official publication of the minnesota association of

TRANSCRIPT

EQUAL EYESOFFICIAL PUBLICATION OF THE MINNESOTA ASSOCIATION OF ASSESSING OFFICERS MNMAAO.ORG

FALL 2020VOLUME 42 NUMBER 162

Covid 19 in theAssessment World

Top 10: Etiquette for a Successful Virtual Meeting Fall ConFerenCe HigHligHts

2 FALL 2020 / Equal Eyes

A

Executive OfficersPresident Daryl Moeller, SAMA1st Vice President Patrick Chapman, SAMA2nd Vice President Joe Udermann, SAMAFinancial Officer Kyle Holmes, SAMAPast President Michelle Moen, SAMA

Regional DirectorsRegion 1 Ryan DeCook, SAMARegion 2 Mike Sheplee, SAMARegion 3 Jean Sowada-Popp, SAMARegion 4 Mike Dangers, SAMARegion 5 David Parsons, SAMARegion 6 Doug Bruns, SAMARegion 7 Chris Odden, SAMARegion 8 Mary Jo Otten, SAMARegion 9 Michele Gelo, AMA

Committee ChairsAgricultural Mark Koehn, CMACAMA and GIS Randy Lahr, SAMAConference Coordinator Paul Knutson, SAMA, RESEditorial Information Systems Michael Neimeyer, CMALegislative Mark Peterson, SAMAMembership Coordinator Rebecca Malmquist, SAMA, RESNominating and Procedures Michelle Snobl, AMAResidential John Conway, SAMARules and Resolutions Daryl Moeller, SAMASales Ratio Dell Sanko, CMAScholarship Carrie Borgheiinck, SAMASecretary Penny Vikre, SAMASilent Auction Lorna Sandvik, SAMASite Selection Lisa Clarke, CMAStrategic Planning Nancy Wojcik, SAMASummer Seminar Coordinator Kim Jensen, SAMA, CAETax Court / Valuations Ann Miller, SAMA Treasurer Reed Heidelberger, SAMA

Educational WorkgroupsAssessor Development Patrick Chapman, SAMACourse Management Tina Diedrich-Von Eschen, SAMACourse Curriculum & Standards Sherri Kitchenmaster/Jessi Glancey, SAMA

Education Coordinator/Online Admin. Emily Squyres

Lori Thingvold, SAMAWright CountyManaging Editor

Amber Hill, SAMAPolk County

Jake Pidde, AMAStearns County

Jamie Freeman, SAMAClearwater County

Nancy Gunderson SAMAClay County

EDITORIALCOMMITTEE

Jason Jorgensen, SAMA

Jason Jorgensen, SAMAWadena County Associate EditorCommittee Chair

Mike Bjork, AMAWashington County

Questions, comments or suggestions? Please email

Missy Manke Wright County

Holly Soderbeck, SAMAMN Dept of Revenue

MAAOLEADERSHIP

FALL 2020 / Equal Eyes 3

IN EVERY ISSUE

* The statements made or opinions expressed by authors in Equal Eyes do not necessarily represent a policy position of the Minnesota Association of Assessing Officers.

Commissioner’s Comments Presidential Perspective MAAP Update Top 10 Classifieds What You Get For Out of the Past Transitions Tax Court SBA Minutes 41

Sponsored By: 456

18212227283141

8covid 19 in the assessment

world

Where Am I?answer on back cover

4 FALL 2020 / Equal Eyes

Commissioner’s Comments

By Cynthia Bauerly MN Revenue Commissioner

A Partnership That Works - Good Times or Bad • Completing and enhancing PRISM (Property Record Information System of Minnesota)

Cynthia’s successor, Sarah Bronson, brings a legal background and strong focus on customer service and relationships to the job of assistant commissioner. She joined Revenue in 2017 as the Taxpayer Rights Advocate, advising agency leadership to create policies and procedures that address the needs of taxpayers.Before joining the department, Sarah spent eight years as director of the Mid-Minnesota Legal Aid Low Income Taxpayer Clinic, providing no-cost legal representations to taxpayers with limited incomes. She earned a Bachelor of Science degree from University of Wisconsin-Madison and a J.D. from the University of Minnesota Law School.Finally, I want to thank you for welcoming me and working with me as revenue commissioner over the last six years. I have enjoyed meeting many of you and working with MAAO on important property tax issues. Your work plays a crucial role in our property tax system, helping fund services our people and businesses rely on, in good times and in bad. This year has brought unprecedented challenges to state and local governments. It has been a privilege to witness how MAAO and Revenue have risen to the occasion.My last day is October 9. Deputy Commissioner Lee Ho will lead the department until the governor names a replacement for me later this year.I know all of you will continue to work hard and do great things on behalf of the Minnesotans we serve. Thank you – again – for your partnership!

Cynthia Bauerly is the commissioner of the Minnesota Department of Revenue.

Due to COVID-19 – among other things – 2020 continues to be an eventful year for property tax administrators, along with the Minnesotans we serve. We’ve had to juggle a range of issues at home and at work which, for most of us, have occupied the same physical space for the last several months.On behalf of the Department of Revenue, thank you for being flexible, patient, and steadfast as we worked through these issues together. We appreciate your hard work and dedication to doing your jobs while keeping yourselves, your families, and your customers safe.

Legislative SessionAt Revenue, we’re preparing for next year’s legislative session. As usual, we expect property taxes will figure into the Capitol discussion. We look forward to working with MAAO on our common concerns and issues such as simplifying the classification system and assuring uniform property assessments across Minnesota.MAAO and the department agree that a simpler, flatter classification system offers many advantages. Having fewer classes and tiers would make our system more understandable to taxpayers while reducing the administrative load (and costs) for counties.For example, one of Revenue’s proposals for 2021 changes the 1b classification rate for homeowners who are blind or disabled to a value exclusion. This change provides the same benefit, or slightly more, for those who qualify for the existing program. And it simplifies how you calculate and report tax information for these properties, especially those valued over $50,000.Another department proposal updates state law to better meet the current education needs of Accredited Minnesota Assessors (AMAs) and Senior Accredited Minnesota Assessors (SAMAs). It requires 30 hours of education on property tax laws each four-

year licensing cycle, as before, but allows more flexibility.The department could provide a wider range of topics than we do now in the PACE course (Professional Assessment Certification and Education). And assessors could use other seminars – such as State Assessed Property forums – and webinars or virtual learning to meet the requirement. This update will help us provide more diverse, timely, and relevant education for assessors. It also aligns state law with the recently updated Minnesota State Board of Assessors training requirements.Each session, the department works with MAAO, other partners, legislators, and the governor to help ensure any tax law changes can be implemented as effectively as possible. Please let us know if you have ideas to improve our state property tax system, and bring us into your discussions early so we can help.

TransitionsThe Revenue-MAAO partnership is built on many relationships between our organizations, even as the faces may change over time. That is happening now, due to the recent retirement of Assistant Commissioner Cynthia Rowley and my own departure.Cynthia retired in September after 18 years with the department. Many of you know her from her stint as Property Tax director from 2016 to 2018. In both roles, she focused on building relationships with property tax officials and other customers. She also oversaw efforts to improve our service to counties and the systems we use to store and share property tax information. Examples include:• Creating the annual Property Tax Services Report, based on listening sessions with local officials

• Improving eCRV to be more customer-friendly and forming the eCRV User Group

FALL 2020 / Equal Eyes 5

president’s perspective

it is going to be. Every day I wake up, I think this is going to be the best day ever. Whether we are in the office or still working from home, we can always make each day the best it can be. Having a positive attitude in life, will allow you to appreciate the little things in it and make them more special. If we can spread more positivity to our coworkers and the public we work with, the better our days will be. It is hard to believe the changes that we have witnessed in the last couple of months or since the last time I wrote my article for Equal Eyes. Keeping a positive outlook, will get us through this pandemic.

Many areas of Minnesota are struggling with the COVID-19 pandemic, a timeframe we have never seen before and hopefully we will never see again, when it ends. Some of us have struggled with the virus personally or probably know someone that has either had it or worse died from it, I do. We have all struggled with it in our professional lives. Some offices are working at full capacity and running business as usual, with extra precautions put in place. While others are working from home as their offices are still closed to the public. Most of us are probably somewhere in the middle. This pandemic has definitely changed our ways of doing business. From going and looking at properties, accepting applications and the computers that we have worked on for years are all changing. Changes that will influence operating the assessor’s office for years to come.

Since my last article, we have started to offer classes again. Prior to COVID-19 classes had been scheduled at locations that were big enough to fit our needs, but many are no longer safe locations Our first class to be offered was ALP.

This class was our first class held at The Park Event Center in Waite Park. This new facility was able to accommodate our needs with plenty of room to be COVID-19 safe. We also used the new Hilton Garden Inn attached to the Conference Center for room reservations. Both locations were welcoming and appreciative for the opportunity to serve us. We have also hosted Assessment Administration and the joint Legislative and Executive Board meeting at these locations. Hopefully we can continue to use their facilities in the future. We also had a successful Principles class at the Kelly Inn, St. Cloud and IAAO 102 at the Holiday Inn in Lake Elmo. For those who like to take classes in person, we are focusing on having locations that promote the guidelines for COVID, so our locations will be limited on where we can have these classes. Please watch our website as classes are being added or locations may change.

I understand people may not feel comfortable taking classes in person. And some have asked why we are still having classes in person. The answer is, the way our classes are being taught right now, is with the large classroom setting, and small group breakouts. It is being accountable for people attending the class and making sure they are comprehending the material presented. We also need to make sure the tests at the end of the class is administered properly. Making a 30-hour weeklong course is much more labor intensive than creating a two or four-hour seminars with no test involved. MAAO courses will need to be rewritten before we can offer them virtually. There will be many I’s to dot and t’s to cross, before this will become a reality. We are making plans to move in this direction, but it will take time.If you have not done so, make sure you

check out the requirements of obtaining your AMA license. Some of the requirements have changed since the beginning of the licensing cycle on July 1st. Also new is the State Board is approving continuing education hours as small as two hours now. I want to strongly remind assessors that are under the deadline to receive their AMA by July 1, 2022, that you are making proper arrangements to achieve this license. It is less than 2 years away and classes are only offered typically once a year.

If you are wanting to get involved with MAAO, there are a couple of committees that could use a few more members to get active within the organization. When you take on a role within our organization, you will truly see the benefits come back to you. I am excited with where MAAO is at right now and even more excited with where we will go in the future. It is going to take many people coming together to keep us moving forward.

In leaving my year as President, I am so honored to have served the organization. I want to thank everyone who has helped me through this year. It was a great team effort to get us through our rough times. And it is through these tough times that we can become better and stronger, together!

Daryl MoellerMAAO President

By Daryl Moeller,

SAMAMille Lacs

County

What a beautiful day

6 FALL 2020 / Equal Eyes

By Amanda Lee 2019-2020 MAAP President [email protected]

MAAPUPDATE

“Ever notice the word ‘rough’ in ‘through’? There is truth to that, though the way may be rough, we are still able to get through it.”

~Anthony Liccione

As with everything else, Covid-19 has changed our plans for our MAAP Conferences. We elected to cancel both conferences in 2020 and will resume again next year! I hope that you and yours are staying healthy and looking at the positive things during this time.

~Amanda LeeMAAP President

FALL 2020 / Equal Eyes 7

meet holly

Holly has worked in the State Assessed Property Section at the Department of Revenue for over 8 years. She has a bachelor’s degree in Economics and minor in statistics from St. Cloud State University, unitary appraiser certificate from the Western States Association of Tax Administrator, and Foundations of 21st Century Finance Award from Colorado State University - Global Campus. She lives in North Branch, MN with her husband and two daughters (2 ½ years and 4 months old).

Holly joins us with experience in publishing The Minute, MAAO’s newsletter. She will also be working on the publishing end of Equal Eyes as our teams join forces to produce quality periodicals to our members. Welcome, Holly!

Holly Soderbeck, SAMA Newest Member of MAAO’s Editorial Committee

We’d love to hear from you! Please send us your ideas for Equal Eyes and The Minute.

8 FALL 2020 / Equal Eyes

Sponsored By:

COVID 19IN THE ASSESSMENT

WORLDWritten By

Jason Jorgensen, SAMAWadena County

Editorial Committee Associate Editor

FALL 2020 / Equal Eyes 9

county and city assessor’s offices throughout the state. The results compiled reached basically all four corners of the state, as well as, several large cities, including the twin cities metro area. At the onset, many counties opted to send all, or part of their employee’s home to work remotely, some on a rotational every other day in the office schedule, while others are working from home indefinitely.

However, none of the offices that completed the survey have had any down time up to this point, a few offices did have to hold off on hiring any new staff until this is under control. Many offices are utilizing Zoom, Web X, Skype, and other forms of web cam communications to hold office meetings, and interior inspections of properties. For the counties that are doing in the field quintile inspections,

some are only doing inspections from the car or sidewalk, while others are door knocking and maintaining a safe distance from the taxpayer when they answer the door. Approximately one third of the offices that responded sent out a notice to the taxpayers prior to doing property inspections letting them know how Covid was a ffec t ing th i s yea r ’s quintile. Appraisers are taking this seriously, as they encounter people in the field, they are being cautious and avoiding contact with the taxpayers. Appraisers and office staff alike are wearing masks, using hand sanitizer, and communicating with taxpayers through Plexiglas windows, in hopes that the virus won’t spread.

Some assessor offices are choosing not to do field inspections, but to use their new aerial photography and the MLS information to meet quintile quota for the year, and only do property inspections for new construction. Others counties have sent out questionnaires to the properties with improved parcels to get needed interior information. Assessors have become creative and have had to put a lot of extra thought into how this year’s quintile is going to get accomplished. Overall, most of the assessor’s staff have had a good attitude toward the situation, with only one person deciding to retire. As we move forward many things are going to change, as we walk into this new normal in the assessment world.

This year has definitely been a year of turmoil and uncertainty throughout the entire world. Covid-19 has grabbed ahold of many areas of our lives and has changed life as we know it. The normal that we once knew is now gradually being replaced with a new normal, and may forever change the assessment world.

As we venture into this new normal, we will find a way to adapt to a new way of property assessment, at least for this year and maybe going forward into the future as well. Some areas of Minnesota have obviously been impacted at a higher level than others, but the response throughout the state has been similar, to protect and coordinate a proactive plan to help eliminate the threat to not only employees, but to the public as well. A recent survey was sent out statewide, and 35 out of 103 responses were recorded from continued on the following page

WORKED REMOTELYFROM HOME

94%

6%

YES NO

10 FALL 2020 / Equal Eyes

SURVEY RESULTS88%

9%3%

HAS YOUR OFFICE LAID OFF ANY PERSONNEL?

YES NO NOT HIRING

100%

HAS YOUR OFFICE HAD ANY DOWN TIME?

YES NO

43%

35%23%

BACK TO WORK?

YES NO PARTIALLY

COVID 19IN THE ASSESSMENT WORLD

NO FIELD WORK NO CHANGE

FALL 2020 / Equal Eyes 11

SURVEY RESULTS

23%

63%

14%

ADAPTED FIELD WORK

EXTERIOR ONLY INTERIOR APPOINTMENTNO FIELD WORK NO CHANGE

QUNTILE NOTICES SENT OUT

69%

31%

YES NO

PUBLIC COUNTER AREA

17%

83%

CLOSED MASKS & PLEXIGLASS

97%

3%

EMPLOYEE RESPONSE TO COVID 19

GOOD NOT WELL

12 FALL 2020 / Equal Eyes

Fall Conference Highlights September 27-30, 2020

Duluth, MN

FALL 2020 / Equal Eyes 13

Thank You Sponsors! 74th Annual MAAO Fall Conference

Gold Level

Bronze Level

14 FALL 2020 / Equal Eyes

FALL 2020 / Equal Eyes 15

16 FALL 2020 / Equal Eyes

FALL 2020 / Equal Eyes 17

18 FALL 2020 / Equal Eyes

Sponsored By:

Jamie Freeman, SAMA Clearwater County

Editorial Committee Member

THE TOP 10Etiquette Tips for

a Successful Virtual Meeting

Dust is slowly accumulating in conference rooms across Minnesota. As we adjust to a new COVID-19 normal, virtual meetings and video conferences are commonplace in the workforce and well on their way to becoming the main way to connect with fellow assessors. It is important to make sure that everyone in attendance is following virtual meeting etiquette. Here are a few tips to help you do just that.

1) Prepare for your online meeting It’s a good idea to prepare yourself in the same manner that you would for an in-person meeting. One of the most important aspects of a virtual meeting is to ensure that you do not waste valuable time, that the meeting is productive and useful.

Prior to the meeting:• Verify you have the correct date and time. • Review the agenda.• Make sure your video and audio work properly. • Familiarize yourself with virtual meeting tools. • Have a list of input/questions ready.

2) Be EarlyTry to be a few minutes early. This is considered common courtesy for any meeting and applies to virtual meetings as well. Log in early and be ready to start a few minutes ahead of time, and observe proper professional meeting behavior throughout the meeting.

3) IDENTIFY yourself Depending on the meeting, it is possible that those in attendance do not know everyone. An introduction of all participants and their role is a nice way to start the meeting. This more effective for a meeting with 20 or fewer participants. Larger meetings may want to simply complete a roll call.

FALL 2020 / Equal Eyes 19

continued on the following page

4) Eliminate distractions • Work from a quiet room. • If working from home – try to limit pets and family members. • Silence your phone and place it away from you. • Mute your microphone when you are not speaking.

5) DRESS APPROPRIATELY

6) Look at the camera and speak clearlySome participants may want to turn up the volume in order to make certain others can hear them.When you are speaking, you want to be sure to look at the camera so that others can feel more engaged. They will feel like you are talking to them. Remember that microphones, speakers, and Wi-Fi issues can make it harder to hear people during virtual meetings, so speak clearly.

7) Be Respectful and courteous• When someone is speaking, let him or her speak. Do not talk over or interrupt others when they are talking. • Make use of the chat box to write questions or comments.• Use a notebook and pen to take notes. Do not type on your keyboard since the microphone inside your

computer is right next to it. • Never put a conference call on hold.

8) PARTICIPATION/focus on the task at handBe an engaged participant. One of the biggest problems associatedwith virtual meetings is engagement. Participation ensures the success of the meeting, to make good decisions, to solve problems and to strengthen relationships. Focus on the task at handDon’t have multiple windows open and try to multitask during the meeting. Documents and presentations that are required for the meeting are the only things you should have up on your screen other than the meeting room.

It is tempting to wear those comfy clothes for virtual meetings. Which is perfectly fine if you are on an audio-only call. However, if you are on camera, dressing professionally is a must. It would be proper to dress in a similar fashion as you would for anin-person meeting.

TOP 10 (CONTINUED)

20 FALL 2020 / Equal Eyes

TOP 10 (CONTINUED)

9) Don’t eat during virtual meetingsEating during virtual meetings is just plain unprofessional. Unless it is a lunchtime meeting, do not eat.Not only is it distracting to others, it’s difficult for you to focus on the meeting when you’re enjoying a meal. Most consider drinking non-alcoholic beverages during the meeting acceptable.

10) Be sure to follow up. Make sure someone is taking minutes for the meeting and emails a copy to all participants. If there are any questions or concerns that were not addressed or resolved, add them to the next agenda or schedule a one-on-one with the appropriate individual.

When everyone commits to virtual meeting etiquette, this way of doing business can be

highly productive, cost effective and successful!

Classifieds

FALL 2020 / Equal Eyes 21

ClassifiedsAmber Hill, SAMA

Polk County Editorial Committee Member

24729 Dodd Boulevard - Lakeville $2,500,000

Take a peek inside this approximately 5,823 square foot all things Minnesota home. Property features an ice rink, brewery, pool, and “riverfront”. The home is a five bedroom and five bath custom built farmhouse with unique features including a silo featuring a playroom accessible by ladder. Did we mention it was owned by former Minnesota Twins pitcher Glen Perkins? Minnesota’s own Ron Swanson.

22 FALL 2020 / Equal Eyes

What You Get For

Amber Hill, SAMAPolk County

Editorial Committee Member

FAST FOOD

1520 W. Lincoln Avenue, Olivia

Renville County

Sold February 2020

$215,000

Dairy Queen franchise

5309 Shoreline Drive, Mound

Hennepin County

Sold April 2020

$241,000

Porta Del Sol is reportedly now closed.

2635 West Division Street, St. Cloud

Sherburne County

Sold May 2020

$1,700,000

Former Ciatti’s Ristorante, building to be demolished.

205 Paul Bunyan Drive NW, Bemidji

Beltrami County

Sold August 2020

$750,000

Hardee’s Franchise

FALL 2020 / Equal Eyes 23

* The statements made or opinions expressed by authors in Equal Eyes do not necessarily represent a policy position of the Minnesota Association of Assessing Officers.

8

14XXXX

XXXCongratulations!

2020 MAAO Scholarship Winner

Adam Thompson

Adam Thompson is the son of Jill Thompson, Hubbard County Assessor’s Office.

Adam is attending Valley City State University in Valley City, North Dakota for exercise science, sports management and strength conditioning.

Congrats again Adam and thank you to everyone who entered. There were 60 entrants total for the random drawing that was held August 4 at the MAAO Executive Board meeting.

24 FALL 2020 / Equal Eyes

Adam Thompson13261 159th Ave.Menahga, MN 56464

RE: 2020 MAAO Family Member Scholarship

Dear MAAO Scholarship Committee & Membership:

It is with my gratitude and thanks to have been selected and awarded as the recipient of the first ever $1,000 Family Member Scholarship through MAAO. It will be a very welcome and great help to pay for my continued college expenses. My mom is MAAO member Jill Thompson, who works in the Hubbard County Assessor’s office in Park Rapids, MN. I am currently in my third year of college at Valley City State University, located in Valley City, North Dakota - majoring in Exercise Science – with a concentration in Sports Management, Strength and Conditioning, along with Coaching, plus managing to make appearances on the Dean’s List multiple times. I also play baseball at VCSU, which I really enjoy – listed as a utility player as I can play most any position, but primarily middle infield, but can also pitch and catch, so am kept quite busy.

Out of the 60+ applicants who applied, all I’m sure were quite deserving, unique individuals, each with their own path and story to tell, yours truly included. So it is with great surprise to be the lucky one who was chosen for this gift of money. I understand the MAAO President, Daryl Moeller was the one who pitched the idea for this scholarship, getting it off the ground and becoming a reality. It was a great idea – so thank-you Daryl as it was a good one. It will help many future MAAO families with students like myself, take a little edge off college tuition costs, as the scholarships out there are competitive and/or specific to a certain major, gender, academic year or location. It’s nice this scholarship had the flexibility and was open to everyone to apply.

Thank you again for this monetary scholarship gift, made possible by the generosity of the members of MAAO, which seems to be a pretty good group of helpful people, who also care about family members.

Sincerely,

Adam ThompsonVCSU Student

tHank you letter From adam tHompson

FALL 2020 / Equal Eyes 25

ike

Well Done!

tHe maao editorial Committee reCeived tHe 2020 international assoCiation oF assessing oFFiCers Zangerle award For outstanding assessor publiCation.

Congratulations!

Lori JakeJamie Amber Nancy

Jason Mike Missy Holly

26 FALL 2020 / Equal Eyes

Winner of the MAAO

Assessor of the Year Award

Mark PetersonCass County

Assessor

nominating paragrapH

“Region IV nominates Mark Peterson for the 2020 MAAO Assessor of the Year. Mark is the chair of the MAAO Legislative Committee and has been for many years, working to improve the assessments in Minnesota through collaborating among legislators, assessors and many other stakeholders. He has provided testimony to the legislature on behalf of MAAO many times. He has helped lead the organization to partner with the Association of Minnesota Counties. Mark has instructed seminars for MAAO sponsored continuing education. Mark is the Cass County Assessor and has served as Region IV President and Director in the past. Mark is a strong mentor and leader in the assessment community in Northern Minnesota.”

Congratulations Mark!

FALL 2020 / Equal Eyes 27

Amber Hill, SAMA

Polk CountyEditorial Committee Member

out of the past Remembering Yesterday

5 Years Ago—2015

• Equal Eyes was awarded the 2015 John A. Zangerle Award. Congratulations to Managing Editor Lori Thingvold, Associate Editor Jason Jorgensen, Committee Chair Solomon Akanki, and the rest of the Editorial Committee team for bringing the award back to Minnesota. The John A. Zangerle Award is named in honor of IAAO’s third President, John A. Zangerle, and is presented to outstanding periodical publications of an assessor’s association, an IAAO chapter, or other similar organization. Equal Eyes last won the Zangerle Award in 2009.

• In July, the online training for Local and County Board of Appeal and Equalization board members was launched.

10 Years Ago—2010

• Lori Thingvold of Wright County was awarded AMA designation.

• Tim Mitchell became the new City of Maple Grove Assessor

15 Years Ago—2005

• MAAP celebrates 30 years.

• David Armstrong was MAAO President and William Peterson was First Vice President for the executive board.

• Patrick Todd became the new Assessor for the City of Minneapolis

20 Years Ago—2000

• The State Board of Assessors brought up the issue of continuing education policies for unlicensed assessors.

• Jerry Carlson (Retired) is remembered for his companion tours of the Duluth area during the MAAO fall conferences.

25 Years Ago – 1995

• The IAAO awarded Mike Amo with CAE designation.

• Marv Anderson changed cities and switched from Brooklyn Park to an Appraiser at Brooklyn Center.

• The average household income was $35,900 per year and the year-end closing of the Dow Jones was 5117. The GDP for the US was $7269.60 billion

30 Years Ago – 1990

• The Commissioner of Revenue was John James.

• Hotels tripled in value according to an analysis of over 3,000 sales of lodging facilities.

• Kathryn Hepburn and 45 of her neighbors are suing the town of Old Saybrook because of property tax bills.

35 Years Ago - 1985

• Bill Krumholz retired from Kittson County as Assessor.

• MAAO created the Commercial Industrial Committee.

• Interest rates have dropped to a prime rate of 9.5%. Farm loans were 12% with 2 points and residential homes around 11%.

• Real estate news of the time was the $1.2 billion proposed by Triple Five Corporation for the 86 acre old Met Stadium site.

• Lake Pulaski in Wright County rose in water level 8’ over a nine year period.

40 Years Ago – 1980

• The 34th Annual Assessor’s Conference was held at the Sheraton Ritz on Nicollet Mall in Minneapolis.

• Article III – Regions was amended to divide the state into nine regions.

• Combining of the Assess Minutes and Equal Eyes was discussed at the fall conference.

28 FALL 2020 / Equal Eyes

transitions

Nancy Gunderson, SAMA, Clay County Editorial Committee Member

Best Wishes Upon Retirement

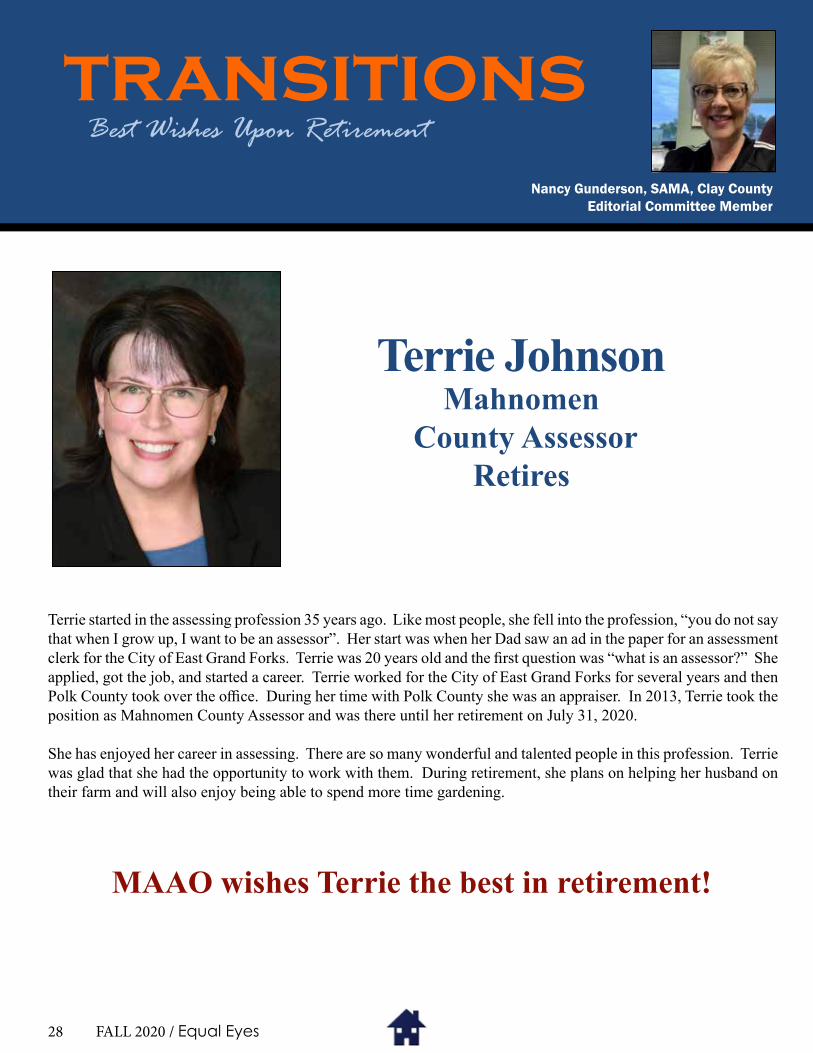

Terrie JohnsonMahnomen

County AssessorRetires

Terrie started in the assessing profession 35 years ago. Like most people, she fell into the profession, “you do not say that when I grow up, I want to be an assessor”. Her start was when her Dad saw an ad in the paper for an assessment clerk for the City of East Grand Forks. Terrie was 20 years old and the first question was “what is an assessor?” She applied, got the job, and started a career. Terrie worked for the City of East Grand Forks for several years and then Polk County took over the office. During her time with Polk County she was an appraiser. In 2013, Terrie took the position as Mahnomen County Assessor and was there until her retirement on July 31, 2020.

She has enjoyed her career in assessing. There are so many wonderful and talented people in this profession. Terrie was glad that she had the opportunity to work with them. During retirement, she plans on helping her husband on their farm and will also enjoy being able to spend more time gardening.

MAAO wishes Terrie the best in retirement!

transitions

Best Wishes Upon Retirement

FALL 2020 / Equal Eyes 29

Happy Retirement!!Dan EischensAnoka County

After 12 years as Senior Appraiser

transitions

Best Wishes Upon Retirement

These current Assessors and retired Assessors got together at the Pennington County Government Center Courtyard June 30, 2020 for Adeline Olson’s retirement coffee hour.Back row: Duane Ebbighausen, Joe Skerik, Steve Carlson, Russ Steer, Carl Bruzek

Front row: Cheryl Grover, Nancy Amberson, Heather Bruley, Adeline Olson, Shelly Nelson

Nancy Gunderson, SAMA, Clay County Editorial Committee Member

30 FALL 2020 / Equal Eyes

transitions

Nancy Gunderson, SAMA, Clay County Editorial Committee Member

Best Wishes Upon Retirement

Bill Riley Sherburne County

Retires After31 Years of Service

Bill Riley retired from Sherburne County on October 2, 2020 after 31 years of service. Bill started on January 3, 1989 in the Sherburne County Assessor’s office as a residential appraiser. During his first few years with Sherburne County, his experience also included doing all personal property assessments. He remembers that he started in this field pre-computer era and used legal descriptions/plat books for directions.

In 1997, Bill was able to participate in the Grand Forks flood reassessment. He said this was an experience he was happy to have done. He remembers that the taxpayers were for once grateful to see the assessor’s staff knowing there would be a financial benefit from the work they did in their assessments.

In 2004, Bill obtained his SAMA designation and moved into the Commercial/Industrial appraiser position assisting the Chief Deputy County Assessor. During the 31 years Bill has worked in the Sherburne County Assessor’s office, he has worked under four different County Assessors. He always enjoyed the Local Board meetings and getting together with everyone.

Bill plans to do a lot of fishing and hunting now in his spare time. He plans to do some traveling to visit siblings that live from the east to the west coasts as well as spending time with his parents. He plans to pursue other hobbies with his kids and grandkids.

We all wish Bill the best in his future adventures!

FALL 2020 / Equal Eyes 31

Jake Pidde, AMA, Stearns County Editorial Committee Member

TAX COURT walmart vs. anoka county

This opinion will be unpublished andmay not be cited except as provided byMinn. Stat. § 480A.08, subd. 3 (2018).

STATE OF MINNESOTAIN COURT OF APPEALS

A19-1926

In the Matter of:Walmart Inc.,

Relator,

vs.

Anoka County,Respondent.

Filed September 14, 2020Reversed and remanded

Ross, Judge

Office of Administrative HearingsFile No. 8-0305-36242

Mark R. Bradford, Edward F. Fox, Jeffrey R. Mulder, Maria P. Brekke, Bassford Remele, Minneapolis, Minnesota; and

Samantha J. Ellingson, Aaron R. Thom, Thom Ellingson, PLLP, Minneapolis, Minnesota (for relator)

Erick G. Kaardal, Mohrman, Kaardal & Erickson, P.A., Minneapolis, Minnesota (for amicus curiae USA Property Tax Associates)

Mahesha P. Subbaraman, Subbaraman PLLC, Minneapolis, Minnesota (for amicus curiae Alliance Property Consultants, Inc.)

Anthony C. Palumbo, Anoka County Attorney, Robert I. Yount, Assistant County Attorney, Anoka, Minnesota (for respondent)

Considered and decided by Ross, Presiding Judge; Segal, Chief Judge; and

Bratvold, Judge.

32 FALL 2020 / Equal Eyes

TAX COURT, continued

2

U N P U B L I S H E D O P I N I O N

ROSS, Judge

Anoka County prepared and presented continuing-legal-education materials

discussing strategies employed by county attorneys to defend property-tax appeals brought

by big-box retailers. Relator Walmart Inc. sought a copy of the presentation from the

county by submitting a request under the Minnesota Government Data Practices Act, but

the county refused, claiming the presentation was work product not subject to disclosure.

An administrative-law judge agreed with the county. We reverse because, even if the

presentation constitutes work product, by broadly presenting the material to third parties

without taking appropriate measures to maintain its confidentiality, the county waived any

work-product protection and the common-interest doctrine would not prevent disclosure.

We remand for the administrative-law judge to amend his order consistent with our

holding.

FACTS

This appeal centers on a presentation for continuing-legal-education (CLE) credit

offered by the Minnesota County Attorneys Association in February 2019. The

presentation, entitled “Litigation of a Big Box Property Tax Appeal,” discussed strategies

that county attorneys might employ to defend against property-tax appeals by businesses

with expansive retail facilities, including Walmart, Target, and Menards.

Assistant Anoka County Attorneys Jason Stover and Christine Carney developed

the presentation materials. Stover contacted the county attorneys association, proposing a

program during which presenters would discuss how Anoka County had responded to

FALL 2020 / Equal Eyes 33

TAX COURT, continued

3

big-box retailers’ property-tax appeals. The association’s education director, Stacy

Albrecht, responded with interest. The planners scheduled the CLE for online presentation

on February 27, 2019. They contemplated limiting attendance to current county attorneys,

retired county attorneys, employees of county attorney offices, and county assessors.

The online CLE presentation occurred on schedule, attended by 76 viewers live and

six others later by recording. It was available only to those who could access it through the

password-protected “members only” section of the county attorneys association’s website.

An attorney representing Walmart, which had been involved in tax litigation against

Anoka County and other Minnesota counties, cited the Minnesota Government Data

Practices Act in May 2019 and made the following request of Anoka County:

I am requesting copies of the following government data:

(1) the webinar, video, or presentation entitled: 2019 Litigation of a Big Box Property Tax Appeal (On-demand Video);

(2) any webinar, presentation, or CLE presented or created by Jason Stover or Christine Carney; and

(3) any communications discussing a webinar, presentation, or CLE relating to big box property tax appeal(s).

Anoka County refused to disclose any documents, maintaining that they were “attorney

data” and therefore not subject to disclosure under the data practices act.

Walmart filed a complaint with the Office of Administrative Hearings in July 2019,

alleging that the county’s nondisclosure violated the data practices act. The county then

disclosed data responding to the third part of Walmart’s data request—communications

discussing the CLE presentation. The disclosed data consisted mainly of emails detailing

34 FALL 2020 / Equal Eyes

TAX COURT, continued

4

the planning and logistics leading up to the CLE presentation, as well as some feedback

from viewers after the CLE. The county refused to disclose the presentation itself.

An administrative-law judge (ALJ) considered the complaint. Walmart moved for

summary judgment based on the county’s nondisclosure, and the county moved for

summary judgment, arguing that the CLE presentation was protected as attorney work

product.

The ALJ granted summary judgment for the county, treating the presentation as

attorney work product not subject to disclosure. The ALJ also determined that the county

did not waive work-product protection by sharing the presentation with other county

attorneys because it was shared only with attorneys who had a “common interest” and who

would protect the information from disclosure to the county’s adversaries. Although

Minnesota has not recognized the common-interest exception to work-product waiver, the

ALJ relied on caselaw from other jurisdictions in concluding that the exception applied

here. The ALJ therefore dismissed Walmart’s complaint.

Walmart appeals by certiorari.

D E C I S I O N

Walmart appeals from the ALJ’s decision granting summary judgment. We may

reverse an agency decision when it is made based on an error in law, unsupported by

substantial evidence in the record, or arbitrary or capricious. Minn. Stat. § 14.69 (2018);

Webster v. Hennepin County, 910 N.W.2d 420, 427–28 (Minn. 2018). On appeal from

summary judgment in which there are no genuine issues of material fact, we consider

FALL 2020 / Equal Eyes 35

TAX COURT, continued

5

whether the ALJ erred in its application of the law, a task we undertake de novo. Prior

Lake Am. v. Mader, 642 N.W.2d 729, 735 (Minn. 2002).

The Minnesota Government Data Practices Act governs access to data held by

government entities. Minn. Stat. § 13.01, subds. 2–3 (2018). The act provides generally

that data created and collected by government entities may be accessed by the public unless

an exception applies. Minn. Stat. § 13.03, subd. 1 (2018). The act creates an exception for

attorney data, providing that “the use, collection, storage, and dissemination of data by an

attorney acting in a professional capacity for a government entity shall be governed by

statutes, rules, and professional standards concerning discovery, production of documents,

introduction of evidence, and professional responsibility.” Minn. Stat. § 13.393 (2018).

The county argues that the CLE presentation is not subject to disclosure because it is

attorney work product under section 13.393, which incorporates existing law regarding

privileges and protections found in other substantive areas of law without expanding or

narrowing their scope. Kobluk v. Univ. of Minn., 556 N.W.2d 573, 576 (Minn. App. 1996),

rev’d on other grounds, 574 N.W.2d 436 (Minn. 1998). The scope of a privilege or

protection under the data practices act presents a question of law that we review de novo.

See id.

Walmart challenges the ALJ’s determinations both that the CLE presentation was

work product and that the county did not waive work-product protection by sharing the

presentation with third parties. We can assume for the purposes of this opinion that the

CLE presentation constituted work product because, when the county shared the

presentation with third parties, it clearly waived any consequent protection.

36 FALL 2020 / Equal Eyes

TAX COURT, continued

6

Documents are protected as work product only when the protection is properly

claimed and is not waived or lost. State ex rel. Humphrey v. Philip Morris Inc., 606 N.W.2d

676, 693 (Minn. App. 2000). Work-product protection generally is waived if the attorney

discloses the protected material to third parties “in circumstances in which there is a

significant likelihood that an adversary or potential adversary in anticipated litigation will

obtain it.” Restatement (Third) of the Law Governing Lawyers § 91(4) (2000). The

common-interest doctrine is an exception to work-product waiver that has been adopted in

some jurisdictions, but not expressly in Minnesota, and that applies when the protected

material is disclosed to individuals who share a “common interest.” Id. cmt. b. The ALJ

applied the doctrine here and concluded that the county did not waive its work-product

protection. For the following reasons, we reach a different conclusion, holding that the

common-interest doctrine would not apply. In doing so, we do not decide whether

Minnesota would adopt the common-interest doctrine in the proper case, which this is not.

Other courts have defined the common-interest exception in various ways, but never

in a fashion so broad as to apply in the circumstances here. The Eighth Circuit explained

that the exception applies when “two or more clients with a common interest in a litigated

or non-litigated matter are represented by separate lawyers and they agree to exchange

information concerning the matter.” In re Grand Jury Subpoena Duces Tecum, 112 F.3d

910, 922 (8th Cir. 1997) (quotation omitted). The Seventh Circuit reasoned that the

exception applies only when “the parties undertake a joint effort with respect to a common

legal interest” and is limited “to those communications made to further an ongoing

enterprise.” United States v. BDO Seidman, LLP, 492 F.3d 806, 816 (7th Cir. 2007). The

FALL 2020 / Equal Eyes 37

TAX COURT, continued

7

D.C. Circuit noted that work-product protection is waived when information is disclosed

“to an adversary or a conduit to an adversary” and explained that the existence of a common

interest could help determine “whether the disclosing party had a reasonable basis for

believing that the recipient would keep the disclosed material confidential.” United States

v. Deloitte LLP, 610 F.3d 129, 140–41 (D.C. Cir. 2010). And the Supreme Court of New

Jersey has concluded that the common-interest exception “applies to communications

between attorneys for different parties if the disclosure is made due to actual or anticipated

litigation for the purpose of furthering a common interest, and the disclosure is made in a

manner to preserve the confidentiality of the disclosed material and to prevent disclosure

to adverse parties.” O’Boyle v. Borough of Longport, 94 A.3d 299, 317 (N.J. 2014)

The county presents a plausible common interest in its strategy-sharing materials

because county attorneys are tasked with defending tax appeals. See Minn. Stat. § 278.05,

subd. 2 (2018). But under the facts derived from the summary-judgment evidence as

construed in the light most favorable to Walmart, no version of the common-interest

doctrine extends far enough to cover these circumstances for at least two reasons: first, the

county allowed the presentation to be accessed by individuals who did not share the

common interest of defending tax appeals, and second, adequate safeguards did not exist

to ensure that the presentation would not be disclosed to adverse parties.

Email exchanges among the planners indicate that they did not intend to limit

viewership to those who shared a common interest with county attorneys. In an early email

discussing the logistics of the presentation, for example, Stover asked Albrecht if the

webinar would be limited to employees of county attorney offices, and Albrecht responded

38 FALL 2020 / Equal Eyes

8

that a few retired county attorneys would also attend. Stover did not object. But a former

county attorney might represent private clients adverse to the counties’ shared interest

opposing big-box tax appeals. And in another email, Stover asked Albrecht “whether

county assessors and their staffs can attend this webinar” because much of the information

would “be applicable to them as well.” County assessors do not share the duties or serve

an advocacy role defending counties in litigation, but are instead tasked with providing a

neutral assessment of real-estate market value. See Minn. Stat. § 273.08 (2018). Albrecht

also indicated that “other county staff” could attend if a county attorney invited them, but

the record does not establish that the other staff would share the interests of county

attorneys. And according to Walmart’s statement of undisputed facts, most of the

individuals who attended had not been involved in tax litigation. It does not appear from

the record that the planners expected the CLE to be restricted to individuals sharing a

common interest, and the record does not establish that all attendees fit such a restriction.

The planners also did not sufficiently ensure that the CLE presentation would not

be disclosed to adverse parties. The county did make some effort, making the presentation

available only to members of the county attorneys association with access through a

password-protected section of the association’s website. But the record does not suggest

that the county asked viewers to keep the information confidential. See Deloitte, 610 F.3d

at 141 (recognizing that, in the absence of a common litigation interest, a reasonable

expectation of confidentiality may be based on a confidentiality agreement or other

arrangement between the disclosing party and the recipient). The CLE presentation was

later “uploaded for distribution on [the association’s] website,” and attendees could

TAX COURT, continued

FALL 2020 / Equal Eyes 39

9

download the materials. This would enable viewers to share the materials with other,

potentially adverse, persons. The record does not demonstrate that the planners took steps

to keep the information confidential during the presentation or afterward.

We add that the disclosure here is far broader than the narrow disclosure in cases

that have applied the common-interest exception, typically involving only one or a small

handful of others. See Deloitte, 610 F.3d at 133, 142 (applying the exception to hold that

work-product protection was not waived when a party disclosed protected information to

one independent auditor); BDO Seidman, 492 F.3d at 817 (applying the exception when

in-house counsel for one party shared a memorandum with counsel for one other party

discussing legal issues); O’Boyle, 94 A.3d at 304, 317–18 (applying the exception to

documents prepared by a private attorney and sent to a single municipal attorney discussing

strategy to defend against the same opposing party in separate lawsuits). This case

involving a well-attended CLE stands in obvious contrast to these limited-dissemination

cases. The county cites no common-interest-exception case involving anywhere near the

number or variety of outsiders with whom the presenters in this case shared their

information. And the county does not circumvent that omission by characterizing the CLE

presentation as a “training program” for county attorneys; the planners did not

communicate about the CLE as a training program, and they did not advertise it in that

fashion. We therefore need not consider whether an actual training program offered to a

limited group and offered with confidentiality protection would warrant the exception.

Again, we do not address whether the common-interest doctrine has been or should

be adopted in Minnesota. We hold only that the county waived its claim to work-product

TAX COURT, continued

40 FALL 2020 / Equal Eyes

TAX COURT, continued

10

protection and that the common-interest exception would not apply here. The county offers

no other basis to support the ALJ’s dismissal of Walmart’s complaint. We therefore reverse

the ALJ’s dismissal and remand for further proceedings consistent with this opinion.

Reversed and remanded.

FALL 2020 / Equal Eyes 41

State Board of Assessors Meeting Minutes

St. Michael City Center Tuesday, July 14, 2020

Chairperson Gregg Larson convened the meeting at 8:30am.

Board members in attendance:

Andrea Fish & Reed Heidelberger were unable to attend

Agenda for the July 14, 2020 meeting was reviewed. Lori Schwendemann moved to approve the agenda. Mike Reed seconded the motion. The motion carried.

Minutes of the May 19, 2020 meeting were reviewed. Joy Kanne moved to approve the minutes. Jane Grossinger seconded the motion. The motion carried.

Updates • Form Report Update

Dates Submitted Reports

Approved Reports

Rejected Reports

Reports being Graded

July 1, 2013 – December 31, 2013 6 6 0 0 January 1, 2014 – December 31, 2014 24 24 0 0 January 1, 2015 – December 31, 2015 27 27 0 0 January 1, 2016 – December 31, 2016 57 57 0 0 January 1, 2017 – December 31, 2017 26 26 0 0 January 1, 2018 – December 31, 2018 25 24 1 0 January 1, 2019 – December 31, 2019 28 27 1 0 January 1, 2020 – July 14, 2020 30 22 6 2

Passed Reports (7/1/2013 – 7/14/2020) Received AMA

Received SAMA

Received CMAS

Have not applied for

AMA

213 154 14 5 41

Gary Amundson Charlie Blekre Jane Grossinger Joy Kanne

Gregg Larson Mike Reed Lori Schwendemann

42 FALL 2020 / Equal Eyes

Board of Assessors Meeting Minutes July 14, 2020 Page 2 of 5

2

Updates (cont.)

• Rule Change: The rule changes were sent from the Office of Administrative Hearings to the Secretary of State’s Office on June 12, 2020 and were filed on June 26, 2020, which is the filing date that starts the Governor’s 14-day veto period.

• MAAO Online Seminars Update: Board members shared their experience after auditing the MAAO online seminars.

• MAAO Online Seminars Surveys: The board reviewed the MAAO surveys they received after the completion of the online seminars.

• Complaint Summary: Since May 2020, the Department of Revenue has received no new complaints. At this time all investigations have been closed, and no new cases have been opened.

• MAAO Curriculum & Assessor Standards Committee Update by Gary Amundson: No updates at this time.

Approved Continuing Education Hours Requests • 7-Hour USPAP Update: Brett Hall requested the board to review the format for a “live

webinar” for this board approved seminar sponsored by North Star Chapter of Appraisal Institute for continuing education. The board’s continuing education committee approved this request for 7 hours of continuing education.

• The Sales Comparison Approach: Craig Anton requested the board review this online course sponsored by McKissock for continuing education. The board’s continuing education committee approved this request for 7 hours of continuing education.

• Evaluating Commercial Leases: Brett Hall requested the board to review the format for a “live webinar” for this board approved seminar sponsored by Appraisal Institute for continuing education. The board’s continuing education committee approved this request for 7 hours of continuing education.

• Fundamentals of Commercial Real Estate: Timothy Vang requested the board to review this online course, sponsored by The CE Shop for continuing education. The board’s continuing education committee approved this request for 3 hours of continuing education.

Request for Assessor Accreditation Waiver Joy Kanne made a motion to grant the Assessor Accreditation Waiver to the following individuals.

Dave Christensen, St. Louis County Steve Halverson, Steele County Roger Schmitz, Local assessor in Pennington & Red Lake Counties

Lori Schwendemann seconded the motion. The motion carried.

Applications for Certified Minnesota Assessor Gary Amundson made a motion to award the Certified Minnesota Assessor license to the following individuals.

FALL 2020 / Equal Eyes 43

Board of Assessors Meeting Minutes July 14, 2020 Page 3 of 5

3

Brandie Hanson, Otter Tail County Joseph Hile, Goodhue County Sheriann LaBuhn, Chisago County Austin Noble, Goodhue County Melanie Oakes, Polk County Jordan Safe, Goodhue County

Mike Reed seconded the motion. The motion carried.

Applications for Accredited Minnesota Assessor Jane Grossinger made a motion to award the Accredited Minnesota Assessor license to the following individuals.

Laura Aamodt, Washington County Patricia Flaa, Polk County Ryan Johnson, Carver County Faye Larson, Washington County Damaris Ledesma, MN Department of Revenue Christine McChesney, Pipestone County Shawn McCoy, Mcleod County Cathleen Pastorius, Washington County Dell Sanko, Carver County Jodi Sell, Mcleod County Lowell Skoog, Local Assessor in Becker & Hubbard Counties Nichole Staehling, Freeborn County Mark Theobald, Olmsted County Ronald Volkman, Winona County Melissa Weston, Nicollet County Lindsey Wetzel, Winona County Michael Wirth, Kandiyohi County

Mike Reed seconded the motion. The motion carried.

Applications for Senior Accredited Minnesota Assessor Lori Schwendemann made a motion to award the Senior Accredited Minnesota Assessor license to the following individuals.

Mark Fritz, Scott County

44 FALL 2020 / Equal Eyes

Board of Assessors Meeting Minutes July 14, 2020 Page 4 of 5

4

Meggie Munsterman, Watonwan County Brian Rosenau, Yellow Medicine County Jane Grossinger seconded the motion. The motion carried.

Gary Amundson made a motion to award the Senior Accredited Minnesota Assessor license to the following individual.

Stacy Westerlund, Aitkin County Jane Grossinger seconded the motion. The motion carried with one nay.

Charlie Blekre made a motion to award the Senior Accredited Minnesota Assessor license to the following individual.

Roy Levitt, St. Louis County Lori Schwendemann seconded the motion. The motion carried with one nay.

Mike Reed made a motion to award the Senior Accredited Minnesota Assessor license to the following individual.

Ryan Carlson, Carlton County Charlie Blekre seconded the motion. The motion carried with two nays.

Discussion Items

• College Courses vs Management & Leadership Course: The board reviewed a few college courses, they all agreed that these types of college courses should be considered, as an equivalent to the proposed Management & Leadership course requirement for the SAMA license. There will be a time limit for when these types of courses were taken, and a note will be added to the SAMA requirements.

• Rule Changes and Board Approved Licensure Courses: o 15-Hour Property Specific Courses: The board determined that there are plenty of course

options on the board approved licensure course list. o Management & Leadership Courses: The board will continue to look for more options for

these types of courses.

Discussion Items (cont.)

• Continuing Education Course List: Joy Kanne and Jane Grossinger reviewed the board approved online continuing education courses from the previous 4-year cycle; they will be presenting their findings. Tabled until September 22, 2020 board meeting.

FALL 2020 / Equal Eyes 45

Board of Assessors Meeting Minutes July 14, 2020 Page 5 of 5

5

• Basic Appraisal Procedures from Kaplan: Jane Grossinger reviewed this course based on the AMA Standards, and she will be presenting her findings. Tabled until September 22, 2020 board meeting.

• Online seminars and courses: Discuss standards and format requirements for approving online and live webinar seminars and courses. Tabled until September 22, 2020 board meeting.

The chairperson set the next meeting date as Tuesday, September 22, 2020 at the St. Michael City Center in St. Michael, MN at 8:30 am.

Joy Kanne made a motion to pay the expenses for the meeting. Charlie Blekre seconded the motion. The motion carried.

Mike Reed made a motion to adjourn the meeting. Lori Schwendemann seconded the motion. The motion carried.

46 FALL 2020 / Equal Eyes

The Sugar Beet Statue

Located in Halstad, Norman County – part of the Red River Valley sugar beet farming community farming community.

Where Am I?

FALL 2020 / Equal Eyes 47

Official Publication of the Minnesota Association of Assessing Officers mnmaao.org