one word makes all the difference - tulsa chapter of the … presentation.pdf · values for risky...

TRANSCRIPT

One Word Makes All the Difference: Updates in Fair Market Value & Fair Value

Oklahoma Society of Certified Public Accountants CPE Tulsa, Oklahoma

Glenn D. Vestrat, CVA, MBA

June 1, 2016

Presented by:

S. Christopher Lopp, CPA/ABV/CGMA, CFE, MBA

About HoganTaylor

HoganTaylor is one of the largest CPA firms in the Oklahoma and Arkansas region with more than 200 professionals and employees, including 29 partners.

HoganTaylor has offices in Oklahoma City, Tulsa, Fayetteville, and Little Rock.

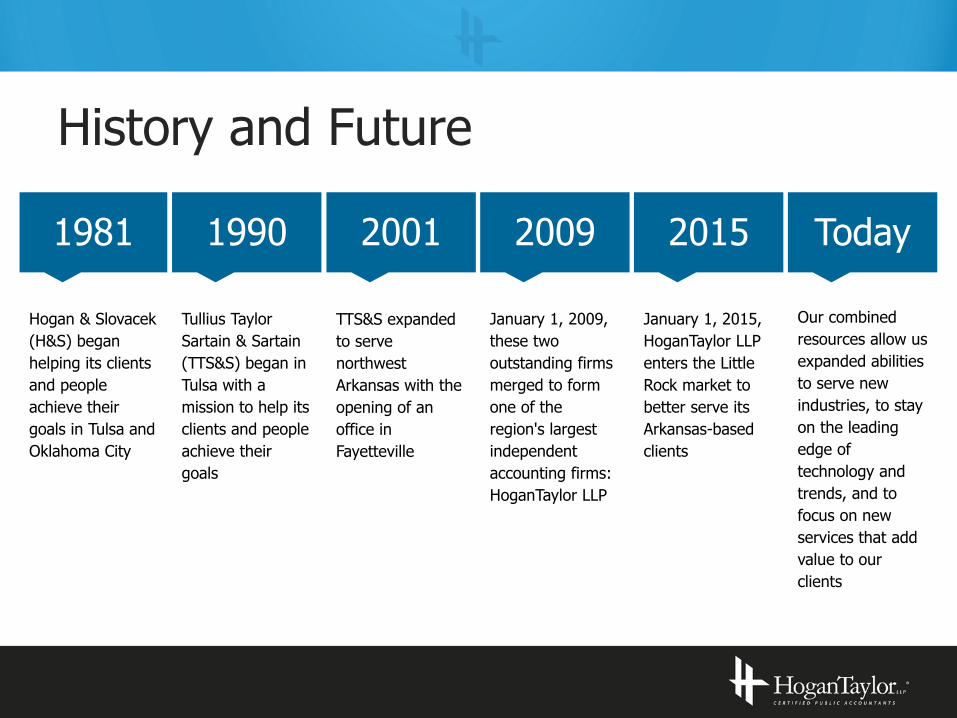

History and Future

1981 2001 1990 2009 Today

Hogan & Slovacek

(H&S) began

helping its clients

and people

achieve their

goals in Tulsa and

Oklahoma City

Tullius Taylor

Sartain & Sartain

(TTS&S) began in

Tulsa with a

mission to help its

clients and people

achieve their

goals

TTS&S expanded

to serve

northwest

Arkansas with the

opening of an

office in

Fayetteville

January 1, 2009,

these two

outstanding firms

merged to form

one of the

region's largest

independent

accounting firms:

HoganTaylor LLP

Our combined

resources allow us

expanded abilities

to serve new

industries, to stay

on the leading

edge of

technology and

trends, and to

focus on new

services that add

value to our

clients

2015

January 1, 2015,

HoganTaylor LLP

enters the Little

Rock market to

better serve its

Arkansas-based

clients

What We Do

HoganTaylor is comprised of professionals who continually demonstrate they are adept at providing services that are on time and well managed to a wide range of business types and specialized industries.

• Litigation Support • Outsourced CFO Services • Risk Assurance • Tax Services • Wealth Management

• Accounting Solutions • Advisory Services • Assurance • Business Valuation • Employee Benefit Plans • Human Capital and

Organizational Strategies

Who We Serve

• Collective Trust Funds

• Construction

• Energy

• Financial Institutions

• Information Technology Services

• Insurance

• Manufacturing and Distribution

• Nonprofit

• Retail

• Transportation

Our focus on key industries ensures we offer our clients specialized expertise and an understanding of important industry trends and issues. Our principal industry expertise includes:

Structure for Today

Updates in Two Widely Used Standards of Value:

• Fair Market Value – Business Valuations

• Fair Value – Financial Reporting

Fair Market Value Defined

“The fair market value is the price at which the property would change hands between a willing buyer and a willing seller, neither being under any compulsion to buy or to sell and both having reasonable knowledge of relevant facts.”

IRS Title 26, Section 20.2031-1, Chapter 1(B)

References

• Revenue Ruling 59-60:

“The purpose of this Revenue Ruling is to outline and review in general the approach, methods and factors to be considered in valuing shares of the capital stock of closely held corporations for estate tax and gift tax purposes.”

Application

Court decisions frequently state, in addition, that the hypothetical buyer and seller are assumed to be able, as well as willing, to trade and to be well informed about the property and concerning the market for such property.

Typical Purposes

• Income tax valuations

• Gift

• Estate

• Inheritance taxes

• Charitable contributions

• Employee Stock Ownership Plans (ESOPs)

• Purchase or sale of a business

Standards of Value

Answers the question:

“Value to Whom?”

UPDATE: Risk-Free Rate Debate

• Risk-free rate used in estimating cost of equity capital:

• Can be used in a cost of capital build-up method

• Build-up method origins based on Capital Asset Pricing Model (CAPM)

• Can only be inferred for a private company

• Is typically equal to the 20 year U.S. Treasury yield

UPDATE: Risk-Free Rate Debate Consequences of the financial crisis beginning in 2008:

1. Flight to safety

2. Prices on U.S. Treasury bonds increased and yields decreased

3. At the same time, equity prices decreased

4. Yield for 20 year U.S. Treasury bond decreased to 3%

5. New normal?

UPDATE: Risk-Free Rate Debate

UPDATE: Risk-Free Rate Debate

• Thought leaders (such as Roger Grabowski, et al.) handle the apparent contradiction by normalizing the Risk-Free Rate

• Recommended Risk-Free Rate:

• As of January 31, 2016 = 4.0%

Duff & Phelps Client Alert

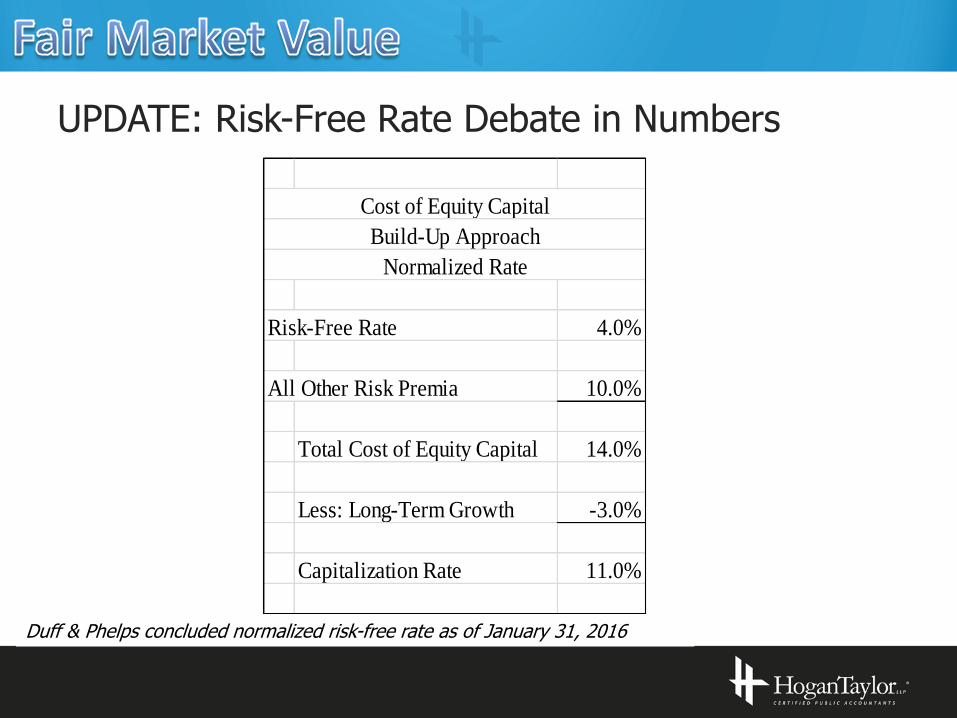

UPDATE: Risk-Free Rate Debate in Numbers

Cost of Equity Capital Cost of Equity Capital

Build-Up Approach Build-Up Approach

Spot Rate Normalized Rate

Risk-Free Rate 2.2%

All Other Risk Premia 10.0%

Total Cost of Equity Capital 12.2%

Less: Long-Term Growth -3.0%

Capitalization Rate 9.2%

U.S. Treasury yield, 20 year, February 26, 2016

UPDATE: Risk-Free Rate Debate in Numbers

Cost of Equity Capital

Build-Up Approach

Normalized Rate

Risk-Free Rate 4.0%

All Other Risk Premia 10.0%

Total Cost of Equity Capital 14.0%

Less: Long-Term Growth -3.0%

Capitalization Rate 11.0%

Duff & Phelps concluded normalized risk-free rate as of January 31, 2016

UPDATE: Risk-Free Rate Debate in Numbers

Capitalization Example Capitalization Example

Build-Up Approach Build-Up Approach

Spot Rate Normalized Rate

Annualized Cash Flow 100,000$

Capitalization Rate 9.2%

Indication of Value 1,086,957$

UPDATE: Risk-Free Rate Debate in Numbers

Capitalization Example Capitalization Example

Build-Up Approach Build-Up Approach

Normalized Rate Difference in Value

Annualized Cash Flow 100,000$

Capitalization Rate 11.0%

Indication of Value 909,091$

UPDATE: Risk-Free Rate Debate in Numbers

Capitalization Example

Build-Up Approach

Difference in Value

Indication of Value - Spot Rate 1,086,957$

Indication of Value - Normalized Rate 909,091

Difference in Value 177,866

Percentage difference in Value 16%

UPDATE: Risk-Free Rate Debate • The future… a continued debate

“… a valuation is an assessment of the future as of a point in time. As such, if the valuation date is today, then you should use the current risk-free rate… lower risk-free rates do not always translate into higher values for risky assets, and it is not necessarily a problem that needs to be solved. It is important to approach all the internal components and external macro-components separately and collectively in order to create the most consistent model possible.”

Kevin Piccolo, ASA, The Value Examiner, March/April 2012

Fair Value Defined

“Fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date.”

ASC Topic 820, Fair Value Measurement

Fair Market Value Defined

“The fair market value is the price at which the property would change hands between a willing buyer and a willing seller, neither being under any compulsion to buy or to sell and both having reasonable knowledge of relevant facts.”

IRS Title 26, Section 20.2031-1, Chapter 1(B)

Mandatory Performance Framework

The Exposure Draft incorporates the joint standards for how to perform a valuation based on those followed by:

1. American Institute of Certified Public Accountants (AICPA) – Statement on Standards for Valuation Services No. 1, Valuation of a Business, Business Ownership Interest, Security, or Intangible Asset (SSVS No. 1)

2. American Society of Appraisers (ASA) – ASA Business Valuation Standards. The Business Valuation Standards of the American Society of Appraisers are used in conjunction with the Uniform Standards of Professional Appraisal Practice (USPAP) of The Appraisal Foundation, and the Principles of Appraisal Practice and Code of Ethics of the American Society of Appraisers

3. Royal Institution of Chartered Surveyors (RICS) – RICS Valuation – Professional Standards incorporate the International Valuation Standards (IVS)

Differences in Definitions of Fair Value and Fair Market Value

• Fair value specifically applies to any engagement, or part of an engagement, that involves estimating the fair value of a subject interest to serve as a basis for management’s preparation of financial statements for public interest reporting

• Fair value considers both assets and liabilities

• Fair value has an exit price assumption and excludes transaction costs

• Fair value requires the consideration of value in various markets and to different types of buyers (i.e. strategic vs. financial)

Fair Value of Liabilities

• ASC Topic 820 assumes that liabilities are transferred to a market participant as of the measurement date, and the liability continues in existence to the counterparty

• The present value of all of the future payments are discounted back at the market discount rate applicable to the risk of the acquired company

• If the company making the acquisition has a better credit rating than the company being acquired, the fair value of the liability will increase, resulting in a charge against earnings and an increase in the balance sheet value of the liability on a re-measurement date

• This is highly controversial, but the desire to have both sides of the transaction reporting the same value is dictating the approach

Exit Price Assumption

• Requires valuation professional to measure amount that would be received if asset were sold, or paid if liability were settled, which does not necessarily equal the transaction price

• For example: if you were measuring the value of a commodity position and it were an asset (long position), you would use the published bid price, but if it were a liability (short position), you would use the published ask price

• Assumption is debatable, especially as it relates to the measurement of the value of liabilities when lower credit ratings reduce the price to settle the liability, which, in turn, leads to paper gains as a reward for having a lower credit rating

Consideration of the Market Fair value must be measured in the principal market, if there is one. If there is not, then the asset or liability must be valued in the most advantageous market that the company is able to access.

• Principal market:

• the market with the greatest level of volume, or

• the market that the entity generally uses

• Transaction costs:

• are not factored into the final determination of fair value

• are considered in the determination of the most advantageous market

• Transportation costs:

• considered a deduction to fair value (i.e. costs to truck product to market or pipeline tariffs)

Market Example Most advantageous market - the market that maximizes the amount that would be received to sell the asset, or minimizes the amount that would be paid to transfer the liability, after taking into account transaction costs and transportation costs.

• Example: Blue company acquires Green company in a business combination. Green has on its balance sheet an investment in the common stock of Purple company, which is traded on the New York Stock Exchange and the Toronto Exchange as follows:

Exchange Price Transaction Cost Net

NYSE $40 $6 $34

Toronto $38 $2 $36

What is the fair value of the common stock of Purple?

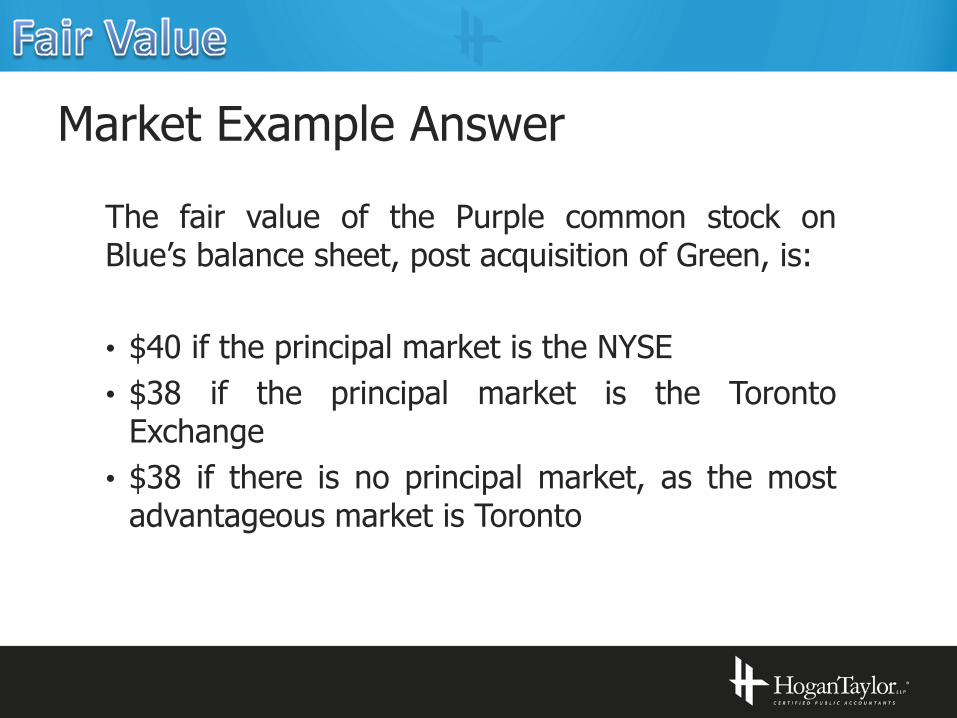

Market Example Answer

The fair value of the Purple common stock on Blue’s balance sheet, post acquisition of Green, is:

• $40 if the principal market is the NYSE

• $38 if the principal market is the Toronto Exchange

• $38 if there is no principal market, as the most advantageous market is Toronto

Related Accounting Standards The following accounting standards are issued by Financial Accounting Standards Board (FASB), and are common subject interest topics that may be applicable when a company engages a valuation professional (not an all-inclusive list):

• ASC 350 – Intangibles – Goodwill and Other

• ASC 360 – Property, Plant, and Equipment (specifically long- lived asset impairment)

• ASC 606 – Revenue from Contracts with Customers

• ASC 718 – Compensation – Stock Compensation

• ASC 805 – Business Combinations

• ASC 820 – Fair Value Measurement

• ASC 825 – Financial Instruments

• ASC 946 – Financial Services – Investment Companies

Source: Proposed Mandatory Performance Framework for the Fair Value Quality Initiative

Related Accounting Standards Valuation professionals should also be aware of auditing standards used by the audit profession as guidance when they conduct an audit of financial statements prepared for public interest reporting. These include, but are not be limited to:

• AS 1105 – Audit Evidence (to supersede AS No.15)

• AS 1210 – Using the Work of a Specialist (to supersede AU 336)

• AS 1215 – Audit Documentation (to supersede AS No.3)

• AS 2501 – Auditing Accounting Estimates (to supersede AU 342)

• AS 2502 – Auditing Fair Value Measurement and Disclosure

(to supersede AU 328)

Source: Proposed Mandatory Performance Framework for the Fair Value Quality Initiative

Questions?

HoganTaylor LLP Tulsa office: (918) 745-2333 OKC office: (405) 848-2020

Fayetteville office: (479) 521-9191 Little Rock office: (501) 227-4343

www.hogantaylor.com

Disclaimer The information contained within this presentation is provided for informational purposes only and is not intended as rendering of accounting, tax, financial, or legal services. Information in these slides was intended for a specific training purpose on a specific date and may not be used or relied upon outside of the context of this training.