nitrogen situation & outlook - firt · nitrogen . situation & outlook . glen buckley –...

TRANSCRIPT

Nitrogen Situation & Outlook

Glen Buckley – Chief Economist/Partner NPK Fertilizer Advisory Service

www.npkfas.com November 15, 2011

TFI Fertilizer Outlook Conference St. Petersburg, Florida

Presentation Outline

2

Review of FY11 Nitrogen Outlook Demand S/D Balances Urea UAN Ammonia

U.S. Nitrogen Fertilizer Demand (MM Tons of N)

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

FY06 FY07 FY08 FY09 FY10 FY11

Other

UAN

Urea

Ammonia

U.S. Annual Average Nitrogen Prices ($/Ton – Weighted by Volume)

0

100

200

300

400

500

600

700

02 03 04 05 06 07 08 09 10 11

AmmoniaUreaUAN

Fertilizer Year Basis

0

50

100

150

200

250

300

350

J06 J07 J08 J09 J10 J11

UANUreaAmmoniaCorn Prices

Index of MW Fertilizer Prices

Source: USDA, CBOT

vs. Nearby Corn Futures (Avg. CY ’06=100)

“Strong year driven by primarily by record crop prices”

Nitrogen Outlook

Source: Source: USDA, NPKFAS

U.S. Corn Supply/Demand Scenarios (Million Bushels)

7

Marketing Years (Yr. Beg. - Sept. 1)

USDA NPKFAS Proj. Fct.

2010/11 2011/12 2012/13

Planted Area 88.2 91.9 94.0 Harvested Area 81.4 83.9 87.0 Yield 152.8 146.7 161.5

Beginning Stocks 1,708 1,128 843 Production 12,447 12,310 14,051 Imports 28 15 30

Total Supply 14,183 13,453 14,923

Feed use 4,792 4,600 5,150 Food/Seed/Ind. 6,428 6,410 6,560

Ethanol 5,021 5,000 5,150 Domestic Use 11,220 11,010 11,710 Exports 1,835 1,600 1,950

Total Usage 13,055 12,610 13,660

Ending Stocks 1,128 843 1,263 Stocks/Use 8.6% 6.7% 9.2% Farm Price $5.18 $6.70 $5.25

Source: USDA, NPKFAS

2012 Crop Budgets Clearly Favor Corn ($/Acre)

8

Corn Soybeans Wheat Cotton Revenue Yield (bu/acre) 161.5 43.7 44.7 830.0 Avg. Season Price $5.25 $11.50 $6.00 $0.90 Crop Revenue (per acre) $848 $503 $268 $747 Total Revenue $850 $503 $276 $881 Variable Costs / Acre Fertilizers $135 $24 $48 $85 Seed Costs $92 $62 $14 $85 Crop Protection Chemicals $29 $18 $10 $70 Other (Fuel, Interest, Ins., Etc.) $68 $40 $45 $248 Total Variable Costs $324 $144 $117 $488 Return Over Variable Cost $525 $358 $159 $393

Source: USDA, NPKFAS

Returns Vary Significantly by Location ($/Acre)

9

Corn Heartland Southern Seaboard

Northern Crescent

Revenue Yield (bu/acre) 164.0 117.0 126.0 Avg. Season Price 5.25 6.00 5.30 Crop Revenue (per acre) $862 $702 $669 Total Revenue $862 $702 $674 Variable Costs / Acre Fertilizers $142 $144 $154 Seed Costs $94 $83 $94 Crop Protection Chemicals $32 $28 $26 Other (Fuel, Interest, Ins., Etc.) $56 $64 $69 Total Variable Costs $324 $319 $343 Return Over Variable Cost $539 $383 $330

Source: Census

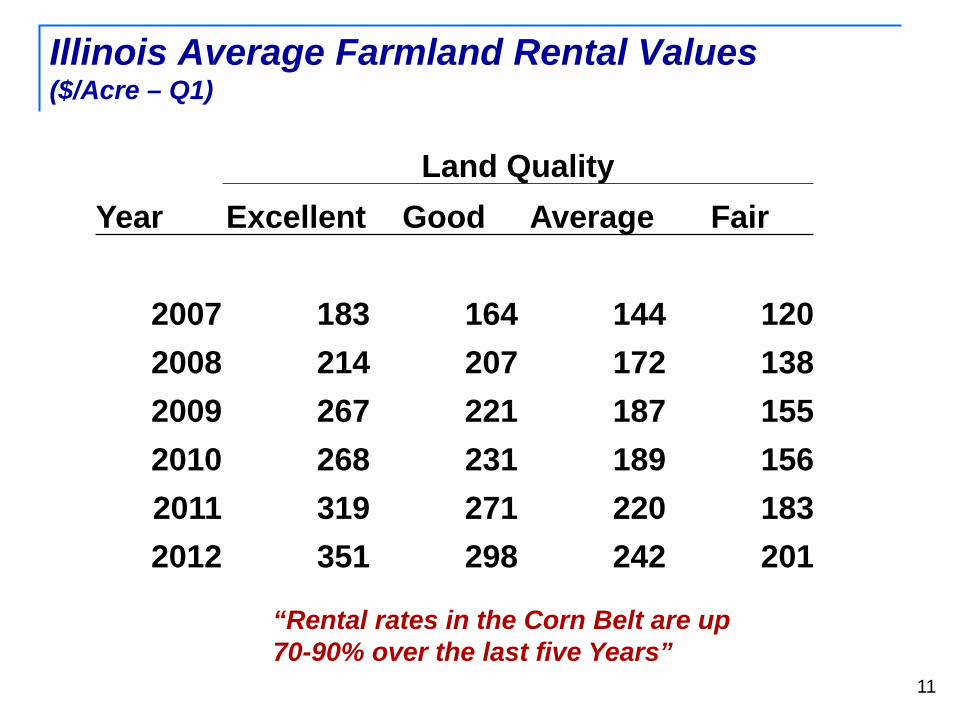

Percent of Farmland Rented/Leased

11

Land Quality Year Excellent Good Average Fair

2007 183 164 144 120 2008 214 207 172 138 2009 267 221 187 155 2010 268 231 189 156 2011 319 271 220 183 2012 351 298 242 201

Illinois Average Farmland Rental Values ($/Acre – Q1)

“Rental rates in the Corn Belt are up 70-90% over the last five Years”

Source: USDA, NPKFAS

Returns Vary Significantly by Location ($/Acre)

12

Corn Heartland Southern Seaboard

Northern Crescent

Revenue Yield (bu/acre) 164 117 126 Avg. Season Price 5.25 6 5.3 Crop Revenue (per acre) $862 $702 $669 Total Revenue $862 $702 $674 Variable Costs / Acre Fertilizers $142 $144 $154 Seed Costs $94 $83 $94 Crop Protection $32 $28 $26 Other (Fuel, Interest, Ins., Etc.) $56 $64 $69

Total Variable Costs $324 $319 $343

Return Over Variable Cost $539 $383 $330

Rental Value $250 $175 $210 Cash Returns Incl. Land $289 $208 $120

Source: USDA, NPKFAS

Corn/Corn vs. Corn/Bean Rotation Decision Not Quite as Clear ($/Acre)

13

Heartland Corn/Bean Corn/Corn Revenue Yield (bu/acre) 163.3 145.3 Avg. Season Price $5.14 $5.14 Crop Revenue (per acre) $838 $746 Total Revenue $840 $748 Variable Costs / Acre Fertilizers $131 $139 Seed Costs $29 $29 Crop Protection Chemicals $88 $93 Other (Fuel, Interest, Ins., Etc.) $71 $71 Total Variable Costs $319 $332 Return Over Variable Cost $521 $416

U.S. Planted Acreage Summary (MM Acres)

Change 2009 2010 2011 2012 2011-12

Corn 86.4 88.2 91.9 94.0 2.1

Soybeans 77.5 77.4 75.0 76.5 1.5

Wheat 59.2 53.6 54.4 59.0 5.6

Cotton 9.2 11.0 14.7 12.0 -2.7

4 Major Crops 232.3 230.2 236.0 241.5 5.5

Other Crops 87.3 91.0 90.0 90.0 0.0 Total Principal Crops 319.6 321.2 326.0 331.5 5.5

Source: USDA, NPKFAS 14

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12

U.S. Nitrogen Fertilizer Demand (MM Tons N)

“Demand expected to increase 4.4% to a record 13.3 MM tons”

Source: TFI, AAPFCO, NPKFAS

U.S. Fertilizer Demand by Product (000 Nutrient Tons)

16

Est. Fct. % Change

2010 2011 2012 2011-12

Nitrogen 12,601 12,701 13,262 4.4%

Ammonia 3,571 3,420 3,760 6.4%

Urea 3,389 3,466 3,592 5.0%

UAN 3,519 4,073 3,958 -2.8%

NOAA Long-Term Drought Indicator

Source: NOAA

Above Normal Temp – Below Average Moisture Expected for Much of the South

Source: National Weather Service

Temperature Moisture

Dec-Feb

Mar-May

Non-Commercial Net Long Positions vs. Nearby Corn Contract

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

-100-50

050

100150200250300350400

J-06 J-07 J-08 J-09 J-10 J-11

$/Bu. 000 Contracts Non Comm. Net Longs (L Axis)

Nearby Futures Contract (R Axis)

Source: CBOT 19

Fertilizer Supply/Demand Outlook

20

Overview World demand expected to hit record levels

Continued recovery in the U.S. Near Record Demand in India, China, L.A.

S/D for nitrogen is expected to remain in somewhat of a tight position.

However – Supply availability is expected improve over the tight conditions in 2011 as growth in capacity outpaces increase in demand

U.S. and World Nitrogen Demand Driven Mostly by Grains (% of Total N Demand)

Corn 47%

Wheat 11% Cotton

3%

High Value 12%

Other 22%

Source: IFA, NPKFAS

Corn 15%

Wheat 20%

Rice 15%

Other 37%

United States World

21

Fruits/ Vegetables

14%

World Food Consumption (MM Tonnes)

Source: FAO, NPKFAS

2008-18 2000 2008 2018 Volume CAGR

Food Grains 1,194 1,322 1,485 163 1.2% Coarse Grains 875 1,026 1,229 202 1.8% Oilseeds 110 133 167 34 2.3% Roots/Tubers 679 764 875 112 1.4% Fruits & Vegetables 1,221 1,339 1,494 155 1.1% Other 194 247 316 69 2.5% Total 4,274 4,831 5,567 736 1.4%

Beef/Veal 60 67 76 9 1.3% Pork 90 100 115 14 1.4% Poultry 69 84 107 23 2.4% Lamb 11 13 16 3 2.1% Total Meat 230 265 314 50 1.7%

Milk (Cows) 580 648 745 97 1.4%

“World food demand is projected to grow at a CAGR of 1.4%, mostly in the coarse grains and oilseed sectors as consumers in developing countries improve diets.”

22

1200

1400

1600

1800

2000

2200

2400

2600

80 84 88 92 96 00 04 08 12 16 20

Production Consumption

(MM Tonnes) World Grain Supply/Demand

0

500

1000

1500

2000

2500

90 92 94 96 98 00 02 04 06 08 10 12 14 16 18 20

Acreage Yield Improvement

(MM Tonnes)

Source: USDA FAS, FAO, NPKFAS

World Grain Production by Source

Yield increases Will Have to come from: BMP Improved Seed Fertilizer/Crop Protection

0

20

40

60

80

100

120

140

160

2000 2002 2004 2006 2008 2010 2012 2014Source: IFA, NPKFAS

(MM Nutrient Tonnes) World Nitrogen Demand

Industrial/Other

Forecast

Fertilizer

25

World Nitrogen Fertilizer Demand (MM Nutrient Tonnes)

Nitrogen

2006 94.8

2007 99.5

2008 99.1

2009 100.3

2010 101.9 2011 104.7

2012 108.8 %

Change 3.9%

0.0

20.0

40.0

60.0

80.0

100.0

120.0

06 07 08 09 10 11 12

Sources: IFDC, IFA , Industry Reports

World Ammonia/Urea Project List (000 Product Tonnes)

Country Company Month Ammonia Urea CY 2011

Qatar QAFCO 5 October 759 1271 Saudi Arabia Ma'aden Feb 1089 Myanmar Petrochemical Industries January 107 165 Pakistan Engro Chemicals Pakistan Ltd April 750 France GPN February 360 Netherlands Yara July 1155 Pakistan Engro Chemicals Pakistan Ltd April 1300 China Various 5320 7880 2011 Total 8025 12131

CY 2012 Russia CJSC Agro Cherepovets October 495 Algeria EDEOLA 1 October 660 1271 Algeria EDEOLA 2 1271 Algeria Sorfert January 726 1155 Algeria Sorfert July 726

Egypt Egyptian Nitrogen Producing Company (ENPC) 1 April 396 635

Egypt Egyptian Nitrogen Producing Company (ENPC) 2 July 396 635

Qatar QAFCO 5 February 759 1271

Vietnam Ninh Binh Fertilizers & Chemicals (Vinachem) January 330 580

Vietnam Petrovietnam Fertilizer and Chemical Company April 450 787

Australia Incitec Pivot Ltd June 149 Venezuela Pequiven July 594 726 China Various 4581 5950

9767 14776

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

0

20

40

60

80

100

120

140

160

99 01 03 05 07 09 11 13 15

DemandCapacityOperating Rate

World Nitrogen Supply/Demand Balance Ex China (MM Tonnes N)

28

U.S. Urea Import Requirements for FY2012 (MM Product Tons)

29

Fertilizer Years 2010 2011 Fct. 2012

Demand Ag Consumption 7.37 7.54 7.81 Industrial/Other 1.46 1.86 1.92 Exports 0.16 0.21 0.17

Total Demand 8.99 9.61 9.90 Supply Production 2.97 2.96 3.22 Required Imports 6.04 6.61 6.71

Source: TFI, DOC, NPKFAS

U.S. Urea Imports (000 Product Tons)

0100200300400500600700800900

10001100

J A S O N D J F M A M J

FY10FY11FY12

♦ Source: TFI, DOC, NPKFAS

“Imports running well ahead of last year”

Source: US DOC

U.S. Urea Imports by Source (000 Product Tons)

% of FY 2008 2009 2010 2011 Total

Canada 1,749 1,770 1,896 1,851 28% Offshore Trinidad 474 483 374 424 6% Middle East 1,968 2,225 1,942 2,304 35% China 1,175 254 427 727 11% Egypt 180 242 564 487 7% Other 1,010 778 839 818 12% Sub-Total 4,807 3,981 4,146 4,760 72%

Total 6,556 5,751 6,042 6,611 100%

300

325

350

375

400

425

450

475

500

525

2/4 3/4 4/1 4/29 5/27 6/24 7/22 8/19 9/16 10/14 11/11

U.S. Gulf Price

M. East Del. Cost

“U.S. prices are currently running roughly $30 per ton below Middle East landed values”

U.S. Gulf Urea Barge Price vs. Middle East Delivered Cost ($/ton)

32 ♦ Source: NPKFAS, Industry Sources

0

5

10

15

20

25

30

35

40

06 07 08 09 10 11 12

33

2009 2010 2011 2012

U.S. 4.70 6.32 5.65 6.09 W. Europe 4.63 4.53 3.88 4.24 L. America 5.67 6.62 7.11 6.93 India 5.47 6.10 7.30 6.73 Rest of Asia 8.50 7.85 8.14 7.90 Other 4.48 6.04 5.39 5.01

World Total 33.45 37.46 37.77 37.00

World Urea Imports (MM Product Tonnes – Calendar Year Basis)

“World imports expected to decline marginally in 2012 from the record levels of the previous two years”

♦ Source: IFA, NPKFAS, Country statistics, Industry sources

-300

-200

-100

0

100

200

300

N D J F M A M J

World Urea Trade Balance (000 Tonnes)

Surplus

Deficit

34

“World Balance expected to move into a balanced/long position in 2012”

Chinese Urea Balance (000 Product Tonnes)

0.0

10.0

20.0

30.0

40.0

50.0

60.0

00 02 04 06 08 10 12

ProductionConsumption

35 ♦ Source: IFA, NPKFAS, Industry sources

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

00 02 04 06 08 10 12

Net Exports

FY 2010 2011 2012 Demand Ag Consumption 10.82 12.73 12.37 Exports 0.30 0.22 0.03 Other/Inv. Change -0.24 0.04 -0.02 Total Demand 10.88 12.99 12.38

Supply Production 9.05 9.47 9.63

Required Imports 1.84 3.52 2.75 10.88 12.99 12.38

36

U.S. UAN Import Requirements for FY2012 (MM Product Tons)

U.S. UAN 32% Imports (000 Product Tons)

0

100

200

300

400

500

J A S O N D J F M A M J

FY10FY11FY12

♦ Source: TFI, DOC, NPKFAS

FY Totals

FY06 2.83 FY07 2.39 FY08 3.49 FY09 1.60 FY10 1.84 FY11 3.52 FY12 2.75

U.S. UAN Producer Inventory (000 Product Tons – 32% Material)

0.00

0.20

0.40

0.60

0.80

1.00

1.20

J A S O N D J F M A M J

FY10FY11FY12 Fct5-Yr Average

♦ Source: TFI, DOC, NPKFAS

U.S. UAN Capacity (000 tons 32% Material)

% of Total

FY11 FY12 Capacity Cumulative

CF 6,240 6,490 51.2% 51.2%

PCS 2,023 2,023 16.0% 67.1%

Koch 1,085 1,085 8.6% 75.7%

Agrium 870 870 6.9% 82.5%

CVR 738 738 5.8% 88.4%

LSB 705 705 5.6% 93.9%

Rentech 390 390 3.1% 97.0%

Dyno Nobel 272 272 2.1% 99.1%

Trademark 110 110 0.9% 100.0%

12,433 12,683 100% Source: IFDC

0.02.04.06.08.0

10.012.014.016.018.020.022.0

2005 2006 2007 2008 2009 2010 2011

Prod.

U.S. Ammonia Supply (MM Tons)

Imports

40 ♦ Source: TFI, DOC, NPKFAS Fertilizer Year

“Imports account for roughly 40% of U.S. ammonia supply. However, the vast majority is used in DAP/MAP production and in the industrial sector”

U.S. Tampa Ammonia Import Price vs. MW Wholesale Price ($/ton)

0

100

200

300

400

500

600

700

800

J09 A J O J10 A J O J11 A J O

DifferentialTampa Import $MW Wholesale $

Limited MW Ammonia Supply

42

Lack of Infrastructure to offload and move imports to the Midwest Ag markets Limited Offloading Limited distribution system - Port to MW Limited storage capabilities downstream

Fall S/D - Mostly fixed supply facing potentially another strong application season

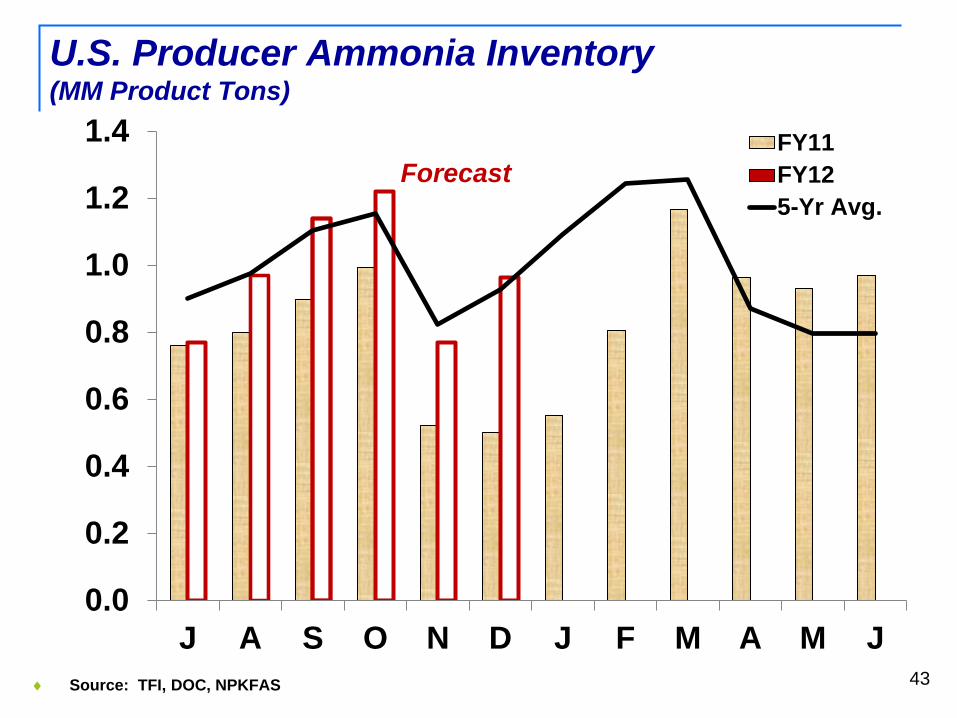

U.S. Producer Ammonia Inventory (MM Product Tons)

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

J A S O N D J F M A M J

FY11FY125-Yr Avg.

Forecast

43 ♦ Source: TFI, DOC, NPKFAS

0.0

1.0

2.0

3.0

4.0

5.0

2004 2005 2006 2007 2008 2009 2010 2011 2012

Fall

U.S. Ammonia Fertilizer Demand (MM Tons)

Spring

44 Fertilizer Year

“Fall demand expected to be down from last year’s near record setting pace, but above historic averages”

Fertilizer Supply/Demand Outlook

45

Overview World demand expected to hit record levels

Continued recovery in the U.S. Near Record Demand in India, China, L.A.

S/D for nitrogen is expected to remain a somewhat of a tight position.

However – Supply availability is expected improve over the tight conditions in 2011 as growth in capacity outpaces increase in demand