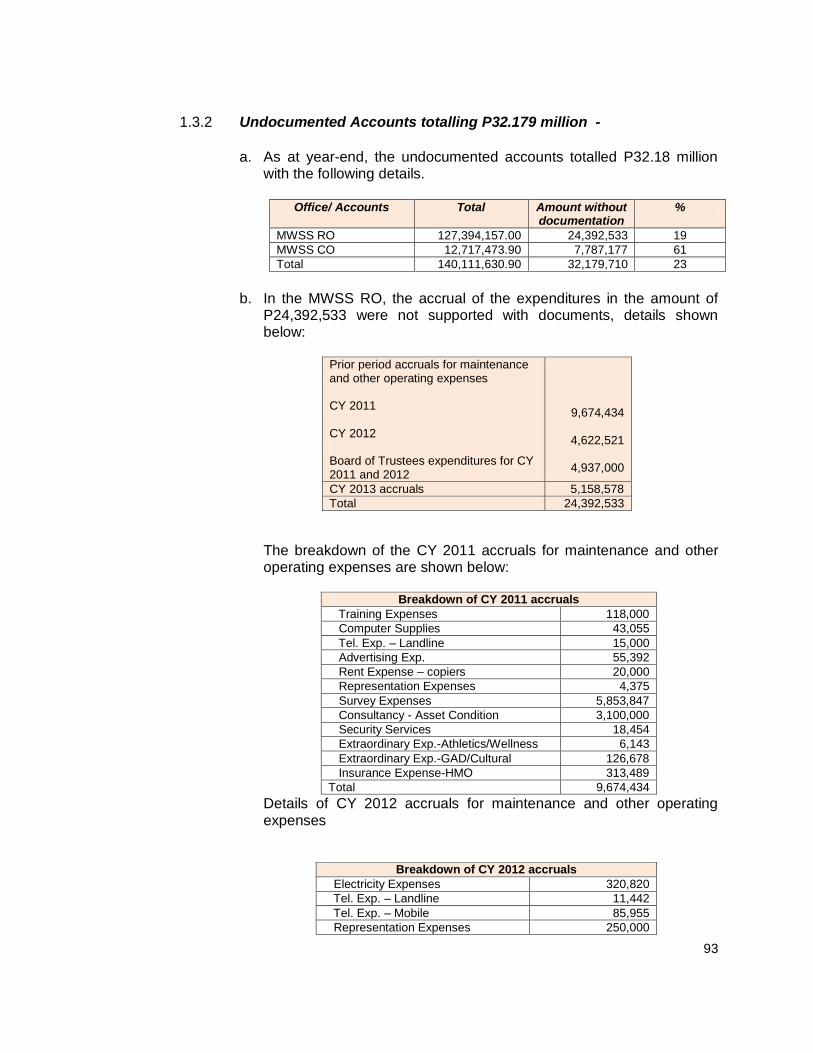

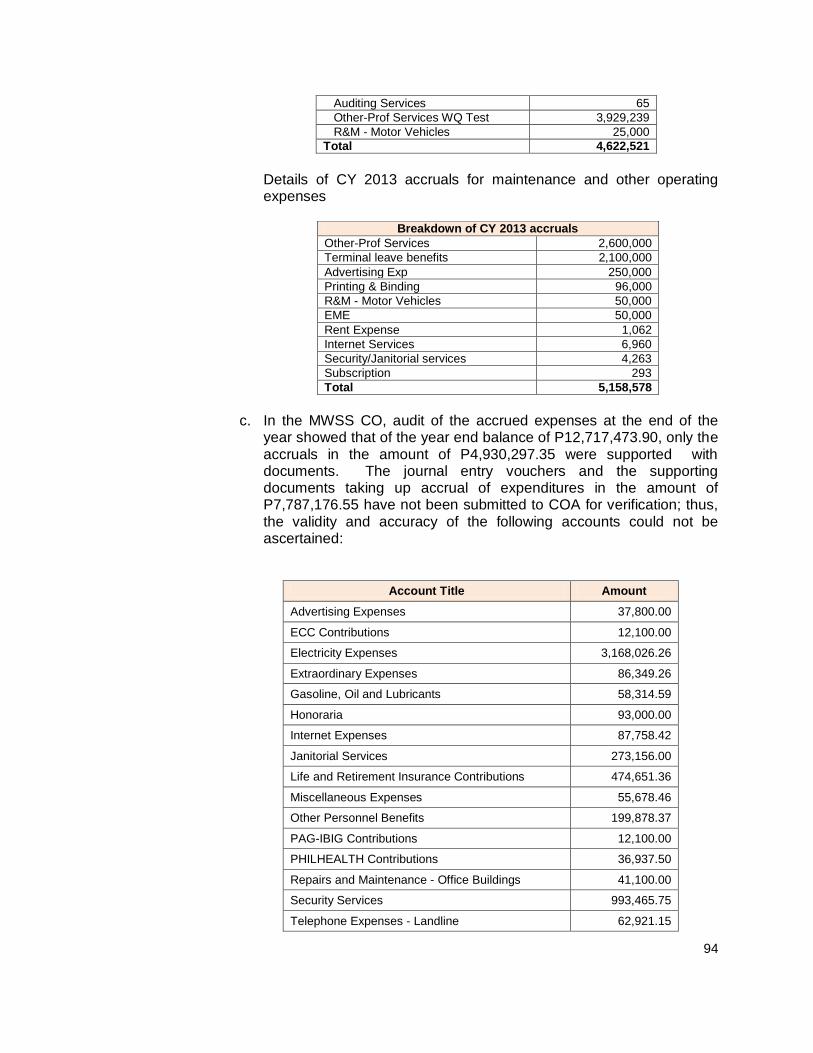

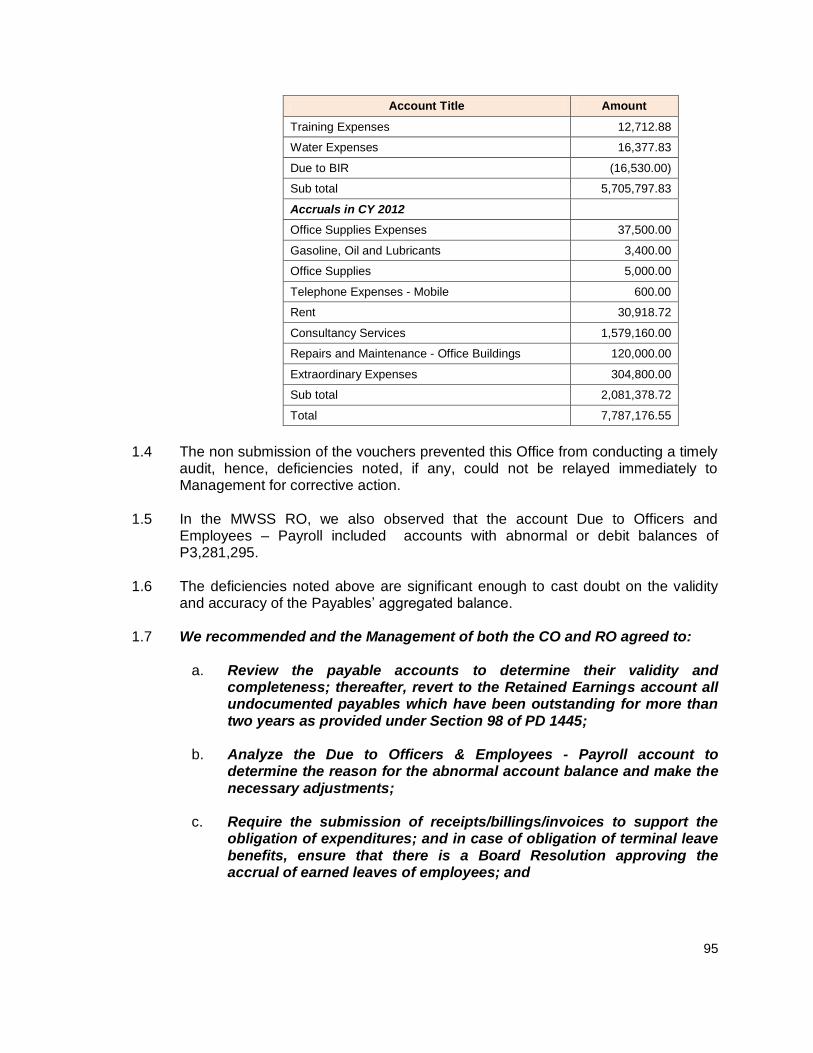

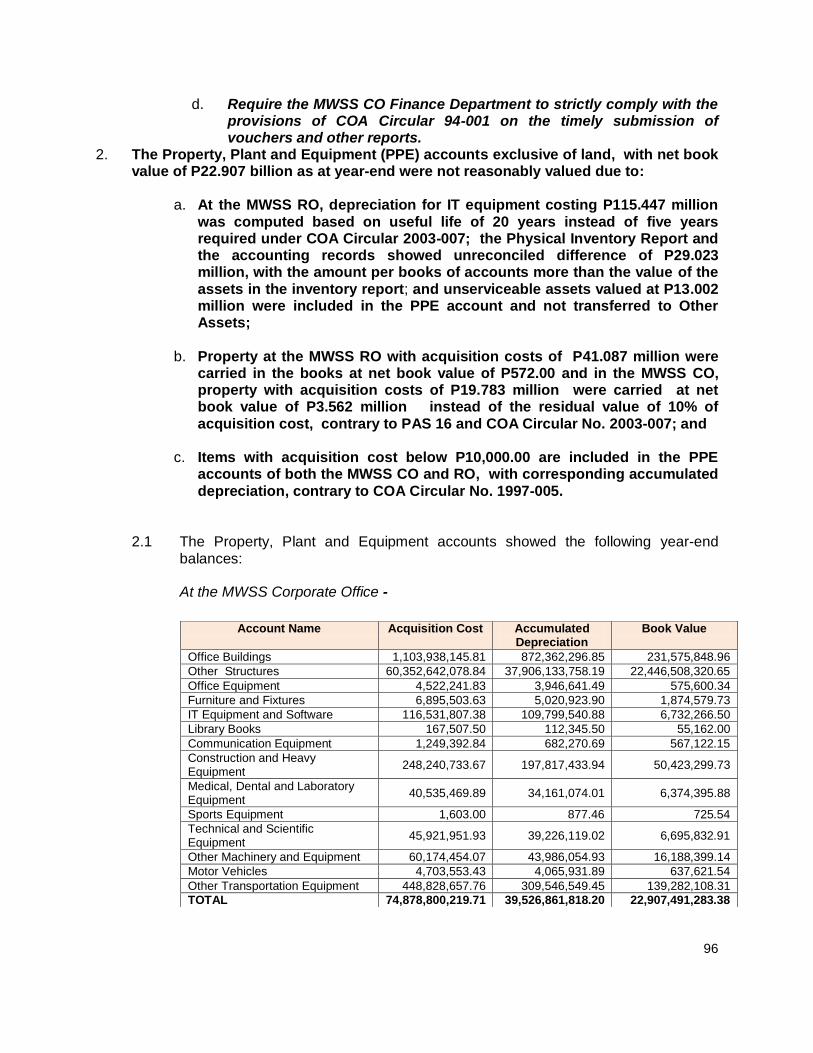

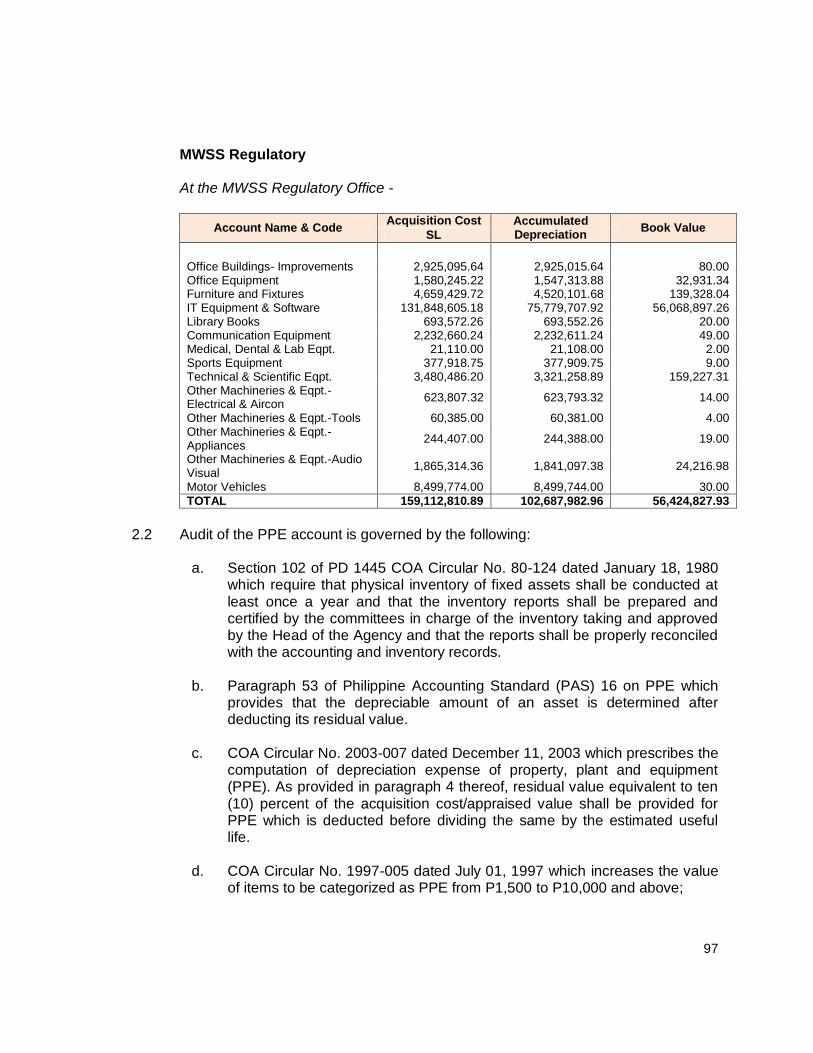

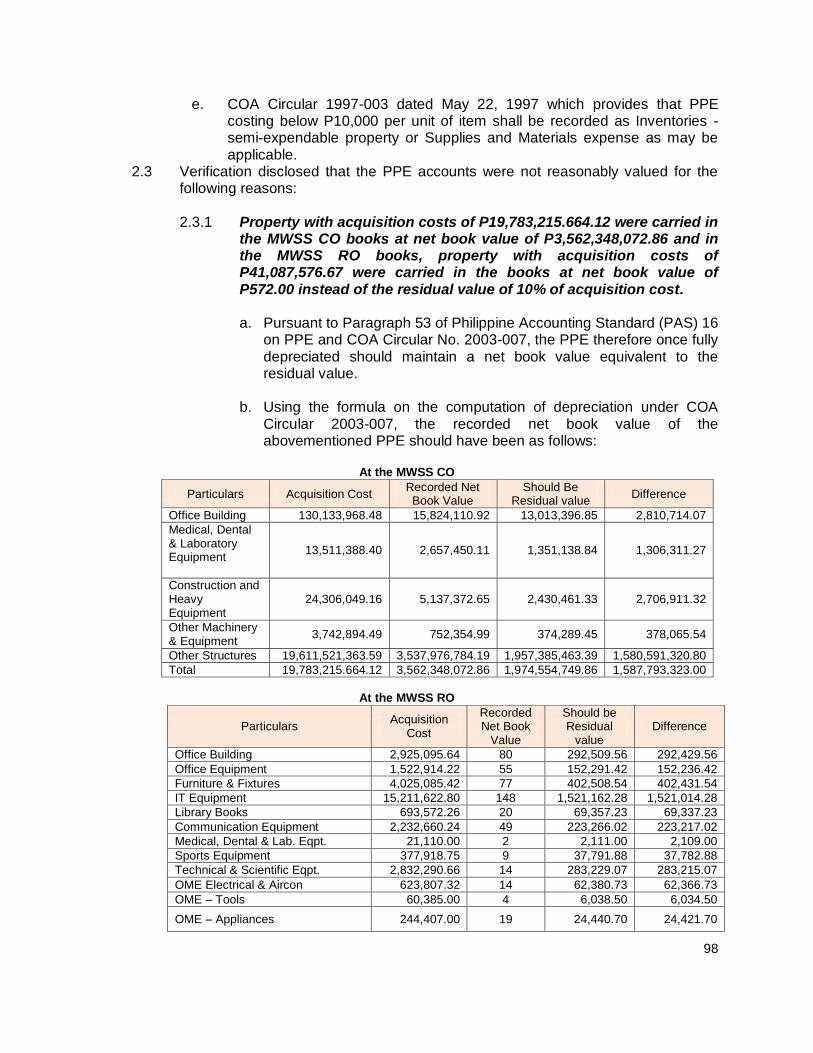

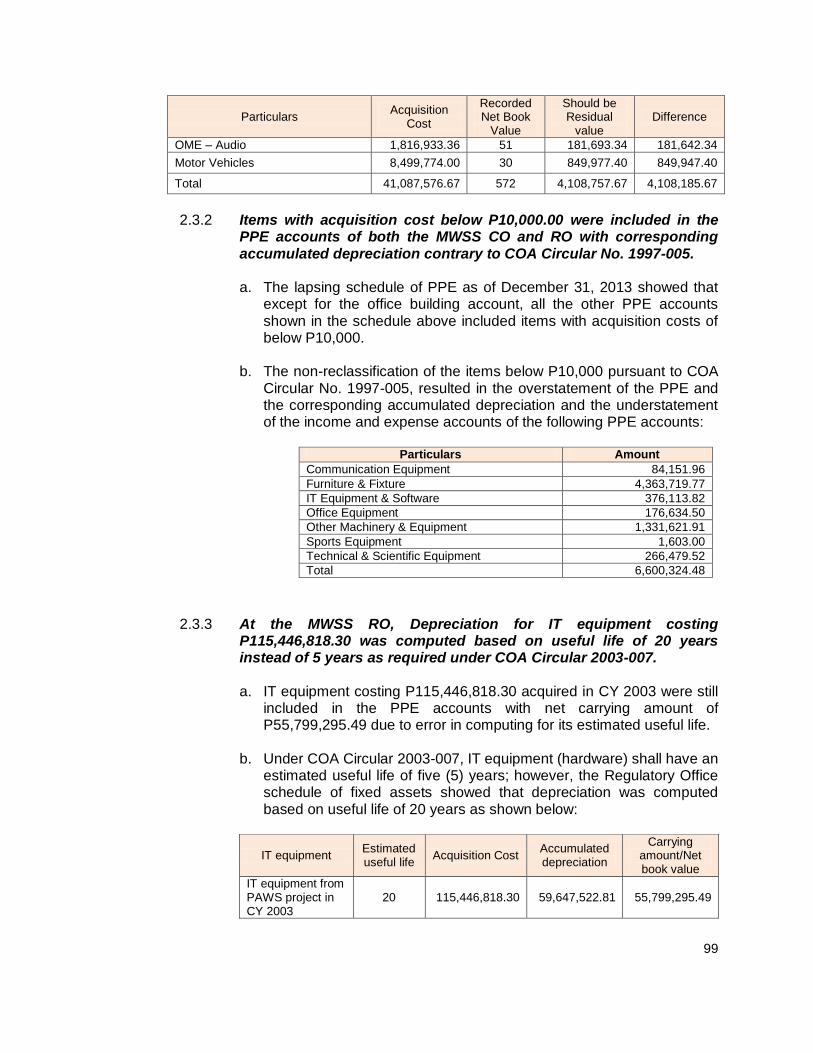

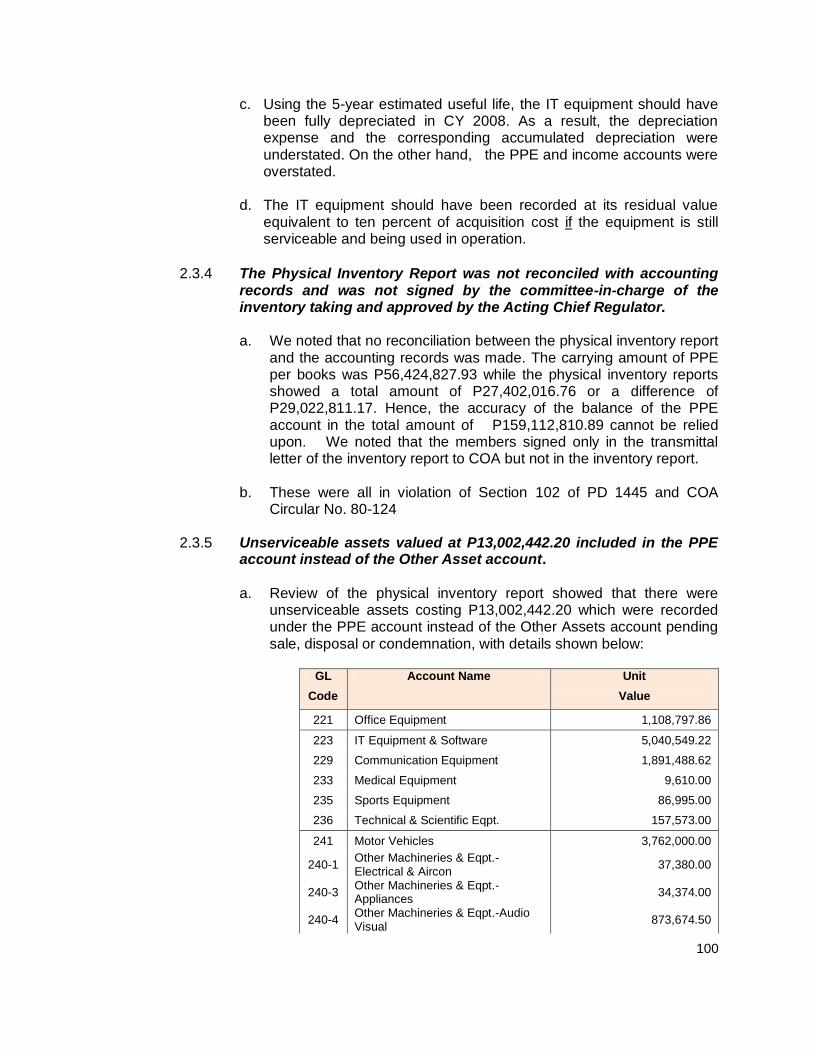

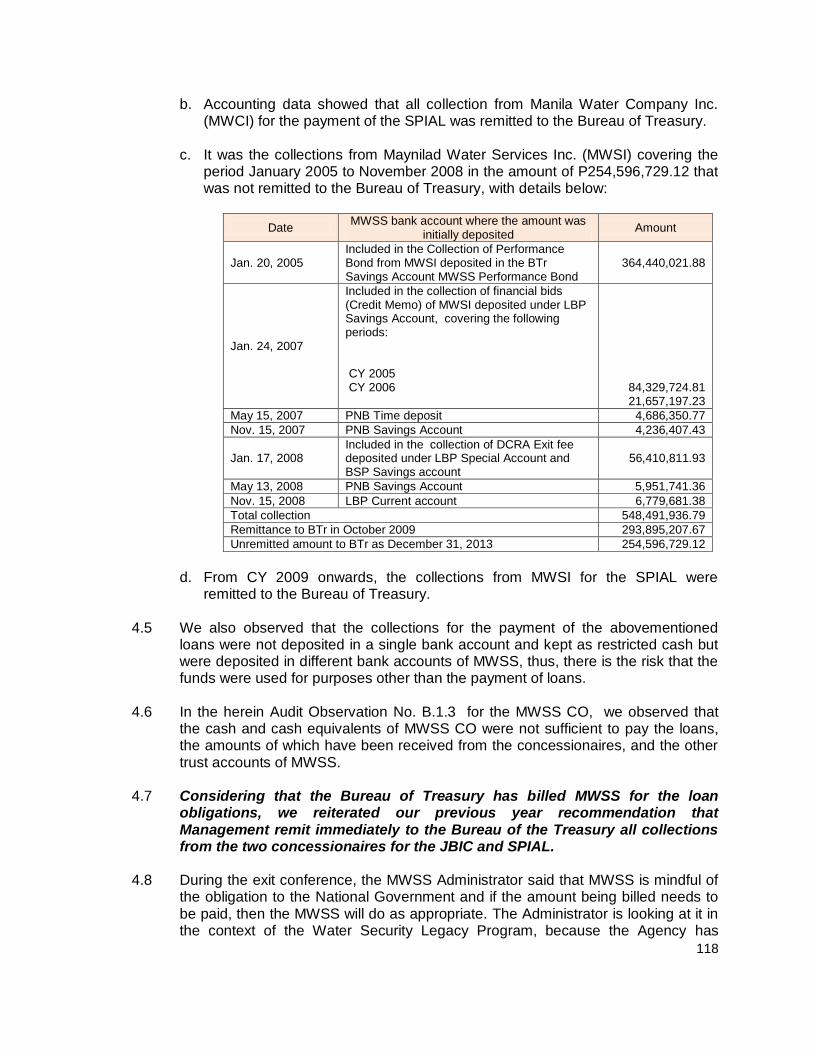

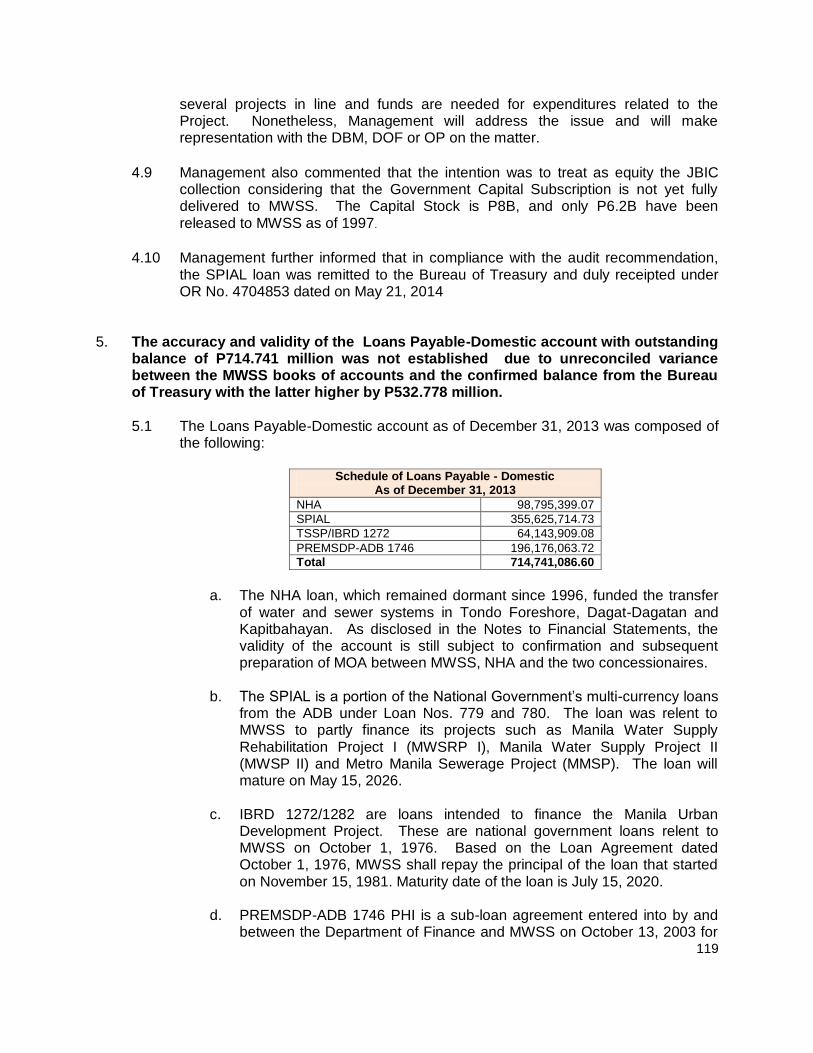

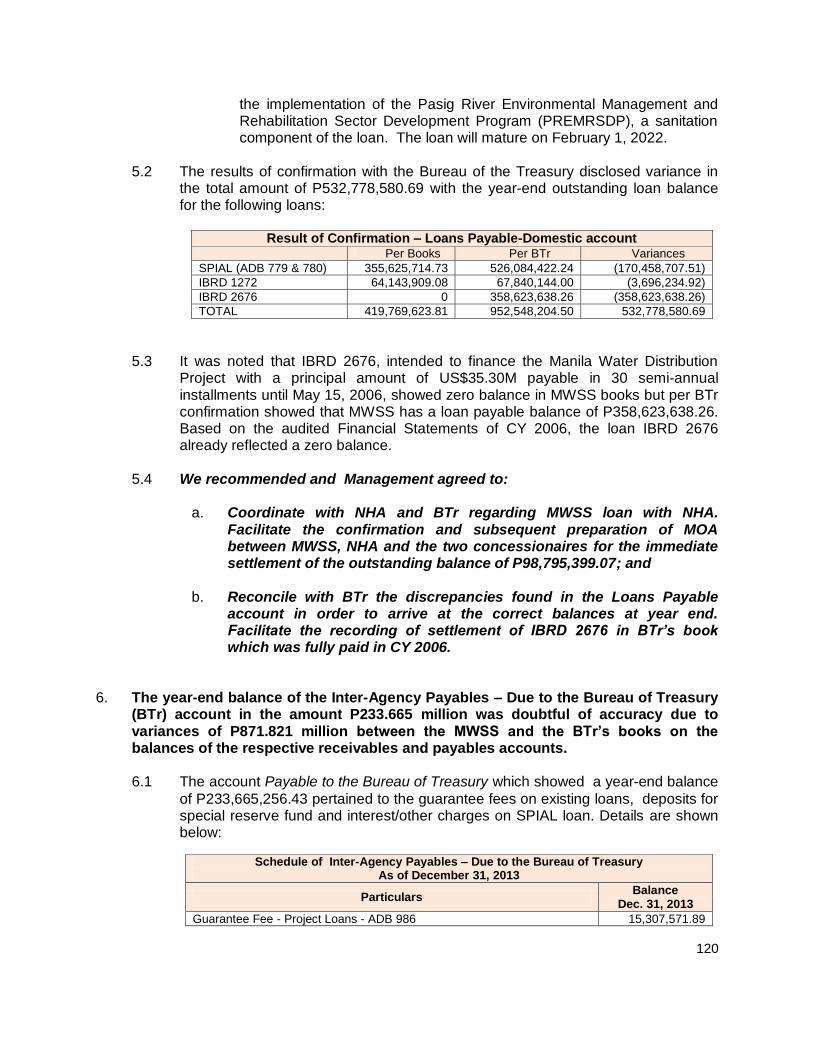

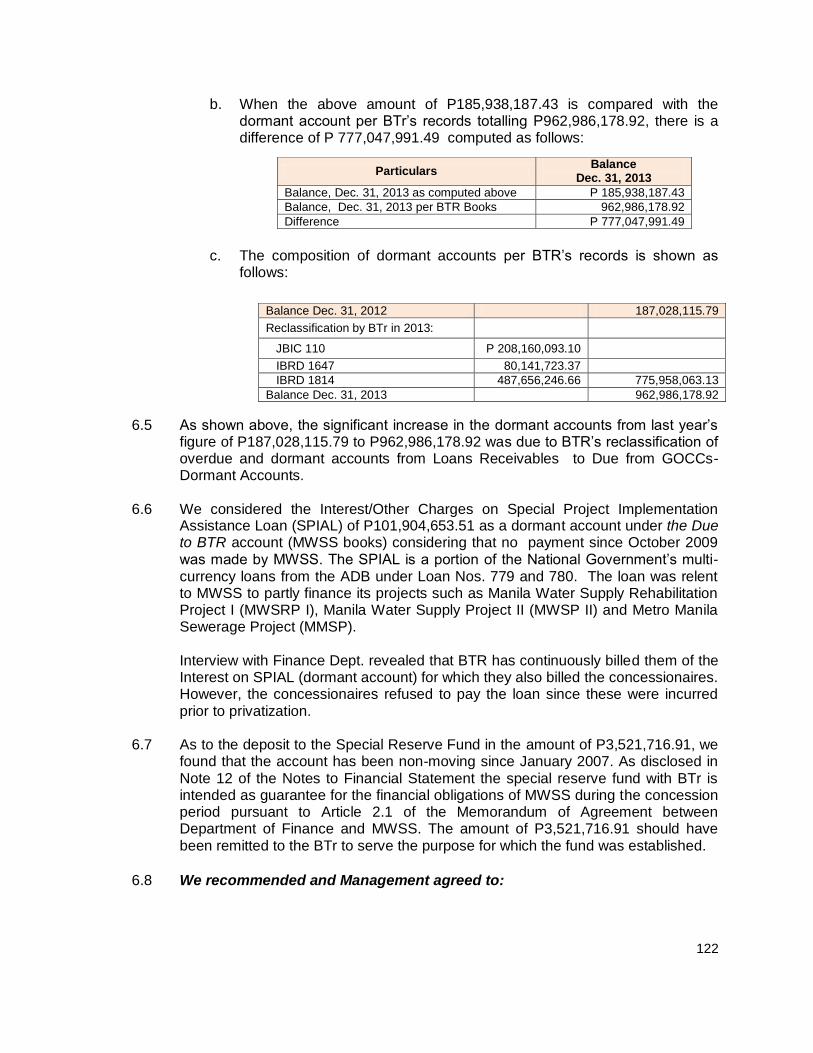

observations and recommendations - regulatory...

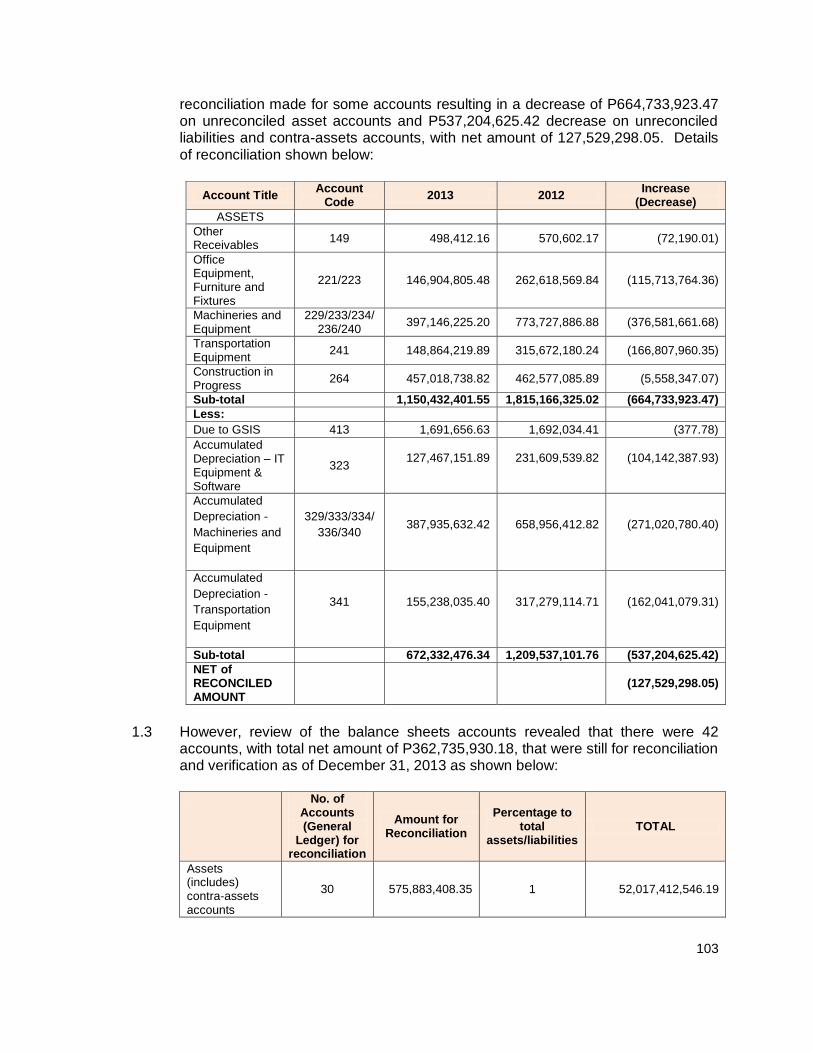

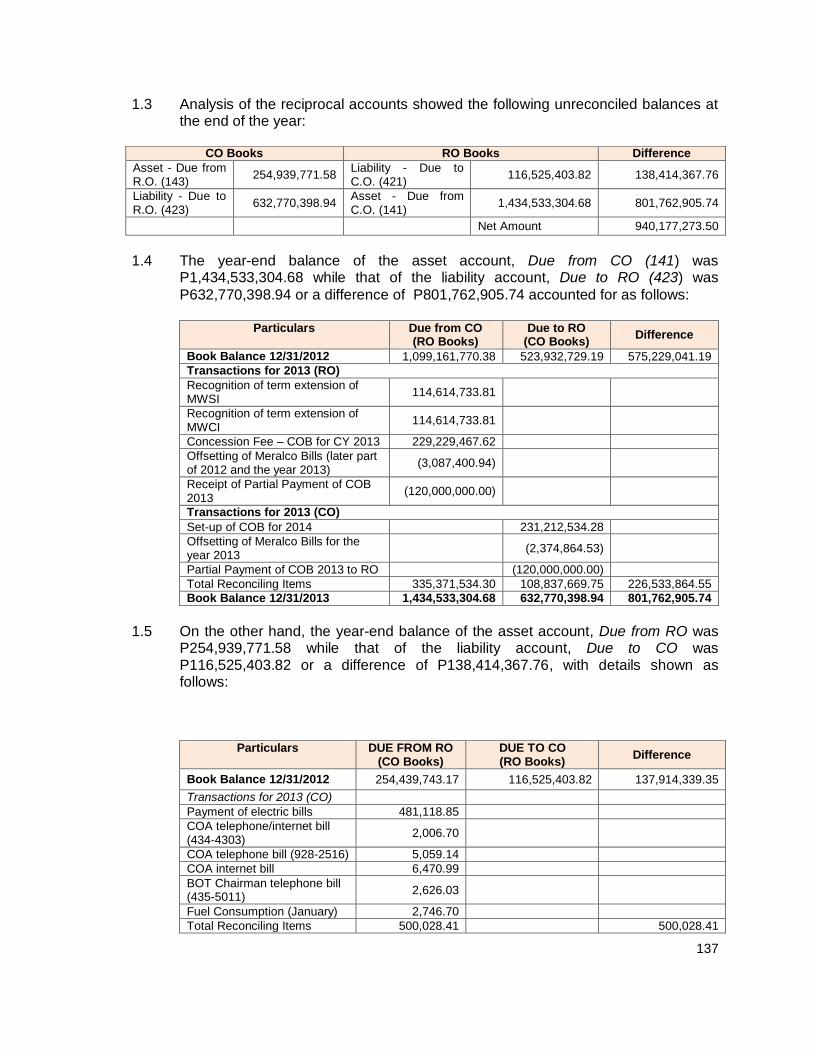

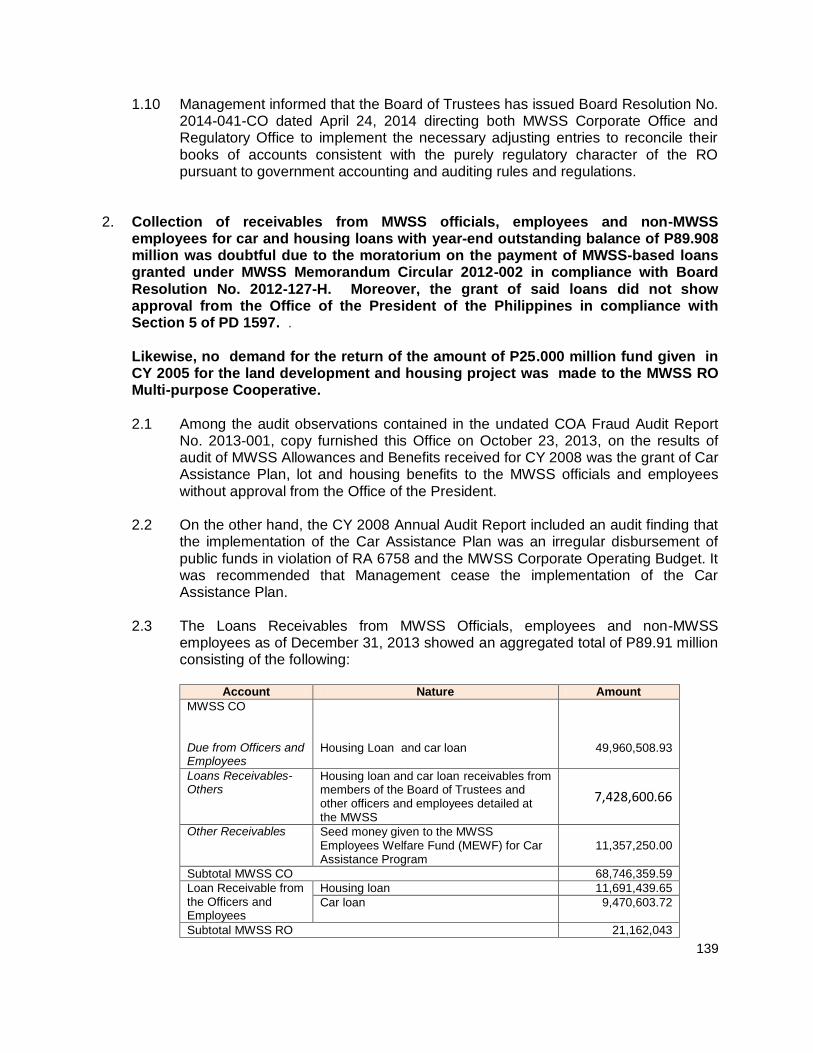

TRANSCRIPT

40

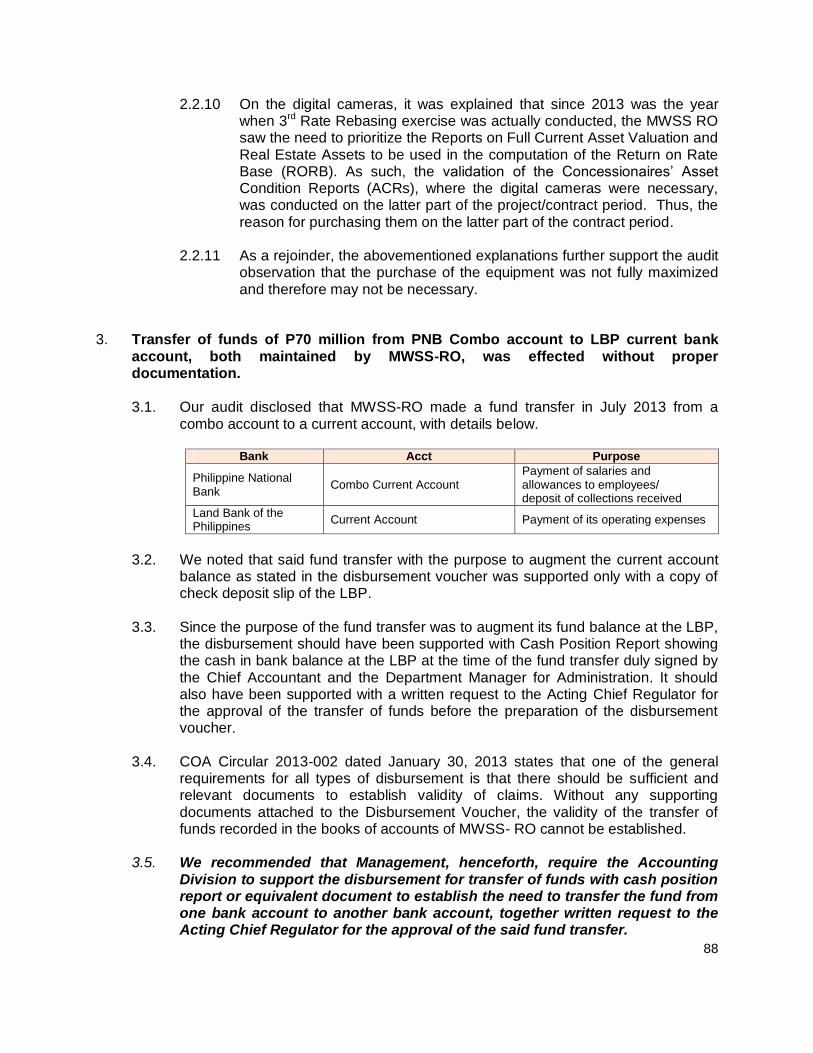

OBSERVATIONS AND RECOMMENDATIONS

A. INTRODUCTION

1. This Part consists of four sections:

Current Year’s Audit Observations and Recommendations (B)

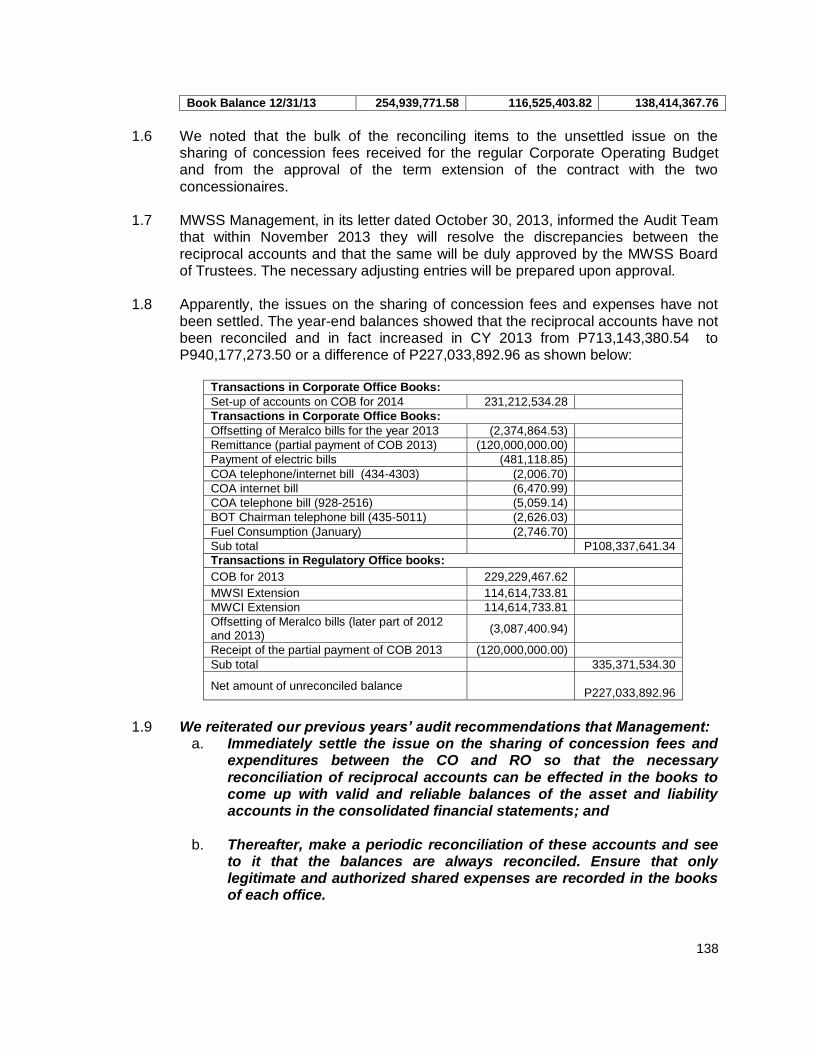

MWSS Corporate Office (CO) – B.1

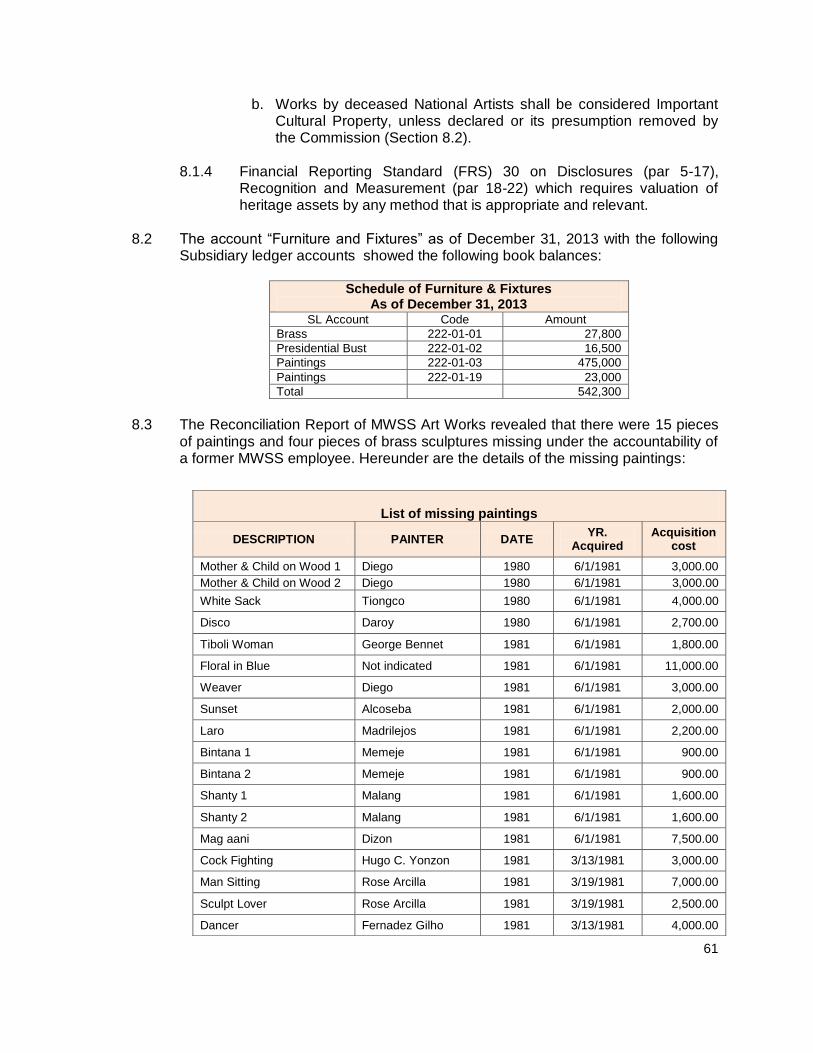

MWSS Regulatory Office (RO) – B.2

Common to MWSS CO and MWSS RO – B.3

Reiteration of Prior Year’s Audit Observations and Recommendations (C)

MWSS Corporate Office (CO) – C.1

MWSS Regulatory Office (RO) – C.2

Common to MWSS CO and MWSS RO – C.3

Value for Money (VFM) Audit (D)

Unsettled Audit Disallowances, Charges and Suspensions (E)

B. CURRENT YEAR’S AUDIT FINDINGS AND RECOMMENDATIONS 1. MWSS CORPORATE OFFICE (CO)

1. The carrying value of the Property, Plant and Equipment (PPE) at P35.408 billion

was not correctly stated due to non-conduct of revaluation/appraisal since CY 1995.

1.1 For this audit observation, we were guided by the following accounting standards and COA rule, as follows:

a. PAS 16 under paragraphs 31and 32 states that:

“31. After recognition as an asset, an item of property, plant and equipment whose fair value can be measured reliably shall be carried at a revalued amount, xxx. Revaluation shall be made with sufficient regularity to ensure that the carrying amount does not differ materially from that which would be determined using fair value at the balance sheet date. 32. The fair value of land and buildings is usually determined from the market- based evidence by appraisal that is normally undertaken by professionally qualified valuers. The fair value of items of plant and equipment is usually their market value determined by appraisal.”

41

b. COA Resolution No. 89-17 dated March 17, 1989 provides that:

“xxx, the revaluation shall be done by an independent appraiser or expert every five (5) years (on fixed assets existing as of the end of the fifth year), or even before the five year period ends, whenever there is a currency devaluation or price increase which raises price levels (based on the Consumer Price Index) xxxx”

1.2 Note 4 of the Notes to Financial Statements for CY 2013 disclosed that PPE were

stated at appraised value based on the appraisal conducted in 1995 by Cuervo Appraiser Inc. PPE acquired after said appraisal was recorded at cost.

1.3 Considering that the appraisal of assets was recommended in CY 1999 AAR,

inquiry on why no appraisal of PPE was conducted revealed that an appraisal was conducted by Cuervo Appraiser Inc. in CY 2006. However, the appraisal increments were not recorded/taken up in the books in CY 2007 because of time constraints due to the migration to eNGAS.

1.4 Since no appraisal on PPE was recorded in the books for the last 18 years, the

carrying value of the assets as of December 31, 2013 in the amount of P35,408,365,000 was not correctly stated. The PPE accounts consisted of the following:

Asset Carrying Amount (Net of Depreciation)

(in Thousand ₱)

Building, Plant, Equipment & Transmission Lines 22,678,084

Land & Land Improvements 12,444,447

Office Furniture & Other Equipment 145,912

Transportation Equipment 322,112

Total 35,408,365

1.5 We recommended and Management agreed to either:

a. Look into the possibility of using the report on the valuation of assets

used in operation by MWSS and its Concessionaires and the review and validation of the Concessionaires’ Asset Condition Report as of CY 2010 submitted by the Consultant hired for the purpose and whose report was accepted by the Regulatory Office; or

b. Immediately conduct appraisal of all its property, plant and equipment

by hiring an independent and qualified appraiser or expert as required under PAS 16 and COA Resolution No. 89-17.

2. The year-end balance of Construction-in-Progress account at P6.401 billion was not

correctly stated in view of the written information from the Deputy Administrator for Engineering & Operations, which was validated by the Audit Team, that MWSS had no on-going construction projects as of the end of CY 2013.

42

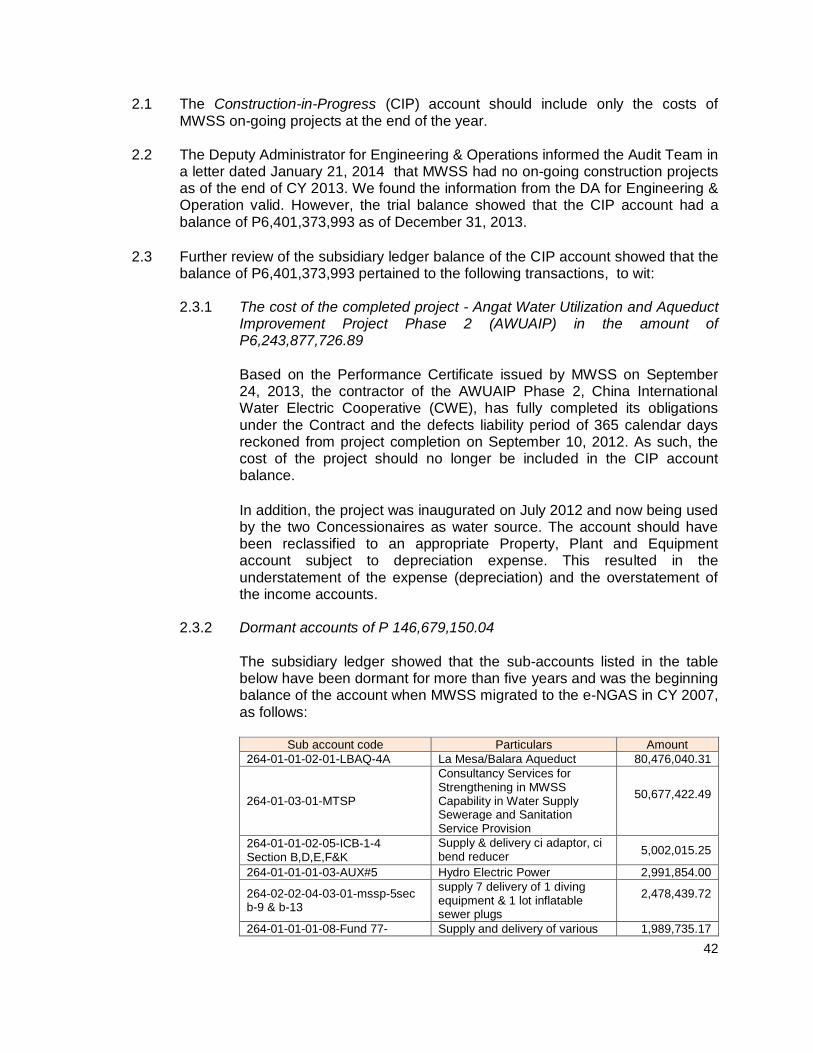

2.1 The Construction-in-Progress (CIP) account should include only the costs of MWSS on-going projects at the end of the year.

2.2 The Deputy Administrator for Engineering & Operations informed the Audit Team in a letter dated January 21, 2014 that MWSS had no on-going construction projects as of the end of CY 2013. We found the information from the DA for Engineering & Operation valid. However, the trial balance showed that the CIP account had a balance of P6,401,373,993 as of December 31, 2013.

2.3 Further review of the subsidiary ledger balance of the CIP account showed that the

balance of P6,401,373,993 pertained to the following transactions, to wit:

2.3.1 The cost of the completed project - Angat Water Utilization and Aqueduct Improvement Project Phase 2 (AWUAIP) in the amount of P6,243,877,726.89

Based on the Performance Certificate issued by MWSS on September 24, 2013, the contractor of the AWUAIP Phase 2, China International Water Electric Cooperative (CWE), has fully completed its obligations under the Contract and the defects liability period of 365 calendar days reckoned from project completion on September 10, 2012. As such, the cost of the project should no longer be included in the CIP account balance.

In addition, the project was inaugurated on July 2012 and now being used by the two Concessionaires as water source. The account should have been reclassified to an appropriate Property, Plant and Equipment account subject to depreciation expense. This resulted in the understatement of the expense (depreciation) and the overstatement of the income accounts.

2.3.2 Dormant accounts of P 146,679,150.04

The subsidiary ledger showed that the sub-accounts listed in the table below have been dormant for more than five years and was the beginning balance of the account when MWSS migrated to the e-NGAS in CY 2007, as follows:

Sub account code Particulars Amount

264-01-01-02-01-LBAQ-4A La Mesa/Balara Aqueduct 80,476,040.31

264-01-03-01-MTSP

Consultancy Services for Strengthening in MWSS Capability in Water Supply Sewerage and Sanitation Service Provision

50,677,422.49

264-01-01-02-05-ICB-1-4 Section B,D,E,F&K

Supply & delivery ci adaptor, ci bend reducer

5,002,015.25

264-01-01-01-03-AUX#5 Hydro Electric Power 2,991,854.00

264-02-02-04-03-01-mssp-5sec b-9 & b-13

supply 7 delivery of 1 diving equipment & 1 lot inflatable sewer plugs

2,478,439.72

264-01-01-01-08-Fund 77- Supply and delivery of various 1,989,735.17

43

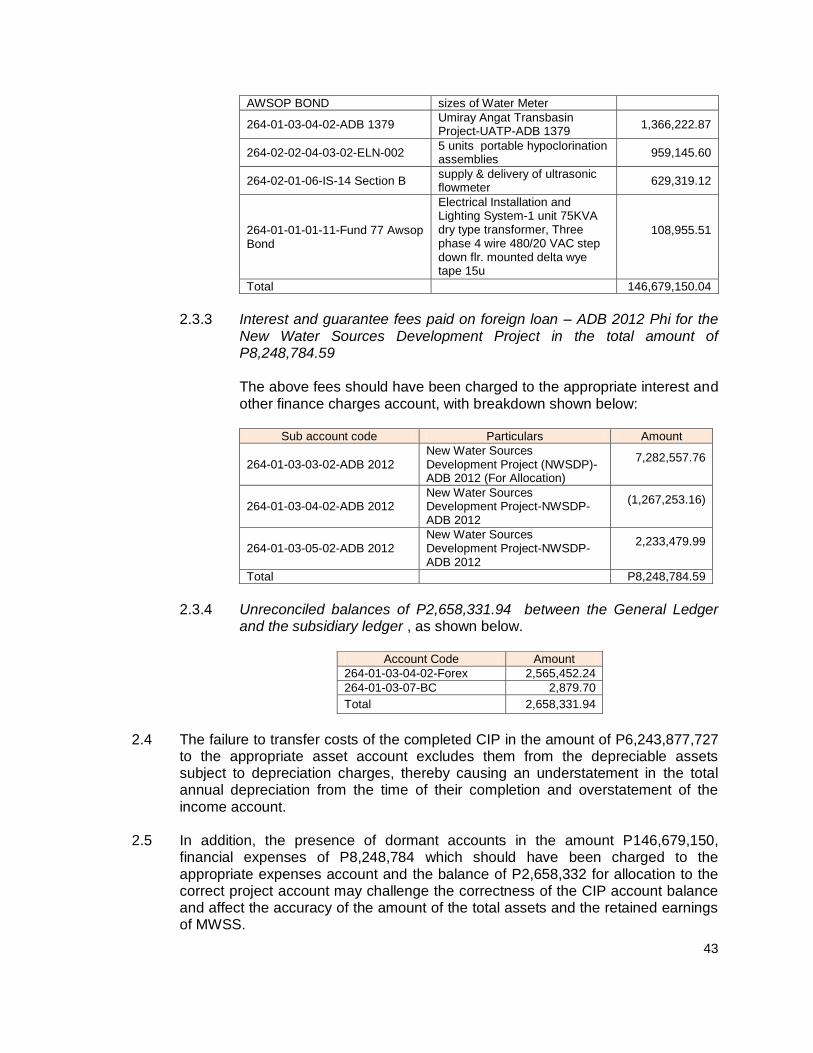

AWSOP BOND sizes of Water Meter

264-01-03-04-02-ADB 1379 Umiray Angat Transbasin Project-UATP-ADB 1379

1,366,222.87

264-02-02-04-03-02-ELN-002 5 units portable hypoclorination assemblies

959,145.60

264-02-01-06-IS-14 Section B supply & delivery of ultrasonic flowmeter

629,319.12

264-01-01-01-11-Fund 77 Awsop Bond

Electrical Installation and Lighting System-1 unit 75KVA dry type transformer, Three phase 4 wire 480/20 VAC step down flr. mounted delta wye tape 15u

108,955.51

Total 146,679,150.04

2.3.3 Interest and guarantee fees paid on foreign loan – ADB 2012 Phi for the

New Water Sources Development Project in the total amount of P8,248,784.59 The above fees should have been charged to the appropriate interest and other finance charges account, with breakdown shown below:

Sub account code Particulars Amount

264-01-03-03-02-ADB 2012 New Water Sources Development Project (NWSDP)-ADB 2012 (For Allocation)

7,282,557.76

264-01-03-04-02-ADB 2012 New Water Sources Development Project-NWSDP-ADB 2012

(1,267,253.16)

264-01-03-05-02-ADB 2012 New Water Sources Development Project-NWSDP-ADB 2012

2,233,479.99

Total P8,248,784.59

2.3.4 Unreconciled balances of P2,658,331.94 between the General Ledger

and the subsidiary ledger , as shown below.

Account Code Amount

264-01-03-04-02-Forex 2,565,452.24

264-01-03-07-BC 2,879.70

Total 2,658,331.94

2.4 The failure to transfer costs of the completed CIP in the amount of P6,243,877,727

to the appropriate asset account excludes them from the depreciable assets subject to depreciation charges, thereby causing an understatement in the total annual depreciation from the time of their completion and overstatement of the income account.

2.5 In addition, the presence of dormant accounts in the amount P146,679,150,

financial expenses of P8,248,784 which should have been charged to the appropriate expenses account and the balance of P2,658,332 for allocation to the correct project account may challenge the correctness of the CIP account balance and affect the accuracy of the amount of the total assets and the retained earnings of MWSS.

44

2.6 We recommended and Management agreed to:

a. Require the Controllership Division to reclassify to the appropriate asset account the cost of the completed project; Recognize corresponding depreciation on the cost of the project;

b. Require coordination between the project implementers and the Controllership Division to ensure the timely recording of projects completed; and

c. Immediately review the charges made to the CIP account which are

dormant and for reconciliation with the General Ledger account and effect the necessary adjustments.

2.7 Management informed that the CIP account on completed project will be

capitalized in CY 2014.

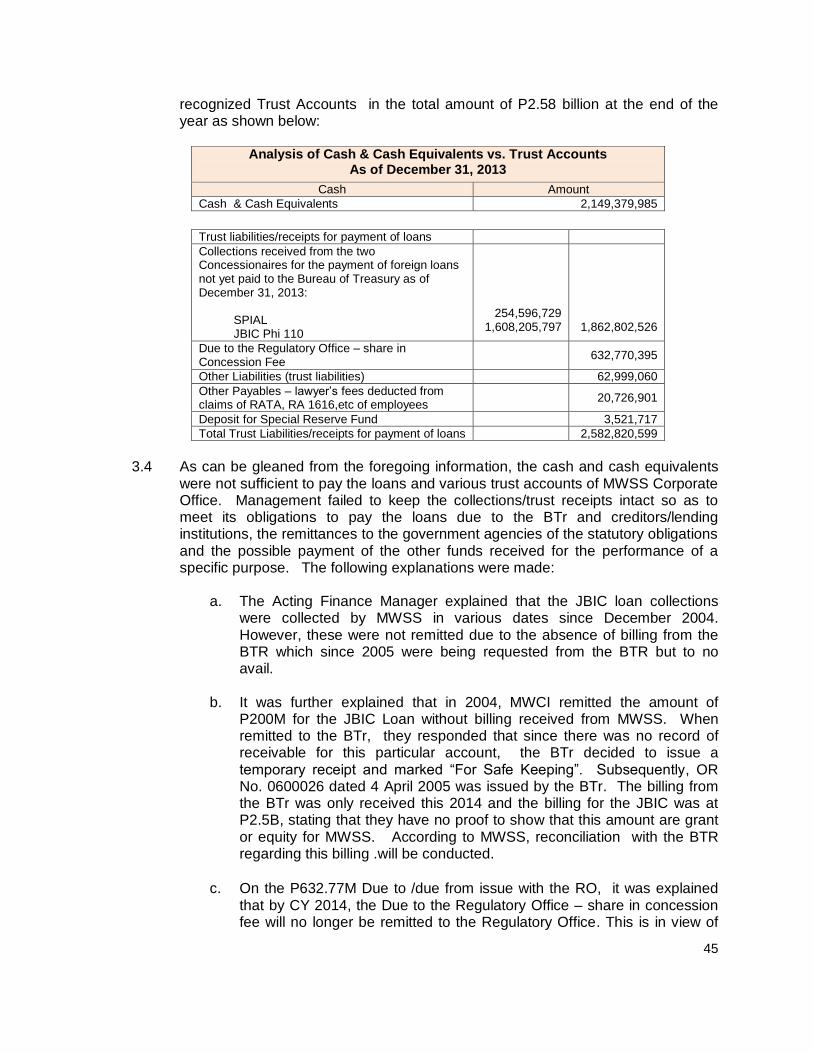

3. The Cash and cash equivalents in the amount of P2.149 billion was not sufficient to cover the Loans Payable to the Bureau of Treasury (BTr), which have been collected from the concessionaires and all recognized Trust Accounts, totalling P2.583 billion at the end of the year. This is indicative that the funds for remittance to the BTr and that the funds intended for specific purposes were used for other purposes. 3.1 Section 6 of the GAA FY 2013 provides that trust funds shall not be paid out except

for the fulfillment of the purpose for which the fund was received. Trust receipts includes receipts which are collected or received by department, bureaus and offices acting as trustee, agent or administrator; which have been received as guaranty for the fulfillment of an obligation; or classified by law, rules and regulations as trust receipts.

3.2 Based on the above definition, trust receipts of MWSS Corporate Office at the end of the year consist of the following:

a. Concession Fees collected from the concessionaires for debt servicing of

loans which have not been paid to the Bureau of Treasury as of yearend;

b. Unremitted share of the MWSS Regulatory Office (RO) from the collections from the concessionaires (MWSI & MWCI) of the Concession Income for the Corporate Operating Budget of MWSS Regulatory Office as provided under Section 11.3 of the Concession Agreement;

c. Receipts held in trust from SM Prime Holdings Inc. and the various financial

assistance for watershed programs and other funds withheld from employees claims.

3.3 Analysis of the account balances of the MWSS Corporate Office as of December

31, 2013 showed that the Cash and cash equivalents in the amount of P2.149 billion was not sufficient to cover the Loans Payable to lending institutions and all

45

recognized Trust Accounts in the total amount of P2.58 billion at the end of the year as shown below:

Analysis of Cash & Cash Equivalents vs. Trust Accounts

As of December 31, 2013

Cash Amount

Cash & Cash Equivalents 2,149,379,985

Trust liabilities/receipts for payment of loans

Collections received from the two Concessionaires for the payment of foreign loans not yet paid to the Bureau of Treasury as of December 31, 2013:

SPIAL JBIC Phi 110

254,596,729 1,608,205,797

1,862,802,526

Due to the Regulatory Office – share in Concession Fee

632,770,395

Other Liabilities (trust liabilities) 62,999,060

Other Payables – lawyer’s fees deducted from claims of RATA, RA 1616,etc of employees

20,726,901

Deposit for Special Reserve Fund 3,521,717

Total Trust Liabilities/receipts for payment of loans 2,582,820,599

3.4 As can be gleaned from the foregoing information, the cash and cash equivalents

were not sufficient to pay the loans and various trust accounts of MWSS Corporate Office. Management failed to keep the collections/trust receipts intact so as to meet its obligations to pay the loans due to the BTr and creditors/lending institutions, the remittances to the government agencies of the statutory obligations and the possible payment of the other funds received for the performance of a specific purpose. The following explanations were made:

a. The Acting Finance Manager explained that the JBIC loan collections were collected by MWSS in various dates since December 2004. However, these were not remitted due to the absence of billing from the BTR which since 2005 were being requested from the BTR but to no avail.

b. It was further explained that in 2004, MWCI remitted the amount of

P200M for the JBIC Loan without billing received from MWSS. When remitted to the BTr, they responded that since there was no record of receivable for this particular account, the BTr decided to issue a temporary receipt and marked “For Safe Keeping”. Subsequently, OR No. 0600026 dated 4 April 2005 was issued by the BTr. The billing from the BTr was only received this 2014 and the billing for the JBIC was at P2.5B, stating that they have no proof to show that this amount are grant or equity for MWSS. According to MWSS, reconciliation with the BTR regarding this billing .will be conducted.

c. On the P632.77M Due to /due from issue with the RO, it was explained

that by CY 2014, the Due to the Regulatory Office – share in concession fee will no longer be remitted to the Regulatory Office. This is in view of

46

MWSS Board of Trustees policy pronouncements under Board Resolution No. 2014-041-CO dated April 24, 2014 which stated that the distribution and allocation of Concession Fees between CO and RO will be in accordance with their Board approved Corporate Operating Budget for the calendar year subject to the limit and release schedule stipulated in Article 11.2 of the Concession Agreement.

3.5 We recommended and Management agreed to efficiently monitor its cash

flows to ensure that funds are disbursed solely for the intended purposes and strictly adhere to the provision of Section 6 of the GAA FY 2013.

3.6 In the exit conference, Management informed that the observation could also be attributed to the following:

a. Payment of Dividends in 2010 after the SONA, where the amount paid was

over the required remittance; and b. When MWSS called on the USD120M Performance bond from Maynilad

which was deposited directly to the BSP, it included the initial collection of P355M for JBIC Loan. However, the USD120M Performance Bond was used in the continuous default of Maynilad and for payment for Cost of borrowings. The said amount was not separated from such collections.

4. MWSS may face the risk of possible lawsuit arising from the lease of MWSS property along Katipunan Avenue covered by a Lease Agreement between MWSS and SM Prime Holdings Inc. which the MWSS Board of Trustees declared as null and void. MWSS received initial deposit of P33.248 million on July 13, 2010.

4.1 Perusal of the submitted documents relative to the lease contract showed that:

4.1.1 Excerpts of Minutes of the September 4, 2009 Special Meeting of the Board, under Resolution No. 2009-178, and confirmed on September 17, 2009, showed that the Board resolved (a) that based on a comparative analysis rendered by the Corporate Office as between separate proposals to lease the 1.4 hectare property of MWSS, they authorize the lease of such property to any party, at the minimum rate of P1,200.00 per square meter per annum and (b) resolved to authorize the Administrator to sign

and execute the lease agreement.

4.1.2 On October 19, 2009 the then MWSS Administrator Diosdado Jose M. Allado requested an opinion from the Office of the Government Corporate Counsel (OGCC) on (a) whether MWSS has the option to grant the lease to SM Prime Holdings Inc., pursuant to a Swiss Challenge similar to those provided in the NEDA Joint Venture Guidelines; and (b) on the appropriate procedures for such a Swiss challenge.

4.1.3 The OGCC, in a letter dated October 19, 2009 opined that:

47

“Considering that the Metropolitan Waterworks Sewerage System (MWSS) would be the lessor in the subject proposal, the applicable law is EO 301 dated 26 July 1987. xxx [i]t appears that what is involved is a negotiated procurement, subject to the provisos under the above-quoted provisions of Executive Order No. 301(1987). In this connection, we note that the request of SM for conducting a competitive challenge is not required under Executive Order No. 301 (1987). Be that as it may, said request is not legally proscribed, and in fact, as a measure of prudence, may be undertaken. In this manner, MWSS will have the opportunity to validate the reasonableness of the terms of the lease and the rental rate proposed by SM.”

Likewise, the OGCC also provided a simplified and abbreviated Swiss – challenge procedure and timeline.

4.1.4 Excerpts from the Minutes of the Committee Meeting of the Board dated

February 19, 2010 stated that Resolution No. 2010-029(E) contained the following information-

a. Board Resolution No. 2009-18 dated September 04, 2009

authorizing the lease of 1.4 hectares MWSS property, to any party, under such terms and conditions beneficial to MWSS, and OGCC Opinion dated October 19, 2009.

b. Approval and confirmation of the proposed lease to SM Prime

Holdings (SM) of the 4.1 hectare MWSS property thru Unsolicited Proposal Mode with Competitive Swiss Challenge;

c. Approval and confirmation of the corresponding procedure and

timelines of the Swiss-Challenge; and d. Approval and confirmation of the creation of the Evaluation

Committee to appraise the Comparative Proposals.

However, it was noted that the Excerpts from the Minute of the Committee Meeting, although signed by Ms. Darlina T. Uy, Manager, Legal Services Dept/Board Secretary Designate, were stamped “CANCELLED”.

4.1.5 A Contract of Lease was entered into by and between the MWSS and

SM on May 27, 2010, signed by Atty. Diosdado Jose M. Allado and Mr. Hans T. Sy, for MWSS and SM, respectively. The rate of lease was P1,200.00 per square meter.

It was noted that the authority invoked for entering into the Lease Contract were Board Resolution Nos. 2008-251 and 2009-178, dated November 20, 2008 and September 04, 2009, respectively, when the

48

latest Board resolution relating to the lease was Board Resolution No. 2010-029(E) dated February 19, 2010, and much earlier than the OGCC Opinion dated October 19, 2009.

4.1.6 MWSS received from SM the amount of P33,248,892.86 on July 13,

2010. Mr. Virgilio P. Matel, who was identified as the signatory of the issued Official Receipt No. 1320987 K also received the check issued by SM. The check was deposited with PNB on the same date under MWSS Account No. PSA 1165219406000506.

4.1.7 Excerpts from the Minutes of the 4th Special Meeting of the Board held on

August 12, 2010 (Annex 7) under Resolution No. 2010-113 stated that: “Considering that the Lease Agreement covering the 1.4 hectare MWSS property xxxx entered into by the former Administrator with SM Prime Holdings, Inc. is not in compliance with the policies and guidelines set by the xxx (OGCC) in its letter of 19 October 2009 and adopted by the Boards of Trustees under Board Resolution No. 2010-029 (E) dated 19 February 2010, the Board, RESOLVED, xxx, to DISAVOW any participation therein, and DIRECT Management to return the P33,248,892.86 payment made by SM Prime Holdings, Inc. thereto.”

Another Excerpt from the same special meeting and on the same date stated that:

“RESOLVED, that the purported Lease Agreement covering the 1.4 xxx not being in compliance with the policies and guidelines set by the Office of the Government Counsel (OGCC) in its letter dated 19 October 2009 and adopted by the Board of Trustees under Board Resolution No. 2010-029(E) dated 19 February 2010, be, as it is hereby declared null and void.” (emphasis ours)

Both resolutions were certified by Ms. Ma. Lourdes R. Naz, Board Secretary VI.

4.2 Our audit revealed the following:

4.2.1 In spite of Board Resolution No. 2010-113 dated August 12, 2010 where the then Board of Trustees disavowed any participation in the Lease Agreement and directed Management to return the payments received from SM, the amount was not returned and still remained with the MWSS bank account;

4.2.2 The copy of the Board Resolution No. 2010-029(E) dated 19 February 2010 submitted to COA was marked “CANCELLED”. However, there was no information if the cancellation was properly authorized or another Board Resolution was issued for the cancellation of the previous Board Resolution;

49

4.2.3 O.R. No. 1320987 dated July 13, 2010, acknowledging receipt of payment from SM, was issued by the Acting Finance Manager, as admitted by the Collecting Offices upon verbal query by the auditor. This was contrary to the general rule stated in GAAM Vol. I that collection of revenues and receipts shall be done by a regularly appointed Collecting Officer/Treasurer

. 4.3 MWSS then replied that:

4.3.1 Check Nos. 0058095 and 0000033962, dated July 13, 2010 and August

17, 2010, respectively, in the total amount of P33,248,892.86, were prepared in an attempt to return the amount paid by SM Prime but were declined by SM Prime.

4.3.2 MWSS agreed with our observation that receipt of the then SM payment by then Acting Finance Manager was contrary to sound internal control, and thus written instruction will be sent to the former Acting Finance Manager to submit a reply directly to the Auditor.

4.3.3 On the issue regarding Board Resolution no. 2010-029 (E) dated

February 19, 2010, a copy of the Certification from the Board Secretary was submitted.

4.3.4 The original accounting entries taking up the payment of SM Prime were

adjusted to reflect the amount received from SM Prime as a credit to Other Payables – Trust Liabilities in the amount of P33,248,892.86.

4.4 As a rejoinder to the above, we requested for the other courses of action taken by

Management after the attempts to return the rental payments including interests were declined by SM Prime Holdings Inc; and for a copy of the informal written instruction sent to the former Acting Finance Manager to explain his issuance of the O.R. instead of the designated collecting officer.

4.5 In response, Management informed, through a letter dated February 5, 2014, that

they had filed a complaint at the Office of the Ombudsman against concerned MWSS officials on September 3, 2013. They had furnished the MWSS-OIC-SA of the copies of the complaint and their letter dated February 3, 2014 addressed to, the former Acting Finance Manager directing/advising him to comment on the AOM regarding the issuance of the OR.

4.6 On April 2, 2014, the former Acting Finance Manager furnished this Office with a

copy of his Counter Affidavit with Motion to Dismiss submitted to the Office of the Ombudsman.

4.7 The filing of the case against the concerned officials of MWSS in the Office of the

Ombudsman is an action of Management to determine any possible liability and accountability of the persons responsible for the Lease Agreement.

4.8 It is our view that another major concern on this issue is on the Lease Agreement

declared as null and void by the Board of Trustees with instruction to return the

50

payment made by SM Prime Holdings Inc. in the amount of P33,248,892.86 which SM Prime Holdings Inc. declined. Considering the above, there is therefore the risk that MWSS may face possible legal action from SM Prime Holdings Inc. if the issue remains unsettled/unresolved.

4.9 We recommended that Management immediately take the best possible legal

action to resolve the issue on the Lease Agreement with SM Prime Holdings Inc.

4.10 During the exit conference, Management informed that the issue was already

discussed with the Office of the Government Corporate Counsel and are looking into the possible legal remedies of returning the money that MWSS received from SM Prime Holdings Inc. and say that the contract is void. If the same is not accepted, the money will be consigned in court.

5. Accounts Receivable from the Concessionaire – MWSI totalling US$55 million or

P2.200 billion based on current dollar rate, representing the disputed claim between MWSS and MWSI arising from MWSI’s refusal to pay for the additional COB incurred by the MWSS, remained uncollected.

Had the amount been collected, the loan could have been avoided and payments totalling P1.164 billion as of December 31, 2013 could have been used for the improvements of the Retained Assets of MWSS. 5.1 We gathered the following information from the MWSS Former Finance Manager

and confirmed by the present Acting Finance Manager :

5.1.1 Beginning on March 8, 2001, the Maynilad Water Services, Inc. (MWSI) suspended payments of concession fees to MWSS on the grounds of force majeure.

5.1.2 On December 2002, Maynilad issued a Notice of Termination of the

Concession resulting to disputes with MWSS.

5.1.3 When MAYNILAD exited from the DCRA in January 2008, the Dispute Committee created after the exit was able to establish that there is an additional Cost of Borrowings payable to MWSS in the amount of $14.79M.

5.1.4 Maynilad offered to pay the recognized Balance of Tranche B (Cost of

Borrowings) as of Jan 16, 2008 amounting to $14.79M as a result of the reconciliation made by the Committee on Disputed Claim created after the Maynilad exited from the Debt & Capital Restructuring Agreement (DCRA) in January 2008.

5.1.5 MWSS rejected the $14.79M offer because of the Quit claim that

Maynilad wanted in exchange.

51

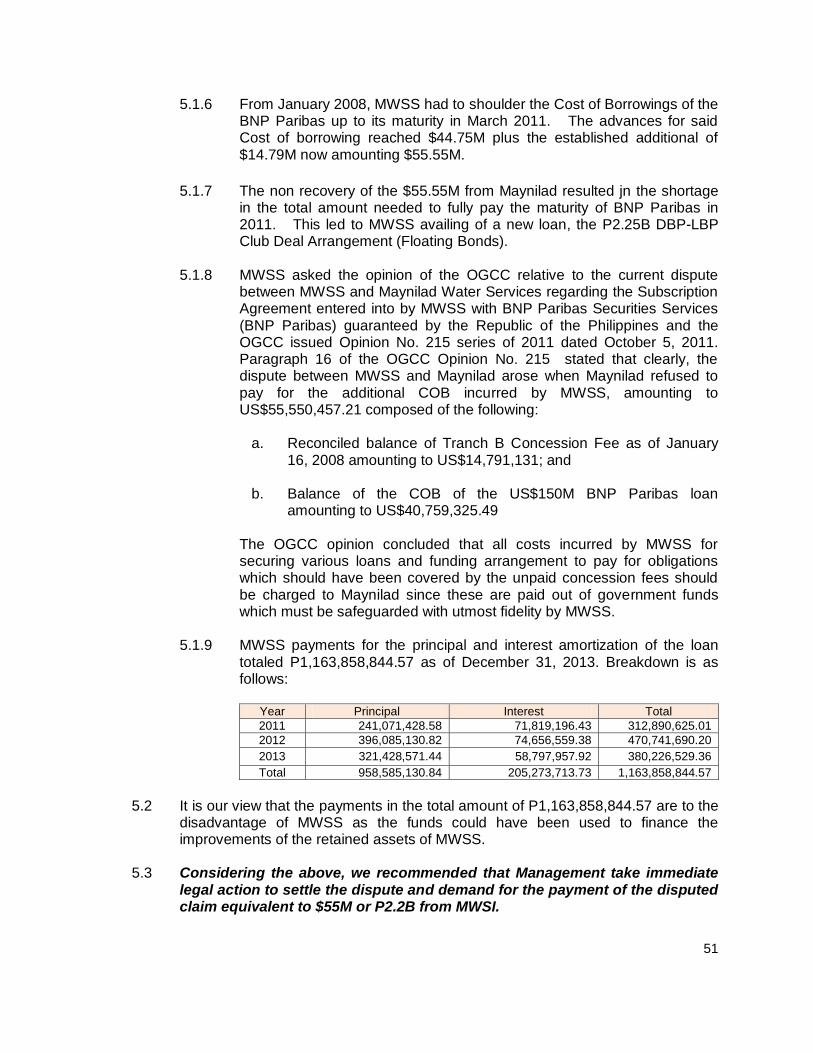

5.1.6 From January 2008, MWSS had to shoulder the Cost of Borrowings of the BNP Paribas up to its maturity in March 2011. The advances for said Cost of borrowing reached $44.75M plus the established additional of $14.79M now amounting $55.55M.

5.1.7 The non recovery of the $55.55M from Maynilad resulted jn the shortage in the total amount needed to fully pay the maturity of BNP Paribas in 2011. This led to MWSS availing of a new loan, the P2.25B DBP-LBP Club Deal Arrangement (Floating Bonds).

5.1.8 MWSS asked the opinion of the OGCC relative to the current dispute

between MWSS and Maynilad Water Services regarding the Subscription Agreement entered into by MWSS with BNP Paribas Securities Services (BNP Paribas) guaranteed by the Republic of the Philippines and the OGCC issued Opinion No. 215 series of 2011 dated October 5, 2011. Paragraph 16 of the OGCC Opinion No. 215 stated that clearly, the dispute between MWSS and Maynilad arose when Maynilad refused to pay for the additional COB incurred by MWSS, amounting to US$55,550,457.21 composed of the following:

a. Reconciled balance of Tranch B Concession Fee as of January

16, 2008 amounting to US$14,791,131; and

b. Balance of the COB of the US$150M BNP Paribas loan amounting to US$40,759,325.49

The OGCC opinion concluded that all costs incurred by MWSS for securing various loans and funding arrangement to pay for obligations which should have been covered by the unpaid concession fees should be charged to Maynilad since these are paid out of government funds which must be safeguarded with utmost fidelity by MWSS.

5.1.9 MWSS payments for the principal and interest amortization of the loan

totaled P1,163,858,844.57 as of December 31, 2013. Breakdown is as follows:

Year Principal Interest Total

2011 241,071,428.58 71,819,196.43 312,890,625.01

2012 396,085,130.82 74,656,559.38 470,741,690.20

2013 321,428,571.44 58,797,957.92 380,226,529.36

Total 958,585,130.84 205,273,713.73 1,163,858,844.57

5.2 It is our view that the payments in the total amount of P1,163,858,844.57 are to the

disadvantage of MWSS as the funds could have been used to finance the improvements of the retained assets of MWSS.

5.3 Considering the above, we recommended that Management take immediate legal action to settle the dispute and demand for the payment of the disputed claim equivalent to $55M or P2.2B from MWSI.

52

5.4 Management informed that the issue was already discussed with the OGCC on the possible filing of arbitration case against MWSI.

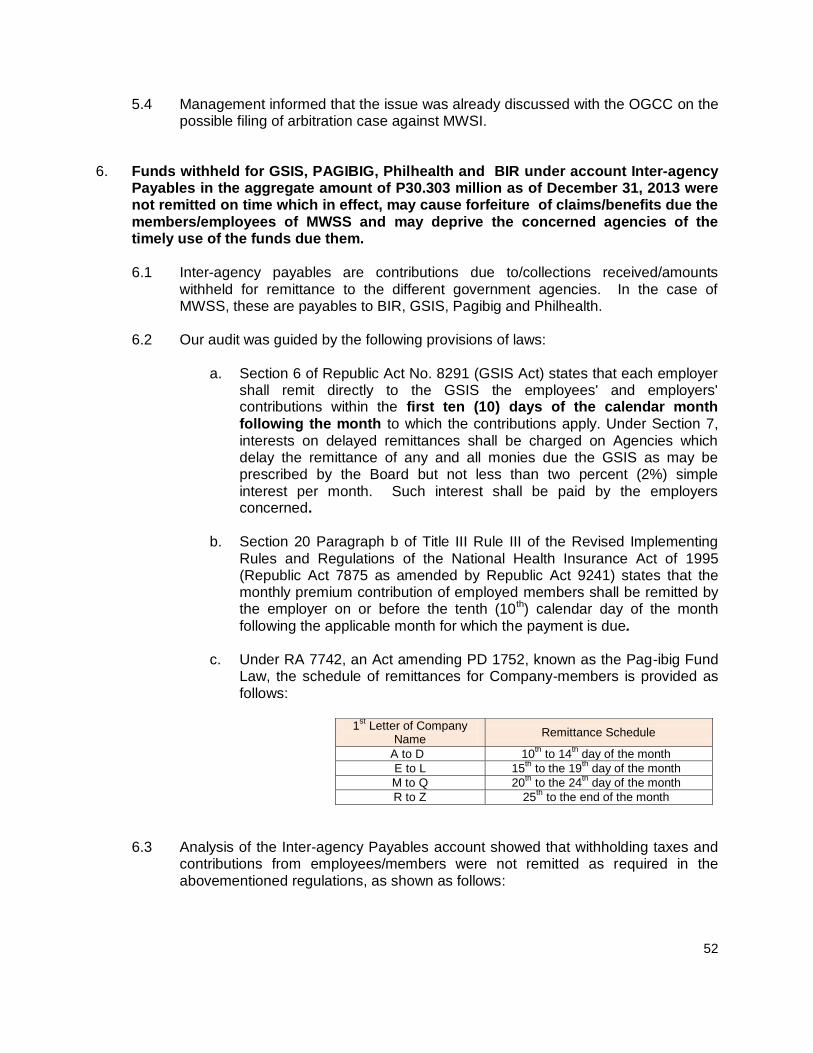

6. Funds withheld for GSIS, PAGIBIG, Philhealth and BIR under account Inter-agency

Payables in the aggregate amount of P30.303 million as of December 31, 2013 were not remitted on time which in effect, may cause forfeiture of claims/benefits due the members/employees of MWSS and may deprive the concerned agencies of the timely use of the funds due them. 6.1 Inter-agency payables are contributions due to/collections received/amounts

withheld for remittance to the different government agencies. In the case of MWSS, these are payables to BIR, GSIS, Pagibig and Philhealth.

6.2 Our audit was guided by the following provisions of laws:

a. Section 6 of Republic Act No. 8291 (GSIS Act) states that each employer shall remit directly to the GSIS the employees' and employers' contributions within the first ten (10) days of the calendar month following the month to which the contributions apply. Under Section 7, interests on delayed remittances shall be charged on Agencies which delay the remittance of any and all monies due the GSIS as may be prescribed by the Board but not less than two percent (2%) simple interest per month. Such interest shall be paid by the employers concerned.

b. Section 20 Paragraph b of Title III Rule III of the Revised Implementing

Rules and Regulations of the National Health Insurance Act of 1995 (Republic Act 7875 as amended by Republic Act 9241) states that the monthly premium contribution of employed members shall be remitted by the employer on or before the tenth (10th) calendar day of the month following the applicable month for which the payment is due.

c. Under RA 7742, an Act amending PD 1752, known as the Pag-ibig Fund

Law, the schedule of remittances for Company-members is provided as follows:

1

st Letter of Company

Name Remittance Schedule

A to D 10th to 14

th day of the month

E to L 15th to the 19

th day of the month

M to Q 20th to the 24

th day of the month

R to Z 25th to the end of the month

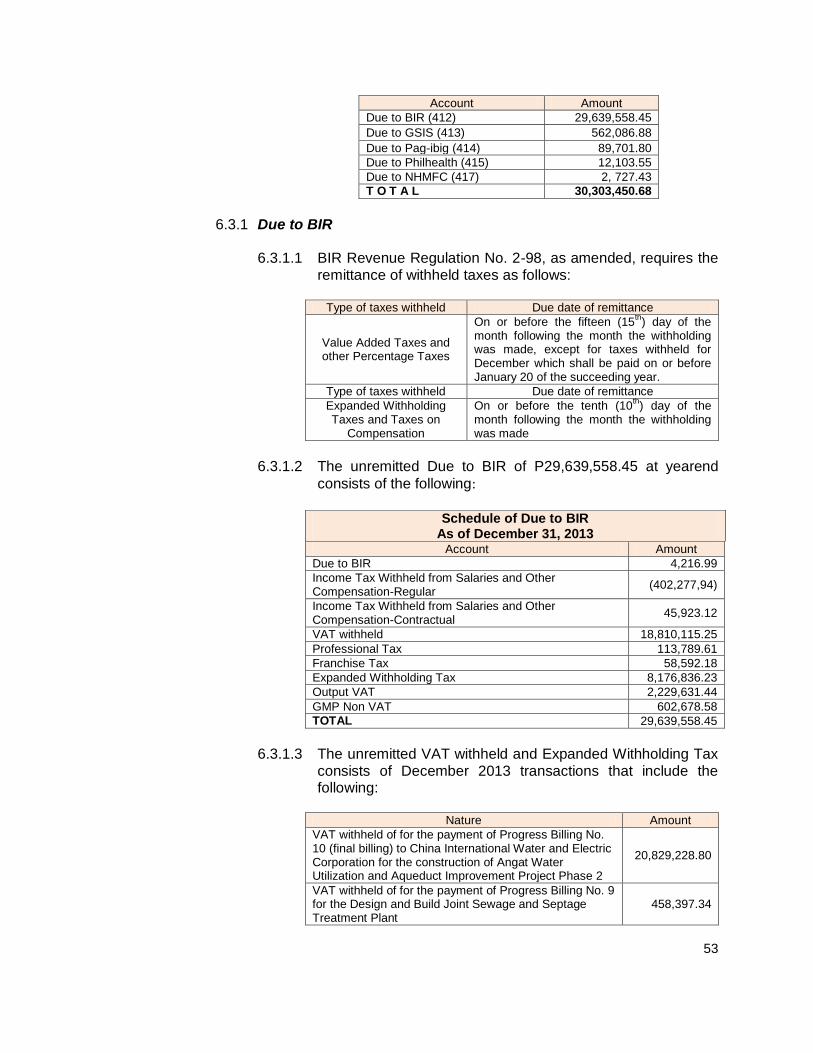

6.3 Analysis of the Inter-agency Payables account showed that withholding taxes and contributions from employees/members were not remitted as required in the abovementioned regulations, as shown as follows:

53

Account Amount

Due to BIR (412) 29,639,558.45

Due to GSIS (413) 562,086.88

Due to Pag-ibig (414) 89,701.80

Due to Philhealth (415) 12,103.55

Due to NHMFC (417) 2, 727.43

T O T A L 30,303,450.68

6.3.1 Due to BIR

6.3.1.1 BIR Revenue Regulation No. 2-98, as amended, requires the

remittance of withheld taxes as follows:

Type of taxes withheld Due date of remittance

Value Added Taxes and other Percentage Taxes

On or before the fifteen (15th) day of the

month following the month the withholding was made, except for taxes withheld for December which shall be paid on or before January 20 of the succeeding year.

Type of taxes withheld Due date of remittance

Expanded Withholding Taxes and Taxes on

Compensation

On or before the tenth (10th) day of the

month following the month the withholding was made

6.3.1.2 The unremitted Due to BIR of P29,639,558.45 at yearend

consists of the following:

Schedule of Due to BIR As of December 31, 2013

Account Amount

Due to BIR 4,216.99

Income Tax Withheld from Salaries and Other Compensation-Regular

(402,277,94)

Income Tax Withheld from Salaries and Other Compensation-Contractual

45,923.12

VAT withheld 18,810,115.25

Professional Tax 113,789.61

Franchise Tax 58,592.18

Expanded Withholding Tax 8,176,836.23

Output VAT 2,229,631.44

GMP Non VAT 602,678.58

TOTAL 29,639,558.45

6.3.1.3 The unremitted VAT withheld and Expanded Withholding Tax

consists of December 2013 transactions that include the following:

Nature Amount

VAT withheld of for the payment of Progress Billing No. 10 (final billing) to China International Water and Electric Corporation for the construction of Angat Water Utilization and Aqueduct Improvement Project Phase 2

20,829,228.80

VAT withheld of for the payment of Progress Billing No. 9 for the Design and Build Joint Sewage and Septage Treatment Plant

458,397.34

54

6.3.1.4 Management informed that the unremitted due to the BIR was due to the provision under Article 8 of the Loan Agreement between MWSS (borrower) with The Export-Import Bank of China (lender), that all payments made by the Borrower shall be paid in full to the Lender without set-off or counterclaim or retention and free and clear of and without any deduction or withholding for or on account of any taxes imposed in the Republic of the Philippines or any charges. In the event the Borrower is required by law to make such deduction or withholding from any payment hereunder, then the Borrower shall forthwith pay to the Lender such additional amount as will result in the immediate receipt by the Lender of the full amount which would have been received hereunder had no such deduction or withholding been made. The Borrower shall promptly forward to the Lender copies of official receipts or other evidence of payment to the relevant taxation or other authorities of any tax so deducted or withheld.

6.3.1.5 During the exit conference, the Acting Finance Manager

informed that Management already billed the contractor, China International Water and Electric Company (CIWEC), for the taxes due in January 2014, but since then they have not responded to the letter. In this regard, Management is contemplating on seeking the assistance of the BIR and the DPWH to be able to collect this tax out of the CIWEC receivable from other agencies.

6.3.2 Due to GSIS

6.3.2.1 Breakdown of the unremitted yearend balance of P562,086.88,

is shown below:

Schedule of Due to GSIS As of December 31, 2013 Particulars Amount

Unremitted various GSIS accounts at the end of CY 2013 5,930,141.34

Accounts with abnormal (debit) balance (5,368,054.46)

Total 562,086.88

6.3.2.2 The unremitted accounts at the end of CY 2013 are the

following:

Account Title Amount

Social Insurance Premium - PS – Regular 406,212.25

Social Insurance Premium - PS - Contractual 2,446.14

Policy Loan – Regular 35,230.94

Policy Loan Optional Contractual 1,475.24

Emergency Calamity Loan – Contractual 500.00

Salary/ Enhanced Salary Loan – Regular 5,455,191.05

Educational Loan – Regular 4,760.00

Emergency Calamity Loan – Regular 2,000.00

Summer One Month Salary – Contractual 188.89

55

Account Title Amount

Cash Advance (e-card) – Regular 3,851.80

Emergency Loan Assistance – Regular 18,185.03

State Insurance Fund – Regular 100.00

Total 5,930,141.34

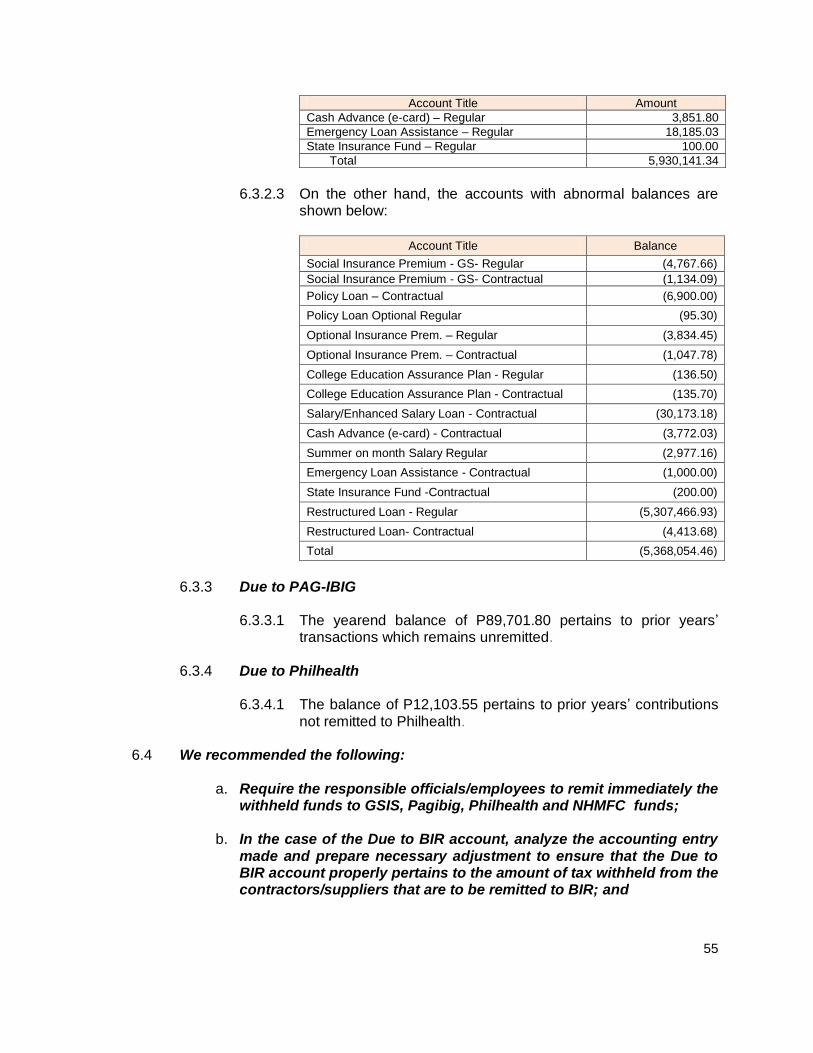

6.3.2.3 On the other hand, the accounts with abnormal balances are

shown below:

Account Title Balance

Social Insurance Premium - GS- Regular (4,767.66)

Social Insurance Premium - GS- Contractual (1,134.09)

Policy Loan – Contractual (6,900.00)

Policy Loan Optional Regular (95.30)

Optional Insurance Prem. – Regular (3,834.45)

Optional Insurance Prem. – Contractual (1,047.78)

College Education Assurance Plan - Regular (136.50)

College Education Assurance Plan - Contractual (135.70)

Salary/Enhanced Salary Loan - Contractual (30,173.18)

Cash Advance (e-card) - Contractual (3,772.03)

Summer on month Salary Regular (2,977.16)

Emergency Loan Assistance - Contractual (1,000.00)

State Insurance Fund -Contractual (200.00)

Restructured Loan - Regular (5,307,466.93)

Restructured Loan- Contractual (4,413.68)

Total (5,368,054.46)

6.3.3 Due to PAG-IBIG

6.3.3.1 The yearend balance of P89,701.80 pertains to prior years’

transactions which remains unremitted.

6.3.4 Due to Philhealth

6.3.4.1 The balance of P12,103.55 pertains to prior years’ contributions not remitted to Philhealth.

6.4 We recommended the following:

a. Require the responsible officials/employees to remit immediately the withheld funds to GSIS, Pagibig, Philhealth and NHMFC funds;

b. In the case of the Due to BIR account, analyze the accounting entry made and prepare necessary adjustment to ensure that the Due to BIR account properly pertains to the amount of tax withheld from the contractors/suppliers that are to be remitted to BIR; and

56

c. Require the Finance Department to reconcile the accounts with abnormal balances and make the necessary adjusting entries to correct the account balance in the balance sheet.

6.5 The Acting Finance Manager explained that in the process review, it was found

that posting of the payments were not reflected in the proper account and all payables were remitted to the concerned office. Adjustments will be taken up in CY 2014.

7. Prior years’ transactions amounting to P28.176 million were recorded only in the current year, resulting in numerous Prior Years’ adjustments. 7.1 One of the underlying assumptions in the preparation of the financial statements is

the accrual basis of accounting. Under this basis, the effects of transactions and other events are recognized when they occur and they are recorded in the accounting records and reported in the financial statements when they occur.

7.2 Timeliness is a quality subset of relevance. If accounting information is not presented in a timely manner, its usefulness to stakeholders is diminished or completely eliminated. The quality of timeliness requires the recording of the financial transaction in the appropriate accounting period.

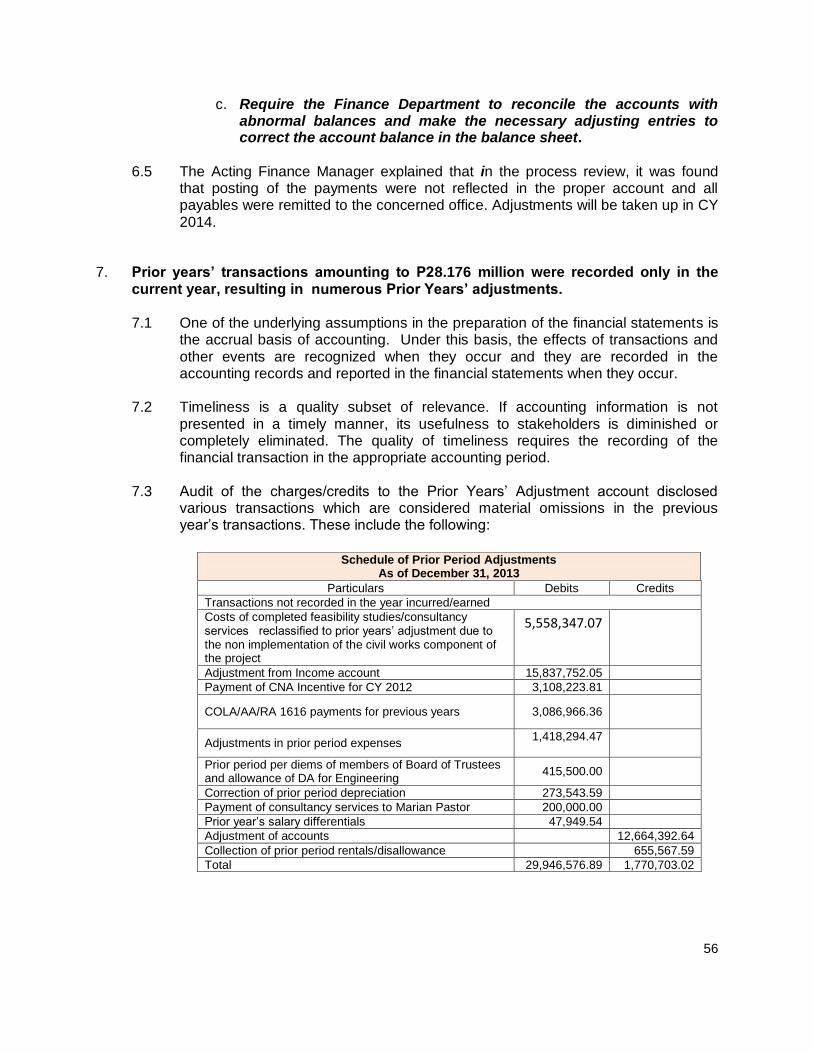

7.3 Audit of the charges/credits to the Prior Years’ Adjustment account disclosed various transactions which are considered material omissions in the previous year’s transactions. These include the following:

Schedule of Prior Period Adjustments As of December 31, 2013

Particulars Debits Credits

Transactions not recorded in the year incurred/earned

Costs of completed feasibility studies/consultancy services reclassified to prior years’ adjustment due to the non implementation of the civil works component of the project

5,558,347.07

Adjustment from Income account 15,837,752.05

Payment of CNA Incentive for CY 2012 3,108,223.81

COLA/AA/RA 1616 payments for previous years 3,086,966.36

Adjustments in prior period expenses 1,418,294.47

Prior period per diems of members of Board of Trustees and allowance of DA for Engineering

415,500.00

Correction of prior period depreciation 273,543.59

Payment of consultancy services to Marian Pastor 200,000.00

Prior year’s salary differentials 47,949.54

Adjustment of accounts 12,664,392.64

Collection of prior period rentals/disallowance 655,567.59

Total 29,946,576.89 1,770,703.02

57

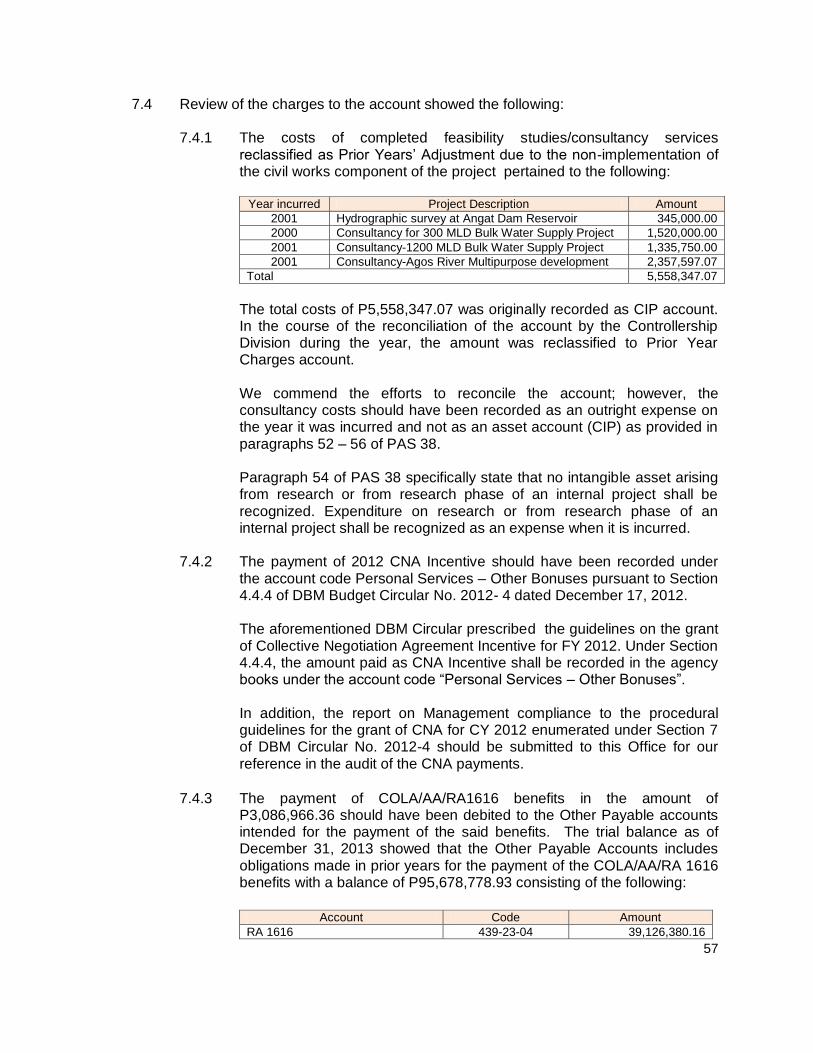

7.4 Review of the charges to the account showed the following: 7.4.1 The costs of completed feasibility studies/consultancy services

reclassified as Prior Years’ Adjustment due to the non-implementation of the civil works component of the project pertained to the following:

Year incurred Project Description Amount

2001 Hydrographic survey at Angat Dam Reservoir 345,000.00

2000 Consultancy for 300 MLD Bulk Water Supply Project 1,520,000.00

2001 Consultancy-1200 MLD Bulk Water Supply Project 1,335,750.00

2001 Consultancy-Agos River Multipurpose development 2,357,597.07

Total 5,558,347.07

The total costs of P5,558,347.07 was originally recorded as CIP account. In the course of the reconciliation of the account by the Controllership Division during the year, the amount was reclassified to Prior Year Charges account.

We commend the efforts to reconcile the account; however, the consultancy costs should have been recorded as an outright expense on the year it was incurred and not as an asset account (CIP) as provided in paragraphs 52 – 56 of PAS 38.

Paragraph 54 of PAS 38 specifically state that no intangible asset arising from research or from research phase of an internal project shall be recognized. Expenditure on research or from research phase of an internal project shall be recognized as an expense when it is incurred.

7.4.2 The payment of 2012 CNA Incentive should have been recorded under the account code Personal Services – Other Bonuses pursuant to Section 4.4.4 of DBM Budget Circular No. 2012- 4 dated December 17, 2012.

The aforementioned DBM Circular prescribed the guidelines on the grant of Collective Negotiation Agreement Incentive for FY 2012. Under Section 4.4.4, the amount paid as CNA Incentive shall be recorded in the agency books under the account code “Personal Services – Other Bonuses”. In addition, the report on Management compliance to the procedural guidelines for the grant of CNA for CY 2012 enumerated under Section 7 of DBM Circular No. 2012-4 should be submitted to this Office for our reference in the audit of the CNA payments.

7.4.3 The payment of COLA/AA/RA1616 benefits in the amount of

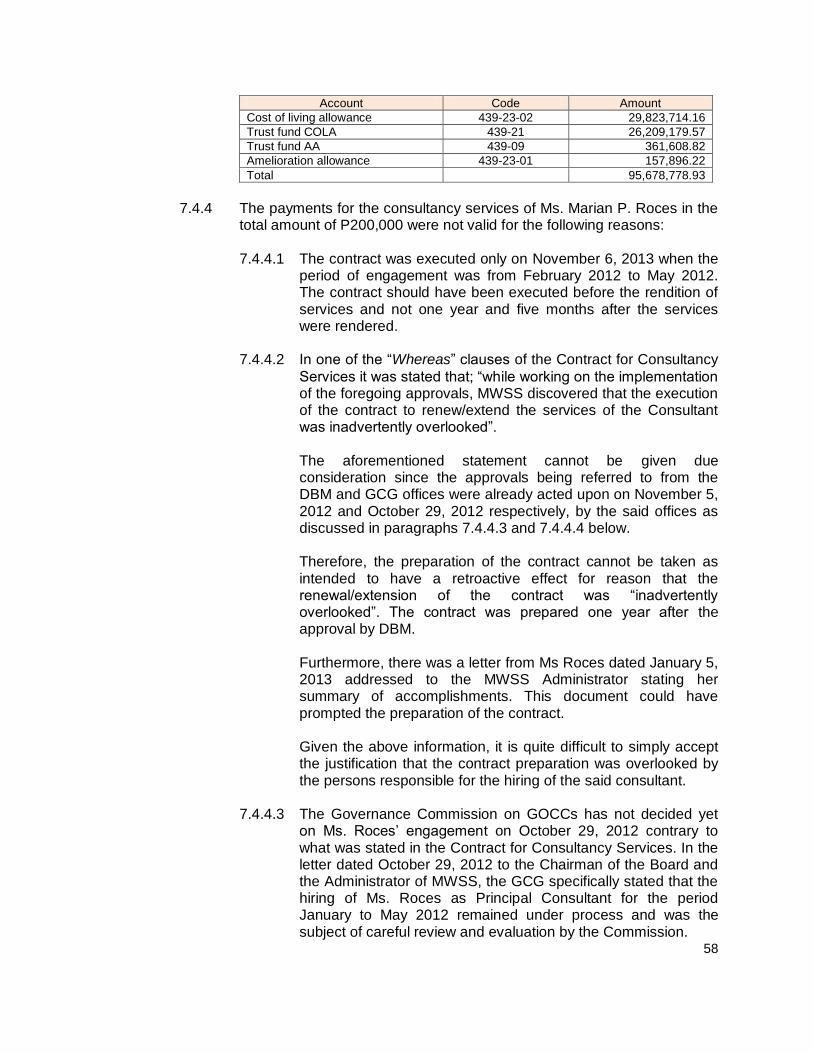

P3,086,966.36 should have been debited to the Other Payable accounts intended for the payment of the said benefits. The trial balance as of December 31, 2013 showed that the Other Payable Accounts includes obligations made in prior years for the payment of the COLA/AA/RA 1616 benefits with a balance of P95,678,778.93 consisting of the following:

Account Code Amount

RA 1616 439-23-04 39,126,380.16

58

Account Code Amount

Cost of living allowance 439-23-02 29,823,714.16

Trust fund COLA 439-21 26,209,179.57

Trust fund AA 439-09 361,608.82

Amelioration allowance 439-23-01 157,896.22

Total 95,678,778.93

7.4.4 The payments for the consultancy services of Ms. Marian P. Roces in the

total amount of P200,000 were not valid for the following reasons: 7.4.4.1 The contract was executed only on November 6, 2013 when the

period of engagement was from February 2012 to May 2012. The contract should have been executed before the rendition of services and not one year and five months after the services were rendered.

7.4.4.2 In one of the “Whereas” clauses of the Contract for Consultancy

Services it was stated that; “while working on the implementation of the foregoing approvals, MWSS discovered that the execution of the contract to renew/extend the services of the Consultant was inadvertently overlooked”.

The aforementioned statement cannot be given due consideration since the approvals being referred to from the DBM and GCG offices were already acted upon on November 5, 2012 and October 29, 2012 respectively, by the said offices as discussed in paragraphs 7.4.4.3 and 7.4.4.4 below.

Therefore, the preparation of the contract cannot be taken as intended to have a retroactive effect for reason that the renewal/extension of the contract was “inadvertently overlooked”. The contract was prepared one year after the approval by DBM. Furthermore, there was a letter from Ms Roces dated January 5, 2013 addressed to the MWSS Administrator stating her summary of accomplishments. This document could have prompted the preparation of the contract. Given the above information, it is quite difficult to simply accept the justification that the contract preparation was overlooked by the persons responsible for the hiring of the said consultant.

7.4.4.3 The Governance Commission on GOCCs has not decided yet

on Ms. Roces’ engagement on October 29, 2012 contrary to what was stated in the Contract for Consultancy Services. In the letter dated October 29, 2012 to the Chairman of the Board and the Administrator of MWSS, the GCG specifically stated that the hiring of Ms. Roces as Principal Consultant for the period January to May 2012 remained under process and was the subject of careful review and evaluation by the Commission.

59

7.4.4.4 Although the DBM approved the request of MWSS for exemption from the moratorium imposed on the hiring of consultants per Circular Letter No. 2011-14 dated December 22, 2011, the hiring of Ms Roces should have been in accordance with the provisions of the IRR of RA 9184. RA 9184 states that all procurement of the Government, whether infrastructure projects, goods and consulting services shall be competitive and transparent. It also provided that all procurement shall be done through competitive bidding, however, when it is impractical to implement competitive bidding, the law provides alternative modes of procurement under certain conditions.

There were no documents attached to prove that the hiring was a result of the bidding process prescribed in RA 9184 and its IRR. The documents attached to the voucher were copies of contract, approval from DBM, GCG letter dated October 29, 2012 and the letter of Ms. Roces stating her accomplishments for the period.

7.5 These charges to Prior Period Adjustments during the year reduced the Retained

Earnings of MWSS by P28,946,576.89.

7.6 Transactions should therefore be immediately recorded as incurred to ensure the correctness of account balances and relevance of financial information.

7.7 We recommended and Management agreed to:

a. Require the Controllership Division for future transactions to:

i. Coordinate with the Engineering Department to determine

whether there are other completed feasibility studies/consultancy services with the civil works component of the project not implemented; verify the account where the payments were previously debited and prepare necessary adjusting entries if necessary;

ii. Henceforth, record all payments for consultancy works on

research or from research phase of an internal project as expenditures on the year incurred in accordance with PAS 38;

iii. Strictly comply with the guidelines issued by the DBM on the

payment of CNA incentive specifically on the charging of expenses;

iv. Strictly record transactions as they occur to ensure that

account balances are correctly stated;

60

b. Clarify/explain the issues raised on the payment of consultancy services to Ms. Marian P. Roces.

7.8 On the above issue on the payment of consultancy services, Management

explained during the exit conference that it is very clear that what Management did was curative. Request from DBM and GCG was post facto which was ultimately approved by the DBM.

7.9 Management also informed that the consultants whose contracts expired on

August 2013 were no longer renewed and gave assurance that in future engagements they will follow the bidding process except for highly confidential positions.

8. Fifteen pieces of paintings and four brass sculptures acquired during the old NAWASA with acquisition cost of P69,400 were missing and the accountability of the persons responsible have not been settled. Moreover, all paintings with recorded value of P0. 542 million were not appraised by the National Museum as required under COA Memo 88-569 and Financial Reporting Standard (FRS) 30, resulting in the undervaluation of the value of the assets recorded in the books. Also, the oil painting by H.R. Ocampo “Abstract in Red and Black” and the water color painting “Rooster” by Kiukok, both declared National Artists of the Philippines, were not registered in the Philippine Registry of Cultural Property of the National Museum contrary to the IRR of RA 10066. 8.1 Our audit of the account is guided by the following rules and regulations:

8.1.1 Section 3 of PD 374 dated January 10, 1974 known as the “Cultural

Properties Preservation and Protection Act”, which defines works of art as paintings, sculptures, carvings, jewelery, xxx; works of industrial and commercial art such as furniture, pottery, ceramics, wrought iron, gold, bronze, silver, wood, xxx in part or in whole;

8.1.2 Section 2 (Scope and Limitations ) of COA Memorandum 88-569 dated August 12, 1988 which states that antique property and works of arts shall be appraised by the National Museum; and

8.1.3 Sections 7.2 and 8.2 Rule IV of the Implementing Rules and Regulations (IRR) of RA 10066, an act providing for the protection and conservation of the National Cultural Heritage, strengthening the National Commission for Culture and Arts (NCCA) and its affiliate cultural agencies, and for other purposes, which requires that:

a. Undeclared property not falling under the presumption of Important Cultural Property, but contains characteristics that will qualify them as such shall be registered in the Philippine Registry of Cultural Property (Section 7.2).

61

b. Works by deceased National Artists shall be considered Important Cultural Property, unless declared or its presumption removed by the Commission (Section 8.2).

8.1.4 Financial Reporting Standard (FRS) 30 on Disclosures (par 5-17),

Recognition and Measurement (par 18-22) which requires valuation of heritage assets by any method that is appropriate and relevant.

8.2 The account “Furniture and Fixtures” as of December 31, 2013 with the following

Subsidiary ledger accounts showed the following book balances:

Schedule of Furniture & Fixtures As of December 31, 2013

SL Account Code Amount

Brass 222-01-01 27,800

Presidential Bust 222-01-02 16,500

Paintings 222-01-03 475,000

Paintings 222-01-19 23,000

Total 542,300

8.3 The Reconciliation Report of MWSS Art Works revealed that there were 15 pieces

of paintings and four pieces of brass sculptures missing under the accountability of a former MWSS employee. Hereunder are the details of the missing paintings:

List of missing paintings

DESCRIPTION PAINTER DATE YR.

Acquired Acquisition

cost

Mother & Child on Wood 1 Diego 1980 6/1/1981 3,000.00

Mother & Child on Wood 2 Diego 1980 6/1/1981 3,000.00

White Sack Tiongco 1980 6/1/1981 4,000.00

Disco Daroy 1980 6/1/1981 2,700.00

Tiboli Woman George Bennet 1981 6/1/1981 1,800.00

Floral in Blue Not indicated 1981 6/1/1981 11,000.00

Weaver Diego 1981 6/1/1981 3,000.00

Sunset Alcoseba 1981 6/1/1981 2,000.00

Laro Madrilejos 1981 6/1/1981 2,200.00

Bintana 1 Memeje 1981 6/1/1981 900.00

Bintana 2 Memeje 1981 6/1/1981 900.00

Shanty 1 Malang 1981 6/1/1981 1,600.00

Shanty 2 Malang 1981 6/1/1981 1,600.00

Mag aani Dizon 1981 6/1/1981 7,500.00

Cock Fighting Hugo C. Yonzon 1981 3/13/1981 3,000.00

Man Sitting Rose Arcilla 1981 3/19/1981 7,000.00

Sculpt Lover Rose Arcilla 1981 3/19/1981 2,500.00

Dancer Fernadez Gilho 1981 3/13/1981 4,000.00

62

8.4 Perusal of the documents showed that the missing paintings and brass sculptures were under the accountability of a former MWSS employee who retired in CY 1999. He has not been granted clearance from money and property accountability and that his gratuity pay of P143,965.28 remained unpaid.

8.5 Furthermore, our audit revealed that there were no appraisal and authentication conducted by the National Museum on the above mentioned works of art as certified by the Manager, Property Management Department in a letter dated January 14, 2014. The book value recorded in the books remained at its acquisition cost of P542,300 which dates back to the old NAWASA era (prior to 1997). Considering the time that had elapsed, the value of the property recorded in the books may no longer be the relevant amount at the present time.

8.6 We recommended that Management:

a. Hold liable the officials/employees responsible for the missing 15

pieces of paintings and four brass sculptures applying the measure of liability expressed in Section 105(1) of PD 1445 which reads as follows:

“Every officer accountable for government property shall be liable for its money value in case of improper or unauthorized use or misapplication thereof, by himself or by any person for whose acts he may be responsible. He shall likewise be liable for all losses, damages, or deterioration occasioned by negligence in the keeping or use of the property, whether or not it be at the time in his actual custody.”

b. Make proper representation with the National Museum on the

conduct of appraisal and authentication of all its paintings and works of arts and the registration with the Philippine Registry of Cultural Property in compliance with the IRR of RA 10066.

8.7 It is our view that the accountability of the person/s liable for the missing paintings and brass sculptures should be based on the appraised value of the painting and the brass sculptures; the rationale being that the government shall not suffer for replacing properties lost thru negligent act of persons accountable/responsible for the property.

8.8 Management informed that on February 27, 2014, requests for appraisal and authentication of its paintings and art works and registration of the works of the National Artists were made and awaiting their positive response on the said request.

Mother And Child Boni Arcilla 1981 3/19/1981 1,500.00

TOTAL 63,200.00

63

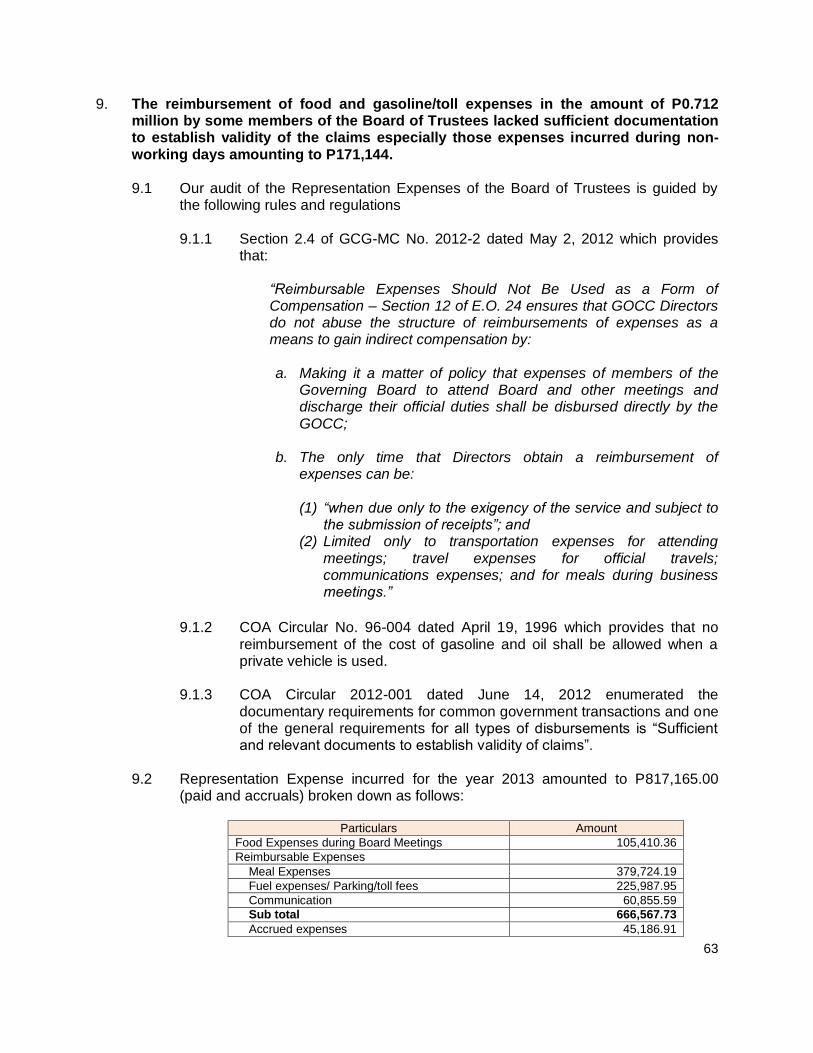

9. The reimbursement of food and gasoline/toll expenses in the amount of P0.712 million by some members of the Board of Trustees lacked sufficient documentation to establish validity of the claims especially those expenses incurred during non-working days amounting to P171,144.

9.1 Our audit of the Representation Expenses of the Board of Trustees is guided by

the following rules and regulations 9.1.1 Section 2.4 of GCG-MC No. 2012-2 dated May 2, 2012 which provides

that:

“Reimbursable Expenses Should Not Be Used as a Form of Compensation – Section 12 of E.O. 24 ensures that GOCC Directors do not abuse the structure of reimbursements of expenses as a means to gain indirect compensation by: a. Making it a matter of policy that expenses of members of the

Governing Board to attend Board and other meetings and discharge their official duties shall be disbursed directly by the GOCC;

b. The only time that Directors obtain a reimbursement of

expenses can be:

(1) “when due only to the exigency of the service and subject to the submission of receipts”; and

(2) Limited only to transportation expenses for attending meetings; travel expenses for official travels; communications expenses; and for meals during business meetings.”

9.1.2 COA Circular No. 96-004 dated April 19, 1996 which provides that no

reimbursement of the cost of gasoline and oil shall be allowed when a private vehicle is used.

9.1.3 COA Circular 2012-001 dated June 14, 2012 enumerated the documentary requirements for common government transactions and one of the general requirements for all types of disbursements is “Sufficient and relevant documents to establish validity of claims”.

9.2 Representation Expense incurred for the year 2013 amounted to P817,165.00

(paid and accruals) broken down as follows:

Particulars Amount

Food Expenses during Board Meetings 105,410.36

Reimbursable Expenses

Meal Expenses 379,724.19

Fuel expenses/ Parking/toll fees 225,987.95

Communication 60,855.59

Sub total 666,567.73

Accrued expenses 45,186.91

64

Total reimbursable expenses 711,754.64

Total representation expenses 817,165.00

9.3 Our audit revealed the following:

a. Of the total representation expenses of P817,165, claims for

reimbursement of expenses by some members of the Board of Trustees in the amount of P666,567.73 were only evidenced with official receipts covering mostly expenses for food, communication, gasoline, parking and toll fees. The accrual of expenses in the amount of P45,186.91 under JEV 2013-12-007445 was supported with only a memorandum from the Board Secretary submitting to the Finance Department the list of reimbursable expenses and the summary of accrued expenses for the year.

There was no documentation showing that these reimbursable expenses were incurred in the performance of official functions required in COA Circular 2012-001 which generally requires “sufficient and relevant documents to establish validity of claim”. Of the amount of P711,754.64,

expenses amounting to P171,144 were incurred on non-working days (Saturdays and Sundays). We also noted that a claim for reimbursement was paid through a credit card of another person and not of the MWSS official.

b. In the case of gasoline and toll fees claimed in the amount of

P225,987.95, only the gasoline receipts were submitted without any information on whether the vehicle was a private or government vehicle. If the vehicle is privately owned, Section 3.1.1.8 of COA Circular 96-004 dated April 19, 1996 provides that under no circumstances should fuel be issued to privately owned motor vehicles. Moreover, there was no justification that a board meeting was attended by the Board Member on the date of the receipt subject of reimbursement.

c. In addition to the reimbursements mentioned above, food expenses

during Board and Committee Meetings at the MWSS were incurred in the amount of P105,410.36.

9.4 Further review of the documents revealed that in some cases, the number of meals

served during Board Meetings costing P 53,371.50 exceeded the actual number of attendees based on the attendance sheets submitted by the Board Secretariat Office.

JEV No. Date of Meeting No. of

food orders

Paid Amount No. of actual attendees

02-000533 01/09/2013 10 2,310.00 7

01/10/2013 15 5,775.00 8

01/24/2013 15 6,600.00 8

02-000988 01/23/2013 10 770.00 7

01/18/2013 10 1,705.00 8

04-001300 03/01/2013 9 550.00 4

65

JEV No. Date of Meeting No. of

food orders

Paid Amount No. of actual attendees

07-002731 03/07/2013 10 4,600.00 8

03/14/2013 15 6,900.00 7

07-002841 05/06/2013 10 1,045.00 2

05/07/2013 12 698.50 3

05/09/2013 12 3,762.00 9

05/14/2013 8 1,628.00 3

05/30/2013 10 2,420.00 7

09-003667 07/03/2013 10 990.00 7

07/04/2013 10 2,497.00 6

07/11/2013 15 4,114.00 12

07/15/2013 10 627.00 No attendance Sheet submitted for the said

date.

07/23/2013 10 1,595.00 6

07/25/2013 12 4,785.00 10

Total 53,371.50

9.5 It was also noted in the review of the attendance sheets that some attendees have

no signatures and only a check () or “present” is indicated beside the names. There were no other documents that would show proof of attendance such as minutes of board meetings where the member attended or other relevant documents.

9.6 The above observations cast doubt on the validity of the expenses

reimbursed/incurred contrary to Section 12 of EO 242 and GCG Memorandum Circular No. 2012-2.

9.7 In COA Decision 2013-130 dated September 18, 2013, it was emphasized that

“While Official Receipts have been duly submitted; this Commission does not find the same sufficient to support the validity of the expenditures. The requirement of full documentation is to establish the propriety of the expenses in relation to the purpose for which the allowance is granted.”

9.8 We recommended and Management agreed to:

a. Require the concerned members of the Board of Trustees to justify

the reimbursements showing that the same were incurred in pursuance with Section 12 of EO 24 and/or GCG Memorandum Circular No. 2012-2 dated May 2, 2012;

b. Ensure that henceforth, expenses of members of the Board of

Trustees shall be supported with justification that the reimbursements were for the purpose of business meeting as provided in the above-mentioned regulations;

66

c. Strictly comply with COA Circular 96-004 which provides that under no circumstances should fuel be issued to privately owned motor vehicles;

d. Require the Board Secretariat to ensure that food expenses to be

incurred during Board Meetings are limited to those who are required/invited to attend and that attendance sheets are duly signed by the attendees or supported with relevant documents that would show proof of attendance in the meetings.

10. Discrepancies between the records of the Board Secretariat and the Finance

Department in the number of board meetings attended were noted, hence the accuracy of the amount of per diems paid to the BOT under account, Personnel Expenses - Honorarium, totalling P2.877 million was not established. 10.1 GCG Authorization Letter dated July 19, 2013 authorized MWSS to grant the FY

2012 PBI to the Appointive Members of its BOT in accordance with the entitlement scheme provided under Section 2 of GCG Memorandum Circular No. 2012-14. Based on the certification from the Corporate Secretary of total actual annual authorized per diems received, four members of the BOT were granted PBI equivalent to 90% of their total actual annual authorized per diems.

10.2 Review showed discrepancies on the number of board meetings attended and the

amount of per diems received by the BOT between the records of the Board Secretariat and the Finance Department, summarized as follows:

Name Board Designation

Total Number of Meetings Attended

Difference

Per Diems Received For CY 2012

Difference Per

Finance Record

Per Board Secretariat Report to GCG

Per Finance Record

Per Board Secretariat Report to GCG

Ramon B. Alikpala

Board Chairman

32 31 1 432,000 432,000 0

Gerardo A.I. Esquivel

Board Member(Ex Officio)

27 35 (8) 369,000 384,000 15,000

(refunded)

Emmanuel L. Caparas

Board Member

47 54 (7) 561,000 561,000 0

Benjamin J. Yambao

Board Member

47 53 (6) 561,000 561,000 0

Hermogenes Fernando

Board Member

29 27 2 357,000 Not

included NA

Ma. Cecilia Soriano

Board Member

43 50 (7) 471,000 Not

included NA

Jose Ramon Villarin, S.J.

Board Member

10 6 4 126,000 Not

included NA

67

10.3 Although the above differences did not result in any overpayment to the other Board Members, the noted discrepancies cast doubt on the correctness of the number of meetings attended and the amount of per diems paid.

10.4 The attendance report is a vital document in the computation of actual per diems

and the allowable Performance Based Incentive of the Board of Trustee by the GCG and should therefore be prepared with utmost care to ensure that an accurate report will be submitted.

10.5 We recommended and Management agreed to require the concerned Office

to exercise diligence in the reporting of data and that the same be validated with the Finance Department to get an accurate information.

11. Inconsistencies/differences in the signatures of the workers appearing in the Daily Attendance Sheet, the Payroll Sheet and in the Consolidated Report of Attendance were observed in the payment of salaries of the 162 workers for the Ipo Watershed reforestation program. 11.1 The disengagement of the Bantay Kalikasan from the Ipo Watershed management

activities had forced upon MWSS the obligation to manage and secure the 560 hectare plantation. Relative to the reforestation program, MWSS hired 162 workers, who are members of People’s Organization who previously reforested the area, on job order status. The payroll and the supporting documents were prepared and prepared/certified correct by the officers of the Organization and approved/noted by the concerned MWSS officers

11.2 Our audit of the payrolls for the period January to May 2013 disclosed the following deficiencies:

a. The signatures of nine workers in the Daily Attendance Sheet was in long handwriting while the one that appears in the Payroll sheet and Consolidated Report of Attendance was the printed name which anyone can write.

b. Some workers were allowed to affix their thumb marks on the Daily Attendance Sheets having no formal education. However, they were able to sign the payroll sheets and other documents as follows;

Marcelino Cruz affixed his thumb mark in the Daily Attendance Sheet

and Payroll Sheet but signed “MC” in the Consolidated Report of Attendance (from January to May 2013)

Romano Cruz signed RC in the Daily Attendance Sheet but affixed his

thumb mark in the Payroll sheet and Consolidated Report of Attendance (from January to May 2013)

Romeo Maalat signed Romeo in the Daily Attendance Sheet but affixed

his thumb mark in the Payroll sheet and Consolidated Report of Attendance for January 2013

68

Jimmy Cruz signed his given name “Jimmy” in the Payroll sheet and Consolidated Report of Attendance but affixed his thumb mark in the Daily Attendance Sheet (January, February & April 2013)

Rogelio Cruz, Jr. signed his given name “Rogelio” in the Daily

Attendance Sheet but affixed his thumb mark in the Consolidated Report of Attendance and Payroll sheet (From January to April 2013)

Rogelio S.J. Cruz signed in full in the Daily Attendance Sheet but affixed

his thumb mark in the Payroll sheet and Consolidated Report of Attendance (from January to May 2013)

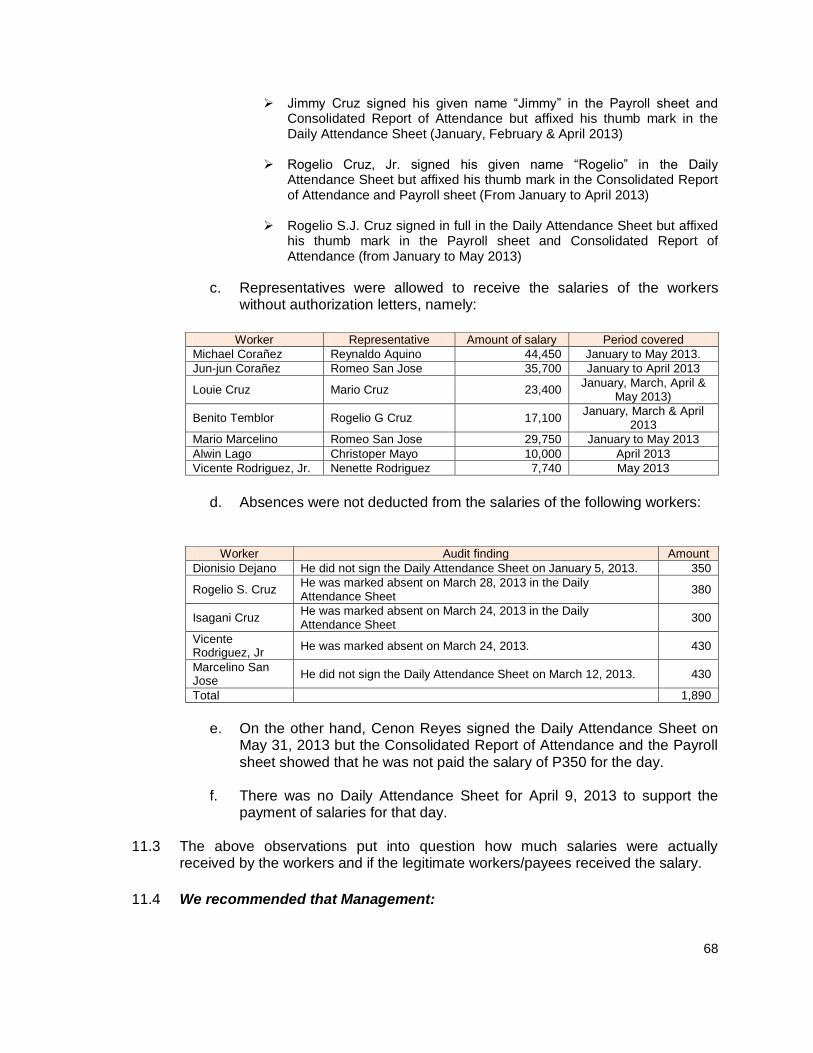

c. Representatives were allowed to receive the salaries of the workers without authorization letters, namely:

Worker Representative Amount of salary Period covered

Michael Corañez Reynaldo Aquino 44,450 January to May 2013.

Jun-jun Corañez Romeo San Jose 35,700 January to April 2013

Louie Cruz Mario Cruz 23,400 January, March, April &

May 2013)

Benito Temblor Rogelio G Cruz 17,100 January, March & April

2013

Mario Marcelino Romeo San Jose 29,750 January to May 2013

Alwin Lago Christoper Mayo 10,000 April 2013

Vicente Rodriguez, Jr. Nenette Rodriguez 7,740 May 2013

d. Absences were not deducted from the salaries of the following workers:

Worker Audit finding Amount

Dionisio Dejano He did not sign the Daily Attendance Sheet on January 5, 2013. 350

Rogelio S. Cruz He was marked absent on March 28, 2013 in the Daily Attendance Sheet

380

Isagani Cruz He was marked absent on March 24, 2013 in the Daily Attendance Sheet

300

Vicente Rodriguez, Jr

He was marked absent on March 24, 2013. 430

Marcelino San Jose

He did not sign the Daily Attendance Sheet on March 12, 2013. 430

Total 1,890

e. On the other hand, Cenon Reyes signed the Daily Attendance Sheet on

May 31, 2013 but the Consolidated Report of Attendance and the Payroll sheet showed that he was not paid the salary of P350 for the day.

f. There was no Daily Attendance Sheet for April 9, 2013 to support the

payment of salaries for that day.

11.3 The above observations put into question how much salaries were actually received by the workers and if the legitimate workers/payees received the salary.

11.4 We recommended that Management:

69

a. Submit conclusive proof that the amounts disbursed were received by the legitimate workers/payees; and

b. Require the persons who certified as to the correctness of the daily

attendance sheet and the payroll to be held liable for the overpayment of salaries to workers who were absent on the dates mentioned in paragraph 11.2 (d).

11.5 In reply, Management submitted the Identification Cards of the 118 out of the 164

Ipo Workers and informed that the other 46 workers were confirmed by the Foresters. Refunds in the total amount of P1,890 were made on May 7, 2014 for

the absences of workers not deducted from their salaries.

11.6 As a rejoinder, the Identification Cards of the Ipo workers were not complete and some did not bear the signatures of the workers. Further, the confirmation by the foresters of the receipt of the 46 workers of the salaries was not acceptable in audit. Thus, there was no conclusive proof that the amount disbursed was actually received by the legitimate workers/payees.

12. MWSS CO did not comply with the submission of Contracts/Purchase Orders/Letter Orders (PO/LO) and its supporting documents required under Section 3.1.1 of COA Circular No. 2009-001, thus, no timely review of contracts was undertaken by the Auditor. 12.1 COA Circular No. 2009-001 dated February 12, 2009 covering all contracts,

purchase orders and the like entered into by any government agency irrespective of amount involved, states:

“Within five (5) working days from the execution of a contact by the government or any of its subdivisions, agencies or instrumentalities, including government owned and controlled corporations and their subsidiaries, a copy of said contracts and each of all the documents shall be furnished to the Auditor concerned.”

12.2 We requested Management, in our letter dated August 3, 2012, to submit all

Contracts/Purchase/Letter Orders within five days from perfection thereof. However, it was observed that to date, the required submission had not been complied with.

12.3 We recommended and Management agreed that, henceforth, all contracts

and Purchase/Letter Orders and its supporting documents will be submitted in compliance with COA Circular 2009-001.

13. Disclosure in the Notes to Financial Statements on the detailed breakdown of input VAT taxes claimed during the year required under BIR Revenue Regulation No. 15-2010 was not complied with. Moreover, the accuracy of the Other Prepaid Expense – Input VAT account balance of P383,771 was not established due to:

70

a. discrepancy of P1.941 million between the total debits (Actual Input VAT) during the year and the Input VAT Summary list of Purchases/BIR return submitted to BIR; and

b. non-indication of the carryover balance of input VAT of P2.011 million in

the 1st Quarterly VAT return for CY 2013, hence it appearing that there were no prepaid tax credits.

13.1 Our audit revealed deficiencies in the required disclosure relative to input VAT taxes and accuracy of the Account Other Prepaid Expense – Input VAT, as follows:

13.1.1 There was no detailed breakdown on the Input VAT tax and

withholding taxes paid during the year as required under BIR RR 15-2010.

a. Revenue Regulation No. 15-2010 which amends Section 2 of RR

21-2002 is quoted hereunder:

“xxx the Notes to Financial Statements shall include information on taxes, duties and license fees paid or accrued during the taxable year, particularly the following:

1. The amount of VAT output tax declared during the year xxx;

2. The amount on VAT input taxes claimed broken

down into:

a. Beginning of the year; b. Current year’s domestic

purchases/payments xxx c. Claims for tax credit/refund and other

adjustments; and d. Balance at the end of the year.”

b. Review of the Notes to Financial Statements showed that the

Report on Supplementary Information Required under Revenue Regulation No. 15-2010 showed only the taxes and withholding taxes paid during the year. There was no detailed breakdown on the Input VAT tax and withholding taxes paid during the year as required under BIR RR 15-2010.

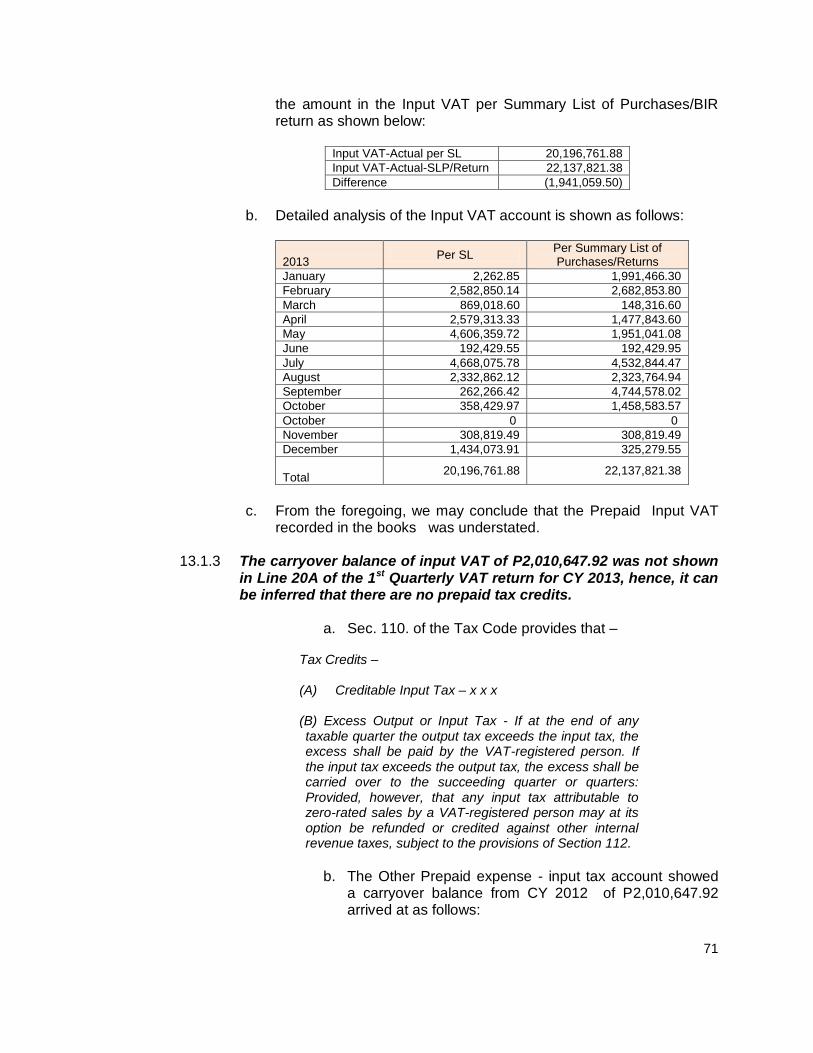

13.1.2 Discrepancy of P1,941,059.50 between the total debits (Actual Input

VAT) during the year and the Input VAT Summary list of Purchases/BIR return submitted to BIR

a. Analysis of the Other Prepaid Expense – Input VAT account

revealed that the total debits (Actual Input VAT) does not tally with

71

the amount in the Input VAT per Summary List of Purchases/BIR return as shown below:

Input VAT-Actual per SL 20,196,761.88

Input VAT-Actual-SLP/Return 22,137,821.38

Difference (1,941,059.50)

b. Detailed analysis of the Input VAT account is shown as follows:

2013 Per SL

Per Summary List of Purchases/Returns

January 2,262.85 1,991,466.30

February 2,582,850.14 2,682,853.80

March 869,018.60 148,316.60

April 2,579,313.33 1,477,843.60

May 4,606,359.72 1,951,041.08

June 192,429.55 192,429.95

July 4,668,075.78 4,532,844.47

August 2,332,862.12 2,323,764.94

September 262,266.42 4,744,578.02

October 358,429.97 1,458,583.57

October 0 0

November 308,819.49 308,819.49

December 1,434,073.91 325,279.55

Total

20,196,761.88 22,137,821.38

c. From the foregoing, we may conclude that the Prepaid Input VAT

recorded in the books was understated.

13.1.3 The carryover balance of input VAT of P2,010,647.92 was not shown in Line 20A of the 1st Quarterly VAT return for CY 2013, hence, it can be inferred that there are no prepaid tax credits.

a. Sec. 110. of the Tax Code provides that –

Tax Credits – (A) Creditable Input Tax – x x x (B) Excess Output or Input Tax - If at the end of any taxable quarter the output tax exceeds the input tax, the excess shall be paid by the VAT-registered person. If the input tax exceeds the output tax, the excess shall be carried over to the succeeding quarter or quarters: Provided, however, that any input tax attributable to zero-rated sales by a VAT-registered person may at its option be refunded or credited against other internal revenue taxes, subject to the provisions of Section 112.

b. The Other Prepaid expense - input tax account showed

a carryover balance from CY 2012 of P2,010,647.92 arrived at as follows:

72

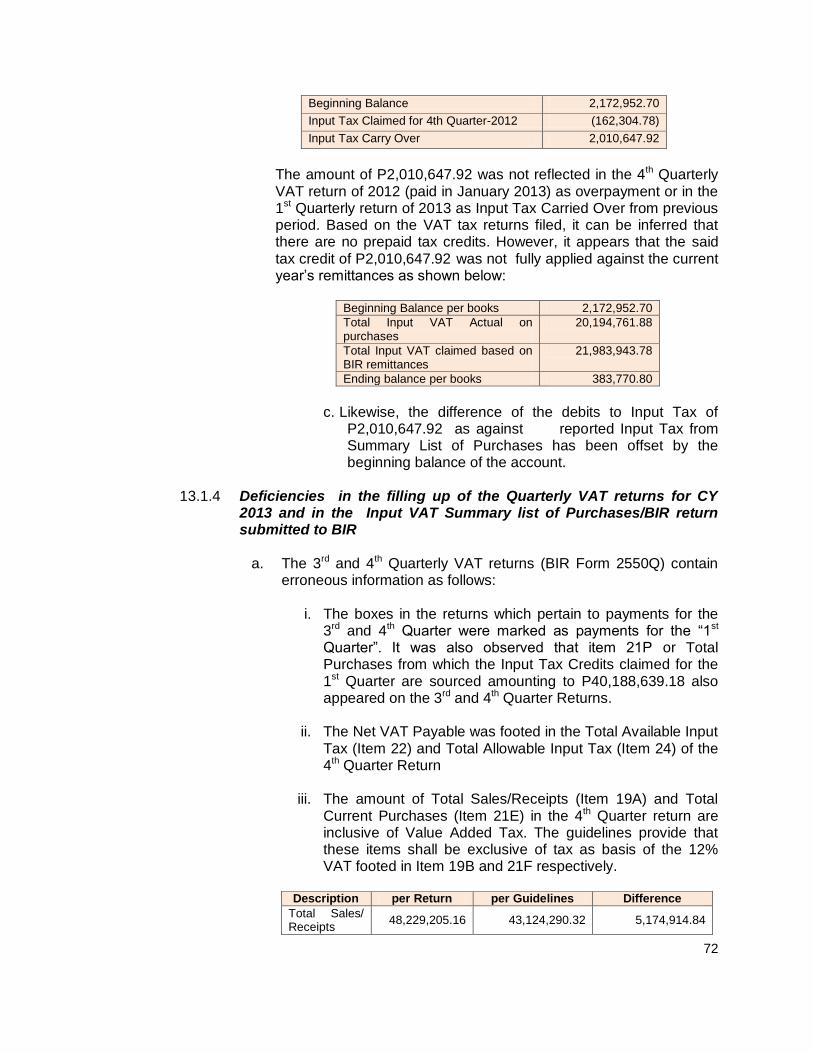

Beginning Balance 2,172,952.70

Input Tax Claimed for 4th Quarter-2012 (162,304.78)

Input Tax Carry Over 2,010,647.92

The amount of P2,010,647.92 was not reflected in the 4th Quarterly VAT return of 2012 (paid in January 2013) as overpayment or in the 1st Quarterly return of 2013 as Input Tax Carried Over from previous period. Based on the VAT tax returns filed, it can be inferred that there are no prepaid tax credits. However, it appears that the said tax credit of P2,010,647.92 was not fully applied against the current year’s remittances as shown below:

Beginning Balance per books 2,172,952.70

Total Input VAT Actual on purchases

20,194,761.88

Total Input VAT claimed based on BIR remittances

21,983,943.78

Ending balance per books 383,770.80

c. Likewise, the difference of the debits to Input Tax of

P2,010,647.92 as against reported Input Tax from Summary List of Purchases has been offset by the beginning balance of the account.

13.1.4 Deficiencies in the filling up of the Quarterly VAT returns for CY

2013 and in the Input VAT Summary list of Purchases/BIR return submitted to BIR

a. The 3rd and 4th Quarterly VAT returns (BIR Form 2550Q) contain

erroneous information as follows:

i. The boxes in the returns which pertain to payments for the 3rd and 4th Quarter were marked as payments for the “1st Quarter”. It was also observed that item 21P or Total Purchases from which the Input Tax Credits claimed for the 1st Quarter are sourced amounting to P40,188,639.18 also appeared on the 3rd and 4th Quarter Returns.

ii. The Net VAT Payable was footed in the Total Available Input

Tax (Item 22) and Total Allowable Input Tax (Item 24) of the 4th Quarter Return

iii. The amount of Total Sales/Receipts (Item 19A) and Total

Current Purchases (Item 21E) in the 4th Quarter return are inclusive of Value Added Tax. The guidelines provide that these items shall be exclusive of tax as basis of the 12% VAT footed in Item 19B and 21F respectively.

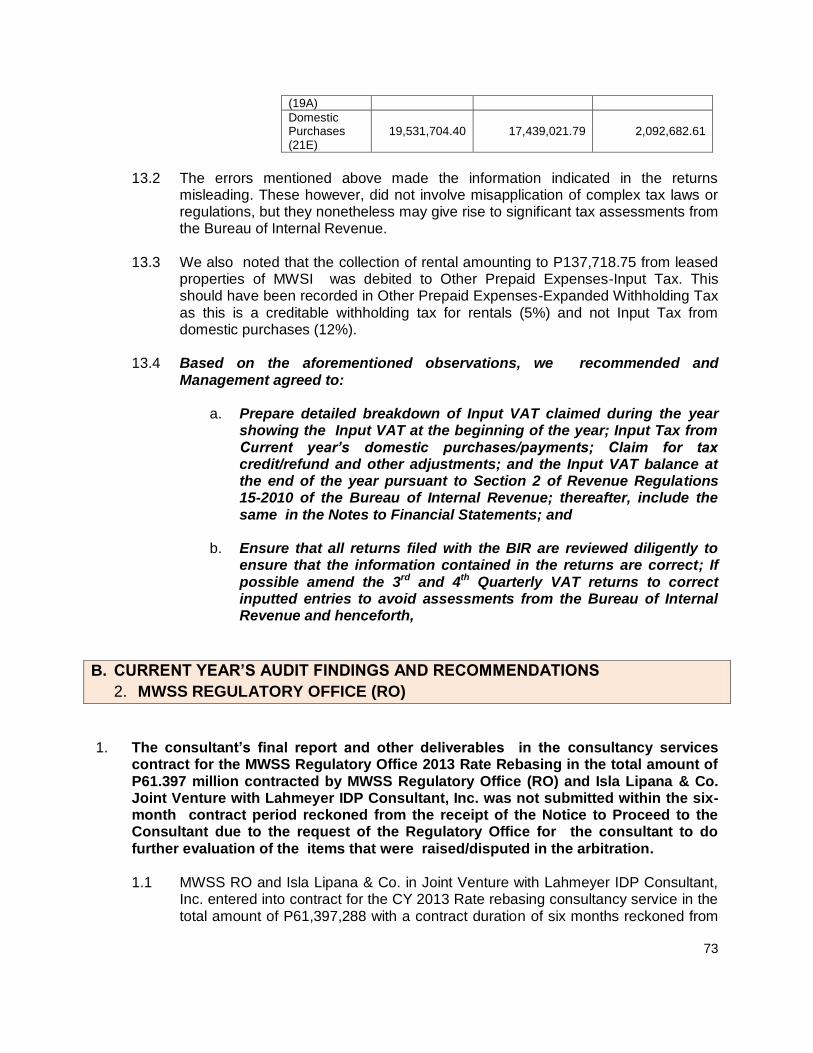

Description per Return per Guidelines Difference

Total Sales/ Receipts

48,229,205.16 43,124,290.32 5,174,914.84

73

(19A)

Domestic Purchases (21E)

19,531,704.40 17,439,021.79 2,092,682.61

13.2 The errors mentioned above made the information indicated in the returns misleading. These however, did not involve misapplication of complex tax laws or regulations, but they nonetheless may give rise to significant tax assessments from the Bureau of Internal Revenue.

13.3 We also noted that the collection of rental amounting to P137,718.75 from leased

properties of MWSI was debited to Other Prepaid Expenses-Input Tax. This should have been recorded in Other Prepaid Expenses-Expanded Withholding Tax as this is a creditable withholding tax for rentals (5%) and not Input Tax from domestic purchases (12%).

13.4 Based on the aforementioned observations, we recommended and

Management agreed to:

a. Prepare detailed breakdown of Input VAT claimed during the year showing the Input VAT at the beginning of the year; Input Tax from Current year’s domestic purchases/payments; Claim for tax credit/refund and other adjustments; and the Input VAT balance at the end of the year pursuant to Section 2 of Revenue Regulations 15-2010 of the Bureau of Internal Revenue; thereafter, include the same in the Notes to Financial Statements; and

b. Ensure that all returns filed with the BIR are reviewed diligently to ensure that the information contained in the returns are correct; If possible amend the 3rd and 4th Quarterly VAT returns to correct inputted entries to avoid assessments from the Bureau of Internal Revenue and henceforth,

B. CURRENT YEAR’S AUDIT FINDINGS AND RECOMMENDATIONS

2. MWSS REGULATORY OFFICE (RO)

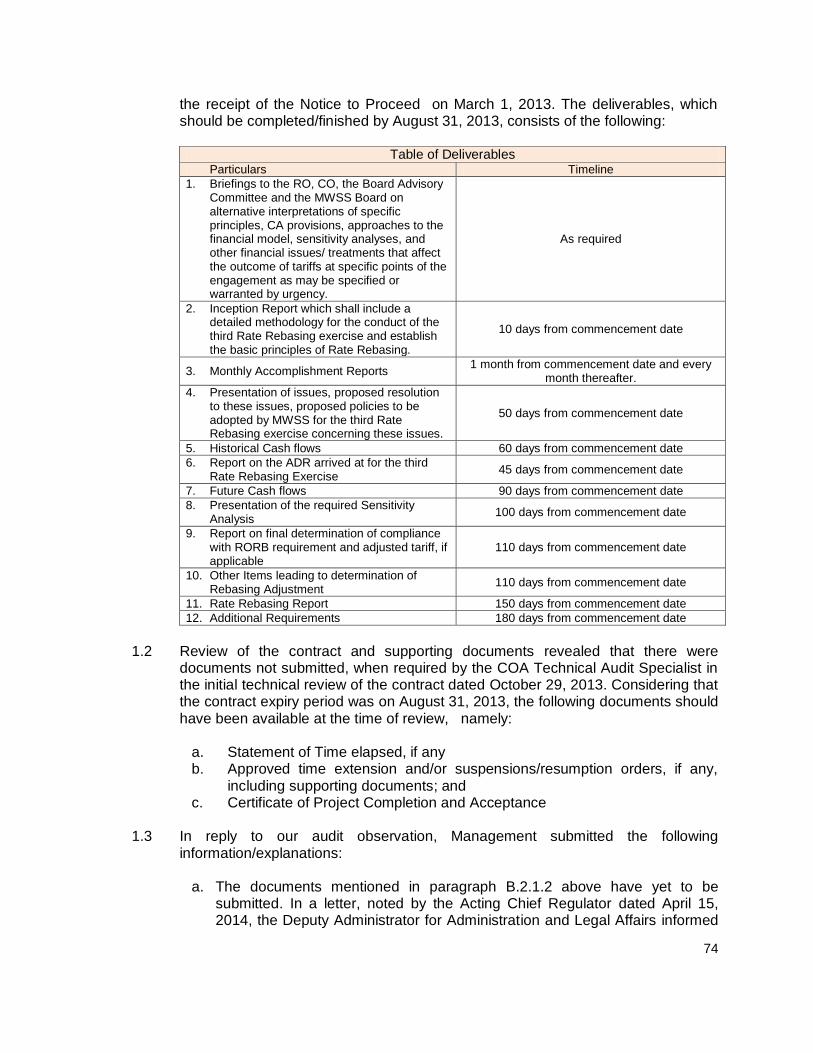

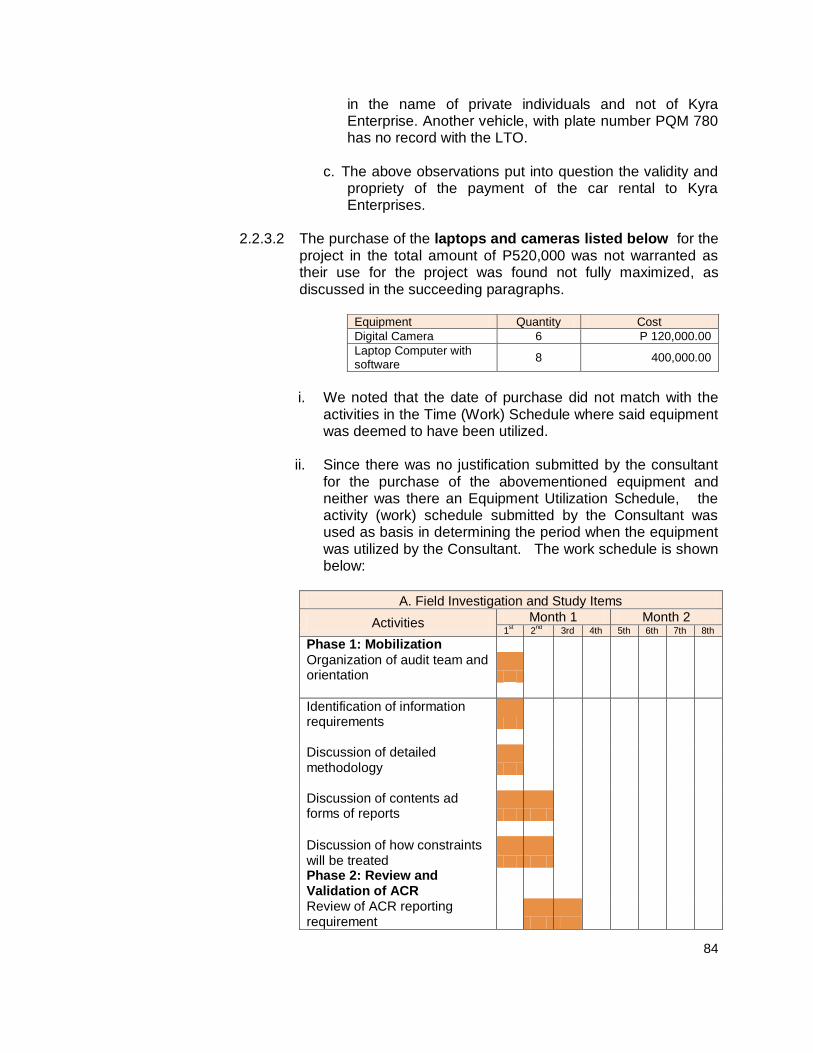

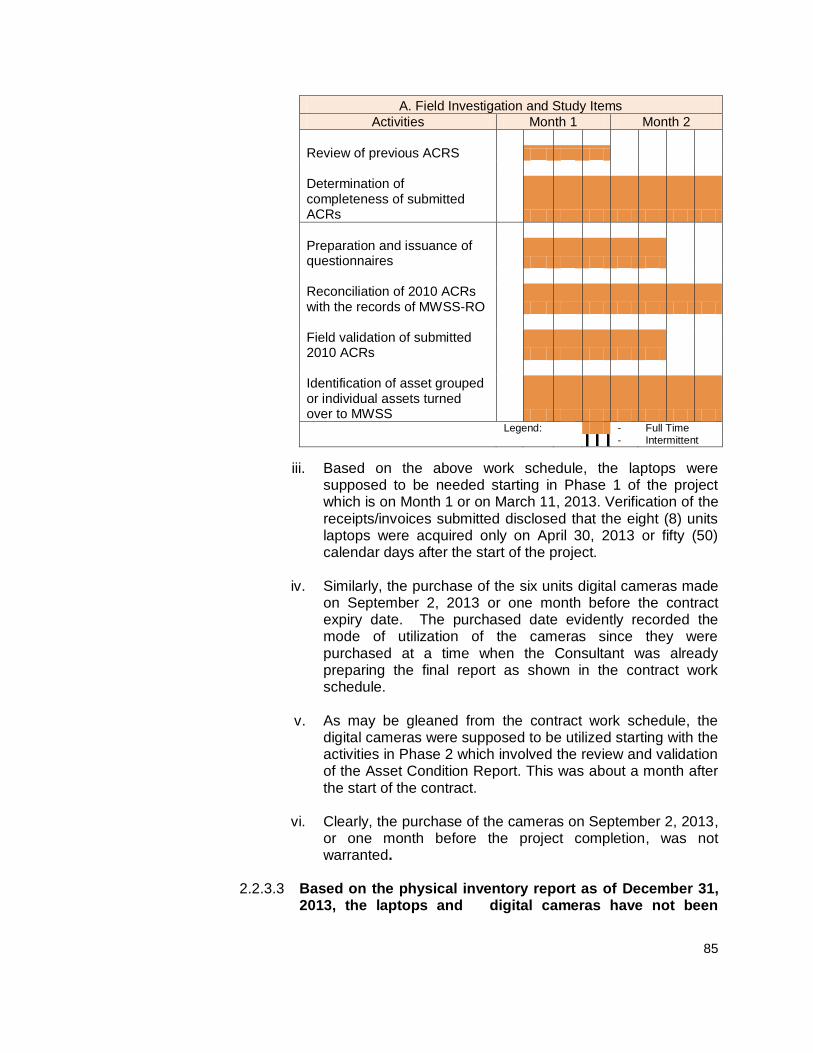

1. The consultant’s final report and other deliverables in the consultancy services