nov 28, 2006 implementation models of mvnos presentation to the information society and media...

Post on 19-Dec-2015

216 views

TRANSCRIPT

Nov 28, 2006

Implementation Models of MVNOs

Presentation to the Information Society and Media Directorate-General - Unit: Communication Technologies

Nov 28, 2006

AGENDA

A few facts/figures to frame MVNO in today’s context- How do telecom groups react today towards MVNO: Opportunity or Threat

- MVNO and Segmentation…Same Answer for the Same Issue

- What a MVNO can bring to capture market shares

Back to Theory….- Definition of MVNO

- Strategic Models of MVNO

- Regulatory Aspects

- How a MNO should organize its operations to host MVNOs

- Economical Models

- Case Study: why no corporate MVNO exist ?

- State of MVNO market within EU

- Conclusion

Nov 28, 2006

AGENDA

A few facts/figures to frame MVNO in today’s context- How do telecom groups react today towards MVNO: Opportunity or Threat

- MVNO and Segmentation…Same Answer for the Same Issue

- What a MVNO can bring to capture market shares

Back to Theory….- Definition of MVNO

- Strategic Models of MVNO

- Regulatory Aspects

- How a MNO should organize its operations ot host MVNOs

- Economical Models

- Case Study: why no corporate MVNO exist ?

- State of MVNO market within EU

- Conclusion

How MNO Should Respond to MVNO entry

Nov 28, 2006

What is the position of telecom groups towards MVNO ?

No common/structured position but a collection of local initiatives:

• MVNO develop at a different speed within EU members• Big telecom (incumbent) groups have mobile assets in most EU countries:

- MVNO is first seen as a threat

• When local MVNOs initiatives becomes important in volume/scope, there is an attempt to harmonize/unify

- Most of the time, local initiatives remain ahead of global program

MVNO or more precisely VNO will become the only means to expand footprint of telecom groups• The wave of privatization of former State owned telecom companies are finishing- All licenses are bought by Middle East countries that have a lot of cash

• The mobile licenses are too expensive because less and less based on a beauty contest- All licenses are bought by Middle East countries that have a lot of cash

But no unified vision of MVNO theory and strategy to date within most telecom groups within EU

Nov 28, 2006

MVNO and Segmentation…Same Answer for the Same Issue

Segmentation appears:• When MNO understand they all fought between each other for the same (national)

market with no possibility to make their offers different from the competitor• When MNO segment the market to focus on niches, ethnical communities, loyalty

programs via new brands to avoid cannibalisation

MVNO appears• When an operator decides to attract volumes and traffic to fill the network• When an operator wants to promote new usages or to launch new services• When an operator feels it can address new markets via 3rd parties without

incurring the necessary (marketing) investment.

Limits between new brands and MVNO blur• MVNO are bought by the MNO• MNO start at the same time MVNO and new brands • More the new brand is independent from the MNO closer it is from a MVNO

because it has its own life parallel to the usual commercial operations (see cases where the network is outsourced)

Nov 28, 2006

What can bring a MVNO to capture market shares Good Surprises:

• MVNO as the first ones to launch web based offers but now copied by MNO• MVNO as the first ones to focus on content (especially in the USA but some

examples in Europe as Universal Mobile)• MVNO as the first ones to make more simple mobile offers and prices• MVNO as the first ones to propose pan European corporate services

- Still in development: they exploit the lack of integration of mobile groups that are still an aggregation of local mobile operators with a local P&L

Remedy to Competition Problems in Mobile Markets• Access: MVNOs compensate the scarcity of spectrum (evident)- MVNO will also exist in any other network economy relying on not replicable assets still

owned by a monopoly operator

• Termination: if MVNOs can fix their termination rates themselves (less evident)- Attempt in Austria

• Roaming: if MVNOs can become member of the GSM Association (less less evident)

- (Missed) Attempt in Austria- Maybe remedy will come with yet-to-come substitution products like WiFi, Wimax- Notable exception and real substitution: multi numbers SIM

Nov 28, 2006

AGENDA

A few facts/figures to frame MVNO in today’s context- How do telecom groups react today towards MVNO: Opportunity or Threat

- MVNO and Segmentation…Same Answer for the Same Issue

- What a MVNO can bring to capture market shares

Back to Theory….- Definition of MVNO

- Strategic Models of MVNO

- Regulatory Aspects

- How a MNO should organize its operations ot host MVNOs

- Economical Models

- Case Study: why no corporate MVNO exist ?

- State of MVNO market within EU

- Conclusion

How MNO Should Respond to MVNO entry

Nov 28, 2006

INTRODUCTION

Definition

3rd Party that operates on its own a piece of the mobile value chain with the exception of the radio access. It controls totally or partly the commercial ownership of the end user (or its representative)

As an evident consequence: it forces the MNO to break its vertical integration…that is a root cause of the lack of competition in the mobile market.

Oligopoly/Guaranteed Income within the mobile sectorRicardo’s theoryThe guaranteed income depends on the market shares (with the exception of UK)The regulator is forced to maintain a minimum price to help the last entrant to survive (!) The guaranteed income creates a monopoly effect that the 1st entrant could use to expel the

last entrant

Impact of MVNO on the guaranteed income breaks the guaranteed income effect as fix assets do not play any more in the game. only the last entrant should host a MVNO otherwise it is another competitor for it !

Other Remedy to break the guaranteed income within the mobile sector Asymmetric Wholesale Regulation: force the 1st entrant to decrease its wholesale rates Asymmetric Retail Regulation: last entrant will suffer from an imposed decrease of rates Taxation of profits: unfair and difficult to implement

Commoditization of mobile = open door for 1st generation MVNOs:Marketing/Distribution

Nov 28, 2006

AGENDA

A few facts/figures to frame MVNO in today’s context- How do telecom groups react today towards MVNO: Opportunity or Threat

- MVNO and Segmentation…Same Answer for the Same Issue

- What a MVNO can bring to capture market shares

Back to Theory….- Definition of MVNO

- Strategic Models of MVNO

- Regulatory Aspects

- How a MNO should organize its operations ot host MVNOs

- Economical Models

- Case Study: why no corporate MVNO exist ?

- State of MVNO market within EU

- Conclusion

How MNO Should Respond to MVNO entry

Nov 28, 2006

STRATEGIC MODELS (1)

TELE2

TMF

Telmore

VIRGIN/T-Mobile (till 2004)

Ay- Yildiz

TRANSATE Tele2 TELENET

MobiLux (agent)

Model of Participation (industrial/financial)

Segmentation = Zone 3

MVNO consolidation = Zone 1 and Zone 2

Carrefour

Cobranding

Zone 2 Zone 3

Zone 4Zone 1

Commercial Agreement for the supply of

connectivity and network capacity

Zone 2 Zone 3

Zone 4Zone 1

Zone 2 Zone 3

Zone 4Zone 1

Zone 2 Zone 3

Zone 4Zone 1

JV between MNO and 3rd party

Simple financial participation

Intensity of the connectivity/hosting (supplier) relationship between the MNO and the MVNO

Fin

anci

al C

ross

-Par

ticip

atio

n be

twee

n th

e M

NO

and

the

MV

NO

Spin off of MVNO (new brands, network separation,…)

Nov 28, 2006

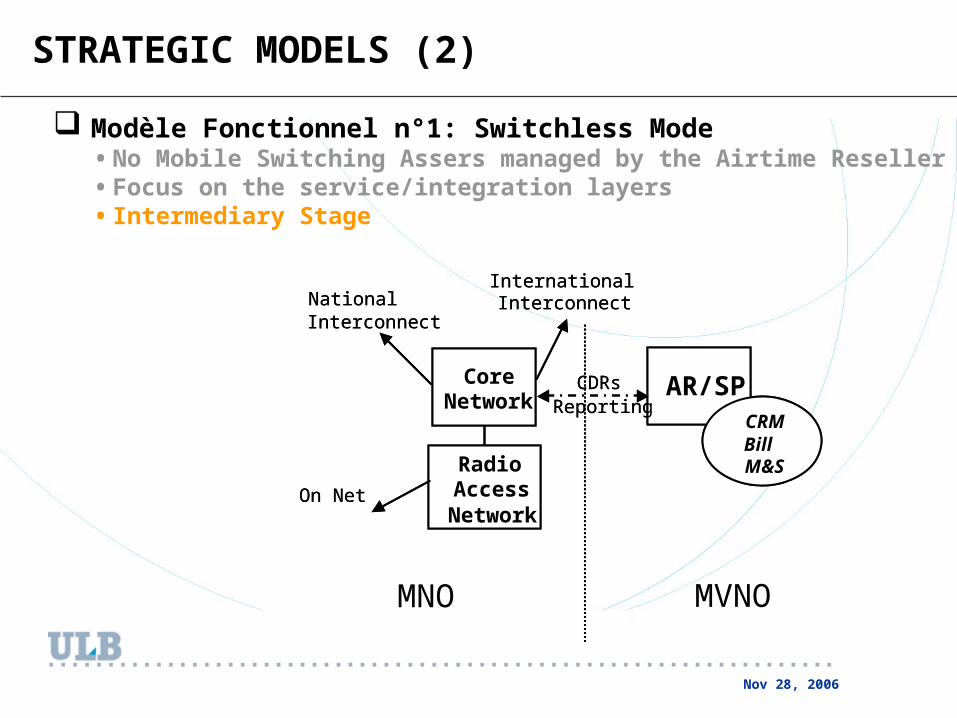

STRATEGIC MODELS (2)

Modèle Fonctionnel n°1: Switchless Mode• No Mobile Switching Assers managed by the Airtime Reseller• Focus on the service/integration layers• Intermediary Stage

CoreNetwork

AR/SPCRMBillM&S

CDRs

National Interconnect

International Interconnect

On Net

Radio AccessNetwork

Reporting

CoreNetwork

AR/SPCRMBillM&S

CDRs

National Interconnect

International Interconnect

On Net

Radio AccessNetwork

Reporting

MNO MVNO

Nov 28, 2006

STRATEGIC MODELS (3)

Modèle Fonctionnel n°2: Enhanced Service Provide Mode

• Integration of VAS services coming from the enhanced service provider with an mobile access

• Stimulation of the usage of both mobile and VAS usage

CoreNetwork

Backbone

CRMBillM&SNetwork Management

National Interconnect

International Interconnect

On Net

VAS/IN

Radio AccessNetwork

Interco

CDRCoreNetwork

Backbone

CRMBillM&SNetwork Management

National Interconnect

International Interconnect

On Net

VAS/IN

Radio AccessNetwork

Interco

CDR

MNO MVNO

Nov 28, 2006

STRATEGIC MODELS (4)

Modèle Fonctionnel n°3: Full MVNO• Full Mobile Switching infrastructure owned and brought by the mobile

operator• Focus on just renting the radio access to the mobile operator • Ultimate stage of a MVNO

Backbone

National Interconnect

International Interconnect

On Net

VAS/IN

CoreNetwork

Radio AccessNetwork

HLR

Everything except Radio Access

Backbone

National Interconnect

International Interconnect

On Net

VAS/IN

CoreNetwork

Radio AccessNetwork

HLR

Everything except Radio Access

MNO MVNO

Nov 28, 2006

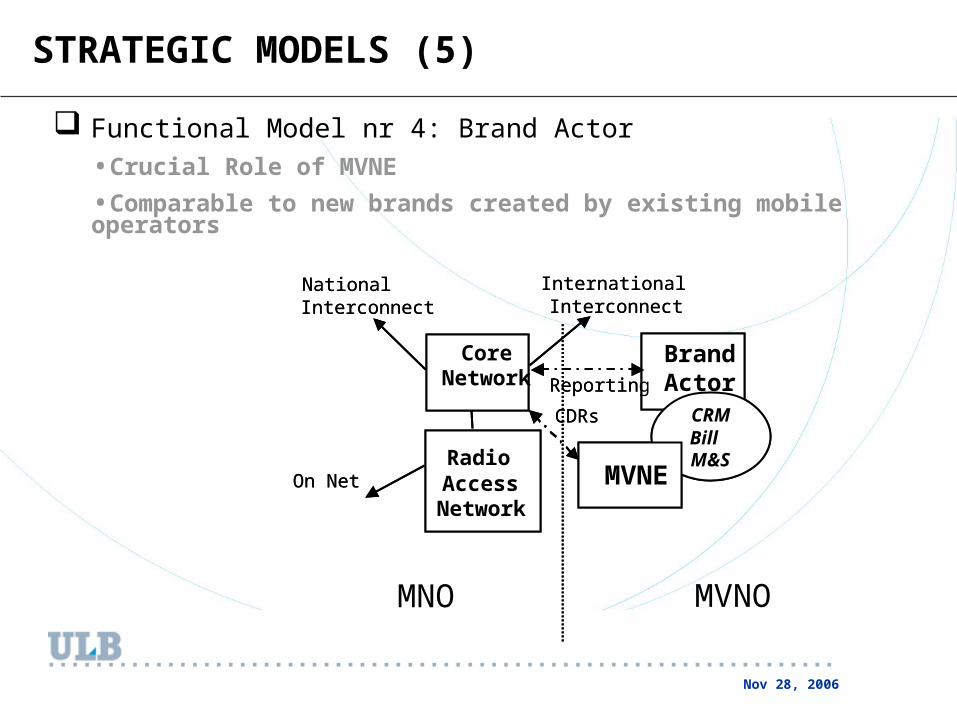

STRATEGIC MODELS (5)

Functional Model nr 4: Brand Actor

•Crucial Role of MVNE

•Comparable to new brands created by existing mobile operators

Brand Actor

CRMBillM&S

CDRs

National Interconnect

International Interconnect

On Net MVNE

Reporting

CoreNetwork

Radio AccessNetwork

Brand Actor

CRMBillM&S

CDRs

National Interconnect

International Interconnect

On Net MVNE

Reporting

CoreNetwork

Radio AccessNetwork

MNO MVNO

Nov 28, 2006

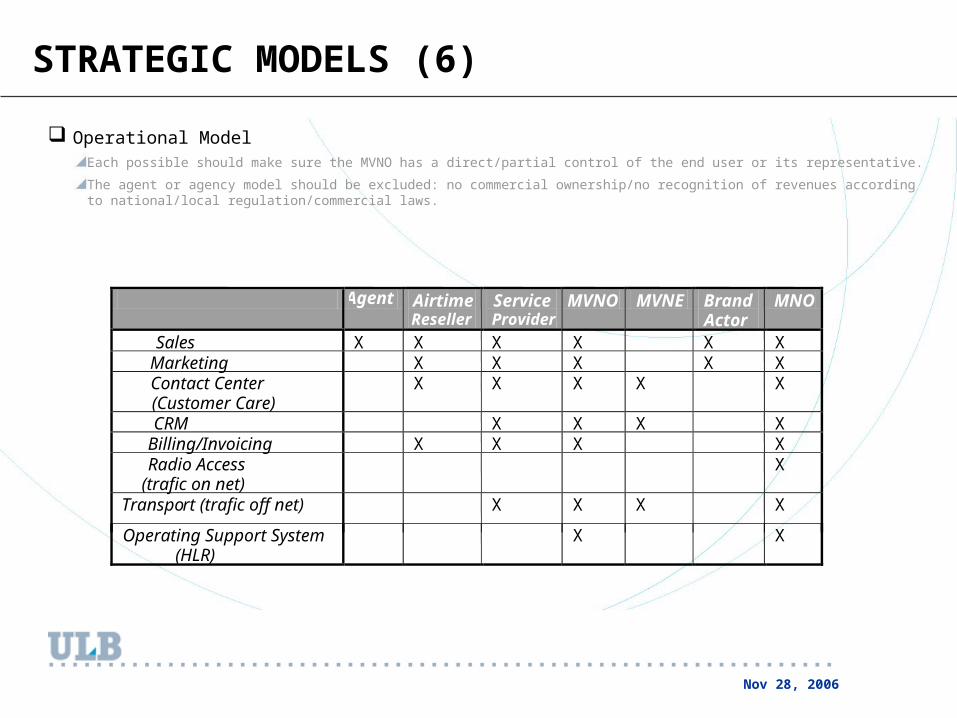

Operational ModelEach possible should make sure the MVNO has a direct/partial control of the end user or its representative.

The agent or agency model should be excluded: no commercial ownership/no recognition of revenues according to national/local regulation/commercial laws.

STRATEGIC MODELS (6)

Agent Airtime

Reseller Service Provider

MVNO MVNE Brand Actor

MNO

Sales X X X X X X Marketing X X X X X Contact Center (Customer Care)

X X X X X

CRM X X X X Billing/Invoicing X X X X

Radio Access (trafic on net)

X

Transport (trafic off net) X

X X X

Operating Support System (HLR)

X X

Nov 28, 2006

Role of a MVNE: good for the MNO and the MVNO

Use of a MVNE• MVNE = Mobile Virtual Network Enabler = Integrator for MVNO candidates• Allows an ‘EBIT=EBITDA’ business model • Divert complexity of one-to-many hosting technical aspects with MVNO to MVNE

that leverage their expertise or even already existing connections- A MVNE is a kind of hosting/connectivity provider to GSM operators

MVNOMVNO

MVNEMVNEMVNO

MarketingPartner

MVNOMarketingPartner

MNOMNO

End-UserEnd-User

MNOMNO

End-UserEnd-User

MVNEMVNE

MVNEMVNE

MNOMNO

End-UserEnd-User

MVNOMVNO

MVNEWholesale

MVNEWholesale

MVNECo-Marketing

MVNECo-Marketing

MVNEASP

MVNEASP

MVNOMVNO

MVNEMVNEMVNO

MarketingPartner

MVNOMarketingPartner

MNOMNO

End-UserEnd-User

MNOMNO

End-UserEnd-User

MVNEMVNE

MVNEMVNE

MNOMNO

End-UserEnd-User

MVNOMVNO

MVNEWholesale

MVNEWholesale

MVNECo-Marketing

MVNECo-Marketing

MVNEASP

MVNEASP

The MVNE ASP plays the role of the MVNO’s integrator for setting up a MVNO business/operating model. It has not other role

A MVNE wholesale will also sell mobile connectivity and airtime to the MVNO besides its integrator role. So the MVNO will benefit from the MVNE existing wholesale agreements without having to negotiate with local mobile operators

Nov 28, 2006

VNO is future proof versus 3G and NGN 6 possible layers to share the infrastructure

STRATEGIC MODELS (8)

NodeB

RNC

MSCVLR

SGSN

GMSC GGSN

HLR

GMSC GGSN

HLR

3rd party networks (PSTN, PLMN,….)

NodeB

HOsting operator MVNO

Location CRM Content Voice Mail

Call Setup QoSAuthen-tication

Rating&Billing

Billing&Invoicing

IP on Fibre Optique

ATM TDM Broadcast

Switching Access Netowrks (PSTN, ISDN, GSM)

Packet Access Networks (UTRAN, ADSL, Ethernet, WLAN)

Services

Control

Transport

Access

Nov 28, 2006

AGENDA

A few facts/figures to frame MVNO in today’s context- How do telecom groups react today towards MVNO: Opportunity or Threat

- MVNO and Segmentation…Same Answer for the Same Issue

- What a MVNO can bring to capture market shares

Back to Theory….- Definition of MVNO

- Strategic Models of MVNO

- Regulatory Aspects

- How a MNO should organize its operations to host MVNOs

- Economical Models

- Case Study: why no corporate MVNO exist ?

- State of MVNO market within EU

- Conclusion

How MNO Should Respond to MVNO entry

Nov 28, 2006

ECONOMICAL/FINANCIAL MODEL (1)

Aim: define cost and access price to the network: 3 methods/2 approaches Cost Plus - Retail Minus – BenchmarkTop Down – Bottom Up (closely linked to Cost Plus)

Retail MinusPa= Pr-CrPr = Retail price Cr = Cost of Sales (Cr is the ‘retail minus’ part)Avoid squeeze out (predatory pricing eg: TELE2 - ORANGE) but not adapted if cross subsidiation exists MVNO is forced to address the same market as the hosting operator Allows the MVNO to be more efficient if it has a smaller Cr for a specific marketNot adapted if the objective is to bring more competition via ex ante regulation (not pressure on costs)

Cost PlusLRIC ou FDC/FACLRIC= Long Run Incremental Cost including fix costs (and sometimes joint cost, which is not orthodox)

Adapted in case of strongly integrated operatorMVNO is forced to address markets not yet addressed by MNOFinancial risk is on the MVNO not on the MNO (all minutes are sold with a gross margin)

Benchmark

Nov 28, 2006

MNO should favour « Cost Plus » models to host one’s MVNOs with payback of interco revenues

« Cost Plus » Avoid Price Wars:• MNO takes no financial risks as any subsidization is avoided• MVNO can not copy its MNO’s retail prices as its cost to address the same market

is higher (no economy of scale)• MVNO is forced to focus on its own markets (where its own subsidisation policy

will be the most efficient)• MVNO is forced to be innovative• See What happened to the first Service Providers of the early days of GSM

But takes more time to take off• Not easy for new MVNO entrant to understand the subtle subsidization

mechanisms So also the reason why MVNO simplified their offers

• Limited risks for MNO to be accused of earning too much money with termination revenues

- As wholesale prices can be higher than corporate offers- As « Cost Plus » is normally based on a accurate cost model of the network

Nov 28, 2006

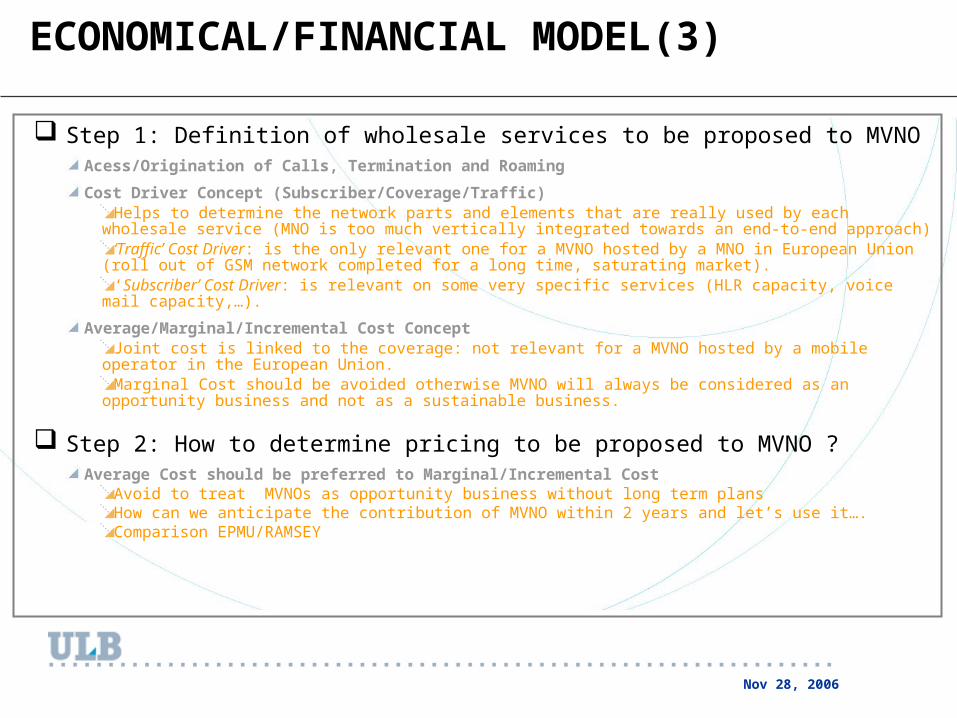

ECONOMICAL/FINANCIAL MODEL(3)

Step 1: Definition of wholesale services to be proposed to MVNOAcess/Origination of Calls, Termination and Roaming

Cost Driver Concept (Subscriber/Coverage/Traffic)Helps to determine the network parts and elements that are really used by each wholesale service (MNO is

too much vertically integrated towards an end-to-end approach) ‘Traffic’ Cost Driver: is the only relevant one for a MVNO hosted by a MNO in European Union (roll out of

GSM network completed for a long time, saturating market). ‘Subscriber’ Cost Driver: is relevant on some very specific services (HLR capacity, voice mail capacity,…).

Average/Marginal/Incremental Cost ConceptJoint cost is linked to the coverage: not relevant for a MVNO hosted by a mobile operator in the European

Union. Marginal Cost should be avoided otherwise MVNO will always be considered as an opportunity business and

not as a sustainable business.

Step 2: How to determine pricing to be proposed to MVNO ?Average Cost should be preferred to Marginal/Incremental Cost

Avoid to treat MVNOs as opportunity business without long term plansHow can we anticipate the contribution of MVNO within 2 years and let’s use it…. Comparison EPMU/RAMSEY

Nov 28, 2006

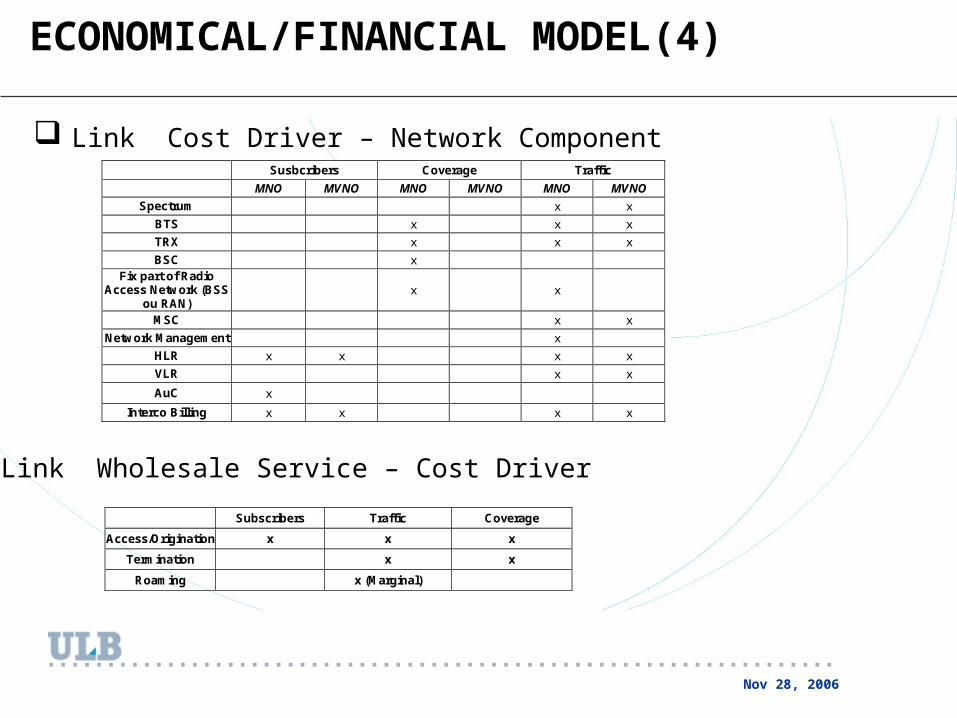

ECONOMICAL/FINANCIAL MODEL(4)

Link Cost Driver – Network Component Susbcribers Coverage Traffic

MNO MVNO MNO MVNO MNO MVNO

Spectrum x x

BTS x x x

TRX x x x

BSC x Fix part of Radio

Access Network (BSS ou RAN)

x x

MSC x x

Network Management x

HLR x x x x

VLR x x

AuC x

Interco Billing x x x x

Subscribers Traffic Coverage

Access/Origination x x x

Termination x x

Roaming x (Marginal)

Link Wholesale Service – Cost Driver

Nov 28, 2006

ECONOMICAL/FINANCIAL MODEL(5)

MODELLING OF WHOLESALE SERVICES AND COSTS TO BE CONSIDERED

1 leg

1 leg

BTSBSC

BTSBSC

MSC

Client/Utilisateur du partenaire wholesale

Client/Utilisateur de BASE ou d’un autre partenaire w holesale

1 leg

1 leg

BTSBSC

BTSBSC

MSC

Client/Utilisateur du partenaire wholesale

Client/Utilisateur de BASE ou d’un autre partenaire w holesale

1 leg

BTSBSC

(G)MSC

Client/Utilisateur du partenaire wholesale

Réseau Tiers (Fixe ou mobile domestique/International

1 leg

BTSBSC

(G)MSC

Client/Utilisateur du partenaire wholesale

Réseau Tiers (Fixe ou mobile domestique/International

1 leg

BTSBSC

(G)MSC

Client/Utilisateur du partenaire wholesale

Réseau Tiers (Fixe ou mobile domestique/International

1 leg

BTSBSC

(G)MSC

Client/Utilisateur du partenaire wholesale

Réseau Tiers (Fixe ou mobile domestique/International

1 leg

BTSBSC

(G)MSC

Client/Utilisateur du partenaire wholesale

Réseau Tiers (Fixe ou mobile domestique/International

1 leg

BTSBSC

(G)MSC

Client/Utilisateur du partenaire wholesale

Réseau Tiers (Fixe ou mobile domestique/International

ACCESS/ORIGINATION OF ON NET CALLS + TERMINATION

ACCESS/ORIGINATION OF ON NET CALLS

MNOMNO

MNOMVNO end user Other end user

3rd party Network

(Fix Mobile or International)

3rd party Network

(Fix Mobile or International)

MVNO end user

MVNO end user

Nov 28, 2006

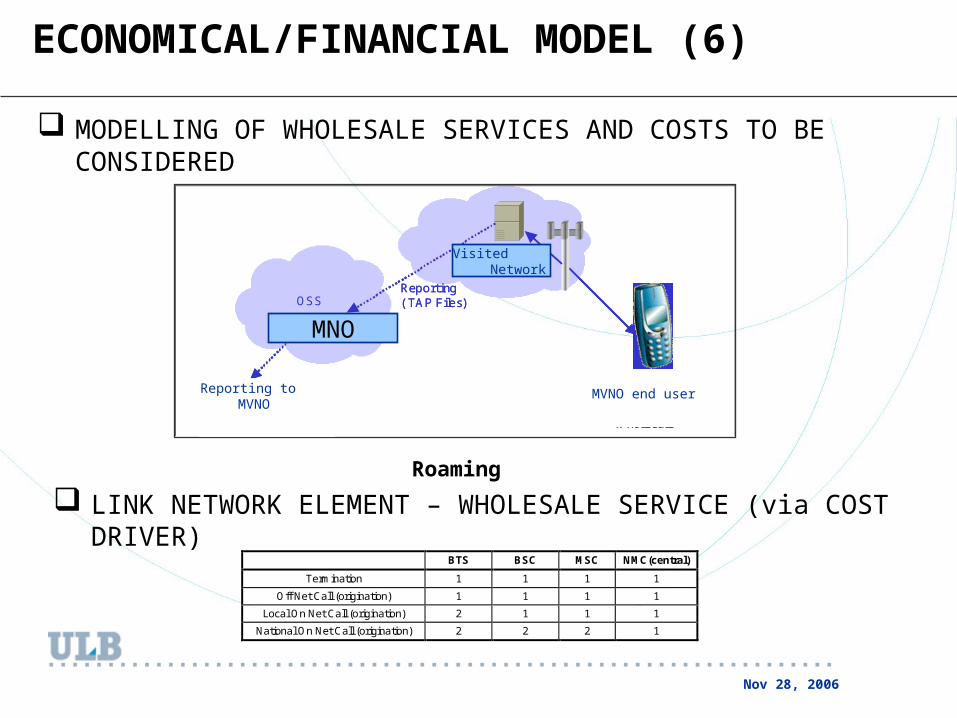

ECONOMICAL/FINANCIAL MODEL (6)

MODELLING OF WHOLESALE SERVICES AND COSTS TO BE CONSIDERED

Client/Utilisateur du partenaire wholesale

Réseau Mobile Visité

Reporting( TAP Files)OSS

Reportingvers partenaire

wholesale

Client/Utilisateur du partenaire wholesale

Réseau Mobile Visité

Reporting( TAP Files)OSS

Reportingvers partenaire

wholesale

Roaming

LINK NETWORK ELEMENT – WHOLESALE SERVICE (via COST DRIVER)

BTS BSC MSC NMC(central)

Termination 1 1 1 1

Off Net Call (origination) 1 1 1 1

Local On Net Call (origination) 2 1 1 1

National On Net Call (origination) 2 2 2 1

MNO

Visited Network

Reporting to MVNO MVNO end user

Nov 28, 2006

ECONOMICAL/FINANCIAL MODEL (7)

RESULTS: Off Net Calls Origination/Termination without GPRSCost to be removed from Interco Revenue for the off net Termination

Coût Moyen et Marginal pour l'Emission - Terminaison d'Appel Off Net

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

18.00

1 1.5 2 2.5 3 3.5 4 4.5 5 5.5 6 6.5 7 7.5 8 8.5 9

Capacité Réseau - milliards min/an

Co

ût

€c

en

t/m

in

Emission/Terminaison d'Appels Off Net (Moyen)

Emission/Terminaison d'Appels Off Net (MarginalThéorique)Emission/Terminaison d'Appels Off Net (MarginalRéaliste)

Average/Marginal Cost for the Origination & Termination of Off Net Calls

Cos

t €c

ent/

min

Network Capacity (billion min/year)

Origination/Termination - Average Cost

Origination/Termination - Marginal (Theoretical)

Origination/Termination - Marginal (Realistic)

Nov 28, 2006

ECONOMICAL/FINANCIAL MODEL (8)

GPRS Costs GPRS = Incremental Cost in a GSM Network (software upgrade)

• 1 channel reserved permanently for GPRS in the model channel reserved permanently for GPRS connectivity voice overcapacity decreases, incl. marginal costs as they are not constant….

Capacity millions MB/yr 5 10 15 20 25 30 35 40 45 50

BTS 1870 1870 1870 1870 1870 1870 1870 1870 1870 1870

BSC 18 18 18 18 18 18 18 18 18 18

MSC 1 1 1 1 1 1 1 1.5 1.5 1.5

NMC 0 0 0 0 0 0 0 0 0 0

BTS allocated 8.6% 8.6% 8.6% 8.6% 8.6% 8.6% 8.6% 11.0% 11.8% 13.2%

Coût Moyen et Marginal pour la Transmission GPRS à 10 Kps

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

0 5 10 15 20 25 30 35 40 45 50 55

Capacité Réseau - Millions Mbytes/an

Co

ût

€c

en

t/m

in

Moyen 10 KbpsMarginal Planifié 10 Kbps

Marginal Réaliste 10 Kbps

GPRS alone

Empty network dedicated to GPRS

Marginal Cost is flat (evident)

Network Capacity (billion min/year)

Cos

t €c

ent/

min

Average/Marginal Cost for the GPRS at 10 kbps

Nov 28, 2006

ECONOMICAL/FINANCIAL MODEL (9)

HOW TO DETERMINE PRICING (your own pricing and competition pricing)What cost should be considered ? Average Cost ? Forward Looking Cost (in order not to penalize the last entrant who host a MVNO) ? Direct sales enjoy this too as the network costs decrease too. Add interconnection costs/revenues in case of incoming traffic.

Coût Moyen et Marginal pour l'Emission d'Appel Local

0.00

4.00

8.00

12.00

16.00

20.00

24.00

28.00

32.00

1 1.5 2 2.5 3 3.5 4 4.5 5 5.5 6 6.5 7 7.5 8 8.5 9

Capacité Réseau - milliards min/an

Co

ût

€c

en

t/m

in

Emission d'Appel Local

Emission d'Appel Local (Marginal Théorique)

Emission d'Appel Local (Marginal Réalis te)

Re mplissage du réseau grâce à l'apport de trafic des

partena ires wholesale e t de la vente directe

(Moyen)

Coût Moyen et Marginal pour l'Emission d'Appel Local

0.00

4.00

8.00

12.00

16.00

20.00

24.00

28.00

32.00

1 1.5 2 2.5 3 3.5 4 4.5 5 5.5 6 6.5 7 7.5 8 8.5 9

Capacité Réseau - milliards min/an

Co

ût

€c

en

t/m

in

Emission d'Appel Local

Emission d'Appel Local (Marginal Théorique)

Emission d'Appel Local (Marginal Réalis te)

Re mplissage du réseau grâce à l'apport de trafic des

partena ires wholesale e t de la vente directe

(Moyen)

Average/Marginal Cost for the Origination & Termination of Off Net Local Calls

Cos

t €c

ent/

min

Network Capacity (billion min/year)

Origination/Termination - Average Cost

Origination/Termination - Marginal (Theoretical)

Origination/Termination - Marginal (Realistic)

Capacity filled with supplementary traffic

Nov 28, 2006

ECONOMICAL/FINANCIAL MODEL (10)

HOW TO DETERMINE PRICINGSpecial Case of Roaming: Cost plus = Retail minus via IOT Cost of Special Services: according to the provision of service:• SIM manufacturing • Use of Storage Capacity for Voice mail/HLR • Use of processing power of prepaid platform• Legal Tapping• Fraud Monitoring

Nov 28, 2006

ECONOMICAL/FINANCIAL MODEL (11)

Comparison with a Generic Cost Model From a Typical Regulator How a regulator will audit you if it imposes MVNO with cost orient.

“BIPT/ANALYSIS GENERIC MODEL” “PRESENT MODEL”Top Down Bottom Up

LRIC (Long Run on Incremental Prices) par opposition au FDC-FAC (that considers only past investments)

Emphasis on Incremental Costs because they are the most efficient according to theory.

LRAC (Long Run on Average Prices)

Emphasis on average costs but anticipated in 2 years.

Generic Cost Model applied to MNO specific data (this was not the case for fix telephony)

Idem

UMTS and Commercial Costs not considered (although were considered before even with MNO notified as SMP)

No Commercial Cost

No UMTS Costs

Economical depreciation (not an accounting depreciation)

Accounting Depreciation

Nov 28, 2006

AGENDA

A few facts/figures to frame MVNO in today’s context- How do telecom groups react today towards MVNO: Opportunity or Threat

- MVNO and Segmentation…Same Answer for the Same Issue

- What a MVNO can bring to capture market shares

Back to Theory….- Definition of MVNO

- Strategic Models of MVNO

- Regulatory Aspects

- How a MNO should organize its operations ot host MVNOs

- Economical Models

- Case Study: why no corporate MVNO exist ?

- State of MVNO market within EU

- Conclusion

How MNO Should Respond to MVNO entry

Nov 28, 2006

REGULATORY ASPECTS

Impact of the NRF (New Regulatory Framework)Authorization Directive replaces the licensing regime by a notification regime unless scarce resources are concerned. This makes MVNO entry easier

Impact of MVNOs on market definitions and dominanceAccess Market (Market 15) Marché de l’Accès Mobile

MVNO provokes an uncoupling between access and origination

MVNOs decrease simple dominance ( a little) but especially joint dominance (players so tacit collusion )

Termination Market (Market 16)Simple Dominance for fix to mobile calls and Joint Dominance for mobile to mobile calls.

MVNO provokes more substitution if it can resell mobile termination.

MVNO Modifies the perimeter of the market (especially if he is a fix operator) and can make it more convergent.

Simple Dominance decreased if MVNO can resell mobile termination

BUT: simple dominance will transform in joint dominance if only a few MVNOs (so we should not a policy of big MVNOs)

Opportunity to introduce RPP ? As it makes the externality more symmetric for fix to mobile.

Other Remedies: (1) Clearing House for mobile termination (2) bill and keep (back to back of externality)

Roaming Market (Market 17) MVNO will have no imapct due to cartel game between mobile operators.

Remedy: Create a secondary market outside the GSM Association

Some models are able to decrease the dominance on this market (TRANSATEL).

Nov 28, 2006

AGENDA

A few facts/figures to frame MVNO in today’s context- How do telecom groups react today towards MVNO: Opportunity or Threat

- MVNO and Segmentation…Same Answer for the Same Issue

- What a MVNO can bring to capture market shares

Back to Theory….- Definition of MVNO

- Strategic Models of MVNO

- Regulatory Aspects

- How a MNO should organize its operations to host MVNOs

- Economical Models

- Case Study: why no corporate MVNO exist ?

- State of MVNO market within EU

- Conclusion

How MNO Should Respond to MVNO entry

Nov 28, 2006

MODELS OF ORGANIZATION (1) EVOLUTION OF INTERCONNECTION BETWEEN OPERATORS

First strong link with the Regulatory/Legal

ONP Obligation has provoked the shift of interconnection to a P&L driven entity upstream from retail in order to make no discrimination between new entrants and one’s own retail operations.

This constitutes the basis to host MVNO: MVNO are a form of extension of interconnection/access to operators with no or with partial infrastructure.

OBJECTIVES OF A MVNO-minded ORGANIZATIONAvoid the usually protectionist behavior

- Delay Provisioning of MVNOs (eg: MNP et i-mode)

- Retain information or discriminate their release to MVNOs (so one must set up of wholesale at network side)

- Unbundling not granular enough (Threat of cannibalization will determine the right level of unbundling)

- Demand unuseful guarantee in regard to the service delivered

- Not the same quality of service is delivered to MNO and one’s own retail operations.

- Utilize the information collected with MVNO for competition purposes (Chinese Wall) (so one must set up of wholesale at network side)

- Pricing Policy not transparent enough (e.g.T-Mobile and VIRGIN Mobile)

Nov 28, 2006

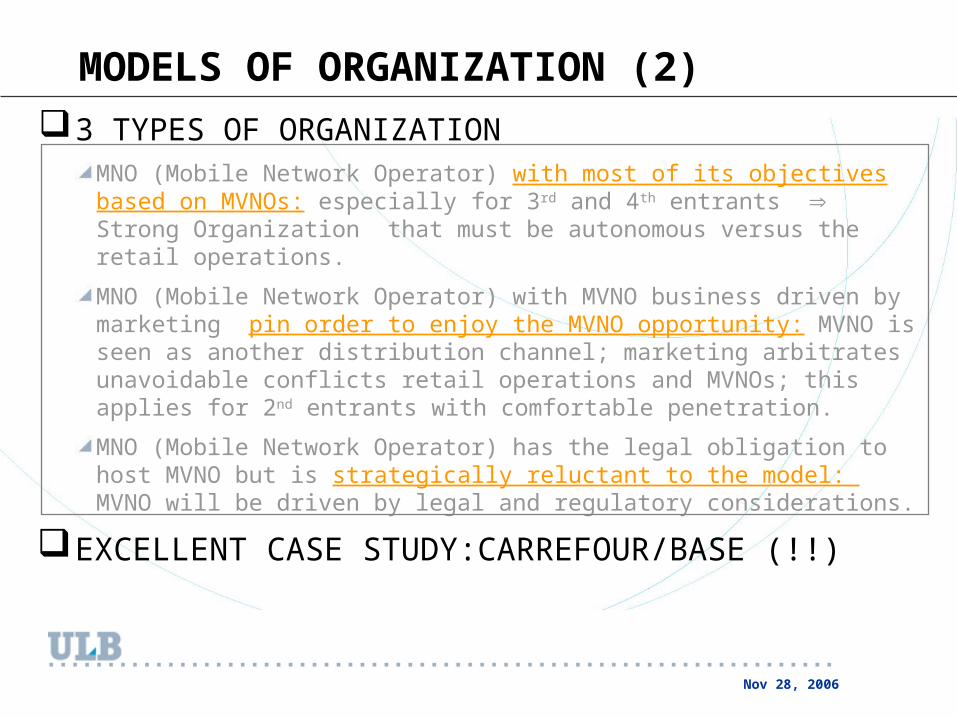

MODELS OF ORGANIZATION (2)

3 TYPES OF ORGANIZATIONMNO (Mobile Network Operator) with most of its objectives based on MVNOs: especially for 3rd and 4th entrants Strong Organization that must be autonomous versus the retail operations.

MNO (Mobile Network Operator) with MVNO business driven by marketing pin order to enjoy the MVNO opportunity: MVNO is seen as another distribution channel; marketing arbitrates unavoidable conflicts retail operations and MVNOs; this applies for 2nd entrants with comfortable penetration.

MNO (Mobile Network Operator) has the legal obligation to host MVNO but is strategically reluctant to the model: MVNO will be driven by legal and regulatory considerations.

EXCELLENT CASE STUDY:CARREFOUR/BASE (!!)

Nov 28, 2006

MODELS OF ORGANIZATION (3) OBJECTIVE OF A WHOLESALE ORGANIZATION THAT IS MVNO-minded

Set up of the organization: • Outside and upstream of retail operations, inside the technical department.

Give the organization a P&L responsibility

In order for it not to discriminate between MVNO and retail operations

WHOLESALE SERVICES

Product Lines:RoamingInterconnectionConnectivity/Access

ICT Production

Technical Product Management

Intercon -nect

Roaming

BASE Retail

3rd Party Retail

Mass

M

ark

et

Busi

ness

M

ark

et

Whole

sale

M

ark

et

Carr

ier

Mark

et

(roam

ing

/In

terc

o)

ICT

Sales & MKT

ICT Production

Technical Product Management

Intercon -nect

Roaming

BASE Retail

3rd Party Retail

Mass

M

ark

et

Busi

ness

M

ark

et

Whole

sale

M

ark

et

Carr

ier

Mark

et

(roam

ing

/In

terc

o)

ICT

Sales & MKT

ICT Production

Technical Product Management

Intercon -nect

Roaming

Retail

3rd Party Retail

Mass

M

ark

et

Busi

ness

M

ark

et

Whole

sale

M

ark

et

Carr

ier

Mark

et

(roam

ing

/In

terc

o)

ICT

Sales & MKT

Nov 28, 2006

AGENDA

A few facts/figures to frame MVNO in today’s context- How do telecom groups react today towards MVNO: Opportunity or Threat

- MVNO and Segmentation…Same Answer for the Same Issue

- What a MVNO can bring to capture market shares

Back to Theory….- Definition of MVNO

- Strategic Models of MVNO

- Regulatory Aspects

- How a MNO should organize its operations ot host MVNOs

- Economical Models

- Case Study: why no corporate MVNO exist and other cases

- State of MVNO market within EU

- Conclusion

How MNO Should Respond to MVNO entry

Nov 28, 2006

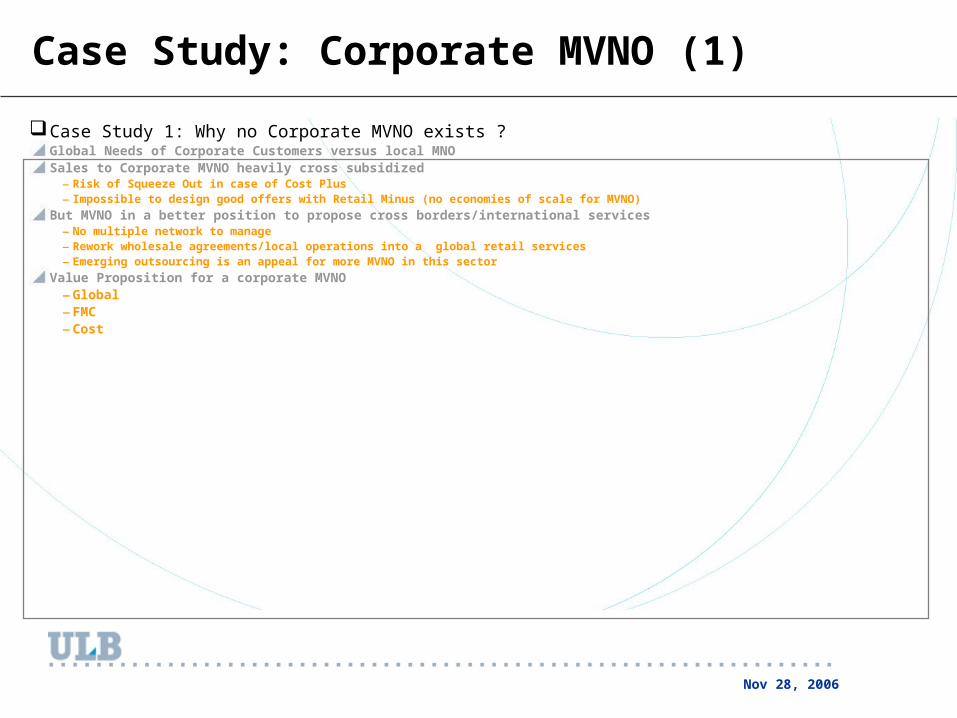

Case Study: Corporate MVNO (1)

Case Study 1: Why no Corporate MVNO exists ?Global Needs of Corporate Customers versus local MNO Sales to Corporate MVNO heavily cross subsidized

– Risk of Squeeze Out in case of Cost Plus– Impossible to design good offers with Retail Minus (no economies of scale for MVNO)

But MVNO in a better position to propose cross borders/international services – No multiple network to manage– Rework wholesale agreements/local operations into a global retail services– Emerging outsourcing is an appeal for more MVNO in this sector

Value Proposition for a corporate MVNO–Global–FMC–Cost

Nov 28, 2006

Case Study: Corporate MVNO (2)

MOBILE OPERATORS or GROUPS ARE COUNTRY-minded

Recent History of Mobile Operators – licenses are national

P&L of ORANGE & VODAFONE are local, not global

FreeMove et STARMAP = presales master agreement ou brand agreement

SYMPAC: is KPN credible with only 3 real networks and an image of competitor when it asks for a MVNO agreement → Risk for SYMPAC to become a new FreeMove…

TELE2 is the only multi country MVNO but its residential positioning prevent it to leverage this….

Nov 28, 2006

Case Study: Corporate MVNO (2): Business Plan

CAPEX AssumptionsInterconnection to 5 mobile operators : 100 000 €

Take on its own the billing chain till mediation rating: 20000 €

Interconnection as an enhanced service provider + use of MVNE OSS (economies of scope of MVNE towards MNO) : 30 000 €

OPEX AssumptionsSet up cost of 10 000 € for the first 5000 end users

2 €/SIM/month beyond 5000 users

Activation Cost of 5 € per new user

CRM outsourced to the MVNE.

Calcul du Break Even en Nombre de SIM Cards Actives

-60 €

-40 €

-20 €

0 €

20 €

40 €

60 €

0 10000 20000 30000 40000 50000 60000

Nombre de SIM Cards

Coû

t/Pro

fit P

ar S

IM C

ard

(€)

CAPEX par utilisateur

OPEX per end user

Total cost par utilisateur

Profit par utilisateur

ARPU & Cost Per User 70 €

OPEX: 2.5 €/month (Life cycle of 12 months)

CAPEX: 5 € (base de 30 000 utilisateurs)

SG&A de 17 %

wholesale fee paid to the mobile operator:60 €

CAPEX amortized immediately

Break even vs Active SIM cards

Cos

t/P

rofit

per

SIM

car

d

# SIM cards

Nov 28, 2006

CASE STUDY: Belgium

Case Study 3: Belgium Mix between Option 2 and Option 4 with recently Option 1 BASE (3rd entrant) has started a MVNO program in 2001

– Ethnic/Niche MVNO– Use of MVNE to aggregate small MVNOs– CARREFOUR bypasses BASE to engage with an MVNE– War price CARREFOUR/BASE on prepaid cards

MOBISTAR (2nd entrant) – Has decided to not to miss this opportunity even if it does not need it– Use of MVNE as ASP (same MVNE present within BASE and MOBISTAR) – Co-branding with CARREFOUR Competitor (DELHAIZE – Loyalty program) – MVNO with 3 play CATV operator TELENET

PROXIMUS (incumbent) –What will they do ?

Nov 28, 2006

AGENDA

A few facts/figures to frame MVNO in today’s context- How do telecom groups react today towards MVNO: Opportunity or Threat

- MVNO and Segmentation…Same Answer for the Same Issue

- What a MVNO can bring to capture market shares

Back to Theory….- Definition of MVNO

- Strategic Models of MVNO

- Regulatory Aspects

- How a MNO should organize its operations ot host MVNOs

- Economical Models

- Case Study: why no corporate MVNO exist ?

- State of MVNO market within EU

- Conclusion

How MNO Should Respond to MVNO entry

Nov 28, 2006

BRIEF OVERVIEW OF EU MARKETS (1)

Types of MVNO

Key Success Factors of 1st Generation MVNOs Efficient Distribution ChannelsGood MarketingBrand or NicheNew Content or Content/Service Making the Difference

France as an exception…. Cobranding only - no new brand creaetd by MNOMNO plays the role of MVNERetail MinusIncumbent very active

Country Penetration Group Denmark > 20 % Finland, Norway, Sweden > 10 %

Group 1

Netherlands , United Kingdom > 5 % Group 2 Austria > 2 % Reste of Europe < 2 %

Group 3

Nov 28, 2006

CONCLUSIONS

Mobile Market is not competitive enough

Oligolopy revenues

Too much integrated vertically• No more price competition/No more innovation

Root cause: ownership of scarce resources, assets not replicable,….

Impact of MVNOMVNO remedy for access/origination and termination

MVNO breaks the vertical integration but must be hosted by the last entrant

MVNO today: a lost generation (see USA…) with a focus on price war….

Case StudyMVNO will appear in all network economies that get deregulated