ny2014 welcomefiles.shareholder.com/downloads/meli/3476042122x0x786527/...bomnegocio 13,284 walmart...

TRANSCRIPT

Welcome To the Second

NY2014

This presentation may make forward-looking statements relating to such matters as continued growth prospects for

the company, industry trends and product and technology initiatives. These statements are based on currently

available information and our current assumptions, expectations and projections about future events. While we

believe that our assumptions, expectations and projections are reasonable in view of currently available information,

you are cautioned not to place undue reliance on these forward-looking statements. Our actual results may differ

materially from those included in this presentation, for a variety of reasons, including those described in the forward-

looking statements and risk factor sections of our 10-K and other filings with the Securities and Exchange

Commission, which are available on our investor relations website. (http://investor.mercadolibre.com)

All of the information included in this presentation is updated as of October 15th, 2014. Except as may be required

by applicable law, we assume no obligation to publicly update or revise our statements.

Welcome and Company Overview – Marcos Galperín (CEO)

Marketplace – Stelleo Tolda (COO)

Payments – Osvaldo Giménez (MercadoPago EVP)

Coffee Break

Technology – Daniel Rabinovich (CTO)

Financial Overview – Pedro Arnt (CFO)

Q&A session

Lunch Break

End of the event

Agenda New York October 15, 2014

Company overview Strategic Summary

Marcos Galperín (CEO)

eCommerce is still very early

stage in Latin America

2013 eCommerce Penetration of Total Retail

Source: Euromonitor

0%

5%

10%

15%

The opportunity ahead is enormous;

LATAM eCommerce market to double by 2018

% of Total Retail (LATAM) 2.1 % 2.4 % 2.7 % 3.0 % 3.3 % 3.8 %

% of Total Retail (USA) 7.4 % 8.2 % 9.0 % 9.9 % 10.8 % 11.6 %

2013 2014 2015 2016 2017 2018

CAGR

(13-18)

20 %

10 %

17 %

14 %

Rest of LATAM Argentina

Mexico Brazil

Source: Euromonitor

CAGR 16%

$23B $27B

$31B $36B

$41B

$47B

As the leader in all of its

markets, MELI is poised to

benefit from these tailwinds

Source: Comscore August 2014 (Desktop only)

Brazil

24,675

Netshoes 17,074

Americanas.com 14,689

OLX 14,655

BomNegocio 13,284

Walmart 12,463

Buscapé 11,489

Submarino 9,290

Magazineluiza.com 8,145

AliExpress 8,234

Argentina

7,640

AlaMaula 2,223

OLX 2,101

Amazon 1,678

NetShoes 956

Garbarino 896

Frávega 856

Musimundo 715

Netflix 675

Falabella 667

4,471

VivaAnuncios 2,153

Amazon 2,029

Ebay 1,749

Netflix 1,278

Apple 1,265

Segundamano.mx 1,256

Walmart 1,019

TicketMaster 1,011

Trovit 871

Mexico Venezuela

4,100

Amazon 2,416

OLX 1,123

QueBarato! 415

Apple 401

Ebay 362

Clasf 209

Alibaba.com 209

VivaStreet 191

HP 188

Colombia

2,319

Amazon 968

OLX 930

Ebay 707

Linio 516

Apple 502

Buscapé 472

Exito 468

Trovit 457

Dafiti 441

1,271

Yapo.cl 934

Falabella 924

Amazon 663

Sodimac 622

OLX 599

Paris.cl 589

Riplay 563

Buscapé 468

QueBarato! 393

Chile

864

OLX 566

Amazon 564

Falabella 366

Linio 293

Apple 263

Nuestromercado 249

Ebay 232

Neoauto.com 227

Urbania.pe 209

Peru

Unique Visitors (K)

Consistent focus on seven strategic initiatives

Drive payments

growth both on

and off MercadoLibre

Spread desktop leadership

to mobile, managing an

accretive transition

Drive shipping adoption through

MercadoEnvíos, paving the way

for complete logistics solutions

Attract new vendor

segments: brands,

manufacturers, and large retail

Generate developers

ecosystem on top of MELI´s

open platform

Bring tailored vertical

solutions to a growing

number of product categories

Invest in CX, transforming it

into a clear competitive

advantage

We continue to

Advance new

solutions on a

growing platform

Logistics

service

Your own

virtual store

Send &

receive

payments

Advertise & grow

your sales

We still have room to expand existing solutions

across our current markets

Monetized marketplace On-platform Off-platform Financing Marketplace

Brazil

Argentina

Mexico

Venezuela

Colombia

Chile

Uruguay

Peru

Ecuador

Costa Rica

Dominican Republic

Panama

Portugal

We are building an enhanced marketplace

…With significant

volume across

the platform in

the past year

6M items

shipped

112K active

virtual stores

37M

Transactions

13K

Advertisers

90M

Items Sold

There is still much more opportunity to capture

in the market and within MercadoLibre

Note: Figures not drawn to scale, Numbers shown are approximate

Source: WorldBank, Euromonitor, ComScore, Company Estimates

Mercado

Libre 600M People

300M Internet Users

200M

Online Shoppers

Latin

America GMV

TPV

Financing

Mercado

Envios

MercadoLibre is best positioned to capture

the immense opportunity

Source: ComScore, Company

Market presence Presence in 12 countries in Latin America

Largest online payment network in the region

Experienced Management Founder and senior management team

at MELI since inception

Industry and regional expertise

Leading eCommerce brand Traffic leader in all markets

Top of mind in eCommerce

Network externalities favoring

leadership and scale 24M Live Listings, unmatched in prices and selection

7M Annual Sellers

21M Annual Buyers

Solid financials One of few profitable e-commerce models in the region

Strong balance sheet, $500M+ Cash

Strong IT Team Proven, large and rapidly growing Tech Team

500 IT resources

Marketplace

Stelleo Tolda (COO)

The scale of our

marketplace

attracts sellers

and buyers

across Latin

America

24M Live Listings

21M

Buyers

90M Items

Purchased

7M

Sellers

$7.6B

GMV

Note: Live listings as of June 2014; other data shown represents trailing twelve months through June 2014

Our marketplace continues to show

strong growth in key metrics

Note: TTM = Trailing twelve months

Successful Items (M) Gross Merchandise

Volume ($B) Sellers (M) Buyers (M)

0

2

4

6

8

June 2011TTM

June 2014TTM

0

2

4

6

8

June 2011TTM

June 2014TTM

0

20

40

60

80

100

June 2011TTM

June 2014TTM

0

5

10

15

20

25

June 2011TTM

June 2014TTM

CAGR:

20%

CAGR:

17%

CAGR:

27%

CAGR:

25%

It is evolving into an enhanced marketplace

From To

Marketplace

Mostly electronics

Targeted shopping

Hobby sellers

Reactive customer support

eCommerce facilitator

Unmatched selection

Verticalized experiences

SMBs and Large Retail

Proactive customer management

We are maximizing

our user experience

through integrated

platform solutions

Marketplace eCommerce facilitator

Marketplace eCommerce facilitator

Mobile is an

increasingly

important source

of traffic,

registrations and

transactions

16%

of GMV

31%

of New

Registrations

Note: As of June 2014

Marketplace eCommerce facilitator

MercadoEnvios, our new logistics solution,

has gained significant traction since launch

25% Penetration

in Brazil

8% Penetration

in Argentina

6M Items shipped

in the last year

Note: Penetration represents percentage of items sold in June 2014

Marketplace eCommerce facilitator

Brazil, our most advanced

market, shows how current

and future initiatives come

together 58% 33% 25% 11%

Investor Day 2011

% of GMV*

*as of June 2014

Mostly electronics Unmatched selection

Selection is expanding rapidly as more

categories develop

Successful Items Listings (M)

0%

20%

40%

60%

80%

100%

Q2 2011 Q2 20140

5

10

15

20

25

Q2 2011 Q2 2014

Consumer

Electronics

Fashion &

Body Care

Home & Outdoors

Entertainment

& Hobbies

Autoparts

Others

Entertainment

& Hobbies

Consumer

Electronics

Fashion &

Body Care

Autoparts

Home & Outdoors

Others

Consumer

Electronics

Fashion &

Body Care

Home & Outdoors

Entertainment

& Hobbies

Autoparts

Others

Entertainment

& Hobbies

Consumer Electronics

Fashion & Body Care

Autoparts Home & Outdoors

Others

Targeted shopping Verticalized experiences

We have

verticalized

our Fashion

pages

Targeted shopping Verticalized experiences

Our Classifieds sites offer vertical experiences

for Motors, Real Estate, and Services

Motors Real Estate Services

Targeted shopping Verticalized experiences

We have acquired

leading vertical

properties in

the region

Hobby sellers SMBs and Large Retail

We are

building

a mall on

our platform

The meritocracy of our marketplace

drives B2C growth and quality product selection

Hobby sellers SMBs and Large Retail

Products sold on our platform are

98% Fixed Price

89% New

70% B2C

0%

20%

40%

60%

80%

100%

Sellers Listings SI GMV

B2C

B2C

B2C B2C

C2C C2C

C2C

C2C

Note: As of Q2 2014

Reactive customer support Proactive customer management

We are transforming

customer experience

into a competitive

advantage

Decreased contact rate

Increased number of channels

Increased NPS

100

105

110

115

120

125

130

135

NPS (Base 100) March 2012 – June 2014

Technology

Daniel Rabinovich (CTO)

Technology foundations

Quick look into some of the things we’ve been doing

Open Platform

Agenda

Split MELI into 100 interconnected “cells” Each cell operates as if it were a separated company

Dramatic Lift in the Pace of Execution Descentralized teams deploy into production at their own pace

1 5,000 Huge Deploy

a Week

Small Deploys

a Week

Decoupling enabled healthy team growth Doubled our team in the last 3 years. We’re in good shape to continue growing.

Deep Technology Overhaul Monolithic -> Decoupled

Technology Foundations

Quick look into some of the things we’ve been doing

Open Platform

Agenda

Design Overhaul – New Home Page example New Design Standards + Curated Content

Merchandising Push Notifications Curated content

Leveraged Data – An Example Search is constantly “learning” from our users, finding real time new trends

New iPhone 6

(Subexposed)

Old iPhone 5s

(Overexposed)

Click-through rate

Row in search results

Verticalized the Experience (Real Estate) Challenge was to seamlessly verticalize from the regular search box

Belgrano

“neighborhood”

Belgrano “street”

Ambiguities

Verticalized the Experience (Fashion)

Standardized thousands

of different retailers in

one consistent product

Studio Quality Pictures:

Enforced using machine learning

algorithms to detect good pictures

Multi-SKU (Size, Color)

Blends different standards in

one consistent scale

Official Stores: a Mall inside the Marketplace Gradually creating a premium, curated marketplace

Customized “Environment” Brand Logo Search in the Store

Shipping: a strong Drop-Ship implementation

Same Day / Next Day delivery

+

Free Shipping

Delivery to carrier branch

(lockers):

faster and inexpensive

Along with payments, Shipping closes the loop to a great shopping experience

Went Multiscreen Solved four completely different environments, with minimum productivity lost

iOS Android Desktop Web Mobile & Tablets

Strong mobile penetration growth Mobile continues to gain share, as apps get better

16% mobile

GMV

2012 2013 2014

Mobile Off Platform: Payments Leveraged our infrastructure to launch a Wallet,

an in-app Payments SDK and a mPOS

Technology Foundations

Quick look into some of the things we’ve been doing

Open Platform

Agenda

From a Website to a Platform Built an API, rewrote our properties on top of it, and then opened to 3rd parties

External

innovation

unleashed An entire ecosystem

was created on top of

our Open Platform

A Strong impact on our ecosystam Power Sellers are using external tools to manage

sales (don’t use our platform directly)

25% Of new listings

are created through

our Open Platform

Technology Foundations

Quick look into some of the things we’ve been doing

Open Platform

Wrapping up…

Agenda

Wrapping Up...

Strong Technology Foundations

Performed a Design Overhaul

Big Data allows our product to “learn” from users

Verticalized the first Core Category (Fashion), more to come

Launched “Official Stores”, closer to a Mall experience

Strong progress in Shipping

Solid Progress on Mobile, 16% share and growing

Opened our Platform, 25% of New Listings from 3rd party apps

MercadoPago

Osvaldo Giménez (EVP MercadoPago)

MercadoPago facilitates online payments

Buyer’s CC

Buyer’s Bank

Account

Buyer’s Cash

Payment

Money in Money Through Money Out

Buyer’s

MP Account

Seller’s

MP Account

Fraud Prevention

Buyer Protection Program

Seller Protection Program

Seller’s Bank

Account

Revenue sources Countries Value Proposition

· Financing Revenues (On

and Off MercadoLibre)

· Processing Fee (Off

MercadoLibre)

· Bundled with FVFs on

MercadoLibre

· Brazil

· Argentina

· Mexico

· Colombia

· Venezuela

· Chile

· For buyers:

· Secure

· Convenient

· Offers installments

· For sellers:

· Easy & flexible to set up

· High conversion rate

· Large user base & stored cc’s

MercadoPago has experienced strong growth

Note: TTM = Trailing twelve months

Total

Payment Volume ($B)

Total

Transactions (M)

0

10

20

30

40

June 2011 TTM June 2014 TTM

0

1

2

3

June 2011 TTM June 2014 TTM

CAGR

54%

CAGR

43%

37M $2.8B

Five avenues for growth

Growth opportunities

Share of GMV Verticals

Countries

Cross Border

Open Platform

Revenues

Interest-free Financing

Cash Flow Positive

In App Payments

Mobile App

Mobile POS

Cobranded Credit Cards

Prepaid Cards

Seller Credits

Mercado

Libre

Merchant

Services Financing

Mobile

Payments

Buyer and

Seller Credit

MercadoLibre

Replicating the Strategy across MercadoLibre Free for buyers & bundled for sellers

Optimized fraud prevention for higher approval rates

Synergistic with Shipping

Integrated Payments for high ticket items

Chile Venezuela

Colombia Mexico Argentina Brazil

100% (of GMV)

Note: Figure not drawn to scale

Merchant Services

Retail

Coupons

Travel

Merchant services growing strongly

in top markets

Merchant Services

Verticals Countries Cross border Open Platform

Merchant Services opportunities

No credit risk Positive cash flow by selling receivables

Half of our TPV is paid in installments

0%

20%

40%

60%

80%

100%

TPV Credit Card TPV Financed TPV by Installments

2014 H1

Bank Transfer & Alternative

Payments

Credit Cards

Non-financed

Financed

12

+12

10

9

6

5

4

3

2

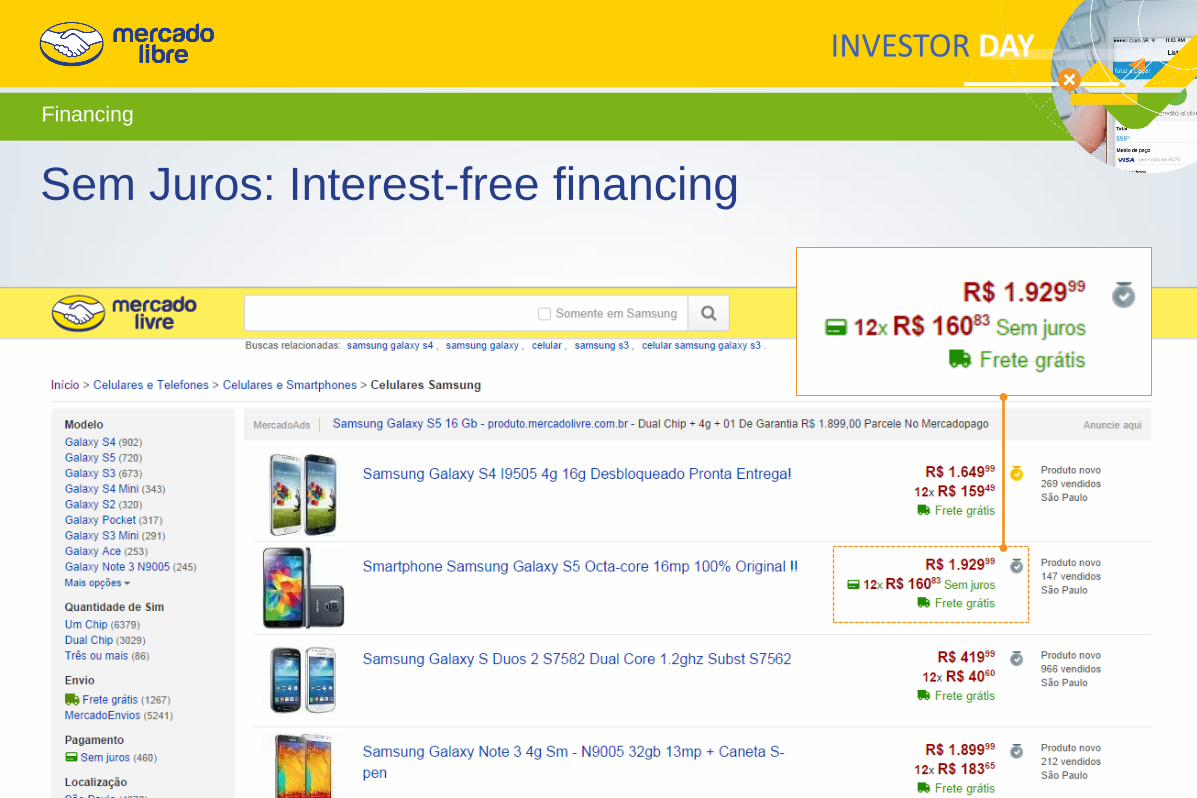

Financing

Financing

Sem Juros: Interest-free financing

Mobile

Mobile Payments

Mobile

POS

SDKs for In

App Payments

MercadoPago

Mobile App

Software Development Kits (SDKs)

for In App Payments

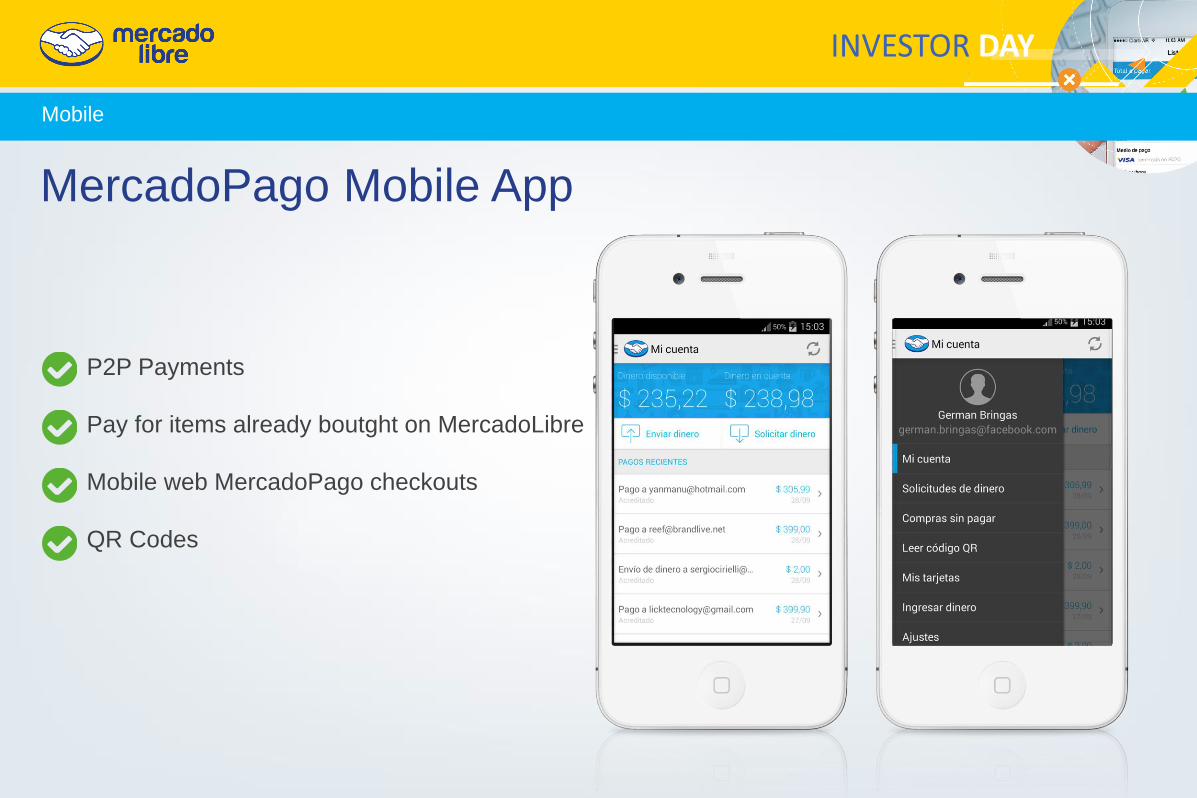

Mobile

MercadoPago Mobile App

P2P Payments

Pay for items already boutght on MercadoLibre

Mobile web MercadoPago checkouts

QR Codes

Mobile

Mobile POS Solution

Features

Interaction with seller stocks,

catalogues and billing systems

Store analytics

Client management tools

Ecosystem Synergies

Payments with MercadoPago balance

Withdrawals to MercadoPago’s

prepaid cards

Interaction with MercadoShops App

Mobile

Cobranded Credit Cards Prepaid Card in Mexico Seller Credit

Buyer and Seller Credit

We are expanding our services with cards and

credit

Focus on executing across key initiatives

Mercado

Libre

Merchant

Services

Financing Mobile

Payments

Buyer and

Seller Credit

Financial Overview

Pedro Arnt (CFO)

What we said…How we are doing

How we think about our financial model

Wrapping Up

Agenda

Strong & Diversified Top Line Growth

What we said in October 2011… Relevant aspects of our financial model

Healthy Gross Margin Profile Impacted by Mix Shift

Scale In Operating Expenses

Growth In Earnings

Cash Flow Generation

Robust Balance Sheet & Efficient Capital Structure

Sustained StrongTop Line Growth How we are doing …

Source: Company Data

216.7

298.9

373.6

472.6

247.2

6.4%

6.9%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

0

50

100

150

200

250

300

350

400

450

500

2010 2011 2012 2013 H1'2014

Millio

ns

Renevue

Take Rate

CAGR

30%

LC CAGR

39%

YoY Growth 15%

YoY Growth LC 58%

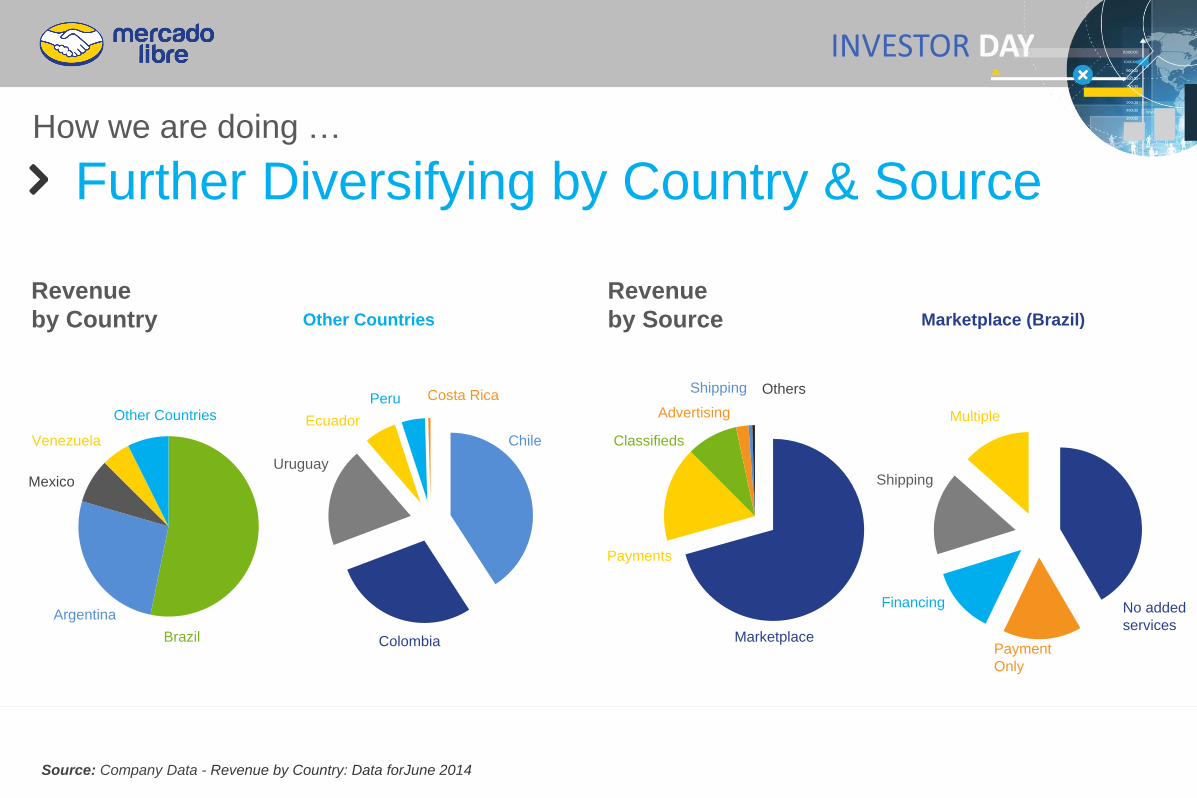

Source: Company Data - Revenue by Country: Data forJune 2014

Revenue

by Country Other Countries

Revenue

by Source

Brazil

Argentina

Mexico

Venezuela

Other Countries

Costa Rica Peru

Ecuador

Uruguay

Colombia

Chile

Marketplace

Payments

Classifieds

Advertising

Shipping Others

Marketplace (Brazil)

Further Diversifying by Country & Source How we are doing …

No added

services

Payment

Only

Financing

Shipping

Multiple

170

227

276

343

179

79% 76%

74% 72%

73%

20%

27%

31% 34%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

0

50

100

150

200

250

300

350

400

2010 2011 2012 2013 H1'2014

Millio

ns

Gross Profit

Gross Margin

TPV/GMV

Healthy Gross Margin Impacted by Mix How we are doing …

44% (1)

(1) Company Data – TPV/GMVE Q2 2014

Source: Company Data - H1 2014: w/o One Time Effects of Venezuela SICAD II adoption

Invest in long

term competitive

advantages…

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

H1 2011 H1 2014

CUSTOMER

ACQUISITION &

RETENTION

S&W

TECHNOLOGY

G&A OVERHEAD

LEGAL/COMPLIANCE

BAD DEBT

CHARGEBACKS

CUSTOMER

ACQUISITION &

RETENTION

S&W

TECHNOLOGY

G&A OVERHEAD

LEGAL/COMPLIANCE

BAD DEBT CHARGEBACKS

Drive scale and

efficiency in our

operations

8%

16%

9%

12%

10%

14%

9%

9%

45%

42%

Delivering OPEX scale “the right way” How we are doing …

Source: Company Data - Net Income Margin H1 2014: w/o One Time Effects of Venezuela SICAD II adoption

54.8

59.6

0%

5%

10%

15%

20%

25%

30%

0

20

40

60

80

100

120

2010 2011 2012 2013 H1'2014

Millio

ns Net Income

Net Income Margin

CAGR

28%

Ven

ezue

la o

ne

- o

ff

56.0 76.8 101.3 117.5

26% 24%

Continue to Grow Earnings How we are doing …

Source: Company Data – Adjusted: Free Cash Flow excluding M&A & purchases of buildings, Net Income Adjusted: H1 2014: without One Time Effects of Venezuela

SICAD II adoption

Adjusted Free Cash Flow

* Adjusted FCF

Adjusted Net Income

Converting NI to FCF* How we are doing …

76.8

101.3 117.5

59.6

54.7

70.5

129.8

119.6

73.3

-

20.0

40.0

60.0

80.0

100.0

120.0

140.0

2010 2011 2012 2013 H1'2014

Source: Company Data

Assets Liabilities & Shareholders Equity

269.7

355.9

478.7

592.4

888.0

-

200.0

400.0

600.0

800.0

1,000.0

2010 2011 2012 2013 H1'2014

Cash and Investments

Accounts & Funds Receivables

Others

Accounts & Funds Payables

Debt

Other Liabilities

Robust & Efficient Capital Structure How we are doing …

Shareholders Equity

269.7

355.9

478.7

592.4

888.0

-

200.0

400.0

600.0

800.0

1,000.0

2010 2011 2012 2013 H1'2014

Agenda

What we said…How we are doing

How we think about our financial model

Wrapping Up

We re committed to

investing efficiently

to generate growth

and capture the

opportunity we are

presented with... Context

Capture

Growing

User

Base

Transition to

Enhanced

Marketplace

Model

Increase

User

Engagement

Scale Generates

Profit and Capital

for Growth

Continuous

Investment In

Innovation

…Efficiency requires

balancing investment

in growth with solid

financial results

Invest for Growth Solid Financials

We operate in a very dynamic context…

Transition to Enhanced Marketplace Model

Capture

Growing

User Base

Increase User Engagement

Scale Drives Profitable-Cash Generating Financial Model

Continuous Investment In Innovation / Iteration

Co

nte

xt

Source: Top 10 retail: Comscore, Latinfocus, World Celular Forecast 14-19,

EuroMonitor

Secular trends and consolidation in e-commerce further benefit MELI

Number of Users % Retail online Top 10 retail sites traffic (PV 000)

Mobile = sustained user growth Enabling e-commerce adoption With consolidation in sector

Optimistic mid term macro and currency outlook for Latin America

USD/LC evolution GDP Growth OPEX margin gains due to AR$ devaluation

Accelerating GDP forecast… …leading to currency stability Hedged by costs in local $

H2'14 H1'15 H2'15 H1'16 H2'16

ARS BRL MEX COL CHI USD

-4%

-2%

0%

2%

4%

6%

2014 2015 2016 2017 2018

Arg Bra Mex Ven Col Chi

155

207

H2'13 H1'14*

Capture Growing User Base

Transition to Enhanced Marketplace Model

Increase User Engagement

Scale Drives Profitable-Cash Generating Financial Model

Continuous Investment In Innovation / Iteration

Co

nte

xt

Source: Conversion: Google Analytics 2014/06

Capture

Growing

User Base

Pursuing mobile growth: clear drivers for acceleration going forward

Driving strong mobile growth Increasing mobile investment > conversion can = higher growth Mobile % GMV % Marketing Investment Mobile Traffic Conversion (Base 100)

0%

25%

50%

75%

100%

Desktop Web Mobile

Desktop Web Mobile

Paid Online Marketing

Increasing customer acquisition as platform has become more robust

ROI Paid Online Marketing New Registered Users

Even at lower ROI… Investing more in marketing … to get > new user adoption

2011 2012 2013 H1 2014

as % of Revenues

2011 2012 2013 H1 2014

ROI

-

4

8

12

16

20

2011 2012 2013 H1 2013 H1 2014

Mill

ion

s CAGR 20%

0.0

24.0

48.0

72.0

96.0

120.0

2011 2012 2013

Mill

on

es

Internet Users CRUs

Investing to ignite pent up growth in : Mexico, Colombia, Chile, Peru, Uruguay …receiving more investment Large under-indexed potential… … should yield returns mid term

Registered users vs. total users (reach) Marketing Investment Revenues (LC)

0.0

1.6

3.2

4.8

6.4

8.0

2011 2012 20130.0

1.6

3.2

4.8

6.4

8.0

2011 2012 2013

Transition to enhanced marketplace

Capture

Growing

User Base

Transition to Enhanced Marketplace Model

Increase User Engagement

Scale Drives Profitable-Cash Generating Financial Model

Continuous Investment In Innovation / Iteration

Co

nte

xt

Entering into Shipping and Fulfillment in financially efficient manner

% SI donde throuh MercadoEnvios Shipping Revenues and Costs Consolidated Take Rate

Currently w/ limited margin impact Continued rapid shipping growth …also permits higher take rate

0.0%

1.6%

3.2%

4.8%

6.4%

8.0%

Q3'13 Q4'13 Q1'14 Q2'14

Others Verticals Consumer Electronics Official Stores

Category Expansion and Stores strengthens financial model

Category % GMV # Users Take Rate

Gain share in large merchants Gain share in non CE categories … w/ positive financial impact

Growth in payments has financial benefits to partially off-set margin impact

MP % GMV Gross Margin and OPEX as % Revenue Consolidated Take Rate

More COGS, less OPEX… Continued rapid payments growth …and drives higher take rate

6.2%6.5% 6.5%

6.9%

0.0%

1.5%

3.0%

4.5%

6.0%

7.5%

2011 2012 2013 H1 2014

Consolidated Take Rate

Increase User Engagement…

Capture

Growing

User Base

Increase User Engagement

Scale Drives Profitable-Cash Generating Financial Model

Continuous Investment In Innovation / Iteration

Co

nte

xt

Transition to Enhanced Marketplace Model

SI/User TPN/ Receiver SI/% Financed GMVe

Platform improvements paying off: better engagement metrics…

More purchases per user …as well as payments …and credit transactions

2.5 2.9

Revenue/User Revenue per Listing

$ 50

$ 38 $ 18

$ 14

…driving improved monetization ratios

Improved revenues per listing… …and per receiver Leading to ARPU growth

Revenue per Receiver

Scale Drives Profitable Financial Model…

Capture

Growing

User Base

Increase User Engagement

Scale Drives Profitable-Cash Generating Financial Model

Continuous Investment In Innovation / Iteration

Co

nte

xt

Transition to Enhanced Marketplace Model

Headcount (largest OPEX) efficiency while investing in talent for long term

Headcount Ratios S&W as % of Rev and Opex Headcount vs Revenues

= improving HC ratios Tight headcount control Well managed S&W expenses

16% 14%

36% 34%

0%

10%

20%

30%

40%

0%

15%

30%

45%

60%

H1 2011 H1 2012 H1 2013 H1 2014

As

% o

f O

pe

x

AS

% o

f R

ev

en

ue

s

S&W/ Revs S&W/ Opex

G&A scale generates margin to re-invest in PD and user acquistion

G&A Non S&W / Revenues Ratio G&A to PD & SM

Beyond S&W management Strong G&A scale Permits focus in other areas

166%

120%

166%

156%

0%

50%

100%

150%

200%

250%

2011 2011 2013 2014

G&A / PD G&A / MKT

G&A / Revenues

Efficient Capital Expenditure with asset light low CAPEX financial model

CAPEX / Revenues Operational CAPEX / Revenues M&A + RE CAPEX / Revenues

Frees up $ for strategic investments Low recurring CAPEX … in investment cycle years

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

2011 2011 2013 2014 0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

2011 2011 2013 2014

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

2011 2011 2013 2014

Continuous Investment in Innovation and growth…

Capture

Growing

User Base

Increase User Engagement

Scale Drives Profitable-Cash Generating Financial Model

Continuous Investment In Innovation

Co

nte

xt

Transition to Enhanced Marketplace Model

PD / Revenues PD Headcount PD Projects Capitalized

Committed to investing in PD as competitive edge…

Ramping up PD investment Mainly in engineering talent … allows increased PD output

…across the range of PD investment opportunities

Site Operation / Revenues PD CAPEX / Revenues M&A / Engineers

Also investing in IT operations Through operational CAPEX And strategic CAPEX

0,7%

1,6%

0,0%

0,5%

0,9%

1,4%

1,8%

2011 2012 2013

-

10

20

30

40

50

60

2011 2012 2013 2014

Principles for managing our financial model

Prioritize top line growth

Invest behind what is strategic to our business

Drive scale in less strategic expenditures

Deploy capital more aggressively in certain areas

Focus on capturing the opportunities in Latin American e-commerce

Product development and technology

User acquisition and retention

General and Administrative expenses

Control headcount increases leading to managed compensation growth

Corporate overhead

Under indexed regions, new business opportunities, M&A targets

What we said…. How we are doing!

How we think about our financial model

Wrapping Up

Agenda

We are in an even better position to continue

capturing the opportunity

In the past 15 years we:

Now with e-commerce growth still presenting a huge opportunity…

Built the pre-eminent e-commerce platform in Latin America, and

Created a strong brand that is synonymous with e-commerce

Successfully began the transition to an enhanced marketplace model

We have a much better financial position, access to credit and capitalization

A cutting edge open technology platform, and

An ecosystem of business units that are more diversified and have stronger

network effects than ever before

…this makes us feel optimistic about the long term prospects for the company

Thanks for coming!