north america oil & gas exploration & production · exploration & production sixth...

TRANSCRIPT

See Disclosure Appendix of this report for important Disclosures and Analyst Certifications

North America Oil & Gas Exploration & ProductionSixth Joint IEA-IEF-OPEC Workshop on the Interactions between Physical

and Financial Energy Markets

Developments in Oil Market Financing

Bob Brackett, Ph.D. • Senior Analyst • +1-212-756-4656 • [email protected]

Andrew Pizzi • Senior Research Associate • +1-212-407-5813 • [email protected]

Zhenhao Li • Research Associate • +1-212-756-4007• [email protected]

March 16th, 2018

NORTH AMERICAN OIL & GAS EXPLORATION/PRODUCTION | 2

North American Oil & Gas Exploration & Production team

Bob Brackett, Ph.D. (Senior Analyst)

Bob Brackett is the Senior Research Analyst covering North American Oil & Gas Exploration & Production. He is currently recognized as All-American

#1 by Institutional Investor (for the 5th year in a row) and #1 by Greenwich buy-side surveys. Previously, Bob was Director of E&P Planning and also

Director of Corporate Strategy for Hess Corporation. Before Hess, Bob was an Engagement Manager with McKinsey & Company's Petroleum

Practice, serving the majority of the world’s largest oil companies across five continents and 30 countries throughout the petroleum value chain. Bob

began his career with ExxonMobil, spending eight years in positions in Exploration, Business Development, Development and Research. As a NASA

Space Grant Fellow, Bob received his PhD in Earth & Planetary Sciences from Washington University – St. Louis. He received his MBA from Rice

University in Houston. He also holds a BS in Geophysics and a BA in Astronomy from the University of Texas.

Andrew Pizzi (Senior Associate)

Andrew Pizzi is the Senior Research Associate on the North American Oil and Gas Exploration & Production team. Previously, Andrew was the Senior

Market Analyst at Bloom Energy, a manufacturer of natural gas generators based on fuel cell technology. Prior to Bloom Energy, Andrew spent four

years with NERA Economic Consulting analyzing oil, gas, and power markets and regulation. Andrew received an MBA from Wharton and holds a

Bachelor’s degree in Economics from Williams College.

Zhenhao Li (Associate)

Zhenhao (Zen) Li is the Research Associate on the North American Oil and Gas Exploration & Production and Natural Gas & MLPs team. Previously,

Zhenhao has interned at UBS’ investment banking division in their industrials team and at KKR in their internal auditing team. He holds a Bachelor’s

degree in Economics with concentrations in Finance and Accounting from the Wharton School.

NORTH AMERICAN OIL & GAS EXPLORATION/PRODUCTION | 3

Key points

Developments in oil market financingQuick answer – E&Ps don’t need it.

How do E&Ps think about fundingCash in ~ cash out (except when greedy or scared)

Goldilocks example – E&Ps at top / bottom / mid cycle

How E&Ps won the shale war

What do E&Ps do with fundingE&P mentality towards balance sheet

Role of de-levering

Capex takes lion’s share

Why the “predator prey” model is so importantoil production is a function of price

today’s price means too much production

Lotka-Volterra equation

How to stop the shale “predators”Financing, fiscal terms, inflation, dis-efficiencies, lack of inventory, … or culling

“Culling” – a collapse in oil price – has a strong negative nonlinear reaction – reduces supply & CFO & future growth

NORTH AMERICAN OIL & GAS EXPLORATION/PRODUCTION | 4

Shale Era Business Model: Cash In ~ Cash Out (except when greedy or scared…)

E&P Sector CFO compared to “organic” capex (capital spent drilling & completing existing acreage) i.e., productive capex

Source: Company Data, Bernstein estimates, Bloomberg

-

10

20

30

40

50

601

Q0

42

Q0

43

Q0

44

Q0

41

Q0

52

Q0

53

Q0

54

Q0

51

Q0

62

Q0

63

Q0

64

Q0

61

Q0

72

Q0

73

Q0

74

Q0

71

Q0

82

Q0

83

Q0

84

Q0

81

Q0

92

Q0

93

Q0

94

Q0

91

Q1

02

Q1

03

Q1

04

Q1

01

Q1

12

Q1

13

Q1

14

Q1

11

Q1

22

Q1

23

Q1

24

Q1

21

Q1

32

Q1

33

Q1

34

Q1

31

Q1

42

Q1

43

Q1

44

Q1

41

Q1

52

Q1

53

Q1

54

Q1

51

Q1

62

Q1

63

Q1

64

Q1

61

Q1

72

Q1

73

Q1

7

$/

bo

e

Organic Capex$/boe (left axis) Cashflow From Operations,$/boe (left axis)

Eagle Ford breaks 0.1 mln bopd

NORTH AMERICAN OIL & GAS EXPLORATION/PRODUCTION | 5

Top of cycle… $103 oil and $4.5 gas…too good a business

68

58

37

19

11

32

32

10

-

14

2 2 3

17

2 6

-

17 3

7

-

10

20

30

40

50

60

70

80E

xp. R

eve

nu

e

Re

aliz

atio

n S

pre

ads

Re

po

rted

Re

ven

ue

Pro

d. C

ost

s

Pro

d. T

axe

s

Exp

lora

tio

n E

xp.

SG

&A

EB

ITD

A

DD

&A

EB

IT

Inte

rest

Fin

an

cia

l Ta

x

Cle

an N

et

Inc

om

e

DD

&A

Oth

er

CF

Op

era

tio

ns

Org

an

ic a

nd

…

$ p

er

bo

e

E&P overview: 2Q14

Source: Company Data, Bernstein estimates, Bloomberg

NORTH AMERICAN OIL & GAS EXPLORATION/PRODUCTION | 6

Bottom of cycle… $35 oil and $2 gas…casualty of the shale war

24

21

7

(6)

(8)

4

12

3 10

1 1 2

13

2 0

13

(2)

2

(10)

(5)

-

5

10

15

20

25

30E

xp. R

eve

nu

e

Re

aliz

atio

n S

pre

ads

Re

po

rted

Re

ven

ue

Pro

d. C

ost

s

Pro

d. T

axe

s

Exp

lora

tio

n E

xp.

SG

&A

EB

ITD

A

DD

&A

EB

IT

Inte

rest

Fin

an

cia

l Ta

x

Cle

an N

et

Inc

om

e

DD

&A

Oth

er

CF

Op

era

tio

ns

Cap

ex

$ p

er

bo

e

E&P overview: 1Q16

Source: Company Data, Bernstein estimates, Bloomberg

NORTH AMERICAN OIL & GAS EXPLORATION/PRODUCTION | 7

36

31

16

4

1

14

15

4

11

1 1

2 12

2 1

12 2

2

-

5

10

15

20

25

30

35

40E

xp. R

eve

nu

e

Re

aliz

atio

n S

pre

ads

Re

po

rted

Re

ven

ue

Pro

d. C

ost

s

Pro

d. T

axe

s

Exp

lora

tio

n E

xp.

SG

&A

EB

ITD

A

DD

&A

EB

IT

Inte

rest

Fin

an

cia

l Ta

x

Cle

an N

et

Inc

om

e

DD

&A

Oth

er

CF

Op

era

tio

ns

Org

an

ic a

nd

…

$ p

er

bo

e

E&P overview: 3Q17

3Q17 - $50 oil & $3 gas…from scheme to (poor) business

Source: Company Data, Bernstein estimates, Bloomberg

NORTH AMERICAN OIL & GAS EXPLORATION/PRODUCTION | 8

How E&Ps won the shale war…

...same way we won the revolutionary war…with help

Source: Corporate reports, Bloomberg, L.P., Bernstein analysis

0

50

100

150

200

250

Jan

-15

Jan

-15

Fe

b-1

5

Mar

-15

Mar

-15

Ap

r-1

5

May

-15

May

-15

Jun

-15

Jul-

15

Jul-

15

Au

g-1

5

Se

p-1

5

Oct

-15

Oct

-15

No

v-1

5

De

c-1

5

De

c-1

5

Jan

-16

Fe

b-1

6

Fe

b-1

6

Mar

-16

Ap

r-1

6

Ap

r-1

6

May

-16

Jun

-16

Jun

-16

Jul-

16

Au

g-1

6

Se

p-1

6

Se

p-1

6

Oct

-16

No

v-1

6

No

v-1

6

De

c-1

6

US

$, b

illio

n

Cumulative Cash flow statement, 1Q 2015 to 4Q 2016

Operating Cash Other Sources Cash burn Debt (Net) Asset Sales

Equity (Net) Organic Capex Plus Dividend Plus Acquisitons

“war onshale”OPEC

meeting

“oil cut”OPEC

meeting

NORTH AMERICAN OIL & GAS EXPLORATION/PRODUCTION | 9

-$5

$0

$5

$10

$15

$20

$25C

FO

Div

ide

nd

s

Cap

ex

Ac

qu

isit

ion

s

Sal

es

De

bt

Eq

uit

y

Oth

er

∆ C

ash

E&P Sources & Uses of Cash: 3Q 2017 ($ billion)

E&P mentality today – CFO covers capex & dividends; rest of balance sheet balances

Source: Company Data, Bernstein estimates, Bloomberg

NORTH AMERICAN OIL & GAS EXPLORATION/PRODUCTION | 10

20%

25%

30%

35%

40%

45%

1Q

04

2Q

04

3Q

04

4Q

04

1Q

05

2Q

05

3Q

05

4Q

05

1Q

06

2Q

06

3Q

06

4Q

06

1Q

07

2Q

07

3Q

07

4Q

07

1Q

08

2Q

08

3Q

08

4Q

08

1Q

09

2Q

09

3Q

09

4Q

09

1Q

10

2Q

10

3Q

10

4Q

10

1Q

11

2Q

11

3Q

11

4Q

11

1Q

12

2Q

12

3Q

12

4Q

12

1Q

13

2Q

13

3Q

13

4Q

13

1Q

14

2Q

14

3Q

14

4Q

14

1Q

15

2Q

15

3Q

15

4Q

15

1Q

16

2Q

16

3Q

16

4Q

16

1Q

17

2Q

17

3Q

17

Debt to Total Cap % (left axis)

E&Ps are de-levering but still debt is too high versus history

Source: Company Data, Bernstein estimates, Bloomberg

Eagle Ford breaks 0.1 mln bopd

E&Ps used high oil price

to de-lever

De-levering

likely from CFO and asset sales…not

equity!

NORTH AMERICAN OIL & GAS EXPLORATION/PRODUCTION | 11Source: Company Data, Bernstein estimates, Bloomberg

-

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

4,500,000

5,000,000

Shale Contribution by Quarter (bopd)

Q1 2010 Q2 2010 Q3 2010 Q4 2010 Q1 2011 Q2 2011 Q3 2011 Q4 2011 Q1 2012 Q2 2012 Q3 2012

Q4 2012 Q1 2013 Q2 2013 Q3 2013 Q4 2013 Q1 2014 Q2 2014 Q3 2014 Q4 2014 Q1 2015 Q2 2015

Q3 2015 Q4 2015 Q1 2016 Q2 2016 Q3 2016 Q4 2016 Q1 2017 Q2 2017 Q3 2017

Lion’s share of CFO goes to capex…

NORTH AMERICAN OIL & GAS EXPLORATION/PRODUCTION | 12

Oil production is a function of price…

Source: HPDI, EIA; Baker Hughes, Bernstein analysis and estimates

6,000

8,000

10,000

12,000

14,000

16,000

18,000

Jan

-14

Ap

r-1

4

Jul-

14

Oc

t-1

4

Jan

-15

Ap

r-1

5

Jul-

15

Oc

t-1

5

Jan

-16

Ap

r-1

6

Jul-

16

Oc

t-1

6

Jan

-17

Ap

r-1

7

Jul-

17

Oc

t-1

7

Jan

-18

Ap

r-1

8

Jul-

18

Oc

t-1

8

Jan

-19

Ap

r-1

9

Jul-

19

Oc

t-1

9

Jan

-20

Ap

r-2

0

Jul-

20

Oc

t-2

0

kb

bld

U S Oil Production

$30 $40 $50 $60 $70 SCB

Growth dominated by (a) financing, (b) inflation, and (c) efficiencies

NORTH AMERICAN OIL & GAS EXPLORATION/PRODUCTION | 13Source: Company Data, Bernstein estimates, Bloomberg

0

10

20

30

40

50

60

0

24

48

72

96

12

0

14

4

16

8

19

2

21

6

24

0

26

4

28

8

31

2

33

6

36

0

38

4

40

8

43

2

45

6

48

0

50

4

52

8

55

2

57

6

60

0

62

4

64

8

67

2

69

6

72

0

74

4

76

8

79

2

81

6

84

0

86

4

88

8

91

2

93

6

96

0

98

4

Predator-Prey Model (Lotka-Volterra)

Rabbits (in thousands) Foxes (in thousands)

Lotka-Volterra (1st order nonlinear differential equations describing biologic systems)

NORTH AMERICAN OIL & GAS EXPLORATION/PRODUCTION | 14

0

10

20

30

40

50

60

0

24

48

72

96

12

0

14

4

16

8

19

2

21

6

24

0

26

4

28

8

31

2

33

6

36

0

38

4

40

8

43

2

45

6

48

0

50

4

52

8

55

2

57

6

60

0

62

4

64

8

67

2

69

6

72

0

74

4

76

8

79

2

81

6

84

0

86

4

88

8

91

2

93

6

96

0

98

4

Predator-Prey Model (Lotka-Volterra)

Cash Flow Shale Production

Shale is not a thermostat – it induces waves (and needs culling!)

...”equilibrium price” is lower than where we are today

NORTH AMERICAN OIL & GAS EXPLORATION/PRODUCTION | 15

How to stop the shale “predators”

FinancingInvestor-imposed financial discipline appears to be coming

Fiscal termsU.S. tax reform a modest net positive

Inflationruns at about ½ the beta of the commodity price…dampens impacts a bit

Dis-efficienciesnot any time soon

Lack of inventorynot any time soon

Cullingcoming soon?

NORTH AMERICAN OIL & GAS EXPLORATION/PRODUCTION | 16Source: Company Data, Bernstein estimates, Bloomberg

$(2)

$(4)

$3

$(2)

$1 $(1)

$1 $(1)

$(2)

$2 $(2)

$3

$13

$3

$1 $2

$12

$7

$11

$7

$3 $2

$(3)

$(1)

$(2)

$(6)

$(4)

$(2)

$-

$2

$4

$6

$8

$10

$12

$14

1Q

12

2Q

12

3Q

12

4Q

12

1Q

13

2Q

13

3Q

13

4Q

13

1Q

14

2Q

14

3Q

14

4Q

14

1Q

15

2Q

15

3Q

15

4Q

15

1Q

16

2Q

16

3Q

16

4Q

16

1Q

17

2Q

17

3Q

17

4Q

17

1Q

18

Net Equity (+) Issuance / (-) Repurchases ($bln) Share Repurchase Announced ($bln)

How to stop shale "predators"? Financial discipline…but need a lot!

NORTH AMERICAN OIL & GAS EXPLORATION/PRODUCTION | 17

Tax reform impact on E&Ps unlikely to help – overall a mild to medium positive

Source: Company Data, Bernstein estimates

Policy Change Positive or Negative

Impact Relative to

S&P Comments

Change in Corporate Tax Rate LowThe corporate tax rate was reduced from 35% to 21%. E&Ps benefit far

less than other sectors due to their very low cash tax burden.

Repeal of Corporate AMT Med-High

E&Ps can deduct a large proportion of their (also large) capital budgets

every year through intangible drilling credits - and now 100% bonus

depreciation. This frequently led to minimal tax bills under the tax code

and the imposition of the Corporate AMT. Repeal of the AMT will

immediately benefit companies with significant AMT credits (EOG, COG,

SWN) and those that might have otherwise faced AMT in the future

(many others). Tax credits are refunded on a 50%, 25%, 12.5%,12.5%

schedule over the next 4 years.

Bonus Depreciation Med-Low

E&Ps already deduct ~70% of well cost in year 1 through IDCs, but E&P

is a capital intensive sector and bonus depreciation will be helpful on the

~30% of the capital budget not already eligible to be deducted.

Foreign Earnings Changes Medium

Accumulated foreign earnings are repatriated at 8% (profits) or 15.5%

(cash). This will create a one-time tax hit for firms with profitable foreign

operations. However, going forward, foreign earnings from upstream

operations will only be taxed locally.

Interest Deduction Limitation Low

E&Ps with high leverage could run into the interest deduction limitation

(30% of adjusted taxable income), but are unlikely to present a large

taxable income base in any event due to the deductibility of their capital

spending.

NOL Changes Low

Net Operating Losses can only offset 80% of taxable income, can't be

carried backward, but can be carried forward indefinitely. This will tend

to extend the period over which NOLs get used to offset tax bills. E&Ps

produce lots of NOLs but already have a low cash tax burden which

makes the loss of these NOL provisions less impactful.

NORTH AMERICAN OIL & GAS EXPLORATION/PRODUCTION | 18

83.8

2%

1.6

3%

2.7 50%

39.0

127.1

0

20

40

60

80

100

120

140

160

180

2014 Due to Lateral

Length From 9,263'

to 9,441'

Due to Sand Per Foot

From 719 lb/ft to

824

Due to Other Effects 2017

1s

t 1

2 m

on

ths

cum

ula

tive

oil

(kb

o)

Bakken

Source: DIDestop, FracFocus, Bernstein analysis and estimates

73.4

29%

21.2

41%

38.96%

8.7

142.3

0

20

40

60

80

100

120

140

160

180

2014 Due to Lateral

Length From 4,433'

to 5,715'

Due to Sand Per

Foot From 785 lb/ft

to 2,331

Due to Other Effects 2017

1s

t 1

2 m

on

ths

cum

ula

tive

oil

(kb

o)

Delaware

1

(211)

2

(276)

3

(342)

4

(381)

5

(418)

6

(491)

7

(569)

8

(685)

9

(887)

10

(1,707)

y = 32.379ln(x) - 74.774

R² = 0.8371

80

100

120

140

160

180

200

0 200 400 600 800 1,000 1,200 1,400 1,600 1,800

12

-mo

cum

ula

tive

pro

duc

tion

(kb

oe)

San d (lb/ft)

Bakken Sand vs Cumulative Production

1

(519)

2

(897)

3

(1,129)

4

(1,247)

5

(1,324)

6

(1,402) 7

(1,511)

8

(1,673)

9

(1,973) 10

(2,691)

y = 45.938ln(x) - 184.58

R² = 0.6759

80

100

120

140

160

180

200

0 500 1,000 1,500 2,000 2,500 3,000 3,500

12

-mo

cum

ula

tive

pro

duc

tion

(kb

oe)

San d (lb/ft)

D elaware Sand vs. Cumulative Production

Productivity has increased in the Delaware largely due to lateral length and sand/ft increases but at diminishing rates

Productivity increases in the Bakken were nearly independent of lateral length and sand/ft increases – we suspect improvements from high-grading or geology

Efficiencies are decelerating (but not worsening!)

Correlation between proppant use and productivity – points represent the decile of sand usage

NORTH AMERICAN OIL & GAS EXPLORATION/PRODUCTION | 19

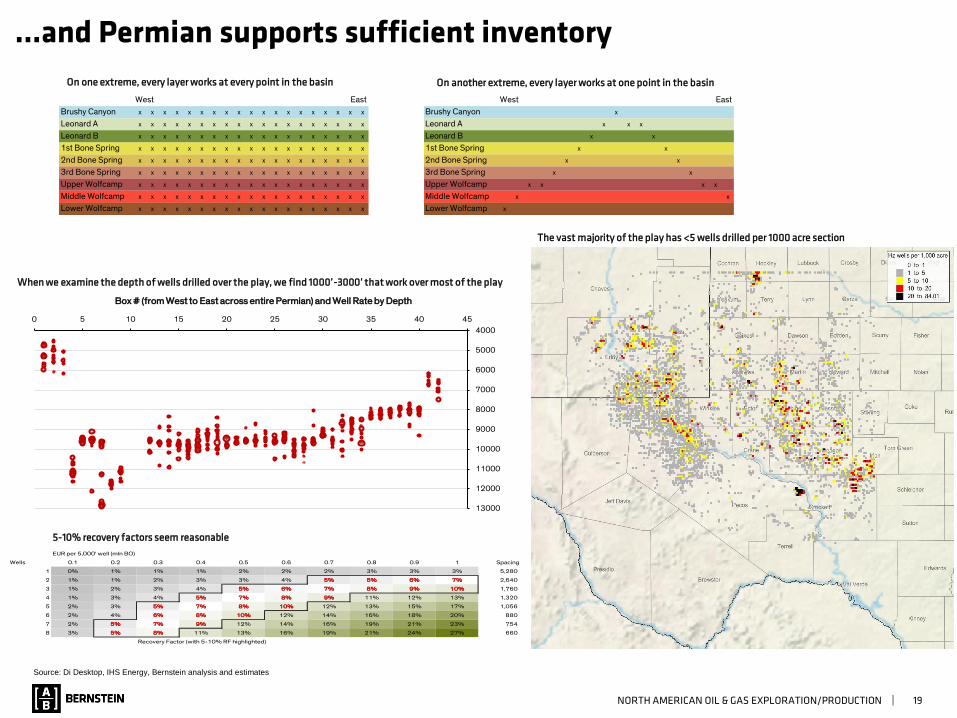

…and Permian supports sufficient inventory

Source: Di Desktop, IHS Energy, Bernstein analysis and estimates

4000

5000

6000

7000

8000

9000

10000

11000

12000

13000

0 5 10 15 20 25 30 35 40 45

Box # (from West to East across entire Permian) and Well Rate by Depth

EUR per 5,000' well (mln BO)

Wells 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 1 Spacing

1 0% 1% 1% 1% 2% 2% 2% 3% 3% 3% 5,280

2 1% 1% 2% 3% 3% 4% 5% 5% 6% 7% 2,640

3 1% 2% 3% 4% 5% 6% 7% 8% 9% 10% 1,760

4 1% 3% 4% 5% 7% 8% 9% 11% 12% 13% 1,320

5 2% 3% 5% 7% 8% 10% 12% 13% 15% 17% 1,056

6 2% 4% 6% 8% 10% 12% 14% 16% 18% 20% 880

7 2% 5% 7% 9% 12% 14% 16% 19% 21% 23% 754

8 3% 5% 8% 11% 13% 16% 19% 21% 24% 27% 660

Recovery Factor (with 5-10% RF highlighted)

West East

Brushy Canyon x x x x x x x x x x x x x x x x x x x

Leonard A x x x x x x x x x x x x x x x x x x x

Leonard B x x x x x x x x x x x x x x x x x x x

1st Bone Spring x x x x x x x x x x x x x x x x x x x

2nd Bone Spring x x x x x x x x x x x x x x x x x x x

3rd Bone Spring x x x x x x x x x x x x x x x x x x x

Upper Wolfcamp x x x x x x x x x x x x x x x x x x x

Middle Wolfcamp x x x x x x x x x x x x x x x x x x x

Lower Wolfcamp x x x x x x x x x x x x x x x x x x x

West East

Brushy Canyon x

Leonard A x x x

Leonard B x x

1st Bone Spring x x

2nd Bone Spring x x

3rd Bone Spring x x

Upper Wolfcamp x x x x

Middle Wolfcamp x x

Lower Wolfcamp x

On one extreme, every layer works at every point in the basin On another extreme, every layer works at one point in the basin

When we examine the depth of wells drilled over the play, we find 1000’-3000’ that work over most of the play

The vast majority of the play has <5 wells drilled per 1000 acre section

5-10% recovery factors seem reasonable

NORTH AMERICAN OIL & GAS EXPLORATION/PRODUCTION | 20

Key points

Developments in oil market financingQuick answer – E&Ps don’t need it.

How do E&Ps think about fundingCash in ~ cash out (except when greedy or scared)

Goldilocks example – E&Ps at top / bottom / mid cycle

How E&Ps won the shale war

What do E&Ps do with fundingE&P mentality towards balance sheet

Role of de-levering

Capex takes lion’s share

Why the “predator prey” model is so importantoil production is a function of price

today’s price means too much production

Lotka-Volterra equation

How to stop the shale “predators”Financing, fiscal terms, inflation, dis-efficiencies, lack of inventory, … or culling

“Culling” – a collapse in oil price – has a strong negative nonlinear reaction – reduces supply & CFO & future growth

NORTH AMERICAN OIL & GAS EXPLORATION/PRODUCTION | 21

Disclosure Appendix

NORTH AMERICAN OIL & GAS EXPLORATION/PRODUCTION | 22

SRO REQUIRED DISCLOSURES

• References to "Bernstein" relate to Sanford C. Bernstein & Co., LLC, Sanford C. Bernstein Limited, Sanford C. Bernstein (Hong Kong) Limited 盛博香港有限公司, Sanford C. Bernstein

(Canada) Limited, and Sanford C. Bernstein (business registration number 53193989L), a unit of AllianceBernstein (Singapore) Ltd. which is a licensed entity under the Securities and

Futures Act and registered with Company Registration No. 199703364C, collectively.

• Bernstein analysts are compensated based on aggregate contributions to the research franchise as measured by account penetration, productivity and proactivity of investment ideas. No

analysts are compensated based on performance in, or contributions to, generating investment banking revenues.

• Bernstein rates stocks based on forecasts of relative performance for the next 6-12 months versus the S&P 500 for stocks listed on the U.S. and Canadian exchanges, versus the MSCI

Pan Europe Index for stocks listed on the European exchanges (except for Russian companies), versus the MSCI Emerging Markets Index for Russian companies and stocks listed on

emerging markets exchanges outside of the Asia Pacific region, and versus the MSCI Asia Pacific ex-Japan Index for stocks listed on the Asian (ex-Japan) exchanges - unless otherwise

specified. We have three categories of ratings:

Outperform: Stock will outpace the market index by more than 15 pp in the year ahead.

Market-Perform: Stock will perform in line with the market index to within +/-15 pp in the year ahead.

Underperform: Stock will trail the performance of the market index by more than 15 pp in the year ahead.

Not Rated: The stock Rating, Target Price and/or estimates (if any) have been suspended temporarily.

• As of 03/06/2018, Bernstein's ratings were distributed as follows: Outperform - 48.9% (0.0% banking clients) ; Market-Perform - 39.3% (0.0% banking clients); Underperform - 11.9% (0.0%

banking clients); Not Rated - 0.0% (0.0% banking clients). The numbers in parentheses represent the percentage of companies in each category to whom Bernstein provided investment

banking services within the last twelve (12) months.

OTHER DISCLOSURES

A price movement of a security which may be temporary will not necessarily trigger a recommendation change. Bernstein will advise as and when coverage of securities commences and ceases.

Bernstein has no policy or standard as to the frequency of any updates or changes to its coverage policies. Although the definition and application of these methods are based on generally

accepted industry practices and models, please note that there is a range of reasonable variations within these models. The application of models typically depends on forecasts of a range of

economic variables, which may include, but are not limited to, interest rates, exchange rates, earnings, cash flows and risk factors that are subject to uncertainty and also may change over time.

Any valuation is dependent upon the subjective opinion of the analysts carrying out this valuation.

Bernstein produces a number of different types of research product including, among others, fundamental analysis and quantitative analysis. Recommendations contained within one type of

research product may differ from recommendations contained within other types of research product, whether as a result of differing time horizons, methodologies or otherwise.

This document may not be passed on to any person in the United Kingdom (i) who is a retail client (ii) unless that person or entity qualifies as an authorised person or exempt person within the

meaning of section 19 of the UK Financial Services and Markets Act 2000 (the "Act"), or qualifies as a person to whom the financial promotion restriction imposed by the Act does not apply by

virtue of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005, or is a person classified as an "professional client" for the purposes of the Conduct of Business Rules of

the Financial Conduct Authority.

This document may not be passed onto any person in Canada unless that person qualifies as "permitted client" as defined in Section 1.1 of NI 31-103.

To our readers in the United States: Sanford C. Bernstein & Co., LLC is distributing this publication in the United States and accepts responsibility for its contents. Any U.S. person receiving this

publication and wishing to effect securities transactions in any security discussed herein should do so only through Sanford C. Bernstein & Co., LLC.

To our readers in the United Kingdom: This publication has been issued or approved for issue in the United Kingdom by Sanford C. Bernstein Limited, authorised and regulated by the Financial

Conduct Authority and located at 50 Berkeley Street, London W1J 8SB, +44 (0)20-7170-5000.

To our readers in member states of the EEA: This publication is being distributed in the EEA by Sanford C. Bernstein Limited, which is authorised and regulated in the United Kingdom by the

Financial Conduct Authority and holds a passport under the Markets in Financial Instruments Directive.

To our readers in Hong Kong: This publication is being distributed in Hong Kong by Sanford C. Bernstein (Hong Kong) Limited 盛博香港有限公司, which is licensed and regulated by the Hong

NORTH AMERICAN OIL & GAS EXPLORATION/PRODUCTION | 23

Kong Securities and Futures Commission (Central Entity No. AXC846). This publication is solely for professional investors only, as defined in the Securities and Futures Ordinance (Cap. 571).

To our readers in Singapore: This publication is being distributed in Singapore by Sanford C. Bernstein, a unit of AllianceBernstein (Singapore) Ltd., only to accredited investors or institutional

investors, as defined in the Securities and Futures Act (Chapter 289). Recipients in Singapore should contact AllianceBernstein (Singapore) Ltd. in respect of matters arising from, or in connection

with, this publication. AllianceBernstein (Singapore) Ltd. is a licensed entity under the Securities and Futures Act and registered with Company Registration No. 199703364C. It is regulated by the

Monetary Authority of Singapore and located at One Raffles Quay, #27-11 South Tower, Singapore 048583, +65-62304600. The business name "Bernstein" is registered under business

registration number 53193989L.

To our readers in the People’s Republic of China: The securities referred to in this document are not being offered or sold and may not be offered or sold, directly or indirectly, in the People's

Republic of China (for such purposes, not including the Hong Kong and Macau Special Administrative Regions or Taiwan), except as permitted by the securities laws of the People’s Republic of

China.

To our readers in Japan: This document is not delivered to you for marketing purposes, and any information provided herein should not be construed as a recommendation, solicitation or offer to

buy or sell any securities or related financial products.

For the institutional client readers in Japan who have been granted access to the Bernstein website by Daiwa Securities Group Inc. (“Daiwa”), your access to this document should not be

construed as meaning that Sanford C. Bernstein is providing you with investment advice for any purposes. Whilst Sanford C. Bernstein has prepared this document, your relationship is, and will

remain with, Daiwa, and Sanford C. Bernstein has neither any contractual relationship with you nor any obligations towards you.

To our readers in Australia: Sanford C. Bernstein & Co., LLC, Sanford C. Bernstein Limited and Sanford C. Bernstein (Hong Kong) Limited 盛博香港有限公司 are exempt from the requirement to

hold an Australian financial services licence under the Corporations Act 2001 in respect of the provision of the following financial services to wholesale clients:

• providing financial product advice;

• dealing in a financial product;

• making a market for a financial product; and

• providing a custodial or depository service.

To our readers in Canada: If this publication is pertaining to a Canadian domiciled company, it is being distributed in Canada by Sanford C. Bernstein (Canada) Limited, which is licensed and

regulated by the Investment Industry Regulatory Organization of Canada ("IIROC"). If the publication is pertaining to a non-Canadian domiciled company, it is being distributed by Sanford C.

Bernstein & Co., LLC, which is licensed and regulated by both the U.S. Securities and Exchange Commission and the Financial Industry Regulatory Authority ("FINRA") into Canada under the

International Dealers Exemption. This publication may not be passed onto any person in Canada unless that person qualifies as a "Permitted Client" as defined in Section 1.1 of NI 31-103.

Sanford C. Bernstein & Co., LLC., Sanford C. Bernstein Limited, Sanford C. Bernstein (Hong Kong) Limited 盛博香港有限公司, Sanford C. Bernstein (Canada) Limited and AllianceBernstein

(Singapore) Ltd. are regulated by, respectively, the Securities and Exchange Commission under U.S. laws, by the Financial Conduct Authority under U.K. laws, by the Hong Kong Securities and

Futures Commission under Hong Kong laws, by the Investment Industry Regulatory Organization of Canada and by the Monetary Authority of Singapore under Singapore laws, all of which differ

from Australian laws.

One or more of the officers, directors, or employees of Sanford C. Bernstein & Co., LLC, Sanford C. Bernstein Limited, Sanford C. Bernstein (Hong Kong) Limited 盛博香港有限公司, Sanford C.

Bernstein (Canada) Limited, Sanford C. Bernstein (business registration number 53193989L), a unit of AllianceBernstein (Singapore) Ltd. which is a licensed entity under the Securities and

Futures Act and registered with Company Registration No. 199703364C, and/or their affiliates may at any time hold, increase or decrease positions in securities of any company mentioned herein.

Bernstein or its affiliates may provide investment management or other services to the pension or profit sharing plans, or employees of any company mentioned herein, and may give advice to

others as to investments in such companies. These entities may effect transactions that are similar to or different from those recommended herein.

Bernstein Research Publications are disseminated to our customers through posting on the firm's password protected website, www.bernsteinresearch.com. Additionally, Bernstein Research

Publications are available through email, postal mail and commercial research portals. If you wish to alter your current distribution method, please contact your salesperson for details.

Bernstein and/or its affiliates do and seek to do business with companies covered in its research publications. As a result, investors should be aware that Bernstein and/or its affiliates may have a

conflict of interest that could affect the objectivity of this publication. Investors should consider this publication as only a single factor in making their investment decisions.

This publication has been published and distributed in accordance with Bernstein's policy for management of conflicts of interest in investment research, a copy of which is available from Sanford

NORTH AMERICAN OIL & GAS EXPLORATION/PRODUCTION | 24

C. Bernstein & Co., LLC, Director of Compliance, 1345 Avenue of the Americas, New York, N.Y. 10105, Sanford C. Bernstein Limited, Director of Compliance, 50 Berkeley Street, London W1J

8SB, United Kingdom, or Sanford C. Bernstein (Hong Kong) Limited 盛博香港有限公司, Director of Compliance, 39th Floor, One Island East, Taikoo Place, 18 Westlands Road, Quarry Bay, Hong

Kong, or Sanford C. Bernstein (business registration number 53193989L) , a unit of AllianceBernstein (Singapore) Ltd. which is a licensed entity under the Securities and Futures Act and

registered with Company Registration No. 199703364C, Director of Compliance, One Raffles Quay, #27-11 South Tower, Singapore 048583. Additional disclosures and information regarding

Bernstein's business are available on our website www.bernsteinresearch.com.

CERTIFICATIONS

• I/(we), Bob Brackett, Ph.D., Senior Analyst(s)/Analyst(s), certify that all of the views expressed in this publication accurately reflect my/(our) personal views about any and all of the subject

securities or issuers and that no part of my/(our) compensation was, is, or will be, directly or indirectly, related to the specific recommendations or views in this publication.

Copyright 2018, Sanford C. Bernstein & Co., LLC, Sanford C. Bernstein Limited, Sanford C. Bernstein (Hong Kong) Limited 盛博香港有限公司, and AllianceBernstein (Singapore) Ltd., subsidiaries of AllianceBernstein L.P. ~1345 Avenue of the Americas ~ NY, NY 10105 ~212/756-4400. All rights reserved.

This publication is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of, or located in any locality, state, country or other jurisdiction where

such distribution, publication, availability or use would be contrary to law or regulation or which would subject Bernstein or any of their subsidiaries or affiliates to any registration or licensing

requirement within such jurisdiction. This publication is based upon public sources we believe to be reliable, but no representation is made by us that the publication is accurate or complete. We do

not undertake to advise you of any change in the reported information or in the opinions herein. This publication was prepared and issued by Bernstein for distribution to eligible counterparties or

professional clients. This publication is not an offer to buy or sell any security, and it does not constitute investment, legal or tax advice. The investments referred to herein may not be suitable for

you. Investors must make their own investment decisions in consultation with their professional advisors in light of their specific circumstances. The value of investments may fluctuate, and

investments that are denominated in foreign currencies may fluctuate in value as a result of exposure to exchange rate movements. Information about past performance of an investment is not

necessarily a guide to, indicator of, or assurance of, future performance.