclosed

► No significant consideration

Effective for annual periods beginning on or after 1 July 2012

Key requirements Financial statement impact Considerations

Page 8

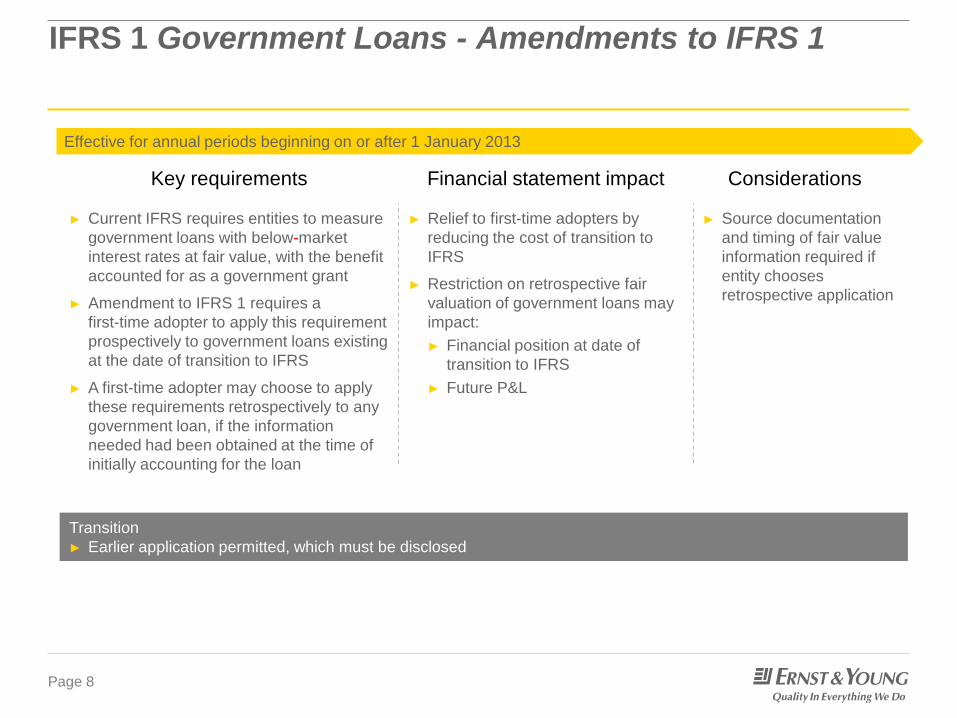

IFRS 1 Government Loans - Amendments to IFRS 1

► Current IFRS requires entities to measure

government loans with below-market

interest rates at fair value, with the benefit

accounted for as a government grant

► Amendment to IFRS 1 requires a

first-time adopter to apply this requirement

prospectively to government loans existing

at the date of transition to IFRS

► A first-time adopter may choose to apply

these requirements retrospectively to any

government loan, if the information

needed had been obtained at the time of

initially accounting for the loan

► Relief to first-time adopters by

reducing the cost of transition to

IFRS

► Restriction on retrospective fair

valuation of government loans may

impact:

► Financial position at date of

transition to IFRS

► Future P&L

Transition

► Earlier application permitted, which must be disclosed

► Source documentation

and timing of fair value

information required if

entity chooses

retrospective application

Effective for annual periods beginning on or after 1 January 2013

Key requirements Financial statement impact Considerations

Page 9

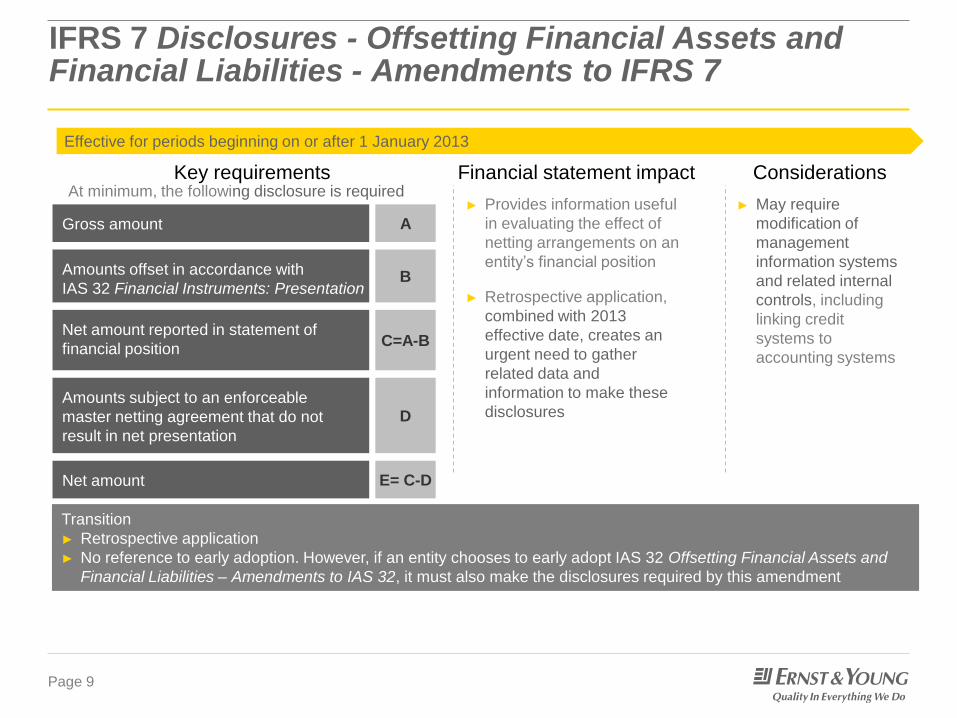

IFRS 7 Disclosures - Offsetting Financial Assets and Financial Liabilities - Amendments to IFRS 7

At minimum, the following disclosure is required ► Provides information useful

in evaluating the effect of

netting arrangements on an

entity’s financial position

► Retrospective application,

combined with 2013

effective date, creates an

urgent need to gather

related data and

information to make these

disclosures

Transition

► Retrospective application

► No reference to early adoption. However, if an entity chooses to early adopt IAS 32 Offsetting Financial Assets and

Financial Liabilities – Amendments to IAS 32, it must also make the disclosures required by this amendment

► May require

modification of

management

information systems

and related internal

controls, including

linking credit

systems to

accounting systems

Effective for periods beginning on or after 1 January 2013

Key requirements Financial statement impact Considerations

Gross amount

Amounts offset in accordance with

IAS 32 Financial Instruments: Presentation

Net amount reported in statement of

financial position

Amounts subject to an enforceable

master netting agreement that do not

result in net presentation

Net amount

A

B

C=A-B

D

E= C-D

Page 10

IFRS 10 Consolidated Financial Statements, IAS 27 Separate Financial Statements

Transition

► Modified retrospective application taking into account whether the control assessment is different under IFRS 10

► Only one comparative period required to be restated

► Early adoption permitted if IFRS 11, IFRS 12, IAS 27(Revised) and IAS 28 (Revised) also adopted at the same time

► Consolidation model entirely founded

on the notion of control applicable to

all entities (including SPEs)

► New definition of control

► Continuous reassessment of control

required

► New and broader definition

of control may result in

changes to a consolidated

group:

► On transition to IFRS 10

► In future reporting

periods due to

continuous

reassessment

Requires:

► Judgement of facts and circumstances

► Assessment of control, including

comprehensive understanding of:

► Investee’s purpose, design and activities

► Investor’s rights and exposures to

variable returns

► Rights and returns of other investors

► Additional procedures and internal controls

to:

► Identify controlled entities

► Assess internal and external evidence

► Inputs from sources outside accounting

function

Effective for annual periods beginning on or after 1 January 2013

Key requirements Financial statement impact Considerations

Power to direct relevant activities

Exposure or rights to variable returns

Link between power and exposure

+

+

Page 11

IFRS 11 Joint Arrangements, IAS 28 Investments in Associates and Joint Ventures

Transition

► Modified retrospective application; similar to the IFRS 10 relief, only one comparative period required to be restated

► Early adoption permitted if IFRS 10, IFRS 12, IAS 27(Revised) and IAS 28 (Revised) also adopted at the same time

Effective for annual periods beginning on or after 1 January 2013

► Requires significant

judgement and

comprehensive analysis

of existing arrangements

to:

► Assess whether joint

control exists

► Determine the

appropriate

classification

Key requirements Financial statement impact Considerations

► New classification may

change accounting for

arrangements previously

considered to be JCEs as

they may be potentially

classified as JOs

► Significant change for

entities currently applying

proportionate consolidation

to account for JCEs

IAS

31

IF

RS

11

Jointly

controlled

entities (JCE)

Jointly controlled

assets (JCA)

Jointly controlled

operations(JCO)

Joint ventures (JV)

Parties have rights to

the net assets of the

arrangement

Joint operations (JO)

Parties have rights to the assets

and obligations for the liabilities of

the arrangement

Recognise assets,

liabilities, expenses

and share of

income

Recognise share of

assets, liabilities,

income and

expenses

Equity method or

proportionate

consolidation

Recognise assets, liabilities,

revenue, and expenses, and/or

relative shares thereof

►Equity method (now

sunder IAS 28)

►Proportionate

consolidation coped

prohibited

Page 12

IFRS 12 Disclosure of Interests in Other Entities

Transition

► Retrospective application with some relief; similar to the IFRS 10, only one comparative period required to be restated

► Earlier application permitted including partial application

Effective for annual periods beginning on or after 1 January 2013

► Disclosure of significant judgements and assumptions

► Key financial information of group entities

► Disclosure of interest in unconsolidated structured entities

► More extensive

disclosures available to

users when making

assessment of the

financial impact of group

entities

► Requires additional

procedures, and

changes to information

systems, to gather

information to make

new disclosures

► Requires significant

judgement to

determine

‘unconsolidated

structured entities’

Key requirements Financial statement impact Considerations

Draws

together

disclosure

related to

Subsidiaries

Joint arrangements

Associates

Unconsolidated structured entities

Objective: to establish the information necessary to evaluate:

► Nature of, and risks associated with, interests in other

entities

► Effects of those interests on the financial position, financial

performance and cash flows

Page 13

IFRS 13 Fair Value Measurement

► Establishes a single set of

principles on how to determine

fair value of financial and

non-financial assets and

liabilities, when required or

permitted under IFRS

► Requires new disclosures on

valuation techniques and inputs

used to determine fair values

and the effect of certain inputs

on fair value measurement

► May lead to changes in fair value

measurement

► May require additional disclosures to be

provided

Transition

► Prospective application; earlier application permitted, which must be disclosed

► Requires:

► Re-evaluation of

techniques, inputs,

processes and procedures

to determine fair value and

provide appropriate

disclosures

► Availability of appropriate

valuation expertise

Effective for annual periods beginning on or after 1 January 2013

Key requirements Financial statement impact Considerations

Page 14

IAS 19 Employee Benefits (Revised)

Transition

► Retrospective application with limited exceptions; earlier application permitted, which must be disclosed

Effective for annual periods beginning on or after 1 January 2013

Defined benefit plans:

► Higher balance sheet

volatility for those following

corridor approach or having

unvested past service cost

► Remeasurements, including

actuarial movements,

permanently bypass earnings

► Requires:

► Compliance by actuaries

with the revised

requirements

► Additional procedures,

internal controls and

actuarial information for

new/revised disclosures,

such as disclosure of

sensitivity analyses

► Additional judgement

and estimates, e.g., to

determine expected timing

of settlement of employee

benefits

Key requirements Financial statement impact Considerations

Defined benefit plans:

► Corridor approach removed, requires immediate

recognition of changes to plan

assets/obligations

► Concept of expected returns removed, interest

must be recognised on net plan obligation/asset

► Service cost and net interest charged to P&L

► Remaining changes in plans recognised in OCI

► Past service cost recognised immediately

► New disclosures, including sensitivity analyses

of defined benefit plans

Other changes:

► Short-term vs long-term employee benefits

classification based on expected timing of

settlement rather than employee entitlements

► Timing of recognition of termination benefits

Page 15

IFRIC 20 Stripping Costs in the Production Phase of a Surface Mine

► Requires capitalisation of production stripping

costs as part of an asset, if criteria met

► Classified as:

► Inventory, if benefits realised in current

period

► Non-current asset (‘stripping activity asset’)

if the benefit is the improved access to ore,

recognised as addition to or enhancement

of existing asset, e.g., mine asset

► Initially measured at cost plus directly

attributable overhead

► Subsequently measured using either:

► Cost model

Or

► Revaluation model

► May represent a change

from the current approach

used, e.g., average life of

mine strip ratio

► Depending on the specific

facts and circumstances,

these changes may

impact both the financial

position and P&L

Transition

► IFRIC 20 applied to stripping costs incurred on or after the beginning of the earliest period presented

► Full retrospective application not required, instead practical expedient provided for stripping costs incurred and

capitalised prior to that date

► Earlier application permitted, which must be disclosed

► Requires management

judgement for assessment of:

► The capitalisation criteria

► Identification of

‘components’ of mine

► Depreciation approach

Effective for annual periods beginning on or after 1 January 2013

Key requirements Financial statement impact Considerations

Page 16

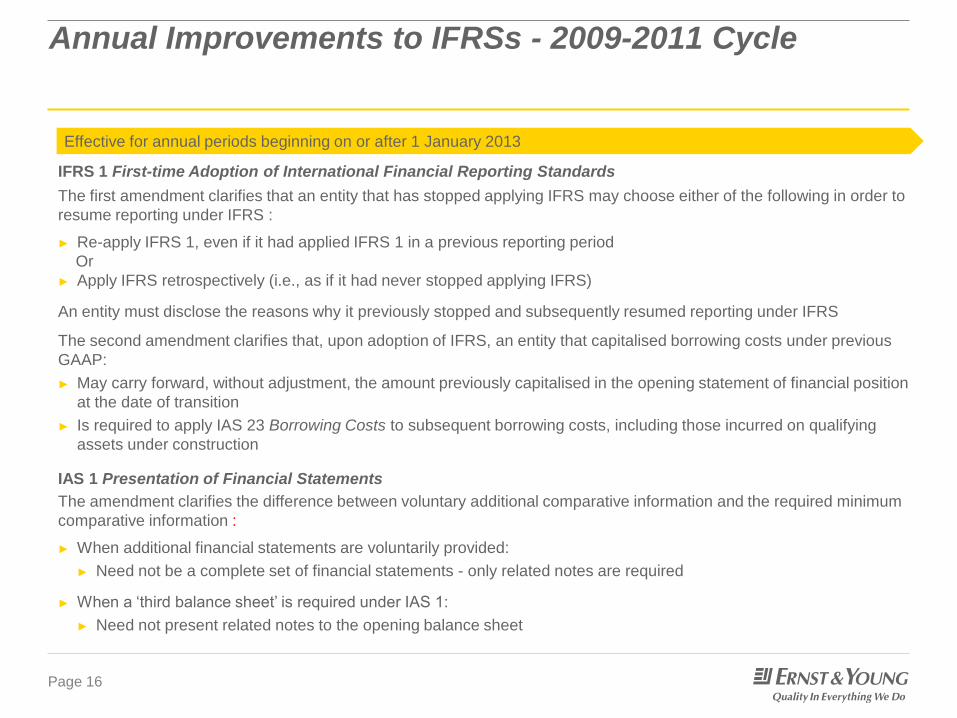

Annual Improvements to IFRSs - 2009-2011 Cycle

Effective for annual periods beginning on or after 1 January 2013

IFRS 1 First-time Adoption of International Financial Reporting Standards

IAS 1 Presentation of Financial Statements

The first amendment clarifies that an entity that has stopped applying IFRS may choose either of the following in order to

resume reporting under IFRS :

► Re-apply IFRS 1, even if it had applied IFRS 1 in a previous reporting period

Or

► Apply IFRS retrospectively (i.e., as if it had never stopped applying IFRS)

An entity must disclose the reasons why it previously stopped and subsequently resumed reporting under IFRS

The second amendment clarifies that, upon adoption of IFRS, an entity that capitalised borrowing costs under previous

GAAP:

► May carry forward, without adjustment, the amount previously capitalised in the opening statement of financial position

at the date of transition

► Is required to apply IAS 23 Borrowing Costs to subsequent borrowing costs, including those incurred on qualifying

assets under construction

The amendment clarifies the difference between voluntary additional comparative information and the required minimum

comparative information :

► When additional financial statements are voluntarily provided:

► Need not be a complete set of financial statements - only related notes are required

► When a ‘third balance sheet’ is required under IAS 1:

► Need not present related notes to the opening balance sheet

Page 17

Annual Improvements to IFRSs - 2009-2011 Cycle (contd.)

Transition

► Retrospective application; earlier application permitted, which must be disclosed

The amendment clarifies the requirements in IAS 34 relating to segment information for total assets and liabilities for

each reportable segment to enhance consistency with the requirements in IFRS 8 Operating Segments:

► Total assets and liabilities for a particular reportable segment need to be disclosed only when:

► The amounts are regularly provided to the chief operating decision maker

And

► There has been a material change in the total amount disclosed in the entity’s previous annual financial statements

for that reportable segment

IAS 16 Property, Plant and Equipment

IAS 12 Income Taxes

IAS 34 Interim Financial Reporting

Classification of servicing equipment:

► The amendment clarifies that major spare parts and servicing equipment that meet the definition of property, plant

and equipment are not inventory

Tax effects of distribution to holders of equity instruments:

► The amendment removes existing income tax requirements from IAS 32 Financial Instruments: Presentation and

requires entities to apply the IAS 12 requirements to any income taxes arising from distributions to equity holders

Page 18

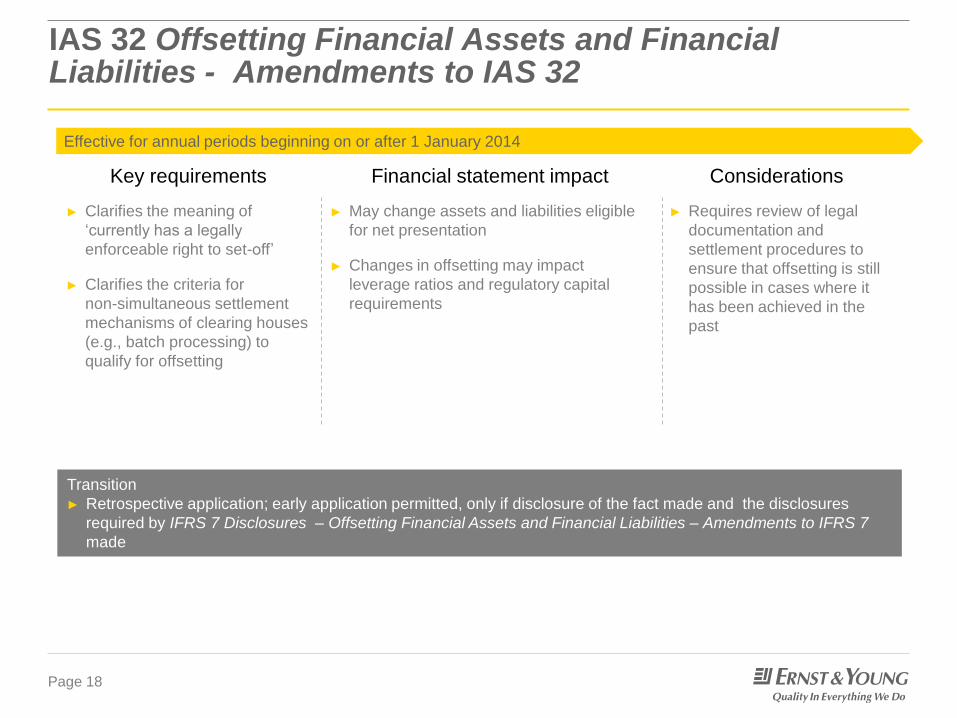

IAS 32 Offsetting Financial Assets and Financial Liabilities - Amendments to IAS 32

Transition

► Retrospective application; early application permitted, only if disclosure of the fact made and the disclosures

required by IFRS 7 Disclosures – Offsetting Financial Assets and Financial Liabilities – Amendments to IFRS 7

made

Effective for annual periods beginning on or after 1 January 2014

► Clarifies the meaning of

‘currently has a legally

enforceable right to set-off’

► Clarifies the criteria for

non-simultaneous settlement

mechanisms of clearing houses

(e.g., batch processing) to

qualify for offsetting

► May change assets and liabilities eligible

for net presentation

► Changes in offsetting may impact

leverage ratios and regulatory capital

requirements

► Requires review of legal

documentation and

settlement procedures to

ensure that offsetting is still

possible in cases where it

has been achieved in the

past

Key requirements Financial statement impact Considerations

Page 19

Investment entities – amendments to IFRS 10, IFRS 12 and IAS 27

Transition

► Retrospective application; early application permitted

Effective for annual periods beginning on or after 1 January 2014

► The exception to consolidation

requires investment entities

to account for subsidiaries at

fair value through profit or loss

in accordance with IFRS 9

Financial Instruments.

► An entity must meet all three

elements of the definition and

consider whether it has four

typical characteristics in order

to qualify as and investment

entity.

► When making an assessment

all facts and circumstances

need to be considered including

purpose and design.

► Entities that meet the definition will de-

consolidate subsidiaries and measure

them at FVTPL.

► May have little to no effect on banks,

insurers and many other organizations

involved in investment activities.

► Entities will need

to consider how much

planning and preparation

time will be needed

to update systems and

processes to accommodate

new requirements including

disclosure requirements.

Key requirements Financial statement impact Considerations

Page 20

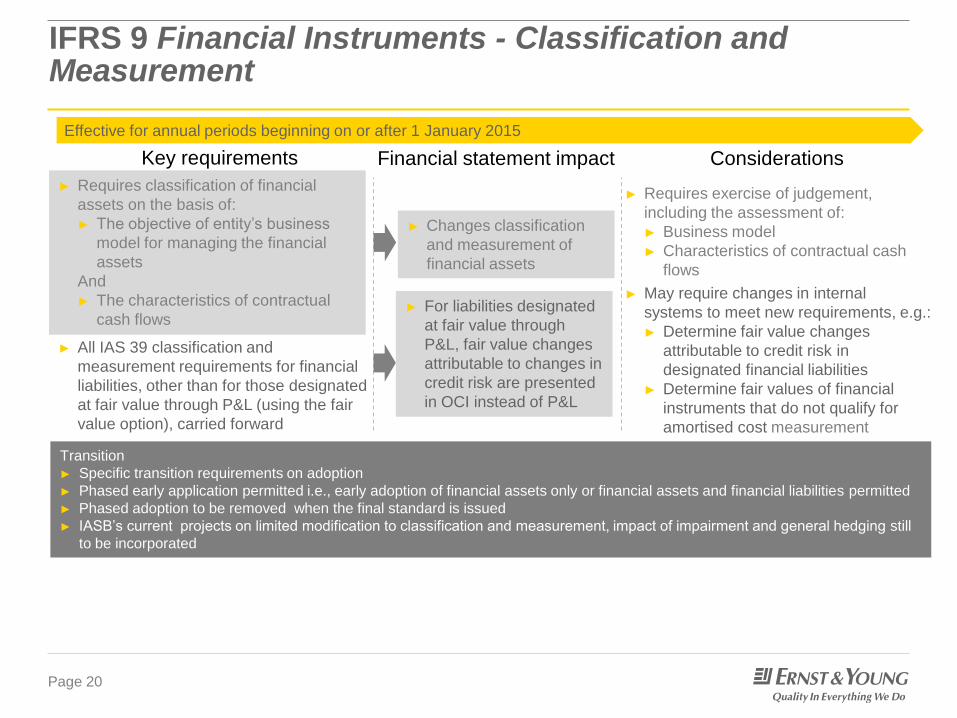

IFRS 9 Financial Instruments - Classification and Measurement

Transition

► Specific transition requirements on adoption

► Phased early application permitted i.e., early adoption of financial assets only or financial assets and financial liabilities permitted

► Phased adoption to be removed when the final standard is issued

► IASB’s current projects on limited modification to classification and measurement, impact of impairment and general hedging still

to be incorporated

Effective for annual periods beginning on or after 1 January 2015

► Requires classification of financial

assets on the basis of:

► The objective of entity’s business

model for managing the financial

assets

And

► The characteristics of contractual

cash flows

► Changes classification

and measurement of

financial assets

► Requires exercise of judgement,

including the assessment of:

► Business model

► Characteristics of contractual cash

flows

► May require changes in internal

systems to meet new requirements, e.g.:

► Determine fair value changes

attributable to credit risk in

designated financial liabilities

► Determine fair values of financial

instruments that do not qualify for

amortised cost measurement

Key requirements Financial statement impact Considerations

► All IAS 39 classification and

measurement requirements for financial

liabilities, other than for those designated

at fair value through P&L (using the fair

value option), carried forward

► For liabilities designated

at fair value through

P&L, fair value changes

attributable to changes in

credit risk are presented

in OCI instead of P&L

Page 21

Questions or comments?