on path to long-term value

TRANSCRIPT

On Path to Long-Term Value

IVL Capital Markets Day 2018

February 22, 2018

2017 Financial Results

Sanjay Ahuja, CFO

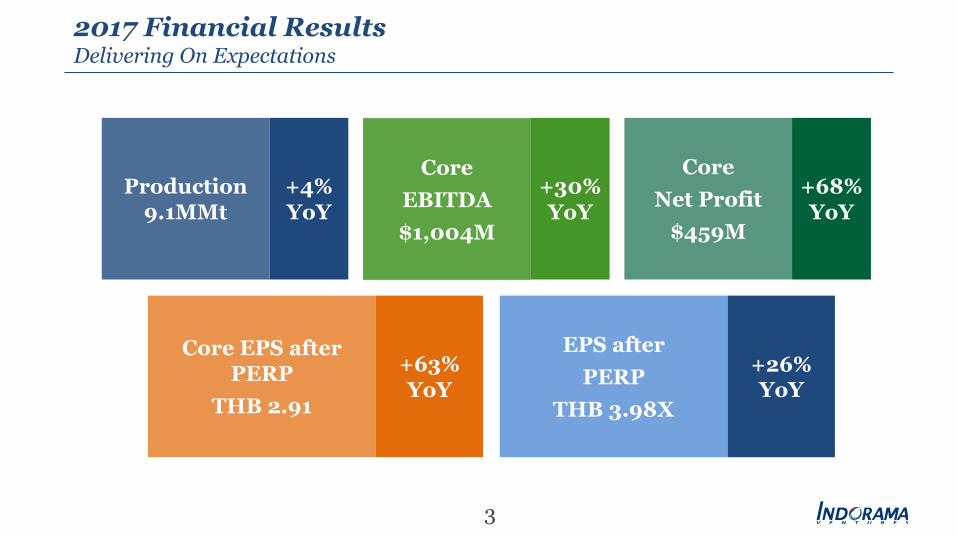

2017 Financial ResultsDelivering On Expectations

3

+30%YoY

Core Net Profit

$459M

+68%YoY

Core EPS after PERP

THB 2.91

+63%YoY

EPS after PERP

THB 3.98X

+26%YoY

Core EBITDA$1,004M

Production9.1MMt

+4%YoY

4

Solid Financial PerformanceStrong Earnings Momentum Continues

EBITDA/ton ($/MT) EBITDA Margin (%)

ROCE (%) ROE (%)

82 91 91 89 110

2013 2014 2015 2016 2017

6% 8% 9% 11% 12%

2013 2014 2015 2016 2017

6% 8% 10% 11% 12%

2013 2014 2015 2016 20173% 6% 8%

13% 17%

2013 2014 2015 2016 2017

Note: Core Financials

Robust Financial Headroom$7 Billion Investment Headroom for Future Growth

5

Dec 31, 2017 Net D/E

Ongoing Project CAPEX Dec 17

Dec 31, 2017 Net Op. D/E

Free Cash Flow in 2018 & 19 based

on approved projects

Estimated Dec 31, 2019 Net D/E

Capex Headroom Estimated Dec 31, 2021 Net D/E

Note: 100% IVL W2 exercise considered, budgeted business plan

0.75x

0.54

$764M

~1x$7B

~0.2x

2017 to 2021 Net Debt to Equity Bridge

Delivering On Our Business Strategy

D.K. Agarwal, CEO PET & Feedstock

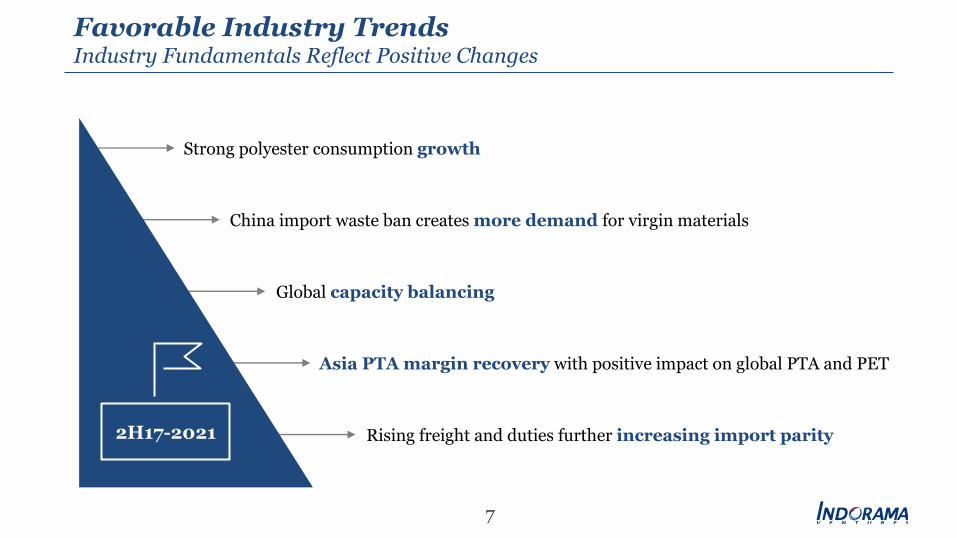

Favorable Industry TrendsIndustry Fundamentals Reflect Positive Changes

7

Strong polyester consumption growth

China import waste ban creates more demand for virgin materials

Global capacity balancing

Asia PTA margin recovery with positive impact on global PTA and PET

Rising freight and duties further increasing import parity2H17-2021

Asia PET BusinessStrong Demand Growth, Capacity Balancing

8

CAGR 2017-21India 12%Indonesia 11%China 7%Thailand 6%

0

1,250

2,500

2016 2017 2018 2019

ChinaRoA

299

757

0

500

1,000

2017China Taiwan ThailandKorea Indonesia India

KM

TK

MT

Asia PET Demand Growth

Asia New PET Capacity 2016-2019

Japan PET Imports - 2017

Strong demand growth, fueled by emerging economies

Limited new PET capacity outside of China

Japan AD creates opportunity for IVL to increase sales in key market with high demand

AD

PET Asia

5075

100125150175

200

2013 2014 2015 2016 2017 2018 2019IVL Industry

Asia PET Spreads

$/M

T

Note: Asia PET spreads over PTA/MEGSource: Industry Data, IVL Analysis

Asia PTA BusinessLower Inventory Levels, Higher Demand Growth, Capacity Balancing

9

0

5

10

15

20

25

30

Jan-14 Jan-15 Jan-16 Jan-17

4 days

20 days

29 days

0

50

100

150

200

250

300

China PTA Inventory

PTA

Spre

ads (

$/M

T)

Effective PTA Capacity – 2022 Basis(KMT)

2018 Demand69 KMT

2022 Demand86 KMT

Global PTA Cost Curve

Day

s

300

250200

150100

50

0

China's PTA inventory end-2017 at its lowest level in last 4 years

China import waste ban creates more demand for PTA

PTA industry spreads will need to continue to improve to justify new investment and plant restarts

PTA

Asia

5075

100125150175

2013 2014 2015 2016 2017 2018 2019

IVL Industry

Asia PTA Spreads

$/M

T

Note: Asia PTA spreads over PXSource: Industry Data, IVL Analysis

Asia Fibers BusinessChina Supply-Side Reforms, China Import Waste Ban

10

China PSF Production

China import waste ban increases demand for virgin fibers

Reducing China cotton supply supports fiber business

Rising recycle feedstock costs pushes virgin PSF margins up

4.06.08.0

10.0

2014 2015 2016 2017 2018 2019 2020 2021Virgin Recycle

MM

t

10,000

7,000

5,000

2000

0

RM

B/M

T

2016 2017 2M18

Virgin PSF PriceRecycle PSF Price

Virgin Raws

Fibers Asia

Asia PSF Spreads

100

150

200

250

300

2013 2014 2015 2016 2017 2018 2019

IVL Industry

$/M

T

China Cotton Supply (MMt)

0102030

13/14 14/15 15/16 16/17 17/18 18/19 19/20 20/21 Demand Imports Production Beginning stocks

China PSF Values

Note: Asia PSF (Polyester Staple Fiber) spreads over PTA/MEGSource: Industry Data, IVL Analysis

West PET BusinessIncreasing Import Parity with Higher Asia PTA, Rising Freight Rates

11

Asia to EU PET Import Parity Drivers-2017/16

US Non-NAFTA PET Imports - 2017

600

0

350

700

2017Brazil Indonesia KoreaTaiwan Pakistan Others

KM

TAD Case490 KMT

0

10

20

30

Asia PTA Margins Increase

Ocean Freights Increase

$/M

T Increase in Asia PTA margins, rising freight rates and other factors as import parity goes up

US PET AD case against 5 countries moving forward

PET West

West PET Spreads

100

150

200

250

300

2013 2014 2015 2016 2017 2018 2019

IVL Industry

$/M

T

Note: West PET spreads over PTA/MEGBased on IVL NAM and EMEA production mixSource: Industry Data, IVL Analysis

West PTA BusinessImport Substitution, Increasing Asian Margins and Freights

12Note: West PTA spreads over PXBased on IVL NAM and EMEA production mixSource: Industry Data, IVL Analysis

Well-established and balanced Western PTA marketplace

EU PTA with substantial import substitution potential (~1,000MMt ~1/3 of demand)

Artlant to partly replace imports

Increase in Asia PTA margins and rising freight rates with positive impact on EU PTA as import parity goes up

West PTA Producers - 2018

EU PTA Demand 2014-2017

Asia to EU PTA Import Parity Drivers-2017/16

0102030

Asia PTA Margins Increase

Ocean Freights Increase

$/M

T

0.0

3.0

6.0

NAM EUIVL BP Alpek PKN EMNCa

paci

ty (M

Mt)

3 producers4 producers

0%

25%

50%

0

1,000

2,000

3,000

2014 2015 2016 2017Domestic Imports Imports Share

KM

T

PTA

West

West PTA Spreads

100

150

200

250

300

2013 2014 2015 2016 2017 2018 2019

IVL Industry

$/M

T

<5 yrs

West MEG BusinessCapturing Integrated Margins in Upcycle Scenario

13Note: US MEG spreads over ethyleneSource: Industry Data, IVL Analysis

80% 82% 79% 80% 77% 80% 81% 80%

60%

70%

80%

90%

2012 2013 2014 2015 2016 2017 2018 2019

Global MEG Operating Rates

Util

izat

ion

(%)

1,6001,4001,2001,000

800600400200

0

Mid

dle

East

Nor

th A

mer

ica

Wes

t Eur

ope

Asia

(e

xcl.

Chin

a)

Chin

a

Oth

erLa

tin A

mer

ica

Rus

sia

& C

aspi

anCh

ina

MTO

/CTO

50,0000 100,000 150,000

1,400 2,500

IVOL New Greenfield0

1,0002,0003,000

Regional Ethylene Production Cost 2020

Brent: $75/bbl Henry Hub NG: $2.85/MMBTU

>7 yrsPayback

Cracker Investment Cost $/

MT

$/M

T Et

hyle

ne

Global MEG market tight for at least 2018-2019 due to project delays

China import waste ban creates more demand for MEG

IVL is investing in one of the most competitive regions

Rising crude makes investment even more accretive

Highly attractive investment vs new build and right-sized

West MEG

US MEG spreads

0100200300400500600700

2013 2014 2015 2016 2017 2018 2019

IVL Industry

$/M

T

220 218205 194

217234 230

0

50

100

150

200

250

2013 2014 2015 2016 2017 2018 2019

Asia PET West PET Asia Fibers

Asia PTA West PTA US MEG

Weighted Average Spread

14

IVL Necessity Business On Recovery PathIndustry Margins Have Bottomed-Out, IVL at Premium to Industry

Industry Necessities Spreads ($/MT) IVL Necessities Spreads ($/MT)

195 193176 169

197217

201

0

50

100

150

200

250

2013 2014 2015 2016 2017 2018 2019

Note: Both Industry and IVL weighted average spreads based on IVL Necessities production mix, US MEG in 2018&19 include crackerSource: Industry Data, IVL Analysis

Nece-ssities

15

IVL Steady HVA BusinessStrong Growth Momentum Continues

ü Innovation-driven

ü Limited numbers of players

ü High barriers to entry

ü High growth potential

ü Investing in Hygiene, Safety and Well-being mega trends

ü Scaling Feedstock, PET and Fibers HVA platforms

ü Sustaining profitability in IPA with production expansion

HVA Fundamentals

IVL HVA BusinessDrivers

IVL HVA Spreads ($/MT)

547

687 721 715815 783 773

0

250

500

750

1,000

2013 2014 2015 2016 2017 2018 2019

IVL PET HVA IVL Fibers HVA

IVL Feedstock HVA IVL HVA Spread

HVA

Note: Weghted average spread based on IVL HVA production mix

16

IVL Necessities & HVA BusinessEnhancing Overall Margins

281 317 312

293 335 343 336

0

100

200

300

400

2013 2014 2015 2016 2017 2018 2019

Asia PET West PET Asia Fibers

Asia PTA West PTA US MEG

PET HVA Fibers HVA Feedstock HVA

Weighted Average IVL Spread (RHS)

Note: Weghted average spread based on IVL overall production mix, US MEG in 2018 and 2019 includes cracker

Nece-ssities

IVL Necessities & HVA Spreads ($/MT)

HVA

Creating Value with HVA

Uday Gill, CEO Fibers

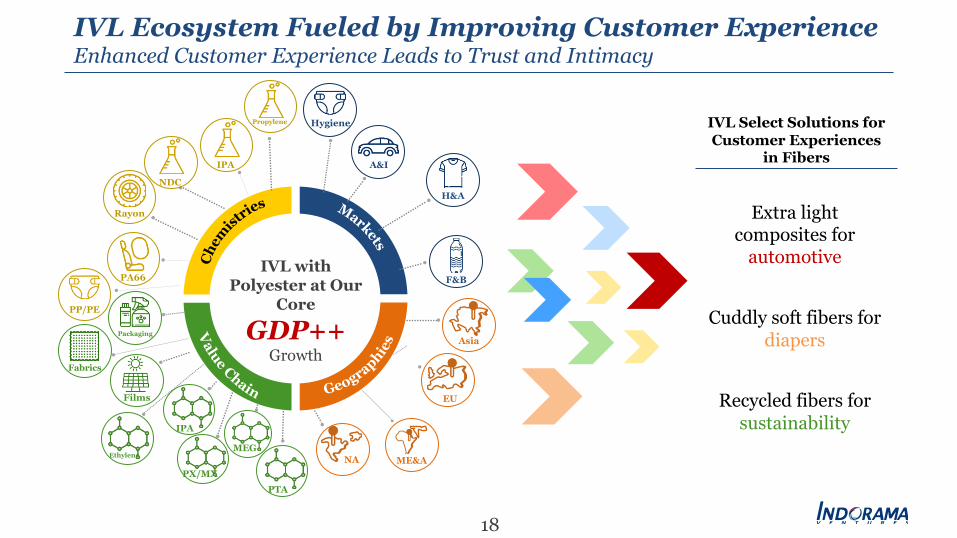

IVL Ecosystem Fueled by Improving Customer ExperienceEnhanced Customer Experience Leads to Trust and Intimacy

Extra light composites for

automotive

Cuddly soft fibers for diapers

Recycled fibers for sustainability

IVL Select Solutions for Customer Experiences

in Fibers

18

IVL with Polyester at Our

Core

GDP++Growth

Hygiene

A&I

H&A

F&B

Propylene

IPA

Rayon

PA66

PP/PE

Packaging

Fabrics

Films

Ethylene

IPA

PX/MX

MEG

PTA

EU

Asia

NA ME&A

NDC

19

Global HVA Fibers Market with Strong Growth PotentialHVA Expected to Capture 50% of Incremental Demand by 2021

2 4 10

17 9

14

23

32

1980-1990 1990 – 2000 2000 – 2010 2010 – 2021

Industry Necessities Fibers

Industry HVA Fibers

Global Incremental Fiber Consumption (MMt)

Source: Industry Data, IVL Analysis

20

Expanding Our HVA Fibers PortfolioThrust on Auto, Industrial, Hygiene to Scale Up Capacities through M&A and Organic Growth

NAM EMEA Asia

IVL HVA Fiber Capacity by Region (KMT) IVL HVA Fiber Production by Segment (KMT)

0

100

200

300

400

2015

2016

2017

2018

2021

2015

2016

2017

2018

2021

2015

2016

2017

2018

2021

0

100

200

300

400

500

2015

2016

2017

2018

2021

2015

2016

2017

2018

2021

2015

2016

2017

2018

2021

Automotive Industrial Hygiene

21

Long Qualification Cycles Create Barriers to Entry HVA Boosts Brand Premium in Necessities Fibers

0 30 60 90 120 150

Tire cord fabric

Hygiene cover stock

Wipes and medical

Automotive interiors

Flame retardant fibers

Fillwell hygiene

Airbag yarn

2013 2014 2015 2016 2017

Qualification period

3 years

2.5 year

2 years

3 years

2.5 years

2 years

3 years

YoY volume growth (KMT)

Spre

ad ($

/MT)

HVA Fibers – Robust Value Driver for IVL Wide Economic Moats Created for Sustainable Growth

0

200

400

600

800

1,000

2014 2015 2016 2017

Published 1.4D Staple Fibers

IVL 1.4D Staple FibersIVL Essentials

IVL HVA

IVL Brand PremiumIVL Value Add

Premium

22

HVA Boosts Overall Fiber Profitability Margin Expansion by Cost/Product Innovation

0

50

100

150

200

250

300

350

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

IVL Fiber HVA

IVL Fiber Average

IVL Fiber Necessities

1x

2x

>4x$/M

T

0

150

300

450

600

750

900

1,050

0

500

1,000

1,500

2,000

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

IVL Fiber HVA conversion cost

IVL Fiber HVA volume (KMT)

3x2x

KM

T

$/M

T

IVL Fiber HVA spread

HVA Fibers – Robust Value Driver for IVL (Cont’d)Wide Economic Moats Created for Sustainable Growth

Growing Our Automotive and Tire Business

Arnaud Closson, MD Glanzstoff

IVL - A Global Leader in Tire ReinforcementAuto & Tire ~$0.9 Billion Business for IVL by 2019, Expanding at ~40% CAGR

24

0

250

500

750

1,000

2014 2015 2016 2017 2018 2019

~40%CAGR

IVL Auto & Tire Revenue ($m)

Note: Includes announced projects

Demographics and Wealth

Greater affluence amongst the middle class

Original Equipment Fitments

Integral part of vehicle Design

Increasingly Stringent Regulation

Regulations demanding higher fuel economy

New Product Developments

New technologies, specialized polymers, unique threads

Global Tire Market With Strong Growth PotentialCreates Opportunity for Investment through M&A and Organic Growth

25

Car Parc 2017-2021

(Million vehicles)1,306

1,475

2017 2021

Tire Production 2017-2021

(Million tires)1,697

1,913

2017 2021

Source: Industry Data, IVL Analysis

+170mn cars

Tire Yarn Demand - 2021(KMT)

16%

84%

IVL Share 2017

930KMT

+220mn

tires

Growth Drivers

Focus on Premium Segments

IVL - Well Positioned Within Tire Industry Leading Supplier to World-Class Customers

26Source: Industry Data, IVL Analysis

Global Customer-CentricPresence

Global Market Leader

Total Solution Provider

PENSingle-

end-cord/Hybrid

Rayon

PA 66/ PET Advanced

PET Standard

IVL Focus

China PET Tire Cord

Global Rayon Tire Cord

Global Single-end-cord/Hybrid

#2

#2

#1Lovosice, CZ

Steinfort, LU

Pizzighettone, IT

Obernburg,DE

Queretaro, MX

Longlaville,FR

Qingdao, CN

Guangdong, CN

SidewallThread

Cap Ply

Belts

Carcass

Inner Liner Bead

Apex

Aramid

PETAdvanced PET

RayonPEN

N66Aramid hybrid

PEN

Winnsboro,US

27

Strong R&D Capability and SynergyCutting-Edge Technology and Production Know-How

Leading technology example –Single-end-cord for Run-flat and High

Performance tiresElectrification

Lightweight materials

Connected vehicles

Shifts in mobility preferences

Autonomous vehicles

New tire design requirements offer an opportunity to partner

with world-class customers and deliver

best-in-class innovative solutions

28

Electric Vehicle Opportunities for Tires, Body and Interior Solutions

comfortable environment

safety features embedded

futuristic features

noise reduction

lightweightnew design opportunities

less complex engine

Taller TiresFuel Economy

Noise Control

Autonomous Driving

Electric Vehicle

Implications

Implications on reinforcement

materials

IVL Solution Platform

ü Passive safety features will prevail

ü Additional active safety features

ü New textile developmentsü Compositesü Insulation

29

Solid Platform for Future Growth and ExpansionIntegrating the Best

A global market leader in tire reinforcement with focus on premium segments

Partnering with world-class customers and delivering best-in-class solutions for their needs

Well positioned, innovation-driven, high growth business for IVL

Robust and long-term value driver for IVL

Clear Direction Towards 2021

Aloke Lohia, Vice-Chairman and Group CEO

Our Debut on DJSI Reflects Our Strong DeliveryIVL Ranks as #5 of all 2017 DJSI Listed Chemical Companies

2014

2015

2016

20%

69%

84%

95%IVL DJSI Score

2017

31Source: RobecoSAM, IVL

Delivering On Our Financial PlanDoubled Our EBITDA in Last 4 Years

32

478 568

640

775

1,004

2013 2014 2015 2016 2017

x2 EBITDA Increase

Core EBITDA ($M)

0.35

0.761.06

1.79

2.91

2013 2014 2015 2016 2017

Creating Superior Shareholder ReturnsStrong EPS Growth in Trough Business Environment

33

Core EPS After PERP (THB/Share)

~70%EPS

Growth

34

Countries 12 15 25

R&D Centers 2 6 11Patents Not material 250 564DJSI Score - - 95% (#51)Employees ~6,000 9,173 15,039

0

2

4

6

8

10

12

14

2010 2013 2017

NA PET

NA Olefins

NA Fibers

NA Aromatics

EMEA PET

EMEA Fibers

EMEA Aromatics

Asia PET

Asia Fibers

Asia Aromatics

34 sites

24 sites

17 sites

20 sites

15 sites

10 sites

15 sites

4sites4 sitesIV

L Ca

paci

ty (M

Mt)

3.7

6.8

11.7

1. Of all 2017 DJSI listed chemical companiesNote: Capacity data including JVs

Constantly Upgrading Our Value PropositionStrategy and Execution Delivered True Value Over Time

35

Our Roadmap for Organic GrowthExpected EBITDA Growth with Approved Projects

247 296195 208197

501

2015 2017 Volume Margins, Costs and Mix

Approved Projects 2019F

Feedstock

Fibers

PET

2015 to 2019 EBITDA ($m)

EBITDA ($/MT) 91 110 Increased

Net Op Debt/Equity 0.81x 0.54x <0.2x

ROCE (%) 10% 12% >15%

1,004

Note: 2019F over 2017 as per management best estimates and may change materially if there are changes in underlying assumptions due to external or internal reasons

640 ~45% EBITDAIncrease

Existing Business

36

IVLConsolidated

By Segment By Region

Increase in Production (%) ~25% ~25% ~20% ~30% ~10% ~40% ~35%

Increase in EBITDA (%) ~35% ~30% ~50% ~35% ~35% ~20% ~70

Growth Capex (2018 and 2019) $ 1.6b ~30% ~20% ~50% ~50% ~30% ~20%

Maintenance Capex (2018 and 2019) $0.3m ~20% ~20% ~60% ~40% ~30% ~30%

Total Capex (2018 and 2019) $1.8b

Simple Payback of Approved Projects ~4.5 yrs

Impact with Existing Business and Approved ProjectsExpected Increase in EBITDA of ~35% in 2019 over 2H17 Annualized

PET Fibers Feedstock NAM EMEA Asia

2H17 Annualized to 2019 EBITDA ($m)

Note: 2019F over 2H17 annualized as per management best estimates and may change materially if there are changes in underlying assumptions due to external or internal reasons, Out of $1.8B capex $764M is spent by 2017

Key Takeaways

37

On Path to Becoming a World-Class Chemical Company Making Great Products for Society

Delivering ~70% Annual EPS Growth in Trough 2013-2017 Business Environment

2H17 Marks a Positive Structural Shift for the industry and Business

~45% Expected EBITDA Growth in 2019 over 2017 with Existing Business and Approved Projects

$7b Investment Headroom by 2021 after $1.8b Committed Capex by 2019

Disclaimer

38

This presentation contains “forward-looking” statements of Indorama Ventures Public Company Limited (the “Company”)1 that relate to future events, which are, by their nature, subject to significant risks and uncertainties. All statements, other than statements of historical fact contained herein, including, without limitation, those regarding the future financial position and results of operations, strategy, plans, objectives, goals and targets, future developments in the markets where the Company participates or is seeking to participate and any statements preceded by, followed by or that include the words “target”, “believe”, “expect”, “aim”, “intend”, “will”, “may”, “anticipate”, “would”, “plan”, “could”, “should, “predict”, “project”, “estimate”, “foresee”, “forecast”, “seek” or similar words or expressions are forward-looking statements.

Such forward-looking statements involve known and unknown risks, uncertainties and other important factors beyond the Company’s control that could cause the actual results, performance or achievements of the Company to be materially different from the future results, performance or achievements expressed or implied by such forward-looking statements. These forward-looking statements are based on numerous assumptions regarding the Company’s present and future business strategies and the environment in which the Company will operate in the future and are not a guarantee of future performance.

Such forward-looking statements speak only as at the date of this presentation, and the Company does not undertake any duty or obligation to supplement, amend, update or revise any such statements. The Company does not make any representation, warranty orprediction that the results anticipated by such forward-looking statements will be achieved.

1Where the context requires, it means the Company, its subsidiaries, joint ventures and associated companies as a group or as members of such group.

Continue Shaping Our Industry LeadershipLeading The Market With Quality, Innovation, Reliability

39Note: Financials Excluding JVs

11R&D Centers

564Patents

$8.4 billionRevenue

15,039Employees

A global presence in

25 countries

75 operating sites

in Asia in EMEA in North America

34 24 17

34%HVA sales

IVL At A Glance - 2017