oil price uncertainty in a small open economy

TRANSCRIPT

Introduction Model Oil price shocks Conclusion Appendix

Oil Price Uncertainty in a Small Open Economy

Yusuf Soner Baskaya Timur Hulagu Hande Kucuk

6 April 2012

Baskaya, Hulagu, Kucuk Central Bank of Turkey

Oil Price Uncertainty in a Small Open Economy

Introduction Model Oil price shocks Conclusion Appendix

Oil price volatility is high and it varies over time...

1985 1990 1995 2000 2005 20100

50

100

150

(a) Mean

1985 1990 1995 2000 2005 20100

0.05

0.1

0.15

0.2

0.25

0.3

0.35

0.4

(b) Coefficient of Variation

Notes: Weekly WTI crude oil prices (90-day moving windows). Data source is Bloomberg.

Baskaya, Hulagu, Kucuk Central Bank of Turkey

Oil Price Uncertainty in a Small Open Economy

Introduction Model Oil price shocks Conclusion Appendix

High volatility creates instability and undermines confidence

I Statement by Gordon Brown and Nicolas Sarkozy on WSJ July 8, 2009

“For two years the price of oil has been dangerouslyvolatile...First it rose by more than $80 a barrel, then fell rapidlyby more than $100, before doubling to its current level of around$70....such erratic price movement in one of the world’s mostcrucial commodities is a growing cause for alarm...The risk isthat a new period of instability [in oil prices] could undermineconfidence just as we are pushing for recovery...”

I OPEC Chief El-Badri on January 31, 2012

“Volatility is bad for investment. If there is conflict [in Iran] wereally cannot invest, there will be clouds all over the investmentprojects.”

Baskaya, Hulagu, Kucuk Central Bank of Turkey

Oil Price Uncertainty in a Small Open Economy

Introduction Model Oil price shocks Conclusion Appendix

Literature on oil price volatility

Empirical: Ferderer (1996), Guo and Kliesen (2005) and Elder and Serletis(2010)

I Negative effect of higher oil price volatility on investment and outputgrowth

I Oil price volatility can partly account for the asymmetric relationshipbetween output growth and oil price changes.

Theoretical:I Bernanke (1983) and Pindyck (1991)

- uncertainty about oil prices induce firms to postpone investment decisions

I Plante and Traum (2011)- investment can increase in response to oil price volatility due to higher

precautionary savings channeled towards domestic capital in a closedeconomy RBC model

Baskaya, Hulagu, Kucuk Central Bank of Turkey

Oil Price Uncertainty in a Small Open Economy

Introduction Model Oil price shocks Conclusion Appendix

What we do in this paper

I analyze the effects of oil price volatility shocks in an oil-importing smallopen economy

I show the importance of the degree of financial market integration for theeffects of oil price shocks

I compare the implications of level and volatility shocks

I discuss the role of volatility shocks in accounting for the asymmetry puzzle

Baskaya, Hulagu, Kucuk Central Bank of Turkey

Oil Price Uncertainty in a Small Open Economy

Introduction Model Oil price shocks Conclusion Appendix

Main features of the model

I Small open economy RBC model similar to Mendoza (1995)

I Trade in a single international bond subject to portfolio adjustment costs- The scale of portfolio adjustment costs captures the degree of financial

market integration

I Tradable and non-tradable good sectors

I Oil in consumption and production as in Kim and Loungani (1992) andBlanchard and Gali (2007)

I Stochastic volatility in real oil prices and sectoral TFP shocks modeled asin Benigno et al. (2010)

Baskaya, Hulagu, Kucuk Central Bank of Turkey

Oil Price Uncertainty in a Small Open Economy

Introduction Model Oil price shocks Conclusion Appendix

HouseholdsFinal good consumption, Ct , is composed of tradable, CT

t , and non-tradablegoods, CN

t :

Ct =

[γ

1κ

(CTt

)κ−1κ

+ (1 − γ)1κ

(CNt

)κ−1κ

] κκ−1

(1)

Oil enters the tradable consumption good:

CTt =

[ν

1ξ

(CQt

) ξ−1ξ

+ (1 − ν)1ξ

(COt

) ξ−1ξ

] ξξ−1

(2)

Households choose Ct , ht , Kt+1 and Bt+1 to maximize lifetime utility

E0

∞∑t=0

βt

(C 1−σt

1 − σ− χ

h1+ηt

1 + η

), (3)

subject to

It +ΦK

2(Kt+1−Kt)

2 +CTt +

PNt

PTt

CNt +Bt+1 = wtht +rtKt +RBt−

ΦB

2(Bt+1−Bt)

2,

(4)It = Kt+1 − (1 − δ)Kt (5)

Baskaya, Hulagu, Kucuk Central Bank of Turkey

Oil Price Uncertainty in a Small Open Economy

Introduction Model Oil price shocks Conclusion Appendix

Firms

Tradable and non-tradable sector firms operate in perfectly competitivemarkets and require capital, labor and imported oil for production.

Y it =

[a

1θi

(Ai

t(hit)αi

(K it )1−αi

) θ−1θ

+ (1 − ai )1θ

(O i

t

) θ−1θ

] θθ−1

, i = T ,N.

Each period, they choose hit , K i

t and O it to maximize profit

Πit =

P it

PTt

Y it − wth

it − rtK

it −

POt

PTt

O it , i = T ,N.

Baskaya, Hulagu, Kucuk Central Bank of Turkey

Oil Price Uncertainty in a Small Open Economy

Introduction Model Oil price shocks Conclusion Appendix

Shocks to real oil prices

I The stochastic process for real oil prices:

log

(POt+1

Pt+1

)= ρP log

(POt

Pt

)+ µP,tεt+1, (6)

I The variance of oil prices can stochastically change over time for a givenlevel of prices:

µ2P,t+1 = (1 − ρµP )µ2

P + ρµPµ2P,t + ψ2

PζP,t+1, (7)

where ζP,t is i.i.d. with zero mean and unit variance.I We solve the model using the methodology developed by Benigno et al.

(2010)I It is sufficient to consider a second-order approximation around the

steady-state to have a distinct and separate role for volatility shocks.I Assumption: Exogenous state variables follow conditionally linear stochastic

processes

Baskaya, Hulagu, Kucuk Central Bank of Turkey

Oil Price Uncertainty in a Small Open Economy

Introduction Model Oil price shocks Conclusion Appendix

Calibration

Standard parameters

I β = 0.99, constant discount factor

I σ = 2, coefficient of constant relative risk aversion

I η = 5, inverse of the Frisch elasticity of labor supply

I κ = 0.41, elasticity of substitution (eos) between traded and non-tradedgoods

I αT = 0.67, labor share in tradable sector value added

I αN = 0.99, labor share in non-tradable sector value added

I γ = 0.43, weight on tradable goods in total consumption

I δ = 0.025, depreciation rate of capital

I ΦK = 0.028, capital adjustment cost parameter

I B/Y = −0.25, foreign bonds as a ratio of GDP

I ΦB = 0.01, 1000, portfolio adjustment cost parameter

Baskaya, Hulagu, Kucuk Central Bank of Turkey

Oil Price Uncertainty in a Small Open Economy

Introduction Model Oil price shocks Conclusion Appendix

Calibration-2

Parameters regarding oil use

I ξ = 0.25, eos between oil and non-oil goods in tradable consumption

I θ = φ = 0.40, eos between oil and non-oil goods in production

I 1 − ν = 0.08, weight on oil in tradable goods consumption

I 1 − aT = 1 − aN = 0.05, weight on oil in production

Parameters regarding the shock processes

I ρT = ρN = 0.90, persistence of TFP level shocks

I ρP = 0.95, persistence of oil level shocks

I ρµT = ρµN = ρµP = 0.50, persistence of volatility shocks

I µ2T = µ2

N = µ2P = 0.0092, variance of level shocks

I ψ2T = ψ2

N = ψ2P = (0.009/10)2, variance of volatility shocks

Baskaya, Hulagu, Kucuk Central Bank of Turkey

Oil Price Uncertainty in a Small Open Economy

Introduction Model Oil price shocks Conclusion Appendix

The Effect of Uncertainty on Physical Investment: Intuition

I Households can save either by accumulating capital, Kt+1, or by buyinginternational bonds, Bt+1

I An increase in oil price volatility leads to

1. higher labor income risk⇒ precautionary saving effect (Kt+1 ↑, Bt+1 ↑)

2. more risky returns to domestic savings (physical capital)⇒ precautionary saving effect (Kt+1 ↑, Bt+1 ↑) andsubstitution effect (Kt+1 ↓, Bt+1 ↑)

I The overall impact on Kt+1 depends on which effect dominates:precautionary saving or substitution effect?

Baskaya, Hulagu, Kucuk Central Bank of Turkey

Oil Price Uncertainty in a Small Open Economy

Introduction Model Oil price shocks Conclusion Appendix

IRFs to Three S.D. Increase in Oil Price Volatility-Normalized Sectoral effects

0 10 20−1

−0.5

0

0.5Investment

ΦB=0.01

ΦB=1000

0 10 20−5

0

5

10x 10

−3 Hours

0 10 20−0.02

−0.01

0

0.01Total Output

0 10 20−0.04

−0.02

0

0.02Oil Consumption

0 10 20−0.01

0

0.01

0.02Oil Input

0 10 20−0.03

−0.02

−0.01

0

0.01Consumption

0 10 20−0.05

0

0.05

0.1

0.15Current Account

0 10 20−0.02

−0.01

0

0.01Real Exchange Rate

0 10 200

1

2

3

4Real Oil Price Volatility

Baskaya, Hulagu, Kucuk Central Bank of Turkey

Oil Price Uncertainty in a Small Open Economy

Introduction Model Oil price shocks Conclusion Appendix

Comparing level and volatility shocks

0 10 20−1

−0.5

0

0.5Investment

LevelVolatility

0 10 20−5

0

5

10x 10

−3 Hours

0 10 20−0.06

−0.04

−0.02

0

0.02Total Output

0 10 20−0.3

−0.2

−0.1

0

0.1Oil Consumption

0 10 20−1

−0.5

0

0.5Oil Input

0 10 20−0.03

−0.02

−0.01

0

0.01Consumption

0 10 20−0.05

0

0.05

0.1

0.15Current Account

0 10 20−0.02

−0.01

0

0.01Real Exchange Rate

0 10 200

1

2

3

4Oil Price Shocks

Baskaya, Hulagu, Kucuk Central Bank of Turkey

Oil Price Uncertainty in a Small Open Economy

Introduction Model Oil price shocks Conclusion Appendix

Comparing level and volatility shocks: sectoral effects

0 10 20−0.04

−0.02

0

0.02Tradable Cons.

0 10 20−0.04

−0.02

0

0.02

0.04Tradable Output

LevelVolatility

0 10 20−0.02

0

0.02

0.04

0.06Tradable Hours

0 10 20−0.03

−0.02

−0.01

0

0.01Non−tradable Cons.

0 10 20−0.03

−0.02

−0.01

0

0.01Non−tradable Output

0 10 20−0.03

−0.02

−0.01

0

0.01Non−tradable Hours

0 10 20−0.06

−0.04

−0.02

0

0.02Tradable Capital

0 10 20−0.6

−0.4

−0.2

0

0.2Tradable Oil Input

0 10 20−0.6

−0.4

−0.2

0

0.2Non−tradable Oil Input

Baskaya, Hulagu, Kucuk Central Bank of Turkey

Oil Price Uncertainty in a Small Open Economy

Introduction Model Oil price shocks Conclusion Appendix

Addressing the asymmetry puzzle

I Empirical literature documents the asymmetric effects of oil price changes:increases are associated with a slowdown in growth but decreases do notnecessarily lead to higher growth.

- Mork (1989), Mork et al. (1994), Ferderer (1996)...

I Our model suggests that considering level shocks alongside volatilityshocks can account for this asymmetry.

I If increases and decreases in oil prices are associated with higheruncertainty,

I adverse effects of an increase in oil prices are exacerbated whileI favorable effects of a decrease are mitigated.

Baskaya, Hulagu, Kucuk Central Bank of Turkey

Oil Price Uncertainty in a Small Open Economy

Introduction Model Oil price shocks Conclusion Appendix

Oil price shocks versus TFP shocks

I Adverse oil price level shocks affect investment, tradable consumption andoutput in a similar way compared to adverse TFP level shocks

I The main difference is that TFP level shocks have different sectoral effectsthan oil price level shocks

I Shocks to the volatility of oil prices and sectoral TFP’s have very similarimplications as they all imply an increase in income uncertainty and mainlywork through the precautionary saving channel

Baskaya, Hulagu, Kucuk Central Bank of Turkey

Oil Price Uncertainty in a Small Open Economy

Introduction Model Oil price shocks Conclusion Appendix

Comparing level shocks to real oil prices and sectoral TFP’s

0 10 20

−15

−10

−5

0Investment

Real Oil PriceTrad TFPNon−trad TFP

0 10 20

−0.06−0.04−0.02

00.020.04

Hours

0 10 20

−1.5

−1

−0.5

0

Total Output

0 10 20

−0.25

−0.2

−0.15

−0.1

−0.05

Oil Consumption

0 10 20

−1

−0.8

−0.6

−0.4

−0.2

Oil Input

0 10 20

−0.3

−0.2

−0.1

0

Consumption

0 10 20

0

0.5

1Current Account

0 10 20

−0.5

0

0.5

1

Real Exchange Rate

0 10 20

−0.2

−0.15

−0.1

−0.05

0Trad. Cons.

0 10 20

−0.4

−0.2

0

Non−trad. Cons.

0 10 20

−1

−0.5

0Trad. Output

0 10 20

−0.4

−0.2

0

Non−trad. Output

Baskaya, Hulagu, Kucuk Central Bank of Turkey

Oil Price Uncertainty in a Small Open Economy

Introduction Model Oil price shocks Conclusion Appendix

Comparing volatility shocks to real oil prices and sectoral TFP’s

0 10 20−1.5

−1

−0.5

0

Investment

Real Oil Price Vol.Trad TFP Vol.Non−trad TFP Vol.

0 10 20

0

2

4

x 10−3 Hours

0 10 20

−0.02

−0.01

0Total Output

0 10 20

−15

−10

−5

0x 10

−3Oil Consumption

0 10 20

−10

−5

0

5

x 10−3Oil Input

0 10 20−15

−10

−5

0

x 10−3Consumption

0 10 20

0

0.05

0.1

0.15

Current Account

0 10 20

−10

−5

0x 10

−3Real Exchange Rate

0 10 20

−15

−10

−5

0x 10

−3Trad. Cons.

0 10 20

−10

−5

0

x 10−3Non−trad. Cons.

0 10 20

−0.01

0

0.01

0.02

Trad. Output

0 10 20

−10

−5

0

x 10−3Non−trad. Output

Baskaya, Hulagu, Kucuk Central Bank of Turkey

Oil Price Uncertainty in a Small Open Economy

Introduction Model Oil price shocks Conclusion Appendix

Summary

I We analyze the effects of oil price volatility shocks in an oil-importingsmall open economy.

I Whether or not domestic agents have access to foreign savings is importantfor the response of investment and economic activity to volatility shocks.

I In the case of financial autarky, precautionary savings resulting from higheruncertainty are channeled towards domestic capital. This implies anincrease in investment and output which is at odds with the empiricalevidence.

I The availability of internationally traded bonds as an extra asset canoverturn this result.

I The co-existence of level and volatility shocks can generate an asymmetryin the way the economy responds to increases and decreases in oil prices inline with the empirical evidence.

Baskaya, Hulagu, Kucuk Central Bank of Turkey

Oil Price Uncertainty in a Small Open Economy

Introduction Model Oil price shocks Conclusion Appendix

APPENDIX

Baskaya, Hulagu, Kucuk Central Bank of Turkey

Oil Price Uncertainty in a Small Open Economy

Introduction Model Oil price shocks Conclusion Appendix

IRFs to a One S.D. Adverse Oil Price Level Shock-Normalized Sectoral effects

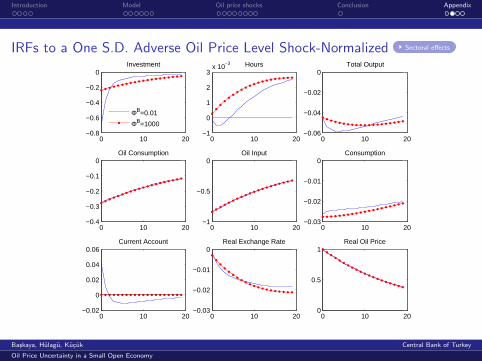

0 10 20−0.8

−0.6

−0.4

−0.2

0Investment

ΦB=0.01

ΦB=1000

0 10 20−1

0

1

2

3x 10

−3 Hours

0 10 20−0.06

−0.04

−0.02

0Total Output

0 10 20−0.4

−0.3

−0.2

−0.1

0Oil Consumption

0 10 20−1

−0.5

0Oil Input

0 10 20−0.03

−0.02

−0.01

0Consumption

0 10 20−0.02

0

0.02

0.04

0.06Current Account

0 10 20−0.03

−0.02

−0.01

0Real Exchange Rate

0 10 200

0.5

1Real Oil Price

Baskaya, Hulagu, Kucuk Central Bank of Turkey

Oil Price Uncertainty in a Small Open Economy

Introduction Model Oil price shocks Conclusion Appendix

IRFs to a One S.D. Adverse Oil Price Level Shock-NormalizedSectoral effects Back

0 10 20−0.04

−0.03

−0.02

−0.01

0Tradable Cons.

ΦB=0.01

ΦB=1000

0 10 20−0.03

−0.02

−0.01

0Tradable Output

0 10 200

0.01

0.02

0.03Tradable Hours

0 10 20−0.03

−0.02

−0.01

0Non−tradable Cons.

0 10 20−0.03

−0.02

−0.01

0Non−tradable Output

0 10 20−0.01

−0.005

0Non−tradable Hours

0 10 20−0.06

−0.04

−0.02

0Tradable Capital

0 10 20−0.8

−0.6

−0.4

−0.2

0Tradable Oil Input

0 10 20−0.8

−0.6

−0.4

−0.2

0Non−tradable Oil Input

Baskaya, Hulagu, Kucuk Central Bank of Turkey

Oil Price Uncertainty in a Small Open Economy

Introduction Model Oil price shocks Conclusion Appendix

IRFs to Three S.D. Increase in Oil Price Volatility-NormalizedSectoral effects Back

0 10 20−0.04

−0.02

0

0.02Tradable Cons.

ΦB=0.01

ΦB=1000

0 10 20−0.02

0

0.02

0.04

0.06Tradable Output

0 10 20−0.05

0

0.05

0.1

0.15Tradable Hours

0 10 20−0.03

−0.02

−0.01

0

0.01Non−tradable Cons.

0 10 20−0.03

−0.02

−0.01

0

0.01Non−tradable Output

0 10 20−0.03

−0.02

−0.01

0

0.01Non−tradable Hours

0 10 20−0.02

−0.01

0

0.01

0.02Tradable Capital

0 10 20−0.02

0

0.02

0.04

0.06Tradable Oil Input

0 10 20−0.03

−0.02

−0.01

0

0.01Non−tradable Oil Input

Baskaya, Hulagu, Kucuk Central Bank of Turkey

Oil Price Uncertainty in a Small Open Economy