not for publication or broadcast 12 aug 2016 sidang akhbar · not for publication or broadcast ......

TRANSCRIPT

Sidang Akhbar Prestasi Ekonomi pada Suku Kedua Tahun 2016

Gabenor Bank Negara Malaysia 12 Ogos 2016

Embargo

Not for publication or broadcast before 1200 hours on Friday, 12 Aug 2016

Sidang akhbar akan meliputi: • Prestasi ekonomi pada suku kedua tahun 2016

• Perkembangan monetari dan kewangan

• Sesi soal jawab

1

2

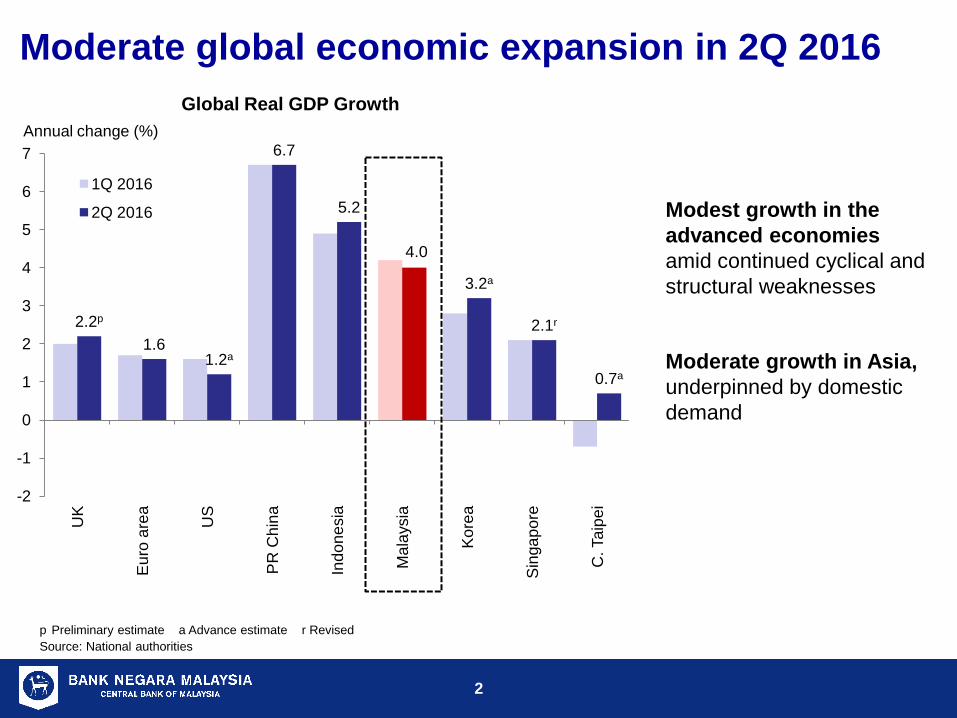

p Preliminary estimate a Advance estimate r Revised Source: National authorities

Moderate global economic expansion in 2Q 2016

2.2p 1.6

1.2a

6.7

5.2

4.0

3.2a

2.1r

0.7a

-2

-1

0

1

2

3

4

5

6

7

UK

Eur

o ar

ea

US

PR

Chi

na

Indo

nesi

a

Mal

aysi

a

Kor

ea

Sin

gapo

re

C. T

aipe

i

1Q 2016

2Q 2016

Modest growth in the advanced economies amid continued cyclical and structural weaknesses

Moderate growth in Asia, underpinned by domestic demand

Global Real GDP Growth Annual change (%)

3

Note: Figures do not necessarily add-up due to rounding Source: Department of Statistics, Malaysia

The Malaysian economy expanded by 4.0% in 2Q 2016

Domestic demand registered a stronger growth in 2Q 2016

• Higher growth contribution from private consumption and private investment

However, growth was set back by the continued decline in net exports and a drawdown in stocks

• Import growth exceeded exports following stronger investment activity

• Drawdown in stocks was due to lower production of palm oil and manufactured products

Contribution to Growth (percentage point)

2015 1Q 2016 2Q 2016

Real GDP 5.0 4.2 4.0

Domestic demand* 4.7 3.3 5.7

Private consumption 3.1 2.8 3.3

Private investment 1.1 0.4 1.1

Public sector 0.5 0.1 1.4

Change in stocks 0.6 2.0 -1.2

Net exports of G&S -0.4 -1.2 -0.6

*Excluding stocks

Contribution to GDP Growth

4

Growth supported by key economic sectors

1 Numbers do not add up due to rounding and exclusion of import duties component 1 Source: Department of Statistics, Malaysia

Real GDP (Annual change,

%)

Share, %

(2015)

2015 2016

2Q 1H 1Q 2Q 1H

Services 53.5 5.0 5.7 5.1 5.7 5.4

Manufacturing 23.0 4.2 4.9 4.5 4.1 4.3

Mining 9.0 6.0 7.8 0.3 2.6 1.4

Agriculture 8.9 4.6 0.3 -3.8 -7.9 -6.0

Construction 4.4 5.6 7.6 7.9 8.8 8.4

GDP 100.01 4.9 5.3 4.2 4.0 4.1

• Services: Faster pace of growth, driven mainly by consumption- related services

• Manufacturing: Growth supported mainly by E&E and primary-related clusters

• Construction: Stronger growth, underpinned by the civil engineering sub-sector

• Mining: Higher growth driven by stronger oil and gas production

• Agriculture: Sharper growth contraction, due mainly to lagged impact of El Niño on CPO production

Real GDP (Annual change, %)

Share, %

(2015)

2015 2016

2Q 1H 1Q 2Q 1H

Domestic demand (excluding stocks) 91.6 4.6 6.3 3.6 6.3 5.0

Private Sector 69.2 5.7 7.6 4.5 6.1 5.4

Consumption 52.4 6.4 7.7 5.3 6.3 5.8

Investment 16.9 3.9 7.4 2.2 5.6 4.0

Public Sector 22.4 0.9 1.8 0.4 6.9 3.6

Consumption 13.5 6.9 5.6 3.8 6.5 5.2

Investment 8.9 -8.1 -3.7 -4.5 7.5 1.1

Net exports of goods and services 8.6 -11.1 -10.5 -12.4 -7.0 -9.8

Exports 72.9 -4.0 -2.4 -0.5 1.0 0.2

Imports 64.3 -3.1 -1.1 1.3 2.0 1.6 Change in stocks (RM billion) -0.2 2.1 -0.6 2.4 -1.1 1.3

GDP (y-o-y) 100.01 4.9 5.3 4.2 4.0 4.1

GDP (q-o-q growth, seasonally adjusted) - 0.9 - 1.0 0.7 -

5

Private sector remained the anchor for growth

1 Numbers do not add up due to rounding 1 Source: Department of Statistics, Malaysia

• Higher domestic demand, driven by improvements in both the private and public sectors

• Private consumption supported by continued wage and income growth, and additional disposable income from Government measures

• Private investment driven by continued capital spending in services and manufacturing sectors

• Net exports registered a decline as real imports grew faster than exports

Source: Department of Statistics, Malaysia and Ministry of Human Resources

Strong growth in private consumption

Real Private Consumption Growth Annual change (%)

Wage Growth in Key Sectors Government measures Annual change (%)

Household spending expanded further…

…supported by favourable wage growth…

…and additional disposable income from Govt. measures

4.1 4.9

5.3

6.3

2

4

6

8

10

2Q 14 4Q 14 2Q 15 4Q 15 2Q 16 2

4

6

8

2Q 14 4Q 14 2Q 15 4Q 15 2Q 16

Manufacturing sector

Distributive trade services sub-sector

• Aidilfitri special assistance to civil servants and pensioners

• Reduction in employees’

EPF contribution rate (11% to 8%)

• BR1M disbursement

(end-April and mid-June)

LT average (1990-2015: 6.6%)

6

7

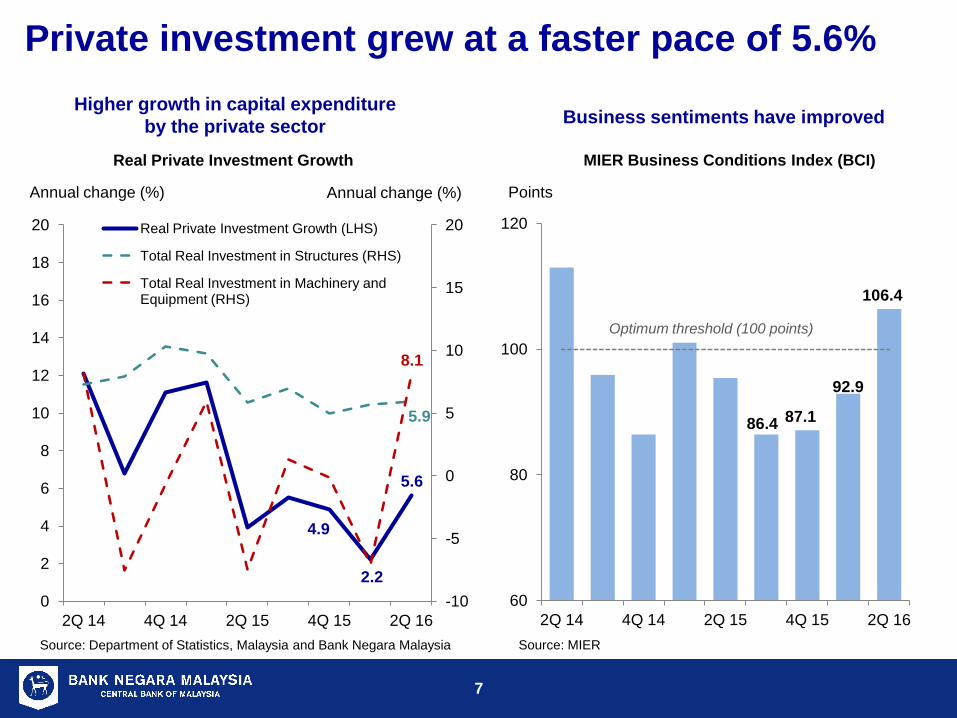

Private investment grew at a faster pace of 5.6%

Annual change (%)

Real Private Investment Growth

Higher growth in capital expenditure by the private sector

Source: Department of Statistics, Malaysia and Bank Negara Malaysia

4.9

2.2

5.6

5.9

8.1

-10

-5

0

5

10

15

20

0

2

4

6

8

10

12

14

16

18

20

2Q 14 4Q 14 2Q 15 4Q 15 2Q 16

Real Private Investment Growth (LHS)

Total Real Investment in Structures (RHS)

Total Real Investment in Machinery and Equipment (RHS)

Points

MIER Business Conditions Index (BCI)

Business sentiments have improved

Source: MIER

86.4 87.1

92.9

106.4

60

80

100

120

2Q 14 4Q 14 2Q 15 4Q 15 2Q 16

Optimum threshold (100 points)

Annual change (%)

8

Steady inflows of foreign direct investment

Note: Others comprises of agriculture and construction sector Source: Department of Statistics, Malaysia

RM bn Net FDI inflows in Malaysia

Recent FDI inflows remain above post-GFC averages

15.0

8.8

0

2

4

6

8

10

12

14

16

18

2Q 14 4Q 14 2Q 15 4Q 15 2Q 16

2009 - 2015 quarterly average: RM7.8bn

Bulk of FDI channelled into the manufacturing and services sector

Manufacturing 72%

Services 16%

Mining 11%

Others 1%

Net FDI inflows by Sector 2Q 2016: RM8.8 billion

… and higher net income payments contributed to smaller current account surplus

Smaller current account surplus due mainly to lower trade surplus and higher investment income

1.8 0.6

-9

-6

-3

0

3

6

9

12

-30

-20

-10

0

10

20

30

40

2Q 14 4Q14 2Q15 4Q15 2Q16

Goods Services Primary income Secondary income CAB % of GNI

RM bn % of GNI

Current account balance (RHS)

Source: Department of Statistics, Malaysia

9

23.9

17.9

1.0 1.4

-0.4

3.1

-16

-12

-8

-4

0

4

8

12

16

20

24

28

32

2Q 14 4Q 14 2Q 15 4Q 15 2Q 16 -10

-5

0

5

10

15

20

Imports

Exports

% yoy RM bn

Trade balance (RHS)

Lower trade surplus due mainly to higher imports for investment and production…

Following the strong appreciation in 1Q 2016, the ringgit retraced some of the gains in 2Q 2016

Performance of Selected Currencies against the USD

Source: Bank Negara Malaysia

• Despite expectations of a slower pace of interest rate increase by the Fed, these expectations can shift swiftly

• Global crude oil prices are expected to remain volatile due to uncertain supply and demand conditions

• Uncertainty surrounding the United Kingdom’s EU referendum and its aftermath

• Malaysia's sound economic fundamentals will provide support for the ringgit over the medium term

10

The ringgit will continue to face volatility, due mainly to uncertainties in the external environment

Ringgit depreciated against most major and regional currencies in 2Q 2016

-6.5

-2.9

-2.7

-2.5

-2.1

-1.9

-0.7

0.1

0.2

0.8

9.4

-2.4

-3.2

-3.3

4.8

0.4

9.4

1.9

3.5

2.7

2.2

4.6

4.0

7.1

4.4

6.2

-10 -5 0 5 10 15

GBP

AUD

CNY

MYR

PHP

EUR

KRW

THB

SGD

IDR

JPY

REER

NEER

Q1 2016 Q2 2016

% change

11

41%

27%

16% 14%

1% 1% 1% 0

20

40

60

80

100

Ass

et M

anag

emen

t

Cen

tral B

ank/

G

over

nmen

t

Ban

ks

Pen

sion

Fu

nds

Insu

ranc

e C

ompa

nies

Nom

inee

s/

Cus

todi

ans

Oth

ers

RM billion

Distribution of Non-resident Holdings in Government Bonds as at end-May’16

31% 34%

0%

5%

10%

15%

20%

25%

30%

35%

0

50

100

150

200

250

300

Jul-14 Jan-15 Jul-15 Jan-16 Jul-16

% NR Holding RM billion

Govt Bond (LHS) % NR of Govt (RHS)

Non-resident holdings of Malaysian government bonds increased to 34% as of July 2016

Majority of non-residents are long-term investors

15 Note: ‘Others’ include individuals, non-financial corporations and unidentified sectors Source: Bank Negara Malaysia

Non-resident holding of Malaysian Government Bonds

Non-resident holdings of Malaysian government bonds have been stable, underpinned by long-term investors

Reserves remain ample while external debt is manageable

International reserves have increased since fourth quarter of 2015

Source: Bank Negara Malaysia

12

External debt is mostly long-term, while foreign-currency exposure is manageable

0

2

4

6

8

10

12

85

95

105

115

125

135

145

Jan-13 Jul-13 Jan-14 Jul-14 Jan-15 Jul-15 Jan-16 Jul-16

USD billion

Net International Reserves Retained import cover (RHS) Reserves/ST ext debt (RHS)

29 July 2016: USD97.3 bn

8.1

1.2

Months/ Times

Total external debt: RM842.2 billion (69.0% of GDP)

Long-term 60.7%

Short-term 39.3%

Foreign Currency

62.0% Ringgit 38.0%

No immediate repayment requirements

By Tenure

Not affected by valuation

Largely hedged and backed by external assets

By Currency Composition

-8.0

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

2Q 14 4Q 14 2Q 15 4Q 15 2Q 16

Inflation

Headline inflation Food and non-alcoholic beverages Transport Housing, water, electricity, gas and other fuels

Annual growth, %

Headline inflation declined to 1.9% in 2Q 2016

Source: Department of Statistics, Malaysia and Bank Negara Malaysia

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

Headline inflation

Food & non-

alcoholic beverages

Housing, water,

electricity, gas &

other fuels

Transport Others

Contribution to Headline Inflation

1Q 2016 2Q 2016

Percentage point

13

• The OPR was reduced by 25 basis points to 3.00% at the July MPC meeting

• The adjustment is to ensure that the domestic economy continues on a steady growth path amid stable inflation

• KLIBOR, Base Rate and fixed deposit rates have declined

3.40 (-25bps)

3.62 (-21bps)

3.00 (-18bps) 3.00

(-25bps)

2.5

2.7

2.9

3.1

3.3

3.5

3.7

3.9

4.1

Jan-15 Apr-15 Jul-15 Oct-15 Jan-16 Apr-16 Jul-16

% Market and Retail Interest Rates

Weighted Average Base Rate (BR)

3-month KLIBOR

Average Fixed Deposit (FD) Rate (1-year and below)

Overnight Policy Rate (OPR)

Reduction in OPR has started to impact market and retail interest rates

14

Source: Bank Negara Malaysia

15

Financing continued to be channelled to the private sector

While outstanding loan growth moderated, with slower growth across segments…

Net Financing1 and Outstanding Loan Growth

1Outstanding loan of the banking system (BS), development financial institutions (DFIs) and outstanding corporate bonds (CB)

*Excludes issuances by Cagamas

Gross Financing through the BS, DFIs and Capital Market Annual change (%) RM billion

0.0

4.0

8.0

12.0

16.0

20.0

2Q13 4Q13 2Q14 4Q14 2Q15 4Q15 2Q16

259 263

308 290 289

310 319

291 295 297

342

291 292

100

150

200

250

300

350

400

2Q13 4Q13 2Q14 4Q14 2Q15 4Q15 2Q16

Loans Disbursed Gross Corporate Bonds Issued* Equity

… gross financing to the private sector was relatively sustained in 2Q 2016

Total loan growth: 5.5%

Net financing growth: 6.9%

SME loan growth: 9.2%

Source: Bank Negara Malaysia

16

Continued access to financing for households and SMEs (including micro enterprises)

Source: Bank Negara Malaysia

9.2

5

10

15

20

100

120

140

160

180

200

220

240

260

280

300

2013 2014 2015 2Q 16

Outstanding financing

Debt growth (RHS)

SMEs

RM (billion)

Annual growth (%)

7.1

-5

0

5

10

15

800

820

840

860

880

900

920

940

960

2013 2014 2015 2Q 16

Outstanding financing

Debt growth (RHS)

RM (million)

Annual growth (%)

940.8

Micro-enterprises1

1Under Skim Pembiayaan Mikro

285.5

10.2

5

7

9

11

13

15

100

150

200

250

300

350

400

450

500

550

2013 2014 2015 2Q 16

Outstanding financing

Debt growth (RHS)

Residential properties

RM (billion)

Annual growth (%)

525.1

Source: Bank Negara Malaysia

17

• Limited risk from EU referendum − Low direct exposures of

Malaysian banks to UK counterparties

− Transient market volatility

• Impact from more challenging business conditions and rising costs expected to be modest

• Strong level and quality of capitalisation continues to provide a buffer against adverse developments

Banking sector 1Q 2016 2Q 2016

Common equity tier 1 capital ratio (%) 13.0 12.9

Tier 1 capital ratio (%) 13.9 13.9

Total capital ratio (%) 16.5 16.4

Capital buffer (RM bil) 121.3 120.8

Net impaired loans ratio (%) 1.2 1.3

ROE (annualised) 12.4 13.2

Liquidity Coverage Ratio (%) 126 125

Insurance/Takaful sector 1Q 2016 2Q 2016

Capital adequacy ratio (%) - Insurance 249.2 234.9

Capital adequacy ratio (%) - Takaful 186.2 187.3

Capital buffer (RM bil) 48.5 33.0

Profit YTD (RM bil) 5.4 9.0

Financial stability preserved amid continued global uncertainties

18

Ample liquidity in the banking system

Source: Bank Negara Malaysia

RM178.5 bil

125 %

70%

60

80

100

120

140

0

100

200

300

400

500

2Q 3Q 4Q 1Q 2Q

2015 2016

% RM bil

Banks' surplus liquidity placed with BNM (including SRR) Stock of high quality liquid assets Liquidity Coverage Ratio (LCR, RHS) LCR minimum regulatory requirement (RHS)

Banking system surplus liquidity remained high at RM178.5 billion

2.55

87.8

82.6

73.8

2.0

2.5

3.0

65

70

75

80

85

90

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q

%

Average cost of deposit (RHS) Loan-to-deposit ratio Loan-to-fund ratio Loan-to-fund & equity ratio

Banks’ funding structure continued to be supportive of financing activities

2016 2013 2014 2015

19

Manageable credit risk exposures to businesses

41.9

4.2

1.1 0

2

4

6

8

10

36

38

40

42

44

46

48

50

1Q13 3Q13 1Q14 3Q14 1Q15 3Q15 1Q16

Debt-to-equity ratio Interest coverage ratio (RHS) Cash-to-short-term debt (RHS)

% times

Overall debt servicing capacity sustained

Source: Bank Negara Malaysia

2.8

0.4

2.6

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

2Q13 4Q13 2Q14 4Q14 2Q15 4Q15 2Q16

Business: Impaired loans ratio Business: Delinquency ratio SMEs: Impaired loans ratio

%

Delinquencies and impairment remained stable

49%

29%

23%

0

500

1,000

1,500

1998 2008 2012 2013 2014 2015 Jun-16

Domestic Loans Domestic PDS External Debt

RM

Annual growth : 6.7%

Businesses, including SMEs, have continued access to financing

20

Household debt servicing capacity remains intact

Source: Bank Negara Malaysia

1.4

1.6

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

2011 2012 2013 2014 2015 2Q 16

Household: Delinquency ratio

Household: Impairment ratio

Quality of household loans remained strong

%

89

181

126

0

500

1,000

1,500

2,000

-50

0

50

100

150

200

2011 2012 2013 2014 2015 2Q 16

Residential Properties (RHS) Passenger Cars (RHS) Personal Financing (RHS) Credit Cards (RHS) Others (RHS) Debt-to-GDP ratio Financial assets-to-GDP ratio Liquid financial assets-to-GDP ratio

Aggregate household financial assets remained at two times of debt

Ratio %

Outstanding HH Debt RM billion

6.2

3.7

0

5

10

15

0

500

1,000

1,500

2,000

2,500

2011 2012 2013 2014 2015 2Q 16

Debt Financial assets Debt growth (RHS) Financial assets growth (RHS)

Growth in household debt continued to moderate

RM (billion)

Annual growth (%)

21

Agensi Kaunseling dan Pengurusan Kredit (AKPK) has helped individuals manage financial obligations

2015 Jan.-Jun. 2016

No. of borrowers benefitted from AKPK’s financial advice and credit counselling 84,664 55,507

Of which, enrolled into Debt Management Programme (DMP) 22,208 11,444

Insurance/Takaful sector Composition (%)

Credit Card 65.3 Personal Loan 25.8 Hire Purchase 1.8 Housing loan 2.0 Others 5.1 Total 100

DMP Cases by Type of Financing (2015 - Jun. 2016)

Number of Individuals Assisted by AKPK

• Since its establishment in 2006,

AKPK has assisted over 450,000

borrowers through its financial

advice and credit counselling

• Of these, more than 155,000

borrowers who have difficulties in

repaying their loans have

enrolled into Debt Management

Programme (DMP)

Despite the challenging economic environment, the Malaysian economy is expected to remain on the current growth trajectory of 4 – 4.5%, driven by domestic demand

Growth prospects supported by:

− Higher wages for civil servants and upward revision to minimum wages

− Continued implementation of infrastructure projects

− Improved commodities production from the diminishing effect of El Niño

However, the uncertainties in the global environment could weigh on Malaysia’s growth in 2H 2016

Growth performance continued to be resilient amid a challenging environment

22

Q&A Session