not super yet

TRANSCRIPT

1 © 2015 Deloitte Touche Tohmatsu

Not super yet…

Stephen Huppert

Partner, Deloitte

@stephenhuppert

2 © 2015 Deloitte Touche Tohmatsu 2 Compliance Considerations © 2013 Deloitte Touche Tohmatsu

2 © 2015 Deloitte Touche Tohmatsu

Congratulations on your retirement. Here’s your superannuation benefit.

Thanks for playing…

3 © 2015 Deloitte Touche Tohmatsu 3 Compliance Considerations © 2013 Deloitte Touche Tohmatsu

3 © 2015 Deloitte Touche Tohmatsu

Source: ABS,

Let’s start with some demographic statistics courtesy of the ABS

2015 2045

http://www.abs.gov.au/websitedbs/d3310114.nsf/home/Population%20Pyramid%20-%20Australia

4 © 2015 Deloitte Touche Tohmatsu

5 © 2015 Deloitte Touche Tohmatsu 5 © 2015 Deloitte Touche Tohmatsu

Life expectancy and pension age

40

45

50

55

60

65

70

75

80

85

90

1881-1890 1946-1948 1975-1977 1994-1996 1999-2001 2004-2006 2010-2012

Life Expectancy at Birth

Life Expectancy at 65

Pension Age

Males, ABS Life Tables

6 © 2015 Deloitte Touche Tohmatsu 6 © 2015 Deloitte Touche Tohmatsu

Future life expectancy and pension age

60

65

70

75

80

85

90

95

2010 2015 2020 2025 2030 2035 2040 2045 2050 2055

Life expectancy at 65 Current Pension Age

NCOA Proposed Pension Age Govt Proposed Pension Age

Govt Proposed Pension Age2 ?

Males, ABS Life Tables

7 © 2015 Deloitte Touche Tohmatsu © 2013 Deloitte Touche Tohmatsu

7 © 2015 Deloitte Touche Tohmatsu

8 © 2015 Deloitte Touche Tohmatsu 8 Compliance Considerations © 2013 Deloitte Touche Tohmatsu

8 © 2015 Deloitte Touche Tohmatsu

What is success for the superannuation system?

What is success for a superannuation fund?

Melbourne Mercer Global Pension Index

9 © 2015 Deloitte Touche Tohmatsu 9 Compliance Considerations © 2013 Deloitte Touche Tohmatsu

9 © 2015 Deloitte Touche Tohmatsu

What is success for the superannuation system?

What is success for a superannuation fund?

10 © 2015 Deloitte Touche Tohmatsu 10 © 2015 Deloitte Touche Tohmatsu

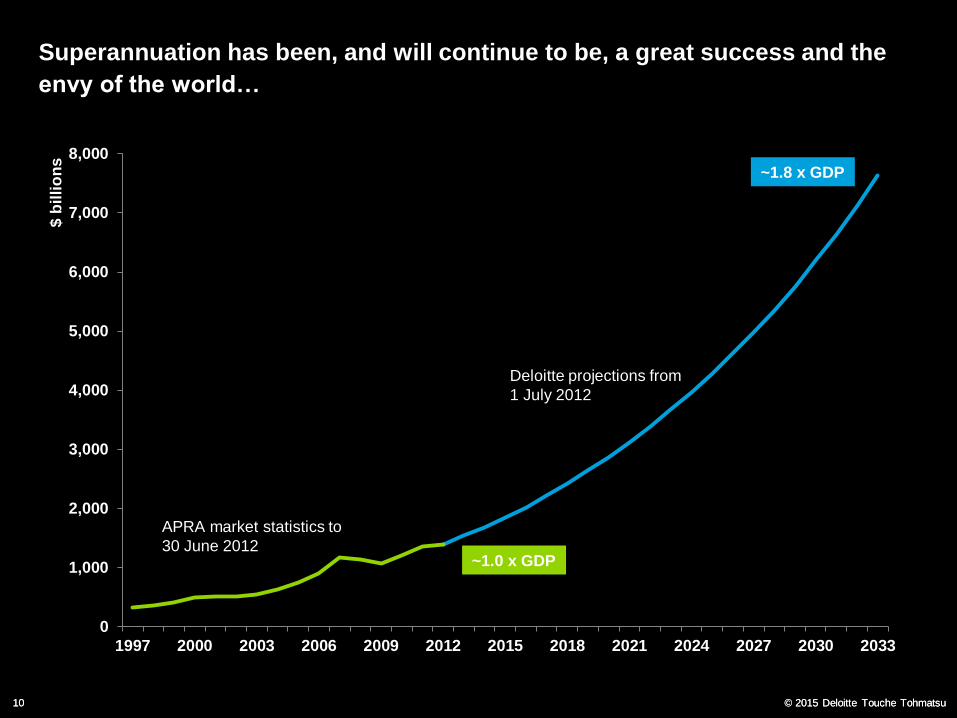

Superannuation has been, and will continue to be, a great success and the

envy of the world…

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

1997 2000 2003 2006 2009 2012 2015 2018 2021 2024 2027 2030 2033

$ b

illi

on

s

APRA market statistics to

30 June 2012

Deloitte projections from

1 July 2012

~1.0 x GDP

~1.8 x GDP

11 © 2015 Deloitte Touche Tohmatsu 11 Compliance Considerations © 2013 Deloitte Touche Tohmatsu

11 © 2015 Deloitte Touche Tohmatsu

What is the purpose of a superannuation fund?

12 © 2015 Deloitte Touche Tohmatsu © 2013 Deloitte Touche Tohmatsu

12 © 2015 Deloitte Touche Tohmatsu

13 © 2015 Deloitte Touche Tohmatsu 13 © 2015 Deloitte Touche Tohmatsu

Pillars of a retirement income system

Pillar 1 Age pension

Pillar 2 Compulsory superannuation contributions.

Pillar 3 Voluntary superannuation contributions and other savings

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

55 56 57 58 59 60 61 62 63 64

65-6

9

70-7

4

75-7

9

80+

Age

Households Persons

Source: Superannuation Policy for Post-Retirement, Productivity Commission Research Paper

Share of people with

super remaining

14 © 2015 Deloitte Touche Tohmatsu 14 Compliance Considerations © 2013 Deloitte Touche Tohmatsu

14 © 2015 Deloitte Touche Tohmatsu

Financial System Inquiry recommendations

Objectives of the superannuation system

Seek broad political agreement for, and enshrine in legislation,

the objectives of the superannuation system and report publicly

on how policy proposals are consistent with achieving these

objectives over the long term.

The retirement phase of superannuation

Require superannuation trustees to pre-select a comprehensive

income product for members’ retirement. The product would

commence on the member’s instruction, or the member may

choose to take their benefits in another way. Impediments to

product development should be removed.

15 © 2015 Deloitte Touche Tohmatsu 15 © 2015 Deloitte Touche Tohmatsu

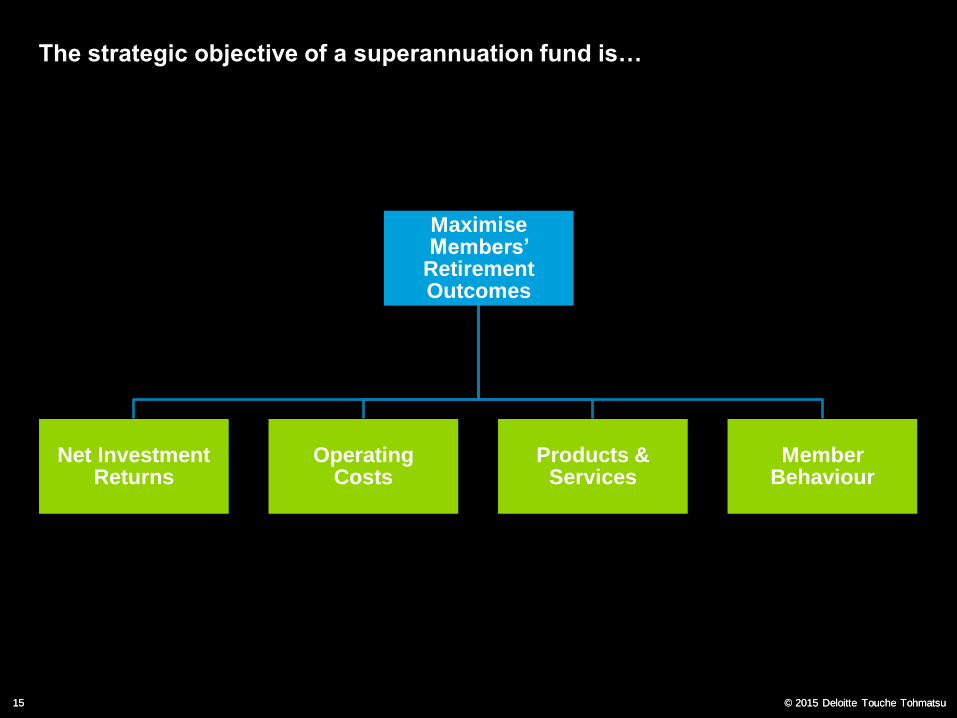

The strategic objective of a superannuation fund is…

Maximise Members’

Retirement Outcomes

Net Investment Returns

Operating Costs

Products & Services

Member Behaviour

16 © 2015 Deloitte Touche Tohmatsu 16 Compliance Considerations © 2013 Deloitte Touche Tohmatsu

16 © 2015 Deloitte Touche Tohmatsu

…and peace in the Middle East

CIPR: comprehensive income product for retirement

Desired features of retirement income products

17 © 2015 Deloitte Touche Tohmatsu 17 Compliance Considerations © 2013 Deloitte Touche Tohmatsu

17 © 2015 Deloitte Touche Tohmatsu

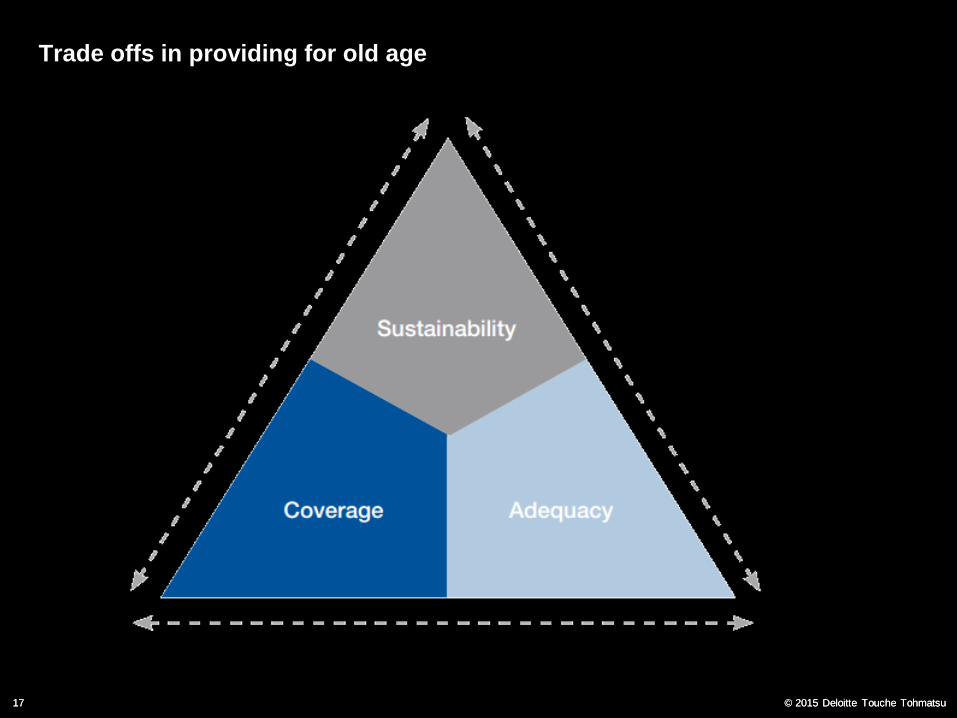

Trade offs in providing for old age

18 © 2015 Deloitte Touche Tohmatsu 18 Compliance Considerations © 2013 Deloitte Touche Tohmatsu

18 © 2015 Deloitte Touche Tohmatsu

Myth: Australia has a lump sum culture…

0

5

10

15

20

25

30

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

$b

Value of lump sums

Value of income streams

0

10

20

30

40

50

60

70

80

90

100

0 - 50 50 -100

100 -200

200 -300

Over 300

Total

Pe

r c

en

t o

f b

en

efi

ts

Lump sum Account-based pension

Source: Superannuation Policy for Post-Retirement, Productivity Commission Research Paper

19 © 2015 Deloitte Touche Tohmatsu 19 © 2015 Deloitte Touche Tohmatsu

Retirement income products in Australia

94%

5%

1%

Account based pensions

Annuity products

Hybrid products

Source: Mercer Post Retirement Market Trends in Australia, June 2014

20 © 2015 Deloitte Touche Tohmatsu 20 © 2015 Deloitte Touche Tohmatsu

Post Retirement Risks

Financial Risks

• Inflation risk

• Interest rate risk

• Stock market risk

• Business risk

• Employment risk

Information and public policy risks:

• Lack of appropriate information risk

• Public policy risks

Care and housing risks

• Changes in housing needs risks

• Loss of ability to live independently

risk

• Health care risk

Personal and Family risks

• Longevity risk

• Change in marital or partnership

status risk

• Unforeseen needs of family members

risk

21 © 2015 Deloitte Touche Tohmatsu 21 Compliance Considerations © 2013 Deloitte Touche Tohmatsu

21 © 2015 Deloitte Touche Tohmatsu

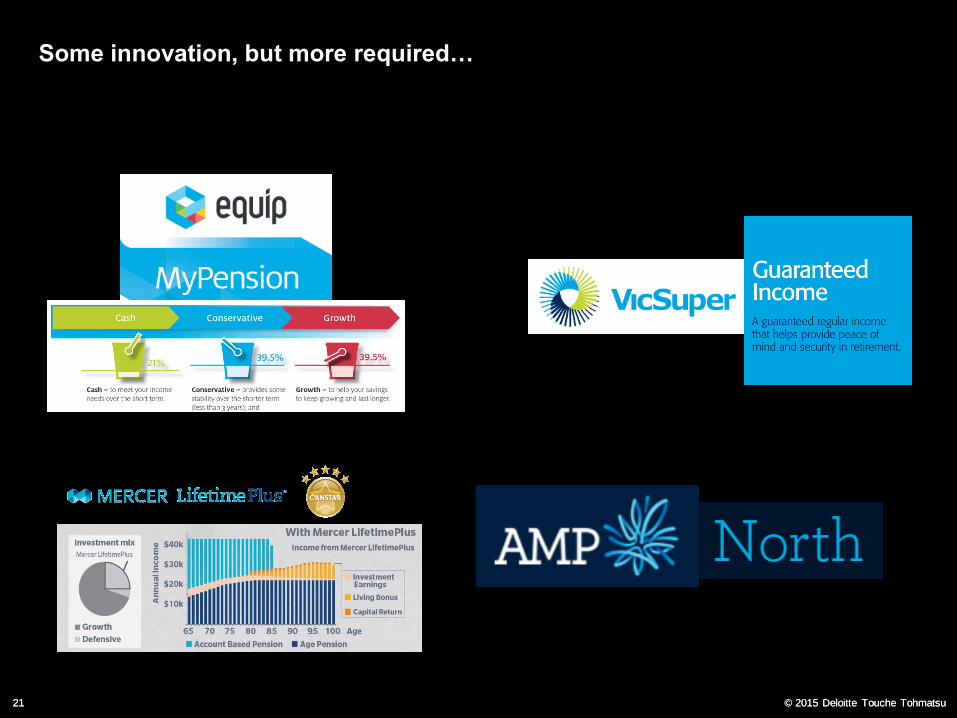

Some innovation, but more required…

22 © 2015 Deloitte Touche Tohmatsu 22 © 2015 Deloitte Touche Tohmatsu

Pillars of a retirement income system

Pillar 1 Age pension

Pillar 2 Compulsory superannuation contributions.

Pillar 3 Voluntary superannuation contributions and other savings

23 © 2015 Deloitte Touche Tohmatsu 23 © 2015 Deloitte Touche Tohmatsu

Pillars of a retirement income system

Pillar 1 Age pension

Pillar 2 Compulsory superannuation contributions.

Pillar 3 Voluntary superannuation contributions and other savings

Pillar 4 ????

24 © 2015 Deloitte Touche Tohmatsu 24 © 2015 Deloitte Touche Tohmatsu

Connect

Stephen Huppert

Partner, Deloitte

au.linkedin.com/in/stephenhuppert

@stephenhuppert

25 © 2015 Deloitte Touche Tohmatsu © 2013 Deloitte Touche Tohmatsu

25 © 2015 Deloitte Touche Tohmatsu

About Deloitte

Deloitte provides audit, tax, consulting, and financial advisory services to public and private clients

spanning multiple industries. With a globally connected network of member firms in 140 countries,

Deloitte brings world class capabilities and deep local expertise to help clients succeed wherever they

operate. Deloitte's 150,000 professionals are committed to becoming the standard of excellence.

Deloitte's professionals are unified by a collaborative culture that fosters integrity, outstanding value

to markets and clients, commitment to each other, and strength from diversity. They enjoy an

environment of continuous learning, challenging experiences, and enriching career opportunities.

Deloitte's professionals are dedicated to strengthening corporate responsibility, building public trust,

and making a positive impact in their communities.

Deloitte refers to one or more of Deloitte Touche Tohmatsu, a Swiss Verein, and its network of

member firms, each of which is a legally separate and independent entity. Please see

www.deloitte.com/au/about for a detailed description of the legal structure of Deloitte Touche

Tohmatsu and its member firms.

About Deloitte Australia

In Australia, Deloitte has 12 offices and over 4,500 people and provides audit, tax, consulting, and

financial advisory services to public and private clients across the country. Known as an employer

of choice for innovative human resources programs, we are committed to helping our clients and

our people excel. Deloitte's professionals are dedicated to strengthening corporate responsibility,

building public trust, and making a positive impact in their communities. For more information,

please visit Deloitte’s web site at www.deloitte.com.au.

Confidential This document and the information contained in it is confidential and should not be

used or disclosed in any way without our prior consent.

Liability limited by a scheme approved under Professional Standards Legislation.

General information only

This presentation is provided as general information only and does not consider your specific objectives, situation or needs. You should not rely on the information in this presentation or disclose it or refer to it in

any document. We accept no duty of care or liability to you or anyone else regarding this presentation and we are not responsible to you or anyone else for any loss suffered in connection with the use of this

presentation or any of its content.

© Deloitte Touche Tohmatsu, 2013. All rights reserved.

26 © 2015 Deloitte Touche Tohmatsu 26 Compliance Considerations © 2013 Deloitte Touche Tohmatsu

26 © 2015 Deloitte Touche Tohmatsu

Quiz: Identify the review…