oat outlook - poga.ca · oat outlook oatinformation.com ... 10,021 8,829 12,277 9,822 10,243 10,238...

TRANSCRIPT

Oat Outlook OATINFORMATION.COM

OATINFORMATION.COM

Key Factors Driving Oat Markets•Canadian rail car supply•Fund/Specs•CBOT oat carry•High price of oats in US horse markets•Tighter 2014/15 oat end stocks

OATINFORMATION.COM

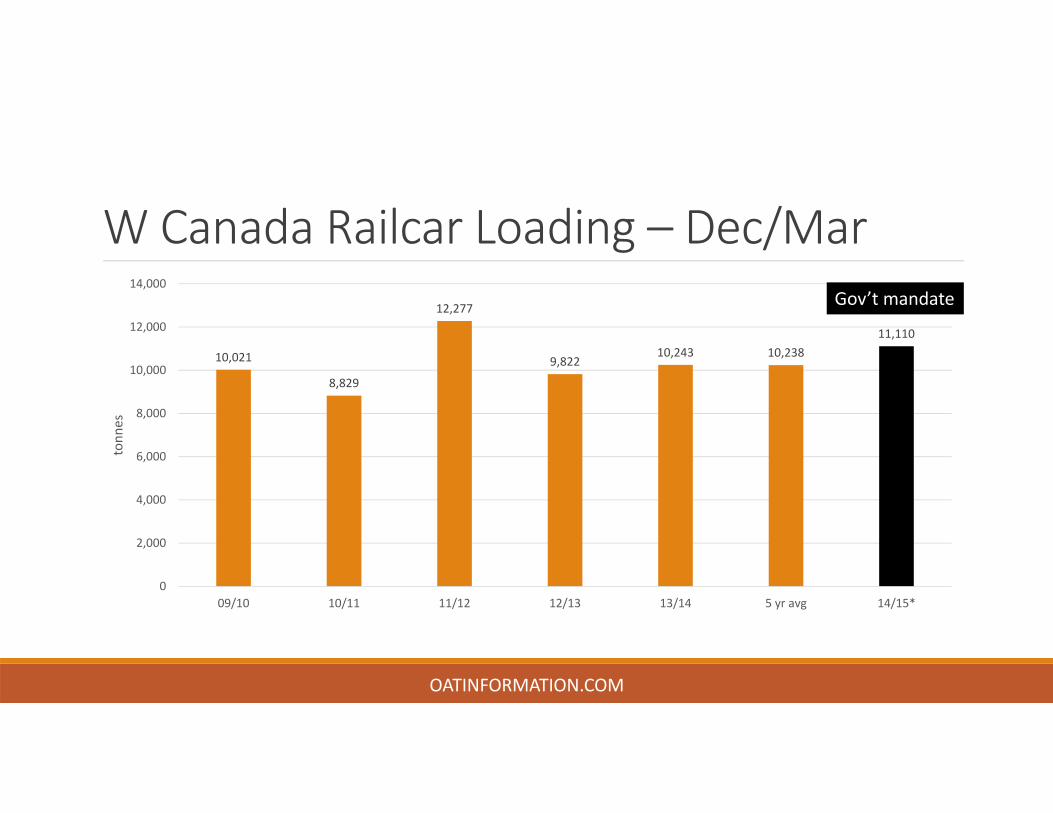

Canadian Rail Car Supply•This is primary to oat price direction•Minimum rail car mandate extended;

• To March 31, 2015• Car numbers reduced and varied• Impact to oats will be limited

•Crude oil shipments up sharply Y‐O• Future exports will depend on US demand• Current longer term forecasts call for increased exports

•Higher wheat and canola margins•Implied corridor restrictions for oats

OATINFORMATION.COM

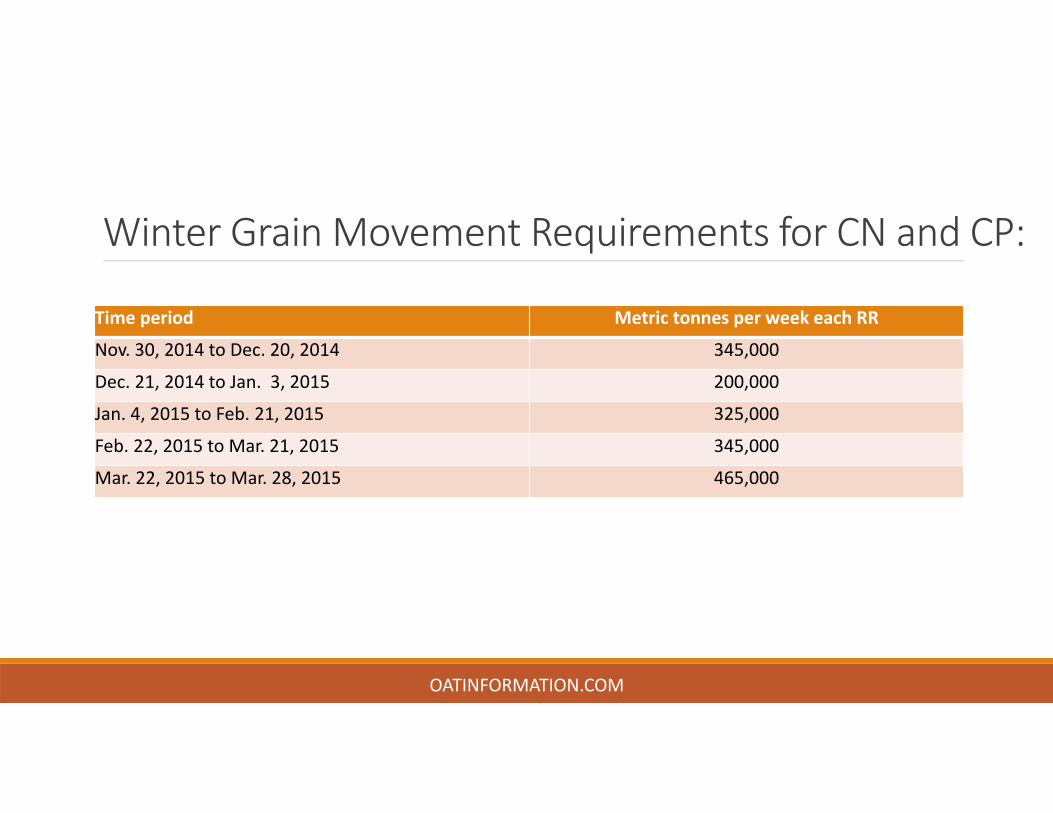

Winter Grain Movement Requirements for CN and CP:

OATINFORMATION.COM

Time period Metric tonnes per week each RR

Nov. 30, 2014 to Dec. 20, 2014 345,000

Dec. 21, 2014 to Jan. 3, 2015 200,000

Jan. 4, 2015 to Feb. 21, 2015 325,000

Feb. 22, 2015 to Mar. 21, 2015 345,000

Mar. 22, 2015 to Mar. 28, 2015 465,000

W Canada Railcar Loading – Dec/Mar

10,021

8,829

12,277

9,82210,243 10,238

11,110

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

09/10 10/11 11/12 12/13 13/14 5 yr avg 14/15*

tonn

es

OATINFORMATION.COM

Gov’t mandate

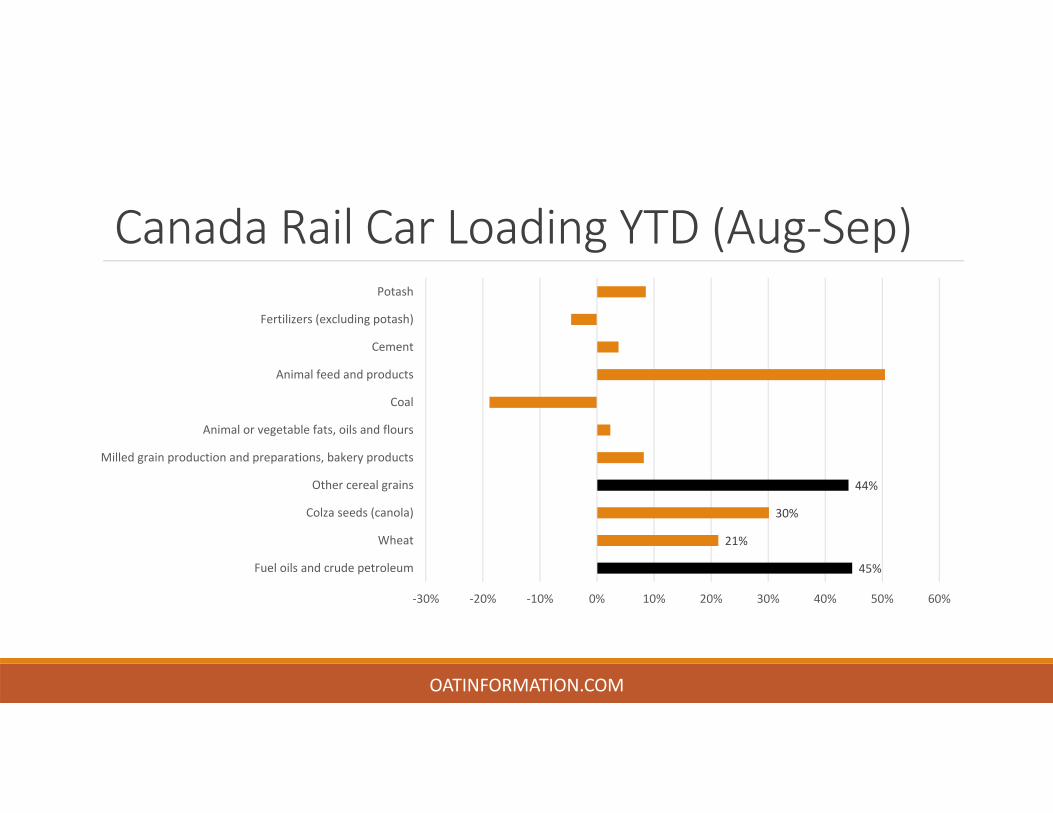

Canada Rail Car Loading YTD (Aug‐Sep)

45%

21%

30%

44%

‐30% ‐20% ‐10% 0% 10% 20% 30% 40% 50% 60%

Fuel oils and crude petroleum

Wheat

Colza seeds (canola)

Other cereal grains

Milled grain production and preparations, bakery products

Animal or vegetable fats, oils and flours

Coal

Animal feed and products

Cement

Fertilizers (excluding potash)

Potash

OATINFORMATION.COM

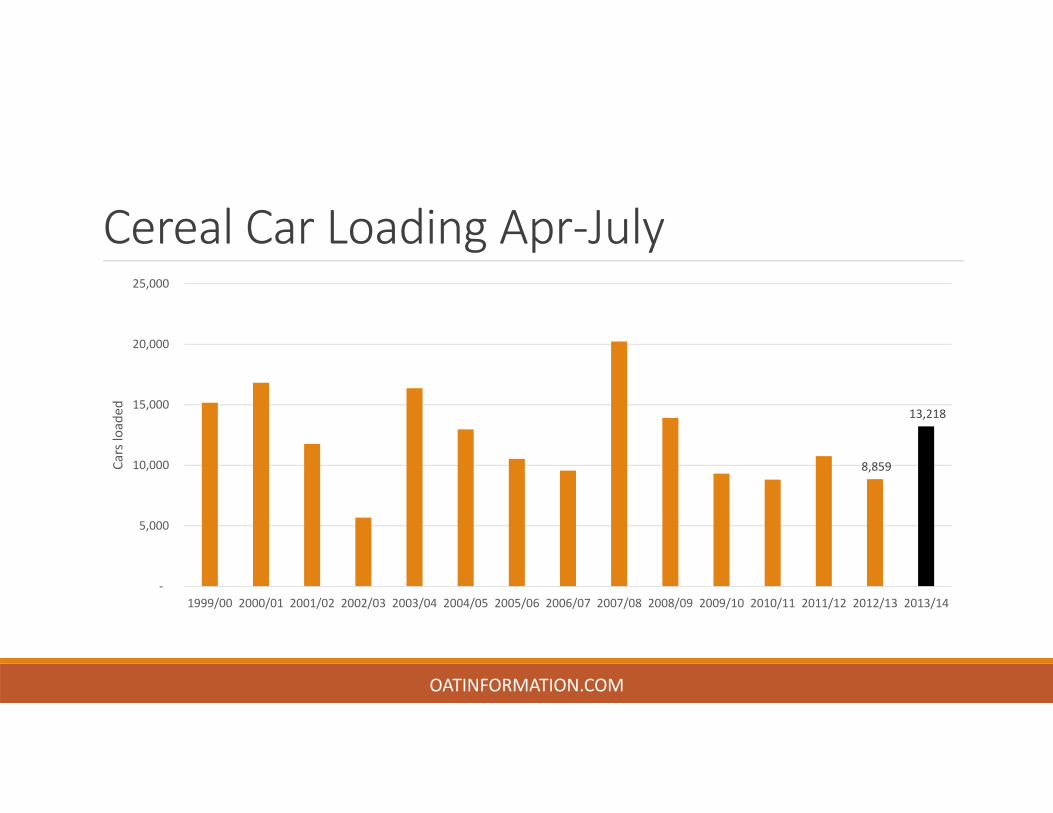

Cereal Car Loading Apr‐July

8,859

13,218

‐

5,000

10,000

15,000

20,000

25,000

1999/00 2000/01 2001/02 2002/03 2003/04 2004/05 2005/06 2006/07 2007/08 2008/09 2009/10 2010/11 2011/12 2012/13 2013/14

Cars loaded

OATINFORMATION.COM

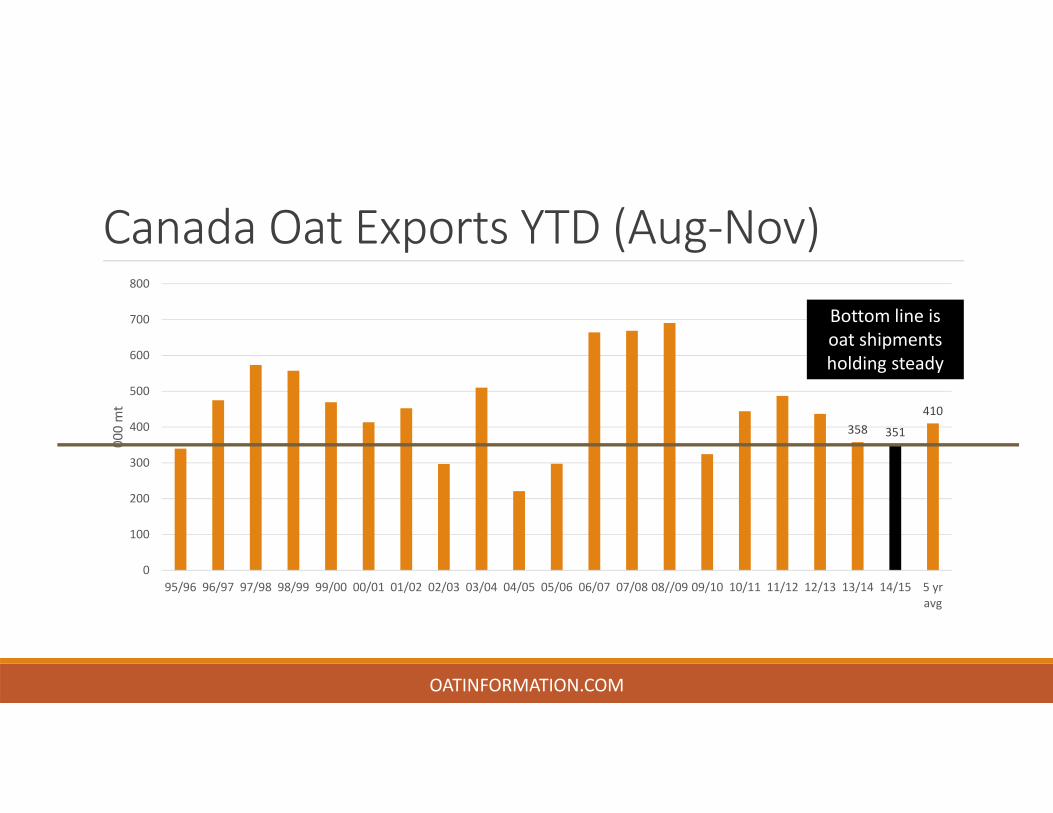

Canada Oat Exports YTD (Aug‐Nov)

358 351

410

0

100

200

300

400

500

600

700

800

95/96 96/97 97/98 98/99 99/00 00/01 01/02 02/03 03/04 04/05 05/06 06/07 07/08 08//09 09/10 10/11 11/12 12/13 13/14 14/15 5 yravg

000 mt

OATINFORMATION.COM

Bottom line is oat shipments holding steady

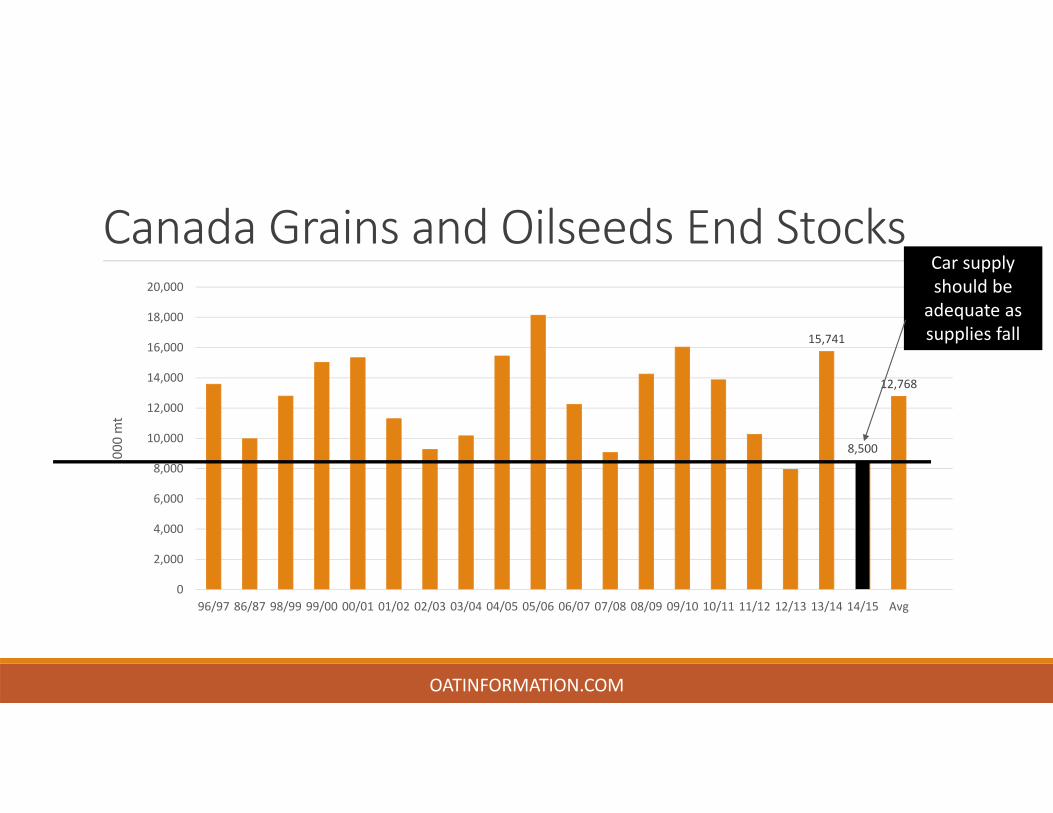

Canada Grains and Oilseeds End Stocks

15,741

8,500

12,768

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

96/97 86/87 98/99 99/00 00/01 01/02 02/03 03/04 04/05 05/06 06/07 07/08 08/09 09/10 10/11 11/12 12/13 13/14 14/15 Avg

000 mt

OATINFORMATION.COM

Car supply should be adequate as supplies fall

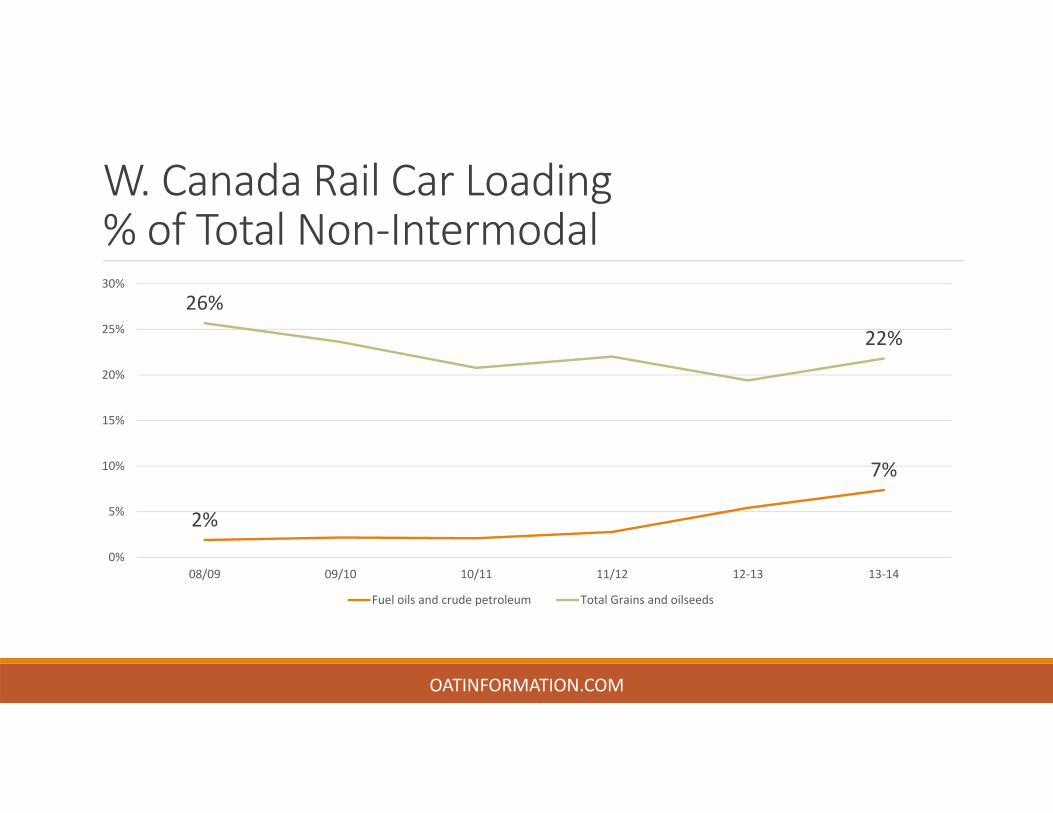

W. Canada Rail Car Loading % of Total Non‐Intermodal

2%

7%

26%

22%

0%

5%

10%

15%

20%

25%

30%

08/09 09/10 10/11 11/12 12‐13 13‐14

Fuel oils and crude petroleum Total Grains and oilseeds

OATINFORMATION.COM

Crude oil by railUS Railroads’ oil‐by‐rail business is dependent on shale plays in North America. Shale plays are unsustainable with oil below $73 per barrel, some say lower. US Railroads haul 8% of U.S. crude.19% of CNR revenues came from shipment of petroleum and chemicals in third quarter 2014. For the first nine months of the year, about 19.3% of revenues came from shipment of petroleum and chemicals, the company reported.If Union Pacific, BNSF Railway, CSX, Norfolk Southern and Canadian National have similar crude‐by‐rail numbers as CNR, these railroads may lose 5% to 10% of their revenues if oil stays below $70 per barrel.

OATINFORMATION.COM

Crude oil by railThe overall revenue exposure in 2014 for both CN and CP stands at roughly 9%.

Several oil experts believe risk to 2015 volume is relatively minimal considering that low prices likely need to stick around for 6‐12 months before there is any major change in production.

OATINFORMATION.COM

Oat Fund/Specs •Volume buyer…..and sellers•Algorithms‘ driving trade…fundamentals????•Non‐reporting reporting traders playing a larger role•Can significantly impact oat prices when entering, exiting and or rolling

OATINFORMATION.COM

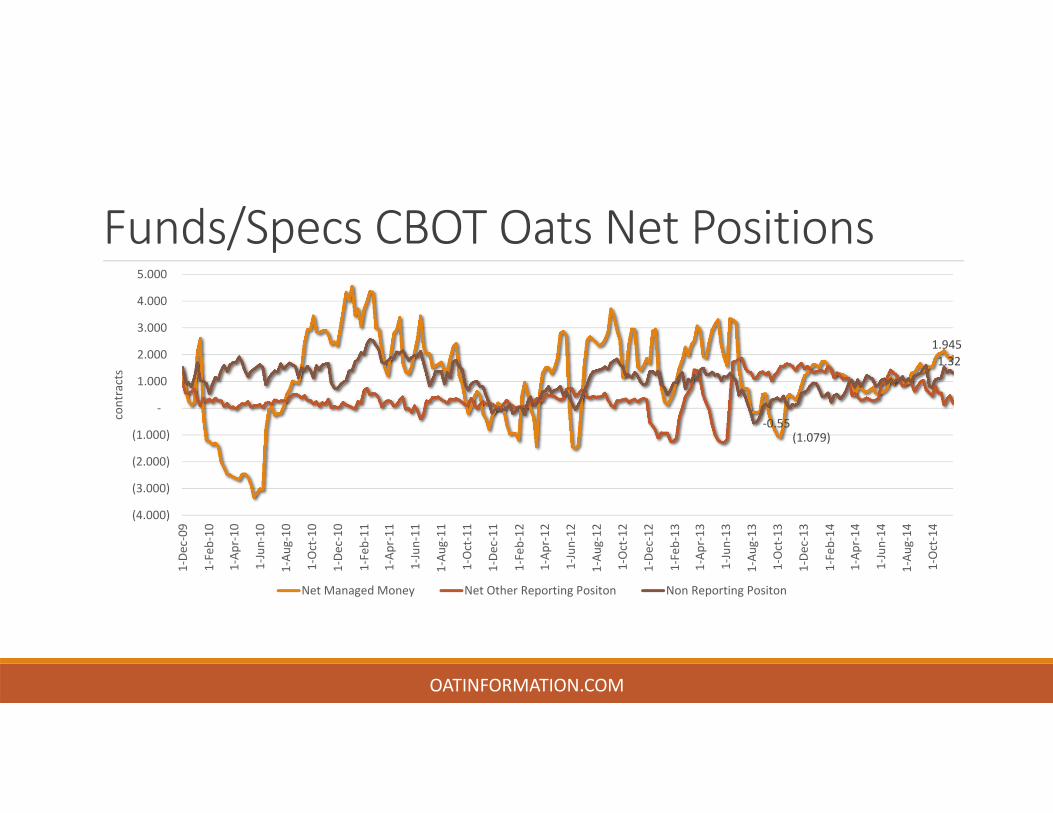

Funds/Specs CBOT Oats Net Positions

(1.079)

1.945

‐0.55

1.32

(4.000)

(3.000)

(2.000)

(1.000)

‐

1.000

2.000

3.000

4.000

5.000

1‐De

c‐09

1‐Feb‐10

1‐Ap

r‐10

1‐Jun‐10

1‐Au

g‐10

1‐Oct‐10

1‐De

c‐10

1‐Feb‐11

1‐Ap

r‐11

1‐Jun‐11

1‐Au

g‐11

1‐Oct‐11

1‐De

c‐11

1‐Feb‐12

1‐Ap

r‐12

1‐Jun‐12

1‐Au

g‐12

1‐Oct‐12

1‐De

c‐12

1‐Feb‐13

1 ‐Ap

r‐13

1‐Jun‐13

1‐Au

g‐13

1‐Oct‐13

1‐De

c‐13

1‐Feb‐14

1‐Ap

r‐14

1‐Jun‐14

1‐Au

g‐14

1‐Oct‐14

contracts

Net Managed Money Net Other Reporting Positon Non Reporting Positon

OATINFORMATION.COM

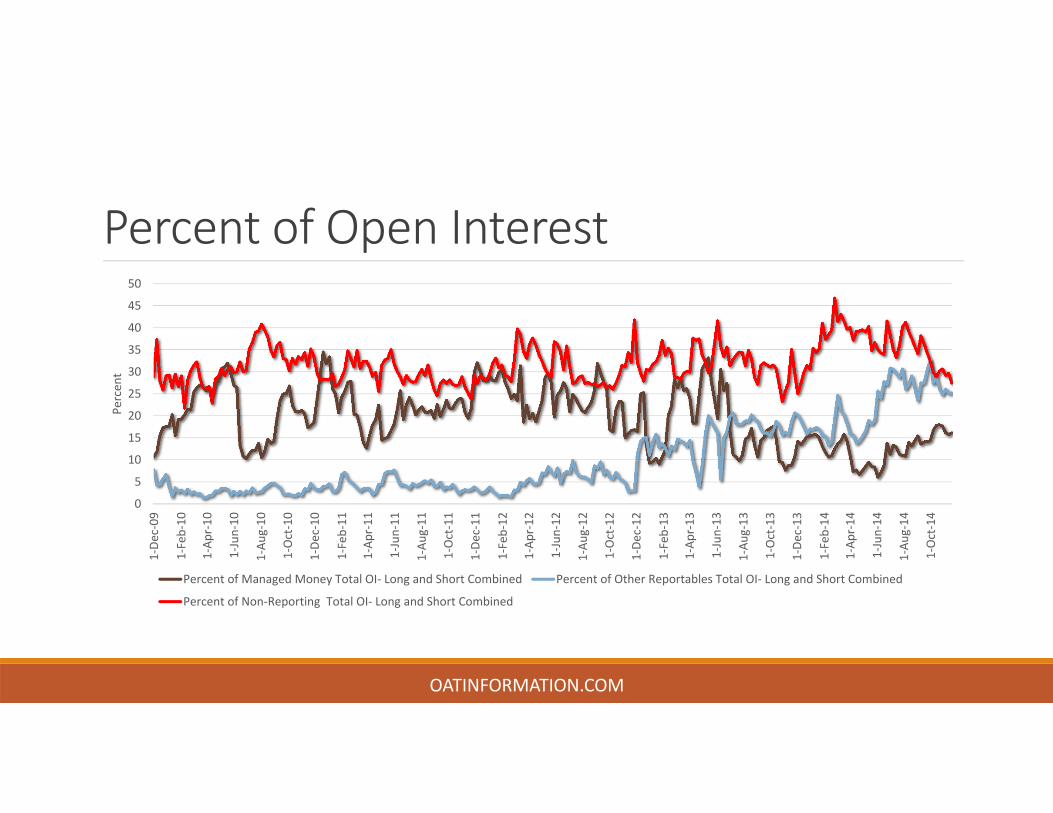

Percent of Open Interest

0

5

10

15

20

25

30

35

40

45

50

1‐De

c‐09

1‐Feb‐10

1‐Ap

r‐10

1‐Jun‐10

1‐Au

g‐10

1‐Oct‐10

1‐De

c‐10

1‐Feb‐11

1‐Ap

r‐11

1‐Jun‐11

1‐Au

g‐11

1‐Oct‐11

1‐De

c‐11

1‐Feb‐12

1‐Ap

r‐12

1‐Jun‐12

1‐Au

g‐12

1‐Oct‐12

1‐De

c‐12

1‐Feb‐13

1‐Ap

r‐13

1‐Jun‐13

1‐Au

g‐13

1‐Oct‐13

1‐De

c‐13

1‐Feb‐14

1‐Ap

r‐14

1‐Jun‐14

1‐Au

g‐14

1‐Oct‐14

Percen

t

Percent of Managed Money Total OI‐ Long and Short Combined Percent of Other Reportables Total OI‐ Long and Short Combined

Percent of Non‐Reporting Total OI‐ Long and Short Combined

OATINFORMATION.COM

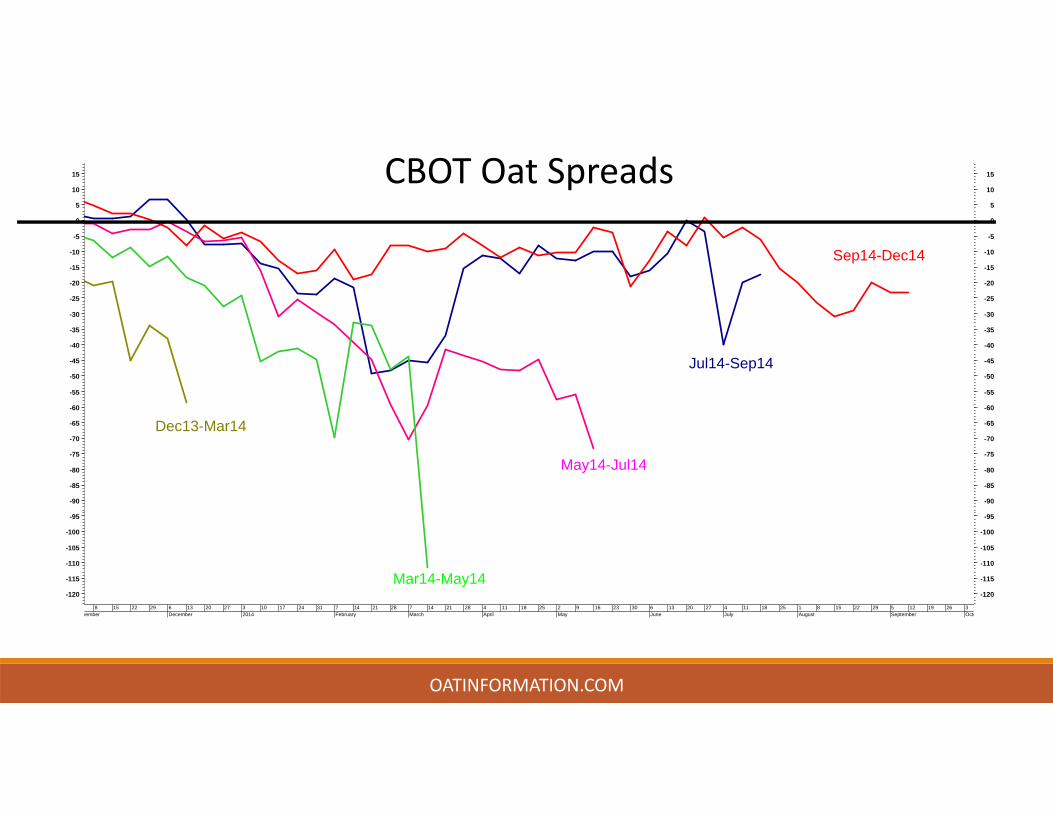

CBOT Oat Carry•Oat markets struggle without it•Carry brings increased:•Commercial cash oat trade•Forward grower selling•Predictability of oat supply, particularly for commercial’s

OATINFORMATION.COM

OATINFORMATION.COM

8vember

15 22 29 6 13December

20 27 32014

10 17 24 31 7 14February

21 28 7March

14 21 28 4April

11 18 25 2May

9 16 23 30 6June

13 20 27 4July

11 18 25 1August

8 15 22 29 5 12September

19 26 3Octo

-120

-115

-110

-105

-100

-95

-90

-85

-80

-75

-70

-65

-60

-55

-50

-45

-40

-35

-30

-25

-20

-15

-10

-5

0

5

10

15

-120

-115

-110

-105

-100

-95

-90

-85

-80

-75

-70

-65

-60

-55

-50

-45

-40

-35

-30

-25

-20

-15

-10

-5

0

5

10

15

Jul14-Sep14

May14-Jul14

Mar14-May14

Sep14-Dec14

Dec13-Mar14

CBOT Oat Spreads

OATINFORMATION.COM

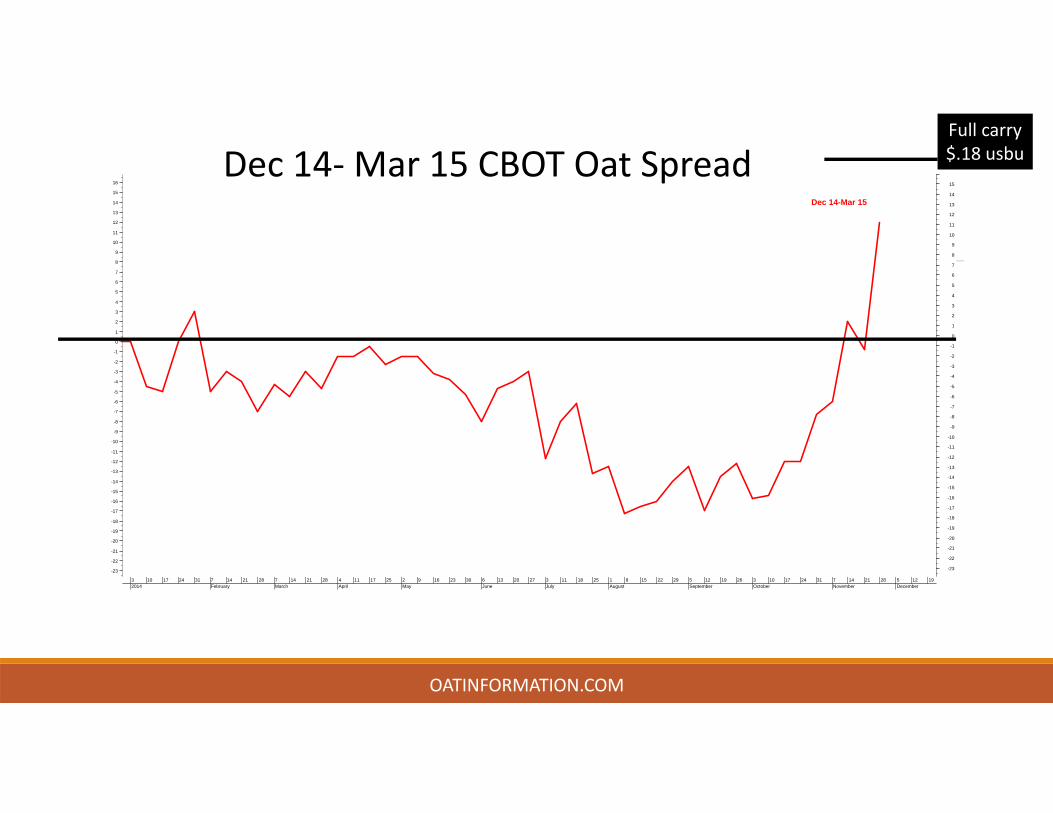

32014

10 17 24 31 7 14February

21 28 7March

14 21 28 4April

11 17 25 2May

9 16 23 30 6June

13 20 27 3July

11 18 25 1 8August

15 22 29 5 12September

19 26 3 10October

17 24 31 7 14November

21 28 5 12December

19

-23

-22

-21

-20

-19

-18

-17

-16

-15

-14

-13

-12

-11

-10

-9

-8

-7

-6

-5

-4

-3

-2

-1

0

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

-23

-22

-21

-20

-19

-18

-17

-16

-15

-14

-13

-12

-11

-10

-9

-8

-7

-6

-5

-4

-3

-2

-1

0

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

Dec 14-Mar 15

Dec 14‐Mar 15 CBOT Oat SpreadFull carry$.18 usbu

Spread Outlook•Dec/Mar should maintain decent to good carry if Canadian oat exports hold current pace•Back end months could tighten if Canadian oat plantings are lower than expected….or exports slow•Oats are expected lose further ground to corn and wheat if;

• Canadian oat export pace holds steady • 2015 Canadian oat plantings are up 10% or more

OATINFORMATION.COM

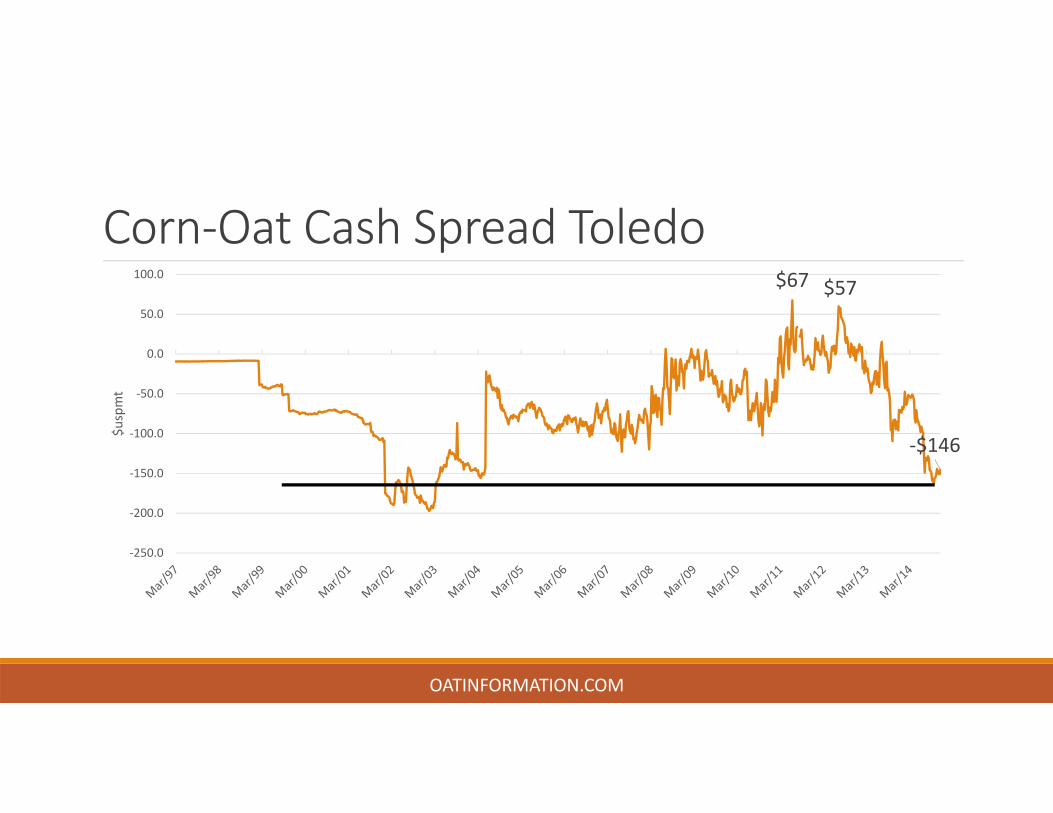

High Price of Oats Relative to other Ingredients

•Killing feed demand in US horse markets•Without feed demand, oat become “contracted” crop•Rail issues are impacting horse demand and price relationships

OATINFORMATION.COM

Corn‐Oat Cash Spread Toledo$67 $57

‐$146

‐250.0

‐200.0

‐150.0

‐100.0

‐50.0

0.0

50.0

100.0

$uspmt

OATINFORMATION.COM

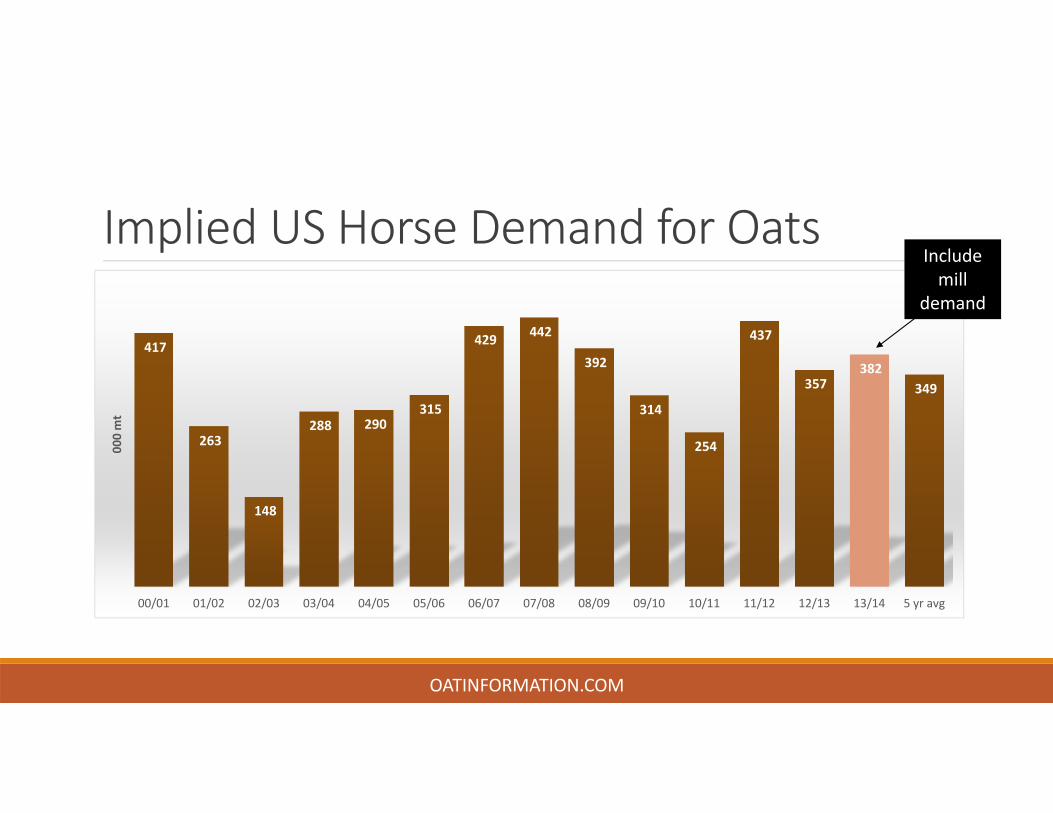

Implied US Horse Demand for Oats

417

263

148

288 290 315

429 442

392

314

254

437

357 382

349

00/01 01/02 02/03 03/04 04/05 05/06 06/07 07/08 08/09 09/10 10/11 11/12 12/13 13/14 5 yr avg

000 mt

OATINFORMATION.COM

Include mill

demand

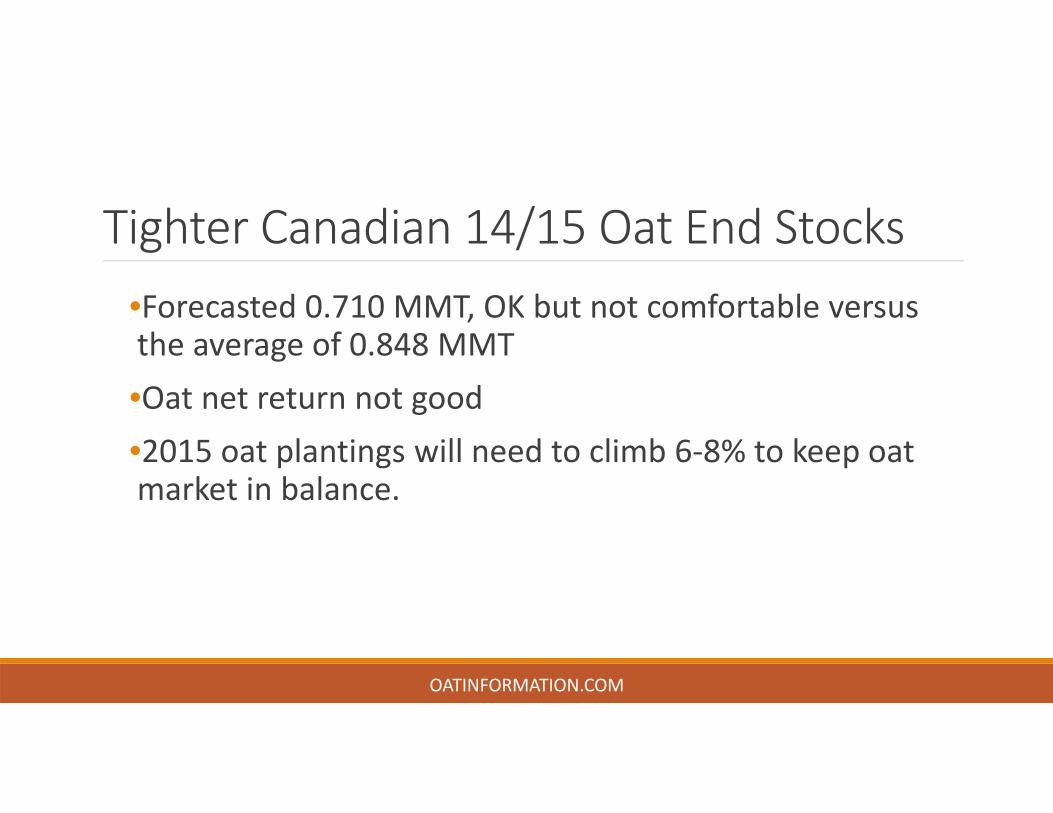

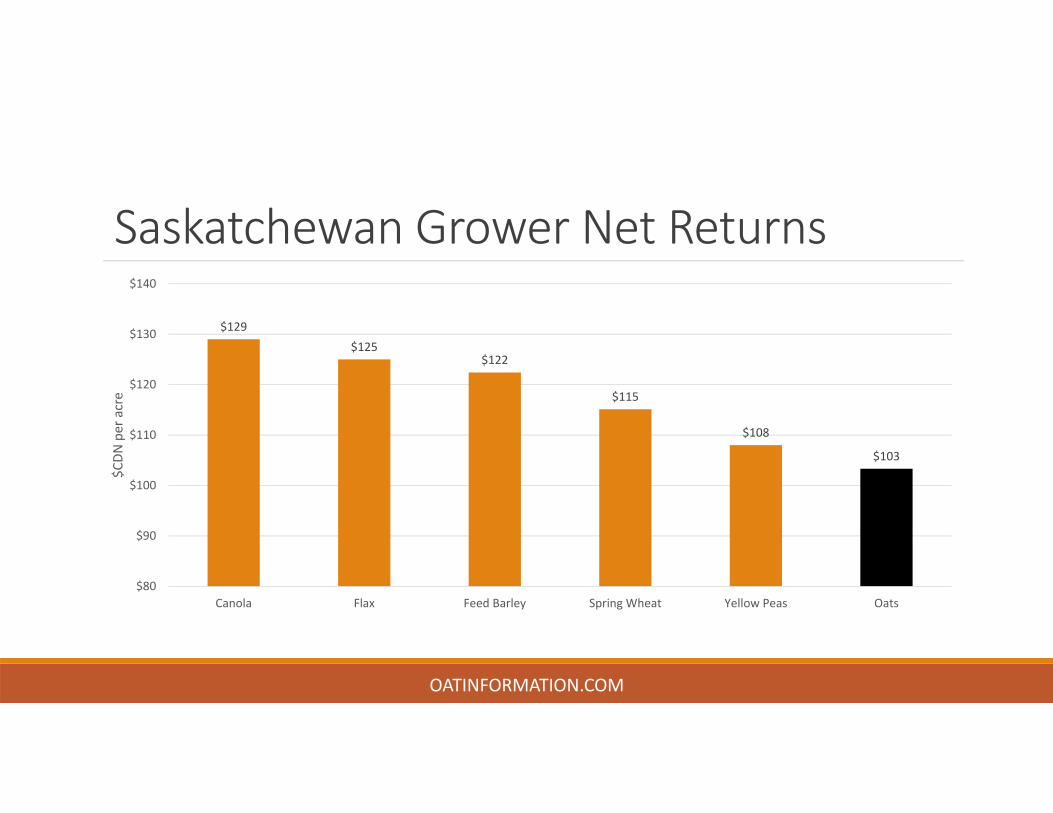

Tighter Canadian 14/15 Oat End Stocks•Forecasted 0.710 MMT, OK but not comfortable versus the average of 0.848 MMT•Oat net return not good•2015 oat plantings will need to climb 6‐8% to keep oat market in balance.

OATINFORMATION.COM

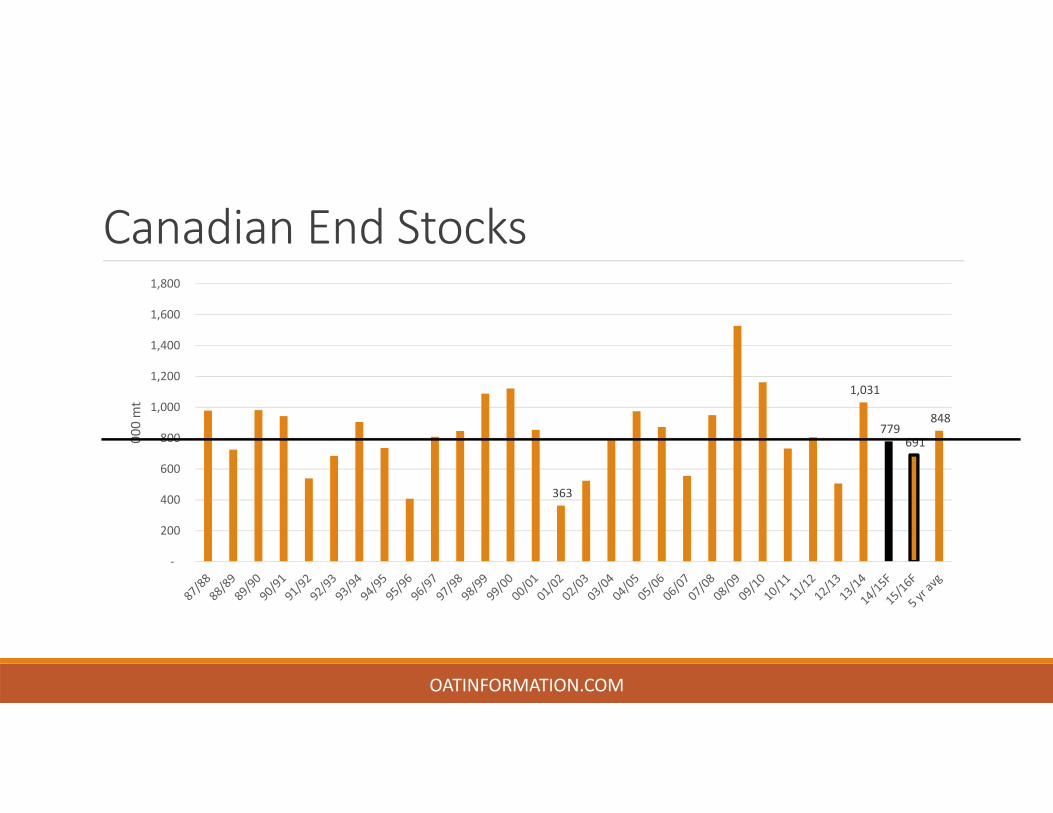

Canadian End Stocks

363

1,031

779 691

848

‐

200

400

600

800

1,000

1,200

1,400

1,600

1,800

000 mt

OATINFORMATION.COM

Oat Metrics

OATINFORMATION.COM

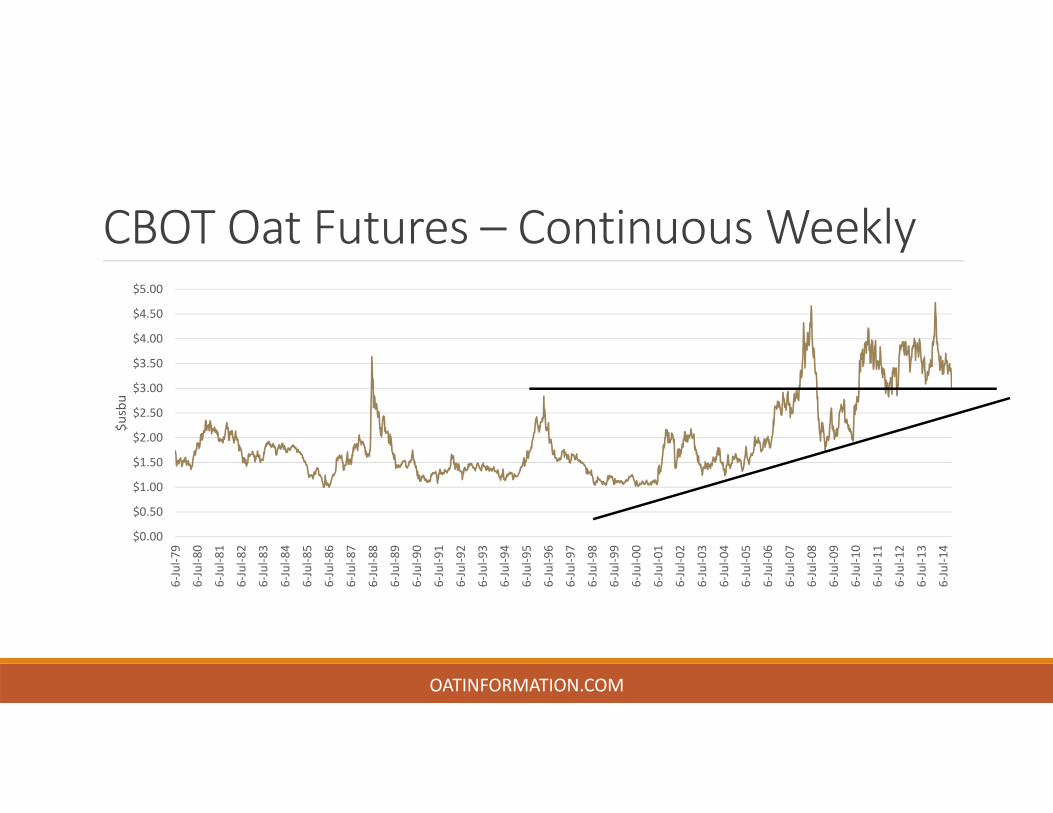

CBOT Oat Futures – Continuous Weekly

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

$3.50

$4.00

$4.50

$5.00

6‐Jul‐7

9

6‐Jul‐8

0

6‐Jul‐8

1

6‐Jul‐8

2

6‐Jul‐8

3

6‐Jul‐8

4

6‐Jul‐8

5

6‐Jul‐8

6

6‐Jul‐8

7

6‐Jul‐8

8

6‐Jul‐8

9

6‐Jul‐9

0

6‐Jul‐9

1

6‐Jul‐9

2

6‐Jul‐9

3

6‐Jul‐9

4

6‐Jul‐9

5

6‐Jul‐9

6

6‐Jul‐9

7

6‐Jul‐9

8

6‐Jul‐9

9

6‐Jul‐0

0

6‐Jul‐0

1

6‐Jul‐0

2

6‐Jul‐0

3

6‐Jul‐0

4

6‐Jul‐0

5

6‐Jul‐0

6

6‐Jul‐0

7

6‐Jul‐0

8

6‐Jul‐0

9

6‐Jul‐1

0

6‐Jul‐1

1

6‐Jul‐1

2

6‐Jul‐1

3

6‐Jul‐1

4

$usbu

OATINFORMATION.COM

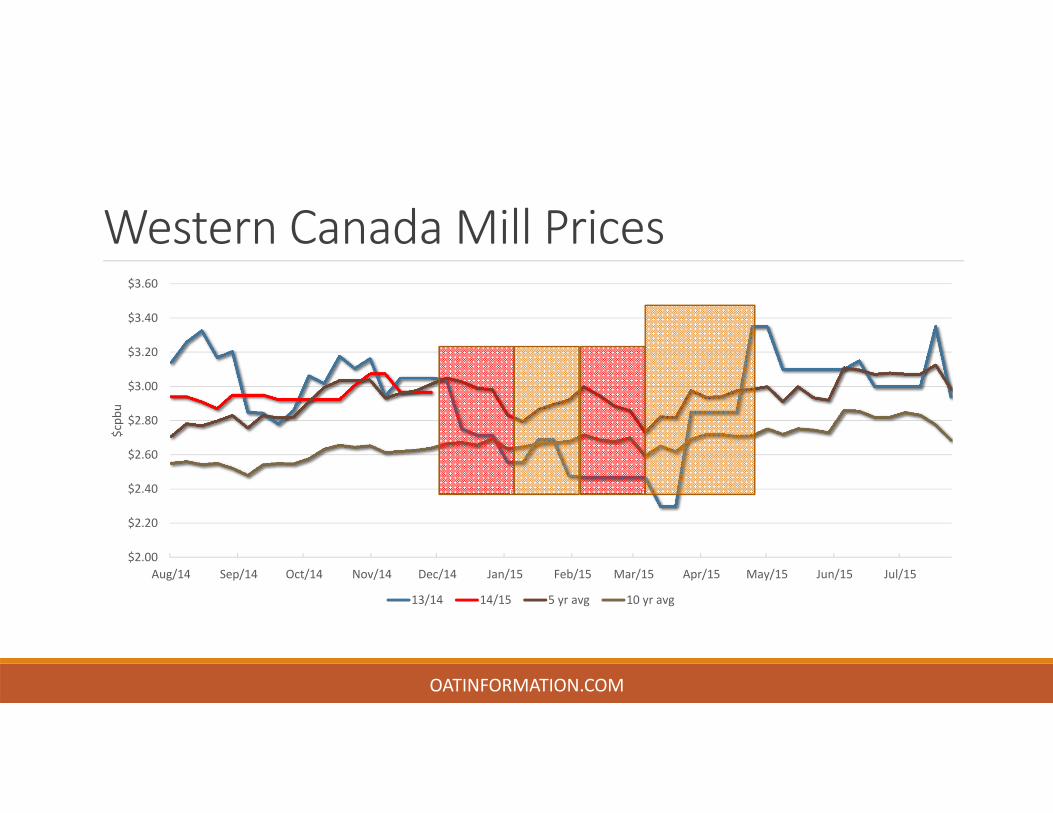

Western Canada Mill Prices

$2.00

$2.20

$2.40

$2.60

$2.80

$3.00

$3.20

$3.40

$3.60

Aug/14 Sep/14 Oct/14 Nov/14 Dec/14 Jan/15 Feb/15 Mar/15 Apr/15 May/15 Jun/15 Jul/15

$cpb

u

13/14 14/15 5 yr avg 10 yr avg

OATINFORMATION.COM

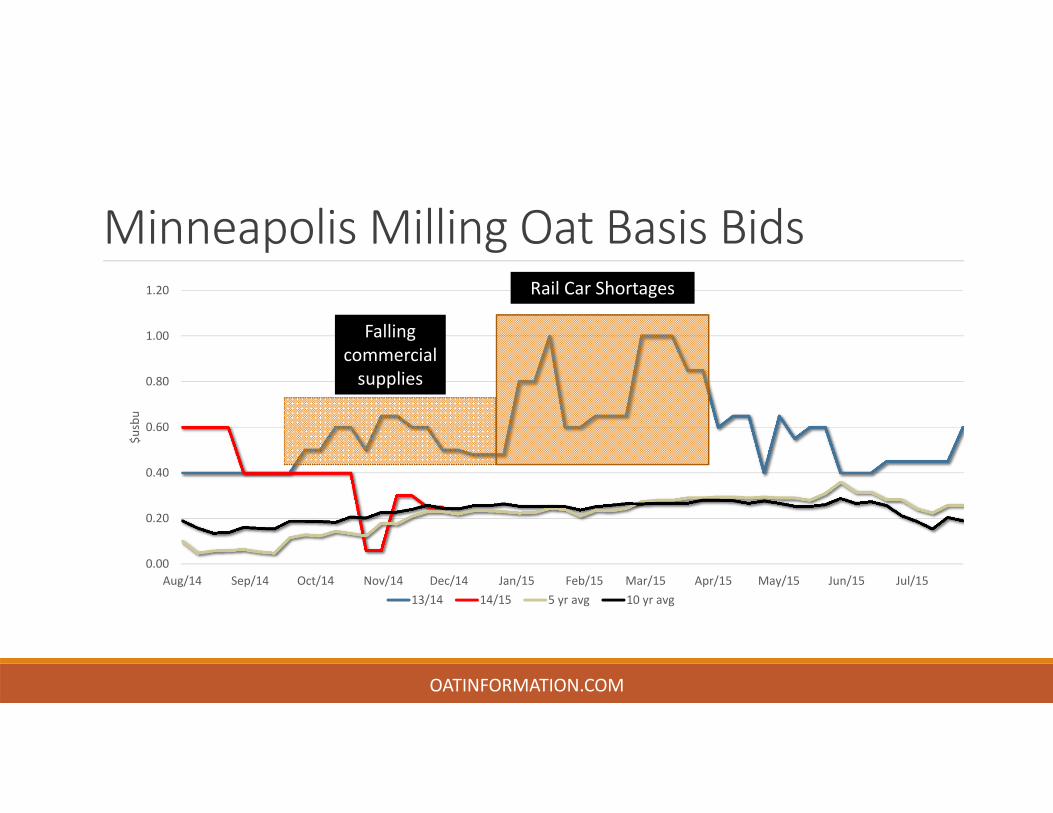

Minneapolis Milling Oat Basis Bids

0.00

0.20

0.40

0.60

0.80

1.00

1.20

Aug/14 Sep/14 Oct/14 Nov/14 Dec/14 Jan/15 Feb/15 Mar/15 Apr/15 May/15 Jun/15 Jul/15

$usbu

13/14 14/15 5 yr avg 10 yr avg

OATINFORMATION.COM

Falling commercial supplies

Rail Car Shortages

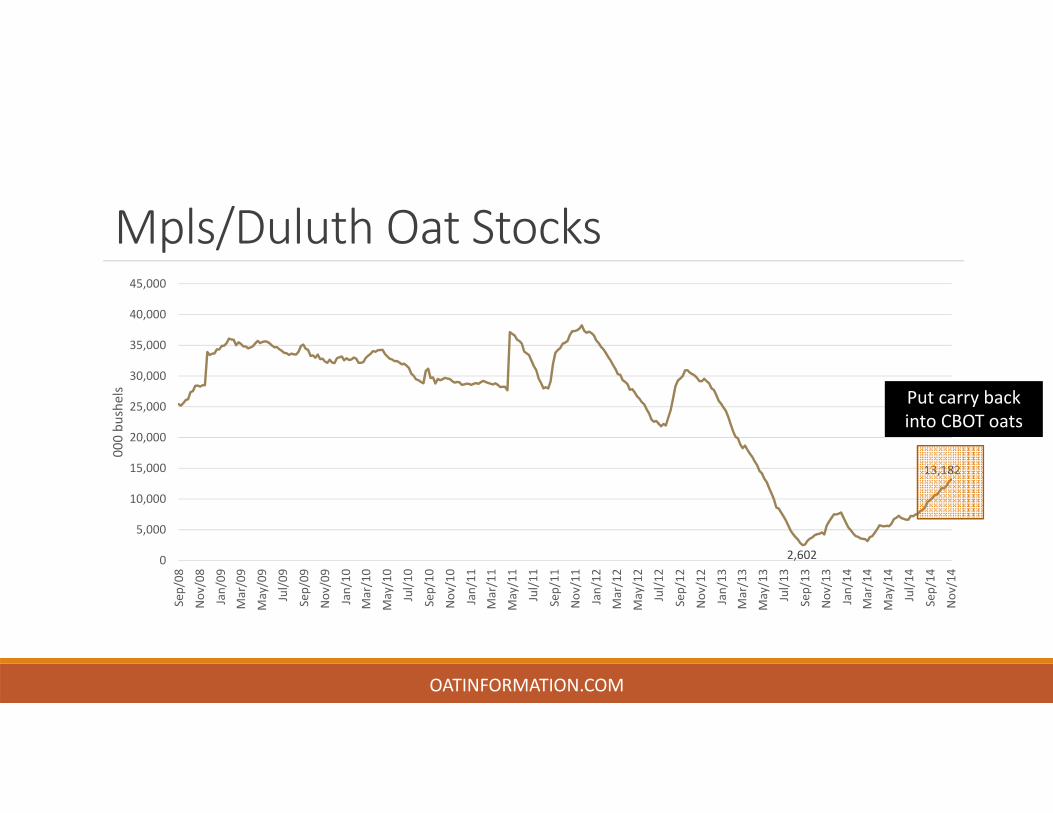

Mpls/Duluth Oat Stocks

2,602

13,182

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

Sep/08

Nov/08

Jan/09

Mar/09

May/09

Jul/0

9

Sep/09

Nov/09

Jan/10

Mar/10

May/10

Jul/1

0

Sep/10

Nov/10

Jan/11

Mar/11

May/11

Jul/1

1

Sep/11

Nov/11

Jan/12

Mar/12

May/12

Jul/1

2

Sep/12

Nov/12

Jan/13

Mar/13

May/13

Jul/1

3

Sep/13

Nov/13

Jan/14

Mar/14

May/14

Jul/1

4

Sep/14

Nov/14

000 bu

shels

OATINFORMATION.COM

Put carry back into CBOT oats

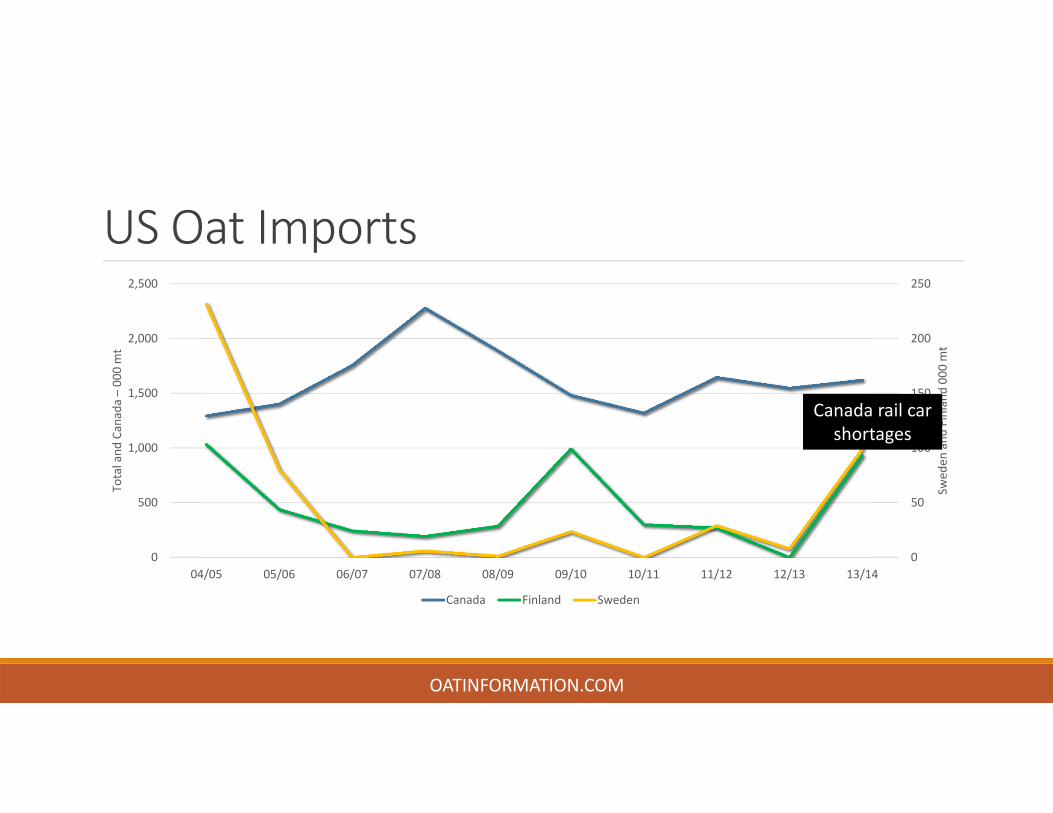

US Oat Imports

0

50

100

150

200

250

0

500

1,000

1,500

2,000

2,500

04/05 05/06 06/07 07/08 08/09 09/10 10/11 11/12 12/13 13/14

Swed

en and

Finland

000

mt

Total and

Canada –00

0 mt

Canada Finland Sweden

OATINFORMATION.COM

Canada rail car shortages

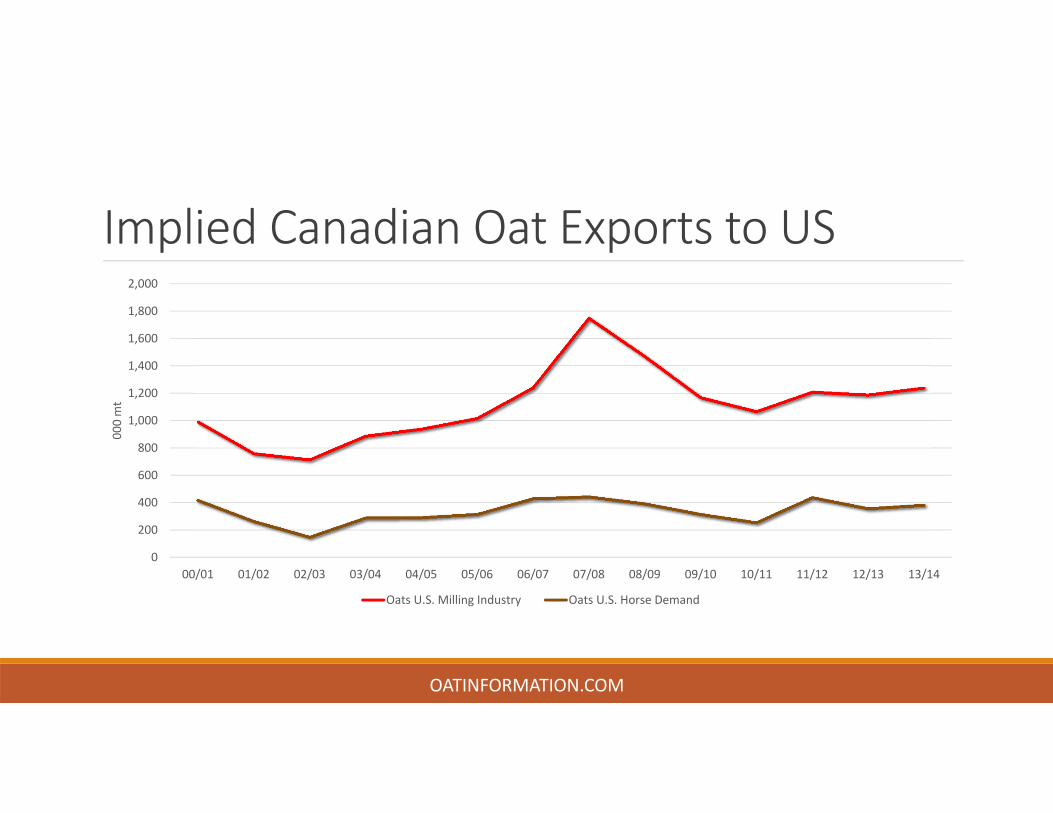

Implied Canadian Oat Exports to US

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

00/01 01/02 02/03 03/04 04/05 05/06 06/07 07/08 08/09 09/10 10/11 11/12 12/13 13/14

000 mt

Oats U.S. Milling Industry Oats U.S. Horse Demand

OATINFORMATION.COM

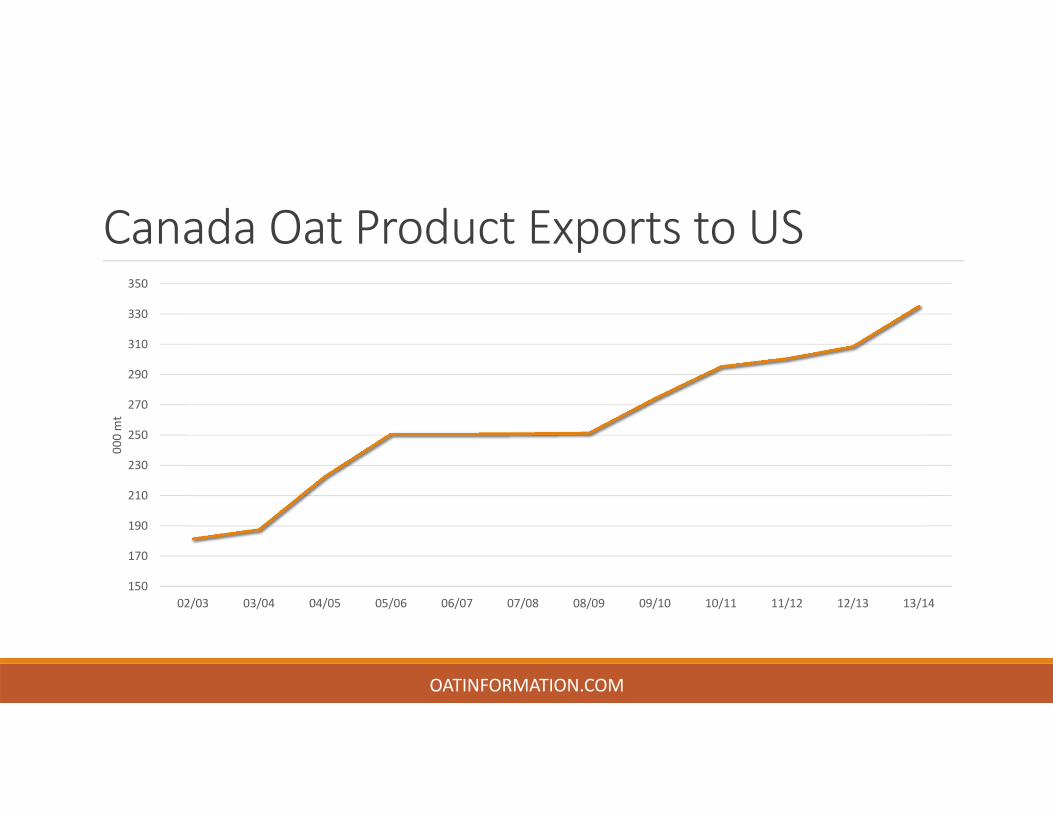

Canada Oat Product Exports to US

150

170

190

210

230

250

270

290

310

330

350

02/03 03/04 04/05 05/06 06/07 07/08 08/09 09/10 10/11 11/12 12/13 13/14

000 mt

OATINFORMATION.COM

Saskatchewan Grower Net Returns

$129$125

$122

$115

$108

$103

$80

$90

$100

$110

$120

$130

$140

Canola Flax Feed Barley Spring Wheat Yellow Peas Oats

$CDN

per acre

OATINFORMATION.COM

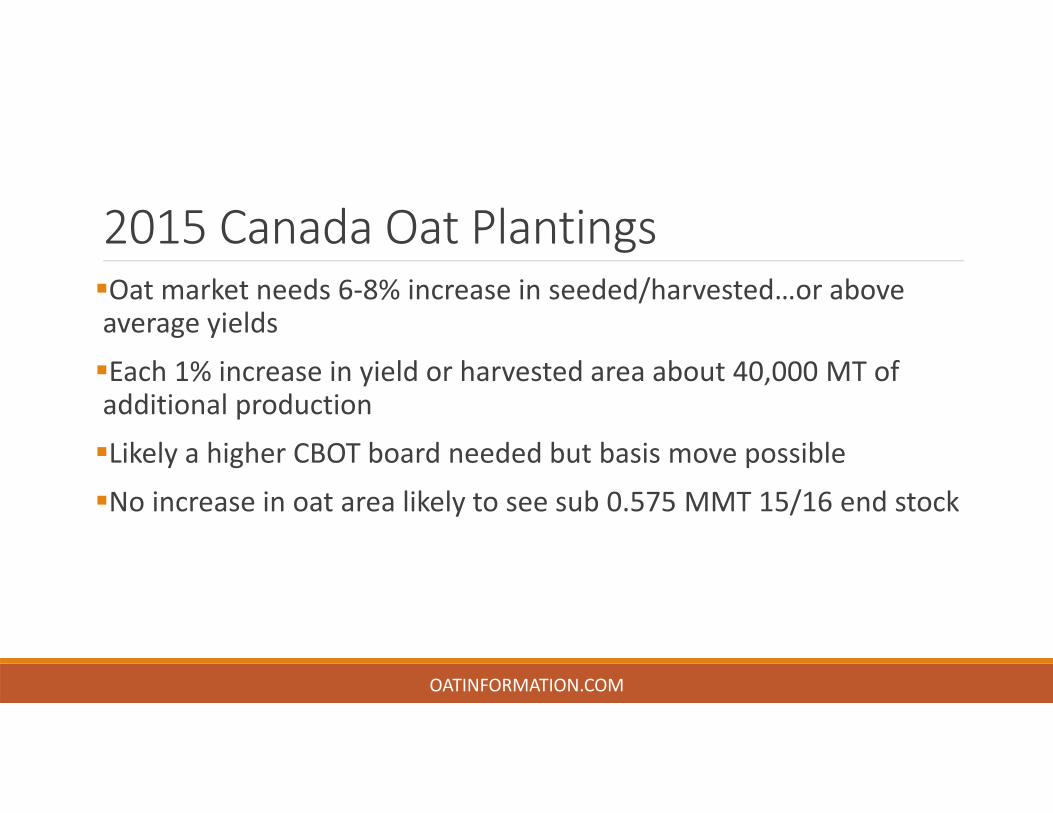

2015 Canada Oat PlantingsOat market needs 6‐8% increase in seeded/harvested…or above average yields

Each 1% increase in yield or harvested area about 40,000 MT of additional production

Likely a higher CBOT board needed but basis move possible

No increase in oat area likely to see sub 0.575 MMT 15/16 end stock

OATINFORMATION.COM

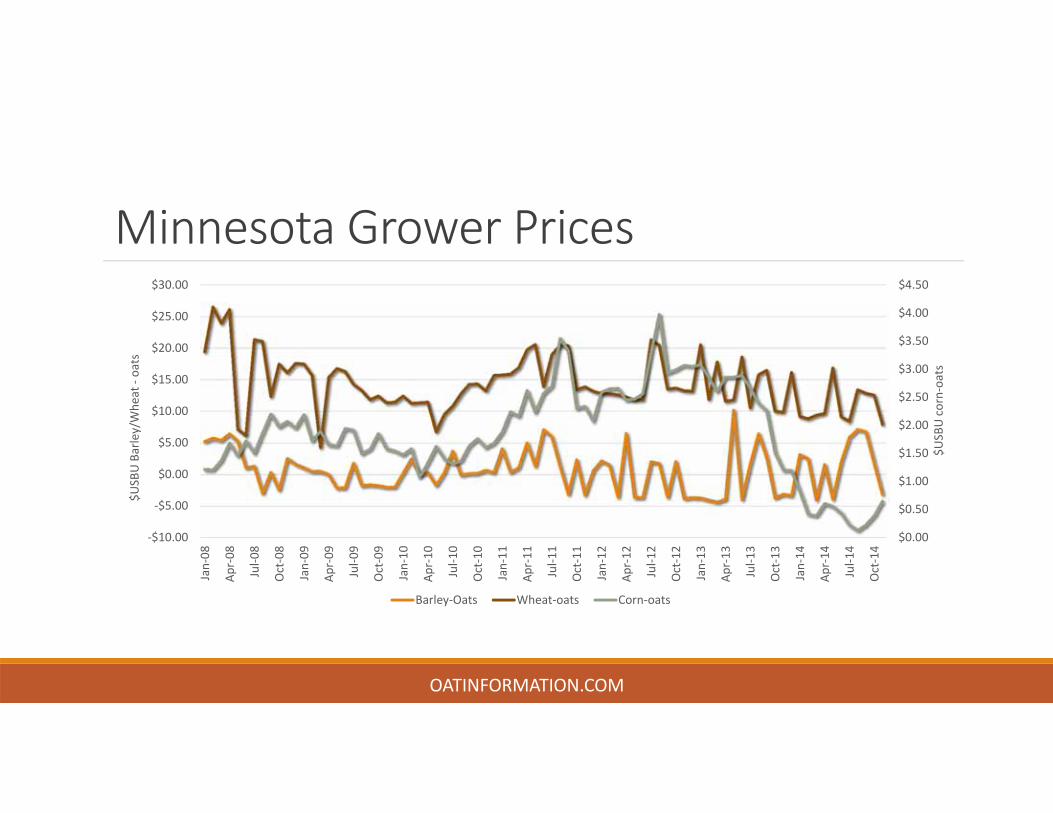

Minnesota Grower Prices

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

$3.50

$4.00

$4.50

‐$10.00

‐$5.00

$0.00

$5.00

$10.00

$15.00

$20.00

$25.00

$30.00

Jan‐08

Apr‐08

Jul‐0

8

Oct‐08

Jan‐09

Apr‐09

Jul‐0

9

Oct‐09

Jan‐10

Apr‐10

Jul‐1

0

Oct‐10

Jan‐11

Apr‐11

Jul‐1

1

Oct‐11

Jan‐12

Apr‐12

Jul‐1

2

Oct‐12

Jan‐13

Apr‐13

Jul‐1

3

Oct‐13

Jan‐14

Apr‐14

Jul‐1

4

Oct‐14

$USBU corn‐oats

$USBU Barley/Whe

at ‐oats

Barley‐Oats Wheat‐oats Corn‐oats

OATINFORMATION.COM

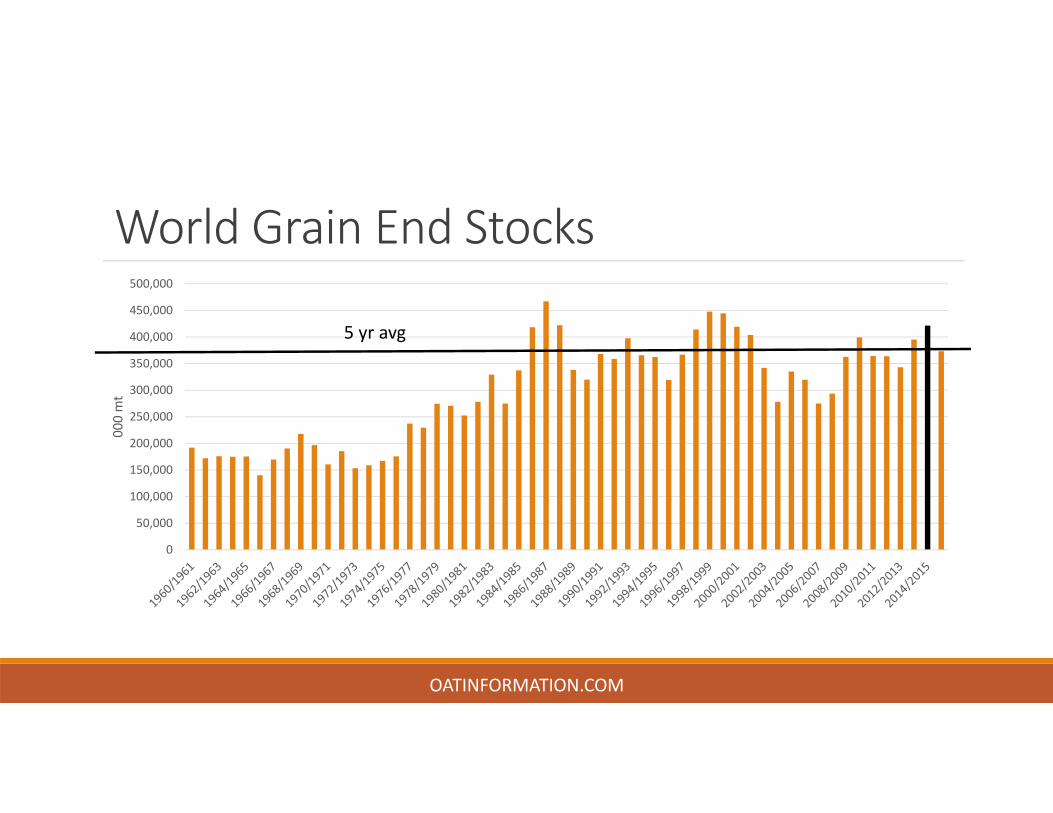

World Grain End Stocks

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

500,000

000 mt

OATINFORMATION.COM

5 yr avg

OATINFORMATION.COM

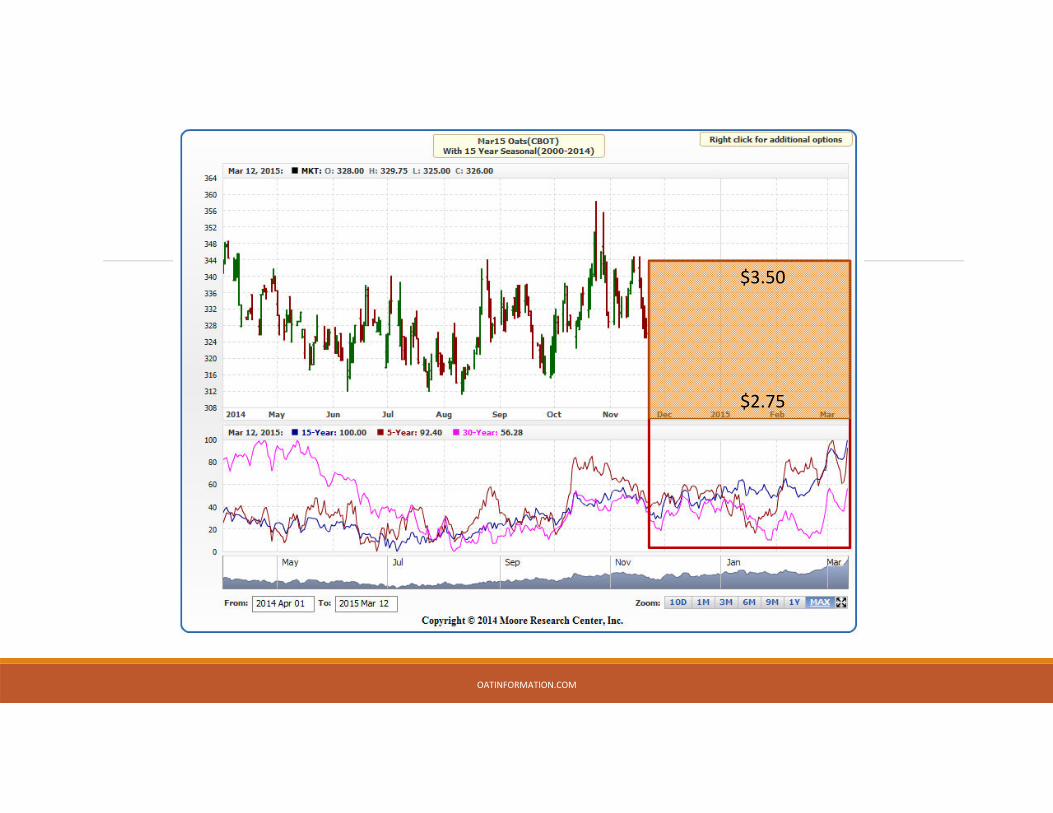

$2.75

$3.50

Oatinformation.com

OATINFORMATION.COM

The Source for Oat Information