open enrollment - d13ak21c8422ai.cloudfront.net · for everything you need to know about open...

TRANSCRIPT

Find out what’s new or changing for 2013

Open Enrollment

Guide

t’s Open Enrollment – the time each year for you to elect, change or cancel your health care coverage and other benefit options for yourself and your dependents for the upcoming plan year.

This year’s Open Enrollment period is Oct. 1-19, 2012, midnight Eastern time. Elections or changes ofhealth care coverage are effective Jan. 1, 2013.* Cancellations are effective Dec. 31, 2012.

IMPORTANT:• If you have medical, dental, vision, disability or life insurance in 2012, you will automatically be enrolled in the sameplan for 2013 unless you elect otherwise during Open Enrollment. If you want to change or cancel your coverage for2013, you must do so during Open Enrollment. If you have a flexible spending account in 2012, you must elect oneduring Open Enrollment if you wish to have one in 2013.

• If you’re a full-time Team Member electing a major medical plan, you will be asked to identify yourself as a tobacco useror non-tobacco user. A tobacco user is someone who has used any tobacco product, even once, within the last six months.

• If you’re a full-time Team Member who currently has major medical coverage in 2012 and you do not activelychoose a major medical plan or cancel your 2013 major medical plan during Open Enrollment, you will automaticallybe enrolled in the same major medical plan for 2013 and receive the tobacco-user surcharge because you will not haveidentified yourself as a tobacco user or non-tobacco user.

• The tobacco-user surcharge means $16 weekly ($32 bi-weekly) will be added to your major medical premium in 2013.*For Team Members on a leave of absence January 1, 2013, critical illness insurance, dental care, short-term/long-term disability insurance,voluntary life, basic life and accidental death and dismemberment insurance become effective upon their return to work.

During Open Enrollment...

FULL-TIME TEAM MEMBERS* ARE ELIGIBLE TO ELECT:Benefit More Information On:Major medical care through BlueCross BlueShield of North Carolina, which includes Prescription Drug coverage..........................................page 6Limited Medical care through Nationwide...........................................page 16Dental care through MetLife...............................................................page 18Vision care through EyeMed..............................................................page 19Flexible Spending Accounts through PayFlex....................................... page 20Voluntary Life insurance through The Hartford......................................page 22Short-term/Long-term Disability insurance through The Hartford.............page 23Critical Illness insurance through Unum...............................................page 24

PART-TIME TEAM MEMBERS* ARE ELIGIBLE TO ELECT:Benefit More Information On:Limited Medical care through Nationwide...........................................page 16Dental care through MetLife...............................................................page 18Vision care through EyeMed..............................................................page 19Voluntary Life insurance through The Hartford......................................page 22Critical Illness insurance through Unum...............................................page 24

* Temporary Team Members may elect Limited Medical care only.

Para obtener una copia en español de la guía de inscripción abierta contáctenos a través de “Ask HR” visitando MyFamilyDollarLife.com, haga click en “Ask HR” en el Store Portal o RedZone, la intranet de nuestra empresa, o bien llame al Centro de Contacto de Recursos Humanos de lunes a viernes de 8am a 8pm (hora del este) al 1-866-377-6420.

I

1

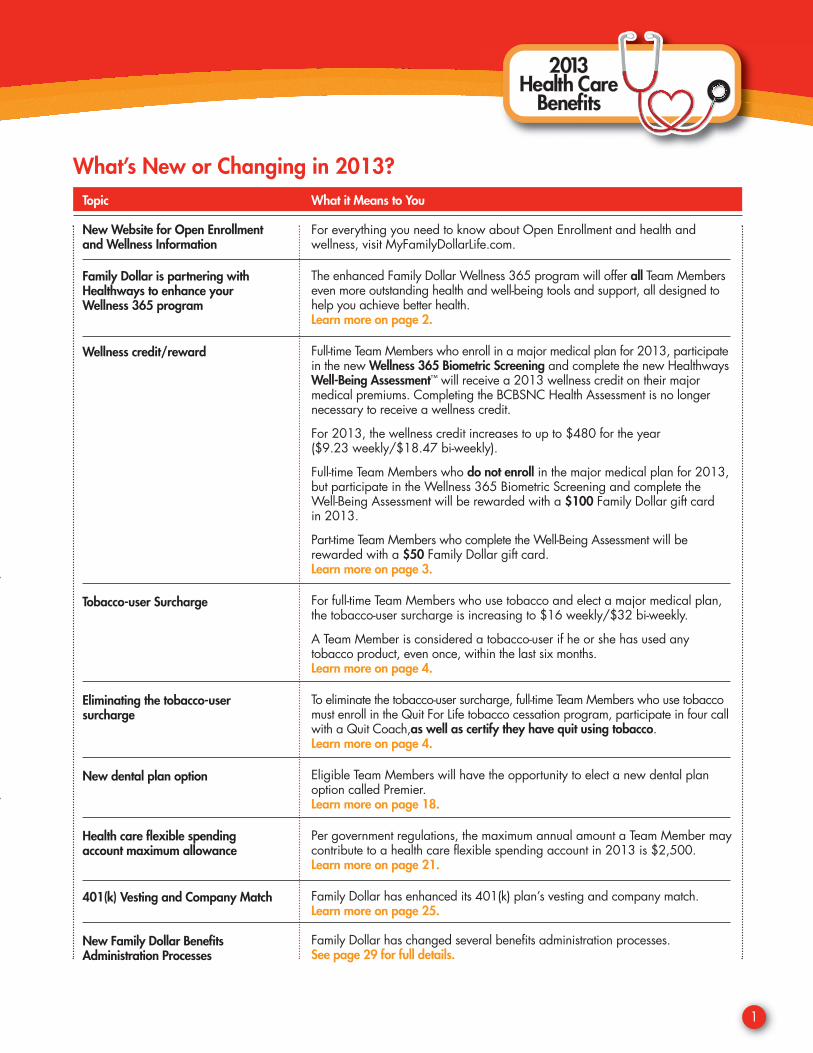

What’s New or Changing in 2013?What it Means to You

For everything you need to know about Open Enrollment and health and wellness, visit MyFamilyDollarLife.com.

The enhanced Family Dollar Wellness 365 program will offer all Team Memberseven more outstanding health and well-being tools and support, all designed tohelp you achieve better health.Learn more on page 2.

Full-time Team Members who enroll in a major medical plan for 2013, participatein the new Wellness 365 Biometric Screening and complete the new Healthways Well-Being Assessment™ will receive a 2013 wellness credit on their major medical premiums. Completing the BCBSNC Health Assessment is no longernecessary to receive a wellness credit.

For 2013, the wellness credit increases to up to $480 for the year ($9.23 weekly/$18.47 bi-weekly).

Full-time Team Members who do not enroll in the major medical plan for 2013,but participate in the Wellness 365 Biometric Screening and complete the Well-Being Assessment will be rewarded with a $100 Family Dollar gift card in 2013.

Part-time Team Members who complete the Well-Being Assessment will be rewarded with a $50 Family Dollar gift card.Learn more on page 3.

For full-time Team Members who use tobacco and elect a major medical plan,the tobacco-user surcharge is increasing to $16 weekly/$32 bi-weekly.

A Team Member is considered a tobacco-user if he or she has used any tobacco product, even once, within the last six months.Learn more on page 4.

To eliminate the tobacco-user surcharge, full-time Team Members who use tobaccomust enroll in the Quit For Life tobacco cessation program, participate in four callwith a Quit Coach,as well as certify they have quit using tobacco.Learn more on page 4.

Eligible Team Members will have the opportunity to elect a new dental plan option called Premier. Learn more on page 18.

Per government regulations, the maximum annual amount a Team Member maycontribute to a health care flexible spending account in 2013 is $2,500.Learn more on page 21.

Family Dollar has enhanced its 401(k) plan’s vesting and company match. Learn more on page 25.

Family Dollar has changed several benefits administration processes. See page 29 for full details.

Topic

New Website for Open Enrollment and Wellness Information

Family Dollar is partnering with Healthways to enhance your Wellness 365 program

Wellness credit/reward

Tobacco-user Surcharge

Eliminating the tobacco-user surcharge

New dental plan option

Health care flexible spending account maximum allowance

401(k) Vesting and Company Match

New Family Dollar Benefits Administration Processes

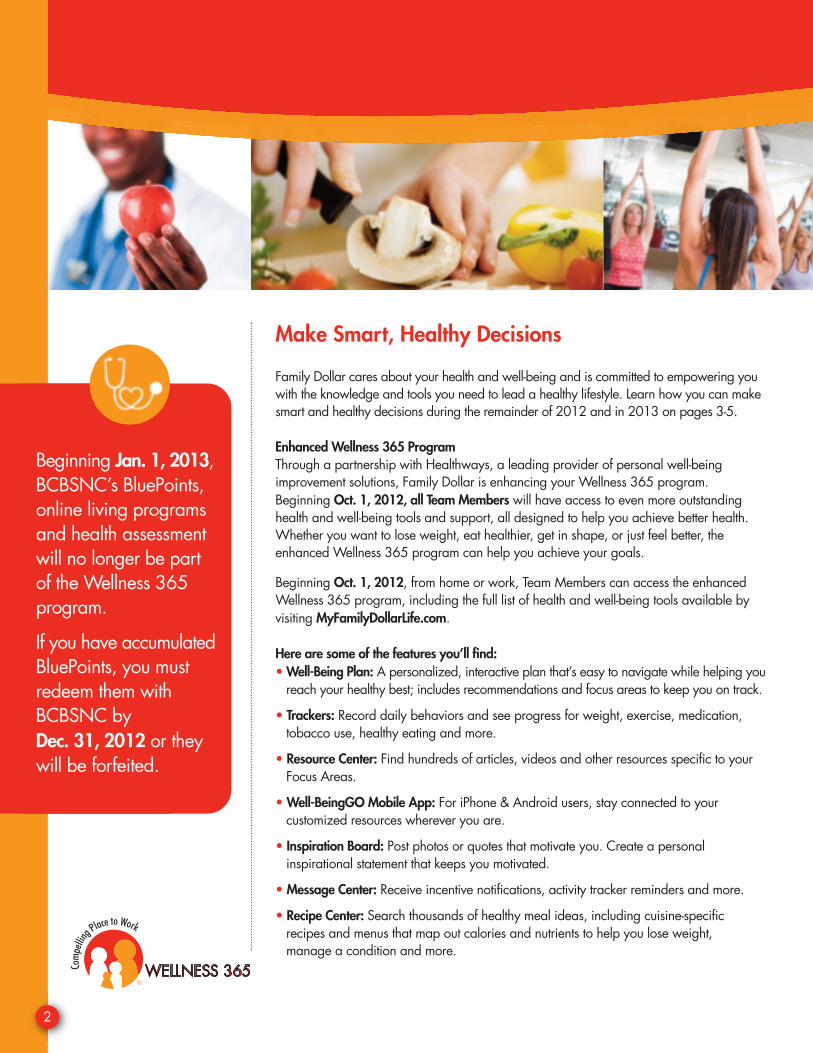

Make Smart, Healthy Decisions

Family Dollar cares about your health and well-being and is committed to empowering youwith the knowledge and tools you need to lead a healthy lifestyle. Learn how you can makesmart and healthy decisions during the remainder of 2012 and in 2013 on pages 3-5.

Enhanced Wellness 365 ProgramThrough a partnership with Healthways, a leading provider of personal well-being improvement solutions, Family Dollar is enhancing your Wellness 365 program. Beginning Oct. 1, 2012, all Team Members will have access to even more outstandinghealth and well-being tools and support, all designed to help you achieve better health.Whether you want to lose weight, eat healthier, get in shape, or just feel better, the enhanced Wellness 365 program can help you achieve your goals.

Beginning Oct. 1, 2012, from home or work, Team Members can access the enhancedWellness 365 program, including the full list of health and well-being tools available byvisiting MyFamilyDollarLife.com.

Here are some of the features you’ll find: • Well-Being Plan: A personalized, interactive plan that’s easy to navigate while helping you

reach your healthy best; includes recommendations and focus areas to keep you on track.

• Trackers: Record daily behaviors and see progress for weight, exercise, medication, tobacco use, healthy eating and more.

• Resource Center: Find hundreds of articles, videos and other resources specific to your Focus Areas.

• Well-BeingGO Mobile App: For iPhone & Android users, stay connected to your customized resources wherever you are.

• Inspiration Board: Post photos or quotes that motivate you. Create a personal inspirational statement that keeps you motivated.

• Message Center: Receive incentive notifications, activity tracker reminders and more.

• Recipe Center: Search thousands of healthy meal ideas, including cuisine-specificrecipes and menus that map out calories and nutrients to help you lose weight, manage a condition and more.

2

Beginning Jan. 1, 2013,BCBSNC’s BluePoints,online living programsand health assessmentwill no longer be partof the Wellness 365program.

If you have accumulatedBluePoints, you must redeem them with BCBSNC by Dec. 31, 2012 or theywill be forfeited.

3

Participate in a Biometric Screening + Complete Well-Being Assessment = Reward

Through a partnership with Healthways, a leading provider of well-being improvement solutions, full-time Family Dollar Team Members have the opportunity to be rewarded for participating in the new Wellness 365 Biometric Screening and completing the Well-Being Assessment. If you have already participated in the Wellness 365 Biometric Screening and Healthways has your screening

information, congratulations! If you haven’t, it’s not too late. Choose one of threeways to participate in the screening:• Visit Your Physician

- Call 866-666-7434 to request a physician form. After you receive the form, have your doctor complete it and return it to Healthways.

• Visit a Quest Diagnostics Lab- To locate a lab near you and schedule your screening appointment, visit my.blueprintforwellness.com. The registration key is FAMILYDOLLAR2012.

• Order a Home Fingerstick Kit- Call 866-666-7434 to request a self-administered home kit be mailed to your home. Simply follow the instructions and mail the kit back in the return envelope provided.

A Biometric Screening is a safe, confidential and convenient way to help you understand the state of your health so you can take the necessary steps to improveit. The screening consists of body composition testing that measures your height,weight waist circumference and blood pressure, as well as a finger stick that collects a small blood sample to measure your glucose, triglyceride, total cholesterol, high density lipoprotein (HDL), low density lipoprotein (LDL) levels.

The Well-Being Assessment is a confidential questionnaire that assesses your physical, emotional and social health and how your lifestyle habits may affect youroverall well-being. It is important to answer all questions as accurately as possible.This ensures the results reflect your true health status.

When full-time Team Members take the Wellness 365 Biometric screening, not onlywill they learn more about their health, but if they also complete the Well-Being Assessment (available Oct. 1, 2012), they will earn a valuable reward. Part-timeTeam Members may also earn a reward for completing the Well-Being Assessment.Please see below:

• Full-time Team Members who enroll in a major medical plan for 2013:Participate in the Wellness 365 Biometric Screening and complete the Well-Being Assessment to receive a 2013 wellness credit on your major medical premiums. For 2013, the wellness credit increases to up to $480 for the year ($9.23 weekly/$18.47 bi-weekly).

• Full-time Team Members who do not enroll in the major medical plan for 2013*:Participate in the Wellness 365 Biometric Screening and complete the Well-Being Assessment to receive a $100 Family Dollar gift card in 2013.

• Part-time Team Members: Complete the Well-Being Assessment to receive a $50 Family Dollar gift card in 2013.*

*Team Members must be employed by Family Dollar at gift card distribution time in 2013.Gift card value is considered taxable income.

For full details, including participation instructions, please visit MyFamilyDollarLife.com.

Key Dates toRemember:Dec. 31, 2012Last day for full-time TeamMembers to get their biometricscreening physician form submitted to Healthways andto take the Well-Being Assessment to receive the full year (January - December2013) major medical planwellness credit.

June 30, 2013Last day for full-time TeamMembers to get their biometricscreening information toHealthways and to take theWell-Being Assessment toreceive any portion of the 2013major medical plan wellnesscredit or to receive their $100Family Dollar gift card.

Also, June 30, 2013is the last day for part-timeTeam Members to take the Well-Being Assessment to receive their $50 gift card.

4

Quit Tobacco, Save Money

To help Team Members kick the habit of using tobacco, your Wellness 365 program includes Quit ForLife, a free* tobacco cessation program available to all Team Members.

Quit For Life is recognized by the American Cancer Society as an effective tobacco cessation program.The program, through Alere Wellbeing, provides phone- and web-based support that can help you quittobacco use for good.

Full-time Team Members who use tobacco will eliminate the $16 weekly ($32 bi-weekly) tobacco usersurcharge on their major medical premiums by enrolling in the Quit For Life program, completing fourcalls with their Quit For Life Quit Coach and certifying they have quit using tobacco.

When you enroll in the Quit For Life program you have access to:

• Quit Coach – Access to highly trained Quit Coaches, many of whom have successfully quit using tobacco themselves. Quit Coaches are there to support you during your quest to quit tobacco. Quit Coaches are available via phone 8 a.m. – 3 a.m. Eastern time.

• Customized Quit Plan – Designed by your Quit Coach.

• Web Coach – Access to a private online community where you can complete activities, watch videos, track your progress and join in discussions with other people committed to quitting tobacco.

• Quit Guide – Easy-to-use printed workbook you can reference in any situation to help you stick with your tobacco quit plan.

• Quitting Aids – You have access to up to eight weeks of free nicotine replacement therapy (gum or patch).

*After enrolling in the Quit For Life program a total of three years, a Team Member will be charged for his/her participation.

To enroll in the Quit For Life program, call 1-866-QUIT-4-LIFE (1-866-784-8454). A registration specialist will verify eligibility to enroll and connect you with a Quit Coach to get started. To learn more, please visit MyFamilyDollarLife.com.

5

Health Line Blue

If your baby wakes up in the middle of the night with a fever, if you don’t know if youshould take certain medications together or if you have any other minor, non-emergency

issue and want professional medical advice, call Health Line Blue. It’s like having your own personal nurse 24 hours a day, seven days a week.

At no additional cost, Team Members who elect a major medicalplan with BCBSNC may call Health Line Blue. The Health LineBlue phone line is staffed by specially trained nurses who can answer your questions whenever you have them and direct you tothe care that’s right for you or your family.

Saving on Health Care Starts with Prevention

With everything going on in your life, it’s sometimes easy to forgetwhat’s really important. Like your health. So, even when you feelgreat, make sure you continue to get your check-ups and screen-ings – to be certain you are well and to help you stay that way.

Don’t have a primary care physician? You should find one –especially if you have a chronic health condition such as highblood pressure, diabetes, migraine or asthma. A primary carephysician who knows you and your medical background canhelp you prevent and treat conditions that may lead to extra costs

for you. To find a doctor who’s right for you, please visit bcbsnc.com/members/familydollarand click Provider Search.

Ask your doctor which preventive services are appropriate for you. Depending on your ageand sex, your preventive services may include the following:

• Annual physical exam• Blood pressure screening• Flu shot• Cholesterol screening• Mammogram

If you elect a BlueCross BlueShield of North Carolina (BCBSNC) major medical plan, a broad range of in-network preventive care services are covered at 100 percent.

“What kind of physical benefits might I experience ifI eat healthy and exercise?”

Regular workouts and eatinghealthy may help fight off coldsand flu, reduce the risk of certain cancers and chronic diseases and slow the process ofaging. In addition, you will haveincreased energy and strength.

Ask a Wellness 365Health Coach

6

Major Medical Plans

Who’s Eligible?All full-time Team Members and their eligible dependents

Family Dollar offers a variety of major medical plans that fit your needs. For 2013, full-time TeamMembers will have three major medical plans through BCBSNC from which to choose:

• Consumer Advantage with Health Savings Account• Core PPO• Core Plus PPO

When you elect a major medical plan, you will receive a BCBSNC Member ID card. This cardshould be shown to your health care provider at the time of your visit or pharmacist when purchasing prescription drugs. If you are a currently enrolled Team Member, you will not receive a new BCBSNC medical ID card unless you change health care coverage elections.

When a Team Member elects a major medical plan he or she will choose a coverage tier:

• Team Member• Team Member + Spouse/Same-sex Domestic Partner • Team Member + Child(ren) • Team Member + Family

Continue reading for details on each major medical plan. BlueCross BlueShield of North Carolina requires

prior review for certain services and procedures,including high-tech diagnostic imaging such as CTscans, MRIs and PET scans. Please visitbcbsnc.com/memberservices/public/ppa for acomplete list of services and procedures and formore information about what your doctor needs todo to complete the prior review process.

7

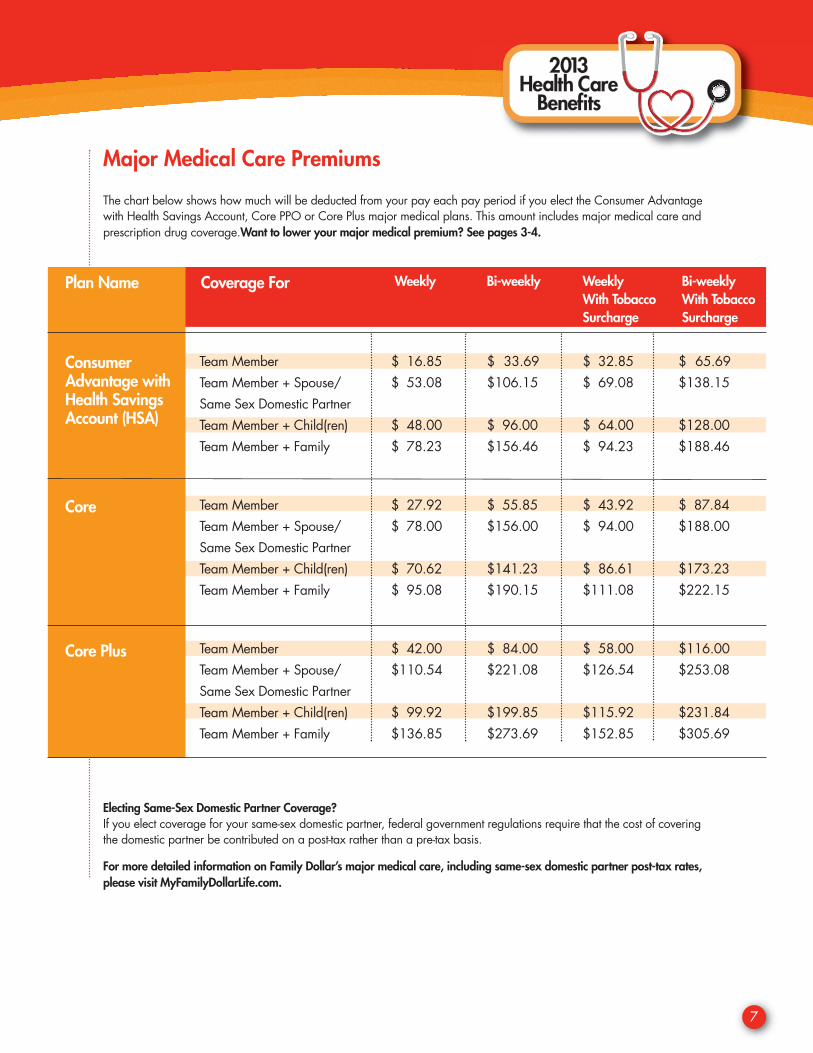

Major Medical Care Premiums

The chart below shows how much will be deducted from your pay each pay period if you elect the Consumer Advantagewith Health Savings Account, Core PPO or Core Plus major medical plans. This amount includes major medical care andprescription drug coverage.Want to lower your major medical premium? See pages 3-4.

Electing Same-Sex Domestic Partner Coverage?If you elect coverage for your same-sex domestic partner, federal government regulations require that the cost of coveringthe domestic partner be contributed on a post-tax rather than a pre-tax basis.

For more detailed information on Family Dollar’s major medical care, including same-sex domestic partner post-tax rates,please visit MyFamilyDollarLife.com.

Coverage For: Weekly Bi-weekly Weekly Bi-weeklyWith Tobacco With TobaccoSurcharge Surcharge

Team Member $ 16.85 $ 33.69 $ 32.85 $ 65.69Team Member + Spouse/ $ 53.08 $106.15 $ 69.08 $138.15Same Sex Domestic PartnerTeam Member + Child(ren) $ 48.00 $ 96.00 $ 64.00 $128.00Team Member + Family $ 78.23 $156.46 $ 94.23 $188.46

Team Member $ 27.92 $ 55.85 $ 43.92 $ 87.84Team Member + Spouse/ $ 78.00 $156.00 $ 94.00 $188.00Same Sex Domestic PartnerTeam Member + Child(ren) $ 70.62 $141.23 $ 86.61 $173.23Team Member + Family $ 95.08 $190.15 $111.08 $222.15

Team Member $ 42.00 $ 84.00 $ 58.00 $116.00Team Member + Spouse/ $110.54 $221.08 $126.54 $253.08Same Sex Domestic PartnerTeam Member + Child(ren) $ 99.92 $199.85 $115.92 $231.84Team Member + Family $136.85 $273.69 $152.85 $305.69

ConsumerAdvantage withHealth SavingsAccount (HSA)

Plan Name Coverage For

Core

Core Plus

8

Consumer Advantage with Health Savings Account Plan

Who’s Eligible?All full-time Team Members and their eligible dependents

The Consumer Advantage with Health Savings Account plan is a consumer-driven health plan. “Consumer-driven” means you take more control over how you spend your health care dollars. Aswith the other plans, you can see any health care provider you wish, but you receive discountedrates when you visit a BCBSNC in-network provider.

Lower Per-Pay-Period PremiumsLess money is deducted from your pay for premiums under the Consumer Advantage with HealthSavings Account plan compared to the other major medical plans.

No Co-paysWhen you visit a health care provider such as a doctor, a specialist, hospital or emergency room,you are responsible for paying 100 percent of what the health care provider charges (after theBCBSNC discount if the provider is in network) until you have paid your annual deductible amount.The amount you pay your health care provider counts toward meeting your annual deductible.Once you have paid your annual deductible amount, the Consumer Advantage with Health Savings Account plan pays 100 percent of the allowable charges made by your health careprovider, and you will not be required to make any co-pays.

After Deductible Is Met, You Pay NothingUnder the Consumer Advantage with Health Savings Account plan, once the annual deductible foryou or any one of your covered family members is met, the plan pays 100 percent of all eligiblemedical expenses for you and your covered dependents, and you pay nothing!

For example, with the Consumer Advantage with Health Savings Account plan, if a child under yourplan meets the family’s annual deductible, for the rest of the year, the plan will pay 100 percent ofallowable charges for any other covered adults or children you have enrolled in the plan.

Family Dollar Helps You Meet Your DeductibleThe Consumer Advantage with Health Savings Account plan’s annual deductible is higher than the deductibles under other plans. However, Family Dollar helps pay for part of your deductible amount under the Consumer Advantage with Health Savings Account plan by contributing funds quarterly to your personal Health Savings Account.

9

You Have Greater ControlTeam Members who elect the Consumer Advantage with Health Savings Account plan feel a greater sense ofcontrol over when and how to use their health care dollars. Since the funds in their health savings account aretheirs to keep and it rolls over year to year, Team Members tend to be better health care consumers by takingadvantage of free in-network preventive screenings so they catch potential health risks before they becomedangers and shopping around by asking health care providers how much procedures cost before committing.

In-Network and Out-of-Network ExpensesJust like under a PPO plan, if you elect the Consumer Advantage with Health Savings Account plan you mayvisit in-network and out-of-network providers. To get the most for your health care dollars, you should alwaysstrive to visit in-network providers.

Just like under a PPO plan, the Consumer Advantage with Health Savings Account plan has an in-networkdeductible and an out-of-network deductible. The plan pays 100 percent of covered expenses for in-networkservices after you have paid your in-network deductible. The plan does not pay for any out-of-network services until you have paid your out-of-network deductible. Amounts you pay for in-network treatment counttoward meeting your in-network deductible. Amounts you pay for out-of-network treatment count towardmeeting your out-of-network deductible.

To learn what providers are considered in network, please visit bcbsnc.com/members/familydollar and clickProvider Search.

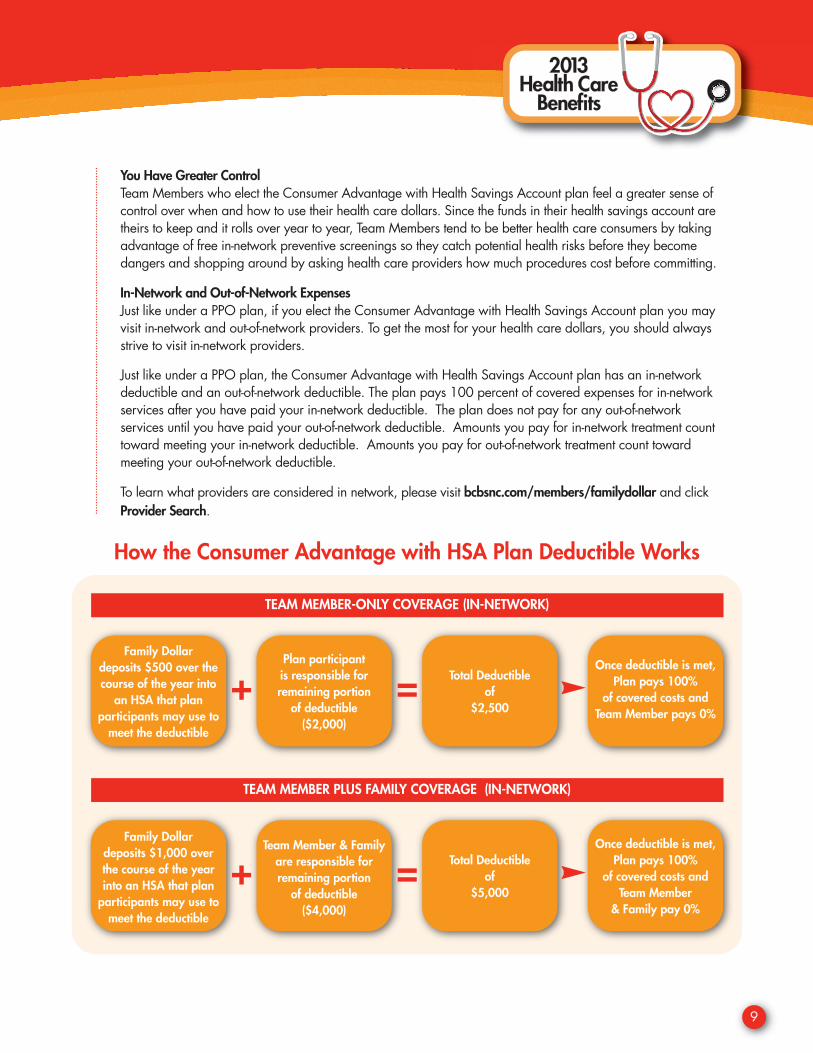

Family Dollardeposits $500 over thecourse of the year into

an HSA that plan participants may use to

meet the deductible

Plan participant is responsible for remaining portion

of deductible($2,000)

Total Deductibleof

$2,500

Once deductible is met, Plan pays 100%

of covered costs and Team Member pays 0%

+ =

Family Dollardeposits $1,000 over the course of the yearinto an HSA that plan

participants may use tomeet the deductible

Team Member & Family are responsible forremaining portion

of deductible($4,000)

Total Deductibleof

$5,000

Once deductible is met, Plan pays 100%

of covered costs and Team Member

& Family pay 0%

+ =

TEAM MEMBER-ONLY COVERAGE (IN-NETWORK)

TEAM MEMBER PLUS FAMILY COVERAGE (IN-NETWORK)

How the Consumer Advantage with HSA Plan Deductible Works

10

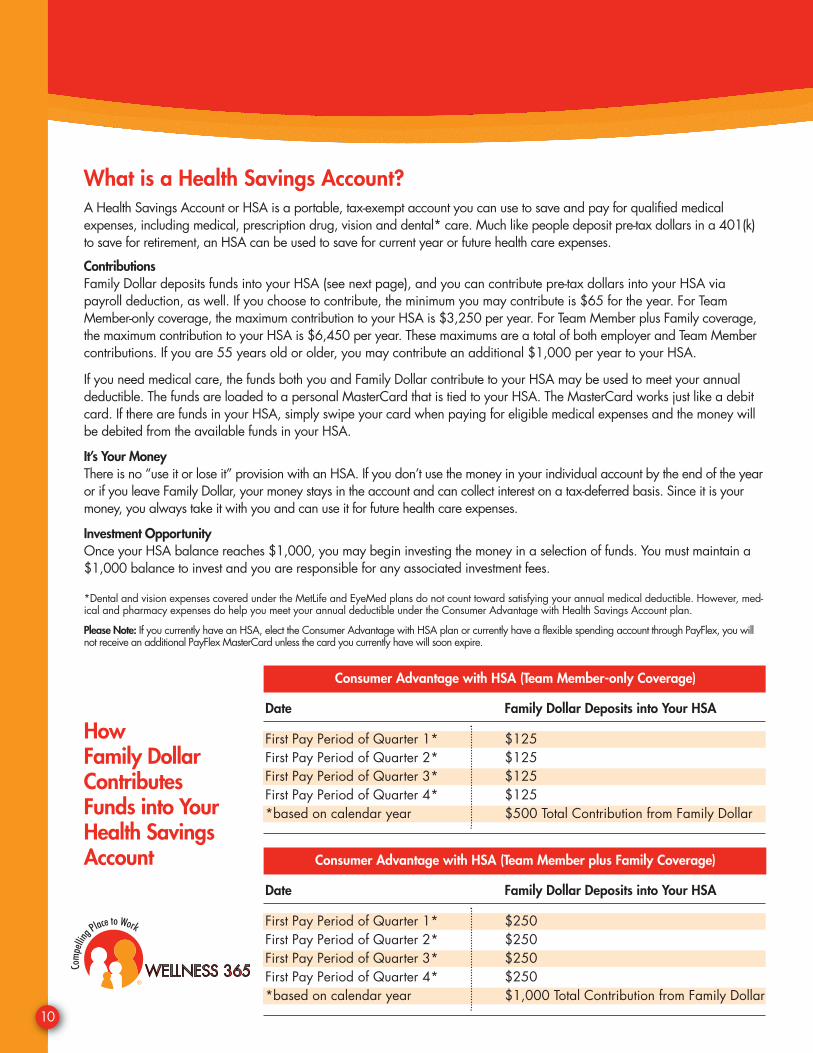

Date Family Dollar Deposits into Your HSA

First Pay Period of Quarter 1* $125First Pay Period of Quarter 2* $125First Pay Period of Quarter 3* $125First Pay Period of Quarter 4* $125*based on calendar year $500 Total Contribution from Family Dollar

Consumer Advantage with HSA (Team Member-only Coverage)

How Family DollarContributesFunds into YourHealth SavingsAccount

Date Family Dollar Deposits into Your HSA

First Pay Period of Quarter 1* $250First Pay Period of Quarter 2* $250First Pay Period of Quarter 3* $250First Pay Period of Quarter 4* $250*based on calendar year $1,000 Total Contribution from Family Dollar

Consumer Advantage with HSA (Team Member plus Family Coverage)

What is a Health Savings Account?A Health Savings Account or HSA is a portable, tax-exempt account you can use to save and pay for qualified medical expenses, including medical, prescription drug, vision and dental* care. Much like people deposit pre-tax dollars in a 401(k)to save for retirement, an HSA can be used to save for current year or future health care expenses.

ContributionsFamily Dollar deposits funds into your HSA (see next page), and you can contribute pre-tax dollars into your HSA via payroll deduction, as well. If you choose to contribute, the minimum you may contribute is $65 for the year. For Team Member-only coverage, the maximum contribution to your HSA is $3,250 per year. For Team Member plus Family coverage,the maximum contribution to your HSA is $6,450 per year. These maximums are a total of both employer and Team Membercontributions. If you are 55 years old or older, you may contribute an additional $1,000 per year to your HSA.

If you need medical care, the funds both you and Family Dollar contribute to your HSA may be used to meet your annual deductible. The funds are loaded to a personal MasterCard that is tied to your HSA. The MasterCard works just like a debitcard. If there are funds in your HSA, simply swipe your card when paying for eligible medical expenses and the money willbe debited from the available funds in your HSA.

It’s Your MoneyThere is no “use it or lose it” provision with an HSA. If you don’t use the money in your individual account by the end of the yearor if you leave Family Dollar, your money stays in the account and can collect interest on a tax-deferred basis. Since it is yourmoney, you always take it with you and can use it for future health care expenses.

Investment OpportunityOnce your HSA balance reaches $1,000, you may begin investing the money in a selection of funds. You must maintain a$1,000 balance to invest and you are responsible for any associated investment fees.

*Dental and vision expenses covered under the MetLife and EyeMed plans do not count toward satisfying your annual medical deductible. However, med-ical and pharmacy expenses do help you meet your annual deductible under the Consumer Advantage with Health Savings Account plan.

Please Note: If you currently have an HSA, elect the Consumer Advantage with HSA plan or currently have a flexible spending account through PayFlex, you willnot receive an additional PayFlex MasterCard unless the card you currently have will soon expire.

11

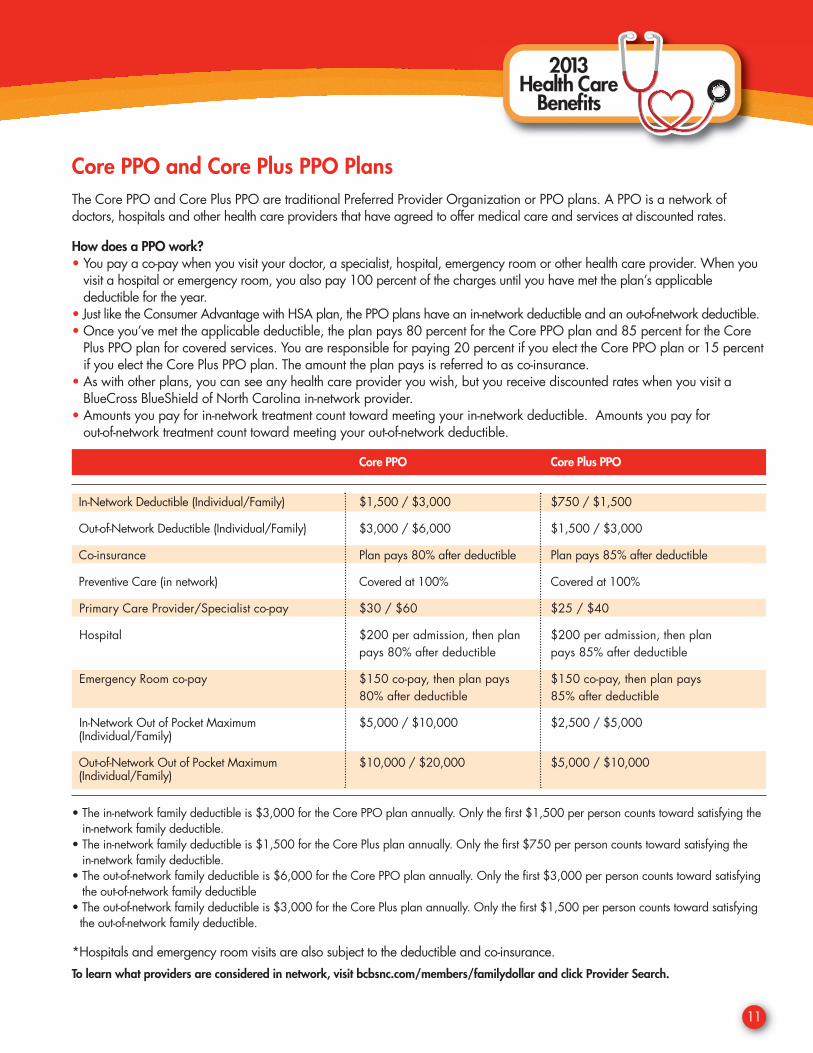

Core PPO and Core Plus PPO PlansThe Core PPO and Core Plus PPO are traditional Preferred Provider Organization or PPO plans. A PPO is a network of doctors, hospitals and other health care providers that have agreed to offer medical care and services at discounted rates.

How does a PPO work? • You pay a co-pay when you visit your doctor, a specialist, hospital, emergency room or other health care provider. When you

visit a hospital or emergency room, you also pay 100 percent of the charges until you have met the plan’s applicable deductible for the year.

• Just like the Consumer Advantage with HSA plan, the PPO plans have an in-network deductible and an out-of-network deductible.• Once you’ve met the applicable deductible, the plan pays 80 percent for the Core PPO plan and 85 percent for the Core

Plus PPO plan for covered services. You are responsible for paying 20 percent if you elect the Core PPO plan or 15 percentif you elect the Core Plus PPO plan. The amount the plan pays is referred to as co-insurance.

• As with other plans, you can see any health care provider you wish, but you receive discounted rates when you visit a BlueCross BlueShield of North Carolina in-network provider.

• Amounts you pay for in-network treatment count toward meeting your in-network deductible. Amounts you pay for out-of-network treatment count toward meeting your out-of-network deductible.

Core PPO Core Plus PPO

In-Network Deductible (Individual/Family) $1,500 / $3,000 $750 / $1,500

Out-of-Network Deductible (Individual/Family) $3,000 / $6,000 $1,500 / $3,000

Co-insurance Plan pays 80% after deductible Plan pays 85% after deductible

Preventive Care (in network) Covered at 100% Covered at 100%

Primary Care Provider/Specialist co-pay $30 / $60 $25 / $40

Hospital $200 per admission, then plan $200 per admission, then planpays 80% after deductible pays 85% after deductible

Emergency Room co-pay $150 co-pay, then plan pays $150 co-pay, then plan pays80% after deductible 85% after deductible

In-Network Out of Pocket Maximum $5,000 / $10,000 $2,500 / $5,000(Individual/Family)

Out-of-Network Out of Pocket Maximum $10,000 / $20,000 $5,000 / $10,000(Individual/Family)

• The in-network family deductible is $3,000 for the Core PPO plan annually. Only the first $1,500 per person counts toward satisfying thein-network family deductible.

• The in-network family deductible is $1,500 for the Core Plus plan annually. Only the first $750 per person counts toward satisfying the in-network family deductible.

• The out-of-network family deductible is $6,000 for the Core PPO plan annually. Only the first $3,000 per person counts toward satisfying the out-of-network family deductible

• The out-of-network family deductible is $3,000 for the Core Plus plan annually. Only the first $1,500 per person counts toward satisfying the out-of-network family deductible.

*Hospitals and emergency room visits are also subject to the deductible and co-insurance.To learn what providers are considered in network, visit bcbsnc.com/members/familydollar and click Provider Search.

12

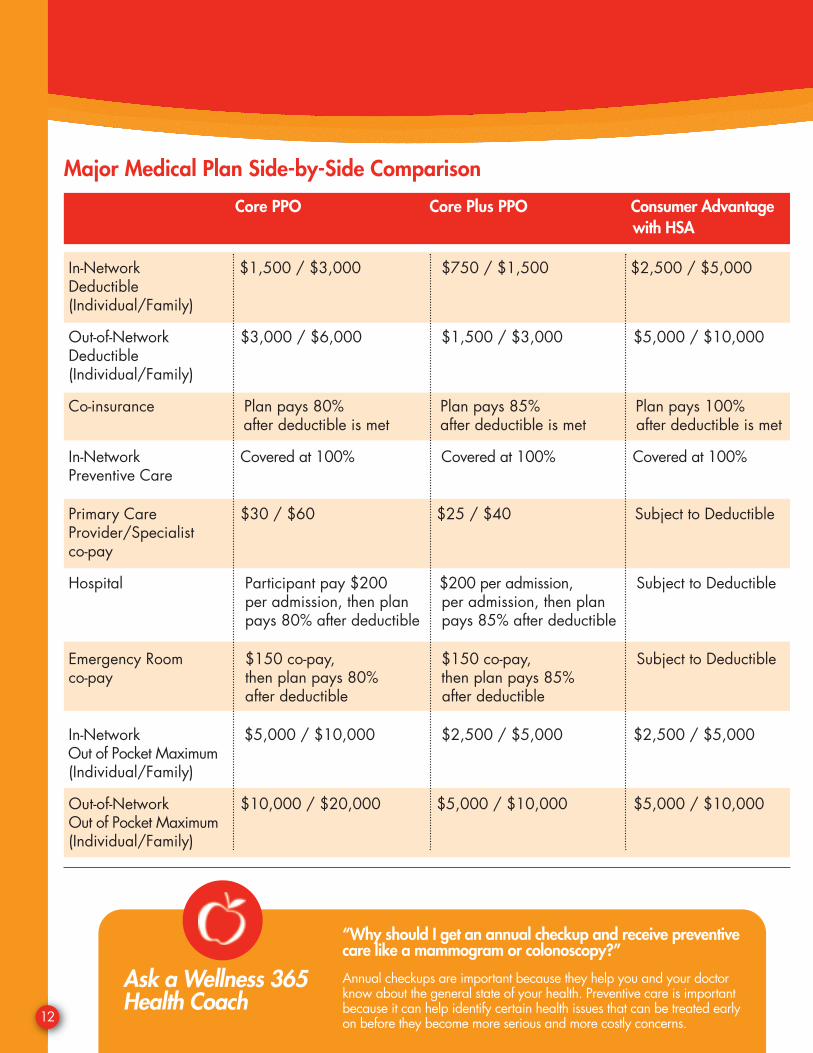

Major Medical Plan Side-by-Side Comparison

Core PPO Core Plus PPO Consumer Advantage with HSA

In-Network $1,500 / $3,000 $750 / $1,500 $2,500 / $5,000Deductible (Individual/Family)

Out-of-Network $3,000 / $6,000 $1,500 / $3,000 $5,000 / $10,000Deductible (Individual/Family)

Co-insurance Plan pays 80% Plan pays 85% Plan pays 100% after deductible is met after deductible is met after deductible is met

In-Network Covered at 100% Covered at 100% Covered at 100%Preventive Care

Primary Care $30 / $60 $25 / $40 Subject to Deductible Provider/Specialistco-pay

Hospital Participant pay $200 $200 per admission, Subject to Deductibleper admission, then plan per admission, then plan pays 80% after deductible pays 85% after deductible

Emergency Room $150 co-pay, $150 co-pay, Subject to Deductibleco-pay then plan pays 80% then plan pays 85%

after deductible after deductible

In-Network $5,000 / $10,000 $2,500 / $5,000 $2,500 / $5,000Out of Pocket Maximum(Individual/Family)

Out-of-Network $10,000 / $20,000 $5,000 / $10,000 $5,000 / $10,000Out of Pocket Maximum(Individual/Family)

“Why should I get an annual checkup and receive preventivecare like a mammogram or colonoscopy?”

Annual checkups are important because they help you and your doctorknow about the general state of your health. Preventive care is importantbecause it can help identify certain health issues that can be treated earlyon before they become more serious and more costly concerns.

Ask a Wellness 365Health Coach

The price you pay when purchasing retail prescriptiondrugs is limited to a tiered co-pay that you continue to paywhen purchasing prescriptions, even after your annualmedical deductible is met.• The cost used to calculate your co-pay reflects a discount.• Co-pays vary depending on which tier of drug you

purchase:> Generic: Team Member pays 20% of cost with

$4 min., $30 max.> Formulary (Preferred Brand*): Team Member pays

30% of cost with $20 min., $50 max.> Non-Formulary (Non-Preferred Brand* & Specialty):

Team Member pays 40% of cost with $40 min., $75 max.

The price you pay when purchasing mail order prescriptiondrugs is limited to a tiered co-pay that you continue to paywhen purchasing prescriptions, even after your annualmedical deductible is met.• The cost used to calculate your co-pay reflects a discount.• Co-pays vary depending on which tier of drug you

purchase:> Generic: Team Member pays 20% of cost with

$10 min., $75 max.> Formulary (Preferred Brand*): Team Member pays

30% of cost with $50 min., $125 max.> Non-Formulary (Non-Preferred Brand* & Specialty):

Team Member pays 40% of cost with $100 min., $187.50 max.

RETAIL MAIL ORDER (90-Day Supply)

Core PPO and Core Plus PPO plans Prescription Drug Features:

• The price you pay when purchasing prescription drugs reflects a discount.• The price you pay when purchasing prescription drugs counts toward meeting deductible. • Once you meet your annual deductible, you pay nothing for prescription drugs.

Consumer Advantage with HSA plan Prescription Drug Features:

Prescription Drug Plans

Whether you elect the Consumer Advantage with HSA, Core PPO or Core Plus PPOplan, each is accompanied by a Prescription Drug plan.

The Prescription Drug plan provides enrolled Family Dollar Team Members and their enrolled dependents competitive prices on generic, formulary (preferred) and non-formulary (non-preferred) brand drugs.

The Prescription Drug plan coverage varies depending on which major medical plan you choose:

When you elect a major medical plan, you will receive a BCBSNC Member ID card foryour health care and prescription drug needs. This card should be presented to thepharmacy when purchasing prescription drugs.

The plan may not cover every drug your doctor prescribes. To get information aboutwhich prescription drugs are covered under the plan, visit bcbsnc.com/members/familydollar and click Prescription Drugs.

*The terms “Preferred Brand” and “Non-Preferred Brand” do not relate to whether one medication is better than another. Your health careprovider is the only person who can decide what prescription drug is right for you.

ans

13

14

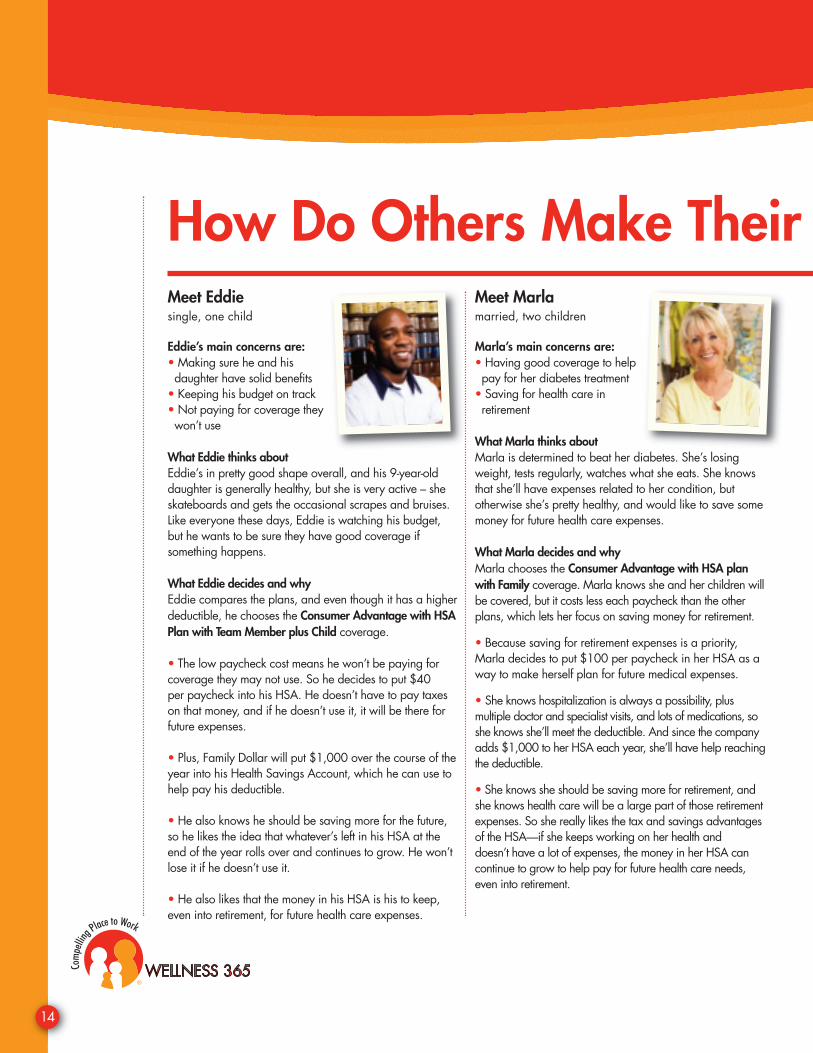

How Do Others Make Their Meet Eddiesingle, one child

Eddie’s main concerns are: • Making sure he and his daughter have solid benefits

• Keeping his budget on track• Not paying for coverage they won’t use

What Eddie thinks aboutEddie’s in pretty good shape overall, and his 9-year-olddaughter is generally healthy, but she is very active – sheskateboards and gets the occasional scrapes and bruises.Like everyone these days, Eddie is watching his budget,but he wants to be sure they have good coverage if something happens.

What Eddie decides and whyEddie compares the plans, and even though it has a higherdeductible, he chooses the Consumer Advantage with HSAPlan with Team Member plus Child coverage.

• The low paycheck cost means he won’t be paying forcoverage they may not use. So he decides to put $40 per paycheck into his HSA. He doesn’t have to pay taxes on that money, and if he doesn’t use it, it will be there for future expenses.

• Plus, Family Dollar will put $1,000 over the course of theyear into his Health Savings Account, which he can use tohelp pay his deductible.

• He also knows he should be saving more for the future,so he likes the idea that whatever’s left in his HSA at theend of the year rolls over and continues to grow. He won’tlose it if he doesn’t use it.

• He also likes that the money in his HSA is his to keep,even into retirement, for future health care expenses.

Meet Marlamarried, two children

Marla’s main concerns are: • Having good coverage to help pay for her diabetes treatment

• Saving for health care in retirement

What Marla thinks aboutMarla is determined to beat her diabetes. She’s losingweight, tests regularly, watches what she eats. She knowsthat she’ll have expenses related to her condition, but otherwise she’s pretty healthy, and would like to save somemoney for future health care expenses.

What Marla decides and why Marla chooses the Consumer Advantage with HSA planwith Family coverage. Marla knows she and her children willbe covered, but it costs less each paycheck than the otherplans, which lets her focus on saving money for retirement.

• Because saving for retirement expenses is a priority,Marla decides to put $100 per paycheck in her HSA as away to make herself plan for future medical expenses.

• She knows hospitalization is always a possibility, plus multiple doctor and specialist visits, and lots of medications, soshe knows she’ll meet the deductible. And since the companyadds $1,000 to her HSA each year, she’ll have help reachingthe deductible.

• She knows she should be saving more for retirement, andshe knows health care will be a large part of those retirementexpenses. So she really likes the tax and savings advantagesof the HSA—if she keeps working on her health and doesn’t have a lot of expenses, the money in her HSA cancontinue to grow to help pay for future health care needs,even into retirement.

15

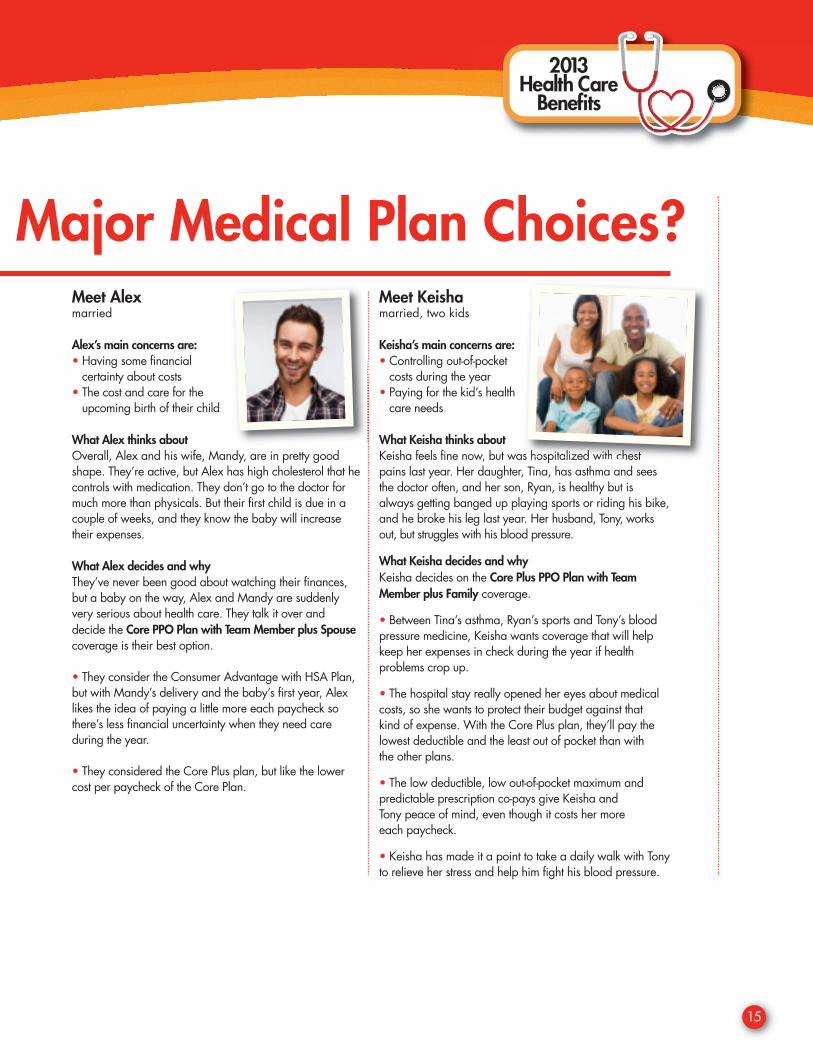

Major Medical Plan Choices?Meet Alexmarried

Alex’s main concerns are:• Having some financial

certainty about costs• The cost and care for the

upcoming birth of their child

What Alex thinks aboutOverall, Alex and his wife, Mandy, are in pretty goodshape. They’re active, but Alex has high cholesterol that he controls with medication. They don’t go to the doctor formuch more than physicals. But their first child is due in acouple of weeks, and they know the baby will increasetheir expenses.

What Alex decides and whyThey’ve never been good about watching their finances,but a baby on the way, Alex and Mandy are suddenlyvery serious about health care. They talk it over and decide the Core PPO Plan with Team Member plus Spousecoverage is their best option.

• They consider the Consumer Advantage with HSA Plan,but with Mandy’s delivery and the baby’s first year, Alexlikes the idea of paying a little more each paycheck sothere’s less financial uncertainty when they need care during the year.

• They considered the Core Plus plan, but like the lowercost per paycheck of the Core Plan.

Meet Keishamarried, two kids

Keisha’s main concerns are:• Controlling out-of-pocket

costs during the year• Paying for the kid’s health

care needs

What Keisha thinks aboutKeisha feels fine now, but was hospitalized with chestpains last year. Her daughter, Tina, has asthma and seesthe doctor often, and her son, Ryan, is healthy but is always getting banged up playing sports or riding his bike,and he broke his leg last year. Her husband, Tony, worksout, but struggles with his blood pressure.

What Keisha decides and why Keisha decides on the Core Plus PPO Plan with Team Member plus Family coverage.

• Between Tina’s asthma, Ryan’s sports and Tony’s bloodpressure medicine, Keisha wants coverage that will helpkeep her expenses in check during the year if health problems crop up.

• The hospital stay really opened her eyes about medicalcosts, so she wants to protect their budget against that kind of expense. With the Core Plus plan, they’ll pay thelowest deductible and the least out of pocket than with the other plans.

• The low deductible, low out-of-pocket maximum and predictable prescription co-pays give Keisha and Tony peace of mind, even though it costs her more each paycheck.

• Keisha has made it a point to take a daily walk with Tonyto relieve her stress and help him fight his blood pressure.

as hospitalized with chest

16

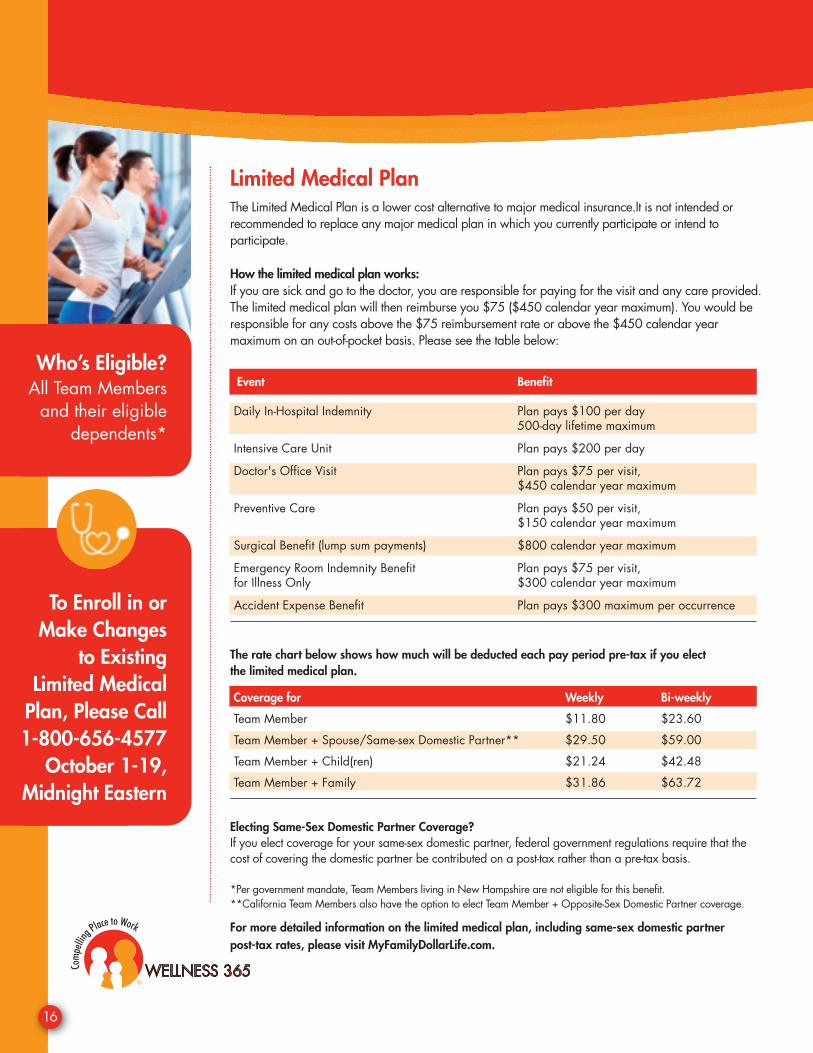

Limited Medical PlanThe Limited Medical Plan is a lower cost alternative to major medical insurance.It is not intended or recommended to replace any major medical plan in which you currently participate or intend to participate.

How the limited medical plan works:If you are sick and go to the doctor, you are responsible for paying for the visit and any care provided.The limited medical plan will then reimburse you $75 ($450 calendar year maximum). You would be responsible for any costs above the $75 reimbursement rate or above the $450 calendar year maximum on an out-of-pocket basis. Please see the table below:

Event Benefit

Daily In-Hospital Indemnity Plan pays $100 per day 500-day lifetime maximum

Intensive Care Unit Plan pays $200 per day

Doctor's Office Visit Plan pays $75 per visit, $450 calendar year maximum

Preventive Care Plan pays $50 per visit, $150 calendar year maximum

Surgical Benefit (lump sum payments) $800 calendar year maximum

Emergency Room Indemnity Benefit Plan pays $75 per visit, for Illness Only $300 calendar year maximum

Accident Expense Benefit Plan pays $300 maximum per occurrence

The rate chart below shows how much will be deducted each pay period pre-tax if you elect the limited medical plan.

Coverage for Weekly Bi-weekly

Team Member $11.80 $23.60

Team Member + Spouse/Same-sex Domestic Partner** $29.50 $59.00

Team Member + Child(ren) $21.24 $42.48

Team Member + Family $31.86 $63.72

Electing Same-Sex Domestic Partner Coverage?If you elect coverage for your same-sex domestic partner, federal government regulations require that thecost of covering the domestic partner be contributed on a post-tax rather than a pre-tax basis.

*Per government mandate, Team Members living in New Hampshire are not eligible for this benefit. **California Team Members also have the option to elect Team Member + Opposite-Sex Domestic Partner coverage.

For more detailed information on the limited medical plan, including same-sex domestic partner post-tax rates, please visit MyFamilyDollarLife.com.

Who’s Eligible?All Team Members

and their eligible dependents*

To Enroll in orMake Changes

to Existing Limited Medical

Plan, Please Call 1-800-656-4577

October 1-19,Midnight Eastern

Why Do Some Elect the Limited Medical Plan?

Meet Aliciasingle, no children

Alicia’s main concerns are:• Squeezing every dollar from her paycheck• Prescription coverage• Having some coverage for doctor visits

What Alicia thinks aboutAlicia is active and healthy, and knows she doesn’t use a lot of health care. But she’s also nota big fan of surprises, so she wants some protection against doctor bills and prescriptioncosts. She’s living by herself for the first time, soher budget is always on her mind.

What Alicia decides and whyAlicia chooses the limited medical plan because it costs less each paycheck than anyother option, but still provides some protection.

• She knows it doesn’t provide the same level of benefits as the other plans, but shedoesn’t expect to have any serious health issues next year.

• When she does see a doctor, her visits usually run about $100, so the $75 per visitbenefit seems about right; and she’s pretty sure she won’t hit the annual $450 maximum benefit.

• Alicia also likes limited medical option’s prescription drug flat copay, because prescriptions are usually her greatest expense.

• She sprained her ankle last year playing basketball, so the plan’s $75 emergencyroom benefit might come in handy, too.

• Alicia weighs the cost savings against the financial risk she faces if she gets seriouslyill or injured, and decides it’s worth it to her for next year, at least.

17

“What are the benefits of someone having a primary carephysician, as opposed to choosing to go to urgent care or theemergency room when illness or injury occurs?”

A primary care physician (PCP) retains your historical medical records, including medications, allergies, previous illness, injuries and treatment. Your PCP can monitor you throughout your illness or injury recovery and follow up to adjust your treatment or medications as needed.

The emergency room and urgent care are intended to diagnose and treatonly your immediate symptoms and refer you to your primary care physician for follow up care.

Ask a Wellness 365Health Coach

18

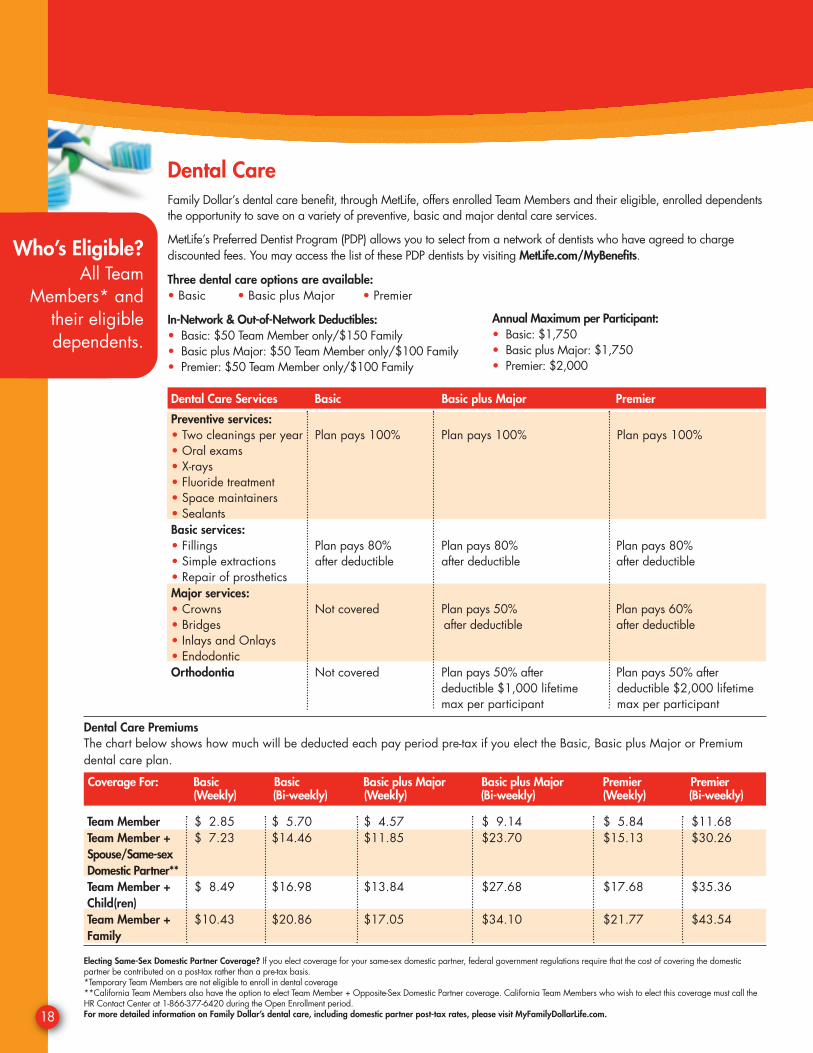

Dental CareFamily Dollar’s dental care benefit, through MetLife, offers enrolled Team Members and their eligible, enrolled dependentsthe opportunity to save on a variety of preventive, basic and major dental care services.

MetLife’s Preferred Dentist Program (PDP) allows you to select from a network of dentists who have agreed to charge discounted fees. You may access the list of these PDP dentists by visiting MetLife.com/MyBenefits.

Three dental care options are available:• Basic • Basic plus Major • Premier

In-Network & Out-of-Network Deductibles:• Basic: $50 Team Member only/$150 Family• Basic plus Major: $50 Team Member only/$100 Family• Premier: $50 Team Member only/$100 Family

Dental Care Services Basic Basic plus Major Premier

Preventive services:• Two cleanings per year Plan pays 100% Plan pays 100% Plan pays 100%• Oral exams• X-rays• Fluoride treatment• Space maintainers• SealantsBasic services:• Fillings Plan pays 80% Plan pays 80% Plan pays 80%• Simple extractions after deductible after deductible after deductible• Repair of prostheticsMajor services:• Crowns Not covered Plan pays 50% Plan pays 60%• Bridges after deductible after deductible• Inlays and Onlays• EndodonticOrthodontia Not covered Plan pays 50% after Plan pays 50% after

deductible $1,000 lifetime deductible $2,000 lifetime max per participant max per participant

Who’s Eligible?All Team

Members* and their eligible dependents.

Annual Maximum per Participant:• Basic: $1,750• Basic plus Major: $1,750• Premier: $2,000

Dental Care PremiumsThe chart below shows how much will be deducted each pay period pre-tax if you elect the Basic, Basic plus Major or Premium dental care plan.

Team Member $ 2.85 $ 5.70 $ 4.57 $ 9.14 $ 5.84 $11.68Team Member + $ 7.23 $14.46 $11.85 $23.70 $15.13 $30.26Spouse/Same-sexDomestic Partner**Team Member + $ 8.49 $16.98 $13.84 $27.68 $17.68 $35.36Child(ren)Team Member + $10.43 $20.86 $17.05 $34.10 $21.77 $43.54Family

Electing Same-Sex Domestic Partner Coverage? If you elect coverage for your same-sex domestic partner, federal government regulations require that the cost of covering the domesticpartner be contributed on a post-tax rather than a pre-tax basis.*Temporary Team Members are not eligible to enroll in dental coverage**California Team Members also have the option to elect Team Member + Opposite-Sex Domestic Partner coverage. California Team Members who wish to elect this coverage must call theHR Contact Center at 1-866-377-6420 during the Open Enrollment period.For more detailed information on Family Dollar’s dental care, including domestic partner post-tax rates, please visit MyFamilyDollarLife.com.

Coverage For: Basic Basic Basic plus Major Basic plus Major Premier Premier(Weekly) (Bi-weekly) (Weekly) (Bi-weekly) (Weekly) (Bi-weekly)

19

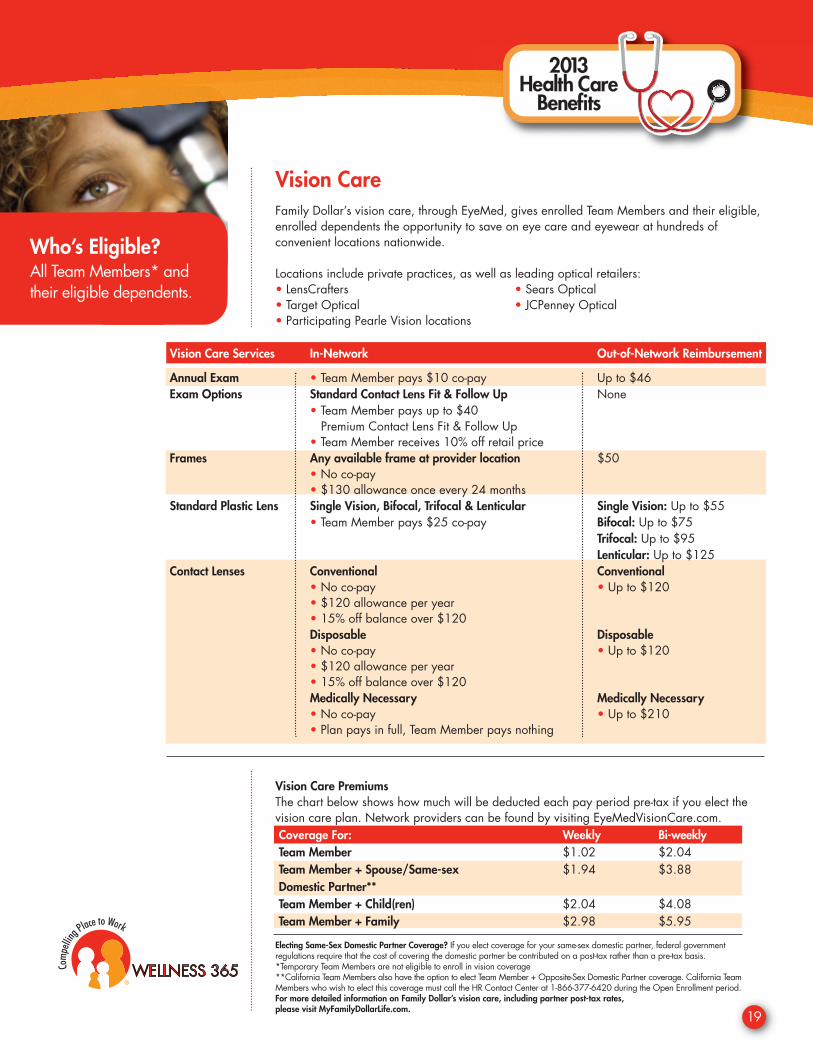

Vision CareFamily Dollar’s vision care, through EyeMed, gives enrolled Team Members and their eligible, enrolled dependents the opportunity to save on eye care and eyewear at hundreds of convenient locations nationwide.

Locations include private practices, as well as leading optical retailers: • LensCrafters • Sears Optical• Target Optical • JCPenney Optical • Participating Pearle Vision locations

Vision Care PremiumsThe chart below shows how much will be deducted each pay period pre-tax if you elect the vision care plan. Network providers can be found by visiting EyeMedVisionCare.com.Coverage For: Weekly Bi-weeklyTeam Member $1.02 $2.04Team Member + Spouse/Same-sex $1.94 $3.88Domestic Partner**Team Member + Child(ren) $2.04 $4.08Team Member + Family $2.98 $5.95

Electing Same-Sex Domestic Partner Coverage? If you elect coverage for your same-sex domestic partner, federal government regulations require that the cost of covering the domestic partner be contributed on a post-tax rather than a pre-tax basis.*Temporary Team Members are not eligible to enroll in vision coverage**California Team Members also have the option to elect Team Member + Opposite-Sex Domestic Partner coverage. California Team Members who wish to elect this coverage must call the HR Contact Center at 1-866-377-6420 during the Open Enrollment period.For more detailed information on Family Dollar’s vision care, including partner post-tax rates, please visit MyFamilyDollarLife.com.

Vision Care Services In-Network Out-of-Network Reimbursement

Annual Exam • Team Member pays $10 co-pay Up to $46Exam Options Standard Contact Lens Fit & Follow Up None

• Team Member pays up to $40Premium Contact Lens Fit & Follow Up

• Team Member receives 10% off retail priceFrames Any available frame at provider location $50

• No co-pay• $130 allowance once every 24 months

Standard Plastic Lens Single Vision, Bifocal, Trifocal & Lenticular Single Vision: Up to $55• Team Member pays $25 co-pay Bifocal: Up to $75

Trifocal: Up to $95Lenticular: Up to $125

Contact Lenses Conventional Conventional• No co-pay • Up to $120• $120 allowance per year• 15% off balance over $120Disposable Disposable• No co-pay • Up to $120• $120 allowance per year• 15% off balance over $120Medically Necessary Medically Necessary• No co-pay • Up to $210• Plan pays in full, Team Member pays nothing

Who’s Eligible?All Team Members* and their eligible dependents.

20

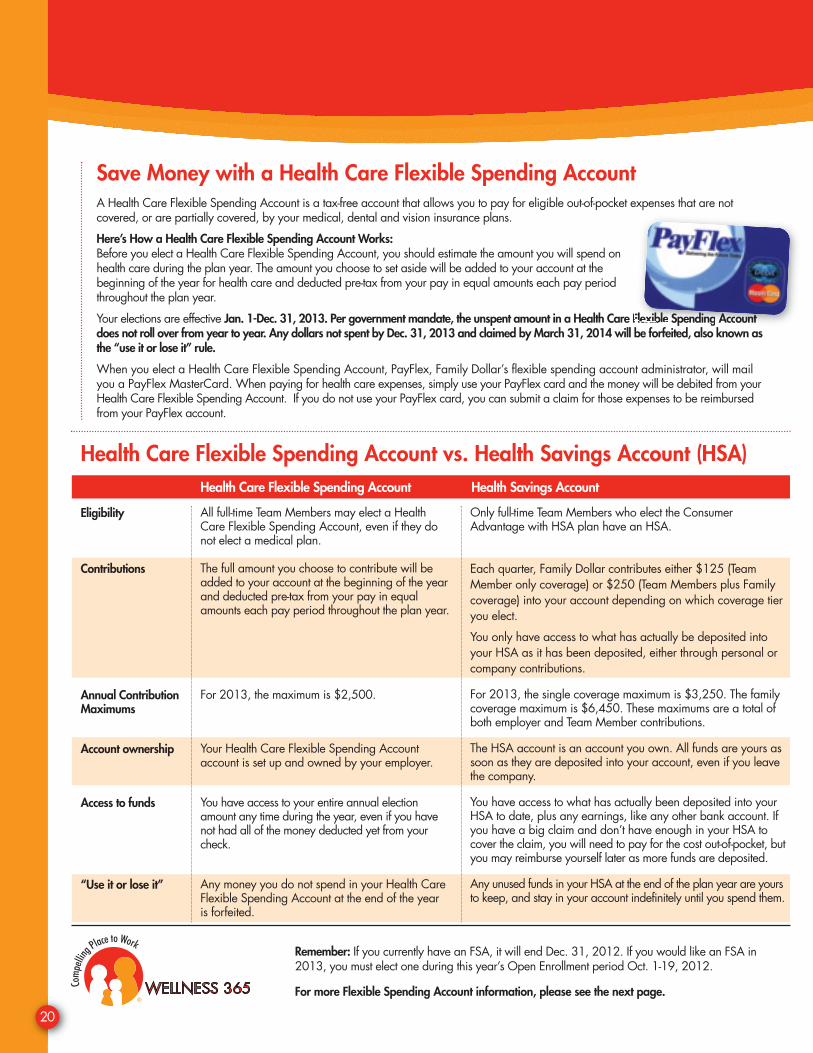

Save Money with a Health Care Flexible Spending AccountA Health Care Flexible Spending Account is a tax-free account that allows you to pay for eligible out-of-pocket expenses that are not covered, or are partially covered, by your medical, dental and vision insurance plans.

Here’s How a Health Care Flexible Spending Account Works:Before you elect a Health Care Flexible Spending Account, you should estimate the amount you will spend on health care during the plan year. The amount you choose to set aside will be added to your account at the beginning of the year for health care and deducted pre-tax from your pay in equal amounts each pay period throughout the plan year.

Your elections are effective Jan. 1-Dec. 31, 2013. Per government mandate, the unspent amount in a Health Care Flexible Spending Accountdoes not roll over from year to year. Any dollars not spent by Dec. 31, 2013 and claimed by March 31, 2014 will be forfeited, also known asthe “use it or lose it” rule.

When you elect a Health Care Flexible Spending Account, PayFlex, Family Dollar’s flexible spending account administrator, will mailyou a PayFlex MasterCard. When paying for health care expenses, simply use your PayFlex card and the money will be debited from yourHealth Care Flexible Spending Account. If you do not use your PayFlex card, you can submit a claim for those expenses to be reimbursedfrom your PayFlex account.

Remember: If you currently have an FSA, it will end Dec. 31, 2012. If you would like an FSA in2013, you must elect one during this year’s Open Enrollment period Oct. 1-19, 2012.

For more Flexible Spending Account information, please see the next page.

Eligibility

Contributions

Annual Contribution Maximums

Account ownership

Access to funds

“Use it or lose it”

All full-time Team Members may elect a HealthCare Flexible Spending Account, even if they donot elect a medical plan.

The full amount you choose to contribute will beadded to your account at the beginning of the yearand deducted pre-tax from your pay in equalamounts each pay period throughout the plan year.

For 2013, the maximum is $2,500.

Your Health Care Flexible Spending Account account is set up and owned by your employer.

You have access to your entire annual electionamount any time during the year, even if you havenot had all of the money deducted yet from yourcheck.

Any money you do not spend in your Health CareFlexible Spending Account at the end of the year is forfeited.

Only full-time Team Members who elect the Consumer Advantage with HSA plan have an HSA.

Each quarter, Family Dollar contributes either $125 (TeamMember only coverage) or $250 (Team Members plus Familycoverage) into your account depending on which coverage tieryou elect.

You only have access to what has actually be deposited intoyour HSA as it has been deposited, either through personal orcompany contributions.

For 2013, the single coverage maximum is $3,250. The familycoverage maximum is $6,450. These maximums are a total ofboth employer and Team Member contributions.

The HSA account is an account you own. All funds are yours assoon as they are deposited into your account, even if you leavethe company.

You have access to what has actually been deposited into yourHSA to date, plus any earnings, like any other bank account. Ifyou have a big claim and don’t have enough in your HSA tocover the claim, you will need to pay for the cost out-of-pocket, butyou may reimburse yourself later as more funds are deposited.

Any unused funds in your HSA at the end of the plan year are yoursto keep, and stay in your account indefinitely until you spend them.

Health Care Flexible Spending Account Health Savings Account

Health Care Flexible Spending Account vs. Health Savings Account (HSA)

Flexible Spendinge Account

Do You CurrentlyHave a Flexible

Spending Account FSA?

If you currently have anFSA, you have throughDec. 31, 2012 to incur

eligible expenses andthrough March 31, 2013

to submit claims foreligible expenses incurred in 2012.

Per federal regulations,FSA funds do not roll overyear to year. Any dollars

not claimed by March 31,2013 for expenses

incurred in 2012 are automatically forfeited.

21

Health Care Flexible Spending Account A Health Care Flexible Spending Account allows you to set aside pre-tax money to pay for qualified medical, dental, vision, hearing and pharmaceutical expenses such as co-pays, co-insurance, certainover-the-counter medications, eyeglasses, contacts, eye care solutions, and laser vision correction foryourself or your dependents.

Annual Contribution:Minimum: $65 Maximum: $2,500

Who’s Eligible?All full-time Team Members may elect a Health Care Flexible Spending Account, unless they elect the Consumer Advantage with HSA major medical plan.

Limited Purpose Flexible Spending Account If you elect the Consumer Advantage with HSA plan, you are not eligible to elect a Health Care Flexible Spending Account, per government regulations. However, you may elect a Limited PurposeFlexible Spending Account (LPFSA). You can contribute pre-tax dollars into an LPFSA via pay deduction.This enables you to preserve your HSA funds for other purposes, including saving for the future.

Annual Contribution: Minimum: $65 Maximum: $2,500

Who’s Eligible?All full-time Team Members who elect the Consumer Advantage with HSA plan may elect a Limited Purpose Flexible Spending Account.

Please note: If you elect the Consumer Advantage with HSA plan and currently have an FSA throughPayFlex, you will not receive a new card. If you elect the Consumer Advantage with HSA and elect an LPFSA, your card will carry your LPFSA balance and your HSA balance. When you use your card,your funds will be debited from the appropriate account. Since LPFSA funds can only be used for dental and vision care only, those expense will be deducted from your LPFSA by default.

Dependent Care Flexible Spending AccountA Dependent Care Flexible Spending Account allows you to set aside pre-tax money for non-reimburseddependent day care expenses, including day care, before-and-after school programs, nursery school or preschool, summer day camp and adult day care. Funds are available as they are deposited intoyour account each pay period.

Annual Contribution: Minimum: $65 Maximum: $2,500 ($5,000 if married and both spouses work)

Who’s Eligible?All full-time Team Members may elect a Dependent Care Flexible Spending Account if they have a dependentyounger than 13 years old or another dependent who is physically or mentally incapable of self-care.

Please note: a Dependent Care Flexible Spending Account is not for dependent health care expenses.

Also Available

22

Who’s Eligible?All Team Members*

and their eligible dependents

Supplemental InsuranceFamily Dollar offers all Team Members the option to elect supplemental insurance of various kinds to help them financially manage unexpected events when they arise. Team Members who elect supplemental insurance benefits have premiums conveniently deducted from their pay. Supplementalinsurance plans can be elected or canceled at any time, not just during Open Enrollment. Pages 22-24 include the supplemental insurance plans Team Members may elect.

Voluntary Life InsuranceFamily Dollar provides Team Members the opportunity to elect voluntary life insurance, administeredby The Hartford.

Life insurance provides Team Members with a way to provide for their families in the event of theirdeath. By purchasing life insurance, a Team Member could provide enough funds to pay for the funeral and other expenses, depending upon the amount of life insurance purchased.

Who can be covered?Voluntary life insurance is available for:• Team Member• Team Member’s Spouse• Team Member’s Child(ren)

When you elect voluntary life Insurance, you will be prompted to name a beneficiary. It is very important you name a beneficiary because he/she would be paid the financial benefit of the life insurance policy in the event of your death.

Please note: The Hartford requires a personal health application (PHA) for enrollment 31 days afterthe date you are first eligible. If enrolling for voluntary life insurance after you are first eligible, the effective date of your coverage will be based upon The Hartford’s approval of your PHA. If yourPHA is not completed and approved within 90 days of your election, coverage will be dropped.Benefit coverage may be subject to carrier approval, plan exclusions, and pre-existing conditions.

Team Member Coverage Amounts Range: $50,000 - $300,000 Child Coverage Amount: $10,000

*Temporary Team Members are not eligible to enroll in voluntary life insurance.

For more detailed information on voluntary life insurance, including rates, please visit MyFamilyDollarLife.com.

Who’s Eligible?All full-timeTeam Members*

23

Short-term and Long-term Disability Insurance

Family Dollar provides eligible Team Members the opportunity to elect an income protection packagethat includes short-term disability and long-term disability insurance through The Hartford.

Short-term and long-term disability insurance pays you a portion of your earnings if you cannot workdue to a non-work related disabling illness or injury. Short-term and long-term disability are offeredas a package; the benefits cannot be elected separately.

Short-term disability:• Benefits begin after 7 days of disability• Benefits could continue for up to six months, based on your position and condition• Benefits vary based on individual earnings• Benefits may be reduced by other income that you receive

Long-term disability:• Benefits can continue for up to five years as long as you remain disabled or until you reach

your Social Security Normal Retirement Age (as stated in the 1983 revision of the US Social Security Act), whichever is sooner.

• Benefits may be reduced if your disability occurs at 65 or above• Benefits are based on 60 percent of your pre-disability earnings, up to a maximum of $15,000

per month.• As long as you remain disabled, benefits can continue until the later of five years after your long-term

disability benefits began or you reach your Social Security Normal Retirement Age (as stated in the 1983 revision of the US Social Security Act).

Please note: The Hartford requires a personal health application(PHA) for enrollment 31 days after the date you are first eligible. If enrolling in the Disability Insurance Package, afteryou are first eligible, the effective date of your coverage willbe based upon the Hartford's approval of your PHA. If PHAis not completed and approved within 90 days of yourelection, coverage will be dropped. Benefit coveragemay be subject to carrier approval, plan exclusions, andpre-existing conditions.

*Temporary Team Members are not eligible to en-roll in short-term and long-term disability insur-ance.

For more detailed information on short-termand long-term disability insurance, includingrates, please visit MyFamilyDollarLife.com.

24

Who’s Eligible?All Team Members*

and their eligible dependents

Critical Illness Insurance

Family Dollar’s critical illness insurance provides Team Members and their eligible dependents theopportunity to receive financial protection when faced with certain unexpected health events.

Critical illness insurance is through Unum and pays a lump sum benefit at the diagnosis of a covered critical illness. You can use the money any way you see fit.

Covered critical illnesses include, but are not limited to:• Heart attack • Invasive cancer • Stroke • Paralysis • Coma

Critical Illness Coverage Amounts

Team Member $10,000 $20,000 $30,000

Spouse/Same-sex $10,000 $20,000Domestic Partner

Child** $2,500 $5,000 $7,500

*Temporary Team Members are not eligible to enroll in critical illness insurance.**If a Team Member enrolls in critical illness insurance, his or her child(ren) are automatically enrolledfor the corresponding coverage amount.

Please note: Rates are based on age and tobacco usage. For critical illness insurance, a tobaccouser is defined as someone who has used tobacco once within the last 12 months.

For more detailed information on critical illness insurance, including rates, please visit MyFamilyDollarLife.com.

Who’s Eligible?All full-time Team

Members* are automatically enrolled

Basic Life and Accidental Death & Dismemberment InsuranceAll full-time Team Members are automatically enrolled in a basic life insurance plan at no cost to theTeam Member. The basic life insurance pays a benefit to a Team Member’s designated beneficiaryin the event of his or her death.

The basic life insurance plan includes accidental death and dismemberment coverage. Under the accidental death portion of this coverage, an additional death benefit above the basic life insurancebenefit may be paid by The Hartford in the event of your accidental death. Under the dismembermentportion of this coverage, a dismemberment benefit may be paid by The Hartford based on loss of ahand, foot, leg, arm, or eye.

Elect or Update Your BeneficiariesElecting beneficiaries (and keeping your choice up to date) allows you to make sure your assets get distributed to your loved ones in a way you desire. If you do not name a beneficiary, or if all the beneficiaries you named have died by the time of your death, life insurance benefits will be paid toyour estate.*Temporary Team Members are not eligible for basic life and accidental death and dismemberment insurance.For more detailed information on basic life and accidental death & dismemberment insurance, including the amount of coverage your beneficiar(ies) are eligible for, please visit MyFamilyDollarLife.com.

Who’s Eligible?

In general, Team Members are eligible toparticipate on their 91stday with Family Dollar.

25

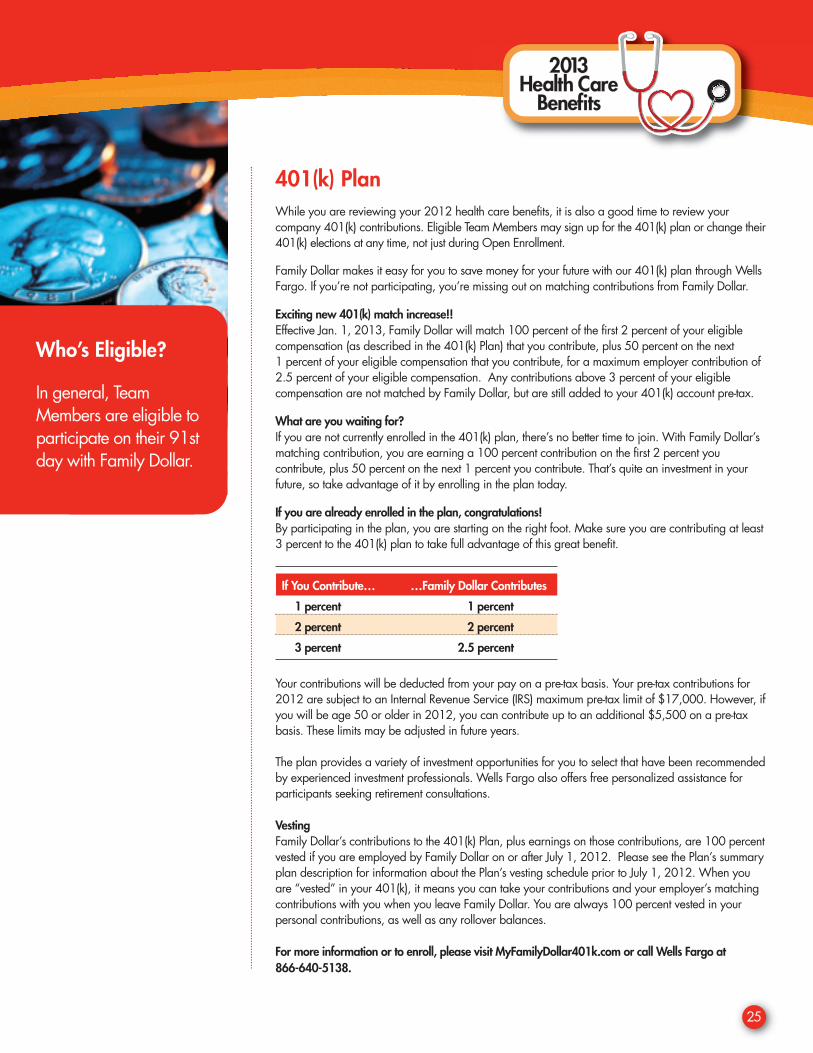

401(k) PlanWhile you are reviewing your 2012 health care benefits, it is also a good time to review your company 401(k) contributions. Eligible Team Members may sign up for the 401(k) plan or change their401(k) elections at any time, not just during Open Enrollment.

Family Dollar makes it easy for you to save money for your future with our 401(k) plan through WellsFargo. If you’re not participating, you’re missing out on matching contributions from Family Dollar.

Exciting new 401(k) match increase!!Effective Jan. 1, 2013, Family Dollar will match 100 percent of the first 2 percent of your eligible compensation (as described in the 401(k) Plan) that you contribute, plus 50 percent on the next 1 percent of your eligible compensation that you contribute, for a maximum employer contribution of2.5 percent of your eligible compensation. Any contributions above 3 percent of your eligible compensation are not matched by Family Dollar, but are still added to your 401(k) account pre-tax.

What are you waiting for?If you are not currently enrolled in the 401(k) plan, there’s no better time to join. With Family Dollar’smatching contribution, you are earning a 100 percent contribution on the first 2 percent you contribute, plus 50 percent on the next 1 percent you contribute. That’s quite an investment in your future, so take advantage of it by enrolling in the plan today.

If you are already enrolled in the plan, congratulations! By participating in the plan, you are starting on the right foot. Make sure you are contributing at least3 percent to the 401(k) plan to take full advantage of this great benefit.

If You Contribute… …Family Dollar Contributes

1 percent 1 percent

2 percent 2 percent

3 percent 2.5 percent

Your contributions will be deducted from your pay on a pre-tax basis. Your pre-tax contributions for2012 are subject to an Internal Revenue Service (IRS) maximum pre-tax limit of $17,000. However, ifyou will be age 50 or older in 2012, you can contribute up to an additional $5,500 on a pre-taxbasis. These limits may be adjusted in future years.

The plan provides a variety of investment opportunities for you to select that have been recommendedby experienced investment professionals. Wells Fargo also offers free personalized assistance for participants seeking retirement consultations.

VestingFamily Dollar’s contributions to the 401(k) Plan, plus earnings on those contributions, are 100 percentvested if you are employed by Family Dollar on or after July 1, 2012. Please see the Plan’s summaryplan description for information about the Plan’s vesting schedule prior to July 1, 2012. When youare “vested” in your 401(k), it means you can take your contributions and your employer’s matchingcontributions with you when you leave Family Dollar. You are always 100 percent vested in your personal contributions, as well as any rollover balances.

For more information or to enroll, please visit MyFamilyDollar401k.com or call Wells Fargo at 866-640-5138.

26

How to Participate in Open Enrollment

Participating in Open Enrollment is easy. You have two convenient methods– online and phone – to elect, change or cancel health care coverage for2013. Here’s how:

Online (24 hours a day, seven days a week) • Visit MyFamilyDollarLife.com

Phone (Monday - Friday, 8 a.m. - 8 p.m. Eastern)• Call 1-866-377-6420, and follow the prompts• A Benefits Specialist will help you make your elections

Here’s what you will need to enroll a dependent:• Dependent’s name• Dependent’s date of birth• Dependent’s relationship to Team Member

Enrolling a Dependent?

If you are enrolling a dependent(s) who you have not enrolled before, you will need to provide Family Dollar with documents (such as a birth certificate) to verify the dependent’s name,date of birth, and relationship to you by Nov. 19, 2012. Beginning Oct. 1,2012, a list of acceptable documents and how to submit them can be foundat MyFamilyDollarLife.com. Please note: If you do not submit dependent verification documentation by the deadline, the dependents will be droppedfrom health care coverage.

Do you have an Open Enrollment Question?

Call the HR Contact Center at 1-866-377-6420, Monday - Friday 8 a.m. - 8 p.m. Eastern time. The HR Contact Center is a team of knowledgeable human resources professionals dedicated to providingTeam Members quick, accurate and courteous service.

•Remember!

Open Enrollment

is October 1- 19,

2012,

midnight Eastern

California TeamMembers who wishto elect dental or vision care withTeam Member+Opposite-Sex Domestic Partnercoverage must call the HR Contact Center at1-866-377-6420during the OpenEnrollment period.

27

Glossary of Open Enrollment Terms

Beneficiary – A person who a Team Member designates to receive benefits, such as life insurance, in the eventof his or her death.

Consumer-Driven Health Plan (CDHP) – A CDHP is a type of high-deductible major medical plan that is linked toa Health Savings Account (HSA) that is partially funded each year by Family Dollar.

Co-pay – The fixed-dollar amount that is due and payable by the member at the time a covered service is provided.

Co-insurance – The sharing of charges by the Plan and the participant for covered services received by a member. Applicable after the plan’s deductible is met.

Deductible – The specified dollar amount for certain covered services that the member must pay before the planpays any coinsurance. The following items do not count toward satisfying the requirement that the Participant mustpay the deductible amount before the plan begins to pay any co-insurance: copayments, coinsurance, charges in excess of the allowed amount, amounts exceeding any maximum, and expenses for non-covered services.

Dependent Care Flexible Spending Account – A Dependent Care Flexible Spending Account allows you to setaside pre-tax money for non-reimbursed dependent day care expenses, including day care, before-and-afterschool programs, nursery school or preschool, summer day camp and adult day care. Funds are available asthey are deposited into your account each pay period. Please note: a Dependent Care Flexible Spending Account is not for dependent health care expenses.

Health Care Flexible Spending Account – A Health Care Flexible Spending Account allows you to set aside pre-tax money to pay for qualified medical, dental, vision, hearing and pharmaceutical expenses such as co-pays, co-insurance, certain over-the-counter medications, eyeglasses, contacts, eye care solutions, and laservision correction for yourself or your dependents.

Formulary (preferred)* – Brand-name drugs designated as “preferred”* by BlueCross BlueShield of North Carolina.*The terms “Preferred Brand” and “Non-Preferred Brand” do not relate to whether one medication is better than another. Your health careprovider is the only person who can decide what prescription drug is right for you.

Generic – A generic drug is identical, or bioequivalent, to a brand name drug in dosage form, safety, route of administration, quality, and intended use. Although generic drugs are chemically identical to their branded counterparts, they are typically sold at substantial discounts from the branded price.

Health Savings Account (HSA) – A Health Savings Account or HSA is a portable, tax-exempt account you canuse to save and pay for qualified medical expenses, including medical, prescription drug, vision and dentalcare now or in the future.

In-network Provider – A hospital, doctor or other medical practitioner or provider of medical services that hasagreed to accept discounted rates for services when working with BlueCross BlueShield of North Carolina (BCBSNC) Plan participants, thus becoming a member of the BlueCard network. Plan participants receivegreater discounts when using a BCBSNC in-network provider. A list of in-network providers can be found by visiting bcbsnc.com/members/familydollar and clicking Provider Search.

continued on page 28

28

Glossary of Open Enrollment Terms continued

Limited Purpose Flexible Spending Account – If you elect the Consumer Advantage with HSA plan you are noteligible to elect a Health Care Flexible Spending Account, per government regulations. However, you mayelect a Limited Purpose Flexible Spending Account (LPFSA) for eligible dental and vision expenses that you canuse in conjunction with your HSA. You can contribute pre-tax dollars into an LPFSA via pay deduction. This enables you to preserve your HSA funds for other purposes, including saving for the future.

Non-formulary (non-preferred)* – Brand-name drugs that have been designated as “non-preferred”* by BlueCrossBlueShield of North Carolina. *The terms “Preferred Brand” and “Non-Preferred Brand” do not relate to whether one medication is better than another. Your health careprovider is the only person who can decide what prescription drug is right for you.

Out-of-Network Provider – A hospital, doctor or other medical practitioner that has not agreed to accept discounted rates for services to BCBCNC participants, thus the provider is outside the BlueCard network. By using out-of-network doctors, Plan participants do not receive the greatest discounts.

Out-of-Pocket Maximum – The maximum the Plan participant will pay out-of-pocket in a given Plan year for covered services.

Personal Health Application (PHA) – A PHA is a document required by some life insurance plans before coverage is granted. The insuring company uses the information provided on the PHA to make coverage under-writing decisions.

Plan year – Each plan year begins January 1 and ends on the following December 31.

Post-tax – After taxes have been deducted from your gross income in your paycheck.

Pre-tax – Before taxes have been deducted from your gross income in your paycheck.

Preferred Provider Organization (PPO) – A PPO is a network of doctors, hospitals and other health careproviders that have agreed to offer medical care and services at discounted rates

Preventive Care – Age appropriate medical services provided in order to prevent a condition or disease (example, immunizations and physicals).

Qualified Life Status Change – A life event such as a birth, marriage, death or divorce that allows you to changeyour health care elections mid-plan year without waiting for the following Open Enrollment period.

Surcharge – An additional charge added to your medical premium (example, tobacco-user surcharge).

Tobacco User – If a full-time Team Member is electing major medical coverage with BlueCross BlueShield ofNorth Carolina, he or she is considered a tobacco user if he or she has used tobacco, even once, within thelast six months.

Vesting – When you can take your account balance from the Family Dollar 401(k) plan (including your employer's matching contributions) with you when you leave Family Dollar. In the Family Dollar 401(k) plan, you are 100 percent vested in your personal contributions, employer match, as well as any rollover balances.

29

Other Important Information

Situation

When you are newly hired or when you change your part-time/full-time status:

When you are adding coverageand/or adding a dependent due to a Qualifying Life Event:

When you are dropping coverageand/or dropping a dependent due to a Qualifying Life Event:

When enrolling in a health care flexible spending account (FSA) orlimited purpose FSA due to a newhire, or Qualifying Life Event:

When you are rehired as a Team Member:

Process

• Enroll in benefits within 31 days from event date.• Submit dependent verification documents within 31 days from event date.• If dependent verification documents are not submitted within 31 days:

o Coverage is dropped retroactively to the event dateo Premiums are not refundedo Team Member is responsible for any claims incurred

• Team Members can make election changes that are consistent with the Qualifying Life Eventwithin 31 days of event date. This includes adding eligible dependents to coverage.

• Submit dependent verification documents within 31 days from event date.• New coverage and premiums are effective on the event date.• Election changes made and/or adding any dependent after the 31-day deadline

will not take effect.• If dependent verification documents are not submitted within 31 days:

o Coverage is dropped retroactively to the event dateo Premiums are not refundedo Team Member is responsible for any claims incurred

• Drop benefits and/or a dependent(s) within 31 days from event date.• Submit documentation within 31 days to verify coverage drop eligibility.• If documentation is not submitted within 31 days:

o Coverage is dropped retroactively to event dateo Premiums are not refundedo Team Member is responsible for any claims incurredo Team Member is responsible for making premium payments for remainder of year

• Team Member’s maximum election for a health care FSA or limited purpose FSA is the sameas the maximum for a Team Member who enrolls during Open Enrollment, which is $2,500for 2013. The amount a Team Member can choose is not reduced or prorated because the election was made during the year. Team Member is responsible for the entire elected contribution. For example, if a Team Member makes an election in June to have the $2,500 annual maximum coverage under an FSA, payroll deductions will be based on dividing the$2,500 amount by the remaining pay periods of the current year.

• Team Member can elect a health care FSA or limited purpose FSA or increase the contribution amount to an FSA due to a Qualifying Life Event if the new election is consistent with the Qualifying Life Event.

• Team Members rehired within 30 days of separation will resume previously elected benefits.• Team Members rehired after 30 days from separation are treated as newly hired Team

Members and must elect benefits as with any other newly hired Team Member. Required coverage waiting periods will apply.