on the financial performance of socially responsible mutual funds

DESCRIPTION

On the Financial Performance of Socially Responsible Mutual Funds. When “Goody-two-shoes” goes “Bad-to-the-bone”. SRI: The Goals. Provide competitive financial returns while fostering better social and environmental performance SRI mutual funds are one SRI vehicle. Bloomberg’s definition. - PowerPoint PPT PresentationTRANSCRIPT

On the Financial Performance of Socially

Responsible Mutual Funds

When “Goody-two-shoes” goes “Bad-to-the-bone”

SRI: The Goals

Provide competitive financial returns while fostering better social and environmental performance

SRI mutual funds are one SRI vehicle

Bloomberg’s definition

Strategies to achieve objectives

Selection or Screening: Investing in companies that meet certain social and/or environmental performance criteria,

Shareholder activism: using their rights as shareowners to encourage companies to be better corporate citizens, or

Community investment: allocating some of the fund’s assets for investment in disadvantaged urban and rural communities.

Socially Responsible Investing in the U.S.

$2.16 trillion in 2003

Community Investing

$14 billion

Shareholder Advocacy Only

$7 billion

Screening Only$1702 billion

Screening + Shareholder$441 billion

Mutual Fund Screen Types

($ Billions)

10.3

11.2

14.1

16.6

22

23.8

28.8

28.9

31.1

93.4

124

0 20 40 60 80 100 120 140 160

Community Impact

Human Rights

Other*

Products/Services

Equal Employment Opportunity

Defense/Weapons

Gambling

Environment

Labor Relations

Alcohol

Tobacco

Total Assets (billions)

How are they Performing Financially?

The Good The Bad The Ugly

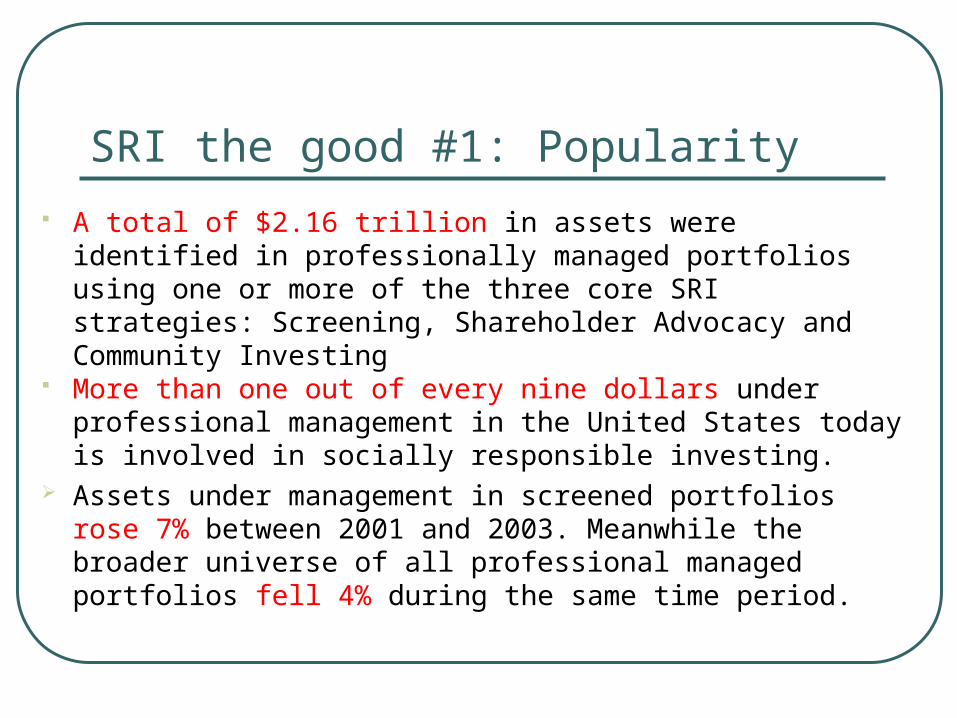

SRI the good #1: Popularity

A total of $2.16 trillion in assets were identified in professionally managed portfolios using one or more of the three core SRI strategies: Screening, Shareholder Advocacy and Community Investing

More than one out of every nine dollars under professional management in the United States today is involved in socially responsible investing.

Assets under management in screened portfolios rose 7% between 2001 and 2003. Meanwhile the broader universe of all professional managed portfolios fell 4% during the same time period.

Growth of SRI Investments ($ Billions) 1997-2003

$5$4$84

$529

$1,185

$736

$265

$1,497

$2,159

$922

$8

$592

$2,320

$897

$2,010 $2,164

$14

$441$448

$2,143

$0

$500

$1,000

$1,500

$2,000

$2,500

Screening Shareholder Both Community Total

1997 1999

2001 2003

Why are they so popular?Why are they so popular? May be Corporate Breakdowns May be Corporate Breakdowns in the Newsin the News

General Electric

Tyco

Enron

Arthur Andersen

Qwest

Xerox

Worldcom

Adelphia

The Good #2: Reported Performance against broad indices

The Good #3: Papers from the mid-nineties Luck (1993, 1998) finds half of the DSI’s

outperformance is due to stock selection, which was, in turn, a function of the social screens

SRI mutual funds actually outperform a sample of matched conventional funds (Statman 2000; Guerard 1997; Kurtz 1997; Mallin, Saadouni and Briston 1995; Luther and Matatko 1994; Luther, Matatko and Corner 1992)

There is a “social factor”, which affects returns. If so, this would need to be estimated and utilized in risk management of socially screened portfolios.

The Bad #1: The Reality

The Bad #2: The Actual Performance Against Broad Indices

1YR 3YR 5YR 10YR

Bond Funds 11 11 10 7Percentage beating LBI 27% 27% 10% 0%Balanced funds 9 8 8 7Percentage beating SP500/ LBI 11% 25% 13% 29%

Large Equity 45 43 34 15Percentage beating SP500 20% 26% 38% 33%Small and Mid Cap Equity 21 21 21 9Percentage beating SP400 19% 19% 14% 33%International Equity 11 11 7 3Percentage beating MSCI WORLD 36% 18% 14% 0%All Funds 97 94 80 41Percentage beating benchmark 21.65% 22.68% 19.59% 10.31%

The Bad #3: Modern Portfolio Theory

Number of Securities

Portfolio Variance

SCREENING PORTFOLIO

NON SCREENING PORTFOLIO

The Bad #4: Recent Findings Studies by Bauer, Kees, and Roger, 2002; Goldreyer

and Diltz 1999; Plantinga and Scholtens 2001; and Sauer, 1997; and Geczym, Stambaugh and Levin, 2003. • SRMF tend to underperform

• If SRMF beat a broad benchmark, it has to do with style investments rather that social investment

• SRI constraint imposes large costs on investors. Entine (2003) questions the validity of screening

methodologies being used and the very legitimacy of the business of SRI.

The Bad # 5: The Rhetoric

"The fact is that social investors as a demographic tend to be better-educated and more affluent than the general population." – Michael Jantzi (Research Associate)

“Over 70% of largest socially responsible mutual funds got top marks from Morningstar, Lipper in 2003” (Socialinvest.org)

“Analysis of expense ratios finds SRI funds neither more or less costly than unscreened funds of similar type” (Socialinvest.org)

Change of tone from 1995-2004: from “we beat broad benchmarks” to “you can potentially perform as well as a regular.”

The Ugly #1: Entrenchment The SRI has been very aggressive towards its

critics. Timothy Middleton (CNBC): “I always attract

critics who assert that SRMF are just as good as the other funds.”

Entine, Miami University Geczy, Stambaugh and Levin (2003) have

been demolished by SRI-Advisor.com- “unsound research design , sloppy work”

Stone, Siena College

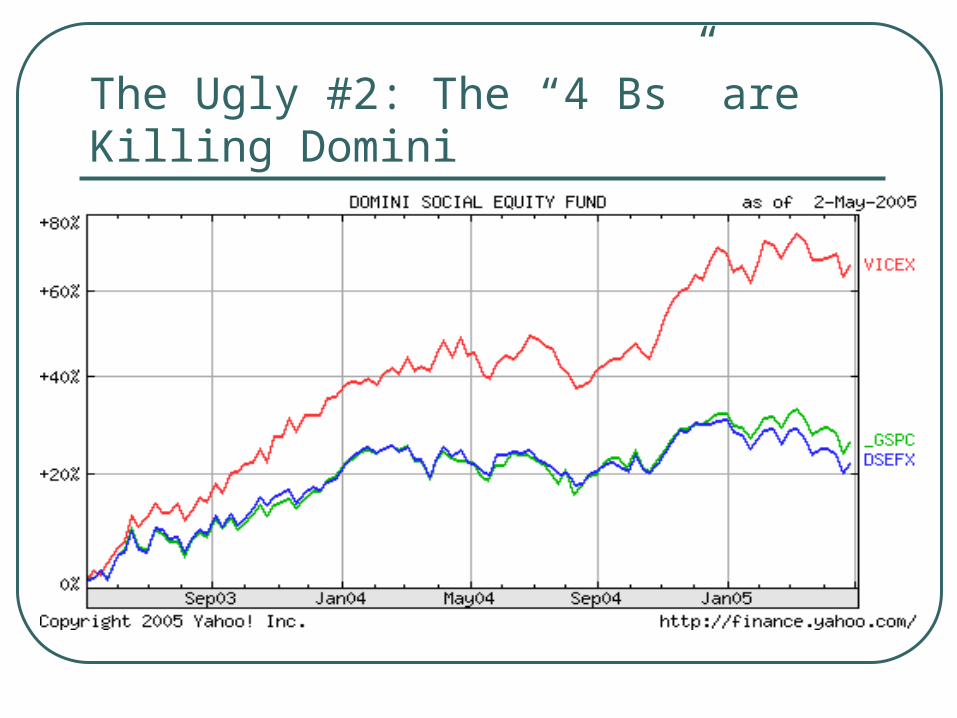

The Ugly #2: The “4 Bs” are Killing Domini

So, How do they perform? Girard, Rahman and Stone (2005): “Between

and within financial performance” Entine (2003) and Geczym, Stambaugh and

Levin, 2003 report that SRI constraint imposes large costs on investors.

Orlitzky, Schmidt and Rynes (2003): “There is a positive association between corporate social performance and financial performance.” It would take “1,000 papers” to change the overall conclusions of their research.

Our methodology We use monthly return in 117 Socially Responsible

Mutual Funds from 1984 to 2003 to investigate:• Selectivity--the ability to select “better securities” (as

compared to Lippers benchmark)• Diversification-- the cost associated with poor

diversification (as compared to Lippers benchmark)• Net Selectivity-- the “true” cost associated with an

investment product • Market timing-- the ability to accurately overweight

(underweight) cash in the expectation of bearish (bullish) market.

Time and cross-sectional analysis of performance

The Model

gminTiMarket

t,pt,ft,mppt,ft,p )RR(RR

ySelectivitNetationDiversific

)RR()( t,ft,mpt,m

t,p

)RR()RR( t,ft,mt,m

t,pt,ft,p

tptftmptftmpptftp RRRRRR ,2

,,,,,, )()(

ySelectivit

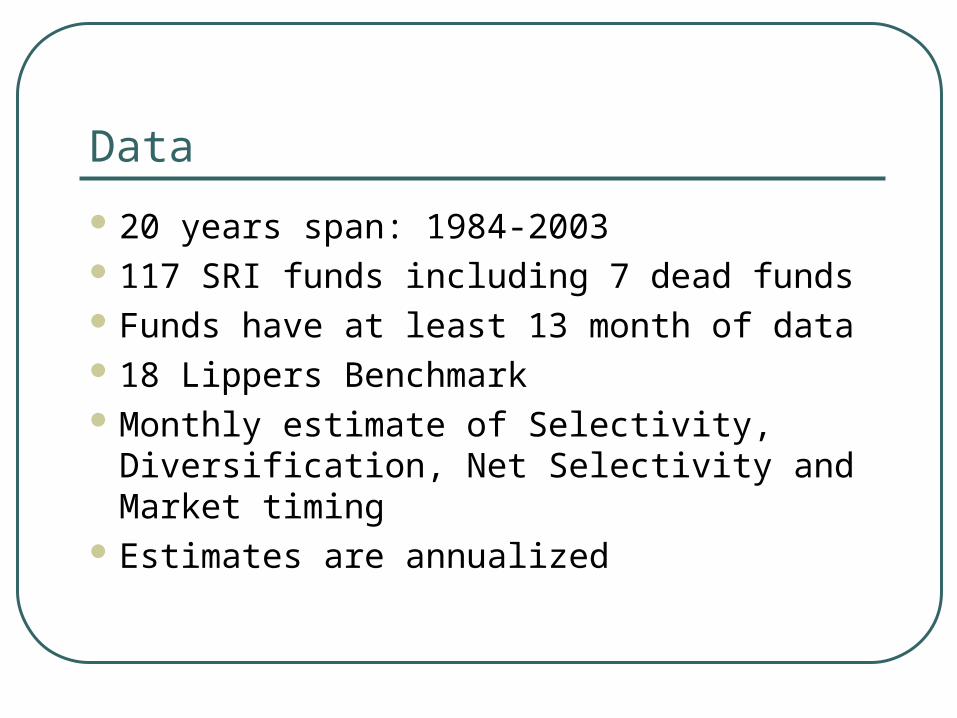

Data

20 years span: 1984-2003 117 SRI funds including 7 dead funds Funds have at least 13 month of data 18 Lippers Benchmark Monthly estimate of Selectivity,

Diversification, Net Selectivity and Market timing

Estimates are annualized

Findings: Net Selectivity

Net Selectivity (# of Months)

10 years (121)

5 Years (180)

3 Years (203)

1 year (228)

All funds -9.32%*** -8.75%*** -8.00%*** -7.34% Equity Funds -8.74%*** -8.10%* -8.49% -7.86%

Balanced Funds -8.80%*** -7.89%** -7.51%* -9.10% Bond Funds -7.19%*** -7.12%*** -7.06%*** -6.98%**

Selectivity and Net Selectivity Over Time (5-year span)

-0.14

-0.12

-0.1

-0.08

-0.06

-0.04

-0.02

0

0.02

0

10

20

30

40

50

60

70

Selectivity

Net Selectivity

# of Funds

Market Timing (5-year span)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

-5

-4

-3

-2

-1

0

1

2

3

4

5% with significant positive market timing

% with significant negative market timing ability

Market timing Ability

Determinants of Performance: Size and Age

Three-year Average (Constant)

Size # of Month

N (obs)

Selectivity -0.060*** 0.00000049 -0.00026575* 88 Diversification -0.068*** -0.0000001 0.0006773*** 88 Net Selectivity 0.009 0.00000059 -0.00041152*** 88 Market Timing -2.726 0.0000564 0.0156603 88

Determinants of Performance: Ethical Screens and Activism

Three-year Average (Constant) # of Screens Proxy Voting N (obs) Selectivity 0.042* -0.01526105** 0.01128622 58

Diversification -0.004 -0.0050942 0.0448974 58 Net Selectivity 0.046** -0.01016690* -0.03361118 58 Market Timing -1.116 -0.1042311 2.0183459 58

In sum We find evidence of poor selectivity, net selectivity and

market timing ability on the part of socially responsible mutual fund managers.

We also find that the size of the fund has nothing to do with its performance.

Older funds tend to have worse selectivity, as well as the highest cost for a lack of diversification.

SRMF with the most ethical screens have the least selectivity and net selectivity.

SRMF bear a significant cost for their lack of diversification, which cannot be legitimately related to the screening.

Conclusion Is it possible to maintain economic returns

while expressing a social concern about corporate conduct?

In accordance with modern portfolio theory, we find that a social responsible constraint entails a cost in the form of a lower reward-to-risk (diversification cost) and this cost can be viewed as a contribution to the cause. However, our paper also shows that SRMF entails costs associated with poor portfolio management skills, this cost is unnecessary and cannot be justified by any ideology.

On the Future of SRMF… Our findings concur with Levine (2003) who contends that

the SRI industry fails to incorporate reliable, objective standards for measuring a firm’s corporate social performance into commonly used ratings or other approaches of assessment.

Individuals that perform the social screening task for their customers do so using subjective, proprietary, and ‘secret’ methodologies.

Simply put, the proprietary ‘black box’ approach, with its inherent subjectivity and lack of transparency, brings into question the validity of screening methodologies being used and the very legitimacy of the business of SRI.

They have to make a choice

The SRI industry is in between 2 chairs:• Client wealth maximization

• Social wealth maximization

They need to choose

Future Research?

Is there a Social Risk factor that explains the return generating process of individual stocks?

Unlikely…or it would have a negative loading

We definitely cannot measure it as the difference between social benchmark and non-social benchmark Returns

As Abraham Lincoln said…

“It has been my experience that folks who have no vices have very few virtues”