october 12, 2012 concepts in federal taxation chapter 6: business expense

TRANSCRIPT

October 12, 2012

CONCEPTS IN FEDERAL TAXATION

CHAPTER 6: BUSINESS EXPENSE

ADMINISTRATIVE

Homework and reading pushed back a week Next week’s homework is chapter 7

Midterm 2 and project due dates stay the same Midterm 2 will cover chapters 6-9

Midterm 1 will be handed back next week

HW ProblemsAssignment #7Chapter 6P30, 38, 47, 55

HOMEWORK PROBLEMS

For each of the following situations, explain whether a deduction should be allowed for entertainment expenses:

a. Gayle, a dentist, invites 50 of her best patients to her daughter’s wedding reception. The cost of the reception related to the presence of her patients is $5,000.

The wedding reception is not an ordinary and necessary expense of Gayle’s business (dentist)

The reception is a personally motivated event which lacks a business purpose

Gayle cannot deduct the $5,000 of entertainment expenses

#30

b. Stan is one of 5 shift supervisors responsible for 100 employees at Label House, Inc. He regularly meets with the other shift supervisors at the plant. In addition, Stan makes it a practice to go to lunch at least once a week with each of the other 4 shift supervisors in order to network. During the current year, Stan pays $1,500 for his and the other supervisors’ lunches. Stan’s job description does not require him to entertain the other supervisors.

Because Stan’s supervisory position is not aff ected by the entertainment (not required as part of his job), the lunches are not an ordinary and necessary expense of his job

The expenses related to Stan’s meals are personal expenses

Stan may not deduct the $1,500

#30

c. Jan is a real estate broker who holds an open house for a diff erent client each Sunday afternoon. During the open house, she provides cookies and soft drinks for whoever visits the house. Jan pays $2,000 for open house entertainment.

Advertising and promotional expenses are an ordinary and necessary expense of a real estate broker

The $2,000 Jan paid for refreshments at the open house is deductible

#30

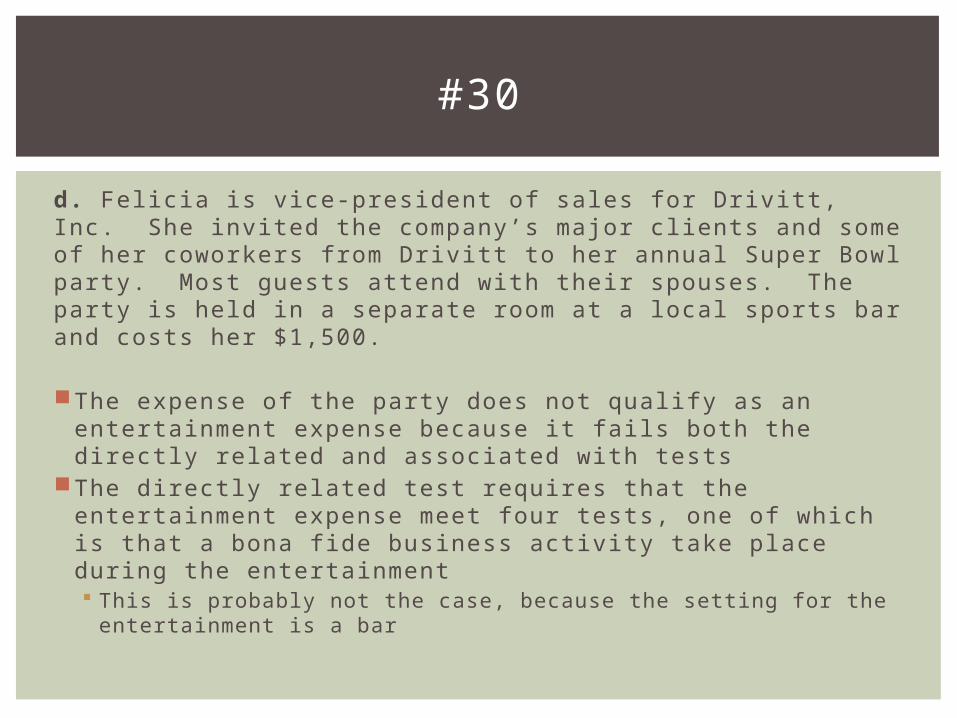

d. Felicia is vice-president of sales for Drivitt, Inc. She invited the company’s major clients and some of her coworkers from Drivitt to her annual Super Bowl party. Most guests attend with their spouses. The party is held in a separate room at a local sports bar and costs her $1,500.

The expense of the party does not qualify as an entertainment expense because it fails both the directly related and associated with tests

The directly related test requires that the entertainment expense meet four tests, one of which is that a bona fi de business activity take place during the entertainment This is probably not the case, because the setting for the

entertainment is a bar

#30

For the entertainment to qualify under the associated with test, two requirements must be met:1. There must exist a clear business purpose

Felicia could probably establish that this test is met

2. Entertainment must occur either preceding or following a substantial business discussion This did not occur The $1,500 entertainment expense is not deductible

#30

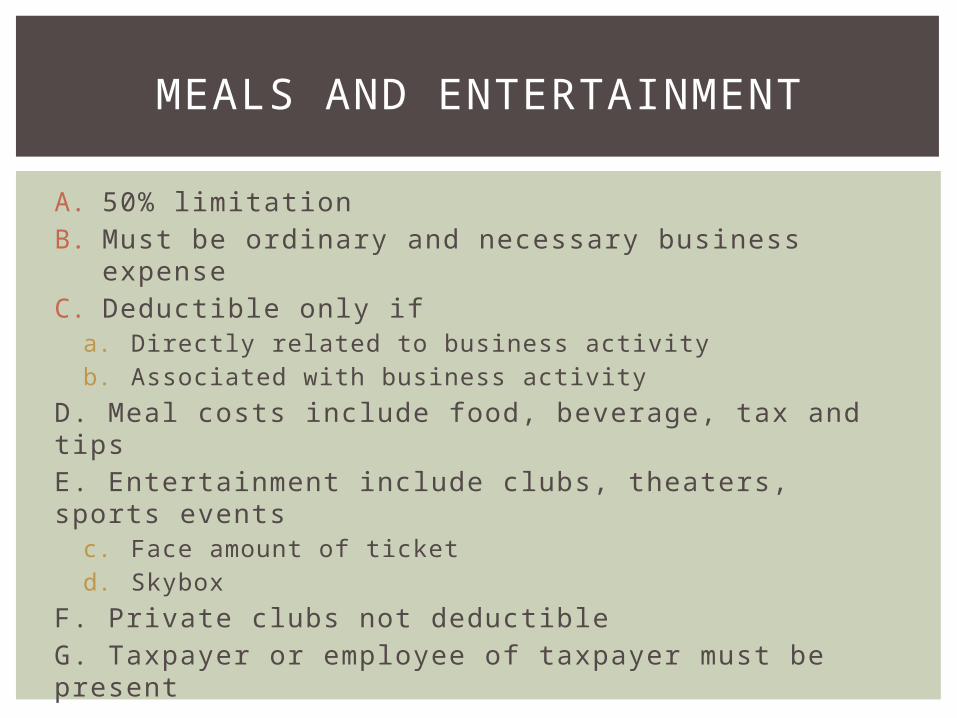

A. 50% limitationB. Must be ordinary and necessary business expenseC. Deductible only if

a. Directly related to business activityb. Associated with business activity

D. Meal costs include food, beverage, tax and tipsE. Entertainment include clubs, theaters, sports events

c. Face amount of ticketd. Skybox

F. Private clubs not deductibleG. Taxpayer or employee of taxpayer must be present

MEALS AND ENTERTAINMENT

H. Reciprocal entertainment not allowedI. Exceptions to 50% limitation

a. Expenses treated as compensationb. Expenses incurred for another person and receive

reimbursement from that person—accountable plan (the reimbursing person is subject to the 50% limit)

c. Recreational/social expenses to benefit employees (de minimis fringe benefit)

MEALS AND ENTERTAINMENT

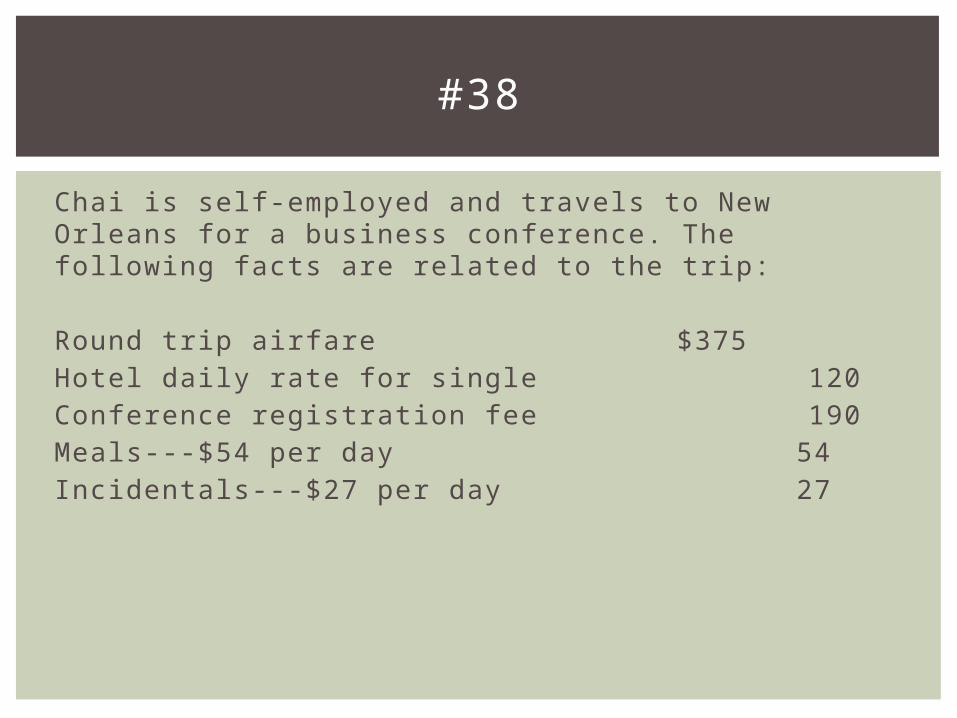

Chai is self-employed and travels to New Orleans for a business conference. The following facts are related to the trip: Round trip airfare $375Hotel daily rate for single

120Conference registration fee

190Meals---$54 per day

54Incidentals---$27 per day

27

#38

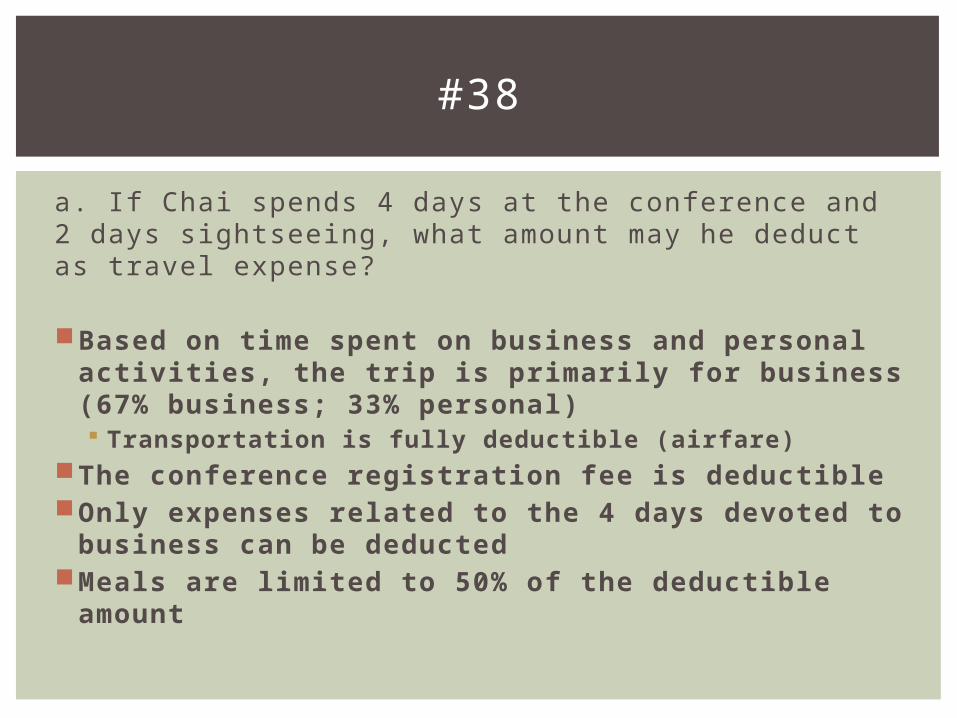

a. If Chai spends 4 days at the conference and 2 days sightseeing, what amount may he deduct as travel expense?

Based on time spent on business and personal activities, the trip is primarily for business (67% business; 33% personal) Transportation is fully deductible (airfare)

The conference registration fee is deductible Only expenses related to the 4 days devoted to

business can be deducted Meals are limited to 50% of the deductible

amount

#38

The expenses are deducted as follows: Airfare $ 375Hotel ($120 x 4) 480Conference registration 190Meals ($54 x 4 x 50%) 108Incidentals ($27 x 4) 108Total deduction $ 1,261

#38

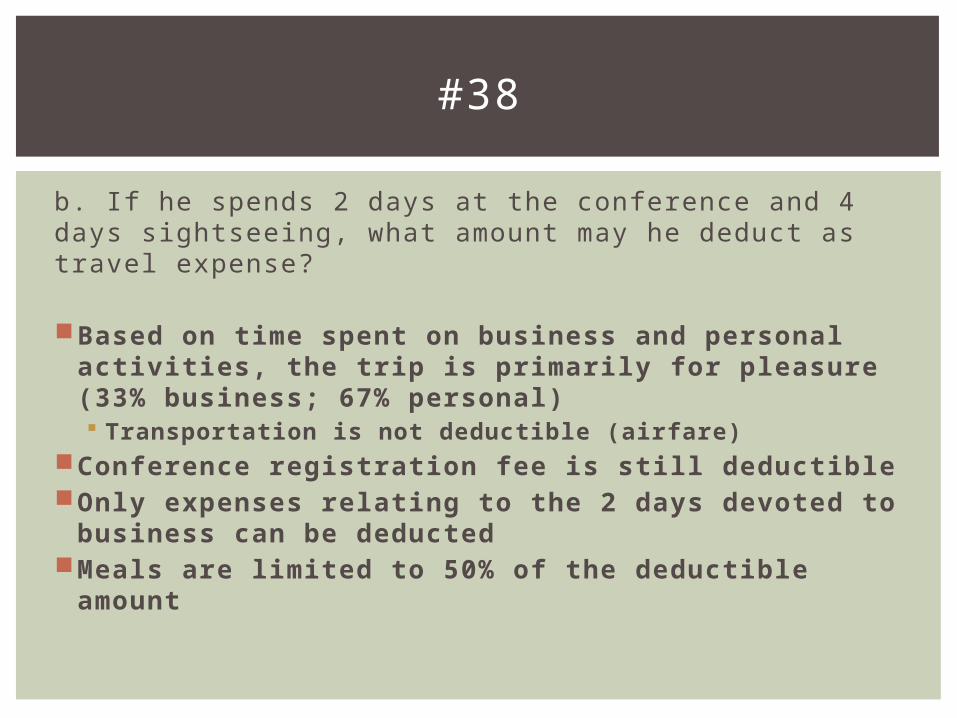

b. If he spends 2 days at the conference and 4 days sightseeing, what amount may he deduct as travel expense?

Based on time spent on business and personal activities, the trip is primarily for pleasure (33% business; 67% personal) Transportation is not deductible (airfare)

Conference registration fee is still deductibleOnly expenses relating to the 2 days devoted to

business can be deductedMeals are limited to 50% of the deductible

amount

#38

The expenses are deducted as follows: Airfare $ -0-Hotel ($120 x 2)

240Conference registration

190Meals ($54 x 2 x 50%)

54Incidentals ($27 x 2) 54Total deduction $ 538

#38

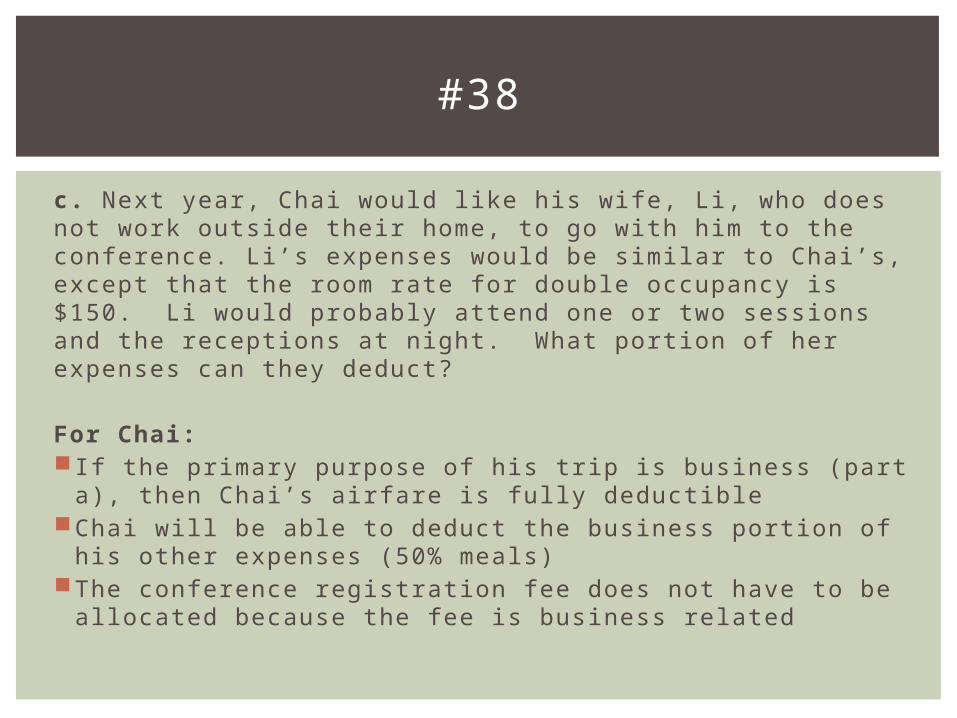

c. Next year, Chai would like his wife, Li, who does not work outside their home, to go with him to the conference. Li’s expenses would be similar to Chai’s, except that the room rate for double occupancy is $150. Li would probably attend one or two sessions and the receptions at night. What portion of her expenses can they deduct?

For Chai: If the primary purpose of his trip is business (part a),

then Chai’s airfare is fully deductibleChai will be able to deduct the business portion of his

other expenses (50% meals)The conference registration fee does not have to be

allocated because the fee is business related

#38

For Chai’s wife Li:No portion of Li’s expenses is deductibleSince the double occupancy rate is greater than the

single occupancy rate ($120 for single; $150 for double), Chai’s deductible portion for the hotel room is limited to the single occupancy rate ($120 per business night)

#38

Chai’s deductible amount would be the same as part a or part b depending on his business to personal activities ratio

#38

A. Deductible if away from home overnighta. Tax home is area of principal business, not residenceb. Overnight is substantially longer than a regular workday

B. More than 50% of the activity must have business purpose

a. Incidental business expenses deductibleb. Personal activity costs not deductible

C. Bona fide business purposea. Spouse cost not deductible, unless business purposeb. Not for investment related meetingsc. Not if the travel itself is educational

TRAVEL EXPENSES

Howard loaned $8,000 to Bud two years ago. The terms of the loan call for Bud to pay annual interest at 8%, with the principal amount due in three years. Until this year, Bud had been making the required interest payments. When Howard didn’t receive this year’s payment, he called Bud and found out that Bud had fi led for bankruptcy. Bud’s accountant estimated that only 40% of his debts would be paid after the bankruptcy proceeding. No payments were received. In the next year, Howard received $2,700 in full satisfaction of the debt under the bankruptcy proceeding. What deductions are allowed to Howard, assuming that the debt was:

#47

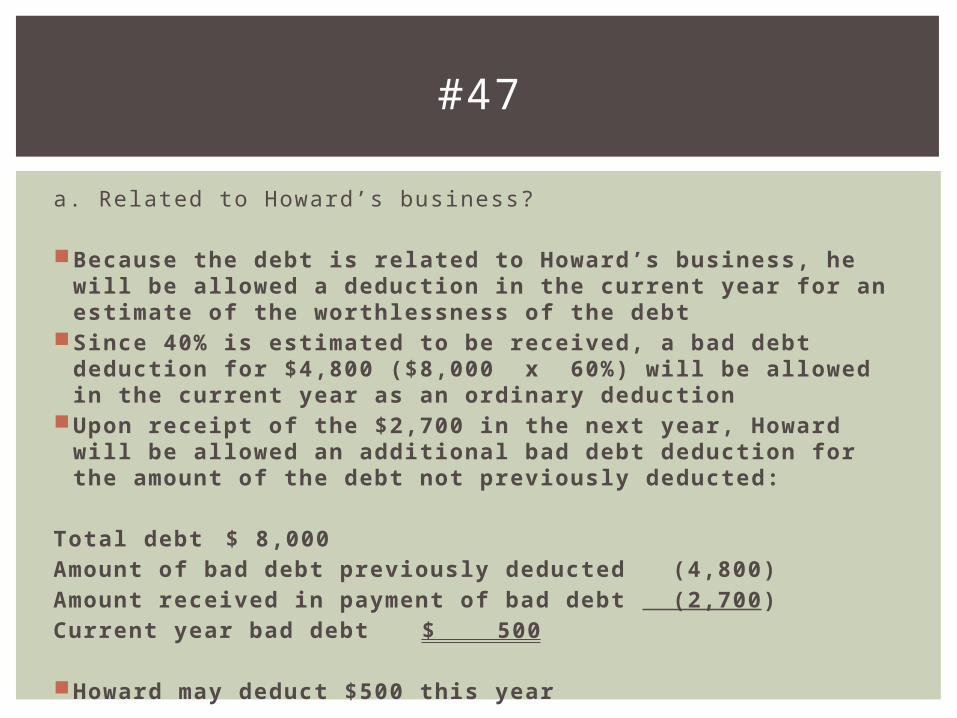

a. Related to Howard’s business?

Because the debt is related to Howard’s business, he will be allowed a deduction in the current year for an estimate of the worthlessness of the debt

Since 40% is estimated to be received, a bad debt deduction for $4,800 ($8,000 x 60%) will be allowed in the current year as an ordinary deduction

Upon receipt of the $2,700 in the next year, Howard will be allowed an additional bad debt deduction for the amount of the debt not previously deducted:

Total debt $ 8,000Amount of bad debt previously deducted (4,800)Amount received in payment of bad debt (2,700)Current year bad debt $ 500

Howard may deduct $500 this year

#47

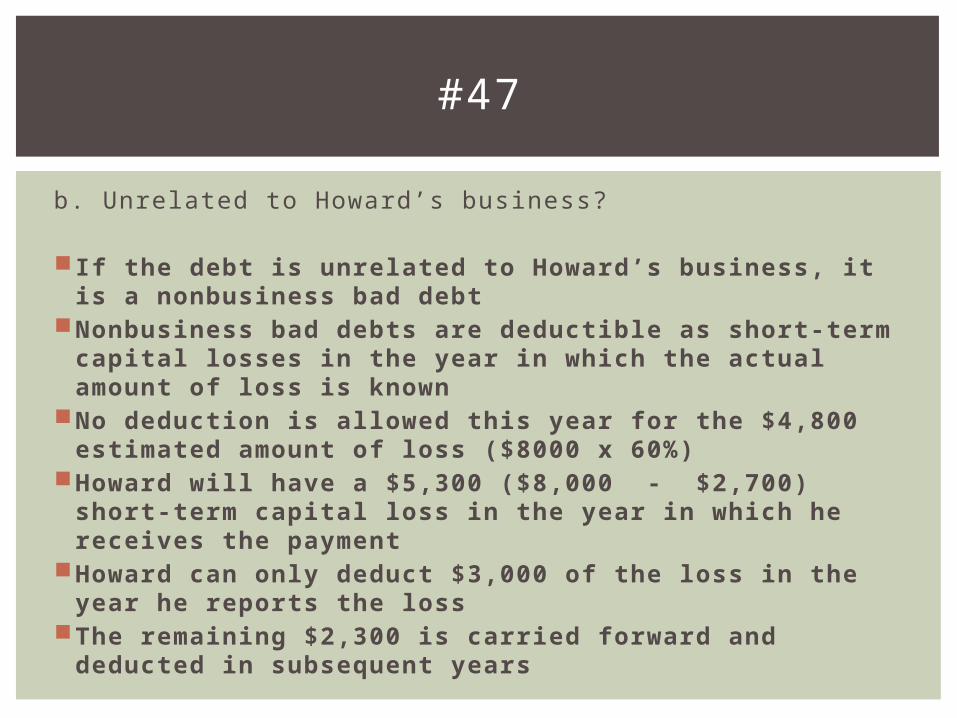

b. Unrelated to Howard’s business?

If the debt is unrelated to Howard’s business, it is a nonbusiness bad debt

Nonbusiness bad debts are deductible as short-term capital losses in the year in which the actual amount of loss is known

No deduction is allowed this year for the $4,800 estimated amount of loss ($8000 x 60%)

Howard will have a $5,300 ($8,000 - $2,700) short-term capital loss in the year in which he receives the payment

Howard can only deduct $3,000 of the loss in the year he reports the loss

The remaining $2,300 is carried forward and deducted in subsequent years

#47

Additional Considerations:If Howard has capital gains in the year he

reports the loss, he can off set part or all of the $5,300 loss against his capital gains Refer to netting procedure

#47

c. How would your answers to parts a and b change if Howard received $3,300 in satisfaction of the debt in the next year?

Part a (business bad debt): If Howard receives $3,300, he will have to include the tax

benefi t he received from the overstatement of the deduction in the previous year:

Total debt $ 8,000Amount of bad debt previously deducted (4,800)Amount received in payment of bad debt (3,300)Current year gross income $ (100)

Under the tax benefi t rule, the deduction that was taken in the previous year will be taxable income in the current year

#47

Part b (nonbusiness bad debt):Howard’s short-term capital loss deduction in

the year of receipt is $4,700 ($8,000 - $3,300) Only deduct $3,000 if no capital gains

Remember, Howard was not permitted to deduct estimated nonbusiness bad debt expenses

#47

A. Bad debts are generally deductible as capital recoveries

B. Business purpose bad debtsa. Limited to basisb. Specific charge-off method

C. Nonbusiness bad debtsa. Not deductible if voluntarily forgivenb. Not deductible if forgiveness is a giftc. Deductible if it’s a bona fide debt that becomes

uncollectiblea. Short term capital loss in year of total worthlessnessb. Annual capital loss limit is $3,000

D. Look at table 6-1

BAD DEBTS

State whether the following taxes are allowed as a current deduction for taxes paid by a business:

a. Sales tax on the purchase of a desk

Sales tax paid on the purchase of an asset is not currently deductible

The sales tax must be added to the basis of the asset and can be recovered through a depreciation deduction (discussed in chapter 10)

A sales tax imposed on a business for items benefi ting only the current tax year can be deducted in the current year (i.e. supplies, small tools, other consumable items)

#55

b. State and local income, real estate, and personal property taxes

State and local income, real estate, and ad valorem (based on value of property) personal property taxes are allowed as a deduction when paid or accrued based on the taxpayer’s accounting method

#55

c. Federal income, estate, and gift taxes

Federal income, estate, and gift taxes may not be deducted

#55

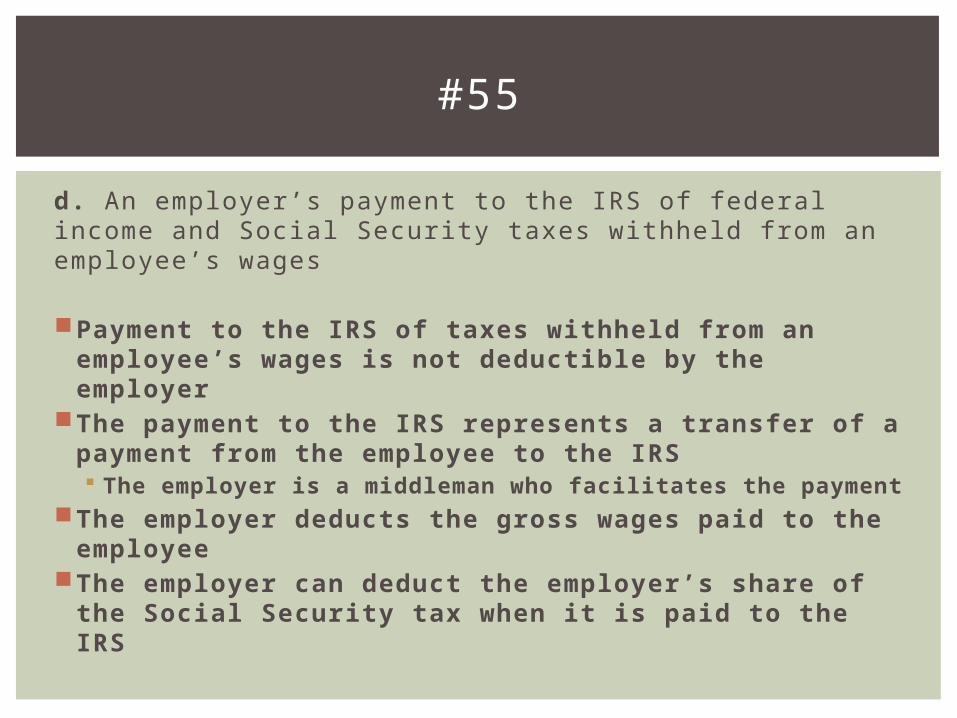

d. An employer’s payment to the IRS of federal income and Social Security taxes withheld from an employee’s wages

Payment to the IRS of taxes withheld from an employee’s wages is not deductible by the employer

The payment to the IRS represents a transfer of a payment from the employee to the IRS The employer is a middleman who facilitates the

paymentThe employer deducts the gross wages paid to

the employee The employer can deduct the employer’s share of

the Social Security tax when it is paid to the IRS

#55

A. Most business-related taxes are deductible except:a. Federal income tax, gift, and estate taxesb. Allowed as itemized deductions:

a. Real and personal property taxb. State, local, and foreign income taxes

B. Sales tax deductible when not paid as a capital expenditure

a. Capitalized when related to purchase of capital assetb. Deducted by capital recovery (depreciation)

C. Real estate tax is allocated between buyer and seller by days owned

D. Assessment for local benefitsa. Sidewalks, streets, etc.b. Tax added to property’s basis

TAXES

For each of the following IRA situations, determine the amount the taxpayer can deduct. Discuss any limitations, which might be placed, on the deduction:

a. Marissa is single and is an active participant in a qualifi ed employee pension plan. Determine the maximum Roth IRA contribution that she can make if her adjusted gross income for the year is $71,000.

If Marissa did not make contributions to other IRA accounts during the year, she is allowed to make a $5,000 contribution to a Roth IRA

Marissa does not receive a deduction for the contribution If Marissa's AGI exceeds $110,000, the amount that can she can

contribute to a Roth IRA is phased out ratably until no contribution is allowed when her adjusted gross income equals $125,000

SPRING 2012 MIDTERM – Q2

b. David and Donna are married and fi le a joint return. Each is covered by an employee-sponsored pension plan, and their adjusted gross income is $100,000. Determine their maximum IRA contribution and deduction for the current year.

They can both contribute $5,000 to IRA accounts Since both are covered by employer-sponsored pension plans,

the amount of the IRA deduction is reduced when their AGI reaches $92,000

The deduction is fully phased out when AGI exceeds $112,000 The maximum contribution amount is not aff ected by this

limitation, only the deductible amount of the contribution The $10,000 deduction must be reduced by 40% [($100,000 -

$92,000) / $20,000] This leaves an allowable deduction for AGI of $6,000 [$10,000

- ($10,000 * 40%)]

SPRING 2012 MIDTERM – Q2

A. Contribution alloweda. $5,000 of earned income per taxpayerb. $6,000 if 50 or older

B. Deduction alloweda. All if single or neither spouse covered by employer

pension planb. Limited if eligible for employer plan

C. Phase outsD. Distributions are taxable after capital recovery of

any non-deductible contributions

CONVENTIONAL IRAS

A. Nondeductible contributionsB. Nontaxable distributionsC. No restrictions for participation in employer pension

planD. Maximum contribution limited to $5,000 to all IRAs

in combination ($6,000 if 50 or older)a. Reduced for contributions made to conventional IRAsb. Phase out

ROTH IRAS