numer - dbs.com.sg tianjin, and inner mongolia), it could increase by over 30%. thus, we...

TRANSCRIPT

DBS Group Research • May 2017DBS Asian Insights42n

um

ber

SECTOR BRIEFING

China Pharmaceutical Sector Inflection Point Emerging

19

DBS Asian Insights SECTOR BRIEFING 4202

China Pharmaceutical Sector Inflection Point Emerging

Produced by:Asian Insights Office • DBS Group Research

go.dbs.com/research @dbsinsights [email protected]

Goh Chien Yen Editor-in-ChiefJean Chua Managing EditorGeraldine Tan EditorMartin Tacchi Art Director

Mark KONG Senior Equity Analyst DBS Group [email protected]

Dennis LAM Senior Equity Analyst DBS Group [email protected]

19

DBS Asian Insights SECTOR BRIEFING 42

03

0405

Introduction

Sales Growth Set to Rebound in 2017

Impact of Price Cuts

Criteria to Select Winners

he Chinese pharmaceutical sector’s sales growth has been decelerating from 19% in 2013 to 9% in 2016 due to the government’s cut in average selling prices (ASP). We believe growth could rebound by late-2017 as two forces emerge: 1) The number of drugs reimbursable from public medical insurance programmes

will increase by over 17% in 2017 and 2) the percentage of China’s floating population (2015: 247 million) under effective public medical insurance protection should increase from 20-32% in 2016 to over 50% in 2018.

For equity investors looking to invest in the pharmaceutical sector or bankers seeking potential customers in the pharmaceutical industry, it is important for them to figure out who will be the long-run winners. We have a set of criteria to pick long-run winners. Our criteria evaluate the growth potential of a player’s current drugs portfolio by looking at the drugs’ exclusiveness, market size, and medical institutes’ incentives to promote them, as well as the player’s ability to launch new drugs in the next three years.

Our proprietary research on the growth trends in China’s pharmaceutical industry and development of criteria to analyse the growth potential of pharmaceutical products are based on in-depth interviews with 1) the management of 19 pharmaceutical companies listed in Hong Kong and mainland China; 2) 10 managers in charge of finance and drug procurement for public hospitals; and 3) six bankers who have business relationships with pharmaceutical companies in China.

Introduction

T

DBS Asian Insights SECTOR BRIEFING 4204

The price cut imposed by the government has been dragging down the industry in the last five years. Recently, there have been two new forces emerging to support the industry’s sales growth. Thus, we believe the sales growth deceleration will end in 2017 and growth is likely rebound mildly in late-2017. The forces are:

Force 1: The number of drugs reimbursable from public medical insurance programmes will increase by over 17% this year. There are two reasons why this will happen:

A. The number of drugs reimbursable from public medical insurance programmes in rural areas could surge by over 30% in 2017, driving the demand for drugs. Based on National Bureau of Statistics data, the rural population made up 44% of the country’s total in 2015.

According to the “State council’s opinion on consolidation of basic medical insurance systems for residents in urban and rural areas” (國務院關於整合城鄉居民基本醫療保險制度的意見) issued in January 2016, the number of drugs reimbursable in rural public medical insurance programmes will be the same as in urban areas by 2017. As the number of drugs reimbursable in urban areas is much bigger than in rural areas, the number in rural areas will drastically increase.

In reference to the number in six provinces (Hebei, Shandong, Guangdong, Ningxia, Tianjin, and Inner Mongolia), it could increase by over 30%. Thus, we conservatively estimate the number of drugs reimbursable from public medical insurance programs in rural areas could surge by at least 30%.

B. The list of drugs reimbursable from public medical insurance programmes in both rural and urban areas are decided based on the National Reimbursement Drug List (“the List”). The new version of the List was released in February 2017. The number of drugs in the List has increased by 17%.

The first version of the List was released in 2000. The government revised it in 2004 and 2009. More medicines were included in each revision. Every time the List expanded, the industry’s sales growth accelerated remarkably in the following year. We believe this will stimulate the industry’s sales growth, similar to what happened in 2004 and 2009.

Sales Growth Set to Rebound in 2017

T

DBS Asian Insights SECTOR BRIEFING 42

05

DBS Asian Insights SECTOR BRIEFING 4206

Diagram 1. Chinese pharmaceutical industry sales growth (year-on-year)

Diagram 2. Chinese pharmaceutical industry sales

Source: CEIC Data, DBS Vickers *The drugs sales above consist of four segments: Chemical medicine,

biological product, Chinese prepared medicine, Chinese herb medicine

Source: CEIC Data, DBS Vickers *The drugs sales above consist of four segments: Chemical medicine,

biological product, Chinese prepared medicine, Chinese herb medicine

DBS Asian Insights SECTOR BRIEFING 42

07

Diagram 3. Pharmaceutical sales after expansion of National Reimbursement Drug List Reimbursement drug list

Source: www.cnstock.com, CEIC Data, DBS Vickers

Number of drugs increased in the National Reimbursement Drug List

Pharmaceutical industry sales growth acceleration in the following year

2004323 8.5ppt

(from 18.3% in 2004 to 26.8% in 2005)

2009340 6.2ppt

(from 20.9% in 2009 to 27.1% in 2010)

We believe the public medical insurance programmes have sufficient financial resources to fund the increase in reimbursable drugs. Based on the numbers from the National Bureau of Statistics and the National Health and Family Planning Commission, we estimate that the aggregate cumulative reserves of public medical insurance programmes in both urban and rural areas equalled 1.13 times of the programmes’ expenditures in 2015 (1,387 billion Chinese yuan/1,225 billion yuan = 1.13 times). That means the reserve is sufficient for the expense over the next 12 months even if there is no revenue. From 2011 to 2015, the revenue of those programmes had always been higher than the expenditure. On average, it was 20% higher annually. Thus, we can say these programmes are in good shape on the whole.

Force 2: China’s floating population of 247 million in 2015 made up 18% of the country’s total. As more of them will be able to claim medical expenses from public insurance programmes going forward, this will boost demand for drugs.

The floating population have public medical insurance accounts in their own registered domiciles. However, when they move to other places to live, it is very difficult for them to reimburse their medical expenses from the public medical insurance accounts in their own registered domiciles, due to lack of information, technology infrastructure, and communication among regional governments. Some of them can participate in the public medical insurance programmes where they live, but, based on a study by Peking University’s School of Economics, (we estimate that) this applies to only 20-32% of the total floating population. That implies that around 70% of the floating population are without effective public medical insurance protection.

To improve the medical coverage of the floating population, Li Keqiang, Premier of the State Council, in March 2016, required all regional governments to connect their public medical insurance programme systems within two years, in order to facilitate their medical expense claims.

By the end of 2016, each of the 30 provinces had successfully connected their cities’ public medical insurance programmes within its own province, according to the Ministry of

List of approved drugs

More medical claims

DBS Asian Insights SECTOR BRIEFING 4208

Human Resources and Social Security. This has already drastically halted the sharp decline in pharmaceutical sales growth – from an average annual drop of 3.9 percentage points in 2012-2015 to only 0.6 percentage points in 2016. The central government targets to achieve inter-province connection within 2017. With the government’s effort, we estimate the percentage of floating population under effective public medical insurance protection could gradually increase from around 30% in 2016 to over 50% in 2018.

With the above-mentioned two forces in play, we project the industry’s sales growth to stabilise at 8.9% in 2017 and rebound to 9-10% in 2018.

Impact of Price Cuts

Price cuts imposed by the government will still be a concern for the pharmaceutical sector. But the impact should be smaller than it was in 2015 and 2016 for two reasons:

Firstly, we believe provincial governments are now more careful before imposing price cuts, because if the cut were too harsh, many drug manufacturers would give up selling to the province. That impacts the overall drug supply to the province, which was exactly what has been happening in the last two years.

For example, according to China Daily, in Zhejiang province in 2015, a big price cut saw foreign players withdraw 60.5% of drugs sold to the public medical institutes through tender. To ensure a stable supply of drugs, some provinces became more flexible on price cuts. This was seen, for example, in Anhui province in 2015, when the provincial government imposed a substantial price cut on uremic clearance granules (UCG), Consun’s key product. (Consun did not disclose how much the cut was). Consun gave up the sales of UCG to the public medical institutes there in the 2015 second half, and was not the only drug maker to do so. That impacted the drug supply to Anhui. Eventually, the Anhui provincial government did not insist on implementing the new lower price. Consun is now selling UCG there at the original price.

Secondly, over half of 31 provinces completed their tenders for drugs in November 2015 to November 2016. The tenders decided the prices of drugs sold to public medical institutes there. As most provinces had already decided the prices and other provinces will make reference to the pre-determined prices in setting of their own prices, we believe drugs’ prices could be relatively stable in 2017 – more so than in 2015 and 2016.

We project the industry’s sales growth to stabilise at 8.9% in 2017 and rebound to 9-10% in 2018

DBS Asian Insights SECTOR BRIEFING 42

09

Criteria to Select Winners

Thanks to the industry sales growth rebound, it is now the time to revisit pharmaceutical companies, whether it is equity investors looking to invest in the pharmaceutical sector or bankers seeking potential customers in the pharmaceutical industry. It is important for them to figure out who will be the long-run winners. We have designed a set of criteria to select companies that may emerge as winners over the long run. The criteria look at two aspects of a pharmaceutical company: 1) the growth potential of the current products portfolio; and 2) the ability to launch new products in the future.

We believe if the drugs of a company hit certain criteria (see below), the drugs should be able to grow steadily. These are:

a) Its exclusiveness and, hence, ability to stand out against the competition; b) Its market size; and c) Incentives for medical institutes to prescribe it.

Growth potential of portfolio

Diagram 4. Criteria to evaluate the potential of a drug

Exclusiveness

1. Protected? Is the drug categorised as Class 1 or Class 2 by the China Food & Drug Administration (CFDA)?

Class 1: A drug with an innovative active ingredient or chemical structureClass 2: A drug with an innovative way to deliver known active ingredient

A drug categorised in either class is an exclusive product. Its exclusiveness protects it from competition so that it can enjoy more stable growth. For example, 3SBio’s (1530 HK) TPIAO, a recombinant human thrombopoietin injection, is a Class-1 medicine used for treatment of platelet deficiency. Its exclusiveness allowed its sales to grow at a 38% CAGR in 2012-2016 (from 210 million yuan to 765 million yuan).

2. Substitutable? Is the drug free from the potential threat of other drug(s) with the same or similar indication that are under clinical trial?

Other drugs with similar indication under clinical trial could threaten the current product. There are some websites providing such information, such as http://db.yaozh.com/

Market size

3. Reimbursable? Is the drug included in the reimbursable drugs list of public medical insurance programmes?

Such inclusion implies that patients' expenditure on the drug is subsided by public medical insurance programmes. As such, patients are more willing to take the drug, which warrants demand. Medicines included in the list are divided into Class A and Class B. The government subsidises 100% of Class-A expenditure while Class B will only be partially subsidised.

DBS Asian Insights SECTOR BRIEFING 42010

4. Nature of disease – fatal? Is the drug tackling a fatal disease with a large number of patients (e.g. stroke)?

A drug that tackles fatal diseases implies that patients cannot live without it. If the number of patients is large, there is higher demand.

For example, CSPC’s (1093 HK) NBP (Chinese name: 恩必普, chemical name: Butylphthalide) is a Class-1 drug used to treat acute ischemic stroke, which is a fatal disease with a large number of patients. Strokes cause around 1.5 million deaths annually. There are over seven million patients in China. The Chinese Center For Disease Control and Prevention projects there are two million new stroke patients each year. Thanks to the above, sales of NBP surged 41% (CAGR) in 2012-2016, from around 674 million yuan to 2.648 billion yuan.

5. Nature of disease – chronic? Is the drug tackling a chronic disease with a large number of patients (e.g. kidney failure)?

Patients suffering from chronic diseases need to take drugs for a long period of time, signalling consistent demand for certain drugs.

Consun’s (1681 HK) uremic clearance granules – an exclusive drug used to delay the onset of kidney failure, considered a chronic disease – is an example. We estimate there are over 50 million patients suffering from different stages of kidney failure. Due to the huge demand, the sales of uremic clearance granules had been growing at a 21% CAGR in 2010-2016, from 232 million yuan to around 710 million yuan.

6. Supply shortage? Is a significant portion of the drug supply in China satisfied by imports?

If so, this implies shortage of the product in China.

For example, human albumin products are plasma-based pharmaceutical products widely used in emergency rooms and intensive care units for surgery. They are used to remedy hypovolemia and hypovolemic shock, abnormally high intracranial pressure, edema, and ascites. According to the National Institutes for Food and Drug Control, in 2012-2015, 48-59% of the industry’s sales were generated by imports, implying supply shortage in China. In this period, industry sales grew at a 23% CAGR.

Market size

7. Market well established? Is the drug well established in the over-the-counter market (i.e. a five-year history and revenue over 100 million yuan)?

Drugs stores or over-the-counter (OTC) sales is the second-largest sales channel for drugs in China. According to IMS, it contributed 17% of pharmaceutical industry sales in 2016. Unlike the other two channels (hospitals and the third-party terminals), the suppliers providing drugs to the OTC channels need not to go through provincial tenders organised by the government. That implies they need not suffer from ASP cuts imposed by tenders. The price-cutting risk is smaller.

In the pharmaceutical universe, the continuous launch of new products on the back of a large product pipeline is the key to achieving strong earnings growth in long run.

To judge if the products pipeline or the research and development (R&D) capability of a drug company is strong, we look at the following aspects:

1. Is the drug to be launched an exclusive product in the market? Exclusiveness is a sign of strong R&D capability. It protects the drug from price-cutting risks due to competition from similar products.

Source: DBS Vickers

DBS Asian Insights SECTOR BRIEFING 42

011

If a drug is well received by the market, the supplier can even raise the price. For example, the cardiovascular drugs portfolio of Dawnrays (2348 HK), including amlodipine besylate tablets, levamlodipine besylate tablets, losartan potassium, hydroclorothiazide tablets, and telmisartan tablets, generate revenue of over 300 million yuan for Dawnrays. Although they are all generic drugs, they are well received by the OTC market. In January 2016, Dawnrays raised their ex-factory prices by double digits.

Incentive to prescribe

8. Core drug? Is the drug regarded as a first-line drug for the treatment of a disease by an authoritative industry association?

If it is regarded as first-line, it should be the first drug to be prescribed by physicians once they encounter the disease. This warrants demand.

For example, oseltamivir phosphate is regarded by the Chinese Medical Association as a first-line drug for the treatment of influenza, while the National Health and Family Planning Commission recommends it as the top drug for the treatment of H1N1 and H7N9 influenza. Its total sales in 2012-2014 grew 106% from 82 million yuan to 349 million yuan.

9. Markup allowed? When hospitals sell the drug, are they allowed to mark up over the procurement cost over the long run?

However, the mark-up of certain kinds of drugs in hospitals is still allowed, for example CCMG. As hospitals can continue to make money due to the mark-up, they have strong incentives to promote the product. Thanks to allowance of the mark-up, the sales of CCMG grew 28% (CAGR) in 2012-2015, from 4.6 billion yuan to 9.8 billion yuan. We believe it can maintain annual growth of around 20% in the next five years.

However, the mark-up of certain kinds of drugs in hospitals is still allowed, for example CCMG. As hospitals can continue to make money due to the mark-up, they have strong incentives to promote the product. Thanks to allowance of the mark-up, the sales of CCMG grew 28% (CAGR) in 2012-2015, from 4.6 billion yuan to 9.8 billion yuan. We believe it can maintain annual growth of around 20% in the next five years.

Sustaining strong earnings growth

Source: Companies, DBS Vickers

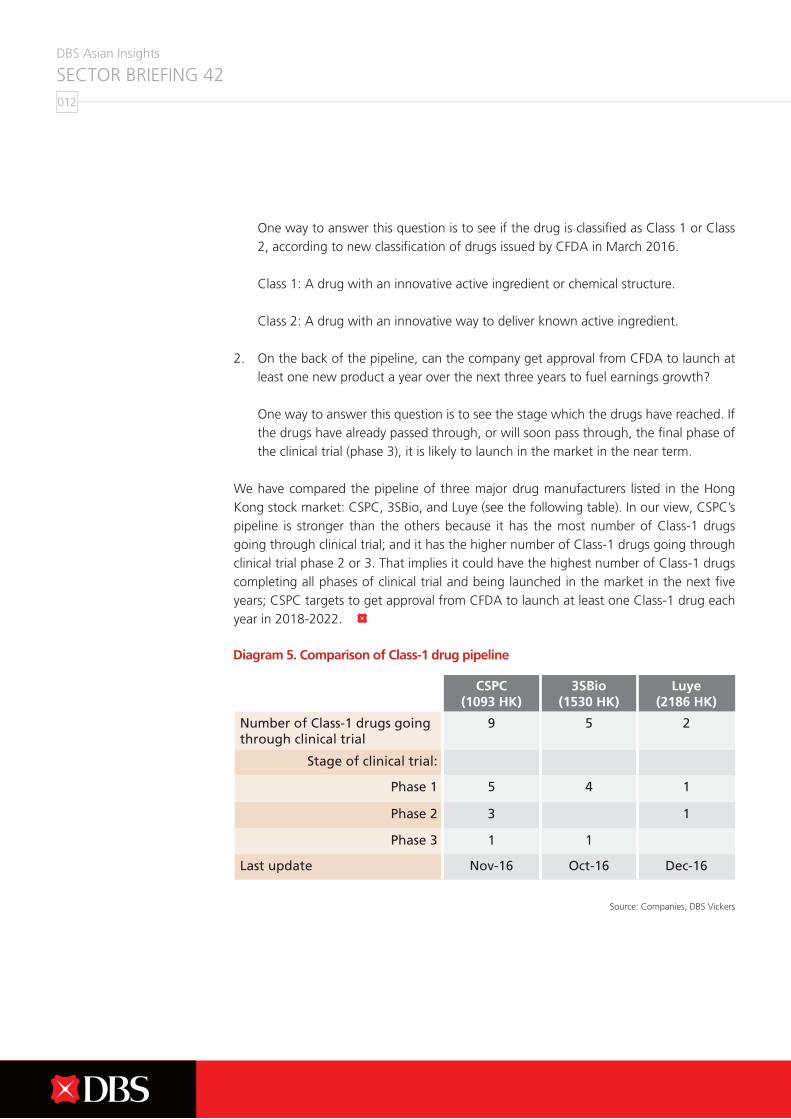

DBS Asian Insights SECTOR BRIEFING 42012

One way to answer this question is to see if the drug is classified as Class 1 or Class 2, according to new classification of drugs issued by CFDA in March 2016.

Class 1: A drug with an innovative active ingredient or chemical structure.

Class 2: A drug with an innovative way to deliver known active ingredient.

2. On the back of the pipeline, can the company get approval from CFDA to launch at least one new product a year over the next three years to fuel earnings growth?

One way to answer this question is to see the stage which the drugs have reached. If the drugs have already passed through, or will soon pass through, the final phase of the clinical trial (phase 3), it is likely to launch in the market in the near term.

We have compared the pipeline of three major drug manufacturers listed in the Hong Kong stock market: CSPC, 3SBio, and Luye (see the following table). In our view, CSPC’s pipeline is stronger than the others because it has the most number of Class-1 drugs going through clinical trial; and it has the higher number of Class-1 drugs going through clinical trial phase 2 or 3. That implies it could have the highest number of Class-1 drugs completing all phases of clinical trial and being launched in the market in the next five years; CSPC targets to get approval from CFDA to launch at least one Class-1 drug each year in 2018-2022.

Diagram 5. Comparison of Class-1 drug pipeline

CSPC (1093 HK)

3SBio(1530 HK)

Luye(2186 HK)

Number of Class-1 drugs going through clinical trial

9 5 2

Stage of clinical trial:

Phase 1 5 4 1

Phase 2 3 1

Phase 3 1 1

Last update Nov-16 Oct-16 Dec-16

DBS Asian Insights SECTOR BRIEFING 42

013

DBS Asian Insights SECTOR BRIEFING 42014

Disclaimers and Important Notices

The information herein is published by DBS Bank Ltd (the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee.

The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof.

The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies.

The information herein is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation.

DBS Asian Insights SECTOR BRIEFING 42

015

www.dbs.com

Living, Breathing Asia