no. a12-1555 state of minnesota in supreme · pdf filea12-1555 state of minnesota in supreme...

TRANSCRIPT

2013 – BACHMAN LEGAL PRINTING – FAX (612) 337-8053 – PHONE (612) 339-9518 or 1-800-715-3582

NO. A12-1555

State of Minnesota

In Supreme Court

Graphic Communications Local 1B Health & Welfare Fund “A”; and

The Twin Cities Bakery Drivers Health and Welfare Fund, individually and on behalf of all others similarly situated,

Plaintiffs-Respondents, vs.

CVS Caremark Corporation, et al, Coborn’s, Incorporated,

Kmart Holding Corporation, et al., Snyder’s Drug Stores (2009), Inc., et al., Target Corporation; Sears, Roebuck And Co., Walgreen Co.,

and Wal-Mart Stores, Inc., Defendants-Appellants.

___________________________

AMICUS BRIEF AND APPENDIX OF THE NATIONAL ASSOCIATION OF CHAIN DRUG STORES, NATIONAL COMMUNITY PHARMACISTS

ASSOCIATION, RETAIL LITIGATION CENTER, MINNESOTA PHARMACISTS ASSOCIATION, MINNESOTA RETAILERS

ASSOCIATION, INDEPENDENT PHARMACY COOPERATIVE, THRIFTY WHITE PHARMACY, AND THE MINNESOTA CHAMBER OF COMMERCE

___________________________

BRIGGS AND MORGAN, P.A. Leah Ceee O. Boomsma (#0389885) 2200 IDS Center 80 South Eighth Street Minneapolis, MN 55402 (612) 977-8400 Attorneys for Amici National Association of Chain Drug Stores, National Community Pharmacists Association, Retail Litigation Center, Minnesota Pharmacists Association, Minnesota Retailers Association, Independent Pharmacy Cooperative, Thrifty White Pharmacy, and the Minnesota Chamber of Commerce

(Counsel for the parties and additional amici continues on following pages)

Wendy J. Wildung (#117055) Craig S. Coleman (#0325491) FAEGRE BAKER DANIELS LLP 2200 Wells Fargo Center 90 South Seventh Street Minneapolis, MN 55402 (612) 766-7000 Attorneys for Defendant-Appellant Target Corporation Todd A. Noteboom (#240047) Elizabeth Wiet Reutter (#316957) LEONARD, STREET AND DEINARD, P.A. 150 South Fifth Street, Suite 2300 Minneapolis, MN 55402 (612) 335-1500 Attorneys for Defendant-Appellant Walgreen Co. Lewis A. Remele, Jr. (#90724) Christopher R. Morris (#230613) BASSFORD REMELE, P.A. 33 South Sixth Street, Suite 3800 Minneapolis, MN 55402-3707 (612) 333-3000 Attorneys for Defendants-Appellants CVS Caremark Corporation, CVS Pharmacy, Inc., Caremark, LLC, Caremark Minnesota Specialty Pharmacy, LLC, and Caremark Minnesota Specialty Pharmacy Holding, LLC Tracy J. Van Steenburgh (#141173) NILAN JOHNSON LEWIS, PA 400 Canadian Pacific Plaza 120 South Sixth Street Minneapolis, MN 55402-4501 (612) 305-7500 Attorneys for Defendants-Appellants Kmart Holding Corporation, Sears, Roebuck & Co., and Sears Holding Corporation

David R. Marshall (#184457) Joseph J. Cassioppi (#388238) FREDRIKSON & BYRON, P.A. 200 South Sixth Street, Suite 4000 Minneapolis, MN 55402 (612) 492-7000

Attorneys for Defendant-Appellant Walmart Stores, Inc.

Kevin D. Hofman (#0179978) Ronald B. Peterson (#0086344) HALLELAND HABICHT, P.A. 33 South Sixth Street, Suite 3900 Minneapolis, MN 55402 (612) 836-5500 Attorneys fro Defendant-Appellant Coborn’s Incorporated

James K. Langdon (#171931) DORSEY & WHITNEY LLP 50 South Sixth Street, Suite 1500 Minneapolis, MN 55402-1498 (612) 340-2600 Attorneys for Defendants- Appellants Snyder’s Drug Stores (2009), Inc., Snyder’s Holdings (2009), Inc., and Snyder’s Holding, Inc.

2013 – BACHMAN LEGAL PRINTING – FAX (612) 337-8053 – PHONE (612) 339-9518 or 1-800-715-3582

David L. Hashmall (#138162) FELHABER, LARSON, FENLON & VOGT, P.A. 220 South Sixth Street, Suite 2200 Minneapolis, MN 55402 (612) 339-6321 Perrin Rynders (admitted pro hac vice) VARNUM LLP Bridgewater Place P.O. Box 352 Grand Rapids, MI 49501-0352 (616) 336-6000 John W. Barrett BAILEY & GLASSER LLP 209 Capitol Street Charleston, WV 25301 (304) 345-6555

Attorneys for Plaintiffs-Respondents

Donald R. McNeil Stephen F. Buterin HELEY, DUNCAN & MELANDER, PLLP 8500 Normandale Lake Boulevard Suite 2110 Minneapolis, MN 55437 (952) 841-0001

Attorneys for Amicus The National Labor Alliance of Health Care Coalitions

Mark S. Olson OPPENHEIMER WOLFF & DONNELLY, LLP Campbell Mithun Tower, Suite 2000 222 South Ninth Street Minneapolis, MN 55402 (612) 607-7000 Attorneys for Amicus Product Liability Advisory Council, Inc. William L. Davidson (#201777) LIND, JENSEN, SULLIVAN & PETERSON, P.A. 1300 AT&T Tower 901 Marquette Avenue South Minneapolis, MN 55402 (612) 333-3637 Attorneys for Amicus Minnesota Defense Lawyers Association Dale O. Thornsjo JOHNSON & CONDON, P.A. 7401 Metro Boulevard Suite 600 Minneapolis, MN 55439 (952) 831-6544 Attorneys for Amici Insurance Federation of Minnesota, et al. Jennifer Y. Dukart Assistant Attorney General MINNESOTA ATTORNEY GENERAL’S OFFICE 1200 Bremer Tower 445 Minnesota Street St. Paul, MN 55101 (651) 296-3353 Attorneys for Amicus State of Minnesota through Attorney General Lori Swanson

5673390v1

NACDS, et al. APPENDIX

1. Kaiser Family Foundation, Prescription Drug Trends (May 2010) .......... NA. 1

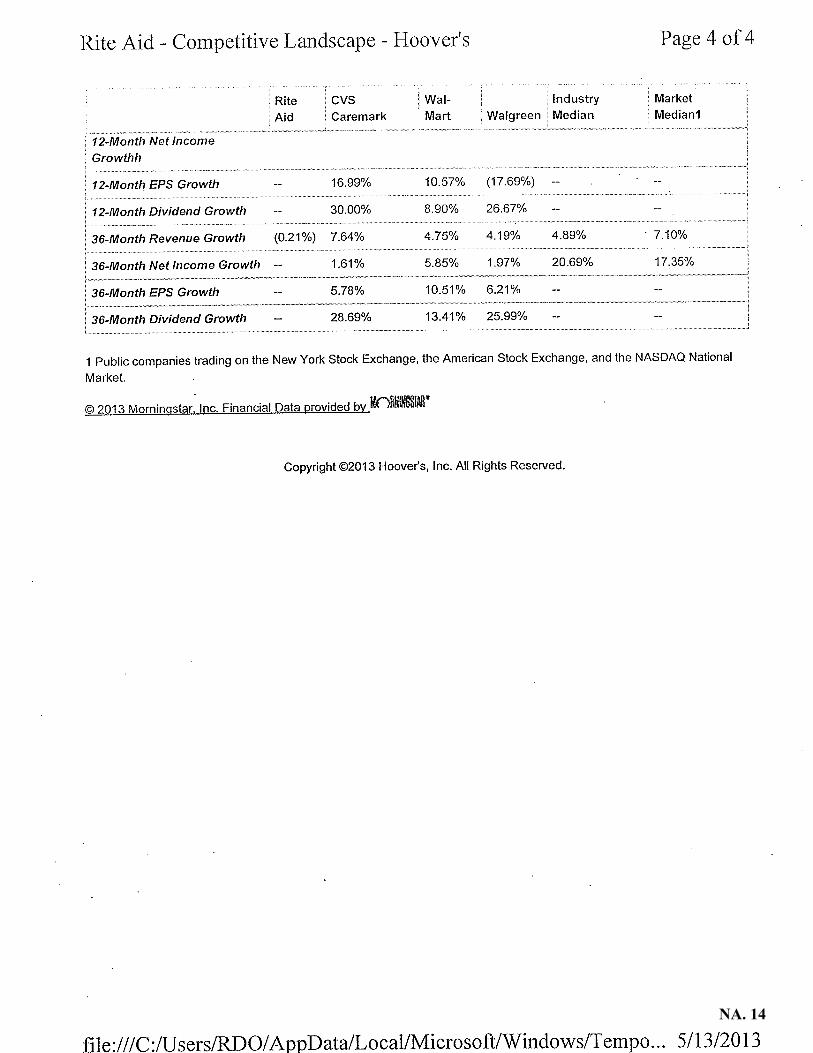

2. Hoovers Competitive Landscape Report ................................................. NA. 11

3. Rural Assistance Center of the U.S. Department of Health and Human Services, Rural Pharmacy and Prescription Drugs, http://www.raconline.org/topics/pharmacy/ (last visited Sep. 3, 2013) ........................................................................................................ NA. 15

4. Mayo Clinic, Brand-name v. Generic Drugs: Is One Better Than the Other?, Medical Edge Newspaper Column (Feb. 3, 2012) ..................... NA. 16

5. United States Food and Drug Administration, Understanding Generic Drugs: Facts About Generic Drugs, FDA.gov, http://www.fda.gov/drugs/resourcesforyou/consumers/ buyingusingmedicinesafely/understandinggenericdrugs/ucm167991.htm (last visited Sep. 3, 2013) ................................................................. NA. 17

6. Kaiser Family Foundation, Follow the Pill: Understanding the U.S. Commercial Pharmaceutical Supply Chain (Mar. 2005) ....................... NA. 19

7. The Federal Reserve Bank of Minneapolis, Cash, Check or Third Party? Prescription Benefit Plans Are Squeezing Retail Pharmacies, Fedgazette (Jan. 1, 2006) .................................................... NA. 51

8. Graphic Communications National, About Us: Plan Design for Local 1B, http://www.gccibthealthfund.org/index-1.html (last visited Sep. 3, 2013) ................................................................................ NA. 58

9. Excerpt of Twin Cities Bakery Drivers Health and Welfare Fund, Summary Plan Description (Sep. 2009) ................................................. N A. 61

10. Centers for Medicare & Medicaid Services, Part II: Draft Methodology for Calculating the National Average Drug Acquisition Cost (May 2012) ...................................................................................... NA. 71

11. Walgreen Co. & The Kroger Co., Declaratory Ruling (W. Va. Bd. of Pharm. Oct. 23, 2012) ............................................................................ NA. 107

The Henry J. Kaiser Family Foundation is a non-profit, private operating foundation dedicated to providing information and analysis on health care issues to

policymakers, the media, the health care community, and the general public. The Foundation is not associated with Kaiser Permanente or Kaiser Industries.

2400 Sand Hill Road, Menlo Park, CA 94025 Phone: (650) 854-9400 Facsimile: (650) 854-4800 www.kff.orgWashington, DC Office: 1330 G Street, NW, Washington, DC 20005 Phone: (202) 347-5270 Facsimile: (202) 347-5274

Prescription Drug Trends

Overview Prescription drugs are vital to preventing and treating illness and in helping to avoid more costly medical problems. Rising drug costs, implementation of the Medicare Part D drug benefit in 2006, and expansion of both the number of people covered by health insurance and the breadth of their benefits from the passage of health reform legislation in March 2010 have highlighted the need for a better understanding of the pharmaceutical market and for new approaches to address increasing prescription costs. Rising Expenditures for Prescription Drugs Spending in the US for prescription drugs was $234.1 billion in 2008, nearly 6 times the $40.3 billion spent in 1990.1 Although prescription drug spending has been a relatively small proportion of national health care spending (10% in 2008, compared to 31% for hospitals and 21% for physician services), it has been one of the fastest growing components, until the early 2000’s growing at double-digit rates compared to single-digit rates for hospital and physician services. Since 2000, the rate of increase in drug spending has declined each year except for 2006, which was the year Medicare Part D was implemented. By 2008, the annual rate of increase in prescription spending was 3%, compared to 5% for hospital care and 5% for physician services (Figure 1). From 1998 to 2008, prescription drugs contributed 13% of the total growth in national health expenditures, compared to 30% for hospital care and 21% for physician and clinical services.2 Annual prescription spending growth slowed from 1999 (18%) to 2005 (6%) because of the increased use of generic drugs, the increase in tiered copayment benefit plans, changes in the types of drugs used, and a decrease in the number of new drugs introduced.3 The annual change in drug spending in 2006 (9%) increased as a result of 1) increased use of prescription drugs which was attributable to a number of factors including the implementation of Medicare Part D, new indications for existing drugs, strong growth in several therapeutic classes, and increased use of specialty drugs; 2) lower rebates from drug manufacturers; and 3) changes in the mix of drugs (both brand versus generic, and changes in the therapeutic mix).4

May 2010

NA. 1

The 2007 change in drug spending (5%) decelerated because of an increase in the generic dispensing rate (which was affected in part by the loss of patent exclusivity for some blockbuster drugs), slower growth in prescription drug prices, and growing consumer safety concerns about certain drugs.5 The 2008 drug spending change (3%) declined (as did the spending growth for most health care goods and services) because of a slight decline in per capita use of prescription drugs due to the impact of the recession, a low number of new drug products, and safety and efficacy concerns.6 The share of prescription drug spending paid by private health insurance increased substantially from 1990 to 2005 (from 26% to 48%), contributing to a decline in the share that people paid out-of-pocket (from 56% to 24%); the public funds (government) share of expenditures increased from 18% in 1990 to 28% in 2005. However, the implementation of the Medicare Part D drug benefit in 2006 substantially changed the mix of funding sources, as the government’s share rose from 28% to 37% between 2005 and 2008, while the private insurance portion fell from 48% to 42%, and the consumer out-of-pocket share declined from 24% to 21% (Figure 2). Medicare’s and Medicaid’s shares of public funding changed when the Medicare drug benefit took effect in 2006: between 2005 and 2008, Medicare’s share grew from 7% to 60%, and Medicaid’s share fell from 70% to 24% (Figure 3) because Medicare replaced Medicaid as the primary source of drug coverage for beneficiaries with coverage under both programs (known as “dual eligibles”).

NA. 2

Factors Driving Changes in Prescription Spending Three main factors drive changes in prescription drug spending: changes in the number of prescriptions dispensed (utilization), price changes, and changes in the types of drugs used.

Utilization. The number of prescriptions dispensed in the US in 2009 increased 2.1% (from 3.8 billion to 3.9 billion), a larger growth rate than the 1.0% increase in 2008 over 2007. From 1999 to 2009, the number of prescriptions increased 39% (from 2.8 billion to 3.9 billion), compared to a US population growth of 9%. The average number of retail prescriptions per capita increased from 10.1 in 1999 to 12.6 in 2009.7 The percent of the population with a prescription drug expense in 2007 was 62%, the same as in 1997. The proportion of those with an expense varied by age -- 58% for those under age 65 and 90% for those 65 and older, with little change since 1997 when the proportions were 59% and 86%, respectively.8 A recent study found that the rate of unfilled prescriptions has increased, from both denials and abandonment. Health plan denials of commercial prescription claims in 2009 were 8.1% for new prescriptions and 4.2% for refills; denials of new brand name drug prescriptions (10.3% in 2009) were down 1.4% from 2008, but were up 22.5% since 2006 (denials are prescriptions that have been submitted to a pharmacy but rejected by a patient’s health plan). Abandoned prescriptions (those that are submitted to a pharmacy but are never picked up) as a percent of commercial prescription drug claims were 6.3% for new prescriptions and 2.6% for refills in 2009; for new brand name prescriptions, the abandonment rate was up 23% from 2008 and up 68% from 2006. Together, health plan denials and patient abandonment resulted in 14.4% of all new, commercial plan prescriptions going unfilled in 2009, up 5.5% from 2008.9 A 2009 study found that the cost of drug-related morbidity, including poor adherence (not taking medication as prescribed by doctors) and suboptimal prescribing, drug administration, and diagnosis, is estimated to be as much as $289 billion annually, about 13% of total health care expenditures. The barriers to medication adherence are many: cost, side effects, the difficulty of managing multiple prescriptions, patients’ understanding of their disease, forgetfulness, cultural and belief systems, imperfect drug regimens, patients’ ability to navigate the health care system, cognitive impairments, and a reduced sense of urgency due to asymptomatic conditions.10 Price. Prescription drug prices as measured by the Consumer Price Index increased 3.4% in 2009, 2.5% in 2008, 1.4% in 2007, and 4.3% in 2006. The average annual growth in prescription drug prices from 2000 to 2009 was 3.6 percent, compared to 4.1% for all medical care and 2.5% for all items.11 Industry data show that retail prescription prices12 (which reflect both manufacturer price changes for existing drugs and changes in use to newer, higher-priced drugs) rose from an average price of $38.43 in 1998 to $71.69 in 2008; the average brand name prescription price in 2008 was almost 4 times the average generic price ($137.90 vs. $35.22).13 Of the average retail prescription price of $71.69, manufacturers received 78%, retailers received 17%, and wholesalers received 4% in 2008.14 Changes in Types of Drugs Used. Prescription drug spending is affected when new drugs enter the market and when existing medications lose patent protection. New drugs can increase overall drug spending if they are used in place of older, less expensive medications; if they supplement rather than replace existing drugs treatments; or if they treat a condition not previously treated with drug therapy. New drugs can reduce drug spending if they come into the market at a lower price than existing drug therapies; this can occur when a new drug enters a therapeutic category with one or two dominant brand competitors. New drug use is affected by the number of new drugs (new molecular entities) approved by the US Food and Drug Administration; approvals have fluctuated over the past decade, with 35 approvals in 1999, 20 in 2005, and 25 in 2009.15 U.S. pharmaceutical research and biotechnology companies spent about $65 million on research and development of new medicines and vaccines in 2009, an Increase of about $1.5 billion over 2008.16 Drug spending is also typically reduced when brand name drugs lose patent protection and face competition from new, lower cost generic substitutes. FDA analysis of 1999-2004 data shows that generic competition is associated with lower drug prices: on average, the first generic competitor prices its product only slightly lower than the brand name manufacturer; the second generic manufacturer reduces the average generic price to nearly half the brand name price; prices continue to fall but more slowly as additional generic manufacturers market the product. For products with a large number of generics, the average generic price falls to 20% of the branded price and lower.17

NA. 3

Almost 80% of FDA-approved drugs have generic counterparts. In 2008, 22% of total prescription drug sales and 72% of total prescriptions dispensed were generic medicines. Generic sales grew 8% from 2005 to 2006.18 Several high-sales brand name drugs are expected to go off-patent in the next 5 years, peaking in 2011 and 2012 when 6 of today’s 10 largest products in the U.S. are expected to face generic competition. While total drug sales may decline as a result, the competition from generic drugs may bring down costs for patients.19 An issue receiving Congressional and Federal Trade Commission attention is the payments that brand name drug companies make to generic drug manufacturers to not release their products for a certain period of time, which the FTC says costs American consumers $3.5 billion per year.20 Advertising. Both prescription use and shifts to higher-priced drugs can be influenced by advertising, which is usually conducted for brand name rather than generic drugs. Manufacturer spending on advertising was over 1.5 times as much in 2009 ($10.9 billion) as in 1999 ($6.6 billion). After increasing every year since 1996, the total amount manufacturers spent on advertising declined from 2004 to 2005 (from $12.1 billion to $11.7 billion), rose to $12.4 billion in 2006, and fell to $11.8 billion in 2007, $11.3 billion in 2008, and $10.9 billion in 2009. The share directed toward consumers in 2009 (through advertising on television, radio, magazines, newspapers, and outdoor advertising), was over twice the amount spent in 1999 ($4.3 billion compared to $1.8 billion), though spending decreased 2% from 2008 ($4.4) to 2009 ($4.3 billion). The share directed toward physicians (through the sales activities of pharmaceutical representatives and through professional journals) in 2009 ($6.6 billion) was almost 1.5 times the amount in 1999 ($4.8 billion); such spending decreased 3% from 2008 ($6.8 billion) to 2009 ($6.6 billion).21 The FDA held hearings in November 2009 and bills have been introduced in the 111th Congress addressing changes to prescription advertising rules, particularly as they relate to on-line advertising. Sales and Profitability. Prescription drug sales were $300.3 billion in 2009, an increase of 5.1% over 2008. This increase was more than 2½ times the 1.9% increase from 2007 to 2008, but lower than the double-digit increases in the early 2000’s. IMS Health attributes the 2009 growth to a stronger demand for prescription drugs despite economic conditions; sustained pricing practices by pharmaceutical manufacturers; inventory management actions by retail pharmacies to bring stocking levels in line with market demand; greater use of specialty pharmaceuticals, which comprise 21% of U.S. market value; lower impact of patent expirations; and no significant product safety issues during the year.22 IMS Health forecasts a 3%-6% annual growth in the U.S. pharmaceutical market in the next 5 years, reaching $360-$390 billion in 2014.23 From 1995 to 2002, pharmaceutical manufacturers were the nation’s most profitable industry (profits as a percent of revenues). They ranked 3rd in profitability in 2003 and 2004, 5th in 2005, 2nd in 2006, and 3rd in 2007 and 2008, with profits of 19.3% in 2008.24 Selected PPACA Changes Affecting the Pharmaceutical Industry. The Patient Protection and Affordable Care Act (PPACA, P.L.11148, enacted March 23, 2010), as amended by the Health Care and Education Reconciliation Act of 2010 (HCERA, P.L.111-152, enacted March 30, 2010), includes several provisions that affect the pharmaceutical industry:

Imposes an annual fee on certain manufacturers and importers of brand name drugs (including biological products but excluding orphan drugs) whose branded sales exceed $5 million: an annual fee of $2.5 billion beginning in 2011, rising to $4.1 billion in 2018 and dropping to $2.8 billion in 2019 and thereafter, allocated across the industry according to the proportion of sales for government programs.

Establishes a process for FDA licensure of biosimilar (i.e., interchangeable) versions of brand name biological products; biological products are granted 12 years of exclusive use before biosimilar versions of a biological product can be approved, with certain drugs receiving additional years of exclusivity; FDA is authorized to collect associated user fees for the review of applications for approval.

Changes certain drug labeling requirements and requires the HHS Secretary to determine whether adding certain information to a prescription drug’s labeling and advertising would improve health care decision-making.

NA. 4

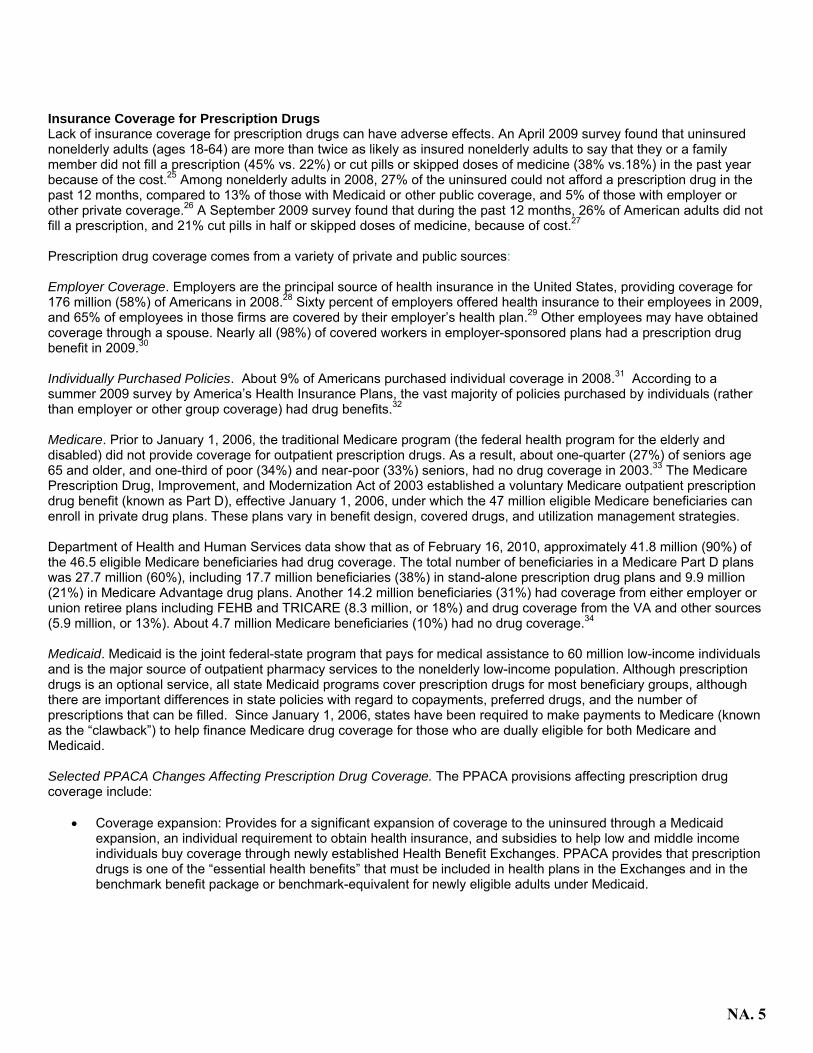

Insurance Coverage for Prescription Drugs Lack of insurance coverage for prescription drugs can have adverse effects. An April 2009 survey found that uninsured nonelderly adults (ages 18-64) are more than twice as likely as insured nonelderly adults to say that they or a family member did not fill a prescription (45% vs. 22%) or cut pills or skipped doses of medicine (38% vs.18%) in the past year because of the cost.25 Among nonelderly adults in 2008, 27% of the uninsured could not afford a prescription drug in the past 12 months, compared to 13% of those with Medicaid or other public coverage, and 5% of those with employer or other private coverage.26 A September 2009 survey found that during the past 12 months, 26% of American adults did not fill a prescription, and 21% cut pills in half or skipped doses of medicine, because of cost.27 Prescription drug coverage comes from a variety of private and public sources: Employer Coverage. Employers are the principal source of health insurance in the United States, providing coverage for 176 million (58%) of Americans in 2008.28 Sixty percent of employers offered health insurance to their employees in 2009, and 65% of employees in those firms are covered by their employer’s health plan.29 Other employees may have obtained coverage through a spouse. Nearly all (98%) of covered workers in employer-sponsored plans had a prescription drug benefit in 2009.30 Individually Purchased Policies. About 9% of Americans purchased individual coverage in 2008.31 According to a summer 2009 survey by America’s Health Insurance Plans, the vast majority of policies purchased by individuals (rather than employer or other group coverage) had drug benefits.32 Medicare. Prior to January 1, 2006, the traditional Medicare program (the federal health program for the elderly and disabled) did not provide coverage for outpatient prescription drugs. As a result, about one-quarter (27%) of seniors age 65 and older, and one-third of poor (34%) and near-poor (33%) seniors, had no drug coverage in 2003.33 The Medicare Prescription Drug, Improvement, and Modernization Act of 2003 established a voluntary Medicare outpatient prescription drug benefit (known as Part D), effective January 1, 2006, under which the 47 million eligible Medicare beneficiaries can enroll in private drug plans. These plans vary in benefit design, covered drugs, and utilization management strategies. Department of Health and Human Services data show that as of February 16, 2010, approximately 41.8 million (90%) of the 46.5 eligible Medicare beneficiaries had drug coverage. The total number of beneficiaries in a Medicare Part D plans was 27.7 million (60%), including 17.7 million beneficiaries (38%) in stand-alone prescription drug plans and 9.9 million (21%) in Medicare Advantage drug plans. Another 14.2 million beneficiaries (31%) had coverage from either employer or union retiree plans including FEHB and TRICARE (8.3 million, or 18%) and drug coverage from the VA and other sources (5.9 million, or 13%). About 4.7 million Medicare beneficiaries (10%) had no drug coverage.34 Medicaid. Medicaid is the joint federal-state program that pays for medical assistance to 60 million low-income individuals and is the major source of outpatient pharmacy services to the nonelderly low-income population. Although prescription drugs is an optional service, all state Medicaid programs cover prescription drugs for most beneficiary groups, although there are important differences in state policies with regard to copayments, preferred drugs, and the number of prescriptions that can be filled. Since January 1, 2006, states have been required to make payments to Medicare (known as the “clawback”) to help finance Medicare drug coverage for those who are dually eligible for both Medicare and Medicaid. Selected PPACA Changes Affecting Prescription Drug Coverage. The PPACA provisions affecting prescription drug coverage include:

Coverage expansion: Provides for a significant expansion of coverage to the uninsured through a Medicaid expansion, an individual requirement to obtain health insurance, and subsidies to help low and middle income individuals buy coverage through newly established Health Benefit Exchanges. PPACA provides that prescription drugs is one of the “essential health benefits” that must be included in health plans in the Exchanges and in the benchmark benefit package or benchmark-equivalent for newly eligible adults under Medicaid.

NA. 5

Medicare changes: Provides for a $250 rebate to Medicare Part D beneficiaries with out-of-pocket spending in the Medicare Part D coverage gap in 2010, a 50% discount for brand name drugs for beneficiaries in the coverage gap starting in 2011, a phasing-in of coverage in the gap for generic and brand name drugs which will reduce the beneficiary coinsurance rate from 100% in 2010 to 25% in 2020, a reduction between 2014 and 2019 in the threshold that qualifies enrollees for catastrophic coverage, and elimination of the tax deduction for employers who receive Medicare Part D retiree drug subsidy payments, starting in 2013.

Responses to Increasing Prescription Drug Costs A variety of public and private strategies have been implemented to attempt to contain rising costs for prescription drugs, as described below.35 Utilization Management Strategies. Health plans have responded to rising prescription drug costs by increasing enrollee cost-sharing amounts, using formularies to exclude certain drugs from coverage, applying quantity dispensing limits, requiring prior authorization, and using step therapy (starting with the most cost-effective drug and progressing to more costly therapy only if necessary). In 2009, over three-quarters (78%) of workers with employer-sponsored coverage were in plans with 3 or more 4 tiers of cost sharing for prescription drugs, almost 3 times the proportion in 2000 (27%).36 Worker copayments have increased from 2000-2009: 25% for generic drugs, 80% for preferred drugs, 59% for nonpreferred drugs, and 44% for fourth-tier drugs (data from 2004-2009) (Figure 4). The average copayment amounts in 2009 were $10 for generics, $27 for preferred drugs, $46 for nonpreferred drugs, and $85 for fourth-tier drugs. Twelve percent of covered workers had a separate annual drug deductible which averaged $108. A 2009 survey of individually purchased health policies found that the vast majority had drug benefits, with copayments being the predominant form of cost sharing. All HMOs and the majority of PPO/POS policies charged copayments which averaged, respectively, about $10/$13 for generic drugs, $26/$28 for preferred brand name drugs, and $44/$48 for non-formulary drugs. Fewer than half of the PPO/POS policies had a prescription drug deductible (averaging $481 for single coverage and $833 for family coverage); over half of the HMOs had a drug deductible (averaging $320 for single coverage and $1,002 for family coverage).37 Discounts and Rebates. Private and public drug programs negotiate with pharmaceutical manufacturers (often using contracted organizations known as pharmacy benefit managers) to receive discounts and rebates which are applied based on volume, prompt payment, and market share. Manufacturers who want their drugs covered by Medicaid must provide rebates to state Medicaid programs for the drugs they purchase; many states have also negotiated additional rebates, known as supplemental rebates.

NA. 6

Several federal government agencies, including the Department of Veterans Affairs, the Defense Department, the Public Health Service, and the Coast Guard, participate in a program known as the Federal Supply Schedule through which they purchase drugs from manufacturers at prices equal to or lower than those charged to their “most-favored” nonfederal purchasers.38 In order to participate in Medicaid, another program, the Section 340B Program, requires manufacturers to provide drugs to certain nonfederal entities (such as community health centers and disproportionate share hospitals) at discounted prices. PPACA expands the entities that qualify for the program to include non-PPS children’s and free-standing cancer hospitals, critical access hospitals and sole community hospitals, and rural referral centers; establishes new auditing, reporting, and other compliance requirements; and provides for an alternative dispute resolution process and penalties for violations.39 Medicaid. Historically, prescription drugs have been one of the fastest-growing Medicaid services, The Deficit Reduction Act of 2005 gave states more authority to control Medicaid drug spending through increased cost sharing for non-preferred drugs, changes in the way Medicaid pays pharmacists, allowing pharmacists to refuse prescriptions for beneficiaries who don’t pay their cost sharing, and inclusion of authorized generic drugs in the calculation of “best price” for drugs. By 2007, most states had already implemented many of these approaches, so new action to control drug spending slowed.40 A 2009 survey of 50 states+DC found that more than half had Medicaid pharmacy cost containment measures in place by FY2009, including preferred drug lists and prior authorization programs (about 45% of states), supplemental rebates from manufacturers and state Maximum Allowable Cost programs for generic and multi-source brand drugs (44%); smaller proportions of states were members of multi-state purchasing coalitions (26%) or had limits on quantities dispensed per prescription (16%).41 Medicaid spent $19.4 billion for prescription drugs in 2008, an increase of 3.5% over 2007; Medicaid drug spending decreased 1.7% between 2006 and 2007.42 Medicaid requires drug manufacturers who want to sell their products to Medicaid patients to agree to pay rebates to states for outpatient drugs purchased on behalf of Medicaid beneficiaries. PPACA increases the Medicaid drug rebate percentages for several types of outpatient drugs and requires that the resulting savings be remitted to the federal government. The law also extends the drug rebate to Medicare Managed Care Organizations and allows states to retain a portion of the savings generated from these rebates. Medicare. The Medicare Part D drug benefit shifted spending from the private sector and Medicaid to Medicare, making Medicare the nation’s largest public payer of prescription drugs (from 7% in 2005 to 60% in 2008). Medicare prescription drug spending as a share of total US prescription spending rose from 2% in 2005 to 22% in 2008. Medicare prescription drug spending totaled $52.1 billion in 2008, an increase of 13% over 2007.43 Part D plans use various cost containment approaches including tiered cost sharing, formulary coverage that varies considerably across plans, and utilization management (UM) restrictions such as prior authorization, step therapy, or quantity limits; UM use among stand-alone drug plans has increased from 18% in 2007 to 28% in 2009.44 Medicare is prohibited by law from directly negotiating drug prices or rebates with manufacturers to control costs. In the 110th Congress, the 2008 presidential campaign, and the 111th Congress, proposals to allow or require Medicare to negotiate drug prices with drug makers have been considered but not enacted. Purchasing Pools. Some public and private organizations have banded together to form prescription drug purchasing pools to increase their purchasing power through higher volume and shared expertise. Examples include joint purchasing by the Department of Defense and VA; multi-state bulk buying pools through which states purchase drugs for their Medicaid, state employees, senior/low-income/uninsured pharmacy assistance programs, or other public programs; and individual state purchasing pools.45 Consumers. Consumers are turning to a variety of methods to reduce their prescription costs,46 including requesting cheaper drugs or generic drugs from their physicians and pharmacies, using the Internet and other sources to make price comparisons, using the Internet to purchase drugs, buying at discount stores, buying over-the-counter instead of prescribed drugs, buying drugs in bulk and pill-splitting, using mail-order pharmacies,47 and using pharmaceutical company or state drug assistance programs. Over half of physicians say they frequently talk with patients about the out-of-pocket costs of medicines they prescribe, 62% say they switch patients to less expensive drugs, and 58% say they give patients office samples.48

NA. 7

Importation. The high cost of prescriptions has led some to suggest that individuals be permitted to purchase prescription products from distributors in Canada or other countries (called “importation,” or “reimportation” if the drug is manufactured in the US). Although it is generally not lawful for individuals or commercial entities such as pharmacies or wholesalers to purchase prescription drugs from other countries, the government does not always act to stop individuals from purchasing drug products abroad. Importation of pharmaceutical products from Canada through Internet sales and travel to Canada totaled about $700 million in sales in 2003, or 0.3% of total US prescription sales. An equivalent amount of prescription drugs was estimated to have entered the US from the rest of the world, mostly through the mail and courier services.49 P.L. 109-295 (enacted in 2006) allows US residents to transport up to a 90-day supply of qualified drugs from Canada to the US. Importation issues such as actual savings amounts, drug safety, and marketplace competition and pricing continue to be debated. Outlook for the Future HHS projects US prescription drug spending to increase from $234.1 billion in 2008 to $457.8 billion in 2019, almost doubling over the 11-year period. The average annual increase in drug spending from the previous year is projected to increase from 3.2% in 2008 to 5.2% in 2009 (reflecting growth in the use of prescription drugs per person, driven by an increase in the use of anti-viral drugs related to the H1N1 virus), and then rise to 7.3% in 2019 (reflecting increases in drugs prices, the number of new drug approvals, and the share of expensive specialty drugs). Drug spending as a percent of overall national health spending is projected to increase somewhat from 10.0% in 2008 to 10.2% in 2019.50 In the coming years, implementation of various provisions of PPACA will affect prescription drug coverage, utilization, prices, and regulation. Coverage and utilization of prescription drugs will be expanded by PPACA’s health insurance mandate and premium and cost-sharing subsidies; the designation of prescription drugs as an essential health benefit to be covered by private health plans through the new health benefit Exchanges and by Medicaid for newly eligible adults; and Medicare’s prescription drug rebate, cost-sharing, and catastrophic threshold changes. Prices charged to government programs will be affected by changes to Medicaid rebate requirements and expansions to the Section 340B program. Prescription drug regulation will be affected by the new process for licensure of biosimilar versions of brand name biological products and by drug labeling requirements. These and other PPACA changes will ultimately impact national spending for prescription drugs in ways yet to be seen.

NA. 8

1 All spending amounts in this report are in current dollars (i.e., not adjusted for inflation.) 2 Centers for Medicare & Medicaid Services, National Health Expenditure Accounts, Historical, http://www.cms.gov/NationalHealthExpendData/, accessed October 6, 2009. 3 Aaron Catlin et al., “National Health Spending In 2005: The Slowdown Continues, “Health Affairs 26, no. 1 (January/February 2007)142-153. 4 Aaron Catlin et al., “National Health Spending In 2006: A Year Of Change For Prescription Drugs,” Health Affairs 27, no. 1 (January/February 2008), 14-29. 5 Micah Hartman et al., “National Health Spending In 2007: Slower Drug Spending Contributes To Lowest Rate Of Overall Growth Since 1998,” Health Affairs 28, no. 1 (January/February 2009) 246-261. 6 Micah Hartman et al., “Health Spending Growth At A Historic Low In 2008,” Health Affairs 29, no. 1 (January 2010)147-155. 7 Kaiser Family Foundation calculations using data from IMS Health, http://www.imshealth.com (Press Room, US Top-Line Industry Data 2008), and Census Bureau, http;//www.census.gov. The per capita number may differ from the number reported at KFF’s website www.statehealthfacts.org because of differing data sources which use different retail pharmacy definitions (e.g., IMS Health includes mail order, Verispan does not). 8 Agency for Healthcare Research and Quality, Medical Expenditure Panel Survey Component Data, “Prescription Medicines – Mean and Median Expenses per Person With Expense and Distribution of Expenses by Source of Payment,” table 2, 1997 and 2007, http://www.meps.ahrq.gov/mepsweb/, accessed March 5, 2010. 9 Wolters Kluwer Pharma Solutions, Inc., Pharma Insight 2009: Patients take More Power Over Prescription Decisions (March 2010), http://www.wolterskluwerpharma.com/Press/Pharma%20Insight%202009%20-%20Media.pdf. 10 New England Healthcare Institute, Thinking Outside the Pillbox: A System-wide Approach to Improving Patient Medication Adherence for Chronic Disease (August 2009), http://www.nehi.net/publications/44/thinking_outside_the_pillbox_a_systemwide_approach_to_improving_patient_medication_adherence_for_chronic_disease. 11 Kaiser Family Foundation analysis of Consumer Price Index, All Urban Consumers, U.S. City Average, not seasonally adjusted, http://www.bls.gov/cpi/home.htm, accessed April 28, 2010. 12 Retail prescription prices reflect the prices paid by insured and uninsured patients, and do not reflect rebates, discounts, and other payments that in effect lower the cost of prescriptions. 13 National Association of Chain Drug Stores, “Industry Facts-at-a-Glance,” http://www.nacds.org (based on data from IMS Health), accessed March 8, 2010. 14 Ibid. 15 US Food and Drug Administration, http://www.fda.gov/Drugs/DevelopmentApprovalProcess/HowDrugsareDevelopedandApproved/DrugandBiologicApprovalReports/ucm121136.htm ; 2004-2009 data include new BLAs (biologic license applications) for therapeutic biologic products transferred from FDA’s Center for Biologics Evaluation and Research to its Center for Drug Evaluation and Research. 16 PhRMA, “R&D Investment by U.S. Biopharmaceutical Companies Remains Strong Despite Ongoing Economic Challenges,” March 16, 2010, http://www.phrma.org/news/news/rd_investment_us_biopharmaceutical_companies_remains_strong_despite_ongoing_economic_chall 17 US Food and Drug Administration, Center for Drug Evaluation and Research, “Generic Competition and Drug Prices,” http://www.fda.gov/AboutFDA/CentersOffices/CDER/ucm129385.htm, accessed March 12, 2010. 18 Generic Pharmaceutical Association, http://www.gphaonline.org/Content/NavigationMenu/AboutGenerics/Statistics/default.htm. 19 IMS Health, “IMS Forecasts Global Pharmaceutical Market Growth of 5-8% Annually Through 2014; Maintains Expectations of 4-6% Growth in 2010,” April 20, 2010, http://www.imshealth.com (Press Room, Press Releases). 20 Federal Trade Commission, “Pay-for-Delay: How Drug Company Pay-Offs Cost Consumers Billions,” January 2010, http://www.ftc.gov/os/2010/01/100112payfordelayrpt.pdf. 21 IMS Health, http://www.imshealth.com (Press Room, US Top-Line Industry Data 2009); Kaiser Family Foundation, Prescription Drug Trends, a chartbook, (July 2000), ex. 3.13, http://www.kff.org/rxdrugs/3019-index.cfm. The data on spending for advertising directed towards physicians excludes the retail value of drug samples left at sales visits to physicians’ offices, which totaled about $16 billion in 2004, the last year such data were available online from IMS Health. 22 IMS Health, “IMS Health Reports U.S. Prescription Sales Grew 5.1 Percent in 2009, to $300.3 Billion” (April 1, 2010), online at http://www.imshealth.com (Press Room, Press Releases). 23 IMS Health Press Release, ibid., April 20, 2010. 24 Fortune 500 online, http://money.cnn.com/magazines/fortune/fortune500/2009/performers/industries/profits/, and personal communication; April issues of Fortune magazine. 25 Kaiser Family Foundation, Kaiser Public Opinion Survey Brief, Economic Problems Facing Families (April 2008), p. 4, http://www.kff.org/kaiserpolls/upload/7773.pdf. 26 Kaiser Family Foundation, The Uninsured, A Primer (October 2009), p. 7, http://www.kff.org/uninsured/upload/7451-05.pdf, using Kaiser Commission on Medicaid and the Uninsured analysis of 2008 NHIS data. 27 Kaiser Family Foundation, Kaiser Health Tracking Poll (September 2009), http://www.kff.org/kaiserpolls/7990.cfm. 28 US Census Bureau, Income, Poverty and Health Insurance Coverage in the United States:2008 (September 2009), Table C-1, p. 59, http://www.census.gov/prod/2009pubs/p60-236.pdf. 29 Kaiser Family Foundation and Health Research and Educational Trust, Employer Health Benefits 2009 Annual Survey (September 2009), pp.37 and 55, http://ehbs.kff.org/pdf/2009/7936.pdf. 30 Ibid, p.170, http://ehbs.kff.org/pdf/2009/7936.pdf. 31 US Census Bureau, op. cit., p. 59. 32 America’s Health Insurance Plans, Center for Policy and Research, “Individual Health Insurance 2009 – A Comprehensive Survey of Premiums, Availability, and Benefits” (October 2009), http://www.ahipresearch.org/pdfs/2009IndividualMarketSurveyFinalReport.pdf. 33 Dana Gelb Safran et al., “Prescription Drug Coverage And Seniors: Findings From A 2003 National Survey,” Health Affairs, Web Exclusive (April 19, 2005): W5-160, http://www.kff.org/medicare/med041905pkg.cfm. 34 Kaiser Family Foundation, Medicare: A Primer (April 2010), p.8, http://www.kff.org/medicare/upload/7615-03.pdf. 35 See also Kaiser Family Foundation, Cost Containment Strategies For Prescription Drugs: Assessing The Evidence In the Literature (March 2005), http://www.kff.org/rxdrugs/loader.cfm?url=/commonspot/security/getfile.cfm&PageID=51885.

NA. 9

36 Kaiser Family Foundation and Health Research and Educational Trust, op. cit., Ex. 9.1, http://ehbs.kff.org/?page=charts&id=2&sn=24&ch=1136. 37 America’s Health Insurance Plans, Center for Policy and Research, Individual Health Insurance 2009: A Comprehensive Survey of Premiums, Availability, and Benefits (October 2009), http://www.ahipresearch.org/pdfs/2009IndividualMarketSurveyFinalReport.pdf. 38 Congressional Budget Office, Prices for Brand-Name Drugs Under Selected Federal Programs (June 2005), http://www.cbo.gov/ftpdocs/64xx/doc6481/06-16-PrescriptDrug.pdf. 39 http://www.hrsa.gov/opa/introduction.htm and Section 7101 of PPACA as modified by Sec. 2302 of HCERA. 40 Kaiser Commission on Medicaid and the Uninsured, Few Options for States to Control Medicaid Spending in a Declining Economy (April 2008), p. 3, http://www.kff.org/medicaid/upload/7769.pdf. 41 Kaiser Family Foundation calculations using data from Vernon Smith et al., The Crunch Continues: Medicaid Spending, Coverage and Policy in the Midst of a Recession: Results from a 50-State Medicaid Budget Survey for State Fiscal Years 2009 and 2010 (Kaiser Commission on Medicaid and the Uninsured, September 2009), p. 48, fig. 32, http://www.kff.org/medicaid/upload/7985.pdf. 42 Centers for Medicare and Medicaid Services, Office of the Actuary, National Health Statistics Group, at http://www.cms.hhs.gov/NationalHealthExpendData/. 43 Ibid. 44 Kaiser Family Foundation, Medicare Prescription Drug Plans in 2009 and Key Changes Since 2006: Summary of Findings (June 2009), http://www.kff.org/medicare/7917.cfm. 45 National Conference of State Legislatures, “Pharmaceutical Bulk Purchasing: Multi-state and Inter-agency Plans, 2008 edition” (Updated May 8, 2008), http://www.ncsl.org/programs/health/bulkrx.htm. 46 Devon Herrick, National Center for Policy Analysis, Shopping for Drugs: 2004, National Center for Policy Analysis, Policy Report No. 270 (October 2004), http://www.ncpa.org/pub/st/st270. 47US mail services sales have increased 54% since 2003, though their share of total US prescription sales has increased only slightly -- 2007: $44.6 billion in sales, 16% of total prescription sales; 2003: $28.9 billion in sales, 13% of total prescription sales. IMS Health, http://www.imshealth.com (About Us, Press Room, US Top-Line Industry Data, 2007 U.S). 48 Kaiser Family Foundation, Prescription Drugs: Advertising, Out-of-Pocket Costs, and Patient Safety from the Perspective of Doctors and Pharmacists (November 2006), http://www.kff.org/kaiserpolls/upload/7583.pdf. 49 US Department of Health and Human Services Task Force on Drug Importation, Report on Prescription Drug Importation (December 2004), ix, http://www.hhs.gov/importtaskforce/Report1220.pdf. 50 Christopher J. Truffer et al., ”Health Spending Projections Through 2019: The Recession’s Impact Continues,” Health Affairs 29, no.3 (March 2010), 522-529. For More Information: In addition to the Kaiser Family Foundation reports found in the Endnotes above, this Fact Sheet (#3057-08) and the following reports are available on the Foundation’s website at http://www.kff.org: Trends and Indicators in the Changing Health Care Marketplace (#7031), Prescription Drug Trends—A Chartbook Update (#3112), Cost Containment Strategies for Prescription Drugs: Assessing the Evidence in the Literature (#7295), Follow the Pill: Understanding the U.S. Commercial Pharmaceutical Supply Chain (#7296), Medicare Prescription Drug Benefit Fact Sheet (#7044-10), Medicare Payments and Beneficiary Costs for Prescription Drug Coverage (#7620), several Data Spotlights on the Medicare Part D drug benefit, Explaining Health Care Reform: Key Changes to the Medicare Part D Drug Benefit Coverage Gap (#8059), Federal Policies Affecting the Cost and Availability of New Pharmaceuticals (#3254), Views on Prescription Drugs & the Pharmaceutical Industry, Public and Physician Views of Direct-to-Consumer Prescription Drug Advertising. See also http://www.statehealthfacts.org for state-specific prescription drug utilization and sales (under Health Costs & Budgets); http://www.kaiserEDU.org (Prescription Drugs) for a Tutorial, Issue Modules, and SmartLinks on prescription drugs; and http://facts.kff.org/ (search for Prescription Drugs) for Fast Facts about prescription drugs.

Prepared by Janet Lundy of the Kaiser Family Foundation.

This publication (#3057-08) is available on the Kaiser Family Foundation’s website at www.kff.org.

NA. 10

NA. 11

NA. 12

NA. 13

NA. 14

pment, technicalrole in the health

Rural Pharmacy and Prescription Drugs Introduction - Rural Assistance C... http://www.raconline.org/topics/pharmacy-and-prescription-drugs/

1 of 1 9/3/2013 5:20 PM

NA. 15

Share on:

Share on:

Brand-name vs. Generic Drugs: Is One Better Than the Other?

February 3, 2012

Dear Mayo Clinic:

If a generic drug really is the same thing as the brand-name version, why are generic drugs so much cheaper? How do I find out if a generic form is available for

some of my medications?

Answer:

The active ingredients in generic drugs are the same as in brand-name drugs. However, they may look different or have different inactive ingredients, such as fillers or

coloring agents. Generic drugs approved by the Food and Drug Administration (FDA) must meet the same rigid standards of strength, quality and purity that are

applied to brand-name drugs. For example, they must be manufactured in a way that's approved by the FDA. In addition, it must be shown that a generic drug

provides an identical or nearly identical blood level of the drug compared to the brand version. In short, every type of regulation that's applied to brand-name drugs by

the FDA is also applied to FDA-approved generic drugs.

Still, myths persist that generic drugs are significantly different from brand-name drugs. If you stick to buying a brand-name drug because you feel that a generic isn't

the same, you're likely spending more money than is necessary.

Generic drugs are less expensive because the companies that make them don't need to spend money on drug research and development, clinical trials, marketing,

and advertising — as do brand-name drug manufacturers. These costs can run into the hundreds of millions of dollars for a single drug.

Once patents and exclusive sales rights of a brand-name drug have expired, generic drugs can begin to enter the market. A generic drug manufacturer needs only to

understand the known chemistry of a brand drug, and then develop a method for manufacturing a product that meets FDA standards.

That said, it can take decades for a brand-name drug to become available as a generic. The initial patent life of a new drug is 20 years, but a patent can be obtained

at any point in the drug-development stage. If a patent is obtained early, research and development time may eat up a decade or more of patent life before the FDA

approves the drug for use. A patent obtained later in the development process may buy more time for the drug to be sold under patent protection.

Beyond the initial patent time, patent extensions of up to five years may be granted if FDA regulatory delays slow the process of bringing the drug to market. In

addition, studying a drug for pediatric use may add six months to the patent extension, even if the drug is never used for children.

After FDA approval of a drug, the FDA may allow a drug company to remain the exclusive seller. Exclusive seller extensions lasting months to years may be added

for a number of reasons. The goal of these extensions is to find a balance between consumer-friendly pricing and offering drug companies enough profit incentive to

continue to invest in research.

The FDA frequently grants a six-month period of exclusive marketing rights to the first generic manufacturer of a brand name drug. Typically, the price of that first

generic is about 6 percent lower than the brand-name. If the initial generic is widely used, chances are good that several other generic manufacturers will enter the

arena and the price usually drops substantially.

When two or more generic manufacturers make a drug, the price of the generic drug is often about 50 to 95 percent less than the cost of the brand-name drug. The

extent of the price drop usually depends on how many manufacturers make the drug and how difficult the drug is to make.

Often state laws and insurance copay rules — not to mention the vigilance of doctors and pharmacists — can alert you or even prevent you from buying a

brand-name drug when a less expensive generic alternative is available. Medicare Part D insurance plans report that when a generic drug is available, it's dispensed

89 percent of the time on average over the brand-name equivalent. However, your doctor can still prescribe a brand-name drug over a generic, if necessary.

Even with this level of consumer protection, it doesn't hurt to ask your doctor or pharmacist if there's a generic alternative to any name brand drug you're taking. Tell

your doctor that you're willing to work together on an ongoing basis to identify medications that meet your health needs but aren't necessarily the latest, heavily

marketed brand-name drugs on the market.

— Lisa Buss Preszler, Pharm.D., R.Ph., Mayo Clinic, Rochester, Minn.

Brand-name vs. Generic Drugs: Is One Better Than the Other? http://www.mayoclinic.org/medical-edge-newspaper-2012/feb-03b.html

1 of 2 9/3/2013 5:25 PM

NA. 16

FACT: FDA requires generic drugs to have the same quality and performance as brand name drugs.

When a generic drug product is approved, it has met rigorous standards established by the FDA with respect to identity, strength, quality, purity, and potency. However, some variability can and does occur during manufacturing, for both brand name and generic drugs. When a drug, generic or brand name, is mass-produced, very small variations in purity, size, strength, and other parameters are permitted. FDA limits how much variability is acceptable.

Generic drugs are required to have the same active ingredient, strength, dosage form, and route of administration as the brand name product. Generic drugs do not need to contain the same inactive ingredients as the brand name product.

The generic drug manufacturer must prove its drug is the same as (bioequivalent) the brand name drug. For example, after the patient takes the generic drug, the amount of drug in the bloodstream is measured. If the levels of the drug in the bloodstream are the same as the levels found when the brand name product is used, the generic drug will work the same.

Through review of bioequivalence data, FDA ensures that the generic product performs the same as its respective brand name product. This standard applies to all generic drugs, whether immediate or controlled release.

All generic manufacturing, packaging, and testing sites must pass the same quality standards as those of brand name drugs, and the generic products must meet the same exacting specifications as any brand name product. In fact, many generic drugs are made in the same manufacturing plants as brand name drug products.

FACT: Research shows that generics work just as well as brand name drugs.

A study evaluated the results of 38 published clinical trials that compared cardiovascular generic drugs to their brand name counterparts. There was no evidence that brand name heart drugs worked any better than generic heart drugs.[1]

FACT: FDA does not allow a 45 percent difference in the effectiveness of the generic drug product.

FDA recently evaluated 2,070 human studies conducted between 1996 and 2007. These studies compared the absorption of brand name and generic drugs into a person’s body. These studies were submitted to FDA to support approval of generics. The average difference in absorption into the body between the generic and the brand name was 3.5 percent[2]. Some generics were absorbed slightly more, some slightly less. This amount of difference would be expected and acceptable, whether for one batch of brand name drug tested against another batch of the same brand, or for a generic tested against a brand name drug. In fact, there have been studies in which brand name drugs were compared with themselves as well as with a generic. As a rule, the difference for the generic-to-brand comparison was about the same as the brand-to-brand comparison.

Any generic drug modeled after a single, brand name drug must perform approximately the same in the body as the brand name drug. There will always be a slight, but not medically important, level of natural variability – just as there is for one batch of brand name drug compared to the next batch of brand name product.

FACT: When it comes to price, there is a big difference between generic and brand name drugs. On average, the cost of a generic drug is 80 to 85 percent lower than the brand name product.

In 2010 alone, the use of FDA-approved generics saved $158 billion, an average of $3 billion every week.[3]

FACT: Cheaper does not mean lower quality.

Facts about Generic Drugs

Today, nearly 8 in 10 prescriptions filled in the United States are for generic drugs. The use of generic drugs is expected to grow over the next few years as a number of popular drugs come off patent through 2015. Here are some facts about generic drugs:

Click image to view larger graphic. 1

Drugs

Home Drugs Resources for You Information for Consumers (Drugs)

Understanding Generic Drugs > Facts about Generic Drugs

Tuesday, September 03, 2013http://www.fda.gov/drugs/resourcesforyou/consumers/%20buyingusing...

NA. 17

Page Last Updated: 09/19/2012 Note: If you need help accessing information in different file formats, see Instructions for Downloading Viewers and Players.

Accessibility Contact FDA Careers FDA Basics FOIA No Fear Act Site Map Transparency Website Policies

U.S. Food and Drug Administration 10903 New Hampshire Avenue Silver Spring, MD 20993 Ph. 1-888-INFO-FDA (1-888-463-6332) Email FDA

For Government For Press Combination Products Advisory Committees Science & Research Regulatory Information Safety Emergency Preparedness International Programs News & Events Training and Continuing Education Inspections/Compliance State & Local Officials Consumers Industry Health Professionals FDA Archive

1. /Drugs/ResourcesForYou/Consumers/BuyingUsingMedicineSafely/UnderstandingGenericDrugs/ucm305896.htm

Generic manufacturers are able to sell their products for lower prices because they are not required to repeat the costly clinical trials of new drugs and generally do not pay for costly advertising, marketing, and promotion. In addition, multiple generic companies are often approved to market a single product; this creates competition in the market place, often resulting in lower prices.

FACT: FDA monitors adverse events reports for generic drugs.

The monitoring of adverse events for all drug products, including generic drugs, is one aspect of the overall FDA effort to evaluate the safety of drugs after approval. Many times, reports of adverse events describe a known reaction to the active drug ingredient.

Reports are monitored and investigated, when appropriate. The investigations may lead to changes in how a product (brand name and generic counterparts) is used or manufactured.

FACT: FDA is actively engaged in making all regulated products – including generic drugs – safer.

FDA is aware that there are reports noting that some people may experience an undesired effect when switching from brand name drug to a generic formulation or from one generic drug to another generic drug. FDA wants to understand what may cause problems with certain formulations if, in fact, they are linked to specific generic products.

FDA is encouraging the generic industry to investigate whether, and under what circumstances, such problems occur. The Agency does not have the resources to perform independent clinical studies and lacks the regulatory authority to require industry to conduct such studies. FDA will continue to investigate these reports to ensure that it has all the facts about these treatment failures and will make recommendations to healthcare professionals and the public if the need arises.

[1] Kesselheim et al. Clinical equivalence of generic and brand name drugs used in cardiovascular disease: a systematic review and meta-analysis. JAMA. 2008;300(21)2514-2526 [2] Davit et al. Comparing generic and innovator drugs: a review of 12 years of bioequivalence data from the United States Food and Drug Administration. Ann Pharmacother. 2009;43(10):1583-97. [3] SAVINGS An Economic Analysis of Generic Drug Usage in the U.S., GPhA, September 2011, page 1.

Links on this page:

Understanding Generic Drugs > Facts about Generic Drugs

Tuesday, September 03, 2013http://www.fda.gov/drugs/resourcesforyou/consumers/%20buyingusing...

NA. 18

Prepared for The Kaiser Family Foundation by:

The Health Strategies Consultancy LLC

March 2005

Follow The Pill:Understanding the U.S. Commercial Pharmaceutical Supply Chain

NA. 19

Table of Contents

I. Executive Summary

II. The Flow of Goods from Manufacturers to Consumers in the U.S.

Pharmaceutical Supply Chain Pharmaceutical Manufacturers Wholesale Distributors Pharmacies Pharmacy Benefit Managers (PBMs)

III. The Flow of Money and Key Financial Relationships in the U.S. Pharmaceutical Supply Chain

Pharmaceutical Manufacturers Wholesale Distributors Pharmacies Pharmacy Benefit Managers (PBMs)

IV. Conclusion

V. Appendix

A. Special Pricing Rules Applicable to Federal Programs Medicaid

Department of Veteran Affairs, Department of Defense, Public Health Service, Coast Guard

Section 340B Drug Pricing Program

B. Other Stakeholders in the U.S. Commercial Supply Chain Physicians Large Employers Health Plans

VI. Key Acronyms and Glossary of Key Terms

NA. 20

I. Executive Summary The pharmaceutical supply chain is the means through which prescription medicines are delivered to patients. Pharmaceuticals originate in manufacturing sites; are transferred to wholesale distributors; stocked at retail, mail-order, and other types of pharmacies; subject to price negotiations and processed through quality and utilization management screens by pharmacy benefit management companies (PBMs); dispensed by pharmacies; and ultimately delivered to and taken by patients. There are many variations on this basic structure, as the players in the supply chain are constantly evolving, and commercial relationships vary considerably by geography, type of medication, and other factors. The intent of this paper is to demystify the U.S. pharmaceutical supply chain. The first section of the paper describes each of the key players (i.e., industry segments) involved in the process of supplying prescription drugs to consumers. The section begins with a discussion of what each player does and the role that it plays in the flow of pharmaceuticals from manufacturer to patient. The second section of the paper describes the financial relationships between each of these key players and how the dollars flow between and among the segments, including the consumer. Highlights from this paper about the key players and their financial relationships include: Pharmaceutical Manufacturers:

• A relatively few large, multinational firms comprise the bulk of the brand pharmaceutical manufacturing industry today – the 10 largest pharmaceutical corporations, as measured by U.S. sales, accounted for almost 60 percent of total U.S. sales in 2004.

• Pharmaceutical manufacturers have the most influence over pharmaceutical prices, assessing expected demand, future competition, and projected marketing costs to establish the wholesale acquisition cost (WAC), which is the baseline price at which wholesale distributors purchase drug products. Discounts and rebates may be applied, based on market share, volume, and prompt payment.

Wholesale Distributors:

• The wholesale distribution industry has consolidated in the last 30 years, with the number of wholesale distributors in the U.S. declining from approximately 200 in 1975 to fewer than 50 in 2000. The top 3 wholesale distributors account for almost 90 percent of the wholesale market.

• Wholesale distributors typically sell drugs to pharmacies at WAC plus some negotiated percentage. They may facilitate discounts negotiated between manufacturers and other customers.

Pharmacies:

• Although comprising a small overall percentage of total prescriptions filled (approximately 6.1 percent in 2004), mail-order pharmacy sales were the fastest-growing sector of the U.S. prescription drug retail market in 2004, increasing by 18 percent over the previous year.

NA. 21

• Pharmacies may negotiate with manufacturers or wholesalers for discounts and rebates based on volume sales or market share, and they may negotiate with PBMs for inclusion in their networks and for their reimbursement (drug cost plus dispensing fee).

Pharmacy Benefit Managers (PBMs):

• Approximately two-thirds of all prescriptions written in the U.S. are processed by a PBM.

• PBMs may achieve savings for their customers by negotiating discounts and through cost containment programs, including use of formularies and cost sharing.

The Appendix briefly describes: (A) special pricing rules applicable to Medicaid and some other federal programs, and (B) the roles physicians, large employers, and health plans have in the pharmaceutical supply chain. The pharmaceutical supply system is complex, and involves multiple organizations that play differing but sometimes overlapping roles in drug distribution and contracting. This complexity results in considerable price variability across different types of consumers, and the supply chain is not well understood by patients or policymakers. Increased understanding of these issues on the part of policymakers should assist in making rational policy decisions for the Medicare and Medicaid programs.

NA. 22

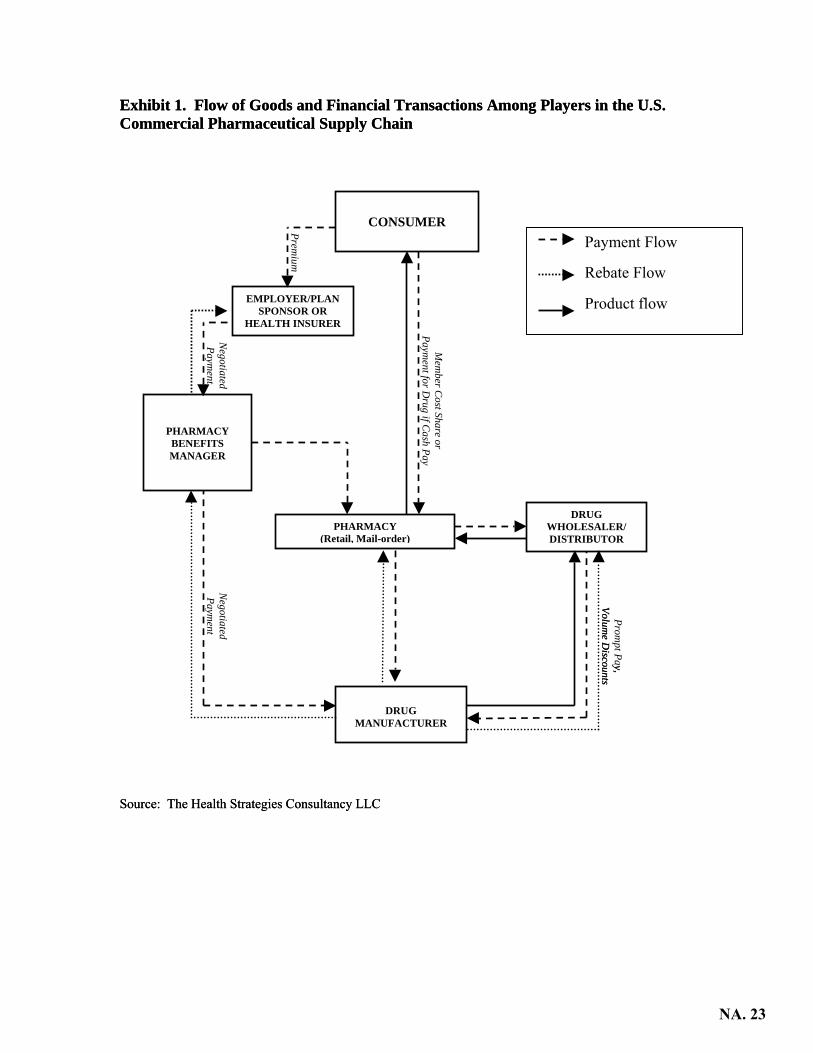

Exhibit 1. Flow of Goods and Financial Transactions Among Players in the U.S. Commercial Pharmaceutical Supply Chain Exhibit 1. Flow of Goods and Financial Transactions Among Players in the U.S. Commercial Pharmaceutical Supply Chain

Negotiated Paym

ent

Premium

Mem

ber Cost Share or

Payment for D

rug if Cash Pay

Negotiated Paym

ent

(

PHARMACY BENEFITS MANAGER

EMPLOYER/PLAN SPONSOR OR

HEALTH INSURER

DRUG WHOLESALER/ DISTRIBUTOR

CONSUMER Payment Flow

Rebate Flow

Product flow

Source: The Health Strategies ConsulSource: The Health Strategies Consul

PHARMACY Retail, Mail-order)

Prompt Pay,

Volume D

iscountsy,

Volume D

iscounts

DRUG

MANUFACTURER

tancy LLCtancy LLC

NA. 23

II. The Flow of Goods from Manufacturers to Consumers in the U.S. Pharmaceutical Supply Chain

Pharmaceutical Manufacturers

Manufacturers are the source of the prescription drugs in the pharmaceutical supply chain. The pharmaceutical manufacturing industry is composed of two distinct business models: manufacturers of brand-name drugs (e.g., Pfizer, Merck, and Novartis) and manufacturers of generic drugs (e.g., Mylan, Roxane, and Barr). There are a few pharmaceutical companies that participate in both the branded and generic parts of the industry, and both models focus on the manufacturing and packaging of pharmaceutical products, but there are other important differences. Most brand manufacturers devote a portion of their expenses to the scientific research and development of new drug therapies. Generic drug manufacturers typically do not develop new drug therapies, but instead manufacture generic compounds that compete directly with the original branded version of a drug once the brand product’s patent protection has expired. Manufacturers manage the actual distribution of drugs from manufacturing facilities to drug wholesalers, and in some cases, directly to retail pharmacy chains, mail-order and specialty pharmacies, hospital chains, and some health plans. Manufacturers may also distribute products directly to government purchasers, such as the Veterans Administration, AIDS Drug Assistance Programs (ADAPs), and Vaccines for Children (VFC), which typically receive the largest price discounts. In a few rare cases, a manufacturer may distribute drugs directly to a self-insured employer with an on-site pharmacy, but the typical employer-sponsored plan does not follow this path. Wholesale distributors are the manufacturers’ largest purchasers. Very few drugs are distributed directly to consumers. At the most basic economic level, a pharmaceutical manufacturer supplies a quantity of its products that is equal to the demand for its products from consumers/patients (of course, consumer demand in this market is expressed through the medium of a prescribing physician or other licensed health care provider). Manufacturers also play roles in stimulating demand for drug products through underwriting clinical studies designed to demonstrate the value proposition of pharmaceutical treatments compared to one another or compared to no clinical treatment at all; by engaging in the promotion and marketing of products to health care providers (including health plans and PBMs) and direct-to-consumer advertising; and by administering patient assistance programs that provide the firm’s products at nominal cost to low-income consumers. Manufacturers also play an important role in ensuring the safety of the pharmaceutical supply chain by producing informational labeling for prescribers and consumers that is consistent with the terms and conditions of a drug’s approval by the U.S. Food and Drug Administration (FDA), and by using electronic bar-coding technology on drug packaging that may be used to track individual production lots, and to prevent prescribing errors.

NA. 24

Overview of Pharmaceutical Manufacturing Industry Pharmaceutical manufacturing is a large global industry. In 2003, worldwide pharmaceutical industry sales totaled $491.8 billion, an increase in sales volume of 9 percent over the preceding year.1 The U.S. represents the largest single national market for pharmaceuticals, accounting for 44 percent of global industry sales in 2003, or a total of $216.4 billion, which was an increase of approximately 12 percent from the previous year’s figure.2

After a decade of significant mergers and acquisitions by drug companies, a relatively few large, multinational firms comprise the bulk of the brand pharmaceutical manufacturing industry today. The ten largest pharmaceutical corporations, as measured by U.S. sales, accounted for almost 60 percent of total U.S. sales in 2004: Exhibit 2. Top 10 Pharmaceutical Corporations by U.S. Sales, 2004

Rank Corporation U.S. Sales

($ Billions) % Growth Over

Previous Year % Market

Share 1 Pfizer $30.7 5 13.1 2 GlaxoSmithKline 18.8 1 8.0 3 Johnson & Johnson 16.2 7 6.9 4 Merck & Co. 15.0 8 6.4 5 AstraZeneca 11.3 12 4.8 6 Novartis 10.2 7 4.3 7 Sanofi-Aventis 10.0 13 4.3 8 Amgen 9.5 23 4.1 9 Bristol-Myers Squibb 9.2 -4 3.9

10 Wyeth 8.2 11 3.5 Total, Top 10 139.1 -- 59.3

Source: IMS Health, IMS National Sales Perspectives,TM February 2005, accessed 2/28/05 at http://www.imshealth.com/ims/portal/front/articleC/0,2777,6599_49695983_69891374,00.html

1IMS Health, “Bruised But Triumphant,” Medical Marketing and Media, May 2004, accessed at http://www.imshealth.com/vgn/images/portal/cit_40000873/23/12/55250930BruisedTriumphant081804.pdf 2IMS Health, “IMS Reports 11.5 Percent Dollar Growth in '03 U.S. Prescription Sales,” February 17, 2004, accessed at http://www.imshealth.com/ims/portal/front/articleC/0,2777,6599_3665_44771558,00.html. Prescription sales figures reported by IMS Health represent manufacturer prices.

NA. 25

When measured by prescription volume, the “top 10” list is similar but not identical, as a few generic drug manufacturers appear on the list: Exhibit 3. Top 10 Pharmaceutical Corporations by Total U.S. Dispensed Prescriptions, 2004

Rank Corporation U.S. Prescriptions

(Millions) % Growth Over

Previous Year % Market

Share 1 Pfizer 360.7 -4 10.2 2 Novartis 225.5 -2 6.4 3 Teva* 221.2 7 6.3 4 Mylan Labs* 215.2 4 6.1 5 Watson* 175.6 7 5.0 6 GlaxoSmithKline 138.8 -13 3.9 7 Merck & Co. 129.5 3 3.7 8 AstraZeneca 100.4 11 2.9 9 Johnson & Johnson 95.6 -9 2.7

10 Abbott 91.5 -4 2.6 Total, Top 10 1754.0. 49.8

* Generic drug manufacturers Source: IMS Health, National Prescription AuditTMPlus, January 2005, accessed 2/28/05 at http://www.imshealth.com/ims/portal/front/articleC/0,2777,6599_49695974_68913574,00.html Exhibit 4 provides a description of the generic pharmaceutical market: Exhibit 4. Top 10 Generic Manufacturers by Total Global Sales, 2003

Rank Corporation Global Sales($ Millions)

% Growth Over Previous Year

1 Sandoz $4,004.0 2 Teva Pharmaceutical Industries Limited 3,276.4 30.1 3 IVAX Corporation 1,420.3 18.6 4 Mylan Laboratories Inc. 1,269.2 15.0 5 Alpharma Inc. 1,297.3 4.8 6 Andrx Corporation 1,046.3 35.7 7 Barr Pharmaceuticals, Inc. 902.9 -24.1 8 Par Pharmaceutical Companies, Inc. 661.7 73.4 9 American Pharmaceutical Partners, Inc. 351.3 26.6

10 Eon Labs, Inc. 329.5 34.9 Source: Hoover’s, Inc. Hoover’s Online, accessed 1/03/2005. To convey the size of the pharmaceutical manufacturing industry from the perspective of individual products, the following tables present data on the biggest selling pharmaceutical products in the United States in 2004, measured by prescriptions dispensed and by sales in dollars. Exhibits 5 and 6 are for individual drug products, while Exhibits 7 and 8 are for broader therapeutic classes of drugs.

NA. 26

Exhibit 5. Top 10 Products by Total U.S. Dispensed Prescriptions, 2004 Rank Product Manufacturer Prescriptions

(Millions) % Growth

Over Previous Year

% Market Share

1 Lipitor Pfizer 74.8 9 2.1 2 HYCD/APAP Mallinckrodt 49.5 12 1.4 3 Synthroid Abbott 47.4 -5 1.3 4 Norvasc Pfizer 38.3 5 1.1 5 Toprol-XL AstraZeneca 35.0 18 1.0 6 Zoloft Pfizer 33.1 1 0.9 7 Zocor Merck 29.6 1 0.8 8 HYCD/APAP Watson 29.0 -2 0.8 9 Albuterol Warrick 26.8 0 0.8

10 Amoxicillin Teva 26.2 -5 0.7 Source: IMS Health, National Prescription AuditTMPlus, January 2005, accessed 2/28/05 at http://www.imshealth.com/ims/portal/front/articleC/0,2777,6599_49695974_68913594,00.html Exhibit 6. Top 10 Products by U.S. Sales, 2004

Rank Product Manufacturer U.S. Sales ($ Billions)

% Growth Over Previous

Year

% Market Share

1 Lipitor Pfizer $7.7 14 3.3 2 Zocor Merck 4.6 4 1.9 3 Prevacid TAP 3.8 -5 1.6 4 Nexium AstraZeneca 3.8 23 1.6 5 Procrit Ortho Biotech 3.2 -3 1.4 6 Zoloft Pfizer 3.1 8 1.3 7 Epogen Amgen 3.0 -4 1.3 8 Plavix Sanofi-Synthelabo 3.0 33 1.3 9 Advair Diskus GlaxoSmithKline 2.9 26 1.2

10 Zyprexa Eli Lilly 2.8 -10 1.2 Source: IMS Health, IMS National Sales Perspectives,TM February 2005, accessed 2-28-05 at http://www.imshealth.com/ims/portal/front/articleC/0,2777,6599_49695983_69890133,00.html Exhibit 7. Top 10 Therapeutic Classes by Total U.S. Dispensed Prescriptions, 2004

Rank Therapeutic Class Total Prescriptions

(Millions)

% Growth over Previous

Year

% Market Share

1 Codeine 157.6 5 4.5 2 SSRIs/SNRIs 147.4 4 4.2 3 ACE Inhibitors 143.8 5 4.1 4 HMG-COA Reductase Inhibitors (Statins) 139.8 11 4.0 5 Beta Blockers 120.6 7 3.4 6 Proton Pump Inhibitors 93.1 -2 2.6 7 Thyroid Hormone, Synthetic 90.0 6 2.6 8 Calcium Blockers 88.4 0 2.5 9 Seizure Disorders 84.8 7 2.4

10 Oral Contraceptives 82.5 -3 2.3 Source: IMS Health, National Prescription AuditTMPlus, January 2005, accessed 2/28/05 at http://www.imshealth.com/ims/portal/front/articleC/0,2777,6599_49695974_68914714,00.html

NA. 27

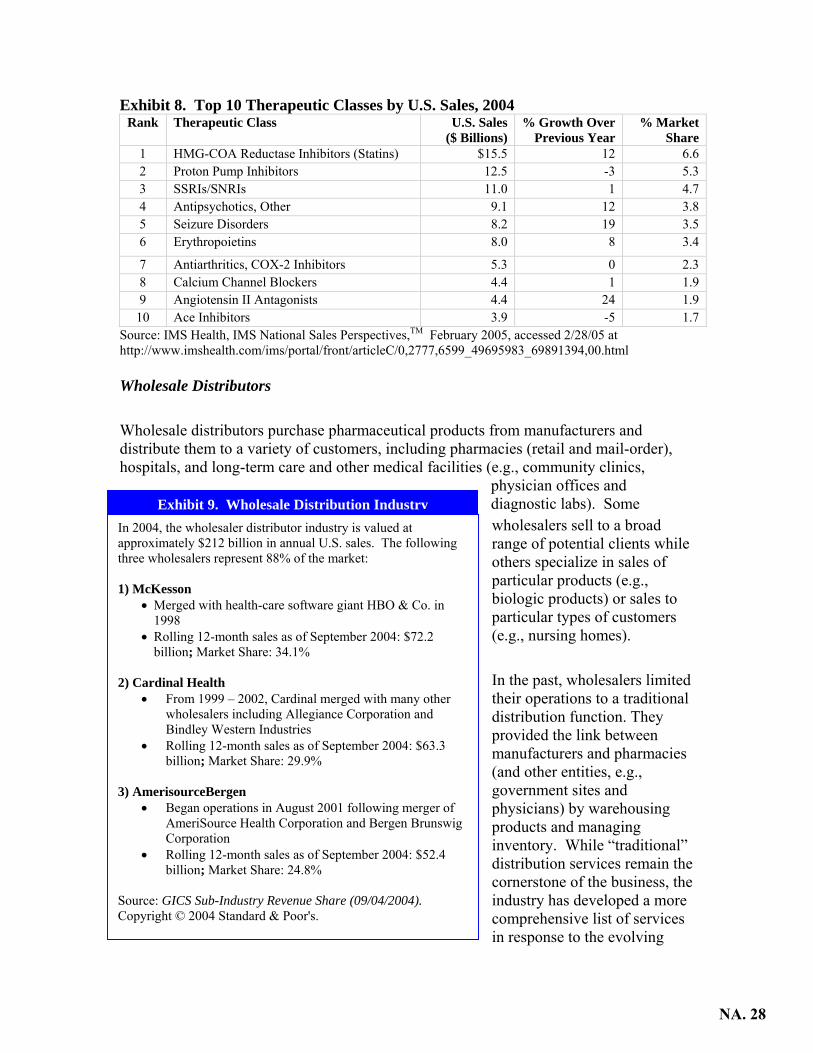

Exhibit 8. Top 10 Therapeutic Classes by U.S. Sales, 2004 Rank Therapeutic Class U.S. Sales

($ Billions) % Growth Over

Previous Year % Market

Share 1 HMG-COA Reductase Inhibitors (Statins) $15.5 12 6.6 2 Proton Pump Inhibitors 12.5 -3 5.3 3 SSRIs/SNRIs 11.0 1 4.7 4 Antipsychotics, Other 9.1 12 3.8 5 Seizure Disorders 8.2 19 3.5 6 Erythropoietins 8.0 8 3.4

7 Antiarthritics, COX-2 Inhibitors 5.3 0 2.3 8 Calcium Channel Blockers 4.4 1 1.9 9 Angiotensin II Antagonists 4.4 24 1.9

10 Ace Inhibitors 3.9 -5 1.7 Source: IMS Health, IMS National Sales Perspectives,TM February 2005, accessed 2/28/05 at http://www.imshealth.com/ims/portal/front/articleC/0,2777,6599_49695983_69891394,00.html Wholesale Distributors

Wholesale distributors purchase pharmaceutical products from manufacturers and distribute them to a variety of customers, including pharmacies (retail and mail-order), hospitals, and long-term care and other medical facilities (e.g., community clinics,

physician offices and diagnostic labs). Some wholesalers sell to a broad range of potential clients while others specialize in sales of particular products (e.g., biologic products) or sales to particular types of customers (e.g., nursing homes).

In the past, wholesalers limited their operations to a traditional distribution function. They provided the link between manufacturers and pharmacies (and other entities, e.g., government sites and physicians) by warehousing products and managing inventory. While “traditional” distribution services remain the cornerstone of the business, the industry has developed a more comprehensive list of services

In 2004, the wholesaler distributor industry is valued at approximately $212 billion in annual U.S. sales. The following three wholesalers represent 88% of the market: 1) McKesson

• Merged with health-care software giant HBO & Co. in 1998

• Rolling 12-month sales as of September 2004: $72.2 billion; Market Share: 34.1%

2) Cardinal Health

• From 1999 – 2002, Cardinal merged with many other wholesalers including Allegiance Corporation and Bindley Western Industries

• Rolling 12-month sales as of September 2004: $63.3 billion; Market Share: 29.9%

3) AmerisourceBergen

• Began operations in August 2001 following merger of AmeriSource Health Corporation and Bergen Brunswig Corporation

• Rolling 12-month sales as of September 2004: $52.4 billion; Market Share: 24.8%

Source: GICS Sub-Industry Revenue Share (09/04/2004). Copyright © 2004 Standard & Poor's.

Exhibit 9. Wholesale Distribution Industry

in response to the evolving

NA. 28

marketplace. Today, wholesale distributors provide a number of specialized services, including specialty drug distribution, drug repackaging, electronic order services, reimbursement support, and drug buy-back programs.3

The wholesale distribution industry has gone through significant change and consolidation in the last 30 years, due in part to the increasing pressures to lower costs. Between 1975 and 2000, the number of wholesale distributors in the U.S. declined from approximately 200 to fewer than 50.4 The top three wholesale distributors, McKesson, Cardinal Health, and Amerisource-Bergen, account for almost 90 percent of the entire wholesale drug market.5

This consolidation has forced the industry to change its revenue model, evolving its core distribution business into a low-margin enterprise that makes money by maximizing economies of scale, creating physical efficiencies in the distribution system (such as “just-in-time” deliveries to customers), and realizing financial efficiencies (such as retaining discounts for prompt payment). The industry has also extended and augmented its business model by moving into specialty pharmacy and disease management services.