new investment choices in your esip - chevron...

TRANSCRIPT

New Investment Choices in Your ESIP | 1

New Investment Choices in Your ESIPYour Wealth.

Human Energy. Yours.TM

2 | February 2013

How you invest the money you save in the ESIP is one of the most important decisions you must make. That’s because the benefit you’ll have when you retire depends on the investment allocations you make — not a fixed plan formula.

Starting April 1, 2013, the Chevron Employee Savings Investment Plan (ESIP) will expand the ESIP’s investment options to provide you with more choices when it comes to investing for your retirement. Target Retirement Trusts will be available in the ESIP for the first time. In addition, we’ll be adding new funds to the core fund lineup, and the Vanguard® Brokerage Option will be expanded to include exchange-traded funds.

New Investment Choices in Your ESIP

What’s InsidePage 4 Target Retirement Trusts

Page 9 New Fund Choices

• Vanguard Total World Stock Index Fund Institutional Shares

• SSgA U.S. Inflation Protected Bond Index Fund Class C

Page 12 Fund Alternatives in the Vanguard Brokerage Option

Page 14 Summary of ESIP Investment Options

Page 15 Connect with Vanguard

New Investment Choices in Your ESIP | 3

Do I Need to Do Anything Now?

You don’t need to take action at this time, but you should review the newsletter to understand what’s changing and to help you decide if you’ll want to make account changes when the new options become available. You’ll also receive a legal notice in February about your new investment options and the costs associated with investing in them.

If you’d like to take advantage of any of the new investment choices described in this newsletter, you can make a change to your account starting April 1, 2013. See the Connect with Vanguard information on page 15 to learn how.

As always, take time to consider the importance of a well-balanced and diversified investment portfolio.

Remember that all investing is subject to risk, including the possible loss of the money you invest, and that

diversification does not ensure a profit or protect against a loss.

4 | February 2013

On April 1, 2013, your ESIP will begin offering a family of all-in-one investment options: Vanguard Target Retirement Trusts. These investments provide another way to build and manage an investment mix.

When building a portfolio, you typically consider the value of diversification — the tactic of including different types of assets in your investment mix — in helping you manage risk. If your asset mix drifts from the proportion of stocks, bonds and short-term reserves you chose, you may need to rebalance to bring your portfolio back in line. In addition, as you move closer to retirement, your financial goals, time horizon and risk tolerance change, so you may want to adjust your asset mix to compensate. It’s a lot to consider, and the task of building, rebalancing and adjusting your ESIP portfolio can involve considerable time and effort.

Vanguard Target Retirement Trusts are an alternative that can simplify the investment process. The Vanguard Target Retirement Trusts are a family of target-date investments that provides an opportunity to create a diversified portfolio containing both stocks and bonds with a single investment. Each trust gradually changes its investment mix from more aggressive to more conservative over time, which may make it possible for a single Target Retirement Trust to serve your investing needs throughout both your career and retirement. Even though Target Retirement Trusts simplify the investment process, they still require some monitoring to ensure the portfolio is in line with your current situation.

Target Retirement TrustsA New Approach to Investing in Your ESIP

New Investment Choices in Your ESIP | 5

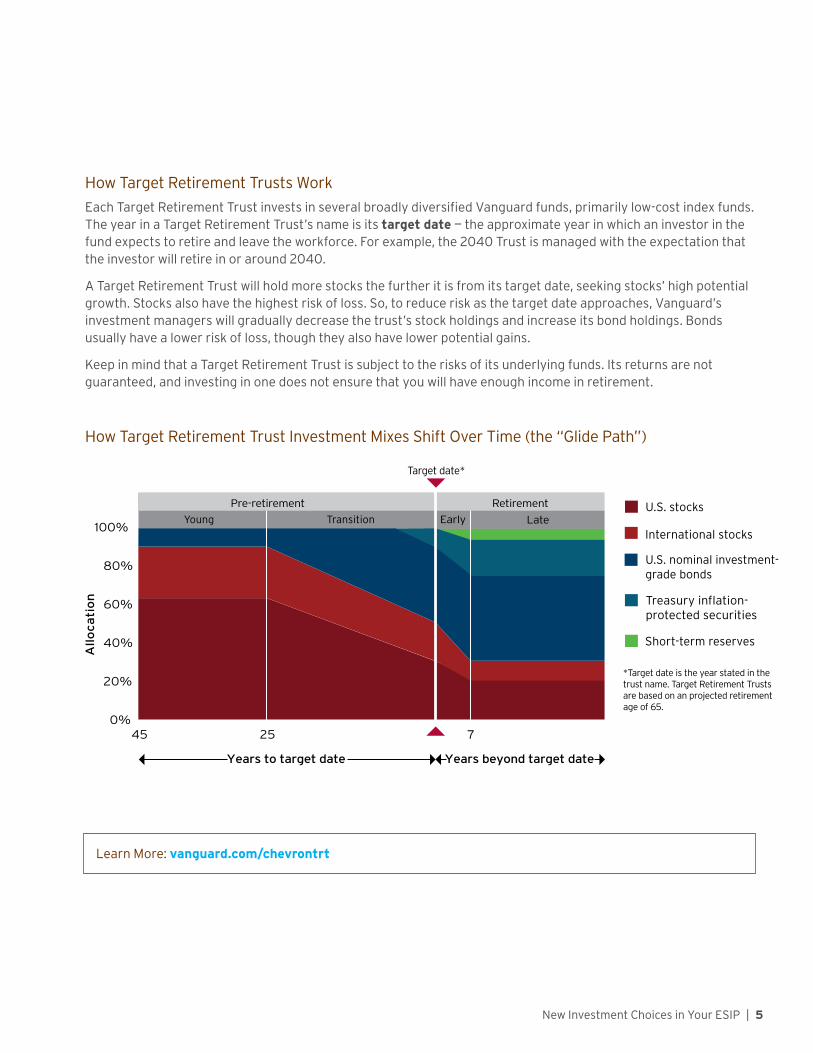

How Target Retirement Trusts Work

Each Target Retirement Trust invests in several broadly diversified Vanguard funds, primarily low-cost index funds. The year in a Target Retirement Trust’s name is its target date — the approximate year in which an investor in the fund expects to retire and leave the workforce. For example, the 2040 Trust is managed with the expectation that the investor will retire in or around 2040.

A Target Retirement Trust will hold more stocks the further it is from its target date, seeking stocks’ high potential growth. Stocks also have the highest risk of loss. So, to reduce risk as the target date approaches, Vanguard’s investment managers will gradually decrease the trust’s stock holdings and increase its bond holdings. Bonds usually have a lower risk of loss, though they also have lower potential gains.

Keep in mind that a Target Retirement Trust is subject to the risks of its underlying funds. Its returns are not guaranteed, and investing in one does not ensure that you will have enough income in retirement.

Learn More: vanguard.com/chevrontrt

0%

20%

40%

60%

80%

100% Young Transition Early Late

45 25

Years to target date

Allo

ca

tio

n

7

Targetdate

RetirementPre-retirement U.S. stocks

International stocks

U.S. nominal investment- grade bonds

Treasury inflation-protected securities

Short-term reserves

Years beyond target date

Target date*

*Target date is the year stated in the trust name. Target Retirement Trusts are based on an projected retirement age of 65.

How Target Retirement Trust Investment Mixes Shift Over Time (the “Glide Path”)

6 | February 2013

Choosing a Trust

Consider the Target Retirement Trust with the target date closest to the year you plan to retire. If you review that trust’s mix of stocks and bonds and decide it’s not a good match for your financial goals, you can choose a different trust. If you prefer a more aggressive investment mix, you can select a trust with a later target date. If you want a more conservative mix, on the other hand, you can choose a trust with an earlier target date. If you’re already in retirement, you may want to consider investing in the Vanguard Target Retirement Income Trust. This trust is designed to provide retirees with current income and some capital appreciation.

Of course, your financial situation could change over time. So if you do choose a Target Retirement Trust, you may want to review its asset mix periodically to make sure it still matches your goals and risk tolerance. You are never locked into a particular trust; you can always choose one with a different investment mix.

Learn More About the Funds

You can learn more about the underlying funds that make up each Target Retirement Trust by going to hr2.chevron.com and choosing Vanguard; then go to the ESIP Investment Guide tab on the top navigation to get started.

Each Target Retirement Trust’s underlying portfolio is monitored and the individual fund offerings may be changed at any time. Participants in the Target Retirement Trusts will always be notified when this happens so they can decide if they want to select different investments. For example, Vanguard expects to make the following changes near the end of the second quarter of 2013:

• The Vanguard Total International Bond Index Fund will be added to every Target Retirement Trust.

• The Vanguard Inflation-Protected Securities Fund will be replaced by the Vanguard Short-Term Inflation-Protected Securities Index Fund in the 2015 and 2010 Target Retirement Trusts and the Target Retirement Income Trust.

• Allocations to the Vanguard Prime Money Market Fund in the Target Retirement 2010 and Target Retirement Income Trusts will be eliminated.

New Investment Choices in Your ESIP | 7

Approximate years until retirement

Stocks Bonds Short-term reserves

2060Trust

100%

80%

60%

40%

20%

0%

2055Trust

2050Trust

2045Trust

2040Trust

2035Trust

2030Trust

2025Trust

2020Trust

2015Trust

2010Trust

RetirementIncomeTrust

48 43 38 33 28 23 18 13 8 3 Transitioning In retirement

Income in Retirement

Target Retirement Trusts with dates in their names don’t retire when you do. Since retirement can last 30 years or more, each trust is designed to continue its shift from stocks to bonds and short-term reserves for approximately seven years after its target date. This shift stops only when the target-date trust has the same mix as the Vanguard Target Retirement Income Trust. Even at that point, the trust will still invest some of its assets in stocks. The long-term growth potential of stocks helps increase the chance that your purchasing power will keep up with inflation.

Investments in Target Retirement Trusts are subject to the risks of their underlying funds. The year in the trust’s name refers to the approximate year (the target date) when an investor in the trust would retire and leave the work-force. The trust will gradually shift its emphasis from more aggressive investments (stocks) to more conservative ones (bonds and short-term reserves) based on its target date. An investment in a Target Retirement Trust is not guaranteed at any time, including on or after the target date. Bond funds are subject to the risk that an issuer will fail to make payments on time, and that bond prices will decline because of rising interest rates or negative perceptions of an issuer’s ability to make payments.

Target Retirement Trust Investment Mixes

8 | February 2013

Mixing Target Retirement Trusts and Other ESIP Investment Options

Vanguard Target Retirement Trusts are designed to serve as a broadly diversified portfolio in a single investment. That doesn’t mean that target-date investments and other funds can’t coexist in the same portfolio. In fact, they often do. Go to Vanguard’s Target-date information center at vanguard.com/targetdatenow to learn more about creating a portfolio that includes both target-date and other investments.

Target Retirement Trusts and the Vanguard Managed Account Program

Please note that Vanguard Target Retirement Trusts are not available to participants in the Vanguard Managed Account Program (VMAP™). If you have a VMAP account, you’ll need to close it before you can invest in a Target Retirement Trust.

New Investment Choices in Your ESIP | 9

New Fund ChoicesChanges in the ESIP Fund Lineup

On April 1, 2013, you’ll have the opportunity to invest in two new core fund options: the Vanguard Total World Stock Index Fund Institutional Shares and the SSgA U.S. Inflation Protected Bond Index Fund Class C.

Vanguard Total World Stock Index Fund

The Vanguard Total World Stock Index Fund Institutional Shares seeks to track the performance of the FTSE Global All Cap Index, a free-float-adjusted, market-capitalization-weighted index designed to measure the market performance of large-, mid- and small-capitalization stocks of companies located around the world. The index includes approximately 7,400 stocks of companies located in 47 countries, including both developed and emerging markets.

The Vanguard Total World Stock Index Fund may be appropriate for investors who seek long-term growth of capital; a simple, low-cost way to track the performance of stocks around the world; and a broadly diversified fund that invests in companies from around the world, including the United States, and investors who expect to hold their investments for at least five years. This fund may not be a good choice for investors who are unwilling to accept significant fluctuations in share price or who seek significant dividend income.

Prices of mid- and small-cap stocks often fluctuate more than those of large-cap stocks. Stocks of companies based in emerging markets are subject to national and regional political and economic risks and to the risk of currency fluctuations. These risks are especially high in emerging markets. Investments in stocks or bonds issued by non-U.S. companies are subject to risks including country/regional risk, which is the chance that political upheaval, financial troubles or natural disasters will adversely affect the value of securities issued by companies in foreign countries or regions, and currency risk, which is the chance that the value of a foreign investment, measured in U.S. dollars, will decrease because of unfavorable changes in currency exchange rates.

10 | February 2013

SSgA U.S. Inflation Protected Bond Index Fund

As with the other investment options offered by the ESIP, the SSgA U.S. Inflation Protected Bond Index Fund Class C can help you build a diversified mix of stocks, bonds and short-term reserves.

The SSgA U.S. Inflation Protected Bond Index Fund seeks an investment return that approximates as closely as practicable, before expenses, the performance of the Barclays Capital U.S. Treasury Inflation Protected Securities (TIPS) Index over the long term. The fund may attempt to invest in the securities comprising the Index in the same proportions as they are represented in the index. However, it may not be possible for the fund to purchase some of the securities comprising the index. In such a case, SSgA will select securities for the fund that SSgA believes will track the characteristics of the index.

The SSgA U.S. Inflation Protected Bond Index Fund may be appropriate for investors seeking a bond fund that provides protection against the effects of inflation and those interested in the additional portfolio diversification that inflation-indexed securities can offer. This fund may not be a good choice for investors who are unwilling to accept some volatility in income distributions, those who are averse to modest fluctuations in share price, and those who seek long-term growth of capital.

What Are Treasury Inflation-Protected Securities (TIPS)?Investors can help mitigate investment risk in their portfolios by choosing funds that invest in bonds with lower credit and interest rate risk. However, if an investment is too conservative, inflation can reduce the purchasing power of investors’ savings over the long run.

New Investment Choices in Your ESIP | 11

Treasury inflation-protected securities, or TIPS, are designed to help investors combat inflation. Here’s how they work: The bond has a fixed interest rate, but its principal — the original amount invested — is adjusted according to changes in the Consumer Price Index. The interest payment can increase or decrease over time as the principal value rises and falls. When the bond matures, the U.S. Treasury pays either the original principal or adjusted principal, whichever amount is greater.

Because TIPS are issued by the U.S. Treasury, they are generally considered lower-risk investments. However, the share price for a fund that invests in TIPS can fluctuate substantially because of short-term changes in interest rates. In times of low inflation, a mutual fund that invests primarily in TIPS could lose money if rising real interest rates drive down the prices of the bonds in the fund’s portfolio. The fund’s income, including the inflation kicker, might not be enough to offset the declining prices of the bonds owned by the fund.

While U.S. Treasury or government agency securities provide substantial protection against credit risk, they do not protect investors against price changes due to changing interest rates. Unlike stocks and bonds, U.S. Treasury bills are guaranteed as to the timely payment of principal and interest.

More information about these new funds is available by going to hr2.chevron.com and choosing Vanguard; then go to the ESIP Investment Guide tab on the top navigation to get started.

12 | February 2013

Fund Alternatives in the Vanguard Brokerage Option

If you have a Vanguard Brokerage Option (VBO®) account, you know that you can currently invest only in mutual funds. On April 1, 2013, you’ll also have a new class of investment alternatives in your VBO: exchange-traded funds (ETFs).

What Are Exchange-Traded Funds?

ETFs are built like conventional mutual funds but are priced and traded throughout the day like individual stocks. They create new opportunities for investors by offering:

• The advantages of mutual funds (diversification, liquidity, economies of scale in purchasing) with the trading features of individual stocks and bonds.

• Generally lower expense ratios than mutual funds.

Are ETFs Right for You?

An ETF may be appropriate if:

• You want the flexibility to buy and sell at current prices.

• You understand the risks of investing in the stock and bond markets.

• You are seeking potentially lower costs.

New Investment Choices in Your ESIP | 13

A Comparison of ETFs and Mutual Funds Within the VBO

How They Are the Same . . .• ETFs and mutual funds can both be bought and sold through your VBO account.

• Index ETFs and index mutual funds both attempt to track an investment benchmark. Likewise, actively managed ETFs and actively managed mutual funds both attempt to outperform an investment benchmark.

• ETFs and mutual funds both cover a wide range of stock market segments, investment styles, sectors, and industries, and bond market segments and maturities.

• Index ETFs and index mutual funds both feature generally lower operating expenses than comparable actively managed ETFs and actively managed mutual funds because of index tracking.

How They Are Different . . .

Exchange-Traded Funds Mutual Funds

Share price Market price fluctuates throughout the trading day.

Priced once a day after financial markets close.

Transaction costs No commissions on purchases of Vanguard ETFs®. For commissions on purchases of non-Vanguard ETFs, consult a VBO commission schedule, which is available from Vanguard.

No transaction costs on Vanguard funds. For transaction costs on non-Vanguard funds, log on to your ESIP account at vanguard.com, select the Research funds tab and choose Fees and expenses.

Trading flexibility Trades processed anytime during the trading day.

Transactions processed at the next closing net asset value.

What Is the Vanguard Brokerage Option (VBO)?

The VBO (your ESIP’s brokerage option) provides you with greater choice in your investment decision-making. With this option, you open an account with Vanguard Brokerage Services® under the ESIP. Then, you can invest a portion of your ESIP savings in thousands of mutual funds and ETFs from Vanguard and other companies that are not included in your ESIP’s core or supplemental investment options.

You can invest up to 50 percent of your plan balance, excluding Roth 401(k) after-tax contributions and earnings (if any), in the VBO. You pay a $50 annual fee for this option. Keep in mind that the risks are substantially higher with this strategy — and you’ll be responsible for paying commissions and other costs. Your plan also has specific provisions and restrictions that apply to your account. To learn more about the VBO or to open an account, you can speak with a Vanguard Participant Services associate (see page 15).

14 | February 2013

Chevron has organized your fund options into four tiers to help you make investment decisions. You can learn more about each of the funds by going to hr2.chevron.com and choosing Vanguard; then go to the ESIP Investment Guide tab on the top navigation to get started.

Tier Investment Option

Target Retirement Trusts – New Vanguard Target Retirement 2060 Trust

Vanguard Target Retirement 2055 Trust

Vanguard Target Retirement 2050 Trust

Vanguard Target Retirement 2045 Trust

Vanguard Target Retirement 2040 Trust

Vanguard Target Retirement 2035 Trust

Vanguard Target Retirement 2030 Trust

Vanguard Target Retirement 2025 Trust

Vanguard Target Retirement 2020 Trust

Vanguard Target Retirement 2015 Trust

Vanguard Target Retirement 2010 Trust

Vanguard Target Retirement Income Trust

Core Funds Vanguard Prime Money Market Fund Institutional Shares

Vanguard Short-Term Bond Index Fund Institutional Plus Shares

Vanguard Total Bond Market Index Fund Institutional Plus Shares

SSgA U.S. Inflation Protected Bond Index Fund Class C – New

Vanguard Balanced Index Fund Institutional Shares

Vanguard Institutional Index Fund Institutional Plus Shares

Vanguard Institutional Total Stock Market Index Fund Institutional Plus Shares

Vanguard Extended Market Index Fund Institutional Plus Shares

Vanguard Total World Stock Index Fund Institutional Shares – New

Vanguard Developed Markets Index Fund Institutional Plus Shares

Chevron Common Stock Fund

Chevron Leveraged ESOP Fund

Supplemental Funds Dodge & Cox Income Separate Account

Vanguard Windsor™ II Fund Admiral™ Shares

Artisan Mid Cap Fund Investor Class

Artisan Small Cap Value Fund Investor Class

Neuberger Berman Genesis Fund Institutional Class

Vanguard PRIMECAP Fund Admiral Shares

American Funds EuroPacific Growth Fund Class R-6

Vanguard Brokerage Option Mutual funds and ETFs

A note about risk. Because they concentrate on a single stock, the Chevron Common Stock Funds and the Chevron

Leveraged ESOP Funds are considered riskier than a stock mutual fund, which is diversified.

Summary of ESIP Investment Options Effective April 1, 2013

New Investment Choices in Your ESIP | 15

Connect with Vanguard® Have Questions or Need to Make a Change?

Contact Vanguard if you have any questions or if you would like to change how your contributions will be invested in light of the plan changes described in this newsletter. The investment choices described in this newsletter will be available starting April 1, 2013.

• Web access. Conduct account transactions, check account balances, research funds, create a financial plan and more. To access your account, go to hr2.chevron.com and choose Vanguard to log on.*

• Interactive phone service. Conduct transactions, get detailed fund information and more. Call 1-888-825-5247 (610-669-8595 if you’re outside the U.S.) and select option 1 to access Vanguard’s 24-hour VOICE® Network. You will need the VOICE personal identification number (PIN) you received in the mail from Vanguard to use this service. This PIN is different than the password you use to access your Vanguard account online.

• Participant Services Associates. Get personal assistance with transactions or ask questions about the ESIP. Call 1-888-825-5247 (610-669-8595 if you’re outside the U.S.) and select option 1. Associates are available from 5:30 a.m. to 6 p.m., Pacific time (7:30 a.m. to 8 p.m., Central time), Monday through Friday, except on stock market holidays.

*For security reasons, you must register for online access. Vanguard.com provides onscreen instructions to complete the registration process. You will be prompted to enter your plan number (095555).

Need Help With Your Retirement Planning?

The upcoming changes in your ESIP investment options may have you thinking seriously about your approach to saving and investing for retirement — maybe for the first time. If you’d like help with your financial planning or understanding how to invest, you may want to explore Vanguard’s advice services. Learn more at vanguard.com/chevronadvice or call Vanguard Participant Services as indicated above.

For more information about any fund, including investment objectives, risks, charges and expenses, call Vanguard

toll-free at 1-888-TALK2HR (1-888-825-5247) and select option 1 to obtain a prospectus for Vanguard funds and

1-800-339-4515 for non-Vanguard funds offered through Vanguard Brokerage Services. If you are outside the U.S.

and unable to dial a toll-free number, call 610-669-8595. The prospectus contains this and other important information

about the fund. Read and consider the prospectus information carefully before you invest. You can also download Vanguard

fund prospectuses at vanguard.com.

An investment in a money market fund is not insured or guaranteed by the Federal Deposit Insurance Corporation or any

other government agency. Although a money market fund seeks to preserve the value of your investment at $1 per share, it is

possible to lose money by investing in such a fund.

You must buy and sell Vanguard ETF Shares through a broker like Vanguard Brokerage Services (we offer them

commission-free) or through another broker (which may incur commissions). See the Vanguard Brokerage Services

Commission and Fee Schedules on vanguard.com for limits. Vanguard ETF Shares are not redeemable directly with the

issuing Fund other than in Creation Unit aggregations. Like stocks, ETFs are subject to market volatility. When buying or

selling an ETF, you will pay or receive the current market price, which may be more or less than net asset value.

Total International Bond Index Fund is subject to currency risk, which is the chance that currency hedging transactions may

not perfectly offset the fund’s foreign currency exposures and may eliminate any chance for a fund to benefit from favorable

fluctuations in those currencies. The fund will incur expenses to hedge its currency exposures.

A registration statement relating to Vanguard Total International Bond Index Fund has been filed with the Securities and

Exchange Commission but has not yet become effective. This security may not be sold nor may offers to buy be accepted

prior to the time the registration statement becomes effective. This communication shall not constitute an offer to sell or

the solicitation of an offer to buy, nor shall there be any sale of, this security in any state in which such offer, solicitation, or

sale would be unlawful prior to registration or qualification under the securities laws of any such state. Copies of the final

prospectus can be obtained from Vanguard. Please note that a preliminary prospectus is subject to change.

Vanguard Target Retirement Trusts are not mutual funds. They are collective trusts available only to tax-qualified plans and their eligible participants. Investment objectives, risks, charges, expenses and other important information should be considered carefully before investing. The collective trust mandates are managed by Vanguard Fiduciary Trust Company, a subsidiary of The Vanguard Group, Inc.

The Vanguard Group has partnered with Financial Engines to provide subadvisory services to the Vanguard Managed Account Program. Financial Engines is an independent, federally registered investment advisor that does not sell investments or receive commission for the investments it recommends. Advisory services are provided by Vanguard Advisers, Inc. (VAI), a federally registered investment advisor and an affiliate of The Vanguard Group, Inc. (Vanguard). Vanguard is owned by the Vanguard funds, which are distributed by Vanguard Marketing Corporation, a registered broker-dealer affiliated with VAI and Vanguard. Neither Vanguard, Financial Engines, nor their respective affiliates guarantee future results.

All rights in the FTSE Global All Cap Index (the “Index”) vest in FTSE International Limited (“FTSE”). “FTSE®” is a trademark of London Stock Exchange Group companies and is used by FTSE under licence. The Vanguard Total World Stock Index Fund (the “Product”) has been developed solely by Vanguard. The Index is calculated by FTSE or its agent. FTSE and its licensors are not connected to and do not sponsor, advise, recommend, endorse or promote the Product and do not accept any liability whatsoever to any person arising out of (a) the use of, reliance on or any error in the Index or (b) investment in or operation of the Product. FTSE makes no claim, prediction, warranty or representation either as to the results to be obtained from the Product or the suitability of the Index for the purpose to which it is being put by Vanguard.

This communication provides only certain highlights of benefits provisions. It is not intended to be a complete explanation. It is neither a summary plan description nor a summary of material modification. If there are any discrepancies between this communication and legal plan documents, the legal plan documents will rule. Chevron, as the plan sponsor, reserves the right to amend, change or terminate these plans for any reason at any time. Some benefit plans and policies described in this communication may be subject to collective bargaining and, therefore, may not apply to union-represented employees.

Vanguard, VBO, Vanguard Brokerage Services, VMAP, Vanguard ETFs, vanguard.com, VOICE, Admiral, Windsor and Connect with Vanguard are trademarks of The Vanguard Group, Inc.

Vanguard Brokerage Services is a division of Vanguard Marketing Corporation, Member FINRA.

Vanguard Marketing Corporation, Distributor of the Vanguard Funds.

© 2013 The Vanguard Group, Inc. All rights reserved. U.S. Pat. No. 6,879,964 B2; 7,337,138; 7,720,749; 7,925,573; 8,090,646.

© 2013 Chevron Corporation. All rights reserved.

BBBBFYPT 022013 Recyclable paper