news u can use - mutual funds · g-sec yields harden during the week on geopolitical concerns in...

TRANSCRIPT

News U Can Use

27th June 2014

The Week that was…

21st June to 27th June

Indian Economy World Bank projects a 5.5% growth for India in 2014-15, 6.3% in 2015-16 and 6.6% in 2016-

17.

Finance Secretary Arvind Mayaram says government would prefer the FDI route over FII

inflows if overseas resources need to be generated to spur economic expansion to its

potential level.

United Nations Conference on Trade and Development (UNCTAD) says India’s

macroeconomic uncertainties remain a major concern for investors, even as the country saw

FDI inflows of $28bn in 2013.

According to RBI’s financial stability report, India’s economic growth, inflation, and banks’

asset quality are still concerns.

CRISIL report says implementation of goods and services (GST) tax could help government

raise tax revenues and reduce fiscal deficit, which has been around 4.5% in the last three

years.

India's forex reserves rose by $1.385 bn to $314.922 bn in the week to June 20 on account

of rise in currency assets.

Source: Crisil Weekly Market Update

Indian Debt Market G-sec yields harden during the week on geopolitical concerns in Iraq and rising global crude

oil prices, domestic inflation concerns and devolvement in weekly G-sec auction. The ten

year benchmark closed the week at 8.75% as against 8.72% in the previous week.

Liquidity in the system was tight during the week with overnight rates shooting up towards

the end of the week on the quarter ending banks’ requirement. Average Net LAF (including

term repo and refinance) at Rs. 1,22,258 cr as against Rs. 1,18,500 cr in the previous

week.

In G-sec auction, RBI auctioned G-Sec (Rs 15000 cr) in following four securities namely -

8.27% GS 2020 (Rs 3,000 cr), 8.83% GS 2023 (Rs 7,000 cr), 8.32% GS 2030 (Rs 2,000 cr)

and 8.30% GS 2042 (Rs 3,000 cr) with cut-off yield of 8.55%, 8.73%, 8.75% and 8.77%

respectively. There was devolvement of Rs 961.50 cr in case of 8.27% GS 2020.

In term repo auction, RBI will conduct 14 day term repo auction (Rs 61,000 cr) with cut-off

yield of 8.25%.

In SDL auction, the RBI conducted auction of SDL (Rs 6130 cr) for 12 states with cut-off

yield of 8.97% and 9.01%.

In T-bill auction, RBI auctioned 91 days T-bills (Rs 8000 cr) and 364 days T-bills (Rs 3079

cr) with cut-off yield of 8.56% (Previous : 8.56%) and 8.70% (Previous : 8.60% )

respectively.

This week, RBI will auction 91 days T-bill (Rs 9000 cr) and 182 days T-bill (Rs 6000 cr) on

July 2, 2014.

Source: RBI,RMF Estimates

Indian Commodities Market

Crude oil prices fell marginally in the week due to rise in the US crude oil inventory data and

easing concerns over supply disruption by Iraq; prices ended at $105.84 a barrel on the

NYMEX on June 26, compared with $106.43 a barrel on June 19.

US crude oil inventories rose by 1.7mn barrels to 388.1mn barrels for the week ended June

20.

Forward Markets Commission directs exchanges to expel members who have been

expelled by any commodity exchange to bring uniformity in the commodity futures market.

National Spot Exchange Ltd urges banks to refrain from extending credit to its defaulters.

RiddiSiddhi Bullion claims Rs 100 cr each in damages from MCX and

PricewaterhouseCoopers for causing harm to its reputation.

Source: Crisil Weekly Market Update

Indian Government

Finance Minister Arun Jaitley to present Union Budget on July 10; Rail Budget to be

presented on July 8.

The Cabinet defers revision of gas prices by three months till September-end saying the

new government needs to comprehensively review the complex issue and take a decision in

public interest.

The Cabinet approves industrial parks to be set up in India by China.

Finance Ministry proposes allowing retirement and gratuity funds to invest up to 30% of their

money in the equity market.

Government accepts the report of a committee on rationalising definitions of FDI and FII;

foreign investment of 10% or more in a listed company will now be treated as FDI.

Government extends excise duty concession for the automobile and consumer durables

sectors by six months to December 31; also mulls bringing back excise duty in the branded

garments category in the coming budget.

Government plans to set up a finance corporation with a corpus of Rs 1 lakh cr, in

partnership with Japan, to fund projects in the road sector.

Ministry for road transport and highways clears road projects worth Rs 40,000 cr.

Government announces Rs 50 per quintal increase in the minimum support price of paddy

to Rs 1,360 to encourage farmers to cultivate rice.

Source: Crisil Weekly Market Update

Indian Government Government imposes a minimum export price (MEP) of $450 per tonne on potatoes to

augment domestic supply of the vegetable.

Government to give additional three months to state governments to implement the National

Food Security Act, which gives two-thirds of the country's population the right to subsidised

foodgrains.

Ministry of Corporate Affairs says foreign companies will not have to mandatorily register their

Indian subsidiaries as a public company.

Government to raise the import duty on sugar to 40% from 15%; also decides to provide

additional interest-free loan of up to Rs 4,400 cr to the cash-starved sugar industry for paying

cane arrears.

Government extends the ban on imports of milk and its products from China for one more

year till June 2015.

Government says industrial license will not be needed to manufacture items for defence

purposes other than those mentioned in a specific negative list.

Government clears a revised project cost of Rs 3568 cr proposed by BSNL for rolling out

mobile networks in nine states affected by Maoist insurgency.

Government asks banks and cash-rich PSUs to float a `reconstruction fund' to buy stakes in

stressed power projects in the country.

India makes a $550mn payment to Iran to partly clear pending oil dues.

Source: Crisil Weekly Market Update

Indian Government

Government proposes about 13 relaxations for private companies from the various

provisions of the Companies Act.

Government directs Employees’ Provident Fund Organisation (EPFO) and Employees State

Insurance Corporation (ESIC) to shift to a more transparent system of inspecting firms if

either the contribution or membership drops below a stipulated level.

Government plans to impose an additional penalty of $578 mn on Reliance Industries for

producing less-than-targeted natural gas from the KG-D6 block.

Ministry of agriculture to set aside 10% under every scheme as a contingency fund to meet

sudden expenditure if there is less rainfall in the country.

Government announces a host of measures to address the slump in investment in power

projects.

Government mulls raising cooking gas (LPG) and kerosene rates in small doses of Rs 5 per

cylinder and Rs 0.50-1 a litre every month to wipe out the Rs 80,000 cr subsidy on the two

fuels.

Government plans to kick off its disinvestment drive with the dilution of a 5% stake in SAIL.

Coal Ministry asks Coal India subsidiary Central Coalfields Ltd to provide details of its 14

projects that are awaiting clearances.

Ministry of Power invites bids for nine new transmission projects with an aggregate cost of

Rs 12,500 cr, as it seeks to fast-track the capacity building of inter-State transmission lines.

Source: Crisil Weekly Market Update

Indian Government

Government asks states to extend the Provident Fund Act to contract and construction

workers.

Ministry of housing plans to include commercial and industrial real estate sector under the

ambit of Real Estate (Regulation and Development) Bill.

Power Ministry sets up 7-member Advisory Group to look into subjects including optimal

energy mix, and requisite transmission and distribution infrastructure.

Power Ministry seeks review of a proposal to impose anti-dumping duty on imports of solar

gear because the country does not have sufficient capacity to make equipment to harness

the sun's energy.

Government initiates steps towards enhancing skill development; forms mentor council in

different sectors such as automobile, and textile to revamp various courses run by the

National Council for Vocational Training (NCVT).

Government says no decision has been taken to privatise Air India and that it is close to

finalising a short-term strategy to strengthen the aviation sector, including slashing taxes on

jet fuel.

Government orders high-level probe to ascertain the cause of fire in GAIL’s pipeline in

Andhra Pradesh; ex-gratia relief of Rs 2 lakh to be provided to the victims’ next of kin.

Source: Crisil Weekly Market Update

Indian Government

Coal Ministry rejects Power ministry’s plea for reconsidering the decision on deallocation of

eight coal blocks of power producers like Essar Power, and Tata Power, a move that may hit

an investment of around Rs 20,000 cr.

Power & Coal Minister Piyush Goyal criticizes Rangarajan gas pricing formula; says

anomalies in the formula should be fixed before revising rates.

National Association of Software and Services Companies (Nasscom) urges government to

invest Rs 500 cr and set up a 'Technology Entrepreneurship Mission' to aid young

technology companies in Tier-II and Tier-III locations.

10 of 19 Source: Crisil Weekly Market Update

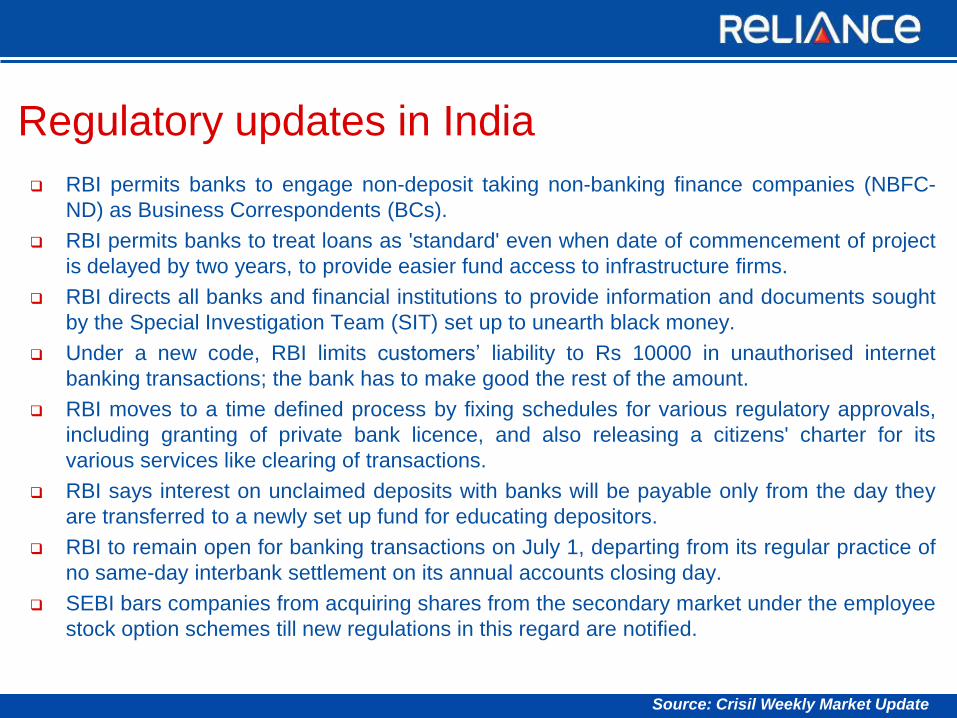

Regulatory updates in India

RBI permits banks to engage non-deposit taking non-banking finance companies (NBFC-

ND) as Business Correspondents (BCs).

RBI permits banks to treat loans as 'standard' even when date of commencement of project

is delayed by two years, to provide easier fund access to infrastructure firms.

RBI directs all banks and financial institutions to provide information and documents sought

by the Special Investigation Team (SIT) set up to unearth black money.

Under a new code, RBI limits customers’ liability to Rs 10000 in unauthorised internet

banking transactions; the bank has to make good the rest of the amount.

RBI moves to a time defined process by fixing schedules for various regulatory approvals,

including granting of private bank licence, and also releasing a citizens' charter for its

various services like clearing of transactions.

RBI says interest on unclaimed deposits with banks will be payable only from the day they

are transferred to a newly set up fund for educating depositors.

RBI to remain open for banking transactions on July 1, departing from its regular practice of

no same-day interbank settlement on its annual accounts closing day.

SEBI bars companies from acquiring shares from the secondary market under the employee

stock option schemes till new regulations in this regard are notified.

Source: Crisil Weekly Market Update

Regulatory updates in India

SEBI and stock exchanges revise norms and periodicity of review for securities in the

trade-for-trade segment; review to be done on a monthly basis as against the current

practice of doing it every fortnight.

SEBI sets up ‘International Affairs’ team in a bid to strengthen international cooperation

with global peers.

SEBI reorganises the committee that advices it on matters related to the secondary market

including suggesting steps to improve market safety, efficiency, and transparency.

SEBI Chief U.K. Sinha says the regulator is keen to implement self-regulation in the mutual

fund industry; also says SEBI is finalising norms for distributors and investor advisors and

will issue them shortly.

SEBI pulls up the mutual fund sector for not complying with the '20-25' minimum exposure

norm and for misuse of funds meant for investor awareness programmes.

SEBI asks the government to do away with tax anomalies in corporate bonds to attract

investors.

SEBI changes the rules governing entities such as employee welfare trusts, ensuring they

do not take short-term market positions.

SEBI orders exchanges to closely monitor the ongoing delisting process of AstraZeneca

India after finding evidence of ‘concerted action’ between the company and the Elliott

Group in 2013.

Source: Crisil Weekly Market Update

Regulatory updates in India

SEBI issues a fresh show-cause notice to HDFC Mutual Fund alleging front-running by a

former employee.

Retirement fund body EPFO to set up Central Analysis and Intelligence Unit (CAIU) for

collecting and analysing field level data for a transparent and accountable labour inspection

system.

Competition Commission of India orders a fresh probe against DLF for allegedly imposing

unfair conditions on office buyers at one of its commercial projects in Gurgaon.

Competition Commission of India dismisses allegations of unfair trade practices by Wipro

GE Healthcare with respect to sale and repair of medical equipment.

Competition Commission of India to consult relevant stakeholders before formulating

regulations pertaining to fair trade practices.

Source: Crisil Weekly Market Update

International Markets

The US economy contracted 2.9% in Q1 2014 according to the final estimate, compared to

the previous Q1 estimate of -1%, and 2.6% growth in Q4 2013.

US consumer confidence rose to 85.2 in June from a downwardly revised reading of 82.2 in

May.

US Existing Home Sales increased 4.9% to an annual rate of 4.89 mn units in May (the

largest monthly increase since August 2011) compared to April’s revised 4.66 mn units.

US new home sales jumped 18.6% in May (the highest level in six years) following a 3.7%

increase in April.

US personal income rose 0.4% in May, after gaining 0.3% in April, while personal spending

rose 0.2% last month, compared with a flat reading April.

US Durable Goods orders fell 1% in May, following a downwardly revised 0.6% gain in April.

US S&P Case-Shiller 20 city composite home price index rose 1.1% in April to come in at

168.71 following March’s reading of 166.80.

US Flash Manufacturing Purchasing Managers Index rose to 57.5 in June (the highest

reading since May 2010), compared to the final reading of 56.4 in May.

US Services PMI hit 61.2 in June, the highest reading since the survey began in October

2009, compared with May's final reading of 58.1; composite PMI hit 61.1 in June, a record

high, versus 58.4 in May.

Source: Crisil Weekly Market Update

International Markets US initial jobless declined in the week ending June 21 by 2,000 to a seasonally adjusted

312,000 from the previous week's revised total of 314,000.

The Chicago Federal Reserve's National Activity Index rose to 0.21 in May from -0.15 in

April.

US Thomson Reuters/University of Michigan's final June reading on the overall index of

consumer sentiment came in at 82.5, up from 81.9 the month before.

Euro zone’s preliminary manufacturing purchasing managers’ index declined to a seasonally

adjusted 51.9 in June, down from a final reading of 52.2 in May.

Euro zone's composite PMI fell to a six month low of 52.8 in June from 53.5 in May.

Euro zone’s services PMI declined to 52.8 in June from 53.2 in May.

Euro zone economic sentiment slumped to 102 in June from a revised 102.6 in May.

UK GfK consumer confidence index rose to 1 in June, up from 0 in May.

UK’s annual GDP growth rate in the first quarter of 2014 was revised down to 3% according

to the final estimate from 3.1% estimated earlier.

China’s HSBC/Markit Flash Manufacturing Purchasing Managers' Index rose to 50.8 in June

from May's final reading of 49.4.

Japan’s consumer price index rose 3.4% in May from a year earlier, compared with a 3.2%

rise in April.

Source: Crisil Weekly Market Update

International Markets Japan's retail sales fell 0.4% year-on-year in May, compared with a 4.3% decline in April.

Japan's seasonally adjusted average unemployment rate fell to 3.5% in May from 3.6% in

April.

Japan's average household spending plunged 8.0% year-on-year in May, compared with a

4.6% drop in April.

Japan’s Markit/JMMA flash Manufacturing Purchasing Managers Index (PMI) rose to a

seasonally adjusted 51.1 in June from a final reading of 49.9 in May.

Pharma company Shire PLC rejects a $46.35bn takeover bid from US rival AbbVie Inc.

HSBC sells its Swiss banking assets worth $12.5bn to LGT Bank.

Wisconsin Energy to buy Integrys for $5.71bn.

Oracle to buy buying Micros Systems Inc for about $5.3bn.

London Stock Exchange to buy Frank Russell Co for $2.7bn.

Japanese automaker Honda recalls nearly three million vehicles worldwide over an airbag

defect that could pose a fire risk.

Source: Crisil Weekly Market Update

Global Equities

Indices June 27 June 20 Change

%

Change

DJIA 16846.13* 16947.08 -100.95 -0.60

Nasdaq Composite 4379.05* 4368.04 11.01 0.25

Nikkei 225 (Japan) 15095.00 15349.42 -254.42 -1.66

Straits Times (Singapore) 3271.05 3258.80 12.25 0.38

Hang Seng (Hong Kong) 23221.52 23194.06 27.46 0.12

FTSE 100 (London) 6735.12* 6825.20 -90.08 -1.32

DJIA – Dow Jones Indust r i al Aver age

*Dat a wi t h r espect t o June 26 Source: Crisil Weekly Market Update

Global Equities

Key global indices closed mixed in the week ended June 26/27, with Singapore’s Straits

Times index gaining the most – up 0.4%, while Japan’s Nikkei index was the biggest decliner

– down 1.7%.

Wall Street stocks posted mixed performance in the week with Dow Jones losing 0.6% while

Nasdaq gained 0.3%.

Markets gained earlier on stock specific buying and positive domestic new home sales data.

Gains were however cut short on profit booking and as US Treasuries advanced amid

concerns over escalating violence in Iraq.

Disappointing domestic growth and durable goods orders data affected investors’ mood

further.

Britain’s FTSE index fell 1.3% in the week primarily on the back of heavy selling in housing

shares on concerns about possible changes to mortgage rules.

More losses were seen after energy and commodity shares fell due to geopolitical

uncertainty in Iraq and Ukraine.

Hong Kong’s Hang Seng index ended little changed in the week amid high volatility.

Market fell sharply earlier on heavy profit selling.

Losses were however erased on hopes of further delay in rate hikes in the US following

weak economic growth data from that country.

Source: Crisil Weekly Market Update

Global Equities Japan’s Nikkei index lost 1.7% in the week mainly on tracking intermittent declines on the

Wall Street, and as a stronger yen dampened exporters’ shares.

Singapore’s Straits Times index gained slightly in the week as losses due to ongoing

tensions in Iraq were overshadowed by optimism that the interest rate hike in US will be

further delayed due to weak US growth numbers.

Source: Crisil Weekly Market Update

Global Debt US treasury prices ended higher in the week ended June 26, following the release of poor

domestic economic data and tensions in Iraq.

Bond prices rallied after the US economy contracted 2.9% in Q1 2014 according to the final

estimate, compared to the previous estimate of -1%, and 2.6% growth in Q4 2013.

Bond prices gained after the US Durable Goods orders unexpectedly fell 1% in May,

following a downwardly revised 0.6% gain in April.

Intermittent fall in the equities and violence in Iraq also boosted the safe-haven appeal of

the US debt.

Bond prices also rose as the business activity data showed that the growth is slowing in

Germany, France and elsewhere in the euro zone.

Euro zone's composite Purchasing Managers Index (PMI) fell to a six month low of

52.8 in June from 53.5 in May.

Germany PMI eased to 54.2 from 55.6 while the French index slumped to 48.0 from

49.3, its lowest reading since February.

Gains were however capped due to few encouraging domestic economic numbers:

US initial jobless declined in the week ending June 21 by 2,000 to a seasonally

adjusted 312,000 from the previous week's revised total of 314,000.

US Flash Manufacturing Purchasing Managers Index rose to 57.5 in June (the highest

reading since May 2010), compared to the final reading of 56.4 in May.

Source: Crisil Weekly Market Update

Global Debt Bond prices fell after data showed manufacturing in China and Japan returning to growth in

June after months of decline.

China’s HSBC/Markit Flash Manufacturing Purchasing Managers' Index rose to 50.8 in

June from May's final reading of 49.4.

Japan’s Markit/JMMA flash Manufacturing Purchasing Managers Index (PMI) rose to a

seasonally adjusted 51.1 in June from a final reading of 49.9 in May.

The yield on the 10 year benchmark bond fell sharply to 2.53% on June 26 from 2.62% on

June 19.

On weekly debt holding front, foreign central banks' investment in US Treasuries and

agency debt at the Federal Reserve rose by $8.59 bn to $3.32 trillion in the week ended

June 18.

Source: Crisil Weekly Market Update

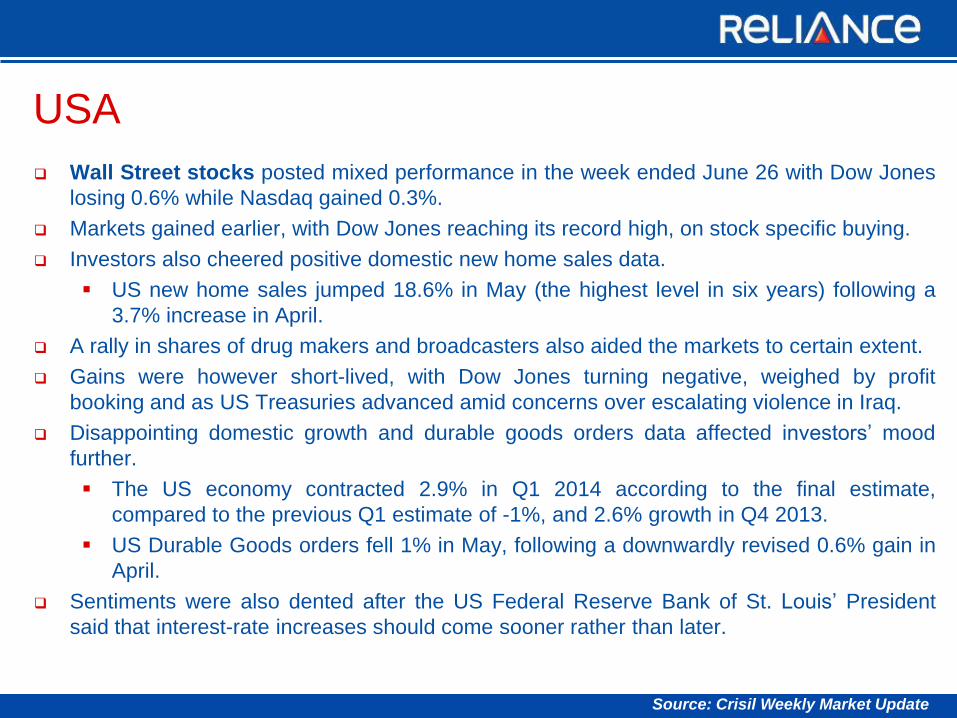

USA

Wall Street stocks posted mixed performance in the week ended June 26 with Dow Jones

losing 0.6% while Nasdaq gained 0.3%.

Markets gained earlier, with Dow Jones reaching its record high, on stock specific buying.

Investors also cheered positive domestic new home sales data.

US new home sales jumped 18.6% in May (the highest level in six years) following a

3.7% increase in April.

A rally in shares of drug makers and broadcasters also aided the markets to certain extent.

Gains were however short-lived, with Dow Jones turning negative, weighed by profit

booking and as US Treasuries advanced amid concerns over escalating violence in Iraq.

Disappointing domestic growth and durable goods orders data affected investors’ mood

further.

The US economy contracted 2.9% in Q1 2014 according to the final estimate,

compared to the previous Q1 estimate of -1%, and 2.6% growth in Q4 2013.

US Durable Goods orders fell 1% in May, following a downwardly revised 0.6% gain in

April.

Sentiments were also dented after the US Federal Reserve Bank of St. Louis’ President

said that interest-rate increases should come sooner rather than later.

Source: Crisil Weekly Market Update

UK

Britain’s FTSE index fell 1.3% in the week primarily on the back of some weak domestic

and global leads.

The benchmark was positive earlier as drug maker Shire Plc surged after rejecting a $46bn

takeover proposal.

A rally in mining shares following positive preliminary manufacturing activity data from China

lifted the market further.

Gains were however erased as housing shares declined on concerns about possible

changes to mortgage rules.

More losses were seen after energy and commodity shares fell due to geopolitical

uncertainty in Iraq and Ukraine.

Source: Crisil Weekly Market Update

ASIA

Hong Kong’s Hang Seng index ended little changed in the week ended June 27 amid high

volatility.

Market fell sharply earlier on heavy profit selling.

The benchmark also tracked a region-wide sell-off following losses on the Wall Street.

Losses were however erased on hopes of further delay in rate hikes in the US following

weak economic growth data from that country.

Upbeat preliminary Chinese manufacturing activity data also cheered the investors.

China’s HSBC/Markit Flash Manufacturing Purchasing Managers' Index rose to 50.8 in

June from May's final reading of 49.4.

Sporadic bargain hunting also supported the market to certain extent.

Japan’s Nikkei index lost 1.7% in the week ended June 27 and emerged as the biggest

decliner among key indices analyzed.

The benchmark started positively following the release of encouraging domestic and

Chinese manufacturing data.

Japan’s Markit/JMMA flash Manufacturing Purchasing Managers Index (PMI) rose to a

seasonally adjusted 51.1 in June from a final reading of 49.9 in May.

Market rose further on hopes that the US Federal Reserve will keep the interest rates low

for longer time after the country reported weaker first quarter GDP data.

Source: Crisil Weekly Market Update

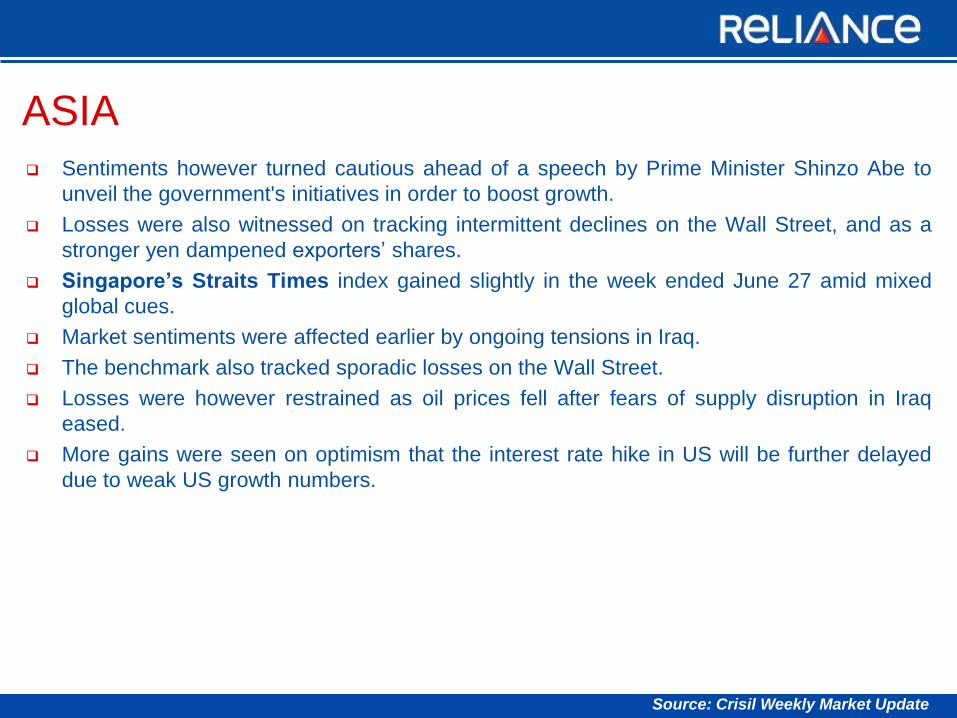

ASIA

Sentiments however turned cautious ahead of a speech by Prime Minister Shinzo Abe to

unveil the government's initiatives in order to boost growth.

Losses were also witnessed on tracking intermittent declines on the Wall Street, and as a

stronger yen dampened exporters’ shares.

Singapore’s Straits Times index gained slightly in the week ended June 27 amid mixed

global cues.

Market sentiments were affected earlier by ongoing tensions in Iraq.

The benchmark also tracked sporadic losses on the Wall Street.

Losses were however restrained as oil prices fell after fears of supply disruption in Iraq

eased.

More gains were seen on optimism that the interest rate hike in US will be further delayed

due to weak US growth numbers.

Source: Crisil Weekly Market Update

Indian Futures and Options Market Review

Nifty Futures

The week saw the near month contract changing from June 26, 2014 to July 31,

2014.

The new Nifty near month contract (July 31, 2014) closed up with 35.10 point

premium to the spot index on June 27, 2014.

Over the week ended June 27, the Nifty spot index ended flat amid lack of any

strong triggers.

The other Nifty future contracts, viz., August contract ended at 7581 points

(down 15 points over the week) and September contract ended at 7617 points.

Overall, Nifty futures saw a weekly trading volume of Rs 71,828 cr arising out of

around 19 lakhs contracts with an open interest of nearly 146 lakhs.

Source: Crisil Weekly Market Update

Indian Futures and Options Market Review

Nifty Options

Nifty 8000 call witnessed the highest open interest of 87 lakh on June 27.

Nifty 7600 call also garnered the higher number of contracts over the week at 40 lakhs.

For put options, Nifty 7000 put witnessed the highest open interest of 46 lakh on June 27.

Nifty 7500 put garnered highest number of contracts over the week at 37 lakhs.

Overall, options saw 233 lakh contracts getting traded at a notional value of Rs 8,79,255 cr

during the week.

Source: Crisil Weekly Market Update

Indian Futures and Options Market Review

Week ended

June 27, 2014

Turnover

Rs. Cr. % to Total

Index Futures 97,546 7.10

Index Options 947,767 69.02

Stock Futures 261,832 19.07

Stock Options 65,975 4.80

Total 1,373,120 100.00

Put Call Ratio 0.85 (27 June) 0.82 (20 June)

Stock Futures and Options –

NSE witnessed 69 lakh contracts in stock futures valued at Rs 2,61,832 cr while stock options saw

volumes of 17 lakh contracts valued at Rs 65,975 cr during the week ended June 27, 2014.

NSE F&O Turnover –

Overall turnover on NSE's derivatives segment stood at Rs 13.73 lakh cr (362 lakh contracts) during

the week ended June 27 vs. Rs 11.33 lakh cr (297 lakh contracts) in the previous week.

Put Call ratio rose to 0.85 on June 27 from 0.82 on June 20.

Source: Crisil Weekly Market Update

Indian Futures and Options Market Review

Sour ce - SEBI

Week Ended

June 26,

2014

Buy Sell Buy % Sell %

No. of

contracts

Amt in Rs

Cr

No. of

contracts

Amt in Rs

Cr

No. of

contracts Amt in Rs Cr

No. of

contracts

Amt in Rs

Cr

Index

Futures 629418 23862 603985 22881 13.46 13.64 12.87 13.02

Index

Options 2034704 76563 2006849 75527 43.51 43.75 42.78 42.99

Stock

Futures 1707436 62895 1770818 65384 36.51 35.94 37.75 37.22

Stock

Options 304961 11662 309693 11898 6.52 6.66 6.60 6.77

Total 4676519 174981.43 4691345 175690 100.00 100.00 100.00 100.00

Source: Crisil Weekly Market Update

FII Segment

On June 26 (last available SEBI data), foreign institutional investors' open interest stood at

Rs 1,02,505 cr (28 lakh contracts). The details of FII derivatives trades for the period June

20 – June 26 are as follows: -

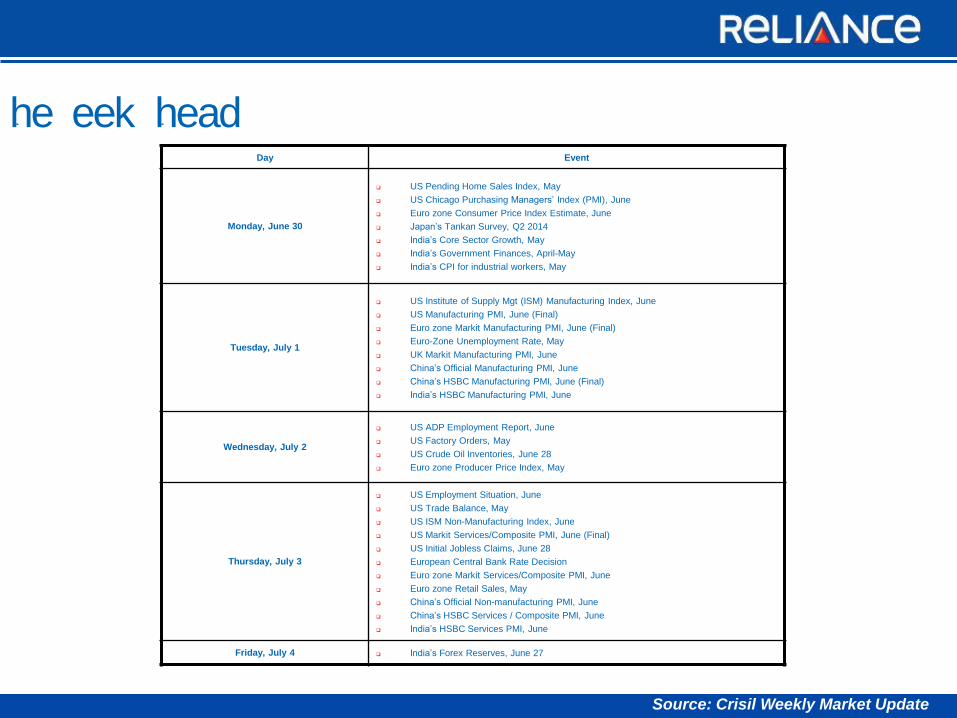

The Week Ahead…

30th June to 04th July 2014

The Week Ahead Day Event

Monday, June 30

US Pending Home Sales Index, May

US Chicago Purchasing Managers’ Index (PMI), June

Euro zone Consumer Price Index Estimate, June

Japan’s Tankan Survey, Q2 2014

India’s Core Sector Growth, May

India’s Government Finances, April-May

India’s CPI for industrial workers, May

Tuesday, July 1

US Institute of Supply Mgt (ISM) Manufacturing Index, June

US Manufacturing PMI, June (Final)

Euro zone Markit Manufacturing PMI, June (Final)

Euro-Zone Unemployment Rate, May

UK Markit Manufacturing PMI, June

China’s Official Manufacturing PMI, June

China’s HSBC Manufacturing PMI, June (Final)

India’s HSBC Manufacturing PMI, June

Wednesday, July 2

US ADP Employment Report, June

US Factory Orders, May

US Crude Oil Inventories, June 28

Euro zone Producer Price Index, May

Thursday, July 3

US Employment Situation, June

US Trade Balance, May

US ISM Non-Manufacturing Index, June

US Markit Services/Composite PMI, June (Final)

US Initial Jobless Claims, June 28

European Central Bank Rate Decision

Euro zone Markit Services/Composite PMI, June

Euro zone Retail Sales, May

China’s Official Non-manufacturing PMI, June

China’s HSBC Services / Composite PMI, June

India’s HSBC Services PMI, June

Friday, July 4 India’s Forex Reserves, June 27

Source: Crisil Weekly Market Update

Indian Debt Market Outlook

This week, the G-Sec market is expected to take cues concerns arising out of geo political

tensions in Iraq & inflation concerns arising out of steep railway fare hikes.

Liquidity is expected to remain comfortable on government expenditure. This week, Money market inflows of around Rs. 17,600 cr are expected as against outflows of around Rs. 29,000 cr.

Corporate bond market is expected to take cues from G-sec market and primary issuances.

Source: RBI,RMF Estimates

Indian Debt Markets

The maturities of duration

funds have increased due to

increased exposure in gsecs

as yields have moved up

considerably in last week.

The maturities of liquid and

liquid plus funds reflects cash

movement in the portfolio.

Source: RBI,RMF Estimates

Product Labeling

Reliance Gilt Securities

Fund

· income over long term.

· investment in Government securities.

· low risk. (BLUE)

Reliance Income Fund · income over long term.

· investment in debt and money market instruments

· low risk. (BLUE)

Reliance Short Term

Fund

·income over short term.

· investment in debt and money market instruments, with the scheme would have maximum

weighted average duration between 0.75-2.75 years

· low risk. (BLUE)

Reliance Monthly

Income Plan

· regular income and capital growth over long term.

· investment in debt & money market instruments and equities & equity related securities

· medium risk. (YELLOW)

Reliance Dynamic Bond

Fund

· income over long term.

· investment in debt and money market instruments

· low risk. (BLUE)

This product is suitable for investors who are seeking*:

*Investors should consult their financial advisers if in doubt about whether the product is suitable for them.

Product Labeling This product is suitable for investors who are seeking*:

*Investors should consult their financial advisers if in doubt about whether the product is suitable for them.

Reliance Floating

Rate Fund – Short

Term Plan

·income over short term.

· investment predominantly in floating rate and money market instruments with tenure exceeding

3 months but up to a maturity of 3 years and fixed rate debt securities

· low risk. (BLUE)

Reliance Money

Manager Fund

·income over short term.

· investment in debt and money market instruments

· low risk. (BLUE)

Reliance Liquidity Fund ·income over short term.

· investment in debt and money market instruments

· low risk. (BLUE)

Reliance Medium Term

Fund

·income over short term.

· investment in debt and money market instruments with tenure not exceeding 3 years.

· low risk. (BLUE)

Reliance Liquid Fund –

Treasury Plan

·income over short term.

· investment in debt and money market instruments

· low risk. (BLUE)

Reliance Liquid Fund –

Cash Plan

·income over short term.

· investment in debt and money market instruments

· low risk. (BLUE)

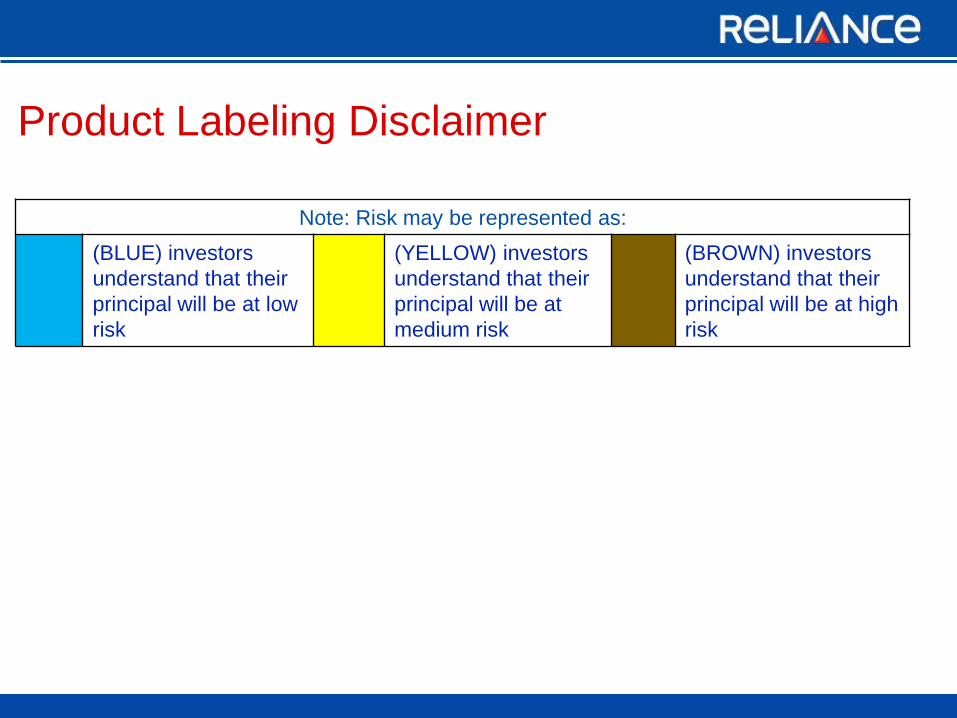

Product Labeling Disclaimer

Note: Risk may be represented as:

(BLUE) investors

understand that their

principal will be at low

risk

(YELLOW) investors

understand that their

principal will be at

medium risk

(BROWN) investors

understand that their

principal will be at high

risk

Information's provided here are meant for general reading purpose only and is not meant to

serve as a professional guide for the readers. This document has been prepared on the

basis of publicly available information, internally developed data and other sources believed

to be reliable. The Sponsor, The Investment Manager, The Trustee or any of their respective

directors, employees, affiliates or representatives do not assume any responsibility for, or

warrant the accuracy, completeness, adequacy and reliability of such information. Whilst no

action has been solicited based upon the information provided herein, due care has been

taken to ensure that the facts are accurate and opinions given fair and reasonable. This

information is not intended to be an offer or solicitation for the purchase or sale of any

financial product or instrument. Recipients of this information should rely on information/data

arising out of their own investigations. Readers are advised to seek independent

professional advice and arrive at an informed investment decision before making any

investments. None of The Sponsor, The Investment Manager, The Trustee, their respective

directors, employees, affiliates or representatives shall be liable for any direct, indirect,

special, incidental, consequential, punitive or exemplary damages, including lost profits

arising in any way from the information contained in this material.

Mutual Fund investments are subject to market risks, read all scheme

related documents carefully.

Thank you