news letter - ifmp

TRANSCRIPT

BUSINESS AND ECONOMIC NEWSFLASH

URDU GLOSSARY

MARKETS IN REVIEW

QUOTES AND JOKES

TERMS OF THE MONTH

VOLUNTARY PENSION SCHEMES IN PAKISTAN

NEWSLETTER JULY 2017

Institute of Financial Markets of Pakistan

The name of the institute has been changed

from Institute of Capital Markets to

Institute of Financial Markets of Pakistan

Contact Us

Address: Park Avenue Building, Suite No. 1009,

10th Floor, P.E.C.H.S Block No. 6, Shahrah-e-Faisal,

Karachi

Tel: +92 (21) 34540843-44

MESSAGE FROM THE CEO

INTRODUCTION TO THE INSTITUTE

TERMS OF THE MONTH

BUSINESS AND ECONOMIC NEWSFLASH

URDU GLOSSARY

QUOTES AND JOKES

MARKETS IN REVIEW

ARTICLE ON

PERFORMANCE OF BANKING STOCKS

IN PAKISTAN

SECURITIES AND FUTURES ADVISORS’

CERTIFICATION PROGRAMME LAUNCHED

00 CONTENT

01

Message from the CEO

02

Introduction to the

Institute

03

Performance of

Banking Stocks in

Pakistan

04

Terms of the Month

07

Quotes and Jokes

08

Markets in Review

06

Urdu Glossary

Page: 3 Page: 4

Page: 12 Page: 14

Page: 15 Page: 16

www.ifmp.org.pk 92 (21) 34540843-44 [email protected]

05

Business and Economic

Newsflash

Page: 13

Page: 5

01

Message from the Chief Executive Officer

◊ July 2017 IFMP Newsletter Page 3 ◊

he last few years have seen a rapid growth in size, quality and

sophistication of financial markets, because of changes in the

policy and regulatory environment, the entrepreneurial initiatives

of individuals and institutions, and the availability of trained man-

power. The continuing growth of financial markets is further adding

to the demand for well-trained professionals.

Institute of Financial Markets of Pakistan is dedicated to the profes-

sional development of financial markets and research on financial markets as well as the

well being of financial markets by educating the professionals about the norms and ethics

being practiced in the markets. IFMP has had a pioneering role in meeting the demand for

educated manpower. It is Pakistan's first specialized institution devoted to the education

and updating of knowledge of manpower for financial markets. It will provide high-

quality educational standards for all types of financial market participants; investors,

brokers, mutual funds, investment banks and policy makers.

The Institute's main activities are (1) Licensing the professionals working in the financial

markets by certifications. The institute’s key responsibility is to educate the professionals

working in different financial markets of Pakistan through examining their knowledge in

their relevant field of work; (2) Studying the latest developments in the financial markets

in order to discover whether there is such a thing as an ideal market economy; and (3)

Contributing to the development of financial markets in Pakistan. By means of these three

activities the Institute seeks to communicate its ideas to the audience both at home and

overseas. The Institute's research is intended, first and foremost, to be neutral, profes-

sional and practical. Rooted in practice, it aims to contribute to the healthy development

of Pakistani financial markets as well as to related policies by conducting neutral and pro-

fessional studies of how these markets and the financial system are regulated and orga-

nized and how they perform.

The economy is changing all the time. The Institute hopes that, by responding to these

changes positively, it can contribute to the dynamic development of the country's finan-

cial markets as well as of the economy itself.

Mr. Muhammad Ali Khan

T

02

Introduction to the Institute

◊ July 2017 IFMP Newsletter Page 4 ◊

The Institute of Financial Markets of Pakistan (IFMP), Pakistan’s first

securities market institute, has been established as a permanent platform to de-velop quality human capital, meet the emerging professional knowledge needs of

financial markets and create standards among market professionals. The Insti-tute has been envisioned to conduct various licensing examinations leading to

certifications for different segments of the financial markets. IFMP develops a pool of trained and certified professionals, skilled not only to deal in convention-

al instruments but also to trade in new and complex financial market products.

◊ FEE STRUCTURE ◊

Candidate Registration Fee Rs.10,000

Examination Registration Fee Rs.7,000

Membership Fee (Annual) Rs.5,000

Study Guide (Hard Copy) Rs.800

◊ EXAMINATION SCHEDULE ◊

-Sun, 24th September, 2017 (last date to

register is 4th September, 2017)

-Sun, 26th November, 2017 (last date to

register is 3rd November, 2017)

PROGRAMMES

LICENSING CERTIFICATIONS INSURANCE CERTIFICATIONS OTHER CERTIFICATIONS

Fundamentals of Capital Markets

Pakistan’s Market Regulations

Stock Brokers Certification

Mutual Funds Distributors

Commodity Brokers Certification

Research Analysts Certification

Mutual Funds Basic Certification

Securities and Futures Advisors’ Certifica-tion Programme—(Core Module: -Financial Advisors Certification) and (Advanced Modules: -Equity , Fixed Income and Derivatives Certification; -Commodity Bro-kers Certification)

General Takaful Training

Family Takaful Training

Life Insurance Agent

Non-Life Insurance Agent

Financial Derivative Traders Certification

Compliance Officers Certification

Clearing and Settlement Operations

Certification

Risk Management Certification

Capital Budgeting and Corporate Finance

Certification

Investment Banking and Analysis Certifica-

tion

Islamic Finance Certification

Fixed Income Certification

03

Performance of Banking Stocks in Pakistan

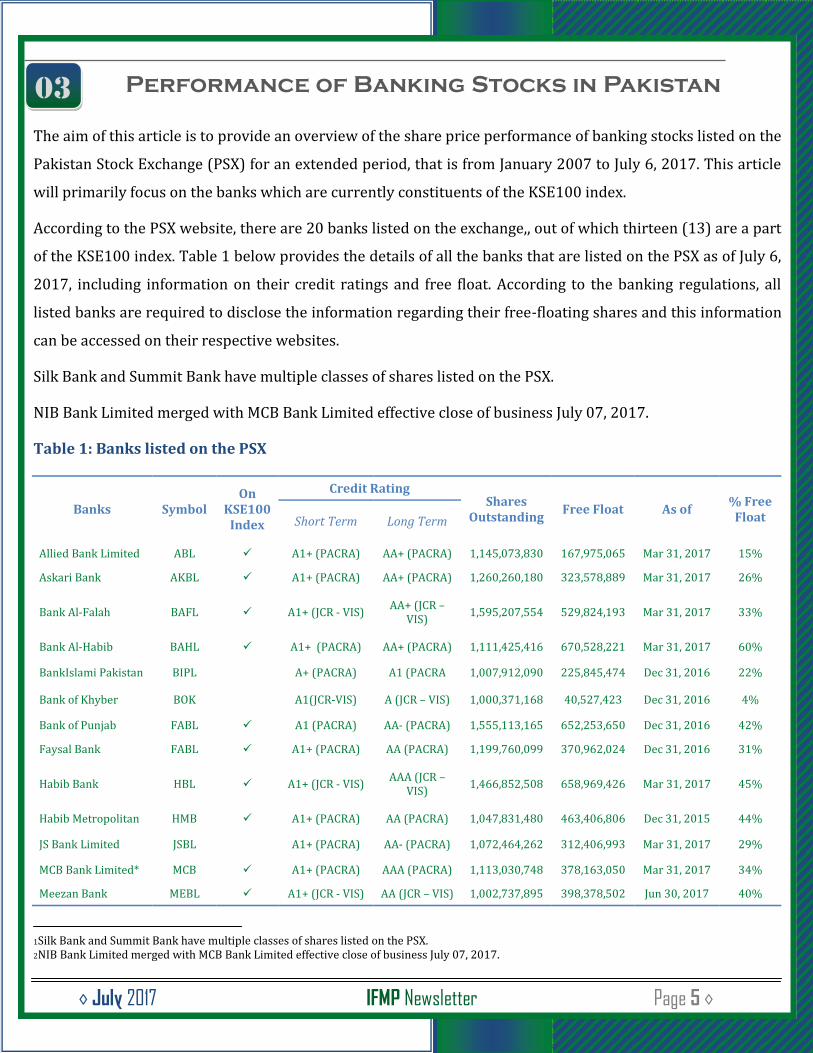

◊ July 2017 IFMP Newsletter Page 5 ◊

The aim of this article is to provide an overview of the share price performance of banking stocks listed on the

Pakistan Stock Exchange (PSX) for an extended period, that is from January 2007 to July 6, 2017. This article

will primarily focus on the banks which are currently constituents of the KSE100 index.

According to the PSX website, there are 20 banks listed on the exchange,, out of which thirteen (13) are a part

of the KSE100 index. Table 1 below provides the details of all the banks that are listed on the PSX as of July 6,

2017, including information on their credit ratings and free float. According to the banking regulations, all

listed banks are required to disclose the information regarding their free-floating shares and this information

can be accessed on their respective websites.

Silk Bank and Summit Bank have multiple classes of shares listed on the PSX.

NIB Bank Limited merged with MCB Bank Limited effective close of business July 07, 2017.

Table 1: Banks listed on the PSX

1Silk Bank and Summit Bank have multiple classes of shares listed on the PSX. 2NIB Bank Limited merged with MCB Bank Limited effective close of business July 07, 2017.

Banks Symbol On

KSE100 Index

Credit Rating Shares

Outstanding Free Float As of

% Free Float Short Term Long Term

Allied Bank Limited ABL A1+ (PACRA) AA+ (PACRA) 1,145,073,830 167,975,065 Mar 31, 2017 15%

Askari Bank AKBL A1+ (PACRA) AA+ (PACRA) 1,260,260,180 323,578,889 Mar 31, 2017 26%

Bank Al-Falah BAFL A1+ (JCR - VIS) AA+ (JCR –

VIS) 1,595,207,554 529,824,193 Mar 31, 2017 33%

Bank Al-Habib BAHL A1+ (PACRA) AA+ (PACRA) 1,111,425,416 670,528,221 Mar 31, 2017 60%

BankIslami Pakistan BIPL A+ (PACRA) A1 (PACRA 1,007,912,090 225,845,474 Dec 31, 2016 22%

Bank of Khyber BOK A1(JCR-VIS) A (JCR – VIS) 1,000,371,168 40,527,423 Dec 31, 2016 4%

Bank of Punjab FABL A1 (PACRA) AA- (PACRA) 1,555,113,165 652,253,650 Dec 31, 2016 42%

Faysal Bank FABL A1+ (PACRA) AA (PACRA) 1,199,760,099 370,962,024 Dec 31, 2016 31%

Habib Bank HBL A1+ (JCR - VIS) AAA (JCR –

VIS) 1,466,852,508 658,969,426 Mar 31, 2017 45%

Habib Metropolitan HMB A1+ (PACRA) AA (PACRA) 1,047,831,480 463,406,806 Dec 31, 2015 44%

JS Bank Limited JSBL A1+ (PACRA) AA- (PACRA) 1,072,464,262 312,406,993 Mar 31, 2017 29%

MCB Bank Limited* MCB A1+ (PACRA) AAA (PACRA) 1,113,030,748 378,163,050 Mar 31, 2017 34%

Meezan Bank MEBL A1+ (JCR - VIS) AA (JCR – VIS) 1,002,737,895 398,378,502 Jun 30, 2017 40%

03

Performance of Banking Stocks in Pakistan

◊ July 2017 IFMP Newsletter Page 6 ◊

Sources: PSX Sector Regime Summary available on PSX website; Free Float information published by the banks available on their respective websites; Credit Ratings from PACRA (2017) and JCR-VIS (2017)

Notes: *NIB Bank Limited merged with MCB Bank Limited effective close of business July 07, 2017. **Silk Bank Limited has another class of shares listed on the PSX. ***Summit Bank has two additional classes of shares listed on the PSX.

Banks Symbol On

KSE100 Index

Credit Rating Shares

Outstanding Free Float As of

% Free Float

Short Term Long Term

National Bank of Pa-kistan

NBP A1+ (JCR -

VIS) AAA (JCR –

VIS) 2,127,513,026 504,727,432 Mar 31, 2017 24%

Samba Bank SBL A1 (JCR-VIS) AA (JCR –

VIS) 1,008,238,648 144,549,258 Mar 31, 2016 14%

Silk Bank Limited** SILK A2 (JCR-VIS) A-(JCR-VIS) 9,081,861,237 2,868,739,343 June30, 2017 32%

Summit Bank*** SMBL A1 (JCR-VIS) A-(JCR-VIS) 1,778,666,303 318,086,920 Mar 31, 2017 18%

Soneri Bank Limited SNBL A1+ (PACRA) AA-

(PACRA) 1,102,463,481 311,740,050 Mar 31, 2017 28%

United Bank Limited UBL A1+ (JCR -

VIS) AAA (JCR –

VIS) 1,224,179,687 465,458,631 Dec 31, 2016 38%

Table 2 provides information for the banks that are a part of the index with respect to their weight on the in-

dex and market capitalization as of July 6, 2017. These thirteen banks constitute more than one-fifth (22.8

percent) of the index.

Table 2: Constituents of the KSE100 Index (As of July 6, 2017)

Source: PSX (2017)

Bank Symbol Closing Price

(PKR) Index Weightage

(%) Shares Traded

(million) Market Capt.

(PKR million)

Habib Bank HBL 247.10 7.31 660 163,107

United Bank UBL 221.12 4.85 490 108,276

MCB Bank Limited MCB 202.78 3.54 390 78,995

Bank AL-Habib BAHL 55.50 1.80 722 40,095

National Bank NBP 58.48 1.33 506 29,618

Bank Al-Falah BAFL 39.18 0.98 558 21,875

Habib Metropololitan Bank HMB 33.50 0.71 472 15,796

Allied Bank Limited ABL 85.11 0.65 172 14,619

Faysal Bank FABL 21.93 0.39 396 8,683

Meezan Bank MEBL 77.00 0.35 100 7,721

Askari Bank AKBL 20.25 0.34 378 7,656

Bank of Punjab BOP 11.17 0.33 653 7,289

Standard Chartered Bank Pakistan Limited SCBPL - 0.19 194 4,317

03

Performance of Banking Stocks in Pakistan

◊ July 2017 IFMP Newsletter Page 7 ◊

The global banking industry appears to have recovered from the Global Financial Crisis of 2008 (GFC hereaf-

ter), that was initiated in September 2008 after Lehman brothers filed for bankruptcy. Most markets around

the world experienced a sharp decline, although in some markets the reaction was lagged and asymmetric.

Bartram and Bodnar (2009), Korinek et al. (2010), and Baur (2012) argue that extreme volatility in the USA

financial market is transmitted heterogeneously to global financial markets, especially during crisis. While

developed markets are greatly affected by the volatility in the USA market, the impact on emerging and fron-

tier markets may not be as pronounced. While the world markets were getting affected by the returns and

volatility spillovers from the US and other developed markets, the Pakistan market was dealing with its own

internal issues, which were primarily associated with political instability, incoherent policy execution, materi-

al weaknesses within the financial markets and weak macroeconomic fundamentals. A floor on the market

was placed on August 28, 2008 to avoid free fall of the market. The floor was in place for several months and

limited investors' exit from the market, which resulted in lost investor confidence. The floor was removed on

December 15, 2008 and the market experienced a sharp decline after that. It is argued that the shock to the

Pakistan financial market was a result of domestic issues.

This analysis performed in this paper is rather preliminary. Daily data with a five-day frequency is analysed.

The article provides an overview of the share price performance of the banks for an eleven-year period

(January 2007 – July 6, 2017). The full period is then classified into various periods as follows:

1. Full period of analysis: January 2007 to July 6, 2017

2. Pre-crisis: January 2007 to August 27, 2008

3. During crisis: August 28, 2008 to October 26, 2009

4. Post crisis: October 27, 20099 to July 6, 2017

In the absence of a definitive end date of the GFC, a date provided by scholars in academic literature is used as

the cut-off for the crisis period. Bartram and Bodner (2009) provide a detailed chronological list of global

events that took place surrounding the GFC. According to the authors, the effects of the GFC started easing off

in October 2009, although the markets were still in the state of recovery. While these dates appear to be arbi-

trary, in the absence of other evidence the period of analysis is segregated according to the dates cited by Bar-

tram and Bodner (2009).

Moreover, a graphical comparison of performance of the banking stocks and the KSE100 index is presented

by using indexed returns. All the data for the banking stocks and the KSE100 index has been extracted from

Bloomberg terminal.

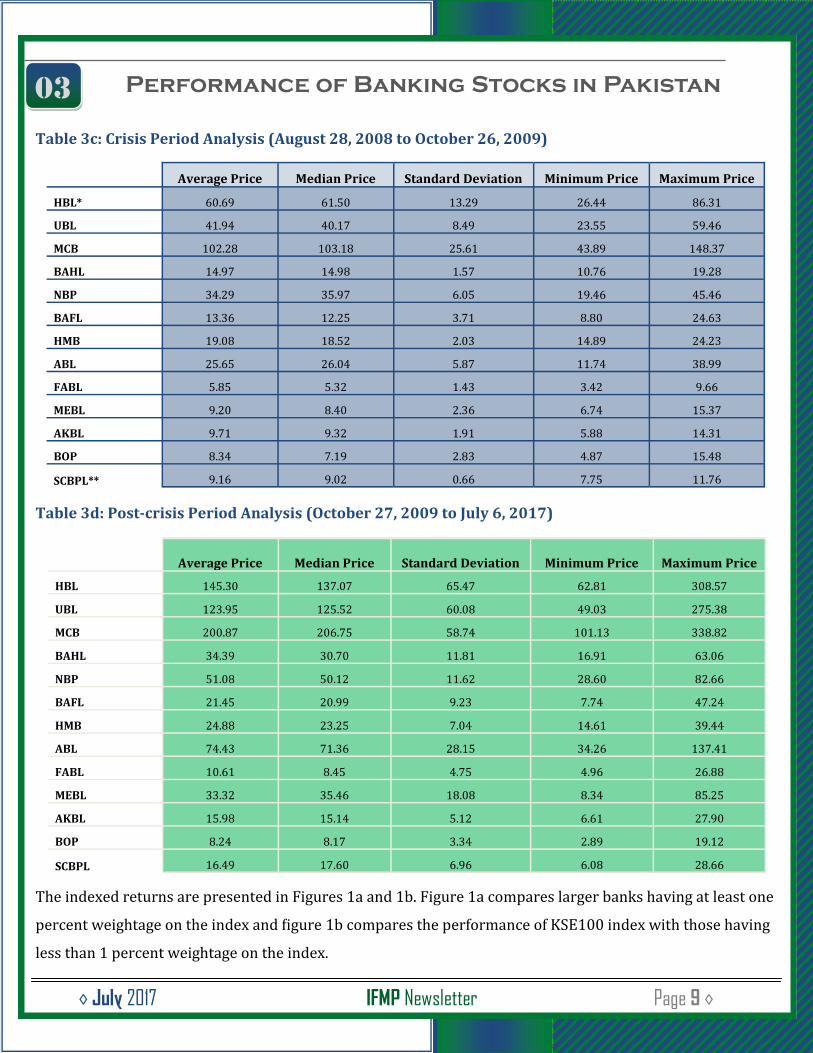

Tables 3a to 3d provide descriptive statistics of share prices of the selected banks in all four periods of analysis.

Table 3a: Full Period Analysis (January 2007 to July 6, 2017)

*Data available from July 16, 2007 **Data available from April 13, 2007

Table 3b: Pre-crisis Period Analysis (January 2007 to August 27, 2008)

*Data available from July 16, 2007 **Data available from April 13, 2007

03

Performance of Banking Stocks in Pakistan

◊ July 2017 IFMP Newsletter Page 8 ◊

Average Price Median Price Standard Deviation Minimum Price Maximum Price

HBL* 134.83 107.81 63.82 26.44 308.57

UBL 114.45 109.15 57.78 23.55 275.38

MCB 189.83 181.38 60.05 43.89 338.82

BAHL 30.55 25.67 12.36 10.76 63.06

NBP 55.45 52.49 19.01 19.46 106.88

BAFL 22.60 24.47 9.80 7.74 47.24

HMB 25.23 23.67 7.08 14.61 41.21

ABL 66.77 58.67 28.86 11.74 137.41

FABL 11.97 9.65 6.38 3.42 30.94

MEBL 28.20 24.38 18.07 6.74 85.25

AKBL 17.42 16.11 7.24 5.88 35.90

BOP 13.51 8.53 13.13 2.89 54.33

SCBPL** 19.33 17.90 12.18 6.08 63.80

Average Price Median Price Standard Deviation Minimum Price Maximum Price

HBL* 124.35 125.89 19.73 71.64 166.99

UBL 110.91 115.24 22.61 53.73 148.26

MCB 187.58 184.92 33.13 121.36 271.23

BAHL 21.40 21.81 3.18 14.70 27.14

NBP 87.89 92.18 14.60 41.28 106.88

BAFL 33.15 33.57 5.31 20.29 44.41

HMB 30.35 32.06 5.51 18.32 41.21

ABL 54.52 56.57 9.78 32.91 73.59

FABL 21.78 22.37 4.63 10.13 30.94

MEBL 15.33 15.60 4.00 8.69 23.14

AKBL 28.49 30.41 6.08 13.27 35.90

BOP 41.08 44.03 10.74 14.06 54.33

SCBPL** 37.40 43.80 15.69 8.00 63.80

03

Performance of Banking Stocks in Pakistan

◊ July 2017 IFMP Newsletter Page 9 ◊

Table 3c: Crisis Period Analysis (August 28, 2008 to October 26, 2009)

Table 3d: Post-crisis Period Analysis (October 27, 2009 to July 6, 2017)

The indexed returns are presented in Figures 1a and 1b. Figure 1a compares larger banks having at least one

percent weightage on the index and figure 1b compares the performance of KSE100 index with those having

less than 1 percent weightage on the index.

Average Price Median Price Standard Deviation Minimum Price Maximum Price

HBL* 60.69 61.50 13.29 26.44 86.31

UBL 41.94 40.17 8.49 23.55 59.46

MCB 102.28 103.18 25.61 43.89 148.37

BAHL 14.97 14.98 1.57 10.76 19.28

NBP 34.29 35.97 6.05 19.46 45.46

BAFL 13.36 12.25 3.71 8.80 24.63

HMB 19.08 18.52 2.03 14.89 24.23

ABL 25.65 26.04 5.87 11.74 38.99

FABL 5.85 5.32 1.43 3.42 9.66

MEBL 9.20 8.40 2.36 6.74 15.37

AKBL 9.71 9.32 1.91 5.88 14.31

BOP 8.34 7.19 2.83 4.87 15.48

SCBPL** 9.16 9.02 0.66 7.75 11.76

Average Price Median Price Standard Deviation Minimum Price Maximum Price

HBL 145.30 137.07 65.47 62.81 308.57

UBL 123.95 125.52 60.08 49.03 275.38

MCB 200.87 206.75 58.74 101.13 338.82

BAHL 34.39 30.70 11.81 16.91 63.06

NBP 51.08 50.12 11.62 28.60 82.66

BAFL 21.45 20.99 9.23 7.74 47.24

HMB 24.88 23.25 7.04 14.61 39.44

ABL 74.43 71.36 28.15 34.26 137.41

FABL 10.61 8.45 4.75 4.96 26.88

MEBL 33.32 35.46 18.08 8.34 85.25

AKBL 15.98 15.14 5.12 6.61 27.90

BOP 8.24 8.17 3.34 2.89 19.12

SCBPL 16.49 17.60 6.96 6.08 28.66

03

Performance of Banking Stocks in Pakistan

◊ July 2017 IFMP Newsletter Page 10 ◊

Figure 1a: Indexed Returned of Banks (with higher weight on the index) vs. KSE100 Index

Figure 1b: Indexed Returned of Banks (with lower weight on the index) vs. KSE100 Index

It is evident that the KSE100 index has outperformed all the banks during the period of analysis. A steep in-

cline in returns of KSE100 index are witnessed since 2013. On the other hand, while the banks appeared to

have performed reasonable well over time.

It is argued that the banking industry in Pakistan was not affected by the GFC due to limited exposure to

global markets and also because they are well capitalized. The Pakistani banks are required to maintain a high

Capital Adequacy Ratio (CAR) as compared to their peers in other countries. While the report published by

SECP argues that the GFC has no impact on the Pakistan market, it is yet to be determined, whether global

events particularly associated with the banking industry impacted the Pakistan market in any manner.

Note: The data presented in Tables 1 and 2 is extracted from the websites of the banks included in the analysis, PA-

CRA, JCR-VIS, SECP, PSX. The daily share price information presented in Tables 3a-d and Figure 1a-b is extracted

from Bloomberg. The data for the KSE100 index is also extracted from Bloomberg.

◊◊◊◊◊◊◊◊◊◊◊◊◊◊◊

Other References

Bartram, S. M. & Bodnar, G. M. 2009. No Place to Hide: The global Crisis in Equity Markets in 2008/2009. Jour-

nal of International Money and Finance 28(8), 1246-1292.

Baur, D. G. 2012. Financial contagion and the real economy. Journal of Banking & Finance, 36(10), 2680-2692.

Korinek, A., Roitman, A. & Vegh, C. 2010. Decoupling and Recoupling. American Economic Review, 100(2), 393-

397.

03

Performance of Banking Stocks in Pakistan

◊ July 2017 IFMP Newsletter Page 11 ◊

L

A

U

N

C

H

E

D

04

Terms of the Month

◊ July 2017 IFMP Newsletter Page 12 ◊

GET YOURSELF REGISTERED!

Last Date for Registration for 24th September, 2017

Examination

4th September, 2017

Book-Entry Security

"Book-entry security" in relation to a central deposi-

tory, means a security which is transferable by book-

entry in the central depository register pursuant to a

declaration made by the central depository under sub

-section ii of section 4 and which is:

i. In the case of a security transferable by registration,

registered in the name of the central depository or

issued to the central depository pursuant to section

14; or

ii. In the case of a security transferable by delivery or

endorsement, deposited with or transferred by en-

dorsement to the Central Depository.

-Central Depositories Act, 1997

Contribution

An amount as may be voluntarily determined by an

individual payable annually, semiannually, quarterly,

or monthly to one or more Pension Fund Managers

and held in one or more individual pension accounts

of a participant, subject to any specified minimum

limit.

-Voluntary Pension System Rules, 2006

Equity

It includes paid-up share capital, reserves and inap-

propriate profits excluding deferred tax reserves, Sur-

plus on Revaluation of Fixed Assets Account as de-

scribed in section 235 of the Ordinance and treasury

stocks.

-Non-Banking and Finance Companies Rules, 2003

Listed Company

A public company, body corporate or other entity any

of whose securities are listed on securities exchange.

-Securities Act, 2015

Participants' Investment Account

The investment account of the participants under a

Family Takaful plan.

-Takaful Rules, 2005

Venture Capital Company

It includes a company which

is engaged principally in

financing through direct

equity investment in another

company and provides

managerial expertise

thereto.

-Securities Act, 2015

05

Business and Economic Newsflash

◊ July 2017 IFMP Newsletter Page 13 ◊

Rs.54 Billion raised through PIBs

The first auction of Pakistan Investment Bonds in

2017-18 showed that the government is not interest-

ed in selling long-term bonds any more. It raised

Rs.54.5 billion through PIBs although the maturing

amount was Rs.689.5 billion.

The target for this auction was Rs.100 billion. The auc-

tion result announced by the SBP indicated that PIBs,

which remained the favored instrument in the first

three years of the present government, is no more a

preferred tool for raising liquidity. The government

raised trillions of rupees through long-term PIBs at

double-digit rates of returns. But they proved costly as

inflation and the benchmark interest rate registered a

steep fall.

The government raised Rs.20.8 billion for three years,

Rs.10.4 billion for five years and Rs.23.1 billion for ten

years. They received no bid for 20-year bonds. The

government requires to raise additional Rs.589.5 bil-

lion to meet maturing PIBs of Rs.689.5 billion.

SBP kept the Policy Rate Unchanged

The State Bank of Pakistan kept the policy rate un-

changed at 5.75% for another couple of months, citing

less-than-targeted inflation, higher domestic demand

and the expectation of the overall balance of payments

staying at a manageable level in 2017-18.

This projection is explained by lower-than-anticipated

increase in international oil prices,

behavior of consumer price index (CPI) in June, stable

administered prices and lower inflationary expecta-

tions. The current account deficit has been managed

by foreign exchange reserves and a financial account

surplus, which reached $9.6 billion during 2016-17

from $6.8 billion a year ago.

Apart from the increase in official inflows, this accu-

mulation incorporates the impact of the increase in

private-sector borrowing for CPEC projects.

Foreign Investment hit 8-year high

Foreign direct investment increased 4.6% to $2.41

billion in 2016-17. China emerged as the top investor

during the last three years with the onset of the China-

Pakistan Economic Corridor.

FDI from China in 2016-17 was $1.18 billion, almost

half of the total inflows received throughout the year.

The government expects the CPEC will stabilize the

economy in the long run as its large scale projects

bear fruit. A Dutch company bought a majority stake

in Engro Foods for $463 million, which made Nether-

lands the second biggest foreign investor.

According to the State Bank of Pakistan, overall for-

eign private investment decreased 5.3% to $1.88 bil-

lion compared to $1.98 billion a year ago. Portfolio

investment witnessed an outflow of $531 million com-

pared to the outflow of $320 million a year ago. Com-

pared to regional countries, Pakistan has been receiv-

ing smaller FDI over the years.

06

Urdu Glossary

◊ July 2017 IFMP Newsletter Page 14 ◊

Bank Liabilities بینک واجبات

Compensation معاوضہ‘ تلافی

Deposits امانتیں

Evaluation تقویم‘ پرکھ ‘ قدر پیما ئی

Futures Contracts ے مستقبل کے سود

Holding Company محلوک کمپنی

Inadequacy کمی‘ عدم کفایت

Kinship ر ی قریبی رشتہ دا

Limit Price حدی قیمت

Notional Cost تصوراتی لاگت

Perfect

Competition کا مل مسابقت

Recovery لی‘ بحالی کا عمل وصو

Stockholder ر حصے دا

Unforeseen Loss ن غیر متوقع نقصا

Windfall Profit فع غیرمتوقع منا

Diploma in Capital Market (In collaboration

with Institute of Business Administration, CEE,

Karachi, Pakistan)

Deadline: August 26, 2017

Fee: PKR 150,000 per head

For Registration: https://goo.gl/

forms/3mlRpOfDvLpgOCVv2

Program Details: http://cee.iba.edu.pk/

diplomaprograms.php

07

Quotes and Jokes

◊ July 2017 IFMP Newsletter Page 15 ◊

“Opportunities always look bigger

after they have passed.”

– Unknown

“In the short run, the market is a

voting machine, but in the long

run, it is a weighing machine.”

– Ben Graham

“There were two sets of

rules when it comes to

money: One set of rules

for the people who work

for money and another

set of rules for the rich

who print money.”

– Robert Kiyosaki

“The most important

word in the world of

money is cash flow.

The second most im-

portant word is lever-

age.”

– Rich Dad

08

Markets in Review

◊ July 2017 IFMP Newsletter Page 16 ◊

◊ Monthly Review ◊

Crude Oil

(WTI)

Beginning 45.58

Ending 49.33

Change +3.75

KIBOR

(6 Months)

Bid % Offer %

Beginning 5.90 6.15

Ending 5.90 6.15

Change 0 0

Pakistan

Stock

Exchange

100 Index

Beginning 46,565.29

Ending 46,010.45

Change -554.84

Gold

10 Grams

Beginning Rs.43,114

Ending Rs.43,714

Change +600

Silver

10 Grams

Beginning Rs.617.14

Ending Rs.625.71

Change +8.57

Foreign Exchange Rates Interbank Market

GBP (£) EURO (€) USD ($)

Buying Selling Buying Selling Buying Selling

Beginning Rs.136.42 Rs.136.68 Rs.119.91 Rs.120.14 Rs.104.80 Rs.105.00

Ending Rs.138.19 Rs.138.45 Rs.123.56 Rs.123.79 Rs.105.30 Rs.105.50

Change +1.77 +1.77 +3.65 +3.65 +0.5 +0.5

Contact Us

www.ifmp.org.pk 92 (21) 34540843-44 [email protected]

Source: Dawn e-Paper