northeast expansion opportunities - platts expansion opportunities ... 2011 | houston, tx | ... icf...

TRANSCRIPT

Northeast Expansion Opportunities

Platts 6th Annual Pipeline Development & Expansion Conference

September 22, 2011

Bobby HuffmanProject Director, Northeast Business Development

Pine River Gas Plant, British Columbia

Platts 6th Annual Pipeline Development & Expansion | September 22, 2011 | Houston, TX |

Safe Harbor Statement

Some of the statements in this document concerning future company performance will be forward-looking within the meanings of the securities laws. Actual results may materially differ from those discussed in these forward-looking statements, and you should refer to the additional information contained in Spectra Energy’s Form 10-K and other filings made with the SEC concerning factors that could cause those results to be different than contemplated in today's discussion.

Reg G Disclosure

In addition, today’s discussion includes certain non-GAAP financial measures as defined under SEC Regulation G. A reconciliation of those measures to the most directly comparable GAAP measures is available on our website.

2

Platts 6th Annual Pipeline Development & Expansion | September 22, 2011 | Houston, TX |

Our Diverse Portfolio of Assets

2010 Pipeline Throughput: 4.1 Tcf

Transmission Pipe: 19,100 mi

Gathering Pipe: 63,800 mi

Distribution Pipe: 40,600 mi

Storage Capacity: 305 Bcf

Retail Customers: 1.3 million

Gas storage facilityGas processing plantPropane terminalNGL StorageShale gas formations

3

Platts 6th Annual Pipeline Development & Expansion | September 22, 2011 | Houston, TX |

Strong Track Record of Executing Growth Plan

2007

2008

2009

2010

2011Shale gas formations

Est. Growth CapEx

Est. Full-Year EBIT ($MM)

TargetedROCE

ActualROCE

2007 – 2010 $ 4B $ 580 10-12% 14.5%

2011 – 2015 $ 5B+ $ 550+ 10-12% TBD

TOTAL $ 9B+ $ 1.1B+ 10-12% 12+%

4

Platts 6th Annual Pipeline Development & Expansion | September 22, 2011 | Houston, TX |

2011-2013 Northeast ProjectsAligned with Rockies and Marcellus Shale

5

Platts 6th Annual Pipeline Development & Expansion | September 22, 2011 | Houston, TX |

TEMAX / TIME III

Purpose:

Provides customers with access to Rockies supply

Project Scope:

TEMAX: 395 MMcf/d expansion connecting REX at Clarington to a new delivery point with Transco at Station 195

Time III: 60 MMcf/d from Oakford to Station 195

CapEx: ~$700 MM

Customers:

TEMAX: ConocoPhillips (10 years)

Time III: CenterPoint Energy (11 years) & PPL (13 years)

Project Status:

FERC certificate received Nov 2009

Construction started Mar 2010

In-Service: 2H10/2H11

Facilities:

93,933 horsepower of additional compression

9.6 miles of 36” loop

25.9 miles of 36” take-up and re-lay

26.5 miles of 30” greenfield pipeline to Station 195

Uprate pressure from 1,000 psi to 1,112 psi between Uniontown and Marietta

Platts 6th Annual Pipeline Development & Expansion | September 22, 2011 | Houston, TX |

TEAM 2012 (Texas Eastern Appalachian Market)

Purpose:

Provides customers with access to Marcellus and Rockies production

Project Scope:

200 MMcf/d expansion from southwestern PA

CapEx: ~$200 MM

Customers:

Range Resources (16 years)

Chesapeake Utilities (15 years)

Project Status:

Filed FERC Application Jan 2011

In-service 2H12

Facilities:

16.3 miles of 36” pipeline loop and replacement

20,720 horsepower of additional compression

Platts 6th Annual Pipeline Development & Expansion | September 22, 2011 | Houston, TX |

New Jersey – New York Expansion Project

Purpose:

Extends Texas Eastern reach farther into New Jersey and into New York for the first time

Project Scope:

800 MMcf/d expansion connecting Northeastern supplies with a new delivery point in Manhattan

CapEx: ~$850 MM

Customers:

Chesapeake Energy (20 years)

Consolidated Edison (15 years)

Statoil Natural Gas (20 years)

Project Status:

Filed FERC application Dec 2010

In-Service: 2H13

Facilities: 15.9 miles of new 30” pipe extending from Goethals to Manhattan, NY Replacement of approximately 5 miles of pipe with 42” pipe on Texas Eastern 3 compressor station reversals on Algonquin and Texas EasternMeter and regulator upgrades

Platts 6th Annual Pipeline Development & Expansion | September 22, 2011 | Houston, TX |

Marcellus Interconnect Program

42 Requests In-Service &Under Agreement 2011-2012(tap capacity)

6.8 Bcf/d

Current Marcellus Flow 625 MMcf/d

21 In-Service (tap capacity) 2200 MMcf/d

21 In Progress & Under Agreement(2011 & 1H 2012 In-Service)

4600 MMcf/d

9

Platts 6th Annual Pipeline Development & Expansion | September 22, 2011 | Houston, TX |

TETLP Marcellus Production Growth

10

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

Dth

/d

Platts 6th Annual Pipeline Development & Expansion | September 22, 2011 | Houston, TX |

Northeast Growth Opportunities

Future expansions deliver increased capacity to growing Northeast markets and access to Marcellus shale supply

Growth Opportunities

TEAM Project

AIM – Algonquin IncrementalMarket Project

MEPS Ethane Pipeline

MarcellusShale

MarcellusShale

Gas storage facility

1

2

3

3

2

11

1

Platts 6th Annual Pipeline Development & Expansion | September 22, 2011 | Houston, TX |

TEAM Project

TEAM Project Concept:

• Multiple receipt and delivery options.

• Within path market forward haul and backhaul.

• Forward haul expansion to:

– growing market demand within M3

– Transco and Columbia IC’s for Mid-Atlantic markets

• Backhaul facilities to:

– existing and future power opportunities in M2, M1, AA, and off of East Tennessee in the growing Southeast markets

– several pipeline interconnects in M2, M1, and AA

– LNG export opportunities

TEAM Project Receipt

TEAM Project Delivery

M2, M1, AA Power and Pipeline IC’s

Portfolio of multiple market and pipeline interconnect options serves to accomplish:• 365 day flow• maximum netback value

AGT – LambertvilleAGT – HanoverBUG – Goethals

Transco – Sta. 195Columbia – Marietta

12

Growing ETNG and SE Markets

35%

45%

20%100%

TEAM Project MDQ = 800 Mdth/d

SW PA

Kosci & Other

Station 195

New Jersey

Platts 6th Annual Pipeline Development & Expansion | September 22, 2011 | Houston, TX |

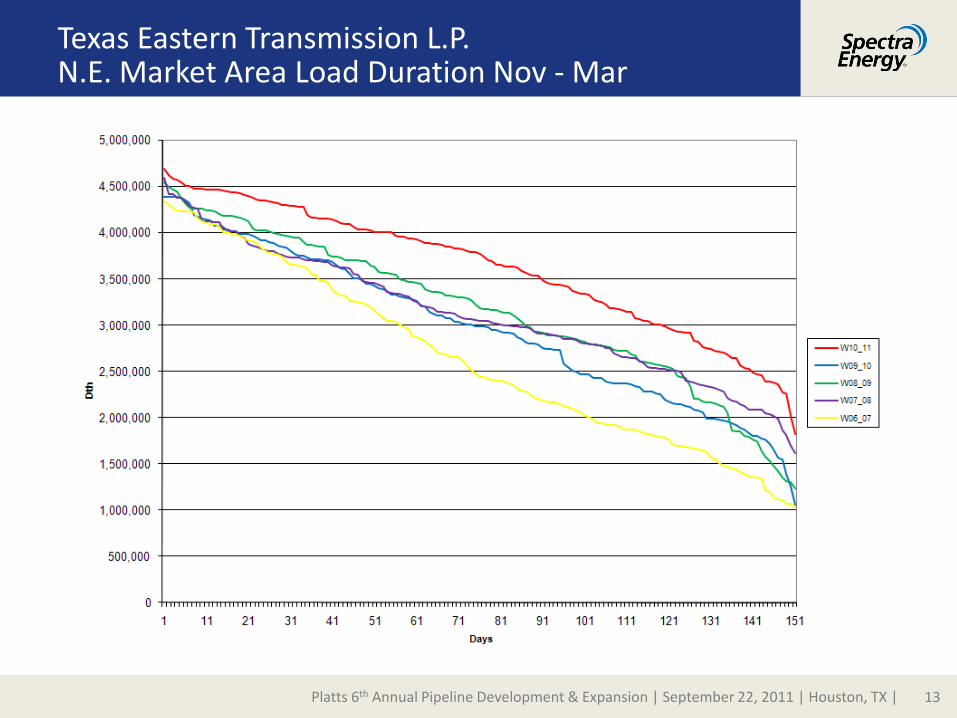

Texas Eastern Transmission L.P.N.E. Market Area Load Duration Nov - Mar

13

Platts 6th Annual Pipeline Development & Expansion | September 22, 2011 | Houston, TX |

Algonquin Incremental Market (AIM) Project

AIM Project Summary:

• Open season concluded February 11, 2011

• ~ 1 Bcf/d of non-binding nominations

• Project size and scope under development

• Target in-service 2H 2014

• Project benefits include:

• Access to premium AGT city gate points

• Increased deliverability to Iroquois

• Increased optionality for producers and end users to get gas to market

AIM Receipt

AIM Delivery

TETLP M3 Lambertville

AGT City Gate Deliveries

Iroquois – Zone 2

14

Platts 6th Annual Pipeline Development & Expansion | September 22, 2011 | Houston, TX |

Spectra Energy – Natural Gas Storage

Benefits to Producers:

• Production imbalance management

• Support reliable and flexible sales to end-users during demand variations

• Price arbitrage opportunities to maximize commodity pricing

Spectra Energy Advantage:

• Flexible Firm and Interruptible services that can be customized to customer’s requirements

• Strategic locations in Northeast and Gulf Coast with access to various shale plays and NE, SE, Midcon, and Texas markets

15

Platts 6th Annual Pipeline Development & Expansion | September 22, 2011 | Houston, TX |

Power Generation Opportunities

15

20

25

30

35

2007 2009 2011 2013 2015 2017 2019

Bcf

/d

North America Natural Gas Demandfor Power Generation

ICF April 2011 Gas Market Compass

Spectra Energy is well positioned for power generation opportunities• Increased utilization of gas-fired power

generation facilities currently attached or adjacent to our system

• Gas-fired power plants replacing coal or oil as a result of retirements

• Gas-fired generation backing up renewable power sources

• New gas-fired power generation facilities to meet power growth

16

Gas storage facility

Gas-fired plant attached

Coal-fired plant

Oil-fired plant

Follow us on:Recognized by: