oil and product market outlook ben holt wood … delivering commercial insight to the global energy...

TRANSCRIPT

www.woodmac.com

Delivering commercial insight to the global energy industry

Oil and Product Market Outlook

Ben HoltVice President, Downstream ConsultingWood Mackenzie, London

Intertanko Seminar

London7th May 2010

2

Delivering commercial insight to the global energy industry

www.woodmac.com

1 Oil Demand

Oil Refining Outlook

Agenda

Implications for Tanker Demand

2

3

3

Delivering commercial insight to the global energy industry

www.woodmac.com

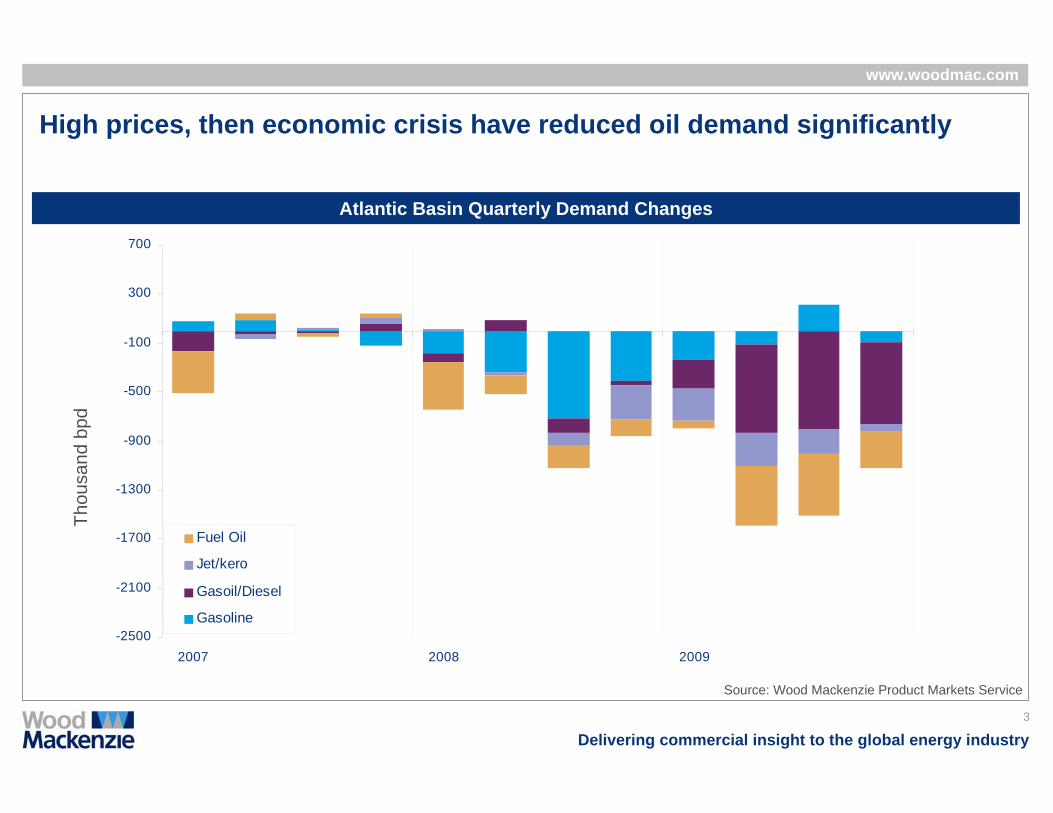

High prices, then economic crisis have reduced oil demand significantly

Atlantic Basin Quarterly Demand Changes

-2500

-2100

-1700

-1300

-900

-500

-100

300

700

2007 2008 2009

Fuel Oil

Jet/kero

Gasoil/Diesel

Gasoline

Thou

sand

bpd

Source: Wood Mackenzie Product Markets Service

4

Delivering commercial insight to the global energy industry

www.woodmac.com

Change in Oil Demand (million b/d) 2007 - 2015

4

aging populations young populations

growing carbon weaker carboncommitment commitment

supply security: supply security:boost efficiency access to resource

weak public finances growing middle class

OECDWeaker GDP Growth

Non-OECDStronger GDP Growth

-2.2mbd

+10.4mbd

Fundamentals of oil demand indicate a structural market shift to the East

Source: Wood Mackenzie Product Markets Service

5

Delivering commercial insight to the global energy industry

www.woodmac.com

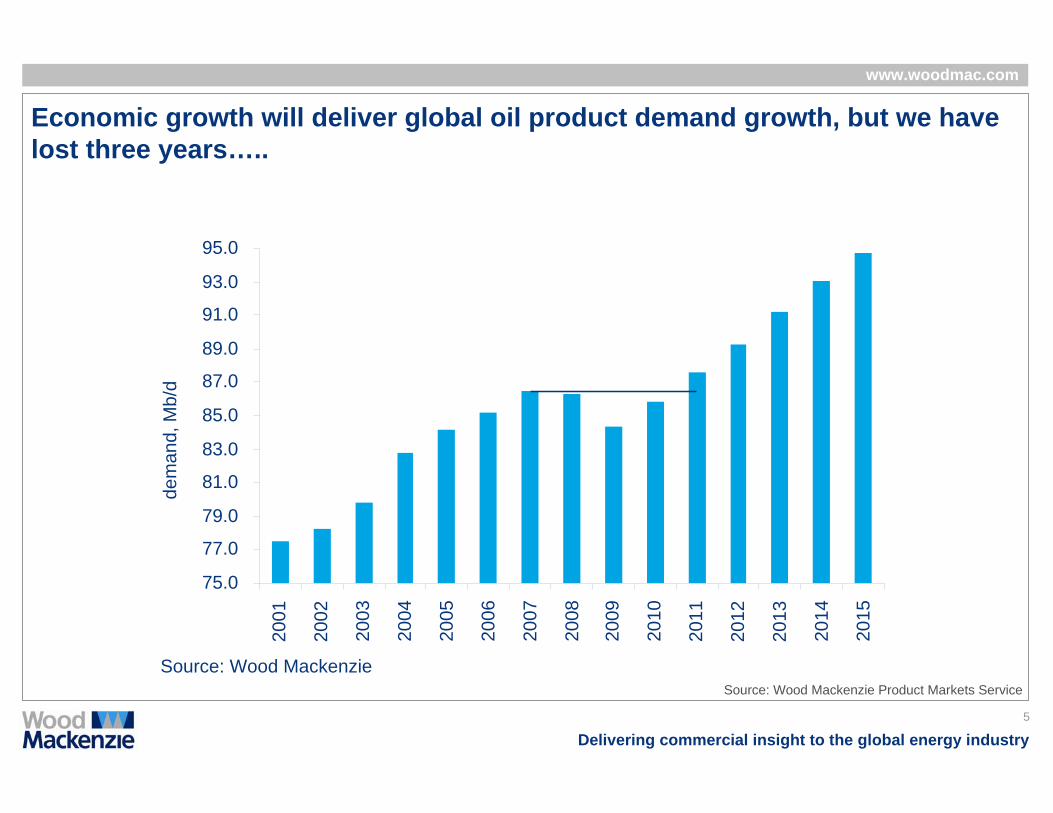

Economic growth will deliver global oil product demand growth, but we have lost three years…..

75.0

77.0

79.0

81.0

83.0

85.0

87.0

89.0

91.0

93.0

95.0

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

Source: Wood Mackenzie

dem

and,

Mb/

d

Source: Wood Mackenzie Product Markets Service

6

Delivering commercial insight to the global energy industry

www.woodmac.com

Globally, transport fuels remain the key market driver as well as naphtha for petrochemicals. Fuel oil demand is in decline.

0

200

400

600

800

1,000

1,200

1,400

1,600

LPG

Nap

htha

Gas

olin

e

Jet/O

ther

Kero

sene

Die

sel/G

asoi

l

Fuel

Oil

Dem

and,

Mt

-0.6

-0.4

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

1.2

Gro

wth

% p

.a. 2

008-

2015

2008 2015 Growth rateSource Wood Mackenzie

7

Delivering commercial insight to the global energy industry

www.woodmac.com

1 Oil Demand

Oil Refining Outlook

Agenda

Implications for Tanker Demand

2

3

8

Delivering commercial insight to the global energy industry

www.woodmac.com

Globally, refining capacity and renewables supply growth has continued, building a significant surplus that extends the downturn a further year or two

-2

-1

0

1

2

2008 2009 2010 2011 2012 2013 2014 2015

Incr

emen

tal (

Mb/

d)

New Crude Capacity Capacity Expansion Net Of Annouced Closures Non-refinery Supply Demand

Almost 6mb/d imbalance created in just 2 years

Only 2-3 mb/d is clawed back in the medium/long term (excluding any future closures)

Source: Wood Mackenzie Product Markets Service

9

Delivering commercial insight to the global energy industry

www.woodmac.com

70%

75%

80%

85%

90%

95%

2005 2006 2007 2008 2010 2015

North America Greater Europe Asia Pacific

Source Wood Mackenzie

utilisation

In 2010, utilisation in Greater Europe and North America is forecast to have fallen 7% compared to 2007. Run rates improve mainly in Asia-Pacific region.

Ongoing low Atlantic Basin runs based on existing refineries imply capacity closures.

Refining runs cut most in North America and Greater Europe…

Subscriber Content

North American utilisation depressed by supply “push” from Europe as well as new export capacity in the Middle East

10

Delivering commercial insight to the global energy industry

www.woodmac.com

0

0.5

1

1.5

2

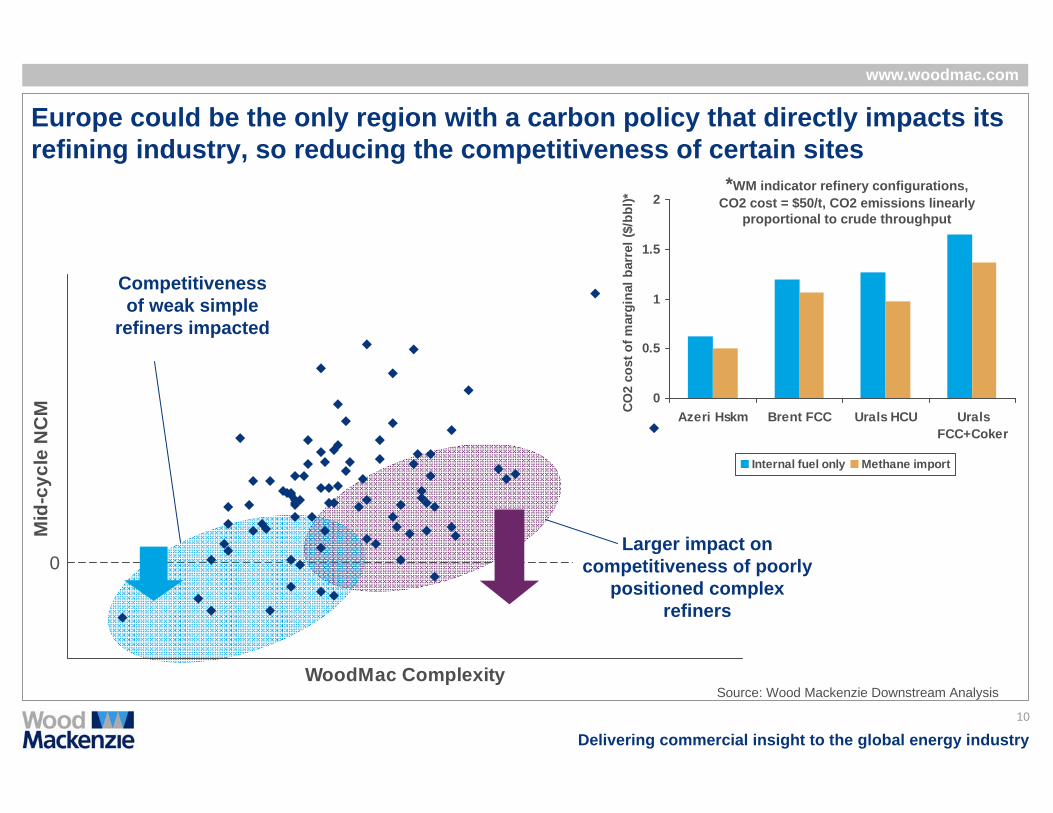

Azeri Hskm Brent FCC Urals HCU UralsFCC+Coker

CO

2 co

st o

f mar

gina

l bar

rel (

$/bb

l)*

Internal fuel only Methane import

WoodMac Complexity

Mid

-cyc

le N

CM

Europe could be the only region with a carbon policy that directly impacts its refining industry, so reducing the competitiveness of certain sites

*WM indicator refinery configurations, CO2 cost = $50/t, CO2 emissions linearly

proportional to crude throughput

Competitiveness of weak simple

refiners impacted

Larger impact on competitiveness of poorly

positioned complex refiners

0

Source: Wood Mackenzie Downstream Analysis

11

Delivering commercial insight to the global energy industry

www.woodmac.com

Bunker fuel market changes- impact on oil product demand N European SECA bunkers reduced from 1.5 to 1.0 wt% in 2010• Achievable with minimum impact as this quality of fuel oil can

be achieved by most sweet crude refineries

SECA bunkers further reduced to 0.1 wt% by 2015• This will require a swing from fuel oil to distillate

In 2015, we estimate 14.4 Mt of fuel oil will have to be replaced with 13.4 Mt of gasoil.

We estimate that a N American ECA would bring an increase in gasoil demand of 15-20 Mta at the expense of fuel oil

Global bunker spec reduced to 0.5 wt% sulphur, effective 1st Jan 2020. May be postponed to 2025 subject to a feasibility review scheduled to be completed no later than 2018.

• This would mean a global swing to distillate (or at least a distillate/fuel oil mix).

• We expect this will be delayed or will not happen at all as the 2018 review and potential for delay will become self-fulfilling

Source: US Environmental Protection Agency. Proposed ECA area

12

Delivering commercial insight to the global energy industry

www.woodmac.com

1 Oil Demand

Oil Refining Outlook

Agenda

Implications for Tanker Demand

2

3

13

Delivering commercial insight to the global energy industry

www.woodmac.com

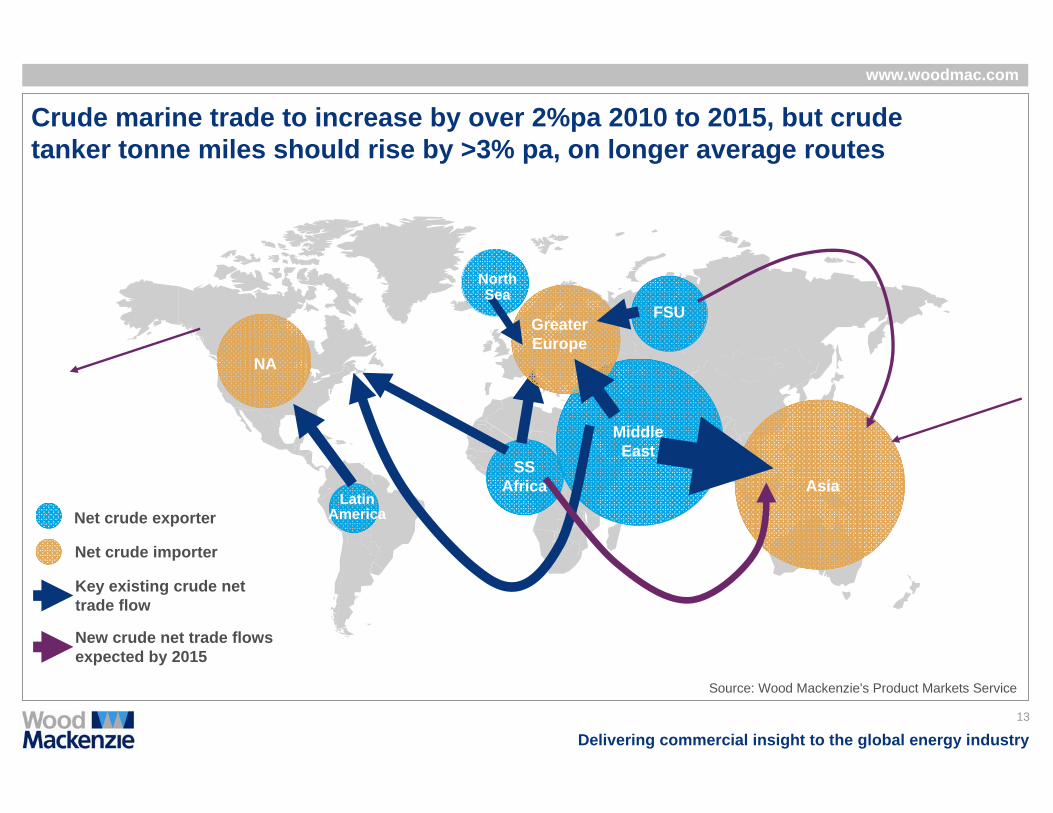

Middle East

Asia

FSU

Latin America

SS Africa

Crude marine trade to increase by over 2%pa 2010 to 2015, but crude tanker tonne miles should rise by >3% pa, on longer average routes

NA

Greater Europe

Net crude importer

Key existing crude net trade flow

Net crude exporter

Source: Wood Mackenzie's Product Markets Service

North Sea

New crude net trade flows expected by 2015

14

Delivering commercial insight to the global energy industry

www.woodmac.com

0

50

100

150

200

250

300

350

400

450

500

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008E

Mta

Other HFO Diesel/Gasoil Jet/Kero Mogas Naphtha LPG

Oil product trade flows have grown quickly in recent years

Annual growth rate =0,5%

Annual growth rate =2,9%

2002-2008 = 6,4%

2002-2006= 6,2%

Source: Wood Mackenzie, IEA

OECD Oil Product Exports

15

Delivering commercial insight to the global energy industry

www.woodmac.com

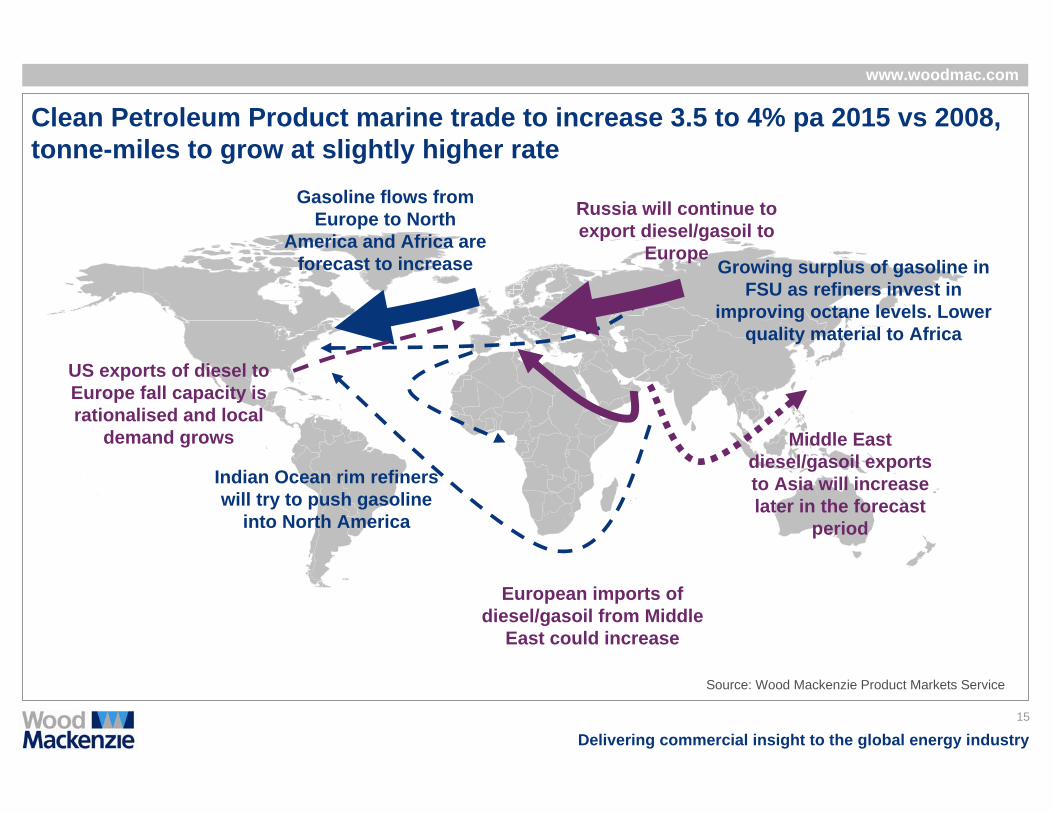

Clean Petroleum Product marine trade to increase 3.5 to 4% pa 2015 vs 2008, tonne-miles to grow at slightly higher rate

Gasoline flows from Europe to North

America and Africa are forecast to increase

Indian Ocean rim refiners will try to push gasoline

into North America

Growing surplus of gasoline in FSU as refiners invest in

improving octane levels. Lower quality material to Africa

US exports of diesel to Europe fall capacity is rationalised and local

demand grows

European imports of diesel/gasoil from Middle

East could increase

Russia will continue to export diesel/gasoil to

Europe

Middle East diesel/gasoil exports to Asia will increase later in the forecast

period

Source: Wood Mackenzie Product Markets Service

16

Delivering commercial insight to the global energy industry

www.woodmac.com

So, after recent downturn in crude marine movements, we expect growth in both dirty and clean tanker demand in coming years

Clean Oil Tanker Demand, trillion tonne.milesDirty Oil Tanker Demand, trillion tonne.miles

0

2

4

6

8

10

12

14

2008 2010 2015

Fuel Oil Crude

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

2008 2010 2015

CPP

17

Delivering commercial insight to the global energy industry

www.woodmac.com

Wood Mackenzie has Global Presence

India

CalgaryFrance

Houston

BostonLondon

EdinburghMoscow

Beijing

Singapore

Sydney

Kuala Lumpur

Tokyo

New York

Dubai

Rio

Argentina

MexicoVenezuela

Associates & PartnersWood Mackenzie Offices

Perth Brisbane

AnnapolisDenver

Houston

18

Delivering commercial insight to the global energy industry

www.woodmac.com

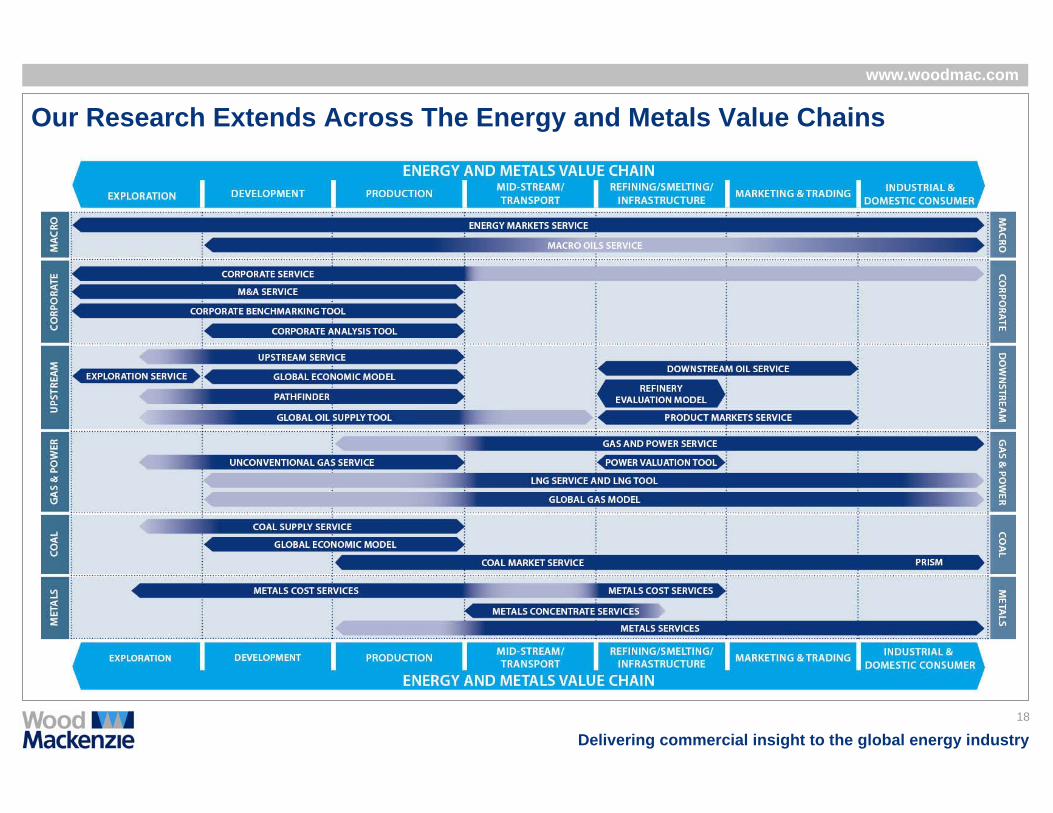

Our Research Extends Across The Energy and Metals Value Chains

ENERGY MARKETS SERVICE

MACRO OILS SERVICE

RADAR

EXPLORATION SERVICE

GLOBAL OIL SUPPLY SERVICE

CORPORATE ANALYSIS TOOL

UPSTREAM SERVICE

GLOBAL ECONOMIC MODEL

PATHFINDER

GLOBAL PRODUCTS OUTLOOK

GRV OPAL

DOWNSTREAM ONLINE

GAS & POWER SERVICE

GLOBAL LNG ONLINE

GLOBAL GAS MODEL

PVT

COAL SUPPLY STUDIES PRISM

19

Delivering commercial insight to the global energy industry

www.woodmac.com

Wood Mackenzie offers consulting services to meet the range of needs of Clients in the Oil Infrastructure business

StrategyIdentification of Target Markets, Locations and CustomersCompetitive Position

Transaction SupportM & A and FinancingCompetitive positioning ValuationsFeasibility Studies

Business EnvironmentRefined product yield and qualityOil trade flow forecastsBiofuels developmentsMarket price structure

Government AdvisorySecurity of Oil Supply

Storage Owner/Operators

Tanker Owners

Infrastructure and Private Equity Fund Investors

Financiers

Trading Companies

Government Agencies

Offering TypesClient Types

20

Delivering commercial insight to the global energy industry

www.woodmac.com

Wood Mackenzie Disclaimer

This presentation has been prepared by Wood Mackenzie Limited for delivery at the Intertanko2010 Seminar. It has not been prepared for the benefit of any particular attendee and may not be relied upon by any attendee or other third party. If, notwithstanding the foregoing, this presentation is relied upon by any person, Wood Mackenzie Limited does not accept, and disclaims, all liability for loss and damage suffered as a result.

The information contained in these slides may be retained by attendees. However, these slides and the contents of this presentation may not be disclosed to any other person or published by any means without Wood Mackenzie Limited's prior written permission.

Ben HoltVP Downstream Oil ConsultingT: +44 203 060 0467 E: [email protected]

21

Delivering commercial insight to the global energy industry

www.woodmac.com

Wood Mackenzie

Kintore House74-77 Queen StreetEdinburgh EH2 4NS

Global Contact Details

Europe +44 (0)131 243 4400Americas +1 713 470 1600Asia Pacific +65 6518 0800Email [email protected]

Global Offices

Australia - Canada - China - Japan - Malaysia - Russia - Singapore - South Africa - United Arab Emirates - United Kingdom - United States

Wood Mackenzie has been providing its unique range of research products and consulting services to the Energy industry for over 30 years. Wood Mackenzie provides forward-looking commercial insight that enables clients to make better business decisions. For more information visit: www.woodmac.com