new year pick - hdfc securities year pick.pdf · music broadcast ltd, 70.5% subsidiary of the...

TRANSCRIPT

NEW

YEARPICKS

JAGRAN PRAKASHAN

THE SOUTH INDIAN BANK

NCC LTD.

2018

01

India Inc earnings on the cusp of recovery amid plentiful domestic liquidity, but valuations weigh…With the BJP winning both the state elections, focus would now shift to important economic events – Bank recap, Union Budget, GST collection trends, economic growth data points, progress under insolvency code and interest rate trajectory. Implementation of the earlier announced reform measures may be seen rather than more big bang fresh announcements. Based on the outcome from these elections and the four more state elections due in the rst half of calendar 2018, the Govt is likely to focus more on the rural and agriculture sector. Creation of jobs at an accelerated pace could be one more focus area. The urban populace may not get anything major to rejoice in the near term.

Markets will watch out for earnings upgrade for companies following normalisation of economic conditions (post GST, demonetisation, RERA related disruptions); also given the fact that global commodity cycle is on the upswing. While condence about earnings growth is rising, current valuation levels could prevent a full-on bull run from these levels.

December 26, 2017

VotE

The recent PSU Bank recap announcement is likely to provide greater avenues for lending for banks and enable banks to take bigger haircuts on stressed assets, push forward the resolution process and set the stage for a capex cycle recovery in the medium term. This along with the Bharatmala and Housing for All initiatives by the Govt has multi-fold implications and can materially revive the capex cycle along with potential acceleration in housing, railways and defence ultimately having a multiplier impact on GDP.

With national elections due in May 2019, Govt has refocused on growth going by its recent actions of fuel tax cuts, raising import duty on agri commodities, GST rate rationalisation, higher MSP hikes and bank recap plan. Though coupled with near term pain of higher scal decit, these initiatives could put India on accelerated growth trajectory FY19 onwards.

Biggest area of concerns would be worsening macros, delay in resumption of GDP growth and sustained interest rate rise in developed economies.

Liquidity in the markets continue to be good especially from the domestic investors through Mutual fund route (both lumpsum and SIP). These investors will keep investing as long as the markets do not fall sharply and then do not stay at low levels.

FIIs could re-evaluate investing in India in a big way only when ination comes under control, and economic growth starts picking momentum. Globally the risk-on sentiment is alive. And a lot of the developed markets are witnessing “rational exuberance”. However there is some uncertainty on the timing, pace and quantum of interest rate hikes to be conducted by the Central banks globally

PICKS

As far as the equity markets are concerned, the focus may slowly shift from liquidity to earnings. An issue for worry is whether the markets have fully discounted all the India positives in advance and is going overboard on valuation just based on expected unending inows from global/domestic sources.

Indian bond yields have hardened in recent months. Larger GoI spending on rural and infra, lower rabi output, state governments’ HRA implementation and higher crude prices could all have a negative impact on ination and interest rates. This could take away some attraction from equities in terms of valuation multiples.

Markets are awaiting resolution of rst large case under the Insolvency and Bankruptcy code, which is taking longer than expected. This could be a positive trigger for both the lenders and the troubled sector/s.

While the largecaps have their own headwinds in different spheres, mid and small caps will keep throwing up surprises in stock moves based on their small size/base, faster adjustment to emerging changes, nancial and operational restructuring, corporate announcements including merger, demerger, hive-offs, turnaround, asset value unlocking etc.

Retail investors would do well to stick to their asset allocation plans, review their small and midcap holdings closely and bring down their return expectations for the next few quarters.

The calendar year 2017 has been a great year for investors with the Nifty giving ~28% return. Investors would do well to moderate their expectations for index returns in calendar 2018. We feel that investors would keep getting individual stock opportunities that could yield much higher returns. Metals, Pharma, IT, Cement and infra are some sectors to watch out for in 2018.

We give below the picks for 2018

Jagran Prakashan

CMP : Rs. 170.45

TARGET PRICE : Rs.199-215

South Indian Bank

CMP : Rs. 31.55

TARGET PRICE : Rs.38-41

NCC Ltd

CMP : Rs. 132

TARGET PRICE : Rs.162-195

RADIO

NEWS

`

02

PICKS

HDFC Scrip Code

BSE Code

NSE Code

Bloomberg

CMP as on 22 Dec 17

Equity Capital (Rs Cr)

Face Value (Rs)

Equity Sh. Outstanding

Market Cap (Rs Cr)

Book Value (Rs)

Avg. 52 Week Volumes

52 Week High

52 Week Low

JAGPRAEQNR

532705

JAGRAN

JAGP

170.45

62.28

2

31.14

5,222

65.6

237824

208.5

161

Promoters

Institutions

Non Institutions

Total

60.85

24.53

14.63

100

Shareholding Pattern

10 newspaper titles in 5 different languages,

sweeping across 13 states with over 400+

editions

Radio industry is expected to grow at an

excellent rate

CMP

Rs. 170.45

Recommendation

Buy at CMP and add on dips

Add on Dips to band

Rs. 170-154

Target

Rs. 199-215

Fundamental Research Analyst:Nisha [email protected]

Indian M&E industry has grown at an excellent pace though well below global average level – which leaves ample room for growth.

Besides traditional advertisers such as the FMCG and automobile industries its growth is also expected to be driven by ecommerce, payment banks, telecom services, financial technology, content distribution platforms, and the social media sector. Election season is always good for print media and the upcoming 8 state elections will lead to higher advertising spend which is likely to benefit the company.

Jagran Prakashan Ltd is India's leading media and communication group. It has a pan India footprint with interests spanning across Print, OOH, Radio and Digital. The Company publishes approximately 10 newspaper titles in 5 different languages, sweeping across 13 states with over 400+ editions. Music Broadcast ltd, 70.5% subsidiary of the company, owns 39 radio stations across India.

Key highlights

Jagran Prakashan

Time Horizon

1 Year

Industry

Media

03

PICKS

Digital Advertising is the fastest growing vertical

in the Indian M&E industry

AAA E

We recommend Jagran Prakashan BUY at CMP of Rs. 170.45 (10x of FY20 EPS) and add on decline of Rs. 154 for the sequential Targets of Rs.199 (12.1x of FY20 EPS) and Rs.215 (13.1x of FY20 EPS).

Radio industry is expected to grow at an excellent rate going forward due to an increase in listenership. It is rapidly becoming a medium of choice of advertisers. Digital Advertising is the fastest growing vertical in the Indian M&E industry and going forward, we expect high growth on the back of higher internet speed, low cost of bandwidth and Government’s push for ‘Digital India’.

We recommend Jagran Prakashan BUY at CMP of Rs. 170.45 (10x of FY20 EPS) and add on decline of Rs. 154 for the sequential Targets of Rs.199 (12.1x of FY20 EPS) and Rs.215 (13.1x of FY20 EPS).

Sales

EBITDA

Net Profit

EPS (Rs)

P/E

BV

P/BV

2079

640

307

10.7

15.4

49.6

3.3

(Rs Cr) FY16

2283

681

349

10.7

15.4

65.6

2.5

Financial Summary (Consolidated)

2477

667

356

11.4

14.5

78.2

2.1

2799

795

435

14.0

11.8

89.0

1.9

(Source: Company, HDFC sec)

FY17 FY18E FY19E

3135

912

510

16.4

10.1

101.6

1.6

FY20E

Jagran Prakashan

04

PICKS

Jagran Prakashan

Total Income

Growth (%)

Operating Expenses

EBITDA

Depreciation

EBIT

Interest

PBT

Tax

RPAT

Growth (%)

EPS

Income Statement

2129

18.2

1488.8

640.4

121.9

519

54.5

464

157.2

307

34.7

10.7

2324

9.2

1643.4

680.8

128.9

552

35.0

517

167.5

349

13.8

10.7

2502

7.7

1835.4

666.6

125.0

542

18.3

523

167.5

356

1.9

11.4

2839

13.5

2043.9

795.1

130.0

665

24.8

640

204.9

435

22.4

14.0

3185

12.2

2272.5

912.4

135.0

777

26.7

751

240.2

510

17.2

16.4

Year ending March (Rs Cr) FY16 FY17 FY18E FY19E FY20E

Share Capital

Reserves

Long Term Debt

Net Deferred Taxes

Long Term Provisions & Others

Total Source of Funds

Net Block

Deferred Tax Assets (net)

Long Term Loans & Advances

Total Non Current Assets

Current Investments

Inventories

Trade Receivables

Short term Loans & Advances

Cash & Equivalents

Other Current Assets

Total Current Assets

Short-Term Borrowings

Trade Payables

Other Current Liab & Provisions

Total Current Liabilities

Total Application of Funds

Balance Sheet

65.4

1568

259.2

179.3

14.8

2120

1422

34.5

90.3

1547

349.0

66.9

448.0

54.2

50.2

38.3

1154

255.6

83.3

239.0

580.9

2119

As at March (Rs mn) FY16

65.4

2095

50.2

197.1

17.0

2661

1491

26.9

559.5

2077

29.3

93.5

515.8

43.4

349.1

53.4

1167

83.3

146.7

348.1

583.1

2661

62.3

2372

65.3

300.0

25.0

2835

1789

30.0

490.6

2310

29.3

101.8

542.9

80.2

581.1

58.7

1352

166.5

172.4

487.4

826.3

2835

62.3

2709

68.5

200.0

35.0

3085

2237

50.0

510.2

2797

35.0

107.4

613.5

120.4

523.0

81.6

1309

174.8

186.9

657.9

1019.7

3086

62.3

3102

69.9

200.0

40.0

3484

2796

60.0

561.7

3417

30.0

111.7

687.1

180.5

496.8

121.6

1321

180.1

205.0

868.5

1253.5

3484

FY17 FY18E FY19E FY20E

EBITDA Margin

APAT Margin

RoE

RoCE

Net Debt/EBITDA (x)

D/E

Interest Coverage

Dividend

Debtor days

Inventory days

Creditors days

EV/EBITDA

EV / Revenues

Dividend Yield (%)

30.8

14.8

20.8

24.5

0.2

0.3

9.5

0.0

79

14

48

7.8

2.4

0.0

29.8

15.3

18.4

20.7

-0.4

0.1

15.8

3.0

82

13

82

7.3

2.2

1.8

26.9

14.4

15.5

19.1

-0.6

0.1

29.7

2.4

80

15

85

7.5

2.0

1.4

28.4

15.6

16.7

21.6

-0.4

0.1

26.9

3.0

80

14

83

6.3

1.8

1.8

29.1

16.3

17.2

22.3

-0.3

0.1

29.2

3.6

80

13

82

5.4

1.6

2.2

Key Ratios (Consolidated)

Year ending March (Rs Cr) FY16 FY17 FY18E FY19E FY20E

05

PICKS

Jagran Prakashan

Year ending March (Rs Cr) FY16 FY17 FY18E FY19E FY20E

Reported PBT

Non-operating & EO items

Interest Expenses

Depreciation

Working Capital Change

Tax Paid

OPERATING CASH FLOW ( a )

Capex

Free Cash Flow

Investments

Non-operating income

INVESTING CASH FLOW ( b )

Debt Issuance / (Repaid)

Interest Expenses

FCFE

Share Capital Issuance

Dividend

FINANCING CASH FLOW ( c )

NET CASH FLOW (a+b+c)

Closing Cash

464

-244

55

122

-513

-157

-273

-649

-922

306

50

-293

147

-55

-829

34

-4

123

-443

50

517

175

35

129

223

-168

912

-69

843

-462

41

-489

-189

-35

619

203

-102

-123

299

349

523

-25

18

125

166

-167

640

-298

342

66

25

-207

126

-18

449

-229

-79

-200

232

581

640

-40

25

130

48

-205

599

-447

151

-40

40

-447

-87

-25

40

0

-98

-210

-58

523

751

-50

27

135

61

-240

683

-559

124

-62

50

-571

6

-27

103

0

-118

-138

-26

497

Cash Flow Statement

06

PICKS

(Source: Company, HDFC sec)

HDFC Scrip Code

BSE Code

NSE Code

Bloomberg

CMP as on 22 Dec 17

Equity Capital (Rs Cr)

Face Value (Rs)

Equity Sh. Outstanding

Market Cap (Rs Cr)

Book Value (Rs)

Avg. 52 Week Volumes

52 Week High (Rs)

52 Week Low (Rs)

SOUBANEQNR

532218

SOUTHBANK

SIB

31.55

180.58

1

180.58

5,679

26.2

17015823

33.5

16.8

Promoters

Institutions

Non Institutions

Total

0

50.17

49.83

100

Shareholding Pattern

SIB has successfully managed to keep a tight leash on bad

assets

Adopted a strategy to increase exposure in

retail & SME– high yield segments

Technology banking will provide significant

uptick in terms of costs, efficiency,

revenue and margins

Industry

Bank

CMP

Rs. 31.55

Recommendation

Buy at CMP and add on dips

Add on Dips to band

Rs. 31.55-29.5

Target

Rs. 38-41

Time Horizon

1 Year

Fundamental Research Analyst:Devarsh [email protected]

The bank is well capitalized with a CAR of 12.4% in FY17. Bank will use this capital to support growth plans and to enhance the business.

While the whole Industry is under NPA pressure, SIB has successfully managed to keep a tight leash on bad assets. Watch list at the end of Q2FY18 has been reduced to “Zero”, and we do not expect any incremental negative news on this front. Its GNPA at the end of Q2FY18 stood at an elevated level of 3.54% vs 2.45% in FY17 and NNPA at 2.57% vs 1.45% in FY17. We expect that as per management guidance, the bank will take active measures in restructuring the stressed assets.

South Indian Bank is a mid-sized bank in the private sector space, which operates network of about 851 branches and about 1,354 ATMs. The bank’s business is largely skewed towards the Southern state with half of its branches located in Kerala. The Bank's segments include Treasury, Corporate/Wholesale Banking, Retail banking and Other Banking Operations.

Key highlights

South Indian Bank

07

PICKS

We recommend SIB a BUY at CMP and add on declines to Rs. 31.55-29.5 band for sequential targets of Rs. 38 (1.3x FY20E ABV) and Rs. 41 (1.4x FY20E ABV).

Bank has adopted a strategy to increase exposure in retail & SME– high yield segments. The change in stance was due to concern over asset quality and slowdown in credit growth in large corporate segment.

Bank has set up a separate digital banking department for product development and process improvement of all technological products. Technology banking will provide significant uptick in terms of costs, efficiency, revenue and margins. At CMP of Rs.31.5, SIB is trading at an attractive valuation of 1x P/ABV of FY20. We recommend SIB a BUY at CMP and add on declines to Rs. 31.5-29.5 band for sequential targets of Rs. 38 (1.3x FY20E ABV) and Rs. 41 (1.4x FY20E ABV).

NII

Growth %

PPOP

PAT

Growth %

BV

P/BV

394.1

7.2

509.7

333.3

8.5

18.7

1.7

(Rs Cr) FY16

522.9

32.7

600.6

392.8

17.9

21.8

1.4

Financial Summary

568.3

8.7

518.9

337.3

-14.1

23.8

1.3

791.1

39.2

861.3

568.5

68.5

26.6

1.2

(Source: Company, HDFC sec)

FY17 FY18E FY19E

1021.7

29.2

1107.5

731.0

28.6

30.3

1.0

FY20E

South Indian Bank

08

PICKS

Interest income

Interest expended

Net interest income

Growth (%)

Other income

Net Operating Income

Growth (%)

Operating expenses

Operating Profit

Provisions and contingencies

PBT

Tax paid (provision)

PAT

Growth (%)

Income Statement

1309.24

915.10

394.14

7.24

517.42

911.56

5.43

1147.84

879.27

369.62

509.65

176.40

333.25

8.46

1686.92

1164.04

522.88

32.66

715.60

1238.48

35.86

1176.00

1215.00

614.37

600.63

207.80

392.83

17.88

1935.72

1367.43

568.29

8.68

772.85

1341.14

8.29

1293.60

1486.83

967.92

518.91

181.62

337.29

-14.14

2446.02

1654.92

791.10

39.21

850.13

1641.23

22.38

1448.83

1883.68

1022.35

861.33

292.85

568.48

68.54

3583.43

2561.69

1021.74

29.15

935.15

1956.89

19.23

1593.72

2287.72

1180.22

1107.50

376.55

730.95

28.58

Year ending March (Rs Cr) FY16 FY17 FY18E FY19E FY20E

Liabilities

Equity Capital

Reserves & surplus

Networth

Deposits

Borrowings

Other Current liabilities & provisions

Assets

Cash and balances with RBI

Money at call and short notice

Investments

Advances

Net fixed assets

Other assets

Balance Sheet

63,522

135.03

3706.89

3,846

55,721

2,615

1,341

63,522

2,476

798

14,744

41,086

487

3,931

As at March (Rs Cr) FY16

74,366

180.28

4665.19

4,848

66,117

1,958

1,442

74,366

3,078

810

19,430

46,389

656

4,003

82,424

180.28

4872.682

5,056

72,729

2,909

1,730

82,424

2,909

5,532

16,000

52,884

695

4,403

92,921

180.28

5311.357

5,495

82,184

3,339

1,903

92,921

3,287

5,357

18,080

60,711

730

4,755

1,07,627

180.28

5912.5

6,096

95,333

4,085

2,113

1,07,627

3,813

6,513

20,973

70,425

767

5,136

FY17 FY18E FY19E FY20E

South Indian Bank

Calc. Yield on adv

Calc. Cost of Fund

NIM

RoAE

RoAA

GNPA

NNPA

Advances

Borrowings

Deposit

NII

PPOP

11.1

7.1

2.5

8.97

0.54

3.8

2.9

9.9

28.7

6.9

10.5

-0.3

10.2

6.5

2.4

9.04

0.57

2.5

1.5

12.9

-25.1

18.7

11.0

38.2

10.9

6.6

2.6

6.82

0.43

2.6

1.4

14.0

48.6

10.0

19.8

22.4

11.0

6.3

2.8

10.78

0.65

2.1

1.2

14.8

14.8

13.0

23.7

26.7

11.0

6.2

2.9

12.62

0.73

1.5

0.9

16.0

22.3

16.0

18.7

21.4

Key Ratios

Year ending March (Rs Cr) FY16 FY17 FY18E FY19E FY20E Year ending March (Rs Cr) FY16 FY17 FY18E FY19E FY20E

PAT

EPS

P/E

Adj. BVPS

P/ABV

Dividend Yield (%)

Cost-Income

Credit-Deposit

CAR (%)

PCR (%)

CASA Ratio%

8.4

2.47

12.8

18.7

1.7

1.6

56.6

73.7

11.8

40.3

22.4

17.9

2.18

14.5

21.8

1.4

1.3

49.2

70.2

12.4

55.1

23.8

-14.4

1.87

16.9

23.8

1.3

1.9

46.5

72.7

11.7

44

24.5

68.7

3.15

10.0

26.6

1.2

1.9

43.5

73.9

11.6

44

24.5

28.6

4.05

7.8

30.3

1.0

1.9

41.1

73.9

11.5

40

24.5

09

PICKS

Key Ratios

(Source: Company, HDFC sec)

HDFCSec Scrip Code

BSE Code

NSE Code

Bloomberg

CMP (as on 22 Dec, 17)

Equity Capital (Rs mn)

Face Value (Rs)

Equity Sh Outs. (mn)

Market Cap (Rs bn)

Book Value (Rs)

Avg. 52 Week Volumes

52 Week High

52 Week Low

NAGCONEQNR

500294

NCC

NJCC IN

132.45

1111.9

2

555.9

73.6

61.92

5,300,000

134.4

75.1

Promoters

Institutions

Non Institutions

Total

19.57

45.61

34.82

100.00

Shareholding Pattern % (Sep 2017)

Industry

Infrastructure

CMP

Rs. 132

Recommendation

Buy at CMP and add on dips

Add on Dips to band

Rs. 109-115

Target

Rs. 162-195

Time Horizon

1 Year

Fundamental Research Analyst:Atul [email protected]

Established in 1978, as a partnership rm and converted into a limited company in 1990, NCC is among the top three construction companies in India in terms of revenues. NCC undertakes civil construction in segments such as buildings, water, roads, irrigation, power, electrical, railways, metals, mining and has also a presence in the Middle East where it currently undertakes works in roads, buildings and water segments. In India, it has operations in 25 out of 29 states. As a developer, NCC owns and operates two road projects both of which are operational. The company also has large land bank in Hyderabad, Bangalore, Vizag and Ranchi which it is developing through its urban infra subsidiary. NCC had an outstanding order book of ~Rs 219 bn (3xTTM revenues) as of Q2FY18.

NCC is among the top three construction

companies in India in terms of revenues

Pickup in government tendering has led to NCC securing fresh

orders worth Rs 149 bn in 7MFY18

The government has announced significant

infrastructure projects. These project could

result in higher order inflows in coming years

Key highlights

NCC Ltd.

Pickup in government tendering has led to NCC securing fresh orders worth Rs 149 bn in 7MFY18, most of which are short duration projects of 12-14 months. Additionally, the

10

PICKS

We are positive on NCC due to the above but our estimates are conservative. It has strong Q2FY18-end balance sheet with net D/E at 0.55x, concentrated focus on Infra EPC segment and well-diversified presence across different sub-segments. We value NCC’s standalone business at 11x/13x FY20E EV/EBIDTA and investments at book value.

company's 51:49 JV with BGR Mining won over Rs 250 bn mine development and operation order for Talai-Palli coal block from NTPC for 25 years from FY20. Order-book to sales after stagnating in 2.1x-2.3x over FY16-FY17 has risen to 3.0x currently.

The government has announced significant plans for roads under Bharatmala road project, given incentives to affordable housing schemes and budgetary support of $23 bn is expected over next 5 years for improvement in rural water supply & sanitation. Metro projects are coming up in large cities and Government is investing in upgrading rail infrastructure and develop Eastern & Western Direct Freight corridors & High Speed Railway. All these projects could result in higher order inflows for NCC in the coming years.

NCC Urban is monetising certain land parcels (has 311 acres across southern cities/Ranchi under development/yet to begin) and repaid part of the debt taken from the parent during the current year. This is likely to bring down the consolidated debt of the company and reduce finance expenses further.

With the crude prices stabilizing and inching up, capex cycle is expected to revive in the Gulf countries in the medium term.

NCC Ltd.

NCC Standalone

Investment in subsidiaries

Total

Construction business

Particulars Segments

11x/13x FY20 EV/EBIDTA

Book Value

SOTP Valuation

79838/98367

10287

64,407

144/177

19

162/195

Methodology Value (Rs mn) Value per share

11

PICKS

Net Revenues

EBITDA

APAT

Diluted EPS (Rs)

P/E (x)

EV / EBITDA (x)

RoE (%)

83,252

7,376

2,402

4.3

30.7

12.2

7.4

(Rs mn) FY16

78,921

6,852

2,255

4.1

32.7

12.9

6.7

Financial Summary

75,634

6,920

2,987

5.4

24.6

13.1

8.5

89,938

8,104

2,477

4.5

29.7

11.5

6.7

FY17 FY18E FY19E

1,02,256

9,265

2,728

4.9

27.0

10.3

7.0

FY20E

NCC Ltd.

12

PICKS

Net Revenues

Growth (%)

EBITDA

EBITDA Margin (%)

Depreciation

Other Income (Including EO Items)

Interest

PBT

Tax (Incl Deferred)

Reported PAT

EO Items

Adj. PAT

APAT Growth (%)

Adjusted EPS (Rs)

Income Statement

78,921

(5.2)

6,852

8.7

1,121

1,401

3,957

3,175

417

2,758

503

2,255

(6.1)

4.1

75,634

(4.2)

6,920

9.15

1,174

1,051

3,680

3,116

843

2,273

(714)

2,987

32.5

5.4

89,938

18.9

8,104

9.0

1,258

897

4,206

3,538

1,061

2,477

-

2,477

(17.1)

4.5

1,02,256

13.7

9,265

9.1

1,341

628

4,654

3,897

1,169

2,728

-

2,728

10.1

4.9

Year ending March (Rs mn) FY17 FY18E FY19E FY20E

STANDALONE FINANCIALS:

SOURCES OF FUNDS

Equity Capital

Reserves

Total Shareholders Funds

Total Debt

Net Deferred Taxes, Other LT Liab, etc.

TOTAL SOURCES OF FUNDS

APPLICATION OF FUNDS

Net Block & CWIP

Investments, LT Loans & Advances

Total Non-current Assets

Inventories

Debtors

Other Current Assets

Cash & Equivalents

Creditors

Other Current Liabilities & Provns

Net Current Assets

TOTAL APPLICATION OF FUNDS

Balance Sheet

As at March (Rs mn)

1,112

33,311

34,423

15,767

(600)

49,590

6,416

12,952

19,368

15,258

23,501

28,713

1,095

28,681

9,871

30,015

49,590

1,112

34,608

35,720

19,267

(600)

54,387

6,503

12,952

19,454

15,675

21,758

31,497

1,920

26,938

8,979

34,933

54,387

1,112

36,822

37,934

21,567

(600)

58,901

6,445

12,952

19,396

18,737

24,640

35,729

1,764

30,801

10,565

39,505

58,901

1,112

39,288

40,400

23,867

(600)

63,667

6,303

12,952

19,255

21,215

26,614

37,821

1,792

32,218

10,812

44,412

63,667

FY17 FY18E FY19E FY20E

(Source: Company, HDFC sec)

13

PICKS

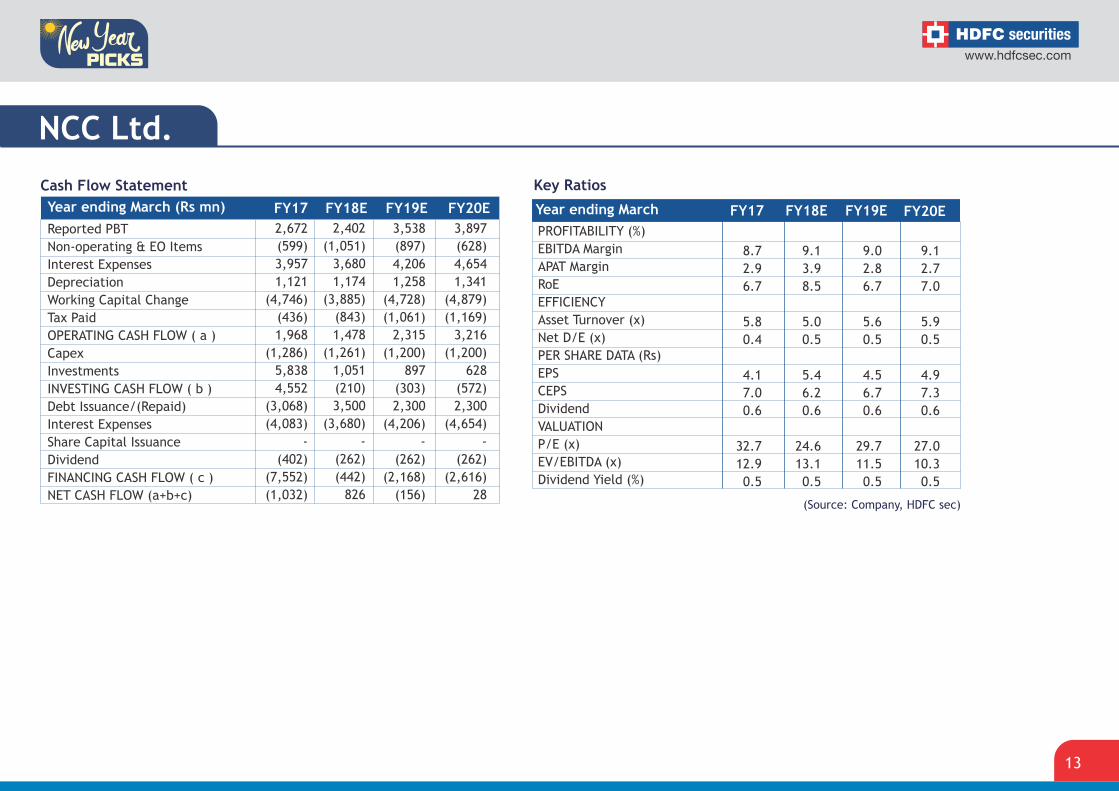

Year ending March (Rs mn) FY17 FY18E FY19E FY20E

Reported PBT

Non-operating & EO Items

Interest Expenses

Depreciation

Working Capital Change

Tax Paid

OPERATING CASH FLOW ( a )

Capex

Investments

INVESTING CASH FLOW ( b )

Debt Issuance/(Repaid)

Interest Expenses

Share Capital Issuance

Dividend

FINANCING CASH FLOW ( c )

NET CASH FLOW (a+b+c)

2,672

(599)

3,957

1,121

(4,746)

(436)

1,968

(1,286)

5,838

4,552

(3,068)

(4,083)

-

(402)

(7,552)

(1,032)

2,402

(1,051)

3,680

1,174

(3,885)

(843)

1,478

(1,261)

1,051

(210)

3,500

(3,680)

-

(262)

(442)

826

3,538

(897)

4,206

1,258

(4,728)

(1,061)

2,315

(1,200)

897

(303)

2,300

(4,206)

-

(262)

(2,168)

(156)

3,897

(628)

4,654

1,341

(4,879)

(1,169)

3,216

(1,200)

628

(572)

2,300

(4,654)

-

(262)

(2,616)

28

Cash Flow Statement

PROFITABILITY (%)

EBITDA Margin

APAT Margin

RoE

EFFICIENCY

Asset Turnover (x)

Net D/E (x)

PER SHARE DATA (Rs)

EPS

CEPS

Dividend

VALUATION

P/E (x)

EV/EBITDA (x)

Dividend Yield (%)

8.7

2.9

6.7

5.8

0.4

4.1

7.0

0.6

32.7

12.9

0.5

9.1

3.9

8.5

5.0

0.5

5.4

6.2

0.6

24.6

13.1

0.5

9.0

2.8

6.7

5.6

0.5

4.5

6.7

0.6

29.7

11.5

0.5

9.1

2.7

7.0

5.9

0.5

4.9

7.3

0.6

27.0

10.3

0.5

Key Ratios

Year ending March FY17 FY18E FY19E FY20E

NCC Ltd.

(Source: Company, HDFC sec)

Jagran Prakashan South Indian Bank

NCC Ltd

1 year price movement

14

PICKS

JAGRAN PRAKASHAN

THE SOUTH INDIAN BANK

NCC LTD

Company Team

PCG

PCG

RETAIL RESEARCH

Disclosure

Holding

NO

YES

No

Analyst

NISHA SANKHALA

DEVARSH VAKIL

ATUL KARWA

HDFC securities Limited, I Think Techno Campus, Building - B, "Alpha", Ofce Floor 8, Near Kanjurmarg Station, Opp. Crompton Greaves, Kanjurmarg (East), Mumbai 400 042 Phone: (022) 3075 3400 Fax: (022) 2496 5066

Website: www.hdfcsec.com

Compliance Ofcer: Binkle R. Oza Email: [email protected] Phone: (022) 3045 3600

Disclosure:

I,/We, authors and the names subscribed to this report, hereby certify that all of the views expressed in this research report accurately reect our views about the subject issuer(s) or securities. HSL has no material adverse disciplinary history as on the date of publication of this report. We also certify that no part of our compensation was, is, or will be directly or indirectly related to the specic recommendation(s) or view(s) in this report.

Research Analyst or his/her relative or HDFC Securities Ltd. does not have any nancial interest in the subject company. Also Research Analyst or his relative or HDFC Securities Ltd. or its Associate does not have benecial ownership of 1% or more in the subject company at the end of the month immediately preceding the date of publication of the Research Report. Further Research Analyst or his relative or HDFC Securities Ltd. or its associate does not have any material conict of interest.

HDFC Securities Limited (HSL) is a SEBI Registered Research Analyst having registration no. INH000002475.

Disclaimer:

This report has been prepared by HDFC Securities Ltd and is meant for sole use by the recipient and not for circulation. The information and opinions contained herein have been compiled or arrived at, based upon information obtained in good faith from sources believed to be reliable. Such information has not been independently veried and no guaranty, representation of warranty, express or implied, is made as to its accuracy, completeness or correctness. All such information and opinions are subject to change without notice. This document is for information purposes only. Descriptions of any company or companies or their securities mentioned herein are not intended to be complete and this document is not, and should not be construed as an offer or solicitation of an offer, to buy or sell any securities or other nancial instruments.

This report is not directed to, or intended for display, downloading, printing, reproducing or for distribution to or use by, any person or entity who is a citizen or resident or located in any locality, state, country or other jurisdiction where such distribution, publication, reproduction, availability or use would be contrary to law or regulation or what would subject HSL or its afliates to any registration or licensing requirement within such jurisdiction.

If this report is inadvertently send or has reached any individual in such country, especially, USA, the same may be ignored and brought to the attention of the sender. This document may not be reproduced, distributed or published for any purposes without prior written approval of HSL.

Foreign currencies denominated securities, wherever mentioned, are subject to exchange rate uctuations, which could have an adverse effect on their value or price, or the income derived from them. In addition, investors in securities such as ADRs, the values of which are inuenced by foreign currencies effectively assume currency risk.

It should not be considered to be taken as an offer to sell or a solicitation to buy any security. HSL may from time to time solicit from, or perform broking, or other services for, any company mentioned in this mail and/or its attachments.

15

PICKS

Education

MBA

MBM

MMS

HSL and its afliated company(ies), their directors and employees may; (a) from time to time, have a long or short position in, and buy or sell the securities of the company(ies) mentioned herein or (b)

be engaged in any other transaction involving such securities and earn brokerage or other compensation or act as a market maker in the nancial instruments of the company(ies) discussed herein or

act as an advisor or lender/borrower to such company(ies) or may have any other potential conict of interests with respect to any recommendation and other related information and opinions.

HSL, its directors, analysts or employees do not take any responsibility, nancial or otherwise, of the losses or the damages sustained due to the investments made or any action taken on basis of this

report, including but not restricted to, uctuation in the prices of shares and bonds, changes in the currency rates, diminution in the NAVs, reduction in the dividend or income, etc.

HSL and other group companies, its directors, associates, employees may have various positions in any of the stocks, securities and nancial instruments dealt in the report, or may make sell or

purchase or other deals in these securities from time to time or may deal in other securities of the companies / organizations described in this report.

HSL or its associates might have managed or co-managed public offering of securities for the subject company or might have been mandated by the subject company for any other assignment in the

past twelve months.

HSL or its associates might have received any compensation from the companies mentioned in the report during the period preceding twelve months from t date of this report for services in respect of

managing or co-managing public offerings, corporate nance, investment banking or merchant banking, brokerage services or other advisory service in a merger or specic transaction in the normal

course of business.

HSL or its analysts did not receive any compensation or other benets from the companies mentioned in the report or third party in connection with preparation of the research report. Accordingly,

neither HSL nor Research Analysts have any material conict of interest at the time of publication of this report. Compensation of our Research Analysts is not based on any specic merchant banking,

investment banking or brokerage service transactions. HSL may have issued other reports that are inconsistent with and reach different conclusion from the information presented in this report.

Research entity has not been engaged in market making activity for the subject company. Research analyst has not served as an ofcer, director or employee of the subject company. We have not

received any compensation/benets from the subject company or third party in connection with the Research Report.

This report is intended for non-Institutional Clients only. The views and opinions expressed in this report may at times be contrary to or not in consonance with those of Institutional Research or PCG

Research teams of HDFC Securities Ltd. and/or may have different time horizons

HDFC Securities Limited, SEBI Reg. No.: NSE-INB/F/E 231109431, BSE-INB/F 011109437, AMFI Reg. No. ARN: 13549, PFRDA Reg. No. POP: 04102015, IRDA Corporate Agent License No.: HDF

2806925/HDF C000222657, SEBI Research Analyst Reg. No.: INH000002475, CIN - U67120MH2000PLC152193

16

PICKS