notice of meeting of the audit committee · that the minutes of the meeting of the audit committee...

TRANSCRIPT

Notice of Meeting of the Audit Committee

NOTICE IS HEREBY GIVEN in accordance with Section 87 of the Local Government Act 1999, that a meeting of the

MEETING OF THE AUDIT COMMITTEE

of the

CITY OF BURNSIDE

will be held in the Boardroom at the Civic Centre 401 Greenhill Road, Tusmore

on

Monday 16 June 2014 at 6.00 pm.

Light refreshments will be available in the Boardroom from 5.30 pm.

Paul Deb Chief Executive Officer

1

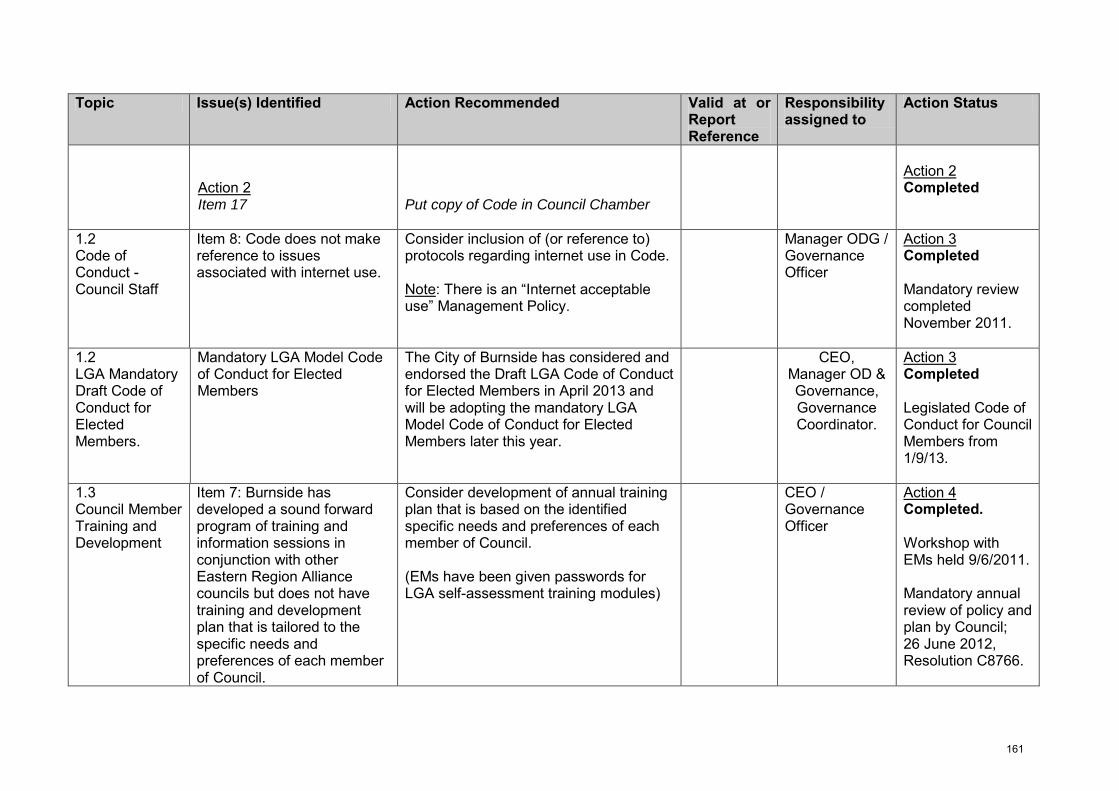

Audit Committee Meeting Agenda

Monday 16 June 2014 at 6.00 pm Boardroom, 401 Greenhill Road, Tusmore

Members: Councillor Osterstock - Chair Mayor, David Parkin Councillor Cornish Mr Andrew Blaskett Ms Lisa Scinto

1. Apologies 2. Leave of Absence 3. Confirmation of the Minutes

That the Minutes of the meeting of the Audit Committee held on 15 April 2014 be taken as read and confirmed.

4 Governance Critical Dates Report p 4

Forward Agenda p 7Action List p 8 Internal Audit – Status Report p 16Council Policy Review Tracking p 19

5. Reports 5.1 Audit Committee Terms of Reference (Strategic) p 31

Attachment A p 33

5.2 Review Draft Treasury Management Policy (Strategic) p 45 Attachment A p 49 Attachment B p 58 Attachment C p 68 Attachment D p 74

5.3 Business Service Review – Finance (Operational) p 89 Attachment A p 92 5.4 Business Service Review – Finance Structure (Operational) p 109

Attachment A p 112

5.5 External Auditor’s Interim Report 2013/14 (Operational) p 145 Attachment A p 149 5.6 Good Governance Assessment Program – Progress Report (Operational) p 157 Attachment A p 160 Attachment B p 171

2

Audit Committee Agenda 16 June 2014

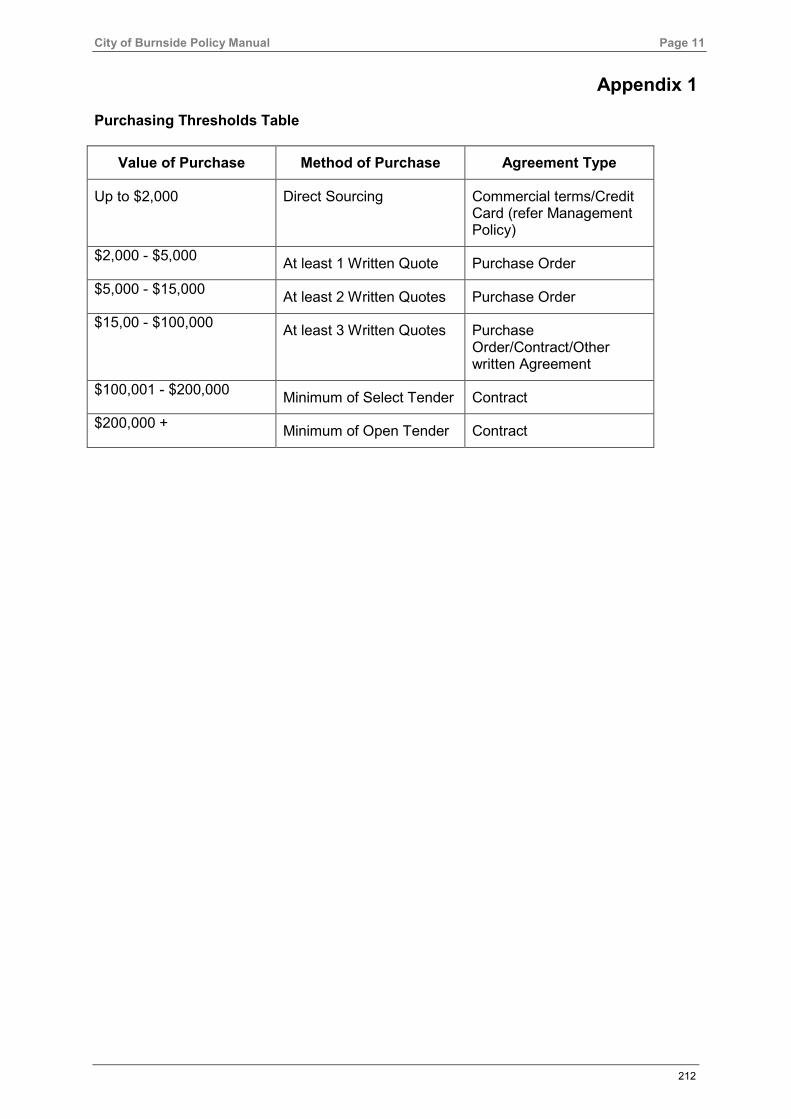

5.7 Procurement Policy Review (Strategic) p 173 Attachment A p 177 Attachment B p 188

Attachment C p 202

6. Confidential Items Nil

7. Date of Next Meeting Meeting to be held during the week commencing 18 August 2014

8. Other Business

9. Closure

3

GOVERNANCE CRITICAL DATES TABLE

July 2013 – June 2014 Note: Reference to the Act refers to the Local Government Act 1999 and Local Government (General) Regulations 1999 unless otherwise indicated.

Date Task Act Reference Action/comment 30 September – 31 May (Inclusive) Next due February 2014

Period during which a regional subsidiary must at least twice consider a report showing a revised forecast of operating & capital investment activities for the relevant financial year. Regional subsidiaries:

Eastern Health Authority Eastern Waste Management Authority Highbury Landfill Authority

Regulation 9(1)(a) of the Local Government (Financial Management) Regulations 2011

Most recent material will be provided at the February 2014 Audit Committee meeting.

30 September – 31 May (Inclusive) Next due February 2014

Period during which a Council must at least twice consider a report showing a r evised forecast of operating & capital investment activities for the relevant financial year.

Regulation 9(1)(a) of the Local Government (Financial Management) Regulations 2011

30 November – 15 March (inclusive)

Period in which a council, council subsidiary or regional subsidiary must consider a report showing a revised forecast of each item shown in its budgeted financial statements for the relevant financial year compared with the estimates set out in the budget presented in a manner consistent with the Model Financial Statements. The report must also include revised forecasts for the relevant financial year of the council’s operating surplus ratio, net financial liabilities ratio and asset sustainability ratio compared with estimates set out in the budget presented in a manner consistent with the note in the Model Financial Statements entitled Financial Indicators

Regulation 9(1)(b) & (2) of the Local Government (Financial Management) Regulations 2011

4

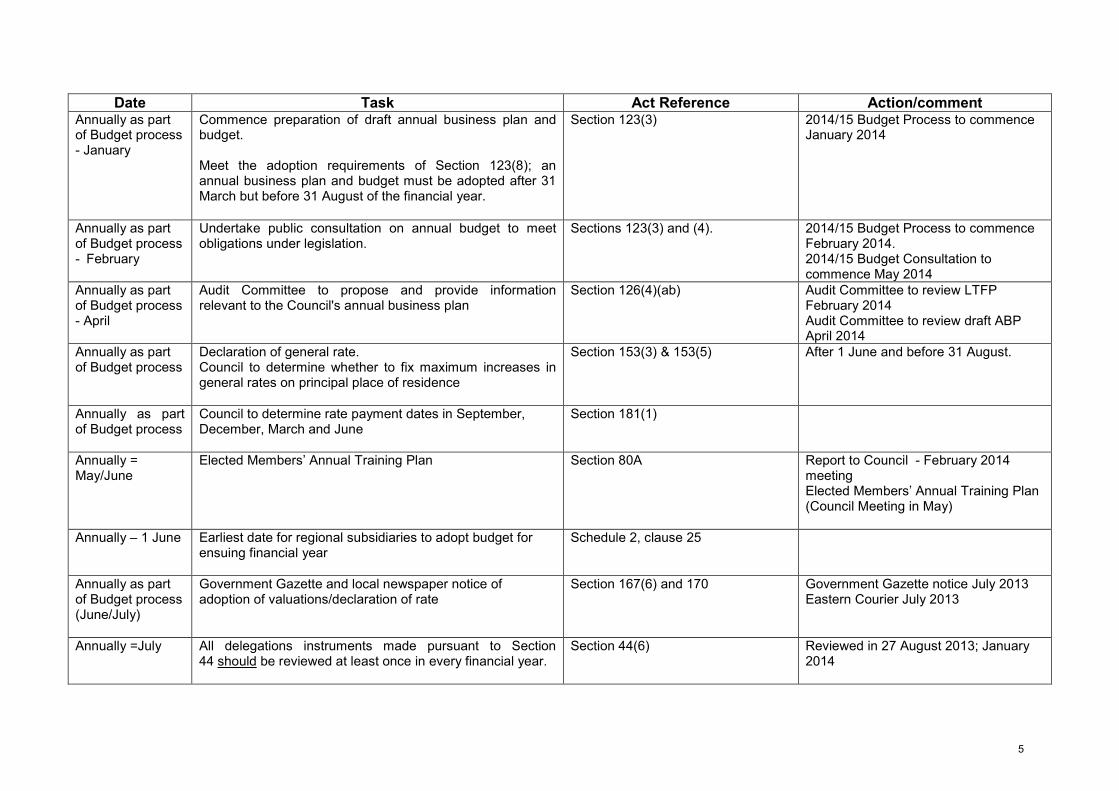

Date Task Act Reference Action/comment Annually as part of Budget process - January

Commence preparation of draft annual business plan and budget. Meet the adoption requirements of Section 123(8); an annual business plan and budget must be adopted after 31 March but before 31 August of the financial year.

Section 123(3) 2014/15 Budget Process to commence January 2014

Annually as part of Budget process - February

Undertake public consultation on annual budget to meet obligations under legislation.

Sections 123(3) and (4). 2014/15 Budget Process to commence February 2014. 2014/15 Budget Consultation to commence May 2014

Annually as part of Budget process - April

Audit Committee to propose and provide information relevant to the Council's annual business plan

Section 126(4)(ab) Audit Committee to review LTFP February 2014 Audit Committee to review draft ABP April 2014

Annually as part of Budget process

Declaration of general rate. Council to determine whether to fix maximum increases in general rates on principal place of residence

Section 153(3) & 153(5) After 1 June and before 31 August.

Annually as part of Budget process

Council to determine rate payment dates in September, December, March and June

Section 181(1)

Annually = May/June

Elected Members’ Annual Training Plan Section 80A Report to Council - February 2014 meeting Elected Members’ Annual Training Plan (Council Meeting in May)

Annually – 1 June Earliest date for regional subsidiaries to adopt budget for ensuing financial year

Schedule 2, clause 25

Annually as part of Budget process (June/July)

Government Gazette and local newspaper notice of adoption of valuations/declaration of rate

Section 167(6) and 170 Government Gazette notice July 2013 Eastern Courier July 2013

Annually =July All delegations instruments made pursuant to Section 44 should be reviewed at least once in every financial year.

Section 44(6) Reviewed in 27 August 2013; January 2014

5

Date Task Act Reference Action/comment February - April Preparation of maps and technical description for revised

ward boundaries from Elector Representation Review.

12 Certification was received from the Electoral Commission on the 8 January 2013.

12/12/2013 Gazettal of Elector Representation Review and maps of changed ward boundaries

12(15) Gazette notice was published on the 7, March 2013.

6

Dataworks/Audit Committee/Audit Committee - Forward Agenda

2014 Meeting Date Reports Resolution

Number Responsible Officer

June 2014 Good Governance Assessment Program – Progress Report

A0335 4/12/13

GO

External Auditor’s Report 2012/13 Procurement Policy MP Business Service Review – Finance 3 IAM Progress Update on Business Service

Review – 1 (Dept Structure) IAM

August Risk Management Framework CP & RC Internal Revenue Review A0304 CFO Scope of External Audit for 2014/15 CFO Comparative Fleet Management 2013/14 MP Progress Update on Business Service

Review – Payroll CFO

Progress Update on Business Service Review – Accounts Payable and Accounts Receivable

CFO

Progress Update on Business Service Review – Rates

CFO

GMCS General Manager Corporate Services Gov Governance Officer MCE Manager Community Engagement CFO Chief Finance Officer MODG Manager Organisational Development and Governance IAM Internal Audit Manager MIS Manager Information Systems MP Manager Procurement and Contracts CP & RC Corporate Planning and Risk Coordinator

7

J:\GMCCS\Agendas & Minutes\Audit Committee\2014\3) 16 June 20124\4 Action List.docx

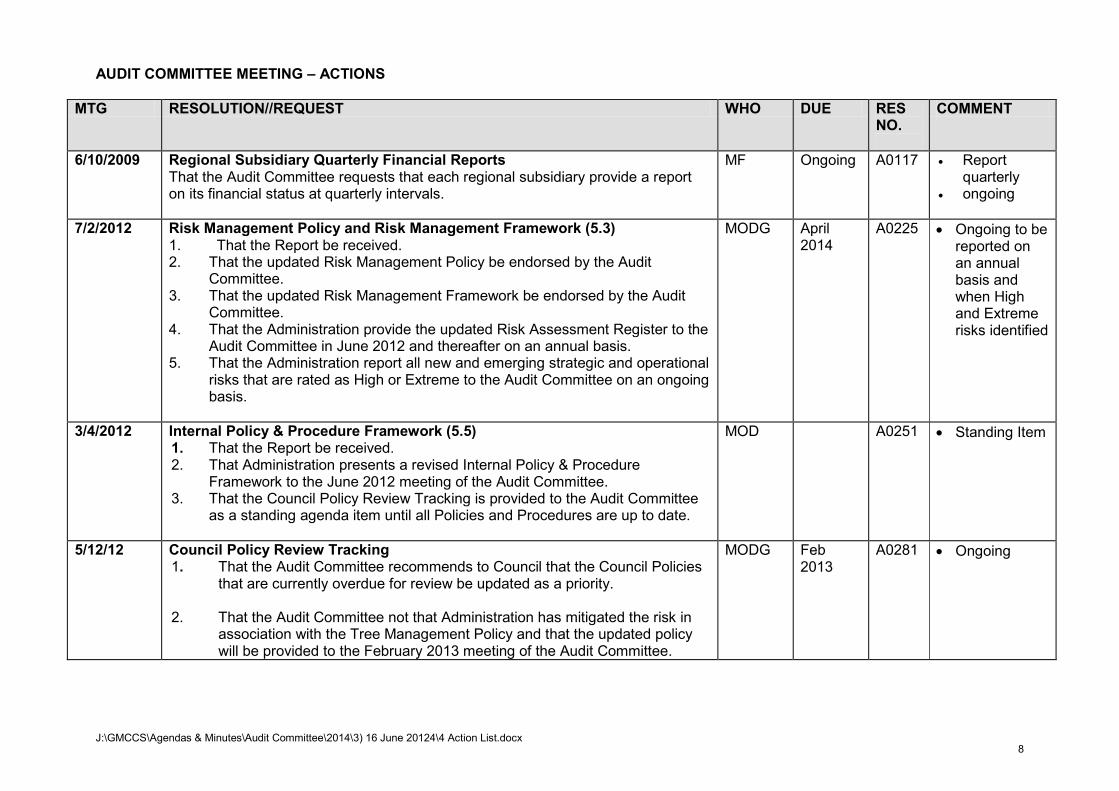

AUDIT COMMITTEE MEETING – ACTIONS

MTG RESOLUTION//REQUEST WHO DUE RES NO.

COMMENT

6/10/2009 Regional Subsidiary Quarterly Financial Reports That the Audit Committee requests that each regional subsidiary provide a report on its financial status at quarterly intervals.

MF Ongoing A0117 • Report quarterly

• ongoing

7/2/2012 Risk Management Policy and Risk Management Framework (5.3) 1. That the Report be received. 2. That the updated Risk Management Policy be endorsed by the Audit

Committee. 3. That the updated Risk Management Framework be endorsed by the Audit

Committee. 4. That the Administration provide the updated Risk Assessment Register to the

Audit Committee in June 2012 and thereafter on an annual basis. 5. That the Administration report all new and emerging strategic and operational

risks that are rated as High or Extreme to the Audit Committee on an ongoing basis.

MODG April 2014

A0225

• Ongoing to be reported on an annual basis and when High and Extreme risks identified

3/4/2012 Internal Policy & Procedure Framework (5.5) 1. That the Report be received. 2. That Administration presents a revised Internal Policy & Procedure

Framework to the June 2012 meeting of the Audit Committee. 3. That the Council Policy Review Tracking is provided to the Audit Committee

as a standing agenda item until all Policies and Procedures are up to date.

MOD A0251 • Standing Item

5/12/12 Council Policy Review Tracking 1. That the Audit Committee recommends to Council that the Council Policies

that are currently overdue for review be updated as a priority. 2. That the Audit Committee not that Administration has mitigated the risk in

association with the Tree Management Policy and that the updated policy will be provided to the February 2013 meeting of the Audit Committee.

MODG Feb 2013

A0281

• Ongoing

8

J:\GMCCS\Agendas & Minutes\Audit Committee\2014\3) 16 June 20124\4 Action List.docx

MTG RESOLUTION//REQUEST WHO DUE RES NO.

COMMENT

5/12/12 Audit Management Letter 2011/12 (5.1)

1. That the Report be received. 2. That the Audit Committee recommends to Council that measures be taken to

ensure the external Auditor findings and recommendations are achieved. 3. That a progress report be brought back to each Audit meeting commencing

2013.

CFO A0282

• Ongoing

3/4/13 Risk Register (4.4) 1. That the Report be received. 2. That the Administration continues to provide a Risk Assessment Register to

the Audit committee on an annual basis. 3. That the Administration report all new and emerging strategic and operations

risks that are rated as High or Extreme to the Audit Committee in accordance with the Risk Policy.

4. The Internal Audit Plan be revised to ensure that the priorities of the risk register have been considered.

5. That the Strategic Risk Register be developed and brought back to the Audit Committee prior to revising the internal audit plan.

MODG A0296

• Ongoing

5/6/2013

Internal Revenue Review (4.2) 1. That the Report be received. 2. That Administration provides an update on the Internal Audit Fees & Charges

Review at the August 2013 meeting of the Audit Committee. Asset Revaluation Project – Progress Report (4.4)

CFO June A0304 • Report to Audit Committee in June 2014

7/8/13 Revision of Internal Audit Plan (4.6) 1. That the Report be received. 2 That the 3-Year Internal Audit Plan be amended as follows:

2.1 Re-schedule the following business service review from 2013/14 to 2014/15:

IAM A0317 • Noted

9

J:\GMCCS\Agendas & Minutes\Audit Committee\2014\3) 16 June 20124\4 Action List.docx

MTG RESOLUTION//REQUEST WHO DUE RES NO.

COMMENT

2.1.1 Procurement & Contracts 3 Re-schedule the following six internal audit projects from 2013/14 to 2014/15:

3.1 Contract Management 3.2 Grant-Funded Programs 3.3 Enterprise Risk Management 3.4 Council Subsidiaries (subsidiary to be selected) 3.5 Customer Management 3.6 Review of Non Full-Time Equivalent (FTE) Resources

4 Completely remove the following two internal audit projects: 4.1 Asset Management II; and 4.2 Development Application Process.

5 That the Procurement Internal Audit Project currently scheduled for future

years be undertaken in 2013/14.

7/8/13 Business Service Review – Finance Department – Report 1 Department

Structure (5.1) 1. That the Report be received. 2. That the Internal Audit Report – Business Service Review Finance

Department – Report 1: Department Structure be endorsed by the Audit Committee.

3. That the Internal Audit Report – Business Service Review Finance Department - Report 1: Department Structure be presented to the 27 August 2013 meeting of Council.

4. That a Report be presented to the Audit Committee at the December 2013 meeting detailing progress of the implementation of the recommendations outlined in the Internal Audit Report – Business Service Review Finance Department – Report 1: Department Structure.

CFO Dec revised date June

A0321 • Summary in December

• Further Report to Audit Committee in June 2014

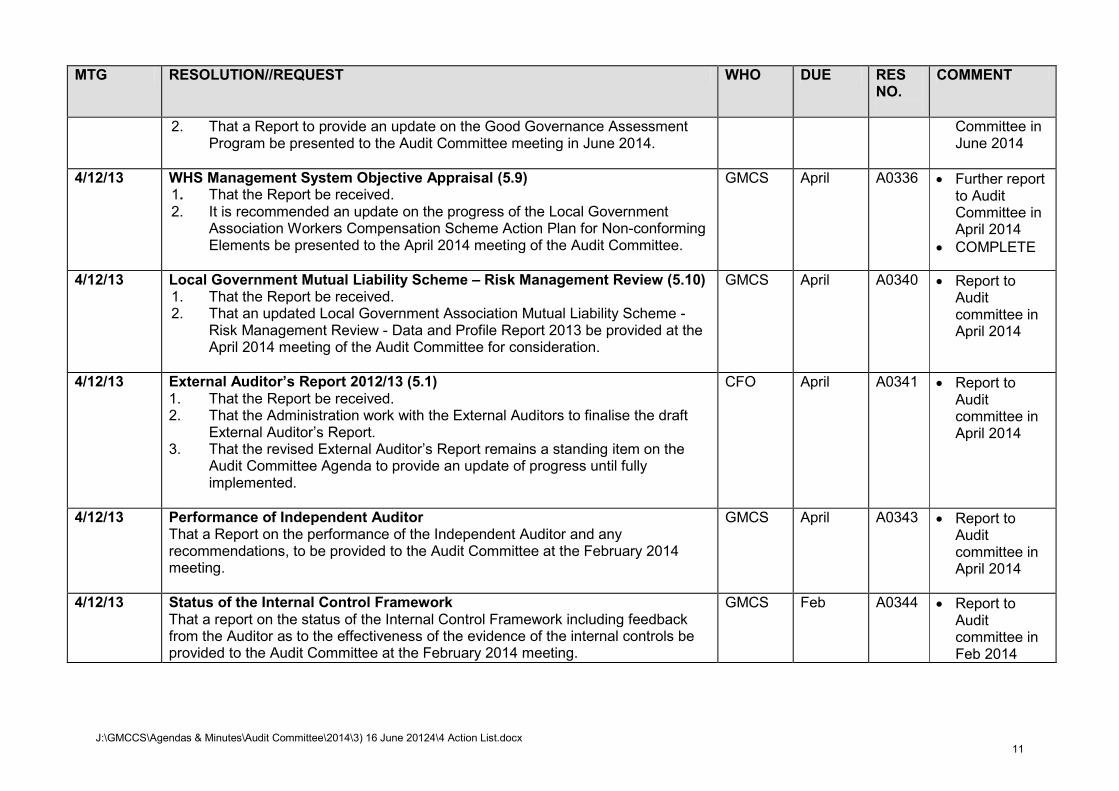

4/12/13 Good Governance Assessment Program – Progress Report (5.8) 1. That the Report be received.

GMCS June 2014

A0335

• Further report to Audit

10

J:\GMCCS\Agendas & Minutes\Audit Committee\2014\3) 16 June 20124\4 Action List.docx

MTG RESOLUTION//REQUEST WHO DUE RES NO.

COMMENT

2. That a Report to provide an update on the Good Governance Assessment Program be presented to the Audit Committee meeting in June 2014.

Committee in June 2014

4/12/13 WHS Management System Objective Appraisal (5.9) 1. That the Report be received. 2. It is recommended an update on the progress of the Local Government

Association Workers Compensation Scheme Action Plan for Non-conforming Elements be presented to the April 2014 meeting of the Audit Committee.

GMCS April A0336

• Further report to Audit Committee in April 2014

• COMPLETE

4/12/13 Local Government Mutual Liability Scheme – Risk Management Review (5.10) 1. That the Report be received. 2. That an updated Local Government Association Mutual Liability Scheme -

Risk Management Review - Data and Profile Report 2013 be provided at the April 2014 meeting of the Audit Committee for consideration.

GMCS April A0340

• Report to Audit committee in April 2014

4/12/13 External Auditor’s Report 2012/13 (5.1) 1. That the Report be received. 2. That the Administration work with the External Auditors to finalise the draft

External Auditor’s Report. 3. That the revised External Auditor’s Report remains a standing item on the

Audit Committee Agenda to provide an update of progress until fully implemented.

CFO April A0341 • Report to Audit committee in April 2014

4/12/13 Performance of Independent Auditor That a Report on the performance of the Independent Auditor and any recommendations, to be provided to the Audit Committee at the February 2014 meeting.

GMCS April

A0343

• Report to Audit committee in April 2014

4/12/13

Status of the Internal Control Framework That a report on the status of the Internal Control Framework including feedback from the Auditor as to the effectiveness of the evidence of the internal controls be provided to the Audit Committee at the February 2014 meeting.

GMCS Feb A0344 • Report to Audit committee in Feb 2014

11

J:\GMCCS\Agendas & Minutes\Audit Committee\2014\3) 16 June 20124\4 Action List.docx

MTG RESOLUTION//REQUEST WHO DUE RES NO.

COMMENT

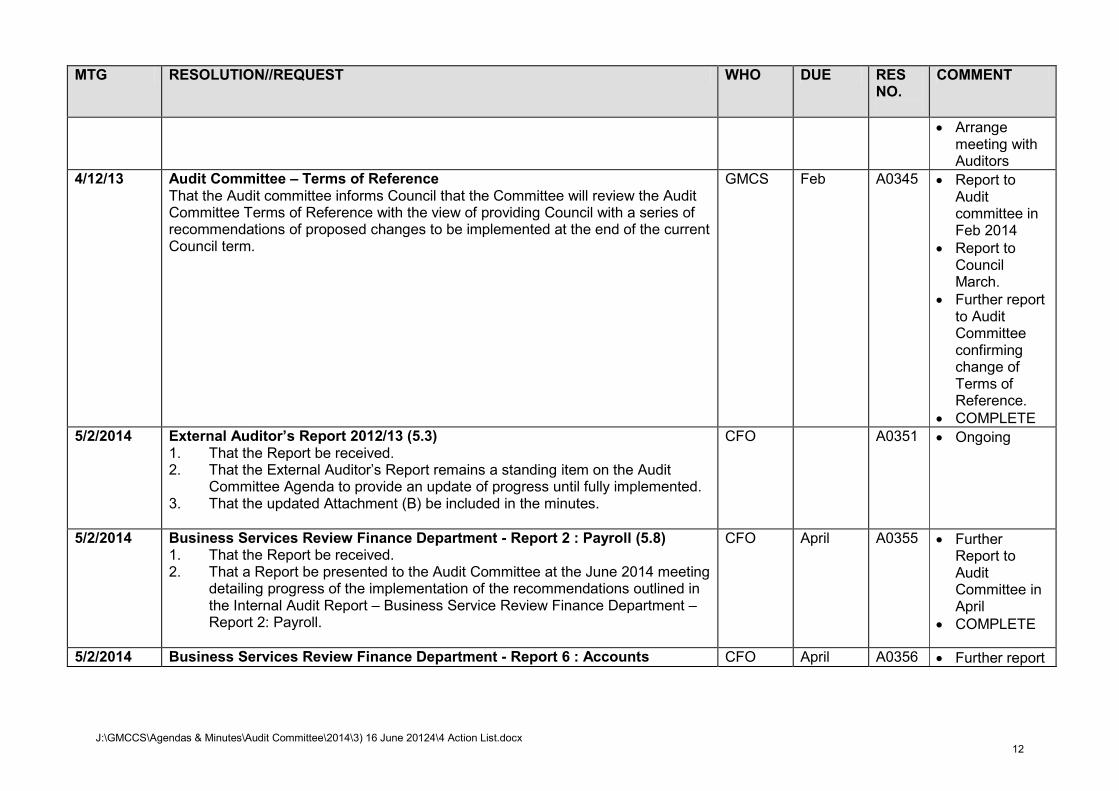

• Arrange meeting with Auditors

4/12/13 Audit Committee – Terms of Reference That the Audit committee informs Council that the Committee will review the Audit Committee Terms of Reference with the view of providing Council with a series of recommendations of proposed changes to be implemented at the end of the current Council term.

GMCS Feb A0345

• Report to Audit committee in Feb 2014

• Report to Council March.

• Further report to Audit Committee confirming change of Terms of Reference.

• COMPLETE 5/2/2014 External Auditor’s Report 2012/13 (5.3)

1. That the Report be received. 2. That the External Auditor’s Report remains a standing item on the Audit

Committee Agenda to provide an update of progress until fully implemented. 3. That the updated Attachment (B) be included in the minutes.

CFO A0351 • Ongoing

5/2/2014 Business Services Review Finance Department - Report 2 : Payroll (5.8) 1. That the Report be received. 2. That a Report be presented to the Audit Committee at the June 2014 meeting

detailing progress of the implementation of the recommendations outlined in the Internal Audit Report – Business Service Review Finance Department – Report 2: Payroll.

CFO April A0355 • Further Report to Audit Committee in April

• COMPLETE

5/2/2014 Business Services Review Finance Department - Report 6 : Accounts CFO April A0356 • Further report

12

J:\GMCCS\Agendas & Minutes\Audit Committee\2014\3) 16 June 20124\4 Action List.docx

MTG RESOLUTION//REQUEST WHO DUE RES NO.

COMMENT

Receivable and Account Payable Functions (5.9) 1. That the Report be received. 2. That a Report be presented to the Audit Committee at the June 2014 meeting

detailing progress of the implementation of the recommendations outlined in the Internal Audit Report – Business Service Review Finance Department – Report 6: Accounts Receivable and Accounts Payable Functions.

to Audit Committee in April

• COMPLETE

5/2/2014 Performance of Independent Auditor (6.1) That Pursuant to section 90(2) of the Local Government Act, 1999 the Committee orders that the public be excluded, with the exception of the Audit Committee Members, the Elected Members of the City of Burnside, the Acting Chief Executive Officer, the Acting General Manager, Corporate Services; the General Manager, Urban Services, the Acting Chief Financial Officer and the Executive Officer on the basis that it will receive and consider the Item 6.1 Performance of Independent Auditor and that the Committee is satisfied that the principle that the meeting should be conducted in a place open to the public has been outweighed in relation to the matter because pursuant to section 90(3)(d) of the Act, on the basis that it contains commercial information of a confidential nature (not being a trade secret) the disclosure of which could reasonably be expected to prejudice the commercial position of the person which supplied the information or confer a commercial advantage on a third party, and to do so would be contrary to the public interest. 1. Confidential Resolution. 2. Confidential Resolution. A0359 1. Pursuant to Section 91(7) and (9) of the Local Government Act, 1999, the Committee orders that: 1.1 the Report, Minutes and Attachments remain confidential on the basis that they contain commercial information of a confidential nature (not being a trade secret) the disclosure of which could reasonably be expected to prejudice the

GMCS A0358 • Further Report to Audit Committee

13

J:\GMCCS\Agendas & Minutes\Audit Committee\2014\3) 16 June 20124\4 Action List.docx

MTG RESOLUTION//REQUEST WHO DUE RES NO.

COMMENT

commercial position of the person which supplied the information and to do so would be contrary to the public interest. 1.2 the Report, Minutes and Attachments will not be available for public inspection for the period of five years at which time this order will be revoked/reviewed by the Audit Committee / Chief Executive Officer. 2. That if:

2.1 the period in respect of any order made under Section 91(7) of the Local Government Act 1999 lapses; or

2.2 Council resolves to revoke an order made under Section 91(7) of

the Local Government Act 1999; or the CEO determines pursuant to delegated authority that the order be revoked any discussions of Committee on that matter and any recording of those discussions are to no longer be treated as confidential.

15/4/2014 Adj to 16/4/2014

Audit Committee Terms of Reference (Operational) (5.1) 1. That the Report be received.

2. That Members note the amended Terms of Reference for the City of

Burnside Audit Committee.

3. The Audit Committee recommends to Council that the Terms of Reference be amended as follows: 3.1 Item 8.1 – The Committee shall meet at 6 pm on a day to be specified

by the Audit Committee in the third week of February, April, June, August, October and November each year or as otherwise determined by Council or the Audit Committee (whether as the result of a motion upon notice or an Officer’s Report to Council.)

3.2 Items 11.2 and 11.2.1 of the Terms of Reference to be amended by

GMCS

A0361 • COMPLETE

14

J:\GMCCS\Agendas & Minutes\Audit Committee\2014\3) 16 June 20124\4 Action List.docx

MTG RESOLUTION//REQUEST WHO DUE RES NO.

COMMENT

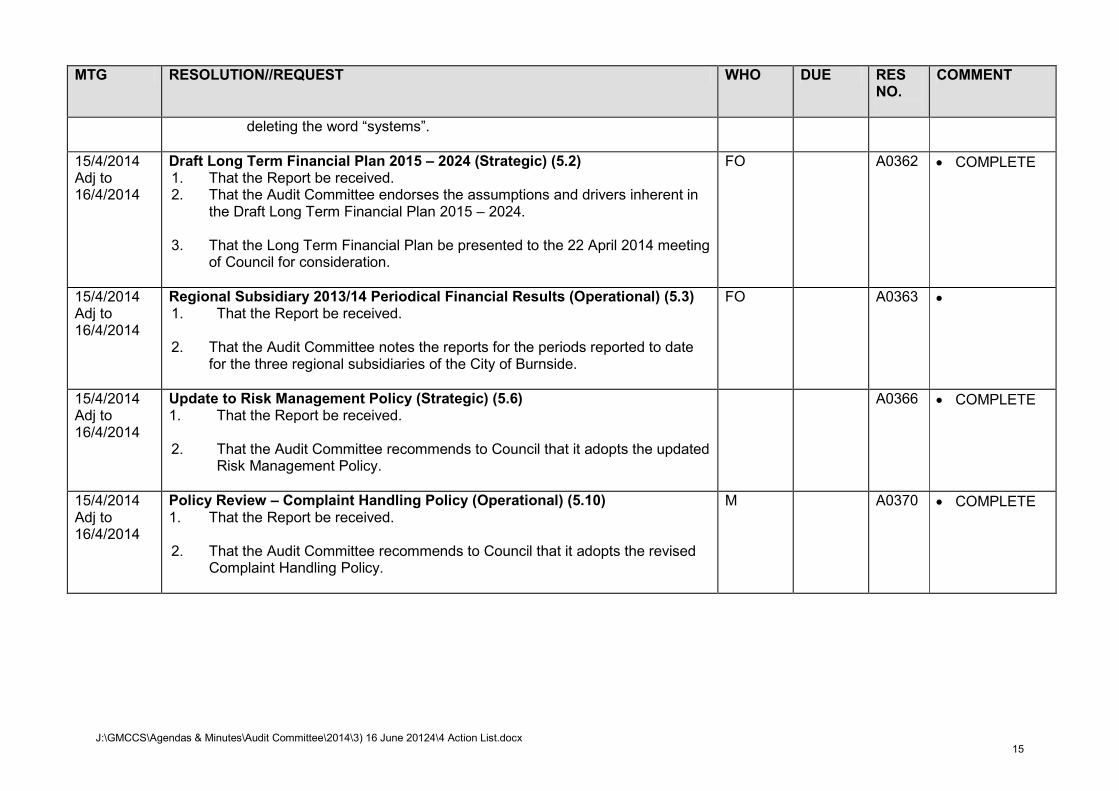

deleting the word “systems”.

15/4/2014 Adj to 16/4/2014

Draft Long Term Financial Plan 2015 – 2024 (Strategic) (5.2) 1. That the Report be received. 2. That the Audit Committee endorses the assumptions and drivers inherent in

the Draft Long Term Financial Plan 2015 – 2024. 3. That the Long Term Financial Plan be presented to the 22 April 2014 meeting

of Council for consideration.

FO A0362 • COMPLETE

15/4/2014 Adj to 16/4/2014

Regional Subsidiary 2013/14 Periodical Financial Results (Operational) (5.3) 1. That the Report be received.

2. That the Audit Committee notes the reports for the periods reported to date

for the three regional subsidiaries of the City of Burnside.

FO A0363

•

15/4/2014 Adj to 16/4/2014

Update to Risk Management Policy (Strategic) (5.6) 1. That the Report be received. 2. That the Audit Committee recommends to Council that it adopts the updated

Risk Management Policy.

A0366 • COMPLETE

15/4/2014 Adj to 16/4/2014

Policy Review – Complaint Handling Policy (Operational) (5.10) 1. That the Report be received. 2. That the Audit Committee recommends to Council that it adopts the revised

Complaint Handling Policy.

M A0370 • COMPLETE

15

INTERNAL AUDIT – STATUS REPORT (June 2014)

4 Internal Audit - Status Report Jun 14- PD FINAL .doc 1

The Internal Audit – Status Report provides a summary of the progress of internal audit projects (completed and in progress).

No. Projects Completed Date

Audit Committee Date

Status

2012-13 Internal Audit Projects 1 12-05 Business Service Review – Library,

Learning & Volunteers Apr 2012 Jun 2012

Feb 2013 Aug 2013

Status on the outstanding audit recommendations are provided below : • The Manager – Library, Learning and Volunteers has commenced developing a

succession plan. How ever, this w ill be f inalised together w ith the development of a standard template succession plan by the People and Culture Department for all departments across Council (w hich is expected by December 2014).

• The revision of w orkf low s for each core service w ill be undertaken w hen the extra w orkload due to 1LMS has been embedded into exist ing pract ices (w hich is expected by August 2014).

2 12-06 Internal Policy & Procedure Framew ork Mar 2012 Apr 2012 We w ere advised by the Execut ive Team that the audit recommendations w ere fully implemented.

3 12-07 Long-Term Financial Plan May 2012 Aug 2012 We w ere advised by the Execut ive Team that the audit recommendations w ere fully implemented.

4 12-08 Management of Consultancies May 2012 To be tabled. This audit report w ill be presented at a future Audit Committee meeting. 5 12-10 Fees and Charges Review Aug 2012 Jun 2013 We w ere advised by the Execut ive Team that the audit recommendations w ere fully

implemented. 6 12-11 External Compliance Jul 2012 To be tabled. This audit report w ill be presented at a future Audit Committee meeting. 7 13-01 Business Service Review – Finance 1

(Department Structure) Dec 2012 Aug 2013

June 2014 New structure has been implemented w ith the except ion of the Finance Business Partner role (delayed due to a lengthy WorkCover claim) and Finance Trainee role (postponed due to funding a temporary business support role). Recruitment for these tw o posit ions is planned for July 2014. Progress report presented to the Audit Committee in June 2014.

8 13-01 Business Service Review – Finance 2 (Payroll)

Dec 2012 Jun 2013 Aug 2013 Feb 2014

Internal Audit completed a follow -up on this project , which w as reported to the Audit Committee in April 2014. The outstanding recommendations w ill be captured under future follow -up review s w hich w ill occur quarterly.

9 13-01 Business Service Review – Finance 3 (Reconciliat ions, Processing of Journals, GST, FBT and Finance Systems)

Dec 2012 June 2014 Good progress made and many recommendations have been implemented. A temporary f inance resource has been engaged in this area. This report w ill be presented to the Audit Committee in June 2014.

10 13-01 Business Service Review – Finance 4 (Performance, Operat ional, Financial & Compliance Management)

Dec 2012 To be tabled. Good progress made and a number of recommendations have been implemented. Responses w ere drafted w ith assistance from Organisat ional Development and Governance and Procurement and Contracts. Management responses w ill be f inalised w hen the Strategic & Corporate Planner returns from maternity leave in July 2014.

11 13-01 Business Service Review – Finance 5 Dec 2012 To be tabled. Good progress made on t he report ing and presentat ion of the Annual Business Plan and

16

INTERNAL AUDIT – STATUS REPORT (June 2014)

4 Internal Audit - Status Report Jun 14- PD FINAL .doc 2

No. Projects Completed Date

Audit Committee Date

Status

(Financial Report ing) Long-Term Financial Plan at Workshops, Council and Audit Committee meetings. Work is ongoing as the restructure of the Finance Department is implemented. Management responses w ill be drafted in July 2014.

12 13-01 Business Service Review – Finance 6 (Accounts Receivable & Accounts Payable)

Dec 2012 Jun 2013 Aug 2013 Feb 2014

Internal Audit completed a follow -up on this project, which w as reported to the Audit Committee in April 2014. The outstanding recommendations w ill be captured under future follow -up review s w hich w ill occur quarterly.

13 13-01 Business Service Review – Finance 7 (Rates)

Dec 2012 Aug 2013 Feb 2014

The proposed audit recommendations w ere endorsed by the Execut ive Team, approved by Council and fully implemented. Internal Audit w ill conduct a follow -up review to be presented to the Audit Committee in August 2014.

14 13-02 Business Service Review - Engineering Services

Mar 2013 Feb 2014 The Engineering Services Department has made small advances in improvement areas since the last report . • A start has been made on the f low chart for services w ith City Development and

Safety. • Capitalisat ion of w ages included in the capital program. • Policy compliance review w as undertaken as part of the annual policy review and

primarily, through w ork on creat ion of the new Streetscape Strategy. • Succession planning has been incorporated into the latest vacancy. Areas of immediate focus include: • Report ing the scheduling of capital w orks to the Execut ive Team. • Formalising the monthly capital w orks report to the Execut ive Team. • Development relat ionship / assessment f low chart.

15 13-03 Project Management – Burnside Sw imming Centre

May 2013 Jun 2013 * We w ere advised by the Strategic Projects Off icer in October 2013 that the recommendations from this report w ere implemented.

16 13-04 Business Service Review – Development Services

Sep 2013 To be tabled. A w orkshop w as scheduled on 28 May for the department’s manager and team leaders to discuss the report and formulate management responses. The responses w ill be presented to the General Manager - Community and Development Services for f inalisat ion.

2013-14 Internal Audit Projects 17 14-01 Project Management – Glenunga

Community Hub Jul 2013 Jul 2013 * We w ere advised by the Strategic Projects Off icer in October 2013 that the

recommendations from this report w ere implemented. 18 14-04 Business Service Review –

Organisat ional Development Dec 2013 To be tabled. The Manager – People an Culture is preparing management responses to the audit report

w hich is expected to be submitted to the General Manager – Corporate Services by July 2014.

19 14-04 Business Service Review –Governance Dec 2013 To be tabled. 20 14-05 Business Service Review – Off ice of the Nov 2013 To be tabled. This project is now expanded to include the Community Engagement and Communicat ions

17

INTERNAL AUDIT – STATUS REPORT (June 2014)

4 Internal Audit - Status Report Jun 14- PD FINAL .doc 3

No. Projects Completed Date

Audit Committee Date

Status

CEO Team. A revised draft report w ith the expanded scope is expected by June 2014. 21 14-06 Enterprise Risk Management Dec 2013 To be tabled. The Manager – People and Culture is preparing management responses to the audit report

w hich is expected to be submitted to the General Manager – Corporate Services by July 2014.

22 14-07 Work Health & Safety Dec 2013 To be tabled. The Manager – People and Culture is preparing management responses to the audit report w hich is expected to be submitted to the General Manager – Corporate Services by July 2014.

23 14-08 Follow -Up on Business Service Review of the Finance Department – Accounts Payable and Accounts Receivable Funct ions

Feb 2014 April 2014 The majority of audit recommendations w ere implemented. The outstanding recommendations w ill be captured under future follow -up review s w hich w ill occur quarterly.

24 14-09 Follow -Up on Business Service Review of the Finance Department – Payroll Funct ion

Feb 2014 April 2014 The majority of audit recommendations w ere implemented. The outstanding recommendations w ill be captured under future follow -up review s w hich w ill occur quarterly.

25 14-10 Financial Internal Controls – Procurement & Purchasing

May 2014 n/a A draft audit report w as presented to the Execut ive Team in May 2014. A revised draft report is being review ed by management. T he draf t report w ill then return to the Execut ive Team for conf irmation in June 2014.

26 14-12 Business Service Review – Community Services

n/a n/a This project is present ly at planning stage.

* Direct to Council.

18

J:\GMCCS\Agendas & Minutes\Audit Committee\2014\3) 16 June 20124\4 Council Policy Review Tracking table for Audit Committee (ECM 1577677).docx 1

COUNCIL POLICY REVIEW TRACKING

As at 27 May 2014 As per Audit Committee Resolution A0251, 3/4/12 in part: That the Council Policy Review Tracking is provided to the Audit Committee as a standing agenda item until all Policies and Procedures are up to date.

KEY: GM CS = General Manager Corporate Services GM C&DS = General Manager Community & Development Services GM US = General Manager Urban Services M OD&G = Manager People & Culture CEO = Chief Executive Officer Review date or adopted date = date of Council Meeting NFA = no further action required Note all policies to be reviewed annually. As requested at the December 2012 meeting of the Audit Committee, an additional column to indicate where the policy is required under the Local Government Act has been added to this table. Policy title Required

under LG Act Responsibility Last

reviewed / adopted

Next review Date

Progress Comments or completed date

Access to development documentation

GM C&DS

25/09/2012 C8873

22/10/2013 C9447

October 2014 Last review completed October 2013

Aged Care

GM C&DS

28/08/2012 C8842

27/08/2013 C9360

Aug 2014 Last review completed August 2013

19

J:\GMCCS\Agendas & Minutes\Audit Committee\2014\3) 16 June 20124\4 Council Policy Review Tracking table for Audit Committee (ECM 1577677).docx 2

Policy title Required under LG Act

Responsibility Last reviewed / adopted

Next review Date

Progress Comments or completed date

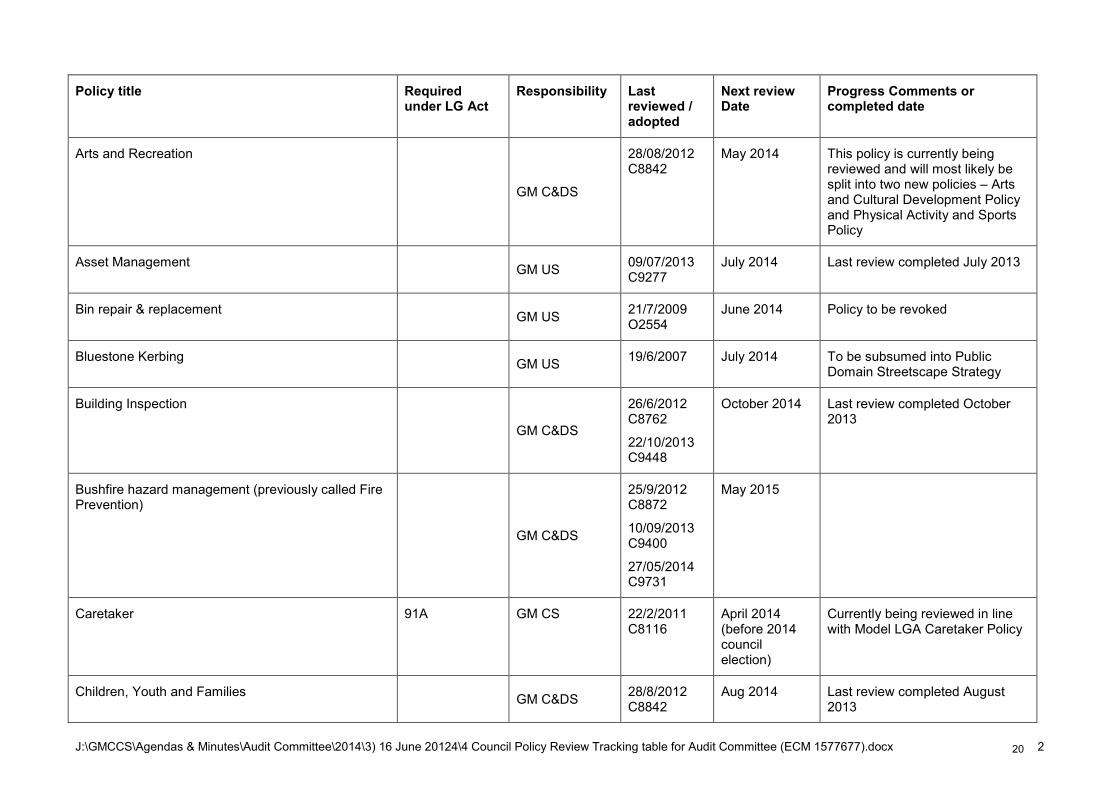

Arts and Recreation

GM C&DS

28/08/2012 C8842

May 2014 This policy is currently being reviewed and will most likely be split into two new policies – Arts and Cultural Development Policy and Physical Activity and Sports Policy

Asset Management GM US 09/07/2013 C9277

July 2014 Last review completed July 2013

Bin repair & replacement GM US 21/7/2009 O2554

June 2014 Policy to be revoked

Bluestone Kerbing GM US 19/6/2007 July 2014 To be subsumed into Public Domain Streetscape Strategy

Building Inspection

GM C&DS

26/6/2012 C8762

22/10/2013 C9448

October 2014 Last review completed October 2013

Bushfire hazard management (previously called Fire Prevention)

GM C&DS

25/9/2012 C8872

10/09/2013 C9400

27/05/2014 C9731

May 2015

Caretaker 91A GM CS 22/2/2011 C8116

April 2014 (before 2014 council election)

Currently being reviewed in line with Model LGA Caretaker Policy

Children, Youth and Families GM C&DS 28/8/2012 C8842

Aug 2014 Last review completed August 2013

20

J:\GMCCS\Agendas & Minutes\Audit Committee\2014\3) 16 June 20124\4 Council Policy Review Tracking table for Audit Committee (ECM 1577677).docx 3

Policy title Required under LG Act

Responsibility Last reviewed / adopted

Next review Date

Progress Comments or completed date

27/08/2013 C9361

City of Burnside Flag Flying

GM US

17/2/2009 CS1654

13/08/2013 C9333

August 2014 Last review completed August 2013

Closed circuit television (CCTV) GM CS 27/7/2010 C7948

July 2014 Review currently being undertaken

Code of Conduct for Council Members (previously Code of Conduct for Elected Members`) (refer also Complaint Handling Procedures for Council Members)

63 GM CS 25/10/2011 C8465

Council review / adoption no longer required.

Legislated Code 1/9/2013 – Parliament reviews, not Council

Code of Conduct for Council Employees (previously Code of Conduct for Employees, Staff & Associates)

110 GM CS 25/11/2011

24/09/2013 C9409

Employees, Staff & Associates – Gifts and Benefits Policy adopted 24/09/2013 C9409 and 2.7 amended in the Code

Legislated Code 12/2/2014 – Parliament reviews, not Council

Any specific clauses not included in mandated code will need to be included in either an existing or new Protocol

21

J:\GMCCS\Agendas & Minutes\Audit Committee\2014\3) 16 June 20124\4 Council Policy Review Tracking table for Audit Committee (ECM 1577677).docx 4

Policy title Required under LG Act

Responsibility Last reviewed / adopted

Next review Date

Progress Comments or completed date

Council review / adoption no longer required.

Code of Practice – Access to Meetings and Documents

Public consultation required. S.92.

GM CS 9/8/2011 Nov 2015 (within 12 months of election)

Last reviewed August 2011 (within12 months of last election)

Code of Practice – Meeting Procedures Meeting Regulations 7(2); Annual review mandatory.

GM CS

29/01/2013 C8998

July 2014

Community Gardens GM US 3/2/2010 S7313

May 2014 Last reviewed February 2010

Community Grants

GM C&DS

09/07/2013 C9274

8/04/2014 C9659

April 2015 Last reviewed April 2014

Complaint Handling 270(a1)(b)

GM C&DS

22/5/2012 C8719

15/04/2014 A0370

13/05/2014 C9710

May 2015

Complaint Handling Procedures for Council Members 63 GM CS 27/05/2014 May 2015

22

J:\GMCCS\Agendas & Minutes\Audit Committee\2014\3) 16 June 20124\4 Council Policy Review Tracking table for Audit Committee (ECM 1577677).docx 5

Policy title Required under LG Act

Responsibility Last reviewed / adopted

Next review Date

Progress Comments or completed date

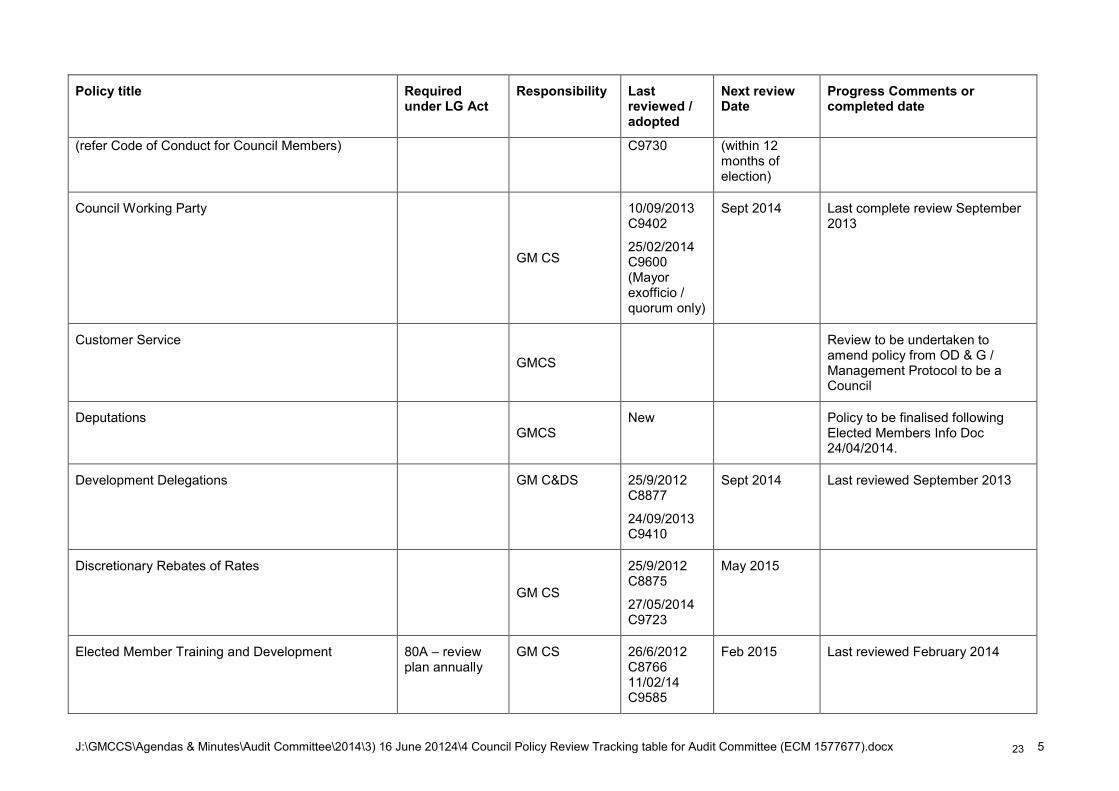

(refer Code of Conduct for Council Members) C9730 (within 12 months of election)

Council Working Party

GM CS

10/09/2013 C9402

25/02/2014 C9600 (Mayor exofficio / quorum only)

Sept 2014 Last complete review September 2013

Customer Service

GMCS

Review to be undertaken to amend policy from OD & G / Management Protocol to be a Council

Deputations GMCS

New Policy to be finalised following Elected Members Info Doc 24/04/2014.

Development Delegations GM C&DS 25/9/2012 C8877

24/09/2013 C9410

Sept 2014 Last reviewed September 2013

Discretionary Rebates of Rates

GM CS

25/9/2012 C8875

27/05/2014 C9723

May 2015

Elected Member Training and Development 80A – review plan annually

GM CS 26/6/2012 C8766 11/02/14 C9585

Feb 2015 Last reviewed February 2014

23

J:\GMCCS\Agendas & Minutes\Audit Committee\2014\3) 16 June 20124\4 Council Policy Review Tracking table for Audit Committee (ECM 1577677).docx 6

Policy title Required under LG Act

Responsibility Last reviewed / adopted

Next review Date

Progress Comments or completed date

Elected Members (incorporating Elected Members Room and Mayors Parlour Policy)

GM CS 19/6/2007 F1565

Feb 2011 (CEO)

27/05/2014 C9732

May 2015

Elected Members’ Allowances and Benefits 76(9) Allowances table updated annually.

S.77(1)(b) policy lapses at each election.

GM CS 12/11/2012

12/11/2013

November 2014 (Allowances)

Dec 2014 (Complete Policy)

Last complete review November 2013

Election signs GM CS 22/2/2011

27/05/2014 C9733

May 2015

Employees, Staff and Associates – Gifts and Benefits (refer also Code of Conduct for Council Employees)

CEO 24/09/2013 C9409

27/05/2014 C9734

May 2015

Environment GM US 23/04/2013 C9148

April 2014 Last reviewed April 2013

Footpath GM US 14/8/2012 C8823

10/09/2013 C9401

July 2014 To be subsumed into Public Domain Streetscape Strategy

24

J:\GMCCS\Agendas & Minutes\Audit Committee\2014\3) 16 June 20124\4 Council Policy Review Tracking table for Audit Committee (ECM 1577677).docx 7

Policy title Required under LG Act

Responsibility Last reviewed / adopted

Next review Date

Progress Comments or completed date

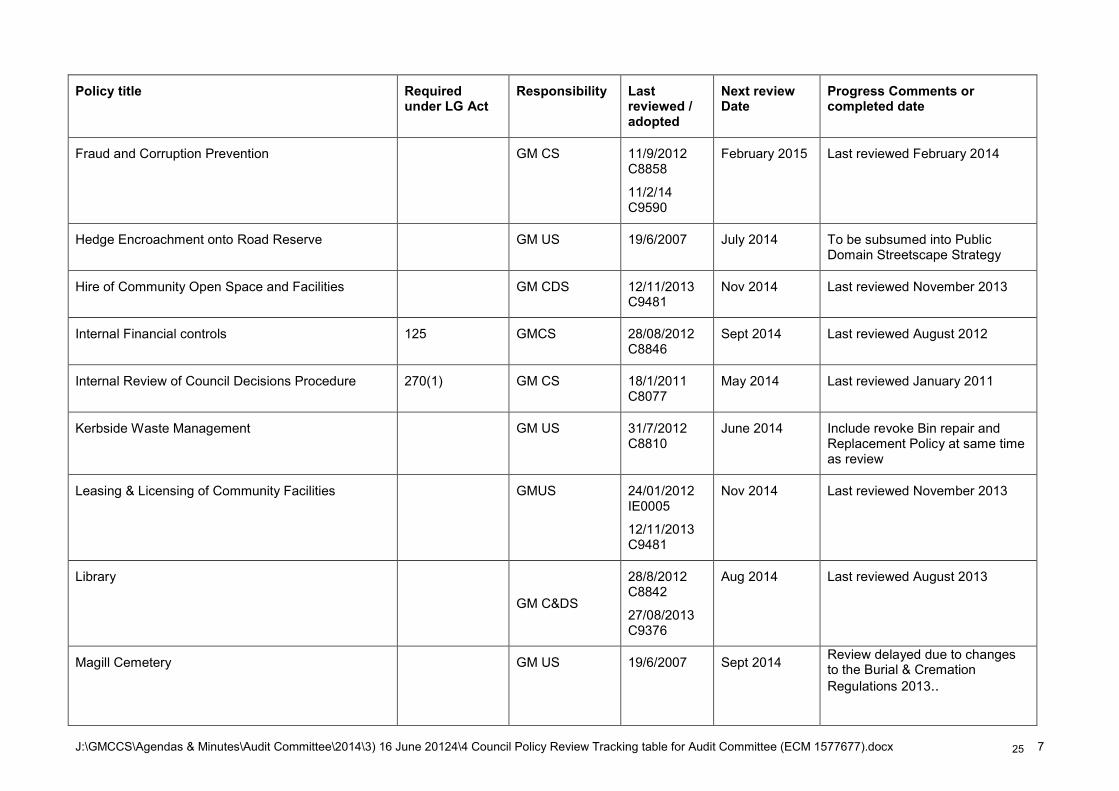

Fraud and Corruption Prevention GM CS 11/9/2012 C8858

11/2/14 C9590

February 2015 Last reviewed February 2014

Hedge Encroachment onto Road Reserve GM US 19/6/2007 July 2014 To be subsumed into Public Domain Streetscape Strategy

Hire of Community Open Space and Facilities GM CDS 12/11/2013 C9481

Nov 2014 Last reviewed November 2013

Internal Financial controls 125 GMCS 28/08/2012 C8846

Sept 2014 Last reviewed August 2012

Internal Review of Council Decisions Procedure 270(1) GM CS 18/1/2011 C8077

May 2014 Last reviewed January 2011

Kerbside Waste Management GM US 31/7/2012 C8810

June 2014 Include revoke Bin repair and Replacement Policy at same time as review

Leasing & Licensing of Community Facilities

GMUS 24/01/2012 IE0005

12/11/2013 C9481

Nov 2014 Last reviewed November 2013

Library

GM C&DS

28/8/2012 C8842

27/08/2013 C9376

Aug 2014 Last reviewed August 2013

Magill Cemetery GM US 19/6/2007 Sept 2014 Review delayed due to changes to the Burial & Cremation Regulations 2013..

25

J:\GMCCS\Agendas & Minutes\Audit Committee\2014\3) 16 June 20124\4 Council Policy Review Tracking table for Audit Committee (ECM 1577677).docx 8

Policy title Required under LG Act

Responsibility Last reviewed / adopted

Next review Date

Progress Comments or completed date

Media

GM C&DS

27/11/2012, C8941

10/09/2013

C9391

Sept 2014 Last reviewed September 2013

Naming of Public Places (formerly Naming of Roads and Public Reserves)

219(5) GM US 27/7/2010 C7942

22/04/2014 C9696

April 2015 Last reviewed April 2014

Occupational Health, Safety & Welfare and Report on Occupational Health Experience & Performance

GM CS 19/6/2007 June 2014 This is to be revoked as it is covered by other formal reporting processes.

Open Space (includes Open Space Reserves Fund)

GM US 20/10/2009 F1732

Oct 2014 Last reviewed October 2009

Order Making May need public consultation. S.259(5)

GM C&DS 25/9/2012 C8876

12/11/13 C9479

Nov 2014 Last reviewed November 2013

Parking

GM C&DS

10/7/2012, C8787

23/07/2013 C9318

11/03/2014 C9623

March 2015 Last reviewed March 2014

Petitions GM CS

09/08/2011 May 2014 Review as part of Review of Code of Practice Access to documents. Policy to be finalised following Elected Members Info Doc

26

J:\GMCCS\Agendas & Minutes\Audit Committee\2014\3) 16 June 20124\4 Council Policy Review Tracking table for Audit Committee (ECM 1577677).docx 9

Policy title Required under LG Act

Responsibility Last reviewed / adopted

Next review Date

Progress Comments or completed date

24/04/2014.

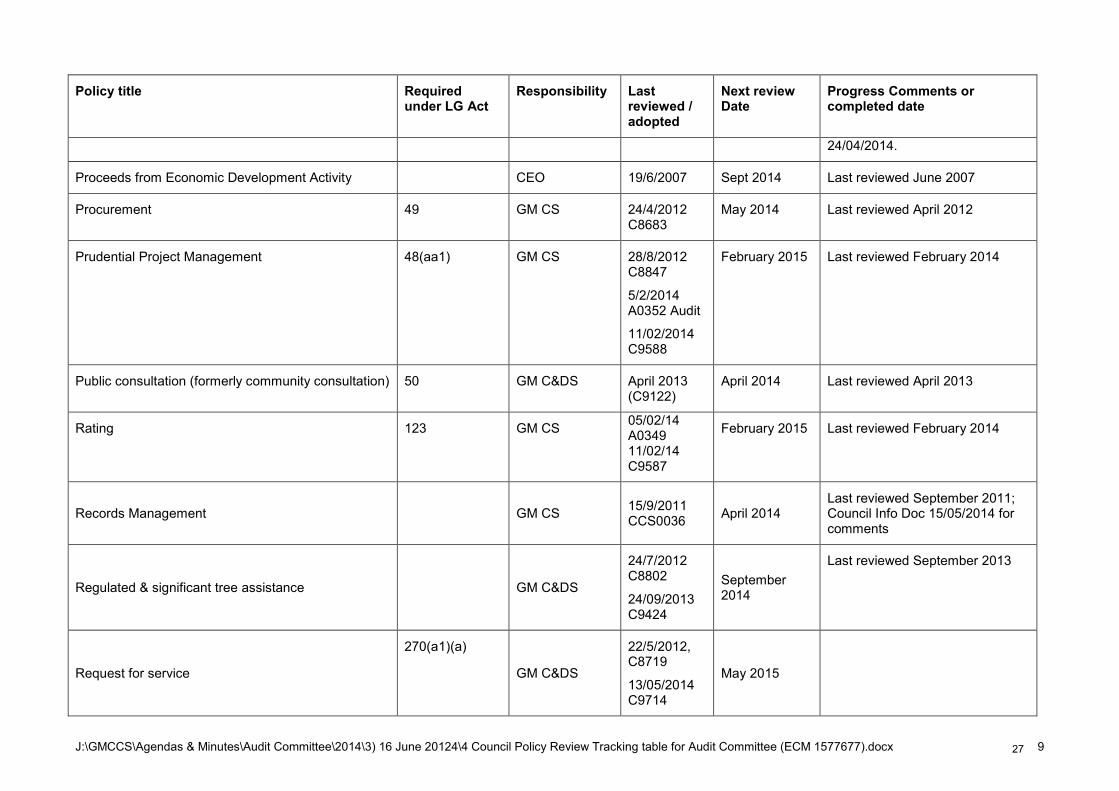

Proceeds from Economic Development Activity CEO 19/6/2007 Sept 2014 Last reviewed June 2007

Procurement 49 GM CS 24/4/2012 C8683

May 2014 Last reviewed April 2012

Prudential Project Management 48(aa1) GM CS 28/8/2012 C8847

5/2/2014 A0352 Audit

11/02/2014 C9588

February 2015 Last reviewed February 2014

Public consultation (formerly community consultation) 50 GM C&DS April 2013 (C9122)

April 2014 Last reviewed April 2013

Rating 123 GM CS 05/02/14 A0349 11/02/14 C9587

February 2015 Last reviewed February 2014

Records Management

GM CS 15/9/2011 CCS0036 April 2014

Last reviewed September 2011; Council Info Doc 15/05/2014 for comments

Regulated & significant tree assistance

GM C&DS

24/7/2012 C8802

24/09/2013 C9424

September 2014

Last reviewed September 2013

Request for service

270(a1)(a)

GM C&DS

22/5/2012, C8719

13/05/2014 C9714

May 2015

27

J:\GMCCS\Agendas & Minutes\Audit Committee\2014\3) 16 June 20124\4 Council Policy Review Tracking table for Audit Committee (ECM 1577677).docx 10

Policy title Required under LG Act

Responsibility Last reviewed / adopted

Next review Date

Progress Comments or completed date

Risk Management

134(4)(b)

M P&C

14/02/2012 C8579

15/04/2014 A0366

13/05/2014 C9715

May 2015

Road & Traffic Management

GM US

12/03/2013 C9078

13/08/2013

C9334

August 2014 Last reviewed August 2013

Social media GM C&DS 25/9/2012, C8842

March 2014 Last reviewed September 2012

Sponsorship GM C&DS 28/08/2012 C8842

10/09/2013 C9392

Sept 2014 Last reviewed September 2013

Street Numbering GMCS Council report to t/f from Management Protocol to Council Policy

Swimming Pool 71AA Development Act 1993

GM C&DS 8/04/2014 C9664

April 2015 Last reviewed April 2014

Telecommunications Facilities on Council Land GM US 19/6/2007 Sept 2014 Last reviewed June 2007

Tree Management

GM US

26/02/2013 C9065 reviewed but not adopted

May 2015

28

J:\GMCCS\Agendas & Minutes\Audit Committee\2014\3) 16 June 20124\4 Council Policy Review Tracking table for Audit Committee (ECM 1577677).docx 11

Policy title Required under LG Act

Responsibility Last reviewed / adopted

Next review Date

Progress Comments or completed date

27/05/2014 C9735

Use of Road Reserves for Commercial Purposes

GM C&DS

28/8/2012, C8842

8/10/2013 C9437

25/02/2014 C9612

February 2015 Last reviewed February 2014

Vehicles GM CS 11/10/2011 CCS0044

May 2014 Last reviewed October 2011

Verge Development GM US 19/6/2007 July 2014 To be subsumed into Public Domain Streetscape Strategy

Volunteers

GM C&DS

25/9/2012, C8876

27/08/2013

C9362

August 2014 Last reviewed August 2013

Ward Forums GM C&DS 11/9/2012, C8858

27/05/2014 C9724

May 2015

Water sensitive urban design GM US 27/9/2011 PHI0064

July 2014 Last reviewed September 2011

Watercourse Management GM US 28/05/2013 C9188

May 2014 Last reviewed May 2013

Whistleblower Protection GMUS 23/04/2013 C9140

February 2015 Last reviewed February 2014

29

J:\GMCCS\Agendas & Minutes\Audit Committee\2014\3) 16 June 20124\4 Council Policy Review Tracking table for Audit Committee (ECM 1577677).docx 12

Policy title Required under LG Act

Responsibility Last reviewed / adopted

Next review Date

Progress Comments or completed date

GMCDS

GMUS

14/02/2014 C9586

30

Audit Committee Item 5.1 16 June 2014 Item No: 5.1 To: Audit Committee Date: 16 June 2014 Author: Louise Miller Frost – General Manager, Corporate Services General Manager and Division

Louise Miller Frost – General Manager, Corporate Services

Contact: 8366 4205 Subject: AUDIT COMMITTEE TERMS OF REFERENCE (STRATEGIC) Attachments: A. Audit Committee Terms of Reference Prev. Resolution: C8044, 14/12/10

C8220, 27/4/11 C8496, 22/11/11 A0279, 7/8/12 C8840, 28/8/12 C9530, 10/12/13 A0350, 5/2/14 C9616, 25/2/14 C9621, 11/3/14 C9622, 11/3/14 C9709, 13/5/14

Officer’s Recommendation

1. That the Report be received.

2. That members note the amended Terms of Reference for the City of Burnside Audit Committee.

Purpose

1. To provide the Audit Committee with the recently adopted Terms of Reference for the Audit Committee which includes a requirement for the minutes of each meeting to specify the date and time of the next meeting.

Strategic Plan

2. The following Strategic Plan provision is relevant:

“A financially sound Council that is accountable, responsible and sustainable”

Communications/Consultation

3. The following communication / consultation was undertaken during the review of the Audit Committee Terms of Reference:

3.1 The revised Terms of Reference was adopted by City of Burnside at the meeting of 11 May 2014 (C9709).

3.2 Discussions with one of the Independent Members, Mr Andrew Blaskett, identified that he would be unable to attend any meetings on the third week of

31

Audit Committee Item 5.1 16 June 2014

any month due to a prior commitment. The presence of both Independent Members is required in order to attain quorum.

Statutory

4. The following legislation is relevant in this instance:

Local Government Act, 1999, Sections 41 and 126

Local Government (Procedures at Meetings) Regulations, 2013

Local Government (Financial Management) Regulations, 2011

Policy

5. The minor change to the Terms of Reference are isn reported in the ‘Discussion’ section of this report.

Risk Assessment

6. There are no risks associated with the recommendation.

Finance

7. There are no financial implications for the City of Burnside in respect of this recommendation.

Discussion

Background

8. The Local Government Act, 1999 (the Act) at section 126, requires each Council to have an Audit Committee; however, they are actually established under section 41 of the Act. Audit Committees have no authority to act independently of Councils and can only act in areas covered by their Terms of Reference (see Attachment A for the current Audit Committee Terms of Reference).

9. At the meeting of 13 May 2014, Council resolved (C9709):

1. That the draft Audit Committee Terms of Reference be adopted.

2. That there be a new paragraph 8.2 inserted as follows;

The minutes of each meeting must specify the date and time of the next ordinary meeting of the Committee.

10. Attachment A is the Audit Committee Terms of Reference amended to reflect the changes indicated in C9709.

11. The Audit Agenda will now include an item the requires the determination of the next Audit Committee meeting, for inclusion in the Minutes.

32

ECM Tracking No. 1167336 Page 1 of 11

Audit Committee Terms of Reference

1. Establishment

1.1 Resolution C8044 of 14 December 2010: The Audit Committee of Council is established under Section 41 of the Local Government Act 1999 (the Act), for the purposes of Section 126 of the Act and in compliance with regulation 17 of the Local Government (Financial Management) Regulations 2011.

1.2 The Committee’s role is to report to Council and provide appropriate advice and recommendations on matters relevant to its Terms of Reference in order to facilitate decision making by the Committee and Council in relation to the discharge of its responsibilities.

1.3 The Audit Committee does not have executive powers or authority to implement actions in areas which management has responsibility and does not have any delegated financial responsibility. The Audit Committee does not have any management functions and is therefore independent from management.

1.4 Resolution C9622 of 11 March 2014

Clauses 3.1, 4.1 and 5.2 will discontinue from the first meeting of the new Council elected after the 2014 Council Election.

1.5 Resolution C9622 of 11 March 2014

Clauses 3.2 & 4.2 will commence at the first meeting of the new Council elected after the 2014 Council Election.

2. Objectives

2.1 The primary objective of the Audit Committee is to assist Council in the effective

conduct of its responsibilities for financial reporting, management of risk and maintaining a reliable system of internal controls.

2.2 The Audit Committee is established to assist the co-ordination of relevant activities of management, the internal audit function and the external auditor to facilitate achieving overall organisational objectives in an efficient and effective manner.

2.3 As part of Council’s Governance obligations to its community, Council has constituted an Audit Committee to facilitate:

2.3.1 the enhancement of the credibility and objectivity of internal and external

financial reporting;

2.3.2 effective management of financial and other risks and the protection of Council assets;

33

City of Burnside – Audit Committee – Terms of Reference

ECM Tracking No. 1167336 Page 2 of 11

2.3.3 compliance with laws and regulations as well as use of best practice and Governance guidelines;

2.3.4 the effectiveness of any audit functions; and

2.3.5 the provision of an effective means of communication between the external auditor, management and the Council.

3. Membership

3.1 Members of the Committee are appointed by Council. The Committee shall consist of three members who shall be Members of Council (one of whom is the Mayor) and two members who are not members of Council (“the Independent Members”). (Refer 1.4)

3.2 Members of the Committee are appointed by the Council. The Committee shall be five of whom a majority shall be persons who are not members of Council (“the Independent Members”). (Refer 1.5)

3.3 Ideally, the non-Mayor Elected Member representative will have experience in business, legal, audit or financial management / reporting knowledge and experience.

3.4 That the Mayor is to be a member of the Audit Committee on an ex-officio basis. (C9600 25/02/14)

3.5 That the Mayor, if not a member on an ex officio basis, is to be a member of the

Audit Committee. (C9622 2.2 11/03/14)

3.6 The Independent Members of the Committee must have recent and relevant financial, risk management, internal audit experience relevant to the functions of Council’s Audit Committee as determined by Council.

3.7 Only members of the Committee are entitled to vote in Committee meetings. Unless otherwise required (by the conflict of interest provisions in the Act) not to vote, each member must vote on every matter that is before the Committee for decision. The Presiding Member has a deliberative vote but does not, in the event of an equality of votes, have a casting vote.

3.8 All decisions of the Committee shall be made on the basis of a majority decision

of the members present.

3.9 In the event of a tied vote the members have not made a decision, the question is neither carried nor lost. If a vote is tied the matter may be referred back to the Committee (either with or without additional information to inform the debate and decision making) or to referred to Council for resolution.

3.10 The Chief Executive Officer, General Manager Corporate Services, General

Manager Community & Development Services, General Manager Urban Services and other Council employees as directed by the Chief Executive Officer may attend any meeting as observers and/or be responsible for preparing papers for the Committee.

3.11 Council’s external auditors and internal auditor’s may be invited to attend

meetings of the Committee. Council’s external auditor must attend meetings considering the draft annual financial report and results of the external Audit.

34

City of Burnside – Audit Committee – Terms of Reference

ECM Tracking No. 1167336 Page 3 of 11

3.12 Elected Member appointments to the Committee shall be for a period of twelve months from the date of appointment, or until the end of the term of the Council. Elected Members are eligible for reappointment at the end of their term.

3.13 The Independent Members shall be appointed for a period of 2 years,

commencing part-way through an election cycle, so that their terms overlap each Council election and provide some continuity. Independent Members are eligible for reappointment at the end of their term.

4. Presiding Member

4.1 The Presiding member of the Committee shall be appointed by the Council and shall be a member of the Council. (refer 1.4)

4.2 The Presiding Member of the Committee shall be appointed by Council and shall be an Independent Member.(Refer 1.5)

4.3 The Presiding Member’s appointment to the Committee shall be for a period of twelve months from the date of appointment, unless their term is due to expire within that period in which case the appointment will be until the date their appointment as an Independent Member is due to expire.

5. Sitting Fees

5.1 The Remuneration Tribunal Determination No. 6 of 2010 dated 23 August 2010 outlines various allowances for Council Members.

5.2 The annual allowance for an Elected Member who is the Presiding Member of one or more standing committees established by a council will be equal to one and a quarter (1.25) times the annual allowance for councillors of that council.(Refer 1.4)

5.3 The Independent Members are to be paid a sitting fee, per meeting, as

determined by Council.

5.4 The annual allowance for an Independent Member who is the Presiding Member of the Audit Committee will be equal to one and a quarter (1.25) times the Independent Member sitting fee per meeting, as determined by Council.

6. Secretarial Resources

6.1 The Chief Executive Officer shall provide sufficient administrative resources to the Committee to enable it to adequately carry out its functions.

7. Quorum 7.1 The quorum for a meeting of the Audit Committee shall be three, of whom at

least 2 must be independent members. If the Mayor is present, the quorum is to be four of whom at least two must be independent members.

35

City of Burnside – Audit Committee – Terms of Reference

ECM Tracking No. 1167336 Page 4 of 11

8. Frequency of Meetings 8.1 The Committee shall meet at 6.00pm on a day to be specified by Audit

Committee within the third week of February, April, June, August, October and November or as otherwise determined by Council (whether as the result of a motion upon notice in or an Officer’s Report to Council).

8.2 the minutes of each meeting must specify the date and time of the next ordinary meeting of the Committee.

9. Notice of Meetings

9.1 A special meeting of the Committee may be called in accordance with the Act.

9.2 Notice of each meeting confirming the venue, time and date, together with an agenda of items to be discussed, shall be forwarded to each member of the Committee and observers, no later than three (3) clear days before the date of the meeting in accordance with Section 87 of the Act. Supporting papers shall be sent to Committee members (and to other attendees as appropriate) at the same time.

10. Minutes of Meetings

10.1 The Chief Executive Officer shall ensure that the proceedings and resolutions of all meetings of the Committee, including recording the names of those present and in attendance, are minuted and that the minutes otherwise comply with the requirements of the Local Government (Procedures at Meetings) Regulations 2000.

10.2 Minutes of Committee meetings shall be circulated within five (5) days after a meeting to all members of the Committee and members of the Council (in accordance with Section 91(3) of the Act).

11. Role of the Committee

11.1 Financial Reporting

11.1.1 The Committee shall monitor the integrity of the financial statements of the Council, including its Annual Report, reviewing significant financial reporting issues and judgements which they contain.

11.1.2 The Committee shall review and challenge where necessary:

a) the consistency of, and/or any changes to, accounting policies;

b) the methods used to account for significant or unusual transactions where different approaches are possible;

c) whether the Council has followed appropriate accounting standards and made appropriate estimates and judgements, taking into account the views of the external auditor;

d) the clarity of disclosure in the Council’s financial reports and the context in which statements are made; and

e) all material information presented with the financial statements.

Formatted: Font color: Red

36

City of Burnside – Audit Committee – Terms of Reference

ECM Tracking No. 1167336 Page 5 of 11

11.2 Internal Controls and Risk Management

The Committee shall:

11.2.1 keep under review the effectiveness of the Council’s internal controls and risk management; and

11.2.2 review and recommend the approval, where appropriate, of any material to be included in the Annual Report concerning internal controls and risk management.

11.3 Whistle blowing

The Committee shall review the Council’s arrangements for its employees to raise concerns, in confidence, about possible wrongdoing in financial recording or reporting or other matters. The Committee shall ensure these arrangements allow independent investigation of such matters and appropriate follow-up action.

11.4 Strategic Management Plans and Annual Business Plans

The Committee shall propose and provide information relevant to, a review of the Council’s Strategic Management Plans or Annual Business Plan.

11.5 Other Investigations

The Committee shall, when necessary, propose and review the exercise of Council’s powers under Section 130A of the Local Government Act 1999, in relation to the conduct of Economy Audits that would not otherwise be addressed or included as part of an annual External Audit.

11.6 Internal Audit

The Committee shall:

11.6.1 monitor and review the effectiveness of the Council’s internal audit function in the context of the Council’s overall risk management system;

11.6.2 consider and make recommendation on the program of the internal audit

function and the adequacy of its resources and access to information to enable it to perform its function effectively and in accordance with the relevant professional standards;

11.6.3 review all reports on the Council’s operations from the internal auditors;

11.6.4 review and monitor management’s responsiveness to the findings and

recommendations of the internal auditor; and 11.6.5 where appropriate, meet the ‘head’ of internal audit at least once a year,

without management being present, to discuss any issues arising from the internal audits carried out. In addition, the head of internal audit shall be given the right of direct access to the Principle Member of the Council and to the Presiding Member of the Committee.

Formatted: Tab stops: 3.5 cm, Listtab + Not at 3.27 cm

Formatted: Tab stops: 3.5 cm, Listtab + Not at 3.27 cm

Formatted: Tab stops: 3.5 cm, Listtab + Not at 3.27 cm

Formatted: Tab stops: 3.5 cm, Listtab + Not at 3.27 cm

Formatted: Tab stops: 3.5 cm, Listtab + Not at 3.27 cm

37

City of Burnside – Audit Committee – Terms of Reference

ECM Tracking No. 1167336 Page 6 of 11

11.7 External Audit

The Committee shall:

11.7.1 oversee the selection process for the external auditors and make a recommendation in this regard to the Council;

11.7.2 develop and implement a policy on the supply of non-audit services by

the external auditor, taking into account any relevant ethical guidance on the matter;

11.7.3 consider and make recommendations to the Council, in relation to the

appointment, re-appointment and removal of the Council’s external auditor. If an auditor resigns the Committee shall investigate the issues leading to this and decide whether any action is required;

11.7.4 oversee Council’s relationship with the external auditor including, but not

limited to:

a) recommending the approval of the external auditor’s remuneration, whether fees for audit or non-audit services, and recommending whether the level of fees is appropriate to enable an adequate audit to be conducted;

b) recommending the approval of the external auditor’s terms of

engagement, including any engagement letter issued at the commencement of each audit and the scope of the audit;

c) assessing the external auditor’s independence and objectivity

taking into account relevant professional and regulatory requirements and the extent of Council’s relationship with the auditor, including the provision of any non-audit services;

d) satisfying itself that there are no relationships (such as family,

employment, investment, financial or business) between the external auditor and the Council (other than in the ordinary course of business);

e) monitoring the external auditor’s compliance with legislative

requirements on the rotation of audit partners; and f) assessing the external auditor’s qualifications, expertise and

resources and the effectiveness of the audit process;

11.7.5 meet as needed with the external auditor. The Committee shall meet the external auditor at least once a year, without management being present; to discuss the external auditor’s report and any issues arising from the audit;

11.7.6 review and make recommendations on the annual audit plan, and in

particular its consistency with the scope of the external audit engagement;

11.7.7 review the findings of the audit with the external auditor. This shall

include but not be limited to the following:

Formatted: Tab stops: 3.5 cm, Listtab + Not at 3.27 cm

Formatted: Tab stops: 3.5 cm, Listtab + Not at 3.27 cm

Formatted: Tab stops: 3.5 cm, Listtab + Not at 3.27 cm

Formatted: Tab stops: 3.5 cm, Listtab + Not at 3.27 cm

Formatted: Tab stops: 3.5 cm, Listtab + Not at 3.27 cm

Formatted: Tab stops: 3.5 cm, Listtab + Not at 3.27 cm

Formatted: Tab stops: 3.5 cm, Listtab + Not at 3.27 cm

38

City of Burnside – Audit Committee – Terms of Reference

ECM Tracking No. 1167336 Page 7 of 11

• a discussion of any major issues which arose during the external audit;

• any accounting and audit judgements; and

• levels of errors identified during the external audit;

11.7.8 review the effectiveness of the external audit; 11.7.9 review any representation letter requested by the external auditor before

they are signed by management;

[Note that these representation letters are a standard practice of any audit and provide the auditor confirmation from management, (in particular the Chief Financial Officer) that, amongst other matters, accounting standards have been consistently applied, that all matters that need to be disclosed have been so disclosed and that the valuation of assets has been consistently applied.];

11.7.10 review the subsequent audit management letter from the external auditor and management’s proposed response, by the Council, to the external auditor’s findings and recommendations in that audit management letter.

11.8 Regional Subsidiaries

In accordance with Section 126(4) of the Act, the functions of the Audit Committee include, if the council has exempted a subsidiary from the requirement to have an audit committee, the functions that would, apart from the exemption, have been performed by the subsidiary’s audit committee.

12. Reporting Requirements

12.1 The Committee shall make recommendations to the Council as it deems

appropriate on any area within these Terms of Reference where in its view action or improvement is needed. The Presiding Member shall attend these meetings and talk on these matters, as and when required.

12.2 In accordance with Section 41(8) of the Act, the Committee shall after every meeting forward the minutes of that meeting to the next meeting of the Council.

12.3 The Committee shall report annually to the Council summarising the activities of

the Committee during the previous financial year.

13. Conduct and Disclosure of Interests

13.1 Members of the Committee must comply with the conduct and conflict of interest provisions of the Act. In particular Sections 62 (general duties), 63 (code of conduct) and 73-74 (conflict of interest, members to disclose interests) must be adhered to.

14. Register of Interest

14.1 Section 64 of the Act (interpretation) applies to the members of the Committee.

Formatted: Tab stops: 3.5 cm, Listtab + Not at 3.27 cm

Formatted: Tab stops: 3.5 cm, Listtab + Not at 3.27 cm

39

City of Burnside – Audit Committee – Terms of Reference

ECM Tracking No. 1167336 Page 8 of 11

15. Delegations

15.1 Council may delegate additional matters that are within the scope of these Terms of Reference to the Committee in accordance with Section 41 of the Act.

16. Reimbursement of Expenses

16.1 Reimbursement of Expenses incurred by members of the Committee will be paid in accordance with the Council's "Elected Members' Allowances and Benefits Policy".

17. Public Access to Meetings

17.1 In accordance with the principles of open, transparent and informed decision making Committee meetings must be conducted in a place open to the public. Members of the public are able to attend all meetings of the Committee, unless prohibited by resolution of the Committee under the confidentiality provisions of Section 90 of the Act.

18. Public Access to Documents

18.1 Members of the public have access to all documents relating to the Committee unless prohibited by resolution of the Committee under the confidentiality provisions of Section 91 of the Act.

19. Other Matters The Committee shall:

19.1 Have access to reasonable resources in order to carry out its duties;

[Note that is subject to any budget allocation being approved by Council.]

19.2 Be provided with appropriate and timely training, both in the form of an induction programme for new members and on an ongoing basis for all members;

19.3 Give due consideration to the Act; and regulations made under the Act;

19.4 Make recommendations on co-ordination of the internal and external auditors;

19.5 Oversee any investigation of activities which are within its terms of reference; and

19.6 At least once a year, review its own performance, constitution and terms of

reference to ensure it is operating at maximum effectiveness and recommend changes it considers necessary to the Council for approval.

40

City of Burnside – Audit Committee – Terms of Reference

ECM Tracking No. 1167336 Page 9 of 11

Document history

Date Resolution number 14/12/2010 C8044 27/04/2011 C8220 22/11/2011 C8496 28/08/2012 C8840 10/12/2013 C9530 25/02/2014 11/03/2014

C9600 C9622

41

City of Burnside – Audit Committee – Terms of Reference

ECM Tracking No. 1167336 Page 10 of 11

Schedule 1

Audit Committee

Meeting Procedure Protocols

1. The Local Government (Procedures at Meetings) Regulations 2013 apply (as a matter of law) to all meetings of the Committee.

2. The decision of the person presiding at meetings of the Committee in relation to the interpretation and application of these Meeting Procedure Protocols shall be absolute and binding on the Committee.

3. A meeting of the Committee will commence as soon after the time specified in the notice of meeting as a quorum is present.

4. Subject to clause 10 of the Terms of Reference the minutes of proceedings at a meeting of the Committee must include:

(a) the names of the members present at the meeting;

(b) the names of the mover and seconder of each motion;

(c) each motion carried or lost at the meeting;

(d) any disclosure of interest made by a member;

(e) details of the making of an order (to exclude the public) under subsection (2) of section 90 of the Act (see subsection (7) of that section); and

(f) a note of the making of an order (to keep minutes, reports etc confidential) under subsection (7) of section 91 of the Act in accordance with the requirements of subsection (9) of that section.

5. The minutes of the proceedings at a meeting must be submitted for confirmation at the next meeting or, if that is omitted, at a subsequent meeting of the Committee.

6. Business may only be transacted at a meeting of the Committee as follows:

(a) by way of a motion without notice in support of a recommendation set out in an officer's report, or

(b) by way of a motion without notice which is accepted by the Presiding Member as suitable having regard to the 'Guiding Principles' at Regulation 4 of the Local Government (Procedures at Meetings) Regulations 2013, or

(c) by way of a motion without notice which has been given consent by the meeting, or

(d) by way of a notice of motion which has been provided in writing (together with a supporting short explanation) to the Committee support officer at least 7 clear days before the meeting at which it is to be considered.

7. Subject to clause 9 of the Local Government (Procedures at Meetings) Regulations 2013, any motion or amendment which is not seconded will lapse.

8. Only the mover of a motion has a right of reply.

9. A member may speak more than once to a motion with the consent of the Presiding Member of the Committee or the consent of the meeting.

42

City of Burnside – Audit Committee – Terms of Reference

ECM Tracking No. 1167336 Page 11 of 11

10. Any member except the mover or seconder of a motion may move an amendment to a motion provided that if they have already spoken in the debate the consent of the Presiding Member of the Committee or the leave of the meeting has first been obtained.

11. Only one amendment may be moved in relation to any motion.

12. All other aspects of the meeting procedure at a Committee meeting will be determined at the discretion of the Principal Member of the Committee having regard to issues of equity and fairness and the Guiding Principles at Regulation 4 of the Local Government (Procedures at Meetings) Regulations 2013 or otherwise with the consent of the meeting.

43

44

Audit Committee Agenda Item 5.2 16 June 2014

Item No: 5.2 To: Audit Committee Date: 16 June 2014 Author: Martin Cooper – Chief Financial Officer General Manager and Division

Louise Miller Frost – General Manager, Corporate Services

Contact Subject:

8366 4202 POLICY REVIEW – TREASURY MANAGEMENT POLICY (STRATEGIC)

Attachments: Prev. Resolution:

A. Treasury Management Policy (ver. April 2011) B. Treasury Management Policy (track changes new version) C. Treasury Management Policy (new version) D. LGA Financial Sustainability Information Paper 15 Treasury

Management A0313, 7/8/13 C9377, 27/8/13 A0328, 6/11/13 C9516, 26/11/13

Officer’s Recommendation

1. That the Report be received.

2. That the draft Treasury Management Policy be endorsed.

3. That the draft Treasury Management Policy be presented to Council for consideration and adoption.

Purpose

1. To provide the Audit Committee with a draft Treasury Management Policy for review and endorsement before presentation to Council for consideration and adoption.

Strategic Plan

2. The following Strategic Plan provisions are relevant:

“A financially sound Council that is accountable, responsible and sustainable”

“Delivery of good governance in Council Business”

Communications/Consultation

3. The following communication / consultation was undertaken during the review of the Treasury Management Protocol:

3.1. LGA Information Paper 15 – Treasury Management Revised February 2012.

3.2. Discussion with Councillor Grant Piggott.

45

Audit Committee Agenda Item 5.2 16 June 2014

Statutory

4. The following legislation is relevant in this instance:

Local Government Act, 1999

The Local Government Financial Management Regulations, 2011

Policy

5. The following Council Policies are relevant in this instance:

Risk Management; and

Proceeds from Economic Development Activity

Risk Assessment

6. Council borrowings and investments in the commercial marketplace are not without risk. The Administration manages these risks in accordance with the legislative requirements of the Local Government Act, 1999 and Council’s Treasury Management Policy.

7. The City of Burnside sets range limits for both fixed and variable rate borrowings and restricts the placement of investments to financial institutions that carry an acceptable low risk Standard and Poors credit rating.

Discussion

Background

8. The Investment Performance Review 2012/13 Report was provided to the Audit Committee at the 7 August 2013 meeting.

9. The Report contained a review of the interest rate return on investments for the financial year ending 30 June 2013 and a revised Treasury Management Protocol with the requirement not to exceed 75 per cent investment in one institution removed.

10. At the 7 August 2013 meeting, the Audit Committee resolved (A0313):

1. That the Report be received.

2. That the draft Treasury Management Protocol be endorsed.

3. That the Report be presented to Council for consideration at its 27 August 2013 meeting.

11. The Report was presented to the Council at the meeting of 27 August 2013. Council raised concerns over the decision to remove the requirement not the exceed 75 per cent investment in one institution and resolved (C9377):

1. That the Report be received.

2. That the Audit Committee review the draft Treasury Management Protocol in respect to investment of Council funds and return to Council for approval.

46

Audit Committee Agenda Item 5.2 16 June 2014

12. At the 6 November 2013 meeting, the Audit Committee considered the limitations of the Protocol; the definition of the word ‘total investments’ for use in calculating the ratio; and the risks associated with any modification to the protocol.

13. The Audit Committee took into consideration the following:

13.1. That Council would only invest in investments with a minimum Standard & Poor’s rating of ‘A-1’. This is rated in the highest category by Standard & Poor’s.

13.2. That the City of Burnside approach to not restrict investment to one institution is in line with the Local Government Association (LGA) Information Paper 15 on Treasury Management produced as part of their Financial Sustainability Program.

13.3. That the removal of the restriction would allow the Administration to enter into longer fixed term deposits and achieve greater interest returns as there would be no need to constantly reshuffle funds and potential break fixed term deposits to keep within ratios.

13.4. That the current Management Protocol be changed to a Council Policy. This will ensure that all changes to the Policy require Council approval and will be reviewed as such on a 12 monthly basis.

14. At the meeting on 6 November 2013, the Audit Committee again confirmed their decision to endorse the changes to the draft Treasury Management Protocol and resolved (A0328):

1. That the Report be received.

2. That the Audit Committee after considering the changes to the Draft Treasury Management Protocol with respect to investment of Council funds endorses the proposed changes.

3. That the Draft Treasury Management Protocol be changed from a Protocol to a Council Policy and be presented to the Council at the meeting 26 November 2013 for consideration.

15. The Report was presented to the Council at the meeting of 26 November 2013. Council resolved (C9516):

1. That the Report be received.

2. That the Treasury Management Policy be returned to the Administration for further review prior to Council approval.

16. The Administration has further reviewed the draft Treasury Management Policy with reference to the Local Government Association (LGA) Financial Sustainability Information Paper 15, Treasury Management, Revised February 2012 (Attachment D) and discussions with Councillor Grant Piggott.

17. In reviewing this Protocol, comparison has been made with a number of other metropolitan Council’s Treasury Management Policy statements to ensure consistency and appropriate coverage of all aspects of the treasury management process.

18. The current Treasury Management Protocol is shown in Attachment A with the proposed changes shown in Attachment B.

19. It is recommended that the current Management Protocol be changed to a Council Policy. This will ensure all changes will require the full Council approval for any changes and will be reviewed as on a regular basis.

47

Audit Committee Agenda Item 5.2 16 June 2014